1. Introduction

In the Paris Agreement Switzerland has committed to reducing its greenhouse gas emissions by 50% in 2030 compared to 1990 levels, with the long-term goal of 70% to 85% in 2050 [

1]. The Swiss energy strategy prohibits the commissioning of new nuclear power plants, and it promotes renewable energy and efficiency [

2]. Much of the additional exploitable renewable potential comes from rooftop solar PV [

3], for which Switzerland implements support policies that encompass feed-in tariff and capital subsidy schemes [

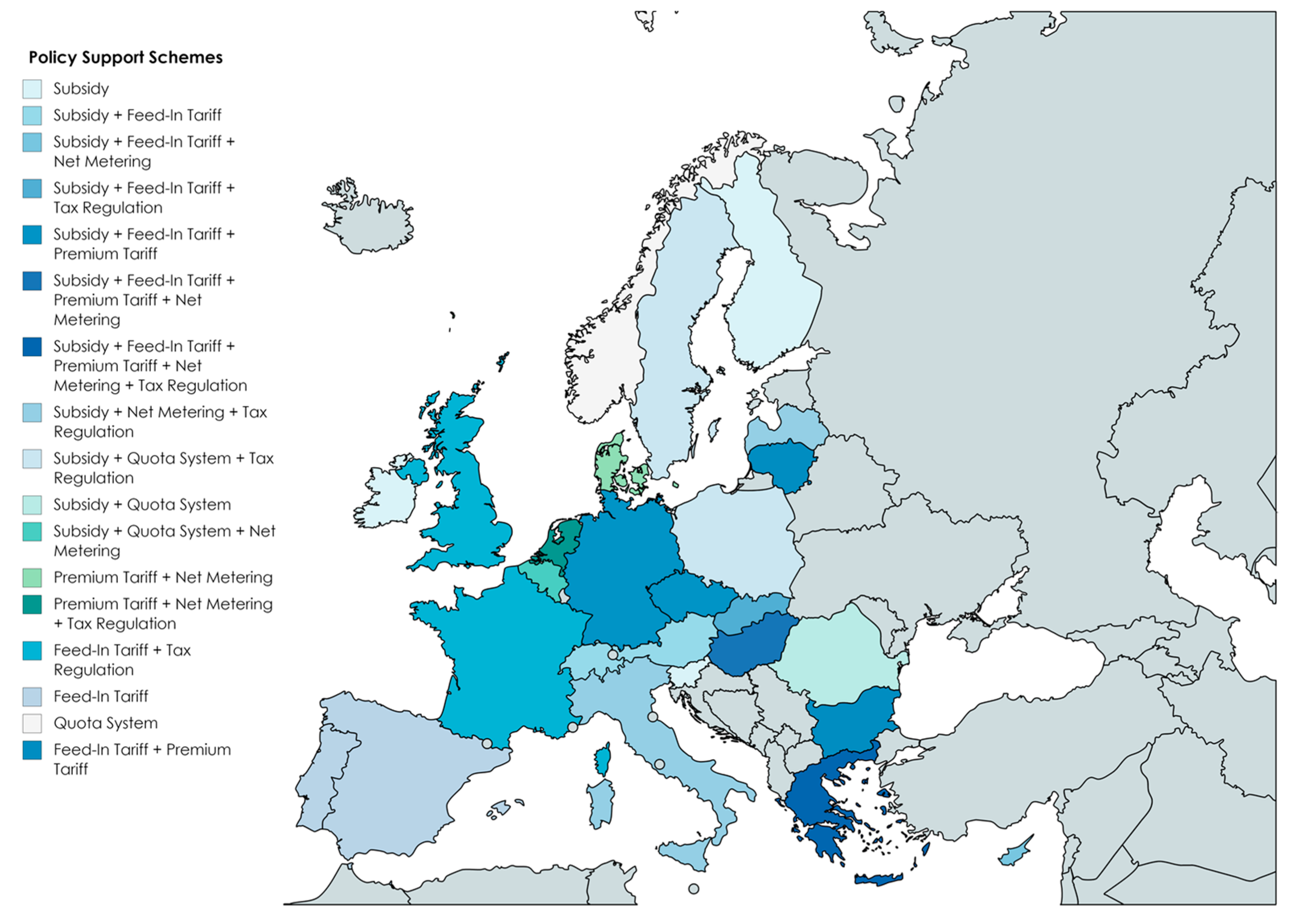

4]. In 2019, the solar PV installations of less than 100 kW were eligible only for the capital subsidy, while installations above 50 MW were eligible only for the feed-in tariff. Installations between 100 kW and 50 MW can choose between the two support schemes. The feed-in tariff was 10 Rp/kWh in 2018 (1 CHF = 100 Rp. = 0.88 EUR in 2018).The guaranteed period of the tariff payment for PV installations was 15 years. The calculation of the investment subsidy, in Swiss francs (CHF), was based on the formula 1400 + 340 x (kWp) for installations less than 30 kWp, and 1400 + 300 x (kWp) for installations larger than 30 kWp.

Similar support schemes are applied in other European countries as well, as shown in

Figure 1 (based on the Renewable Energy Policy Database—RESLegal [

5] for the year of 2017).

