1. Introduction

The deployment of new technologies to manage the grid operational levels, starting from the generation and down to the demand level, is set to create a reliable, efficient and economic power system. This is one of the main benefits of the current evolution of conventional electric grids into smarter and more flexible ones. However, the wide penetration of low carbon technologies, accompanied with the increase of electricity demand, has imposed many challenges on distribution networks. Consequently, various market players and policy makers have encouraged the idea of flexible resources as a way of coping with such challenges. New technologies such as intelligent smart meters, autonomous load controllers and advanced information and communication automations, are capable of providing sustainable minute-by-minute information to efficiently deploy demand response (DR) programs [

1,

2].

DR are programs established to encourage end-user customers in adjusting their electric usage, in response to changes in electricity prices over time, or incentive payments [

3]. DR programs help reducing electricity consumption at hours of high demand or uphold the reliability of electrical systems when their security is jeopardized [

4,

5]. This paper focuses on demand side flexibility (DSF), which is one of main types of incentive-based DR programs [

6,

7,

8]. DSF encourages customers to actively participate in electricity markets by submitting increasing or decreasing capacity volumes [

9,

10,

11]. Moreover, DSF can be used as a portfolio optimization source for market players who need to meet their energy requirements. Besides, it can provide balancing and constraint management services for system operators such as transmission and distribution system operators (TSOs) and (DSOs), to maintain system reliability and security [

12]. However, the deployment of DSF faces many challenges that vastly impacts its value [

13]. The absence of appropriate market mechanisms in current market structures is one of the main causes of delaying its full potential [

14]. Other considerations must be faced in insular systems, where security issues are even more pressing than in large continental grids, as remarked in [

15], and a risk analysis is advisable in order to deal with them for the daily operational planning. Besides, in insular systems, the DSO can dispatch generation and storage units.

The objective of this paper is optimizing the usage of DSF in a day-ahead timeframe at the distribution level to assist the DSO in mitigating network congestions. There has been vast literature addressing this issue, for example, a day-ahead planning framework for flexible demand bidding strategies is introduced in [

16]. The objective of the proposed model is to maximize the profit for the flexibility providers by forecasting the aggregated load demand of customers and consecutively building flexibility offers. Similarly, another short-term planning models for optimal flexibility bidding are introduced in [

17,

18]. These studies focus on the effect of price elasticity on short-term planning in the framework of day-ahead markets. A decision making problem for optimal flexible energy resources scheduling to meet the DSO requests was suggested in [

19]. The paper proposes a new type of aggregator called smart energy provider (SESP) to handle all flexible energy sources. Moreover, it presents a local electricity market for flexibility trading. Optimization models focusing on maximizing the potential of DSF and the financial benefits for both, customers and system operators, are addressed in [

20,

21,

22]. Such studies have concluded that the efficient usage of DSF at the hours of grid contingencies can alleviate such congestions, thus increasing the reliability of the grid operation. Furthermore, DSF can help in deferring the need of grid reinforcements in many cases [

23].

While the aforementioned studies are significant contributions, they mainly focus on the bidding processes, bidding strategies and effects of price elasticity. However, less attention has been given to the effects of demand flexibility in mitigating network congestions. In addition, two mutually important key factors were absent in previous works. First factor has to do with grid power flow constraints. In general, the optimal operation of transmission and distribution networks is controlled by close monitoring of the power flow within the grid and the voltage levels at every node. Modelling the grid constraints can be problematic due to its complexity. However, considering them is essential to realistically model the impact of demand flexibility activations at the distribution level. Secondly, in most cases when customers are asked to provide demand flexibility, their loads are shifted from one point in time to another. This shift can alleviate one congestion and create another one by moving the peak from high priced hours to low priced hours. This effect is regarded in literature as the rebound effect or payback effect [

24]. Such event is crucial to the flexibility beneficiaries as they must consider the repercussions of activating flexibility services on their day-ahead operation.

The work presented here aims to build on what was carried out in [

25,

26,

27] and further advance towards presenting a realistic framework for demand flexibility management. The proposed framework considers two types of demand flexibility, load increase and decrease volumes that can be a valuable tool to the DSO in the congestion management process. In addition, the paper exploits the demand flexibility that can be obtained from the industrial and residential sectors. Two real distribution network feeders in Spain are used as case studies to show the advantages that demand flexibility types can offer in the process of congestion solution, while minimizing the cost of flexibility procurement for the DSO. The main contributions of this paper are:

Proposing a simple but realistic model for a flexibility market operating at the distribution level. This market serves as a platform for flexibility transactions and it facilitates the trading between flexibility beneficiaries and providers. The flexibility market is operated by the DSO and it takes place after the day-ahead wholesale market. The proposed market structure does not require complex changes in regulations and it avoids the DSO’s need to participate in energy trading.

Formulating and solving an optimization problem that models the total cost incurred by the DSO when activating the flexibility services. The method is easy to implement and can be integrated with already existing Optimal Power Flow (OPF) solver tools. The grid power flow constraints and the rebound conditions are considered and modeled. Therefore, the DSO always performs a technical validation of the demand flexibility solution, avoiding unforeseen problems that can arise from the rebound effect.

It must be remarked that the proposed flexibility market mechanism does not deal with security issues that must be solved using a different method, even without making use of market solutions. A risk analysis should be performed in order to meet the security requirements of a distribution system when demand response is considered. This analysis, however, is out of the scope of the paper.

