4.1. Key Drivers of Project’S Profitability

To identify the key drivers of the project’s financial return, we evaluated the role of various model parameters in the financial profitability of the project. To this end, we performed numerical sensitivity analyses to evaluate the impact of a change in each of the model parameters on the overall NPV and IRR of the project. To conduct the numerical sensitivity analyses, we measured the change in the NPV and IRR of the project as a result of incrementally increasing the value of each model parameter, while keeping all other model parameters constant. The results of this analysis along with the the magnitude of the increments in the model parameters are summarized in

Table 3,

Table 4 and

Table 5. A positive change in the NPV and IRR indicates an increase in the profitability of the project as a result of the imposed change in the value of the parameters, while a negative value for change in NPV and IRR suggests a decrease in the profitability of the project. Note that as different parameters have different unit values, the relative magnitudes of change are not exactly comparable; i.e., a one dollar change may be quite different than a percent change in an interest rate. Therefore, these results should be interpreted carefully, including reference to the measurement units. To aid interpretability, we also provided elasticities (percent change in the IRR for a percentage change in the input parameter) in

Table 3,

Table 4 and

Table 5. To support the results of sensitivity analyses, an analytical analysis of the partial derivatives of the NPV function with respect to several model parameters is provided in

Appendix A.

The results of the sensitivity analysis show that the parameters related to project financing, including the loan repayment period,

Y, equity funds,

, and the loan interest rate,

i, play a key role in profitability calculations. According to

Table 3, a unit increase in equity funds,

, and loan repayment period,

Y, would increase the NPV of the project by CAD 2,555,422 and CAD 2,038,852, respectively. On the other hand, a quarter percent increase in the value of loan interest rate,

i, causes a decrease of CAD 697,679 in the NPV of the project.

The loan interest rate, i, and the loan repayment period, Y, are the main drivers of the loan payments occurring over the entire project timeframe and serve as a major cost to the developer. A percent increase in the loan interest rate will significantly increase the finance costs, leading to a reduction in the NPV of the project. Moreover, the loan repayment period, Y, determines the timeframe that developers are required to pay back the borrowed loan. An increase in the loan repayment period will reduce the amount of each loan installment. As assumed here, developers must return the entire loan amount, even if the loan repayment period is longer than the project construction. Keeping the interest rate constant, an increase in the loan repayment period would decrease the amount of loan payments. In this case, this means that developers would repay a significant amount of the principal loan amount in a longer run and delay the loan payoff, thus increasing the NPV of the project.

The amount of equity funds can also impact the amount of loan payments. An increase in equity funds, , will decrease the amount of loan required to cover the project costs, decreasing the project financing costs. This increase in equity funds causes a reduction in the loan payments over the entire repayment period and mitigates the cash outflow of the project, leading to an increase in the overall financial return from the project.

In addition to financing factors, the interplay between the construction rate and total number of units plays a key role in profitability calculations as it influences the distribution of costs and revenues over the duration of the project, thus impacting the overall NPV of the project. The construction rate and the total number of units determine the duration of the project:

where

T is the duration of the project,

N is the total number of units to sell, and

is the construction rate.

According to Equation (

18), the construction rate can be defined as the total number of units built in a year. The construction rate can directly influence two main sources of project costs and revenues, namely the total construction costs and the sales schedule. On the one hand, an increase in the construction rate will increase the construction costs over the early stages of the construction phase since it increases the construction activity. An increase in the construction activity means that the construction costs are imposed on the project sooner than expected. In other words, an increase in the construction rate shifts the construction costs to the earlier stages of the project. In this case, the total units built are increased in the earlier stages of the project with a higher construction rate, and the total units built in the later stages of the construction (e.g., the last year of construction) is decreased since the project is committed to build a particular number of units and most of the units are already built in the earlier stages of the construction phase. Assuming that construction costs stays the same during the construction phase of the project, accumulation of the construction costs in the earlier stages of the project will decrease the NPV of the project since the developers have to pay the same amount of construction costs sooner than expected.

On the other hand, an increase in the construction rate will increase the sources of revenue in the early stages of the project. Since the project sales are formulated as a percentage of units constructed each year, increasing the construction rate precedes the project sales sooner than expected, increasing the sources of project revenue, and thus increasing the NPV of the project. Therefore, the impact of increasing construction costs on the NPV of the project is dependent on the trade-off between the extra costs imposed to the project by shifting the construction costs and the extra revenue added to the project by preceding the sales schedule. According to

Table 4, results of the sensitivity analyses showed that in the test case presented here, a unit increase in construction rate,

, will increase the NPV of the project by CAD 426,774, suggesting that the revenue added to the project is higher than the extra financial burden imposed by increasing the construction rate.

