Persistence of Oil Prices in Gas Import Prices and the Resilience of the Oil-Indexation Mechanism. The Case of Spanish Gas Import Prices

Abstract

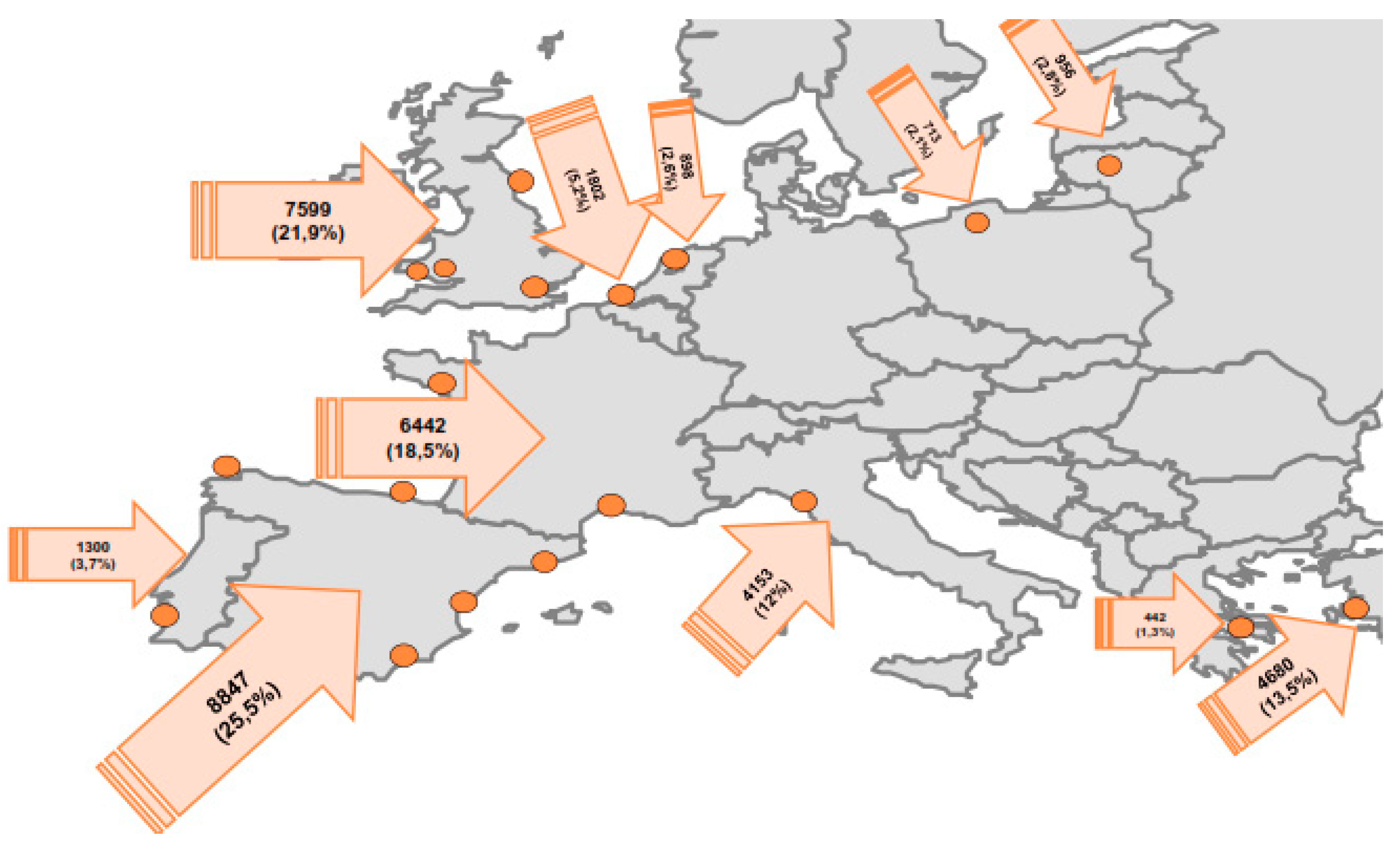

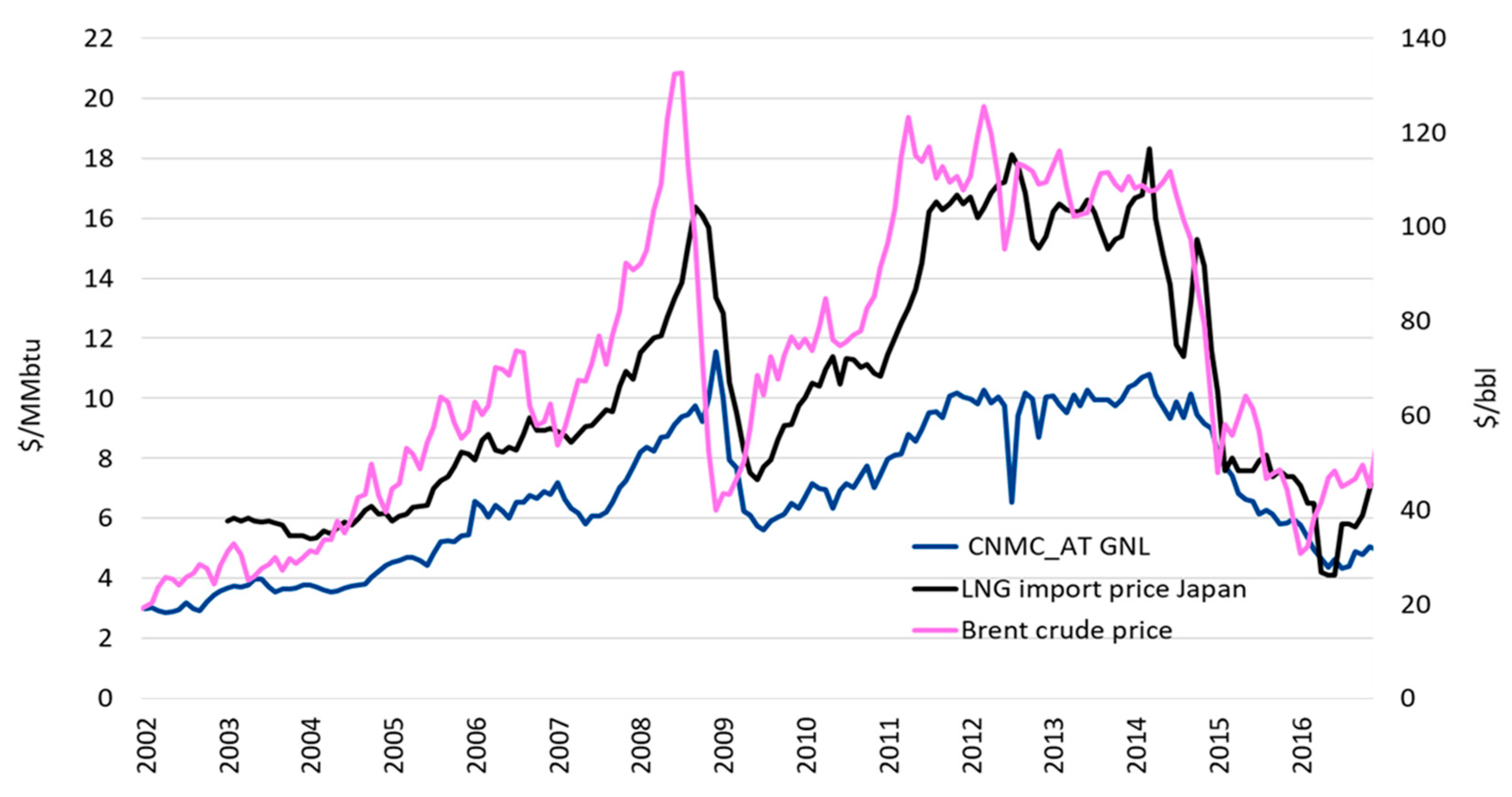

:1. Introduction

2. Results

2.1. Volatility Clustering and Nonlinear Autocorrelation

2.2. The Model

- (1)

- ARCH effects. The model shows a positive and significant ARCH parameter with a value of 0.253. This confirms the fact that larger shocks increase SG returns volatility, regardless of their signs, to a greater extent than smaller shocks. The magnitude of the effect is measured by the term determining the size of the new innovation into the series.

- (2)

- GARCH effects. These are determined by GARCH coefficients commonly named βi, i.e., those determining the influence of the past conditional volatilities on the current conditional variance. In our case since |Σ βi| ˂ 1 (|β|˂ 1 shows that the necessary stationary condition is met and establishes the conditions for covariance stationarity of the EGARCH model under particular specifications of the error distribution.) and the EGARCH model is always stationary (if εt has a Normal Distribution). Moreover, all ARCH and GARCH parameters are highly significant whereas the leverage coefficient is not. Persistence (determined by |Σ βi|) is lower than one reflecting no restrictions in the second moment although its value of 0.802 is not far from the nonstationarity boundary allowed by EGARCH models. Results of the Ljung-Box and ARCH tests on returns and residuals square respectively, using standardized innovations of the estimated model, indicate acceptance (h = 0 with highly significant p-values) of their respective null hypotheses and confirm the validity of the selected EGARCH model. Based on the above mentioned, it is reasonable to state that volatility of SG returns is genuinely persistent, with the estimated |Σ βi|) parameter controlling the decay of the autocorrelation function. Another parameter widely used to measure volatility persistence is the half-life of a volatility shock (HLS), i.e., the time it takes for the volatility to move halfway through its unconditional variance after the shock is perceived. HLS can be measured as: HLS = Ln 0.5/Ln β [33]. In our case, and to be able to compare the results with existing literature on oil price volatility persistence, we consider the β value from our EGARCH (1, 1) specification of 0.781 implying HLS of about 2.8 months or approximately 85 days. Interestingly, the evidence found for high volatility persistence in the Brent market of HLS about 87 days [14], 95 days [12] or even 128 days [13] using also EGARCH (1, 1) specifications for Brent returns reflects the high level of persistence inherited by long-term gas prices from Brent. Moreover, it can be observed that in spite of the fact that volatility persistence is inherently unobservable, it is transmitted effectively through the oil-indexation mechanism.