The organization of this paper can be described as follows. In

Section 2, an overview about demand flexibility is given along with the stakeholders involved in its paradigm. In

Section 3, the proposed flexibility market is introduced and explained.

Section 4 discusses the problem formulation regarding optimizing the cost of purchasing DSF. Moreover,

Section 5 carries out a detailed two-case study to highlight the merits of DSF in efficiently managing grid congestions. Finally,

Section 6 concludes the paper.

2. Demand Flexibility Overview & Stakeholders

Flexibility can be defined as the ability of adjusting generation and/or consumption profiles in response to external market signals. It can be utilized to provide energy balancing services for TSOs and balance responsible parties (BRPs), power quality control or, as proposed here, congestion management [

11]. Demand flexibility has been used for many years at the transmission level in some countries, and expanding it to the distribution level is becoming feasible and convenient. However, a number of challenges must be addressed to allow its implementation [

28]. In this section, the different kinds of flexibility used, the stakeholders involved and the roles that they can play in flexibility markets are described.

2.1. Demand Flexibility Types

The shape, quantity and direction of available flexibility may vary depending on the type of the customer. Such features determine the way flexibility is integrated into electricity markets [

29]. Here, demand flexibility is addressed from the DSO’s perspective. Since the flexibility offered by the demand side can take the form of either increasing or decreasing the load, two kinds of flexibility are defined, named up-regulation (UREG) and down-regulation (DREG) flexibility. Customers offering UREG flexibility provide load reduction volumes, while customers offering DREG flexibility provide load increase volumes. In a market-oriented approach for flexibility management, such as the one considered here, these volumes can be translated into up-regulation bids (URB) and down-regulation bids (DRB) respectively and can be offered for sale to other market participants.

Demand flexibility consists of increasing or decreasing the load at one hour, which then may require shifting that amount to another hour. This shifting of energy may produce further problems in the grid, for instance, if the reduced energy due to UREG flexibility is recovered by the customer at a load peak hour, producing further congestion. This can be referred to as the energy rebound effect [

30]. Thus, it is essential for the DSO to consider the rebound effect properly when managing demand flexibility. Moreover, the conditions under which the rebound effect takes place should be agreed upon between the flexibility supplier and the DSO. The rebound conditions considered here are the rebound hour and the rebound power. The rebound hour is the hour at which the regulation power is shifted to, while the rebound power is the share of regulation power (UREG or DREG) that must be recovered to the customer. The rebound conditions are dependent on the type of customers and the nature of the load providing the flexibility. For example, the rebound power can either be equal to the activated flexibility, or just a percentage of it. For the rebound hour, customers have the possibility of deciding the most convenient hour to have the rebound power. Therefore, rebound hour can either be a specific hour, or any hour during a time interval of the day or it can be unrestricted. Considering the rebound effect of demand flexibility is crucial for the DSO to avoid possible subsequent problems in the network. However, it adds further complexities to the task of the DSO. In very large networks with thousands of customers and possibly hundreds of aggregated flexibility bids, choosing the optimal bid may require sophisticated mathematical methods and computing power.

In order to differentiate between the rebound power of both UREG and DREG flexibilities, two different names will be assigned to each one of them. Since UREG requires supplying back the regulation power at the rebound hour, the rebound effect will be referred to as the payback effect (PB), with payback power at the payback hour [

31]. On the other hand, as the DREG requires a decrease of the load at the rebound hour, it will be referred to as the rebate effect (REB), with rebate power at the rebate hour. As already mentioned, in certain cases the rebound effect may create new network congestions. Such cases may occur if the PB creates unexpected new peaks, or when the REB decreases the load leading to overvoltages.

Table 1 summarizes the types of DSF with their corresponding type of rebound effect. It should be noted that, while previous work has discussed the payback effect from the perspective of UREG flexibility [

24], there are no current studies that address the rebound effect in case of DREG flexibility, up to the knowledge of the authors.

The involvement of the main stakeholders expected to be connected to the management of demand flexibility is summarized in the following subsections.

2.2. Distribution System Operators (DSOs)

Demand flexibility allows the DSO to manage grid congestions by avoiding demand peaks. This can possibly lead to deferring the need for network reinforcements [

32], decreasing the total capital and operation expenditures of distribution networks [

33]. In addition, demand flexibility provides more resources to manage the requirements of the increasingly high penetration of DERs based on RES. One of the key factors to ensure the success of flexibility is having the necessary coordination between the DSO and TSO. Such coordination is essential to avoid needles flexibility requirements which can lead to further grid problems [

34].

Here, demand flexibility is modeled and centered on tackling the issue of congestion management at the distribution level. While there is a major potential for DSF in distribution systems, many complexities and challenges arise, which must be addressed. For example, as highlighted in [

35], the large number of customers at distribution levels requires a state-of-the-art communication infrastructure in order to gather all the information required from the participating customers. Moreover, the current regulatory policies do not incentivize such smart grid solutions nor demand response programs, and may hinder the full exploitation of demand flexibility [

36]. A realistic regulation must keep the basic principle of unbundling activities and limit the activities of the DSO to those coming from its role as a natural monopolist. The market design proposal described in

Section 3 of this paper is intended to preserve this essential point of current market architecture.