Moreover, according to results from

Table 4, a unit increase in total number of units to sell,

N, will increase the NPV of the project by CAD 271,021. An increase in the total number of proposed units will increase the overall scale of the project by increasing the project costs and revenues. On the one hand, it will increase the total development costs by increasing the total construction costs, formulated per square foot, and development charges, formulated per unit, impacting the overall cash flow of the project over the construction phase. An increase in the total development costs also increases the amount of loan required to cover the project costs, increasing the loan payments over the entire project. On the other hand, an increase in the total number of proposed units will increase the project revenues by increasing the unit sales and also by increasing the developer’s fee, since the developer’s fee is formulated as a percentage of the total project costs and is collected in the last year of the project. However, since an increase in the number of proposed units does not impact the fixed costs (e.g., land acquisition costs), the revenue generated as a result of additional units would increase the NPV of the project, a reason that developers push for more height and density in most cases.

Other model parameters that play a considerable role in the profitability of the project include the broker fees, , the project overhead costs, M, the annual tax rate, , and the absorption rate, . Both broker fees and project overhead costs are formulated as a percentage of gross sales, and thus, significantly influence the cash outflow of the project. Since the gross sales stay the same in the experiments where the broker fees, , and project overhead, M, are changed, a unit increase in both broker fees and project overhead costs will equally decrease the NPV of the project by CAD 3,082,494.

Parameters such as taxes and absorption rate also directly impact the project costs and revenues. Since the taxes are formulated as a percentage of land value and considering that land value is one of the enormous costs for land acquisition, a percentage change in the tax rate, , substantially influences the cash flow of the project in the construction period. More specifically, an increase in tax rate will increase the project costs by increasing the tax payments over the construction period, thus decreasing the NPV of the project. Moreover, absorption rates can vary based on the interaction between housing market supply and demand. An increase in the absorption rate can lead to a substantial increase in project revenues, as developers gain extra profit from the unit sales.

As another important cost that can impact the developers’ decisions, construction costs, , here formulated as per square foot, are the main costs to the project over the construction phase. An increase in the total construction costs will add to the overall project costs, thus decreasing the overall return. However, the impact of construction costs on the NPV profitability calculations also depends on the distribution of the costs over the construction phase, adjusted by the construction rate. More specifically, spending the same amount of money on construction costs in the earlier stages of the construction phase rather than the later stages would decrease the NPV of the project.

Furthermore, the developer’s fee, , is a one-time cost to the project that impacts the cash flow of the project on the last year. The developer’s fee is defined as a percentage of total project costs. A percentage increase in the developer’s fee will slightly increase the total development costs by increasing the developer’s salary from the project, increasing the loan amount and loan payments.

According to

Table 5, the results also suggest that some of the parameters have a minor impact on the NPV of the project compared to other model parameters. These parameters include development charges,

, and planning and design costs,

P. However, land costs,

L, have a significant influence on profitability. All of these parameters represent a large cost/revenue influencing the cash flow of the project only once during the project’s lifetime. Development charges, land costs, and planning costs serve as initial investments for the development project, and an increase in each of these parameters will increase the costs in the first year at the beginning of the project.