- (3)

- Asymmetric leverage. Reported results for the asymmetric leverage coefficients show consistent effects: the EGARCH coefficient is positive in agreement with negative coefficients found in all the GJR-GARCH models analyzed, this indicating that positive shocks would increase volatility more than negative shocks. However, none of the leverage parameters in the variance equation are significant at either 5% or 10% levels indicating that evidence of asymmetric response to good and bad news appears mixed in line with results found in literature for Brent returns [13,34,35] and in spite of asymmetry coefficient found significant in other research also using EGARCH models [14]. The potential for positive leverage effects is somehow unexpected as it is in contradiction with negative asymmetric leverage effects sometimes reported for the Brent market, i.e., downward movements (shocks) that raise oil prices are more often followed by greater volatilities than upward movements of the same magnitude that reduce the oil price [12]. In our case, the small value of the leverage coefficients and the fact that parameters are always non-significant would lead to rejecting the hypothesis of asymmetry effects on conditional volatility overall. These results would reinforce the idea of mixed effects found in the literature for asymmetric effects in oil prices.

2.3. Quantitative Evaluation of Volatility Clustering

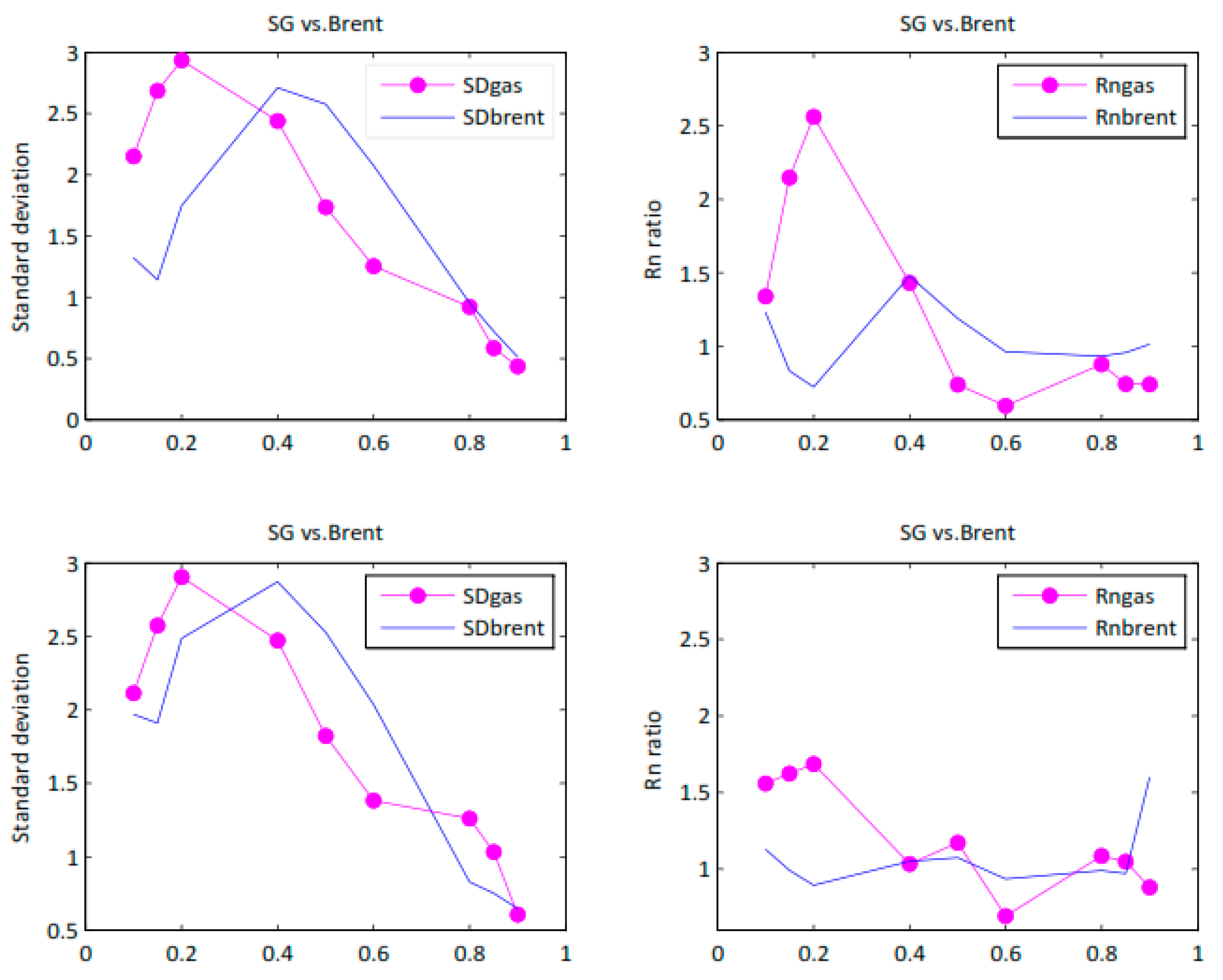

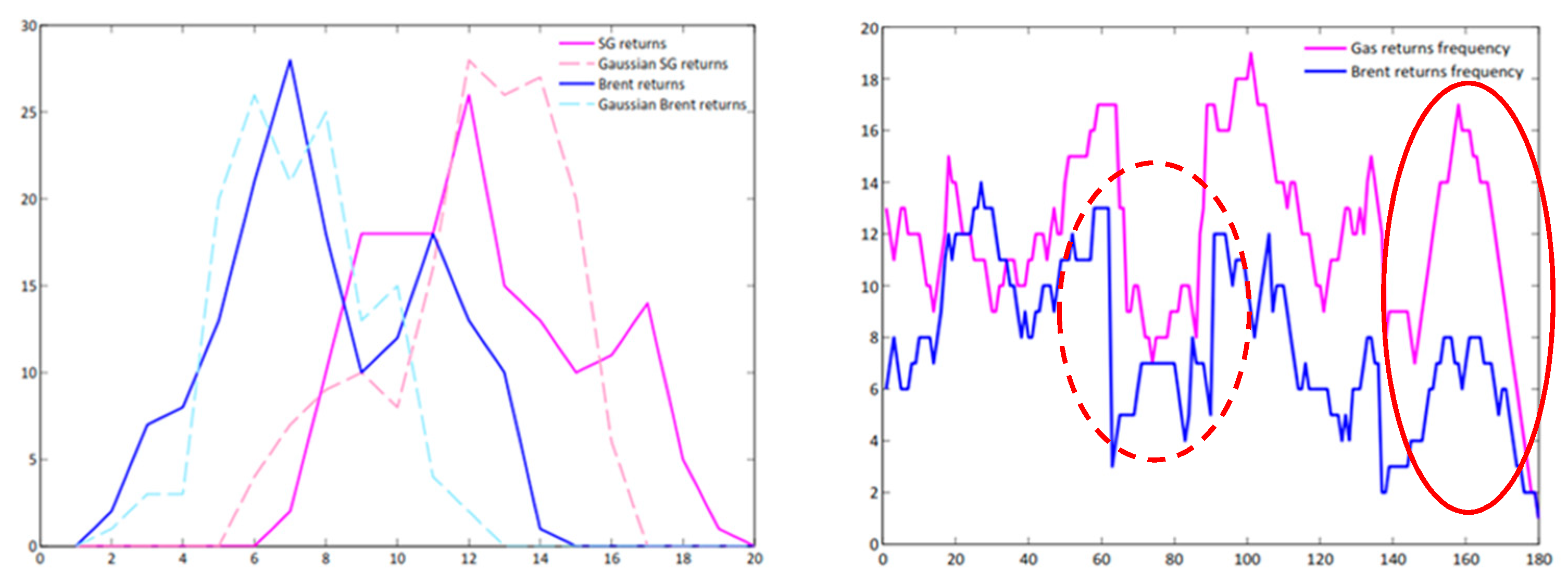

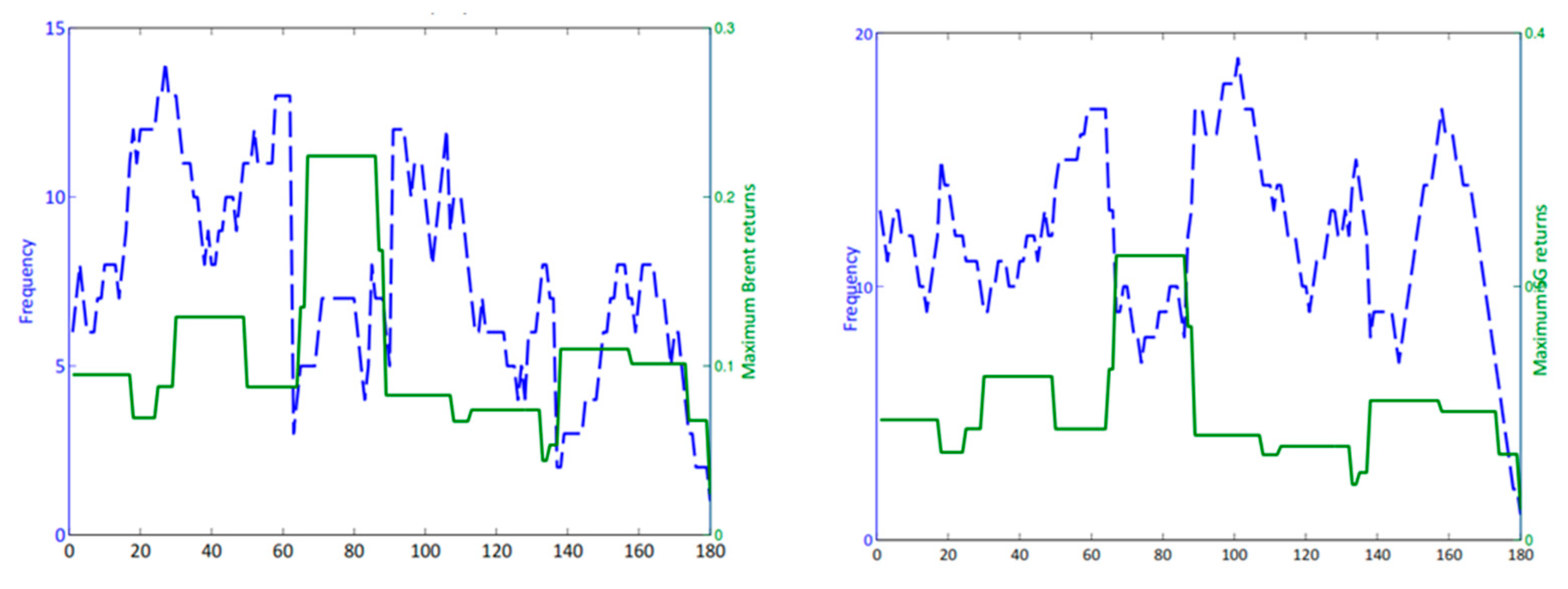

2.4. Qualitative Assessment of Oil-Indexed Effects into Gas Market Dynamics

3. Discussion

4. Material and Methods

Author Contributions

Funding

Conflicts of Interest

Appendix A

ARCH Models

GARCH Models

ASYMMETRIC GARCH Models

References

- International Energy Agency. Available online: https://www.iea.org/publications/freepublications/publication/partner-country-series-developing-a-natural-gas-trading-hub-in-asia.html (accessed on 23 December 2017).