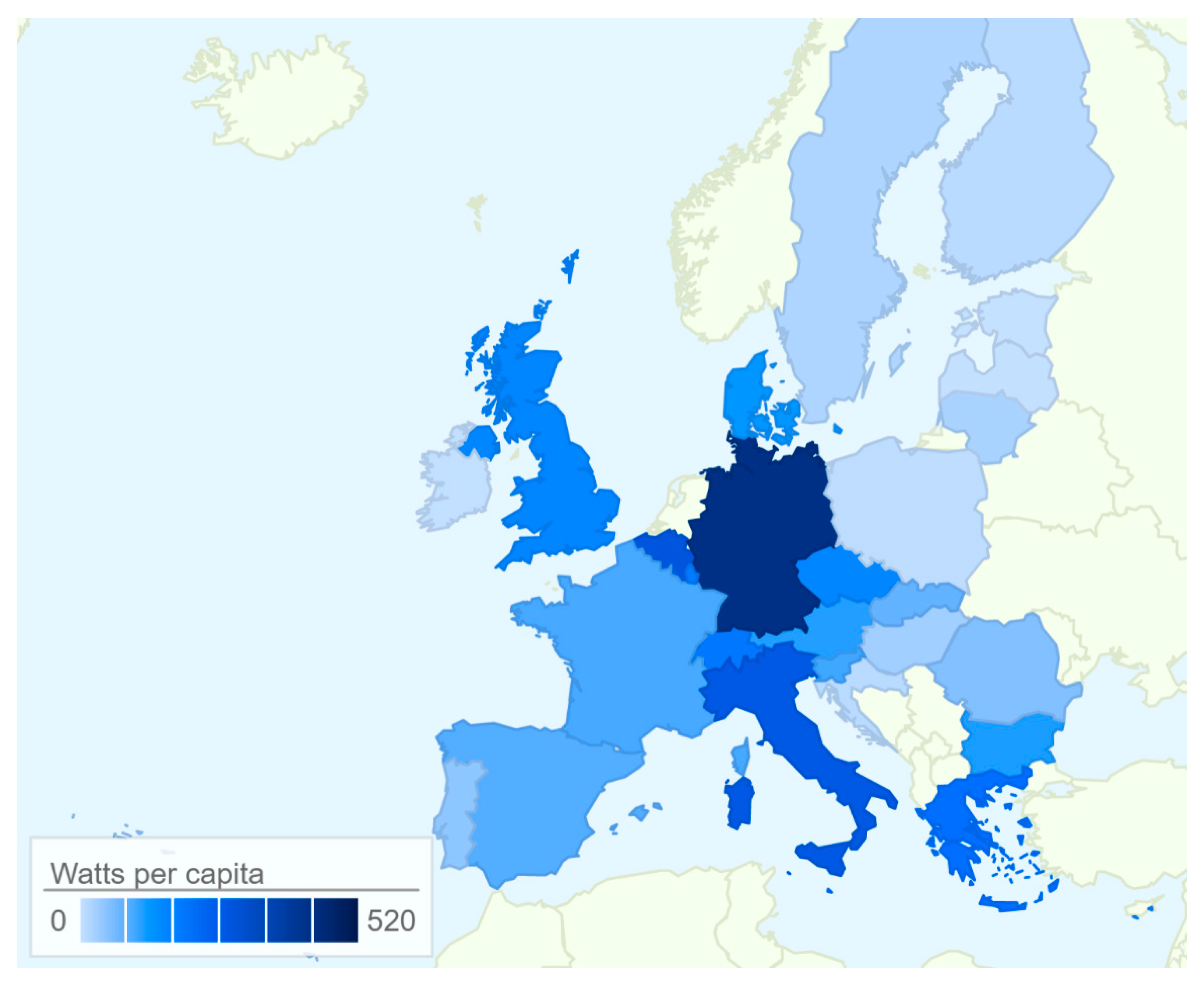

Regarding the diffusion of the solar PV systems (both rooftop and ground-mounted), Switzerland is slightly above than the EU average in terms of watts per capita (

Figure 2). In 2017, the total installed solar PV capacity in Switzerland was 1.9 GWp [

6], which translates to 0.23 kW per capita. For comparison, the EU average is 0.21 kW per capita in the same year. Among the European countries, Germany has the highest installed solar PV capacity per inhabitant (0.51 kW), followed by Italy (0.34 kWp), Belgium (0.33 kW) and Greece (0.25 kW) [

7].