2.3. Aggregators

Given the implementation of the appropriate regulation, the foreseen potential of demand flexibility may be an attractive source of revenue for customers from different sectors. However, the limited resources of many customers may impose certain challenges on their participation in flexibility markets. In that case, aggregation services offered by an aggregator may be of use to these customers. The aggregator has been defined in a general way as “

a company who acts as an intermediary between electricity end-users and DER owners and the power system participants who wish to serve these end-user or exploit the services provided by these DERs” [

37]. To limit the broad scope of that definition, here an aggregator is considered as a company which helps electricity consumers to take part in demand flexibility programs [

38]. Its main responsibility is to collect demand flexibility from its affiliated customers, aggregate it into flexibility bids, and trade such flexibility in flexibility markets considering its and the customers’ best interest [

39,

40].

There are various responsibilities that the aggregator can take, other than aggregation [

41,

42,

43]. Aggregators may take the roles of energy retailers or BRPs. Such many tasks assigned to the aggregator can have advantages and disadvantages. One of the main disadvantages is that assigning the role of retailing to the aggregator could allow him to exercise market power. Aggregators can deliberately create bids in the day-ahead market that would result in network congestions, which then force the DSO to activate their aggregated flexibility [

38]. However, avoiding the issue of market power is rather difficult even if the aggregator is not a retailer (for example, congestions that can be alleviated only by one aggregator). Possible measures to mitigate such issue might be long term contracts, flexibility price caps [

19], and efficient monitoring of irregular market bids comparing them to DSO forecasts. Also, the DSOs’ use of flexibility depends on its economic value compared to reinforcing the grid. Therefore, aggregators will always be inclined to present flexibility prices in the allowed price range of DSOs. On the advantageous side, aggregators remove the complex burden of market participation from the customers by enabling them to deal with only a single entity [

44]. As for the system, it is expected that the aggregator would be responsible for the imbalances resulting between the actual and the forecasted demand and generation, due to the flexibility activation. Thus, a more effective balancing operation will be achieved if the aggregator acts as a BRP. Moreover, the overall efficiency of this arrangement will be higher because of the economies of scope involved [

37]. Some proposals consider this merging of activities (flexibility manager, retailer and BRP) as a possibility, such as CENELEC [

45] or VTT [

38].

A contractual relationship must exist between the aggregator and the customers, where it would comprise all details regarding their energy consumption, flexible loads that the aggregator can harness from demand flexibility and the rebound conditions. In return, it is the aggregator’s responsibility to present to the DSO the aggregated flexibility bids, including their rebound conditions. However, the type of contractual agreement between the aggregator and the customers, and the methods of interaction between them, falls out of the scope of this paper. Additionally, the strategies of aggregators aimed to exercise market power are not considered. We assume that aggregators act in a rational and fair manner.

2.4. Consumers

Consumers, or prosumers in case they are DER owners, are the main providers of demand flexibility. Their participation in flexibility programs is dependent on the sector they belong to and the type of loads involved. Flexibility sources have been characterized in CENELEC [

45], from the least to the most flexible, as uncontrollable, curtailable, shiftable, buffered and freely controllable. Uncontrollable loads are not capable of providing flexibility [

46]. Curtailable loads can offer demand flexibility without the need of rebound conditions, as they are unshiftable. Shiftable loads can be moved at any time during the day, but their rebound conditions must be met, as they are uncurtailable. Here, only curtailable and shiftable loads for industrial and residential sectors are considered.

On average, industrial customers represent 2–10% of the total customers of a given grid. However, they contribute to a 80% of the electricity consumption [

47]. The potential of flexibility in the industrial sector, and the possible forms that it can take, has been investigated thoroughly in [

7,

48]. The level of flexibility offered by the industrial customers can be affected by several factors, such as process criticality, available production lines and production targets. For example, according to [

49], industrial productions of zinc, copper and aluminum are considered as curtailable loads. Other industries such as cement mills and paper recycling can be shifted to either earlier or later times of the day. Thermal industrial loads that depend on cooling or heating may be as well shifted, but in some cases only after the flexibility activations.

The residential sector evolution from a passive to an active behavior can have a large impact on the implementation of flexibility. With the ongoing technological advancements, the typical households’ loads now are of various types, with a full range of flexibility to be harnessed. Typical uncontrollable loads in households are such as microwaves and ovens, which are not capable of providing flexibility [

46]. Other loads such as lightings, TVs and computers are also not suitable for flexibility, as they are frequently used during the day and disrupting their usage might cause discomfort to customers. Cooling and heating appliances can be considered as curtailable and shiftable. For short periods, room temperatures may not be highly affected if an air conditioning unit (AC) is turned off; thus, rebound power may not be required. However, for longer periods, full rebound power may be required when the desired room temperature is in need to be restored [

50]. Similarly, the thermal storage property of refrigerating appliances, such as refrigerators and freezers, can provide direct flexible control, but they cannot be turned off for long periods of time since they are critical for the customers’ comfort [

51]. Shiftable loads, such as washing appliances, can be moved at any time during the day, but their rebound conditions must be met as they cannot be curtailed [

49].

3. Distribution-Level Flexibility Market

As any other commodity, demand flexibility needs a medium to facilitate its transaction between the providers and the buyers. Therefore, reaching the full potential of flexibility requires efficient and regulated flexibility markets. Previous studies have shown different approaches in implementing the framework of flexibility markets. In the two part study [

52,

53], a novel market pool mechanism was proposed, which enables flexible demand participation in current electricity markets. A Danish day-ahead market structure called FLExibility ClearingHouse (FLECH) is proposed in [

54]. This market works in parallel to the existing market structure and its objective is to manage the DSF bids offered by the aggregator to mitigate grid congestions. Similarly, a decentralized market-based instrument for flexibility management called De-Flex-Market is proposed in [

55,

56].