- Aguilera, R.F.; Inchauspe, J.; Ripple, R.D. The Asia Pacific natural gas market: Large enough for all? Energy Policy 2014, 65, 1–6. [Google Scholar] [CrossRef]

- Asche, F.; Oglend, A.; Osmundsen, P. Modeling UK Natural Gas Prices when Gas Prices Periodically Decouple from the Oil Price. Energy J. 2017, 38, 1. [Google Scholar] [CrossRef]

- Ji, Q.; Geng, J.B.; Fan, Y. Separated influence of crude oil prices on regional natural gas import prices. Energy Policy 2014, 70, 96–105. [Google Scholar] [CrossRef]

- IGU (International Gas Union). Wholesale Gas Price Survey; IGU: Barcelona, Spain, 2016. [Google Scholar]

- Erdos, P. Have oil and gas prices got separated? Energy Policy 2012, 49, 707–718. [Google Scholar] [CrossRef]

- Sadorsky, P. Modelling and forecasting petroleum futures volatility. Energy Econ. 2006, 28, 467–488. [Google Scholar] [CrossRef]

- Kang, S.; Yoon, S. Forecasting Volatility of Crude Oil Markets. Energy Econ. 2009, 31, 119–125. [Google Scholar] [CrossRef]

- Cheung, C. Modelling and forecasting crude oil markets using ARCH-type models. Energy Policy 2009, 37, 2346–2355. [Google Scholar] [CrossRef]

- Sevi, B. Forecasting the volatility of crude oil futures using intraday data. Eur. J. Oper. Res. 2014, 235, 643–659. [Google Scholar] [CrossRef]

- Serletis, A.; Xu, L. Volatility and a century of energy markets dynamics. Energy Econ. 2016, 55, 1–9. [Google Scholar] [CrossRef]

- Narayan, P.; Narayan, S. Modelling Oil Price Volatility. Energy Policy 2007, 35, 6549–6553. [Google Scholar] [CrossRef]

- Mohammadi, H.; Su, L. International Evidence on Crude Oil Price Dynamics: Applications of ARIMA-GARCH Models. Energy Econ. 2010, 32, 1001–1008. [Google Scholar] [CrossRef]

- Wei, Y.; Wang, Y.; Huang, D. Forecasting crude oil market volatility using GARCH models. Energy Econ. 2010, 32, 1477–1484. [Google Scholar] [CrossRef]

- Lux, T.; Segnon, M.; Gupta, R. Forecasting crude oil price volatility and value-at-risk: Evidence from historical and recent data. Energy Econ. 2016, 56, 117–133. [Google Scholar] [CrossRef] [Green Version]

- Kang, S.H.; Cheong, C.; Yoon, S.M. Structural changes and volatility transmission in crude oil. Phys. A 2011, 390, 4317–4324. [Google Scholar] [CrossRef]

- Hou, A.; Suardi, S. A non-parametric GARCH model of crude oil price return volatility. Energy Econ. 2012, 24, 618–626. [Google Scholar] [CrossRef]

- Dritsaki, C. The performance of hybrid ARIMA-GARCH modeling and forecasting oil price. Int. J. Energy Econ. Policy 2018, 8, 14–21. [Google Scholar]

- Lin, B.; Li, J. The spillover effects across natural gas and oil markets: Based on the VEC–MGARCH framework. Appl. Energy 2015, 15, 229–241. [Google Scholar] [CrossRef]

- Souza, A.; Righi, M.B.; Schlender, S.G.; Arruda, D. Investigating dynamic conditional correlation between crude oil and fuels in non-linear framework: The financial and economic role of structural breaks. Energy Econ. 2015, 49, 23–32. [Google Scholar]

- Wang, D.; Wu, C.; Yang, L. Forecasting crude oil market volatility: A Markov switching multifractal volatility approach. Int. J. For. 2016, 32, 1–9. [Google Scholar] [CrossRef]

- Fong, W.; See, K. Markov Switching Model of the Conditional Volatility of Crude Oil Futures Prices. Energy Econ. 2002, 24, 71–95. [Google Scholar] [CrossRef]

- Di Sanzo, S. A Markov switching long memory model of crude oil price return volatility. Energy Econ. 2018, 74, 351–359. [Google Scholar] [CrossRef]

- Zhang, Y.; Zhang, Y.; Zhang, L. Interpreting the crude oil price movements: Evidence from the regime switching model. Appl. Energy 2015, 143, 96–109. [Google Scholar] [CrossRef]

- Zhang, J.L.; Zhang, Y.J.; Zhang, L. A novel hybrid method for crude oil price forecasting. Energy Econ. 2015, 49, 649–659. [Google Scholar] [CrossRef]

- Zhang, Y.; Yao, T.; He, L.; Ripple, R. Volatility forecasting of crude oil market: Can the regime switching GARCH model beat the single-regime GARCH models? Int. Rev. Econ. Financ. 2019, 59, 302–317. [Google Scholar] [CrossRef]

- Chiroma, H.; Abdulkareem, S.; Herawan, T. Evolutionary neural network model for West Texas intermediate crude oil price prediction. Appl. Energy 2015, 142, 266–273. [Google Scholar] [CrossRef]