4.2. Impact of Rational Expectations on Perceptions Shifts

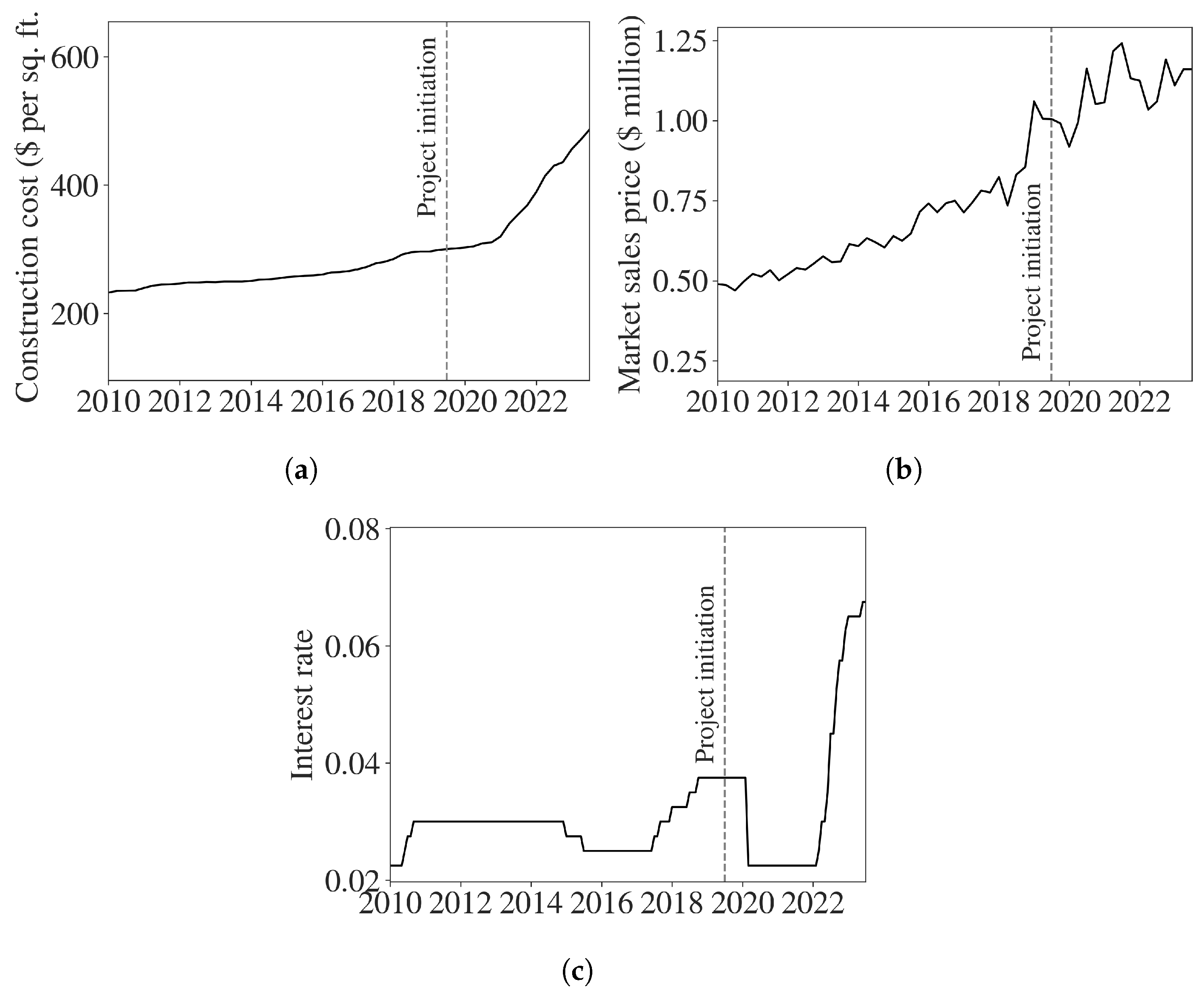

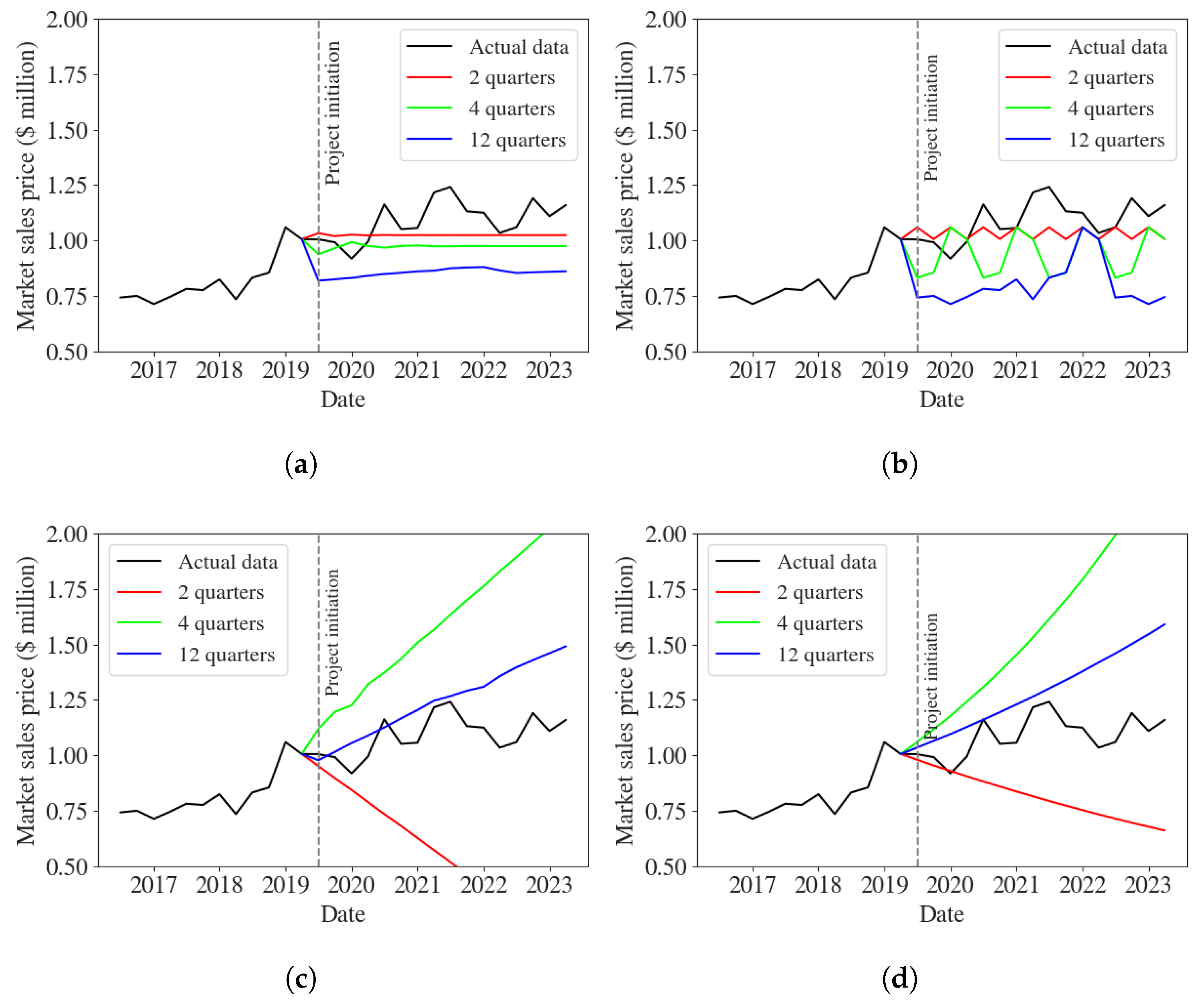

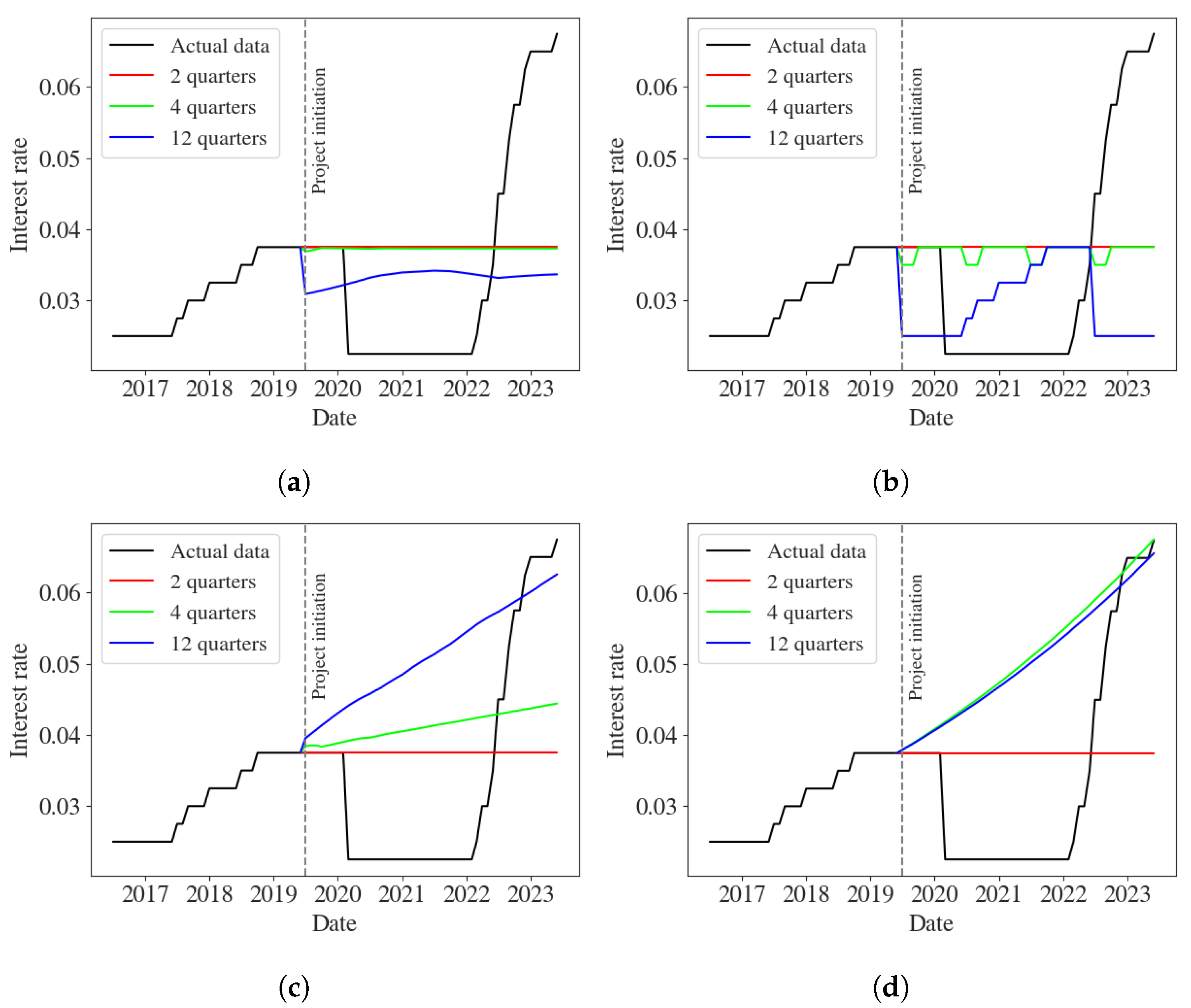

Figure 5,

Figure 6 and

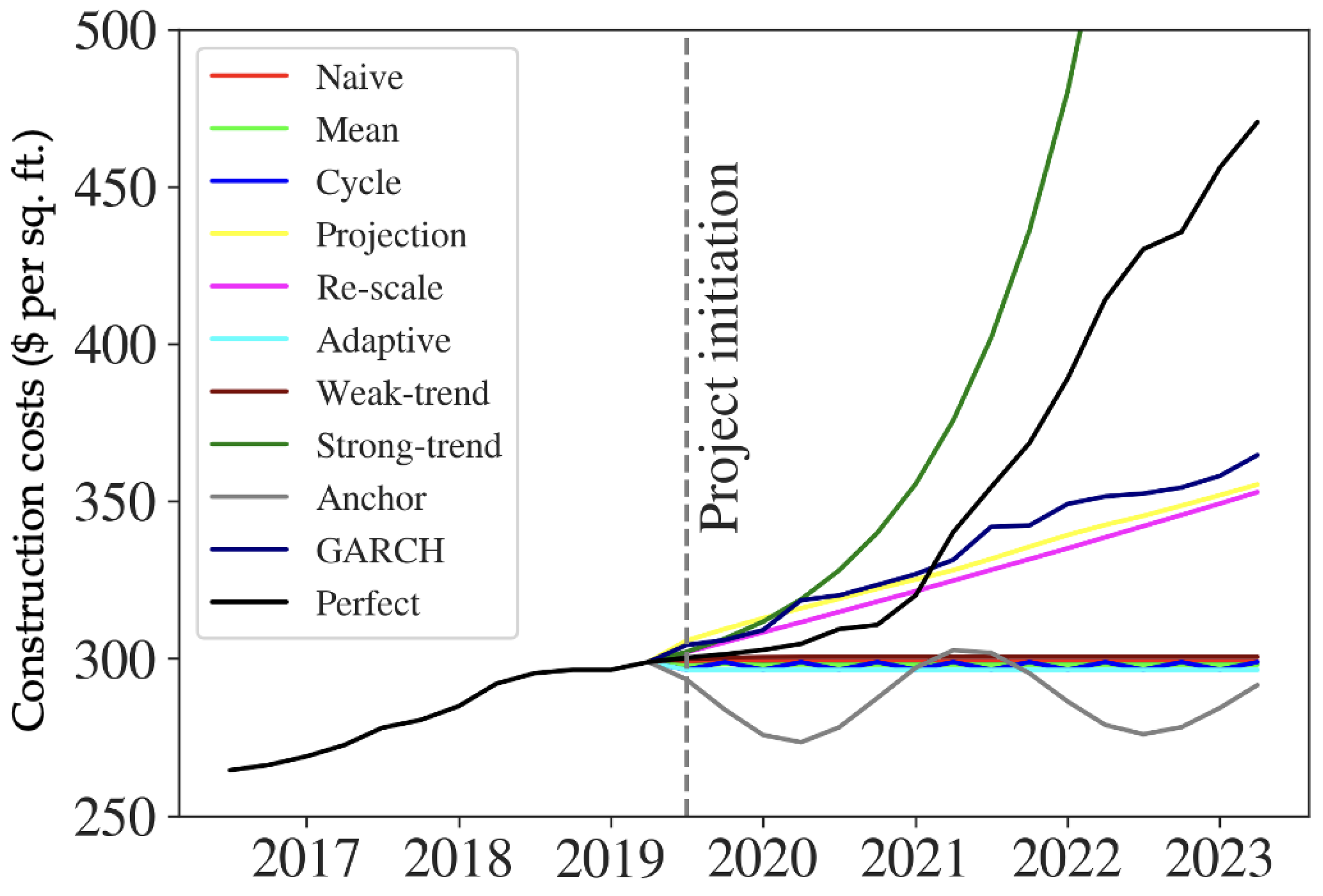

Figure 7 represent various expectation mechanisms used at project initiation in 2019 to project construction costs, unit sales prices, and interest rates, respectively. In comparing and interpreting different expectation formation models to predict market trends, it is important to consider the characteristics and limitations of each model. While some models are simple and easy to implement, they often lack accuracy due to their simplistic assumptions. For instance, models that make less use of historical data, such as the naive model, may not capture market fluctuations, cyclical patterns, or underlying factors affecting price trends. The naive model can be basically considered the “no expectation” scenario since it assumes that future prices will remain unchanged.