The aim of this paper is to provide a more detailed market framework than the conceptual work of the previous studies. This is achieved by clearly defining the flexibility market criteria and operation scheme, defining the roles of the market players involved, considering the rebound effect and its impact on the DSO’s decision, and addressing the imbalances that may arise from flexibility activations. The market proposed here is called the distribution-level flexibility market (Flex-DLM) and it is assumed to be running after the day-ahead market clearing. Usually, energy is scheduled in day-ahead markets based on the offers and bids provided by the generation and demand sides respectively. After the market clearing, system operators are able to detect possible grid contingencies, which can be solved by modifying the initial market solution. In a similar way, the Flex-DLM operates in a day-ahead timeframe and it is designed to participate in the congestion management process at the distribution level. After the day-ahead market clearing, the DSO can identify the upcoming network violations and consequently activates the flexibility call. In the Flex-DLM, the aggregator presents its aggregated flexibility bids and the flexibility market operator clears the market to solve the network constraints. The congestion management process is classified into two main categories:

Feeder overload management: Ensures that the network feeders do not reach its capacity limits, which can be caused by electricity demand growth.

Feeder voltage/var management: Ensures that voltage levels and reactive power at feeders are within acceptable limits. These limits can be violated due to high penetration of RES production as well as local variations of generation and demand.

The Flex-DLM criteria and operation scheme are explained in the forthcoming subsections.

3.1. Market Criteria

The criteria for classifying flexibility markets, as proposed in [

57], are those related to the temporal, spatial, contractual, and price-clearing dimensions of trading.

Table 2 presents the assumptions considered for these dimensions in the proposed Flex-DLM. The operation of Flex-DLM can be linked to the traffic light concept (TLC) introduced in [

58,

59].

According to the TLC, the need of flexibility can be divided into 3 phases associated to the traffic lights in which green refers to safe day-ahead operation, yellow refers to an expected network congestion in the day-ahead operation and red refers to a direct risk to the stability of the system and thus to the security of supply. Considering the TLC criteria, the Flex-DLM is operating at the yellow phase, where the DSO has detected possible contingencies in the day-ahead operation and flexibility is required to solve them. It can be expected that the solutions resulting from the Flex-DLM can change in real-time according to the actual generation and consumption. However, the real-time operation process and the emergency management fall out of the scope of this paper. For a proper consideration of security issues, a risk-based analysis should be made in the operational planning. It should be noted that while the Flex-DLM maybe simple in its format, it can be considered a mature and realistic scheme for what flexibility markets should be in the future. Moreover, it values the aggregator role in optimizing the usage of demand flexibility and it does not require complex regulatory changes.