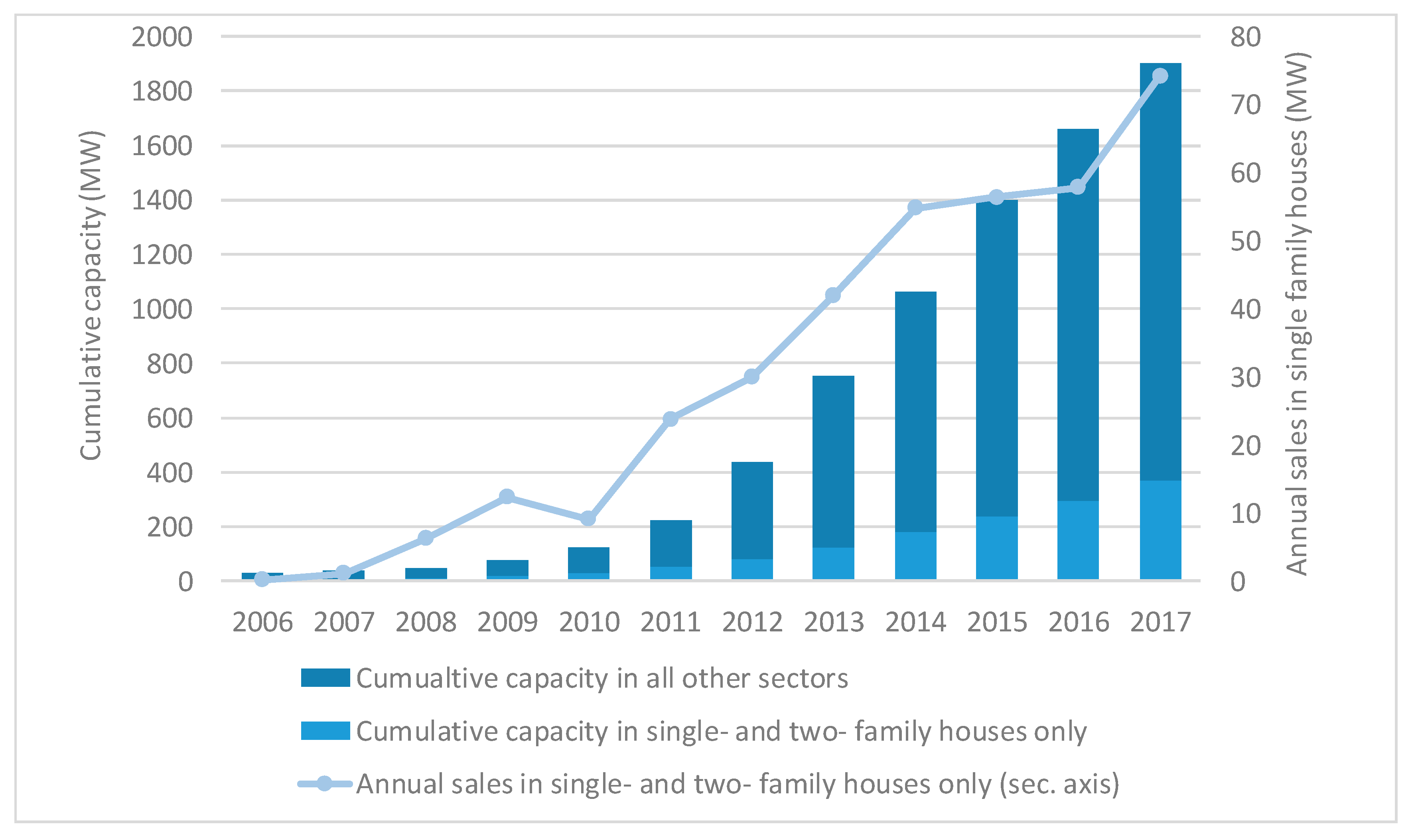

Accelerating the deployment of solar PV systems on residential buildings is claimed as an effective decarbonization strategy [