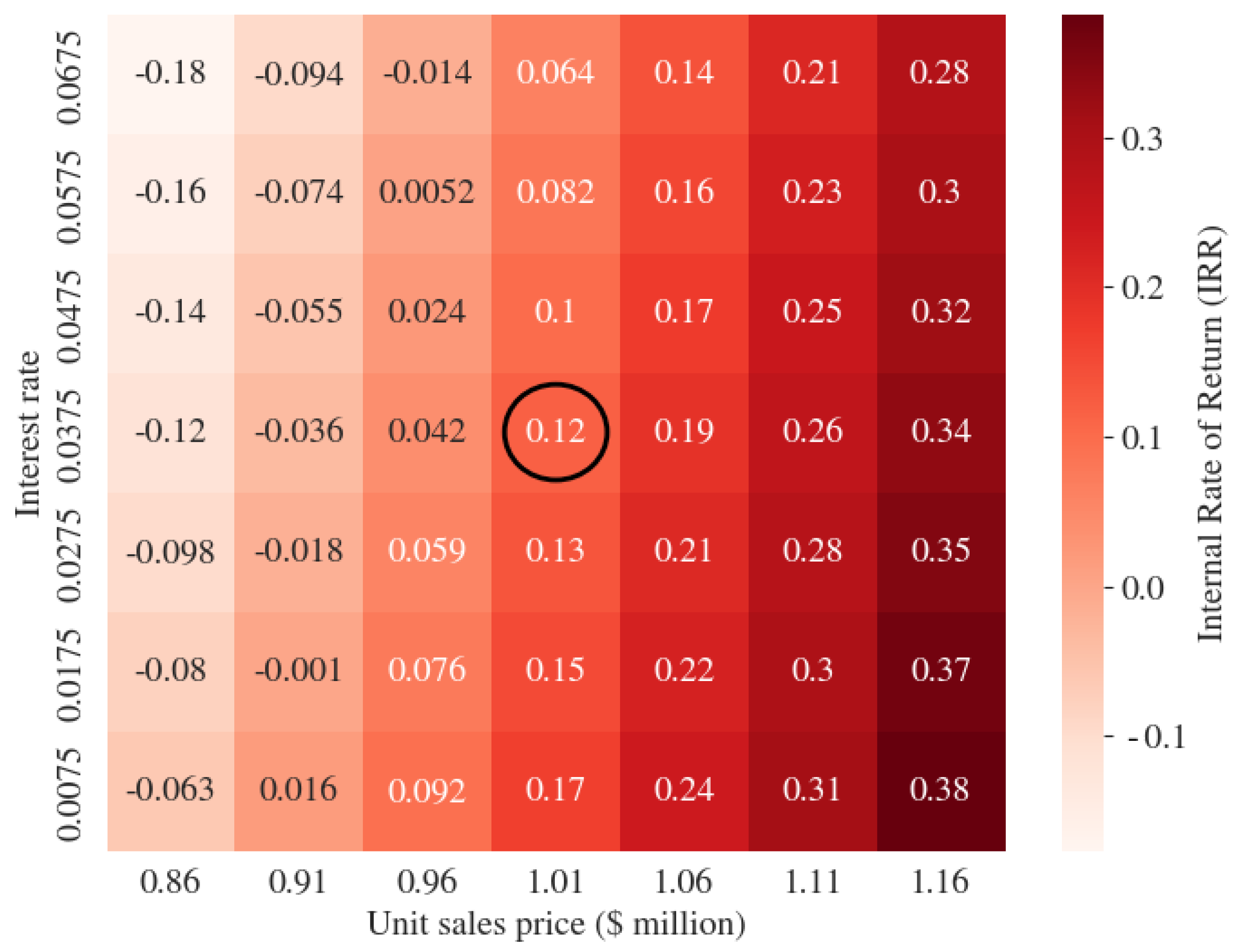

The IRR estimated for our hypothetical project is demonstrated in

Figure 8, considering the same boundedly rational expectation mechanisms are used at project initiation in 2019 to project construction costs, unit sales prices, and interest rates. In the examples provided in

Figure 8, the IRR calculated based on the actual data, shown in black bar, represents the IRR over the lifetime of the development project given that developers could perfectly predict market trends. Therefore, this value can be used as a gauge to evaluate how each of the incorporated expectation models replicates or deviates from the actual IRR values for the project.

Results highlight that alternative expectation mechanisms for each of the primary factors influencing the profitability of the development project can alter the estimated IRR value. According to

Figure 8, the IRR for the development project is estimated to be 12.6% using perfect expectation of construction costs, unit sales prices, and interest rates, while use of various models of expectation formations to project these trends leads to various IRR estimations at project initiation. The results suggest that boundedly rational developers who consider a MARR of 10% (the lower limit of IRR for project initiation according to key developer informants) would probably undertake the project in most cases, since the project meets their financial profitability criteria based on their perception of market trends.

As the project progresses, developers update their perception of costs and revenues based on new observation of market trends. By actively monitoring market trends, incorporating new data, and adapting their expectations, developers ensure that their financial projections remain relevant and reflective of the current market realities. This continuous updating process allows them to make more informed decisions throughout the development process and respond effectively to changing market dynamics.