3.2. Operation Scheme

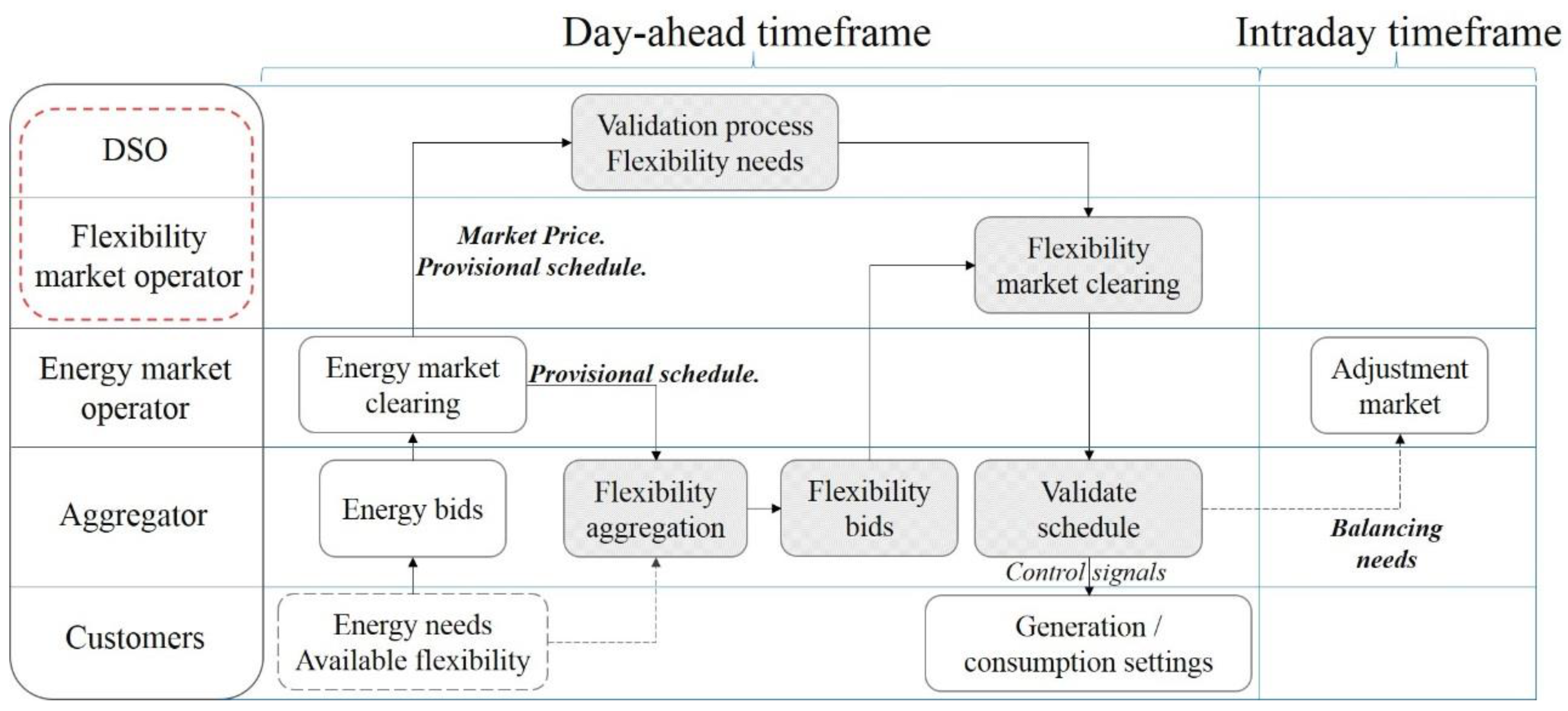

The general scheme for the proposed operations, as well as the actors and the time sequence for the day-ahead timeframe, is illustrated in

Figure 1. It should be noted that the paper only deals with the shaded blocks of that figure. The actors involved in such timeframe from bottom to top are: the customers; the aggregator, the energy market operator, who is responsible for clearing the wholesale day-ahead market; the flexibility market operator, who is responsible for clearing the Flex-DLM; and finally, the DSO, who is the operator of the distribution grid.

In the Flex-DLM framework, it is assumed that the aggregator is also the energy retailer and the BRP. As an energy retailer, the aggregator participates in the day-ahead market to purchase the required energy for its customers. Once the energy market operator clears the market, the provisional schedule is sent to the DSO for technical validation. Based on such schedule, the DSO can forecast forthcoming grid contingencies occurring on the following day of operation. Consequently, a flexibility call is activated, and all aggregators are notified. The role of clearing the Flex-DLM can be carried out by a separate market entity. However, here it is assumed that this role is carried out by the DSO in order to simplify the flexibility trading process. As a result, after all aggregators submit their flexibility bids, the DSO clears the Flex-DLM and then the aggregator receives the Flex-DLM solution. The market solution should consist of the accepted flexibility bids and the time when the rebound energy can take place, thus allowing the aggregator to adjust the flexible loads accordingly. The flexibility bids modeled here (whether UREG or DREG), offered at a particular node

for a trading period time

, consist of a number of

blocks of flexibility amounts

, with different prices

ordered in a non-decreasing manner, and the rebound conditions. The rebound conditions must define two main factors: the rebound hour and rebound power. The rebound hour can take place at any hour during the day, i.e., unrestricted, or it can be time restricted to a specific hour or interval. The rebound power can either be equal to or only a part of the flexibility activated.