- Li, T.; Zhou, M.; Guo, C.; Luo, M.; Wu, J.; Pan, F. Forecasting crude oil price using EEMD and RVM with adaptive PSO-based kernels. Energies 2016, 9, 1014. [Google Scholar] [CrossRef]

- Yu, L.A.; Dai, W.; Tang, L. A novel decomposition ensemble model with extended extreme learning machine for crude oil price forecasting. Eng. Appl. Artif. Intell. 2016, 47, 110–121. [Google Scholar] [CrossRef]

- Chiroma, H.; Abdulkareem, S.; Noor, A.S.M.; Abubakar, A.I.; Safa, N.S.; Shuib, L. A review on artificial intelligence methodologies for the forecasting of crude oil price. Intell. Autom. Soft Comput. 2016, 22, 449–462. [Google Scholar] [CrossRef]

- Gao, X.; Fang, W.; An, F.; Wang, Y. Detecting method for crude oil price fluctuation mechanism under different periodic time series. Appl. Energy 2017, 192, 201–212. [Google Scholar] [CrossRef]

- Kristjanpoller, W.; Minutolo, M. Forecasting volatility of oil price using an artificial neural network-GARCH model. Expert Syst. Appl. 2016, 65, 233–241. [Google Scholar] [CrossRef]

- Nelson, D. Conditional heteroskedasticity in asset returns: A new approach. Econometrica 1991, 59, 347–370. [Google Scholar] [CrossRef]

- Yang, C.; Gong, X.; Zhang, H. Volatility forecasting of crude oil futures: The role of investor sentiment and leverage effect. Resour. Policy 2018. [Google Scholar] [CrossRef]

- Chen, L.; Zerilli, P.; Baum, C. Leverage effects and stochastic volatility in spot oil returns: A Bayesian approach with VaR and CVaR applications. Energy Econ. 2018. [Google Scholar] [CrossRef]

- Niu, H.; Wang, J. Volatility clustering and long memory of financial time series and financial price model. Digit. Signal Process. 2013, 23, 489–498. [Google Scholar] [CrossRef]

- Ning, C.; Xu, D.; Wirjanto, T. Is volatility clustering of asset returns asymmetric? J. Bank. Financ. 2015, 52, 62–76. [Google Scholar] [CrossRef]

- Verme, A. A Cluster Driven Log-Volatility Factor Model: A Deepening on the Source of the Volatility Clustering. Quant. Financ. 2018, 1–16. [Google Scholar] [CrossRef]

- Tseng, J.; Li, S. Quantifying volatility clustering in financial time series. Int. Rev. Financ. Anal. 2012, 23, 11–19. [Google Scholar] [CrossRef]

- Alexander, C. Market Models: A Guide to Financial Data Analysis; John Wiley & Sons: Chichester, UK, 2011. [Google Scholar]

- Dacorogna, M.; Genc, R.; Müller, U.; Olsen, R.; Pictet, O. An Introduction to High-Frequency Finance; Academic Press: San Diego, CA, USA, 2001. [Google Scholar]

- Zivot, E.; Wang, J. Modelling Financial Time Series; Springer: Berlin, Germany, 2006. [Google Scholar]

- Buhanist, P. Path Dependency in the Energy Industry: The Case of Long-term Oil-indexed Gas Import Contracts in Continental Europe. Int. J. Energy Econ. Policy 2015, 5, 934–948. [Google Scholar]

- Konoplyanik, A. Long-term investments in the gas industry: The role of oil indexation. In Proceedings of the Workshop on Contractual Issues Related to Energy Trade, Conference Organized Jointly by the Energy Charter Secretariat & Hungarian Ministry of National Development, Budapest, Hungary, 20 March 2013. [Google Scholar]

- ACER. 5th Annual Market Monitoring Report on Gas Wholesale Markets. Available online: http://www.acer.europa.eu/Events/ACER-Workshop-on-Market-Monitoring-Wholesale-Electricity-and-Gas/Documents/Gas%20Wholesale%20MMR%20presentation%20Workshop%20-%2021%20September.pdf (accessed on 21 September 2016).

- Geng, J.; Ji, Q.; Fan, Y. How regional natural gas markets have reacted to oil price shocks before and since the shale gas revolution: A multi-scale perspective. J. Nat. Gas Sci. Eng. 2016, 36, 734–746. [Google Scholar] [CrossRef]

- Geng, J.; Ji, Q.; Fan, Y. The impact of the North American shale gas revolution on regional natural gas markets: Evidence from the regime-switching model. Energy Policy 2016, 96, 167–178. [Google Scholar] [CrossRef]

- Bachmeier, L.J.; Griffin, J.M. Testing for market integration, crude oil. Coal and natural gas. Energy J. 2006, 27, 55–72. [Google Scholar] [CrossRef]

- Hartley, P.R.; Medlock, K.B., III; Rosthal, J.E. The relationship of natural gas to oil prices. Q. J. IAEE’s Energy Econ. Educ. Found. 2008, 29, 3. [Google Scholar] [CrossRef]

- Villar, J.A.; Joutz, F.L. The Relationship between Crude Oil and Natural Gas Prices; Energy Information Administration, Office of Oil and Gas: Washington, DC, USA, 2006.