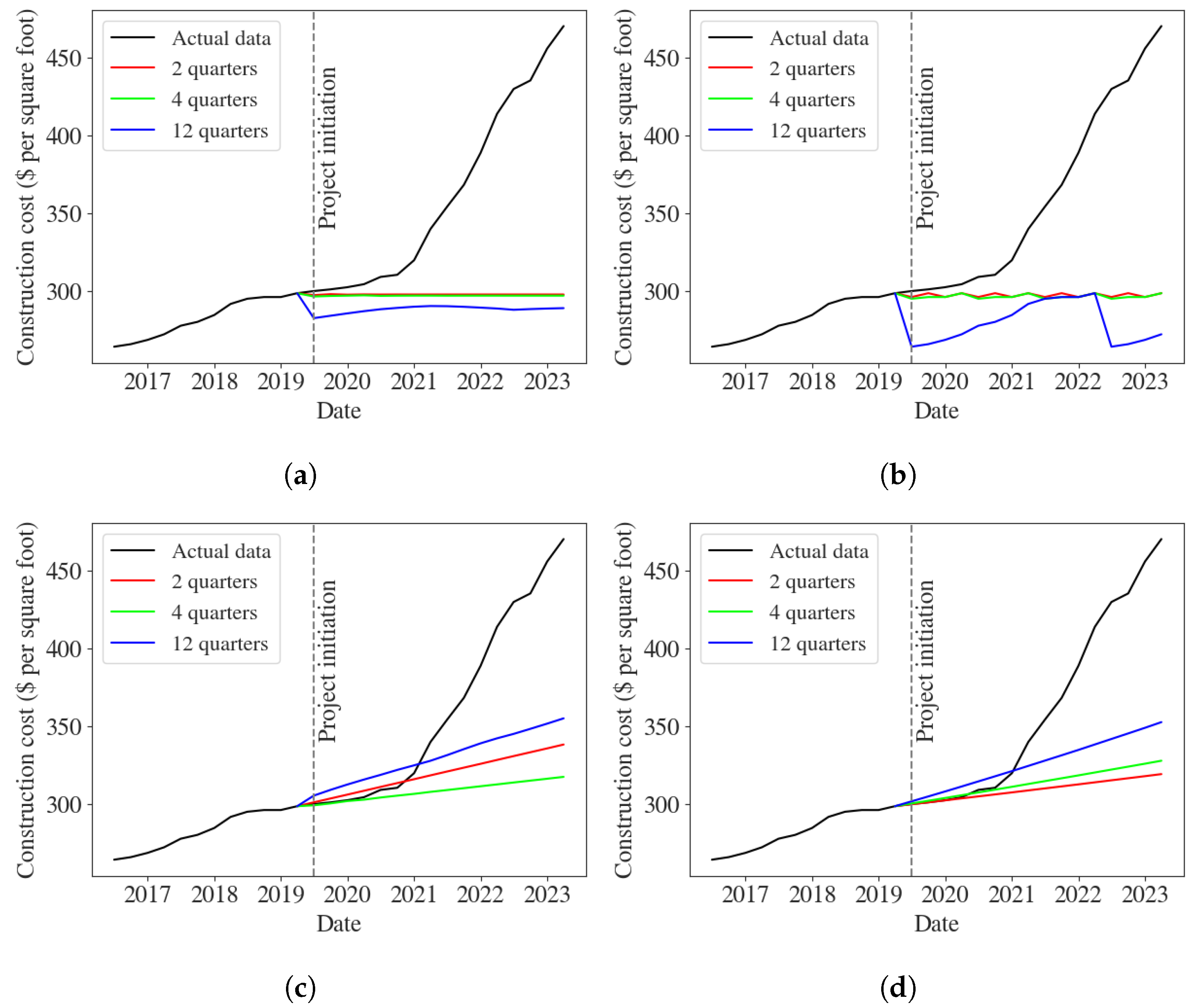

To explore how developers’ expectations of market trends during the project timeline can cause alterations in the projects, we estimated the project IRR when boundedly rational expectations are used to project construction costs, unit sales prices, and interest rates, at different times during the project. The results of this analysis are shown in

Figure 9. In performing this analysis, we used the historical data prior to the decision time to reparameterize the expectation models using the same methods described in

Section 3.4. This means that developers update their perceptions of market trends according to their new observations. For instance, when estimating the IRR a year after project initiation, developers use the historical data observed during the first year of the project to update their perceptions of trends for construction costs, unit sales prices, and interest rates for the rest of the project timeline.

As shown in

Figure 9, use of boundedly rational expectation mechanisms to project construction costs, unit sales prices, and interest rates can lead to significant variation in the estimated IRR for the project over the project timeline. Although the initial estimation of IRR in 2019 may suggest undertaking the project, the adaptively estimated IRR for the project can significantly drop in early 2020, according to the observed decreasing trends in unit sales prices and continuously increasing construction costs. According to