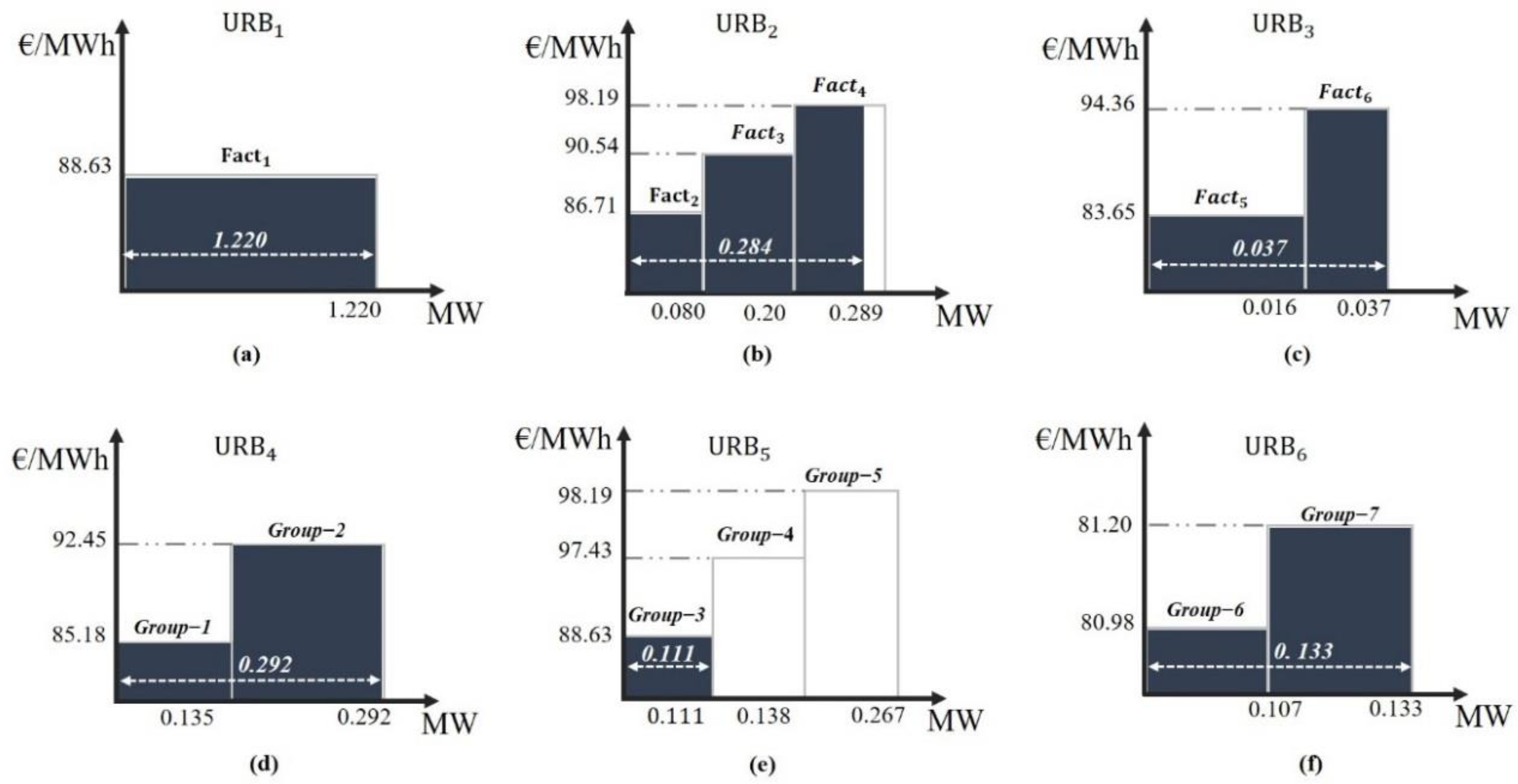

Table 3 illustrates an example for an aggregated DSF bid consisting of 3 blocks and the given possibilities of the rebound conditions. It must be remarked that the additional information required by the DSO to run this market is small compared to the amount of information the DSO is already managing.

At the moment, literature about flexibility pricing is limited. The work in [

44] provided a proposal for valuing demand elasticity. In this paper, demand flexibility trading is different from the normal electricity trading in wholesale markets. In order to comply with the Flex-DLM solution, aggregators must carry out further energy trading processes in forthcoming adjustment markets to balance the energy differences arising between the energy already bought by the aggregator in the day-ahead market and the adjusted new load profile after the Flex-DLM clearing. The aggregator will be also responsible for acquiring the rebound power (payback or rebate) for its customers. Therefore, as a BRP, the aggregator takes the responsibility of trading these differences in adjustment markets. In this arrangement, demand flexibility can be regarded as a trading of service and not a trading of energy, since it is the aggregator who trades the energy in future adjustment markets. This framework differs from other approaches, for instance for insular systems [

15], where the DSO directly commits the generation and makes use of the demand response to solve congestion and security problems. In the proposed Flex-DLM scheme, hence, the prices of flexibility services can be independent of the day-ahead market marginal prices. However, the flexibility prices can be affected by the level of competition between different aggregators in flexibility markets. Also, they can be limited by the maximum prices that the DSO will be willing to pay in order to avoid investing in network reinforcement. The operation scheme of the Flex-DLM limits the DSO role to clearing the Flex-DLM and choosing the optimal bids to balance its network. This is consistent with the current regulatory policies that do not allow the DSOs’ participation in energy trading.

Table 4 illustrates the trading by the DSO and the aggregator across the markets involved in the proposed scheme.

6. Conclusions

The objective of this paper is to propose a market for flexibility transactions that facilitates the trading between the DSO and the aggregators, who are bidding on behalf of their customers. The paper explains demand flexibility and classifies it into two types of flexibility namely up-regulation and down-regulation flexibility, which correspond to decreasing and increasing load volumes, respectively. Both can be valuable tools for the DSO when trying to mitigate network constraints at the distribution level. In addition, the rebound effect that is linked to both types of flexibility is defined and explained. The main stakeholders that are involved in the flexibility transactions are as well identified and their roles and responsibilities are shown. In order to ensure an effective trading for flexibility, a market for flexibility is proposed, which takes place in the day-ahead timeframe after the main wholesale market is cleared. The proposed market, named Flex-DLM, presents a simple but realistic scheme for what flexibility markets could be in the future. In addition, the Flex-DLM highlights the important role of the aggregator in maximizing the potential of demand flexibility and it does not involve the DSO in energy trading. Also, the Flex-DLM does not require complex regulatory changes which makes it easy to implement. Only the task of market clearing is assigned to the DSO, while balancing the differences between the market solutions before and after flexibility activations is assigned to the aggregator. Moreover, the proposed operation scheme of the Flex-DLM highlights the fact that demand flexibility trading should not be regarded as a trading of energy, but rather as a trading of a service.