- Brigida, M. The switching relationship between natural gas and oil markets. Energy Econ. 2013, 43, 48–55. [Google Scholar] [CrossRef]

- Caporin, R.; Fontini, F. The long-run oil–natural gas price relationship and the shale gas revolution. Energy Econ. 2017, 64, 511–519. [Google Scholar] [CrossRef]

- Ashe, F.; Oglend, A.; Osmundsen, P. Gas versus oil prices the impact of shale gas. Energy Policy 2012, 47, 117–124. [Google Scholar] [CrossRef]

- Geng, J.; Ji, Q.; Fan, Y. The behavior mechanism analysis of regional natural gas prices: A multi-scale perspective. Energy 2016, 101, 266–277. [Google Scholar] [CrossRef]

- Ferderer, J.P. Oil price volatility and the macroeconomy. J. Macroecon. 1996, 18, 1–26. [Google Scholar] [CrossRef]

- Huang, B.; Hwang, M.; Peng, H. The Asymmetry of the Impact of Oil Price Shocks on Economic Activities: An Application of the Multivariate Threshold Model. Energy Econ. 2005, 27, 455–476. [Google Scholar] [CrossRef]

- Mensi, W.; Hammoudeh, S.; Min Yoon, S. Structural breaks, dynamic correlations, asymmetric volatility transmission, and hedging strategies for petroleum prices and USD exchange rate. Energy Econ. 2015, 48, 46–60. [Google Scholar] [CrossRef]

- Su, X.; Zhu, H.; You, W.; Ren, Y.; Hwang, M.J.; Huang, B.N. Heterogeneous effects of oil shocks on exchange rates: Evidence from a quantile regression approach. SpringerPlus 2016, 5, 1187. [Google Scholar] [CrossRef]

- Tiwari, A.K.; Albulescu, C.T. Oil price and exchange rate in India: Fresh evidence from continuous wavelet approach and asymmetric, multi-horizon Granger-causality tests. Appl. Energy 2016, 179, 272–283. [Google Scholar] [CrossRef]

- Sun, X.; Lu, X.; Yue, G.; Li, J. Cross-correlations between the US monetary policy, US dollar index and crude oil market. Phys. A 2017, 467, 326–344. [Google Scholar] [CrossRef]

- Sadorsky, P. Correlations and volatility spillovers between oil prices and the stock prices of clean energy and technology companies. Energy Econ. 2012, 1, 248–255. [Google Scholar] [CrossRef]

- Hayette, G. Linking the gas and oil markets with the stock market: Investigating the U.S. relationship. Energy Econ. 2016, 53, 5–15. [Google Scholar]

- Huang, S.; Haizhong, A.; Gao, X.; Sun, X. Do oil price asymmetric effects on the stock market persist in multiple time horizons? Appl. Energy 2017, 185, 1799–1808. [Google Scholar] [CrossRef]

- Plourde, A.; Watkins, G. Crude oil prices between 1985 and 1994: How volatile in relation to other commodities? Resour. Energy Econ. 1998, 20, 245–262. [Google Scholar] [CrossRef]

- Zhang, C.; Shi, X.; Yu, D. The effect of global oil price shocks on China’s precious metals market: A comparative analysis of gold and platinum. J. Clean. Prod. 2018, 186, 652–661. [Google Scholar] [CrossRef]

- Pindyck, R.S. Volatility in Natural Gas and Oil Markets; Massachusetts Institute of Technology: Cambridge, MA, USA, 2004; in press. [Google Scholar]

- Regnier, E. Oil, and energy price volatility. Energy Econ. 2006, 29, 405–427. [Google Scholar] [CrossRef]

- Rafiq, S.; Bloch, H. Explaining commodity prices through asymmetric oil shocks: Evidence from nonlinear models. Resour. Policy 2016, 50, 34–48. [Google Scholar] [CrossRef]

- Meyer, D.F.; Sanusi, K.A.; Hassan, A. Analysis of the asymmetric impacts of oil prices on food prices in oil-exporting, developing countries. J. Int. Stud. 2018, 11, 82–94. [Google Scholar] [CrossRef]

- Haugom, E.; Langeland, H.; Molnár, P.; Westgaard, S. Forecasting volatility of the US oil market. J. Bank. Financ. 2014, 47, 1–14. [Google Scholar] [CrossRef]

- Baumeister, C.; Lutz, K. Forecasting the Real Price of oil in a Changing World: A Forecast Combination approach. J. Bus. Econ. Stat. 2015, 33, 338–351. [Google Scholar] [CrossRef]

- Balaban, E.; Lu, S. Forecasting the term structure of volatility of crude oil price changes. Econ. Lett. 2016, 141, 116–118. [Google Scholar] [CrossRef]

- Barunik, J.; Malinska, B. Forecasting the term structure of crude oil futures prices with neural Networks. Appl. Energy 2016, 164, 366–379. [Google Scholar] [CrossRef]

- Pindyck, R.S. The long-run evolution of energy prices. Energy J. 1999, 20, 1–27. [Google Scholar] [CrossRef]

- Ozdemir, Z.A.; Korhan, G.; Cagdas, E. Persistence in Crude oil spot and future prices. Energy 2013, 59, 29–37. [Google Scholar] [CrossRef]

- Engle, R. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica 1982, 55, 987–1007. [Google Scholar] [CrossRef]

- Bollerslev, T. Generalized Autoregressive Conditional Heteroscedasticity. J. Econom. 1986, 31, 307–327. [Google Scholar] [CrossRef]