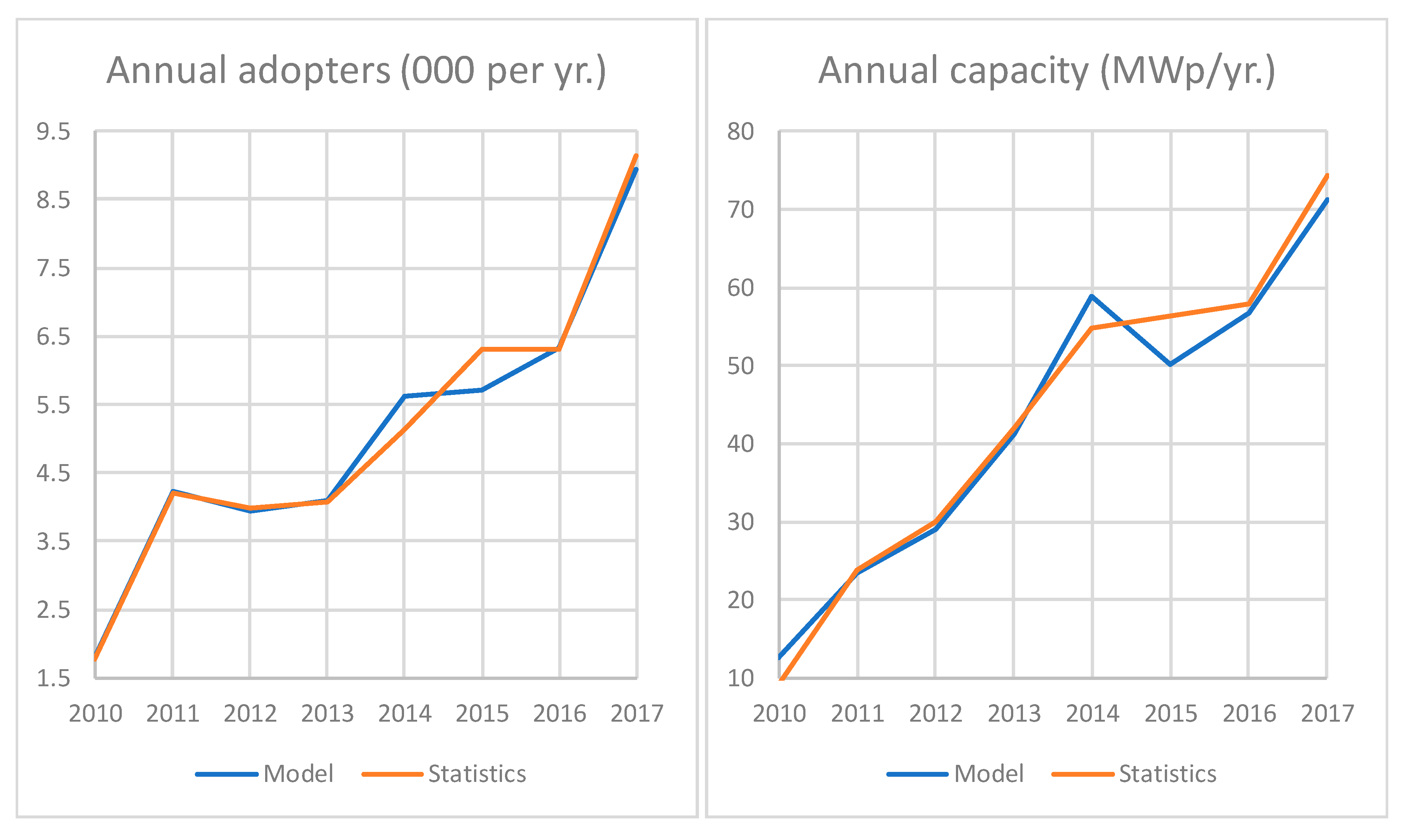

2]. However, the market of single- and two-family houses in Switzerland has shown a deceleration of the annual sales of solar PV systems between 2014 and 2016 (

Figure 3), mainly attributable to the revision of the policy. As there are low return rates for excess power injected to the grid, system owners dimension their PV systems as small as possible to optimize their consumption. Given that the single and two-family houses constitute more than two thirds of the residential building stock in Switzerland [

8], it is crucial to increase the adoption rate of solar PV technology in this sector to meet the climate change mitigation objectives (see for example [

9]). Hence, the importance of single- and two-family houses in achieving a low-carbon energy system and the dependence of this particular market segment on the level and type of policy support [

10], constitutes an interesting case study to examine and understand the dynamics of the adoption (i.e., investing) of the solar PV technology.

The decision to invest in a solar PV system depends on multiple factors. For example, different time preferences of money and risk stances of the (potential) investors in a solar PV system, which are captured via the weighted average cost of capital and discount rates, may render the investment financially unattractive [

11] and defer it. On the contrary, social influence (peer effects), the environmental sensitivity of the individuals, and their knowledge about the technology can positively influence the decision to invest [

12,

13,

14]. In [

14], a survey was conducted for Switzerland in a dataset of 408 homeowners, and it was found that also aesthetic aspects of solar panels play an important role in expanding the customer base. Moreover, the intensities of different support policies and technical progress play a significant role in investment decisions [

10]. While solar PV technology is a mature technology, there are still barriers to increasing its adoption rates. A range of studies, based on qualitative analysis and interviews with experts, have already assessed the most important of them. For example, in [

15] adopter-specific and institutional barriers are identified for Switzerland, such as high initial costs, high product complexity, low awareness and knowledge regarding the technology, as well as political risks that might arise due to unreliable policies. The same study also finds that social norms play an important role in explaining PV adoption decision and diffusion patterns, which is a finding similar to other studies for other world regions. For example in [

16] a survey in California also found that installers and neighbors play important, often supplementary, roles in the decision-making process, and have an influence on both the decision to adopt and the mode of adoption (e.g., purchase versus leasing). Installers and experts can help to lift the barriers related to adoption, via expert advice and provision of realistic information about costs and energy that can be produced, as shown in a survey from Finland [

17].

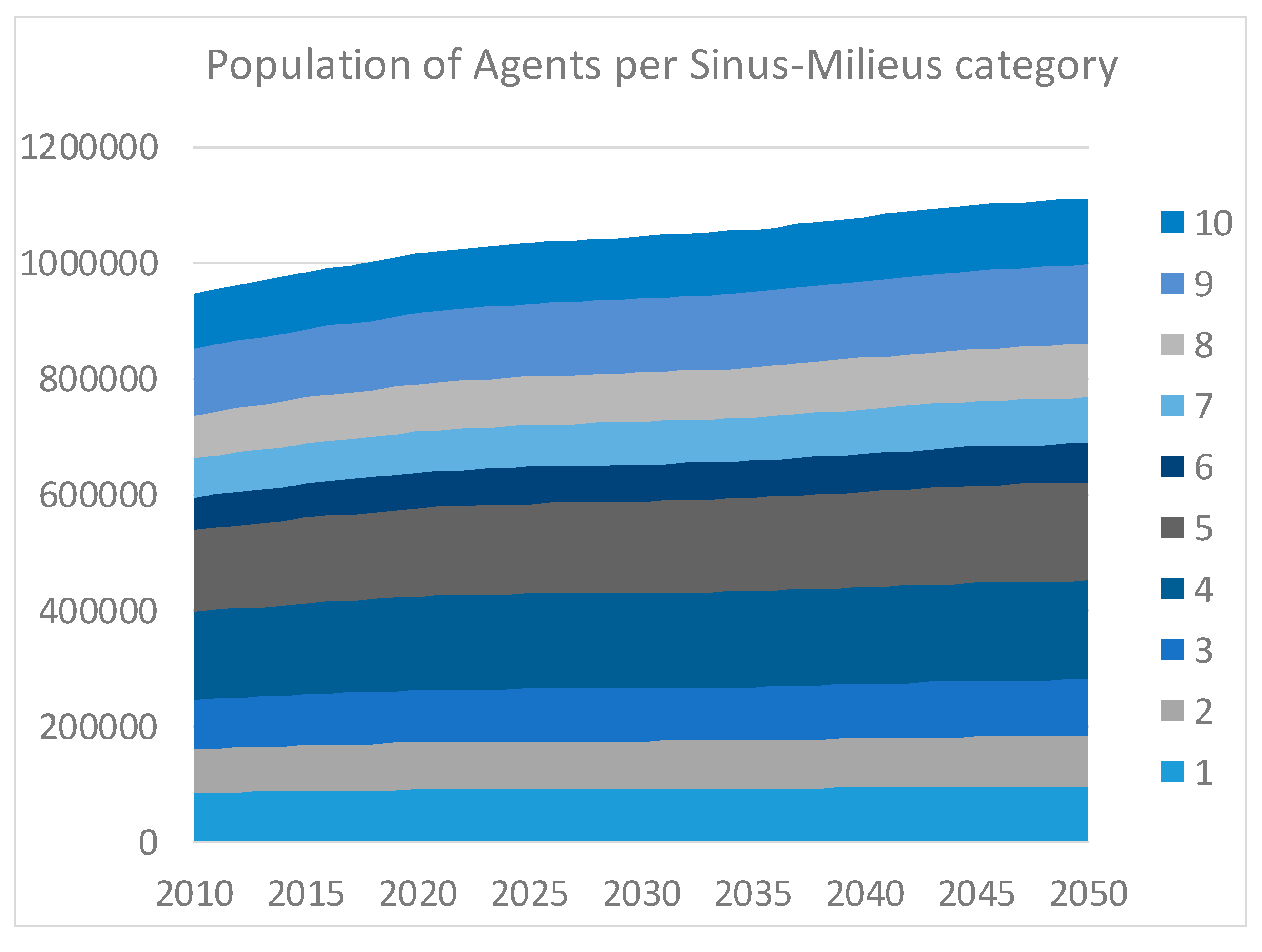

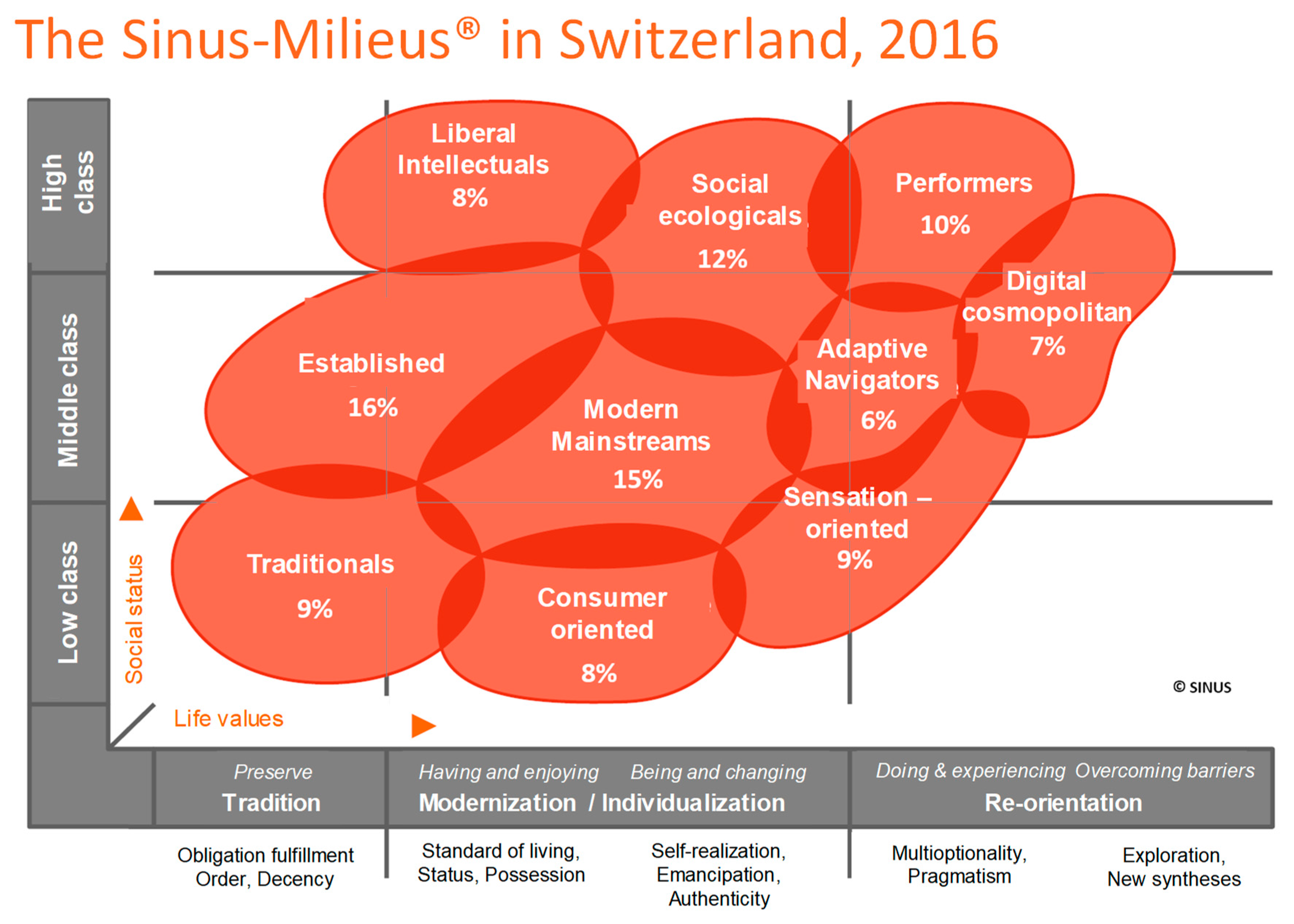