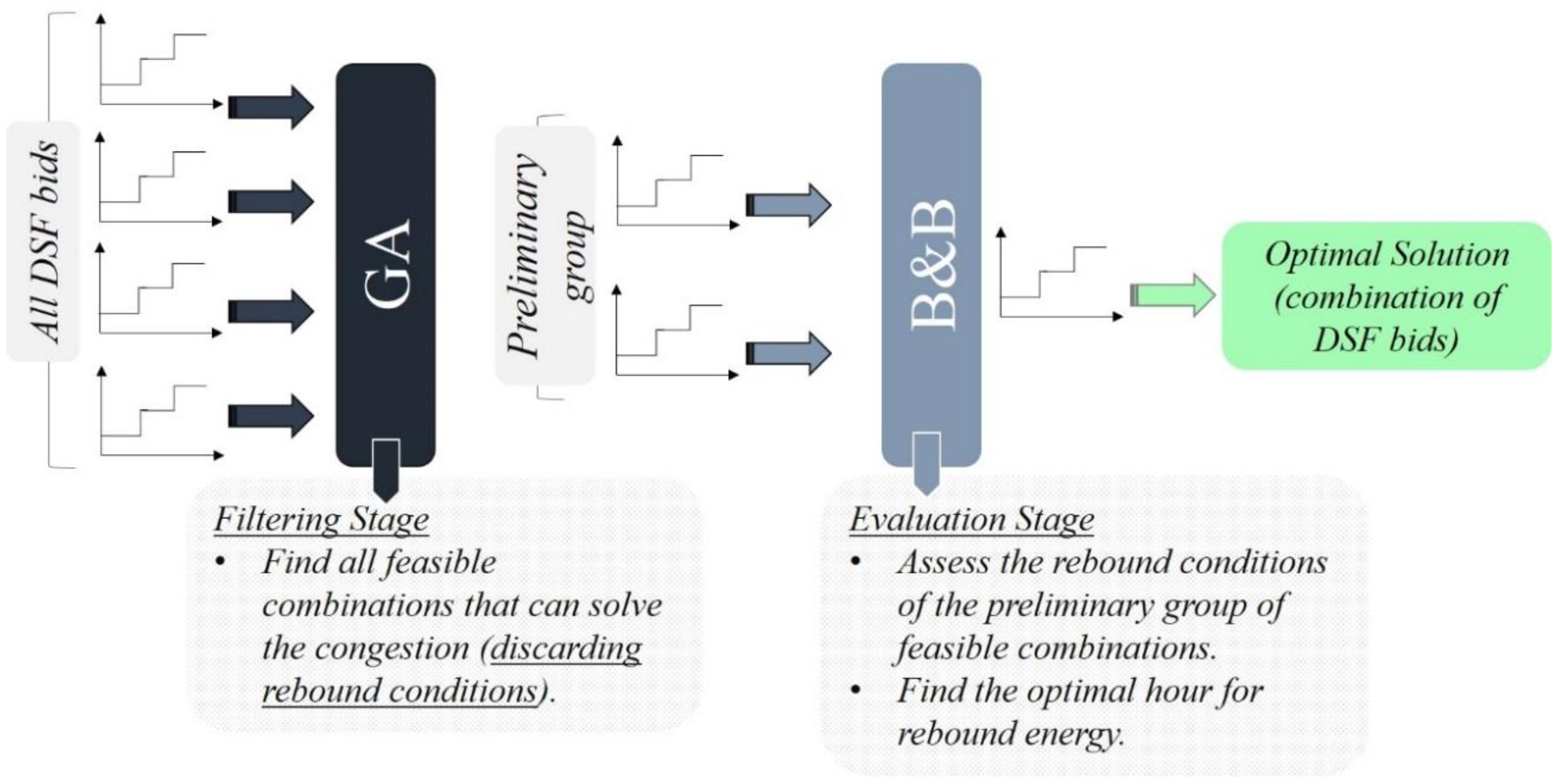

The DSO responsibility as the Flex-DLM operator involves optimizing its purchase for demand flexibility, while ensuring that the flexibility activated alleviates the network constraints expected to occur and that the rebound conditions do not cause further network congestion. Therefore, an optimization problem is formulated that models the total cost incurred by the DSO for activating flexibility. The added value of such optimization problem is that it considers two important factors which are frequently not considered in previous literature. These two factors are the modelling of the grid power flow constraints and the complex rebound effect. The problem can be complex to handle for large networks with hundreds of customers and complex rebound conditions. The optimization methodology proposed here uses a combination of genetic algorithms and branch and bound techniques to solve the problem. Also, the proposed approach has the advantage of scalability, where it can be implemented on larger networks and its computation time is not largely affected when the problem size increase. In addition, the approach does not require complex optimal power flow solver tools to be modeled, it can be integrated with ready-made tools and a limited amount of additional information and computation capacity are needed.