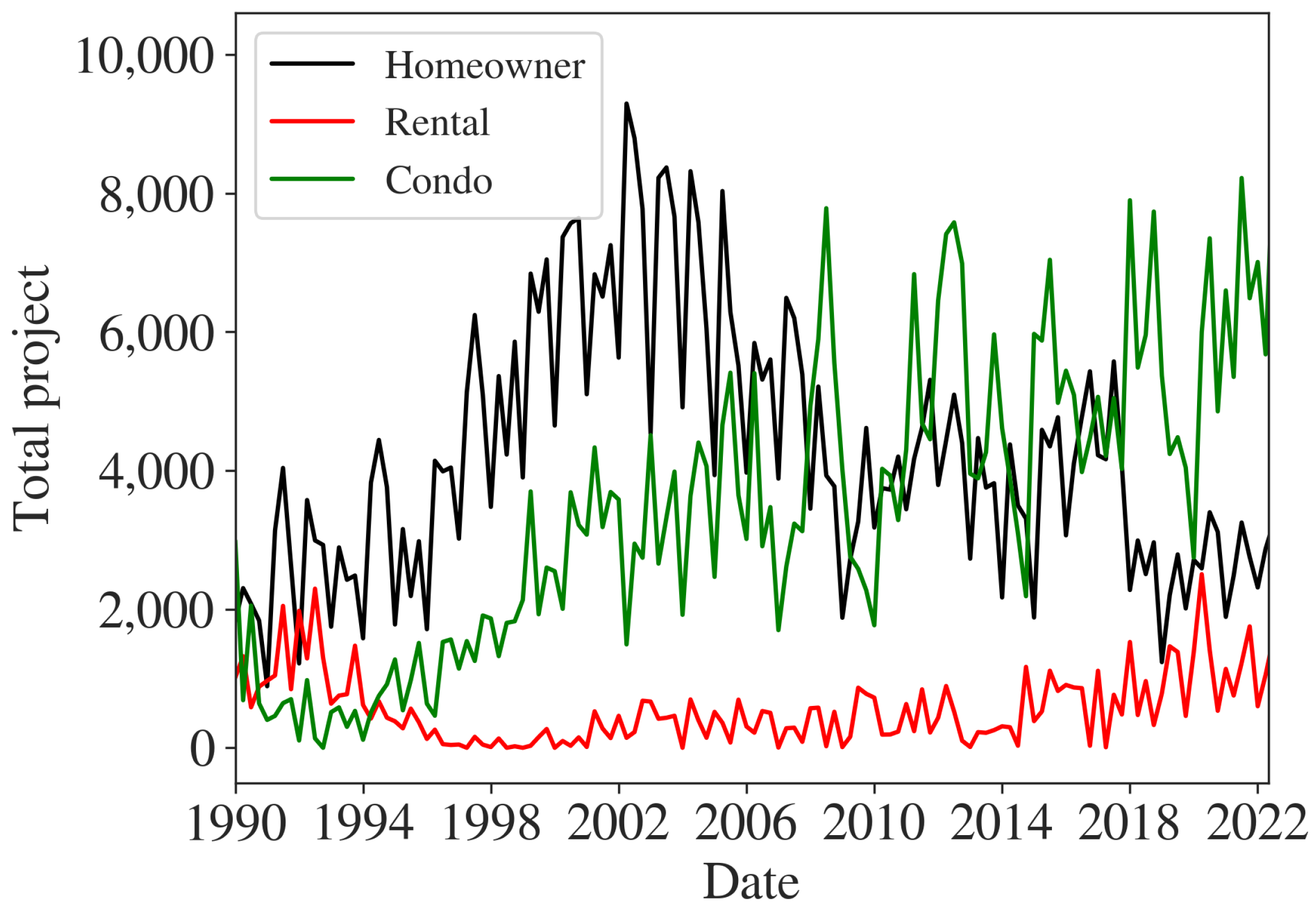

Figure 9, after one year of project initiation in April 2020, expectation models such as the naive, the mean, the cycle, and the weak-trend estimate the project IRR at −1.63%, 1.62%, 3.42%, and −1.21%, respectively. This significant drop in the estimated IRR can put the project on pause, considering that the project is no longer expected to achieve the initially estimated financial return. These results also align with historical project cancellation trends, as shown in

Figure 2, where there is an increase in the total number of project cancellations in 2020.

As time proceeds, two spikes in the project’s IRR are estimated in late 2020 and late 2021, due to decreasing interest rates and increasing unit sales prices in this period. Although the increase in construction costs has accelerated in late 2021, the results indicated that the significant increase in unit sales price during the same period could cover the extra costs imposed on the project and justify the financial feasibility of the project at this time. Observing these market trends can encourage boundedly rational developers to continue on the initiated development, hoping to achieve even higher financial returns than their initial estimations at the project start. For instance, the IRR is estimated at 33.94%, 26.55%, 33.08%, 52.01%, and 46.02% using the naive, the mean, the projection, the re-scale, and the weak-trend models, respectively. However, moving forward in the project, the estimated IRR for the project can significantly drop in 2022 and early 2023 to values below 8%, according to the rising interest rates, decreasing unit sales prices, and increasing construction costs at this period. Therefore, re-examining the financial feasibility of the project at this period can inform what adjustments in the builder’s behaviour are necessary to avoid further financial losses.

The results also indicate that adaptive expectation models that capture shifts in the market with higher accuracy can more precisely estimate the IRR values for the project. According to

Figure 9, while using the naive, the mean, the cycle, and the re-scale models of expectation leads to higher variations in the IRR estimation during the project, other models that adapt to changing trends in data, such as the projection and the adaptive model, can lead to more realistic estimations of IRR during the project timeline, meaning that these models can potentially help developers make more accurate decisions. For instance, the re-scale, the weak-trend, and the anchor and adjustment models estimate the IRR to be 47.23%, 5.9%, and −1.0% at project initiation, while the projection and the adaptive models estimate the IRR to be 16.47% and 20.34%, which are closer to the actual IRR of 12.6%. Furthermore, the GARCH model failed to capture the major shift in construction cost trends and mostly overestimated the housing prices, although it captures more accurately the volatility in prices compared to other boundedly rational expectation models. The use of the GARCH model to project construction costs, unit prices, and interest rates led to an overestimation of the expected IRR by 40.3%, as the model significantly overestimated future housing prices. According to

Figure 5, the GARCH model failed to capture the major shift in construction costs trends in 2020. Moreover, according to

Figure 6, it mostly overestimated the housing prices since 2021, although it can more accurately capture the volatility in prices compared to other boundedly rational expectation models. However, according to

Figure 9, the GARCH model can still represent the shifts in financial perceptions of housing market developers. As the project proceeds in time, recalculating the financial projections using the GARCH model for construction costs, housing prices, and interest rates, as well as also reassessing the financial viability of the projects, led to variation in the estimated IRR for the project.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}