- Glosten, L.; Jagannathan, R.; Runkle, D. On the Relation between the Expected Value and the Volatility of the Nominal Excess Return on Stocks. J. Financ. 1993, 48, 1779–1801. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Model | Number of Parameters | L | AIC | BIC |

|---|---|---|---|---|

| G11 | 4 | 301.647 | −595.294 | −583.415 |

| EG11 | 5 | 300.629 | −591.258 | −576.409 |

| GJR11 | 5 | 301.652 | −593.305 | −578.456 |

| G21 | 5 | 301.647 | −593.294 | −578.445 |

| EG21 | 6 | 304.176 | −596.353 | −578.534 |

| GJR21 | 6 | 301.652 | −591.305 | −573.486 |

| G33 | 8 | 303.121 | −590.242 | −566.483 |

| EG33 | 11 | 304.790 | −587.581 | −554.913 |

| GJR33 | 11 | 303.291 | −584.583 | −551.915 |

| G23 | 7 | 303.036 | −592.072 | −571.284 |

| EG23 | 10 | 304.669 | −589.337 | −559.639 |

| GJR23 | 10 | 303.420 | −586.840 | −557.142 |

| G31 | 6 | 301.647 | −591.294 | −573.475 |

| EG31 | 7 | 304.177 | −594.354 | −573.565 |

| GJR31 | 7 | 301.652 | −589.305 | −568.516 |

| G32 | 7 | 303.073 | −592.146 | −571.357 |

| EG32 | 9 | 304.604 | −591.209 | −564.480 |

| GJR32 | 9 | 303.282 | −588.564 | −561.836 |

| SG Returns | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| GARCH (1,1) | EGARCH (2,1) | GJR-GARCH (1,1) | |||||||

| Coefficients | Error | Statistic | Coefficients | Error | Statistic | Coefficients | Error | Statistic | |

| C | 0.007 | 0.003 | 1.954 | 0.006 | 0.003 | 2.110 | 0.007 | 0.003 | 1.958 |

| K | 0.001 | 0.000 | 1.630 | −1.229 | 0.372 | −3.305 | 0.001 | 0.000 | 1.526 |

| GARCH(1) | 0.531 | 0.186 | 2.853 | 1.507 | 0.138 | 10.952 | 0.536 | 0.196 | 2.737 |

| GARCH(2) | −0.705 | 0.160 | −4.395 | ||||||

| ARCH (1) | 0.248 | 0.092 | 2.688 | 0.253 | 0.089 | 2.848 | 0.259 | 0.125 | 2.080 |

| Leverage 1 | 0.020 | 0.049 | 0.398 | −0.019 | 0.159 | −0.118 | |||

| Log(L) | 301.647 | 304.176 | 301.652 | ||||||

| Ljung-Box Q-test | p-value | Qstat | Critical | p-value | Qstat | Critical | p-value | Qstat | Critical |

| p-value[2]/Q[2]/Critical | 0.315 | 2.312 | 5.992 | 0.738 | 0.609 | 5.992 | 0.311 | 2.336 | 5.992 |

| p-value[5]/Q[5]/Critical | 0.357 | 5.513 | 11.071 | 0.664 | 3.234 | 11.071 | 0.336 | 5.706 | 11.071 |

| p-value[10]/Q[10]/Critical | 0.116 | 15.453 | 18.307 | 0.309 | 11.652 | 18.307 | 0.105 | 15.827 | 18.307 |

| p-value[15]/Q[15]/Critical | 0.197 | 19.377 | 24.996 | 0.405 | 15.665 | 24.996 | 0.183 | 19.713 | 24.996 |

| p-value[20]/Q[20]/Critical | 0.341 | 22.000 | 31.410 | 0.597 | 17.860 | 31.410 | 0.320 | 22.393 | 31.410 |

| h Engle´s Arch test | 0 | 0 | 0 | ||||||

| p-value/stat/critical Engle´s Arch | 0.528 | 0.398 | 3.842 | 0.659 | 0.195 | 3.842 | 0.511 | 0.570 | 3.842 |

| Jarque-Bera Test/p-value/stat | 0 | 0.221 | 2.553 | 0 | 0.500 | 0.532 | 0 | 0.208 | 2.652 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cansado-Bravo, P.; Rodríguez-Monroy, C. Persistence of Oil Prices in Gas Import Prices and the Resilience of the Oil-Indexation Mechanism. The Case of Spanish Gas Import Prices. Energies 2018, 11, 3486. https://doi.org/10.3390/en11123486

Cansado-Bravo P, Rodríguez-Monroy C. Persistence of Oil Prices in Gas Import Prices and the Resilience of the Oil-Indexation Mechanism. The Case of Spanish Gas Import Prices. Energies. 2018; 11(12):3486. https://doi.org/10.3390/en11123486

Chicago/Turabian StyleCansado-Bravo, Pablo, and Carlos Rodríguez-Monroy. 2018. "Persistence of Oil Prices in Gas Import Prices and the Resilience of the Oil-Indexation Mechanism. The Case of Spanish Gas Import Prices" Energies 11, no. 12: 3486. https://doi.org/10.3390/en11123486

APA StyleCansado-Bravo, P., & Rodríguez-Monroy, C. (2018). Persistence of Oil Prices in Gas Import Prices and the Resilience of the Oil-Indexation Mechanism. The Case of Spanish Gas Import Prices. Energies, 11(12), 3486. https://doi.org/10.3390/en11123486