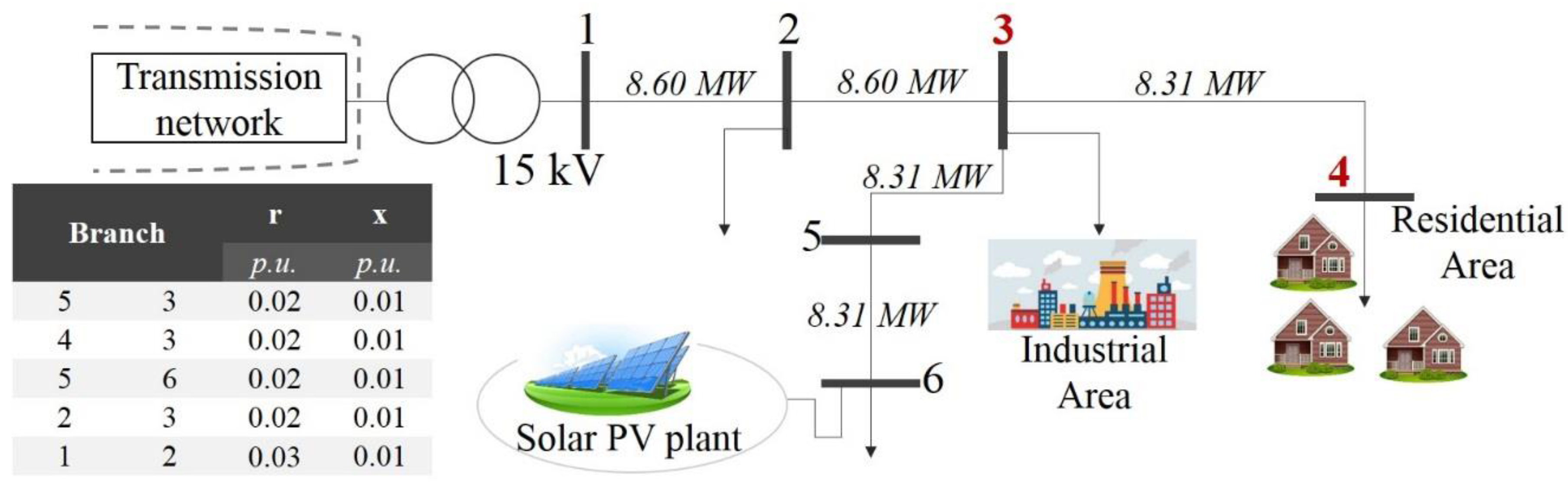

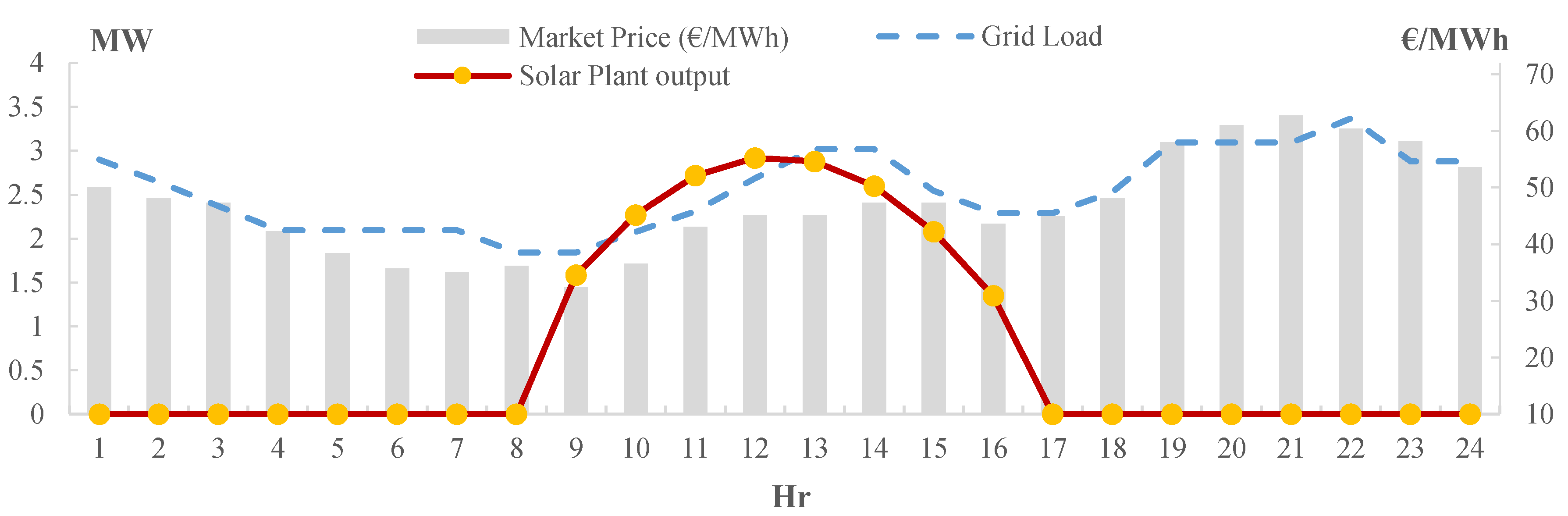

Two case studies were carried out using two real distribution network feeders in Spain in order to illustrate how the proposed methodology takes advantage of the two types of demand flexibility, UREG and DREG, in the congestion management process. In the first case study, the distribution network suffers from occasional overvoltages due to the high penetration of solar PV power plant. Since the renewables are given priority access for serving their energy in Spain, the optimal solution for the DSO will not be curtailing the solar PV energy, but rather installing voltage regulators that can be expensive. The solution proposed for such problem is activating down-regulation flexibility, where load increase volumes can be procured by the DSO to sustain the voltage levels in the permissible range. Even though this case study does not have a large network, the effect of the down-regulation flexibility can be achieved as the flexibility activated assisted the DSO in managing the voltage levels of its network. The second case study highlights the value of up-regulation flexibility for the DSO in managing feeders’ overloads. The large network presented has a forecasted consumption at the day-ahead operation that is overloading some of the lines. The up-regulation flexibility offered by the customers can assist the DSO in avoiding overload congestion in the network. While there are many feasible solutions for relieving this congestion, the rebound conditions imposed further congestions in the network for some of these solutions. Thus, the optimal solution can be activated by the DSO. The proposed optimization saves a considerable amount of time as opposed to using a conventional technique.

The flexibility market proposed in this paper operates in the day-ahead timeframe. However, the grid congestions forecasted at this time might not take place and the DSO could need a different amount of flexibility. The proper consideration of the uncertainties of the forecasting process would require probabilistic optimization algorithms and a proper risk management method. This is the subject of future research.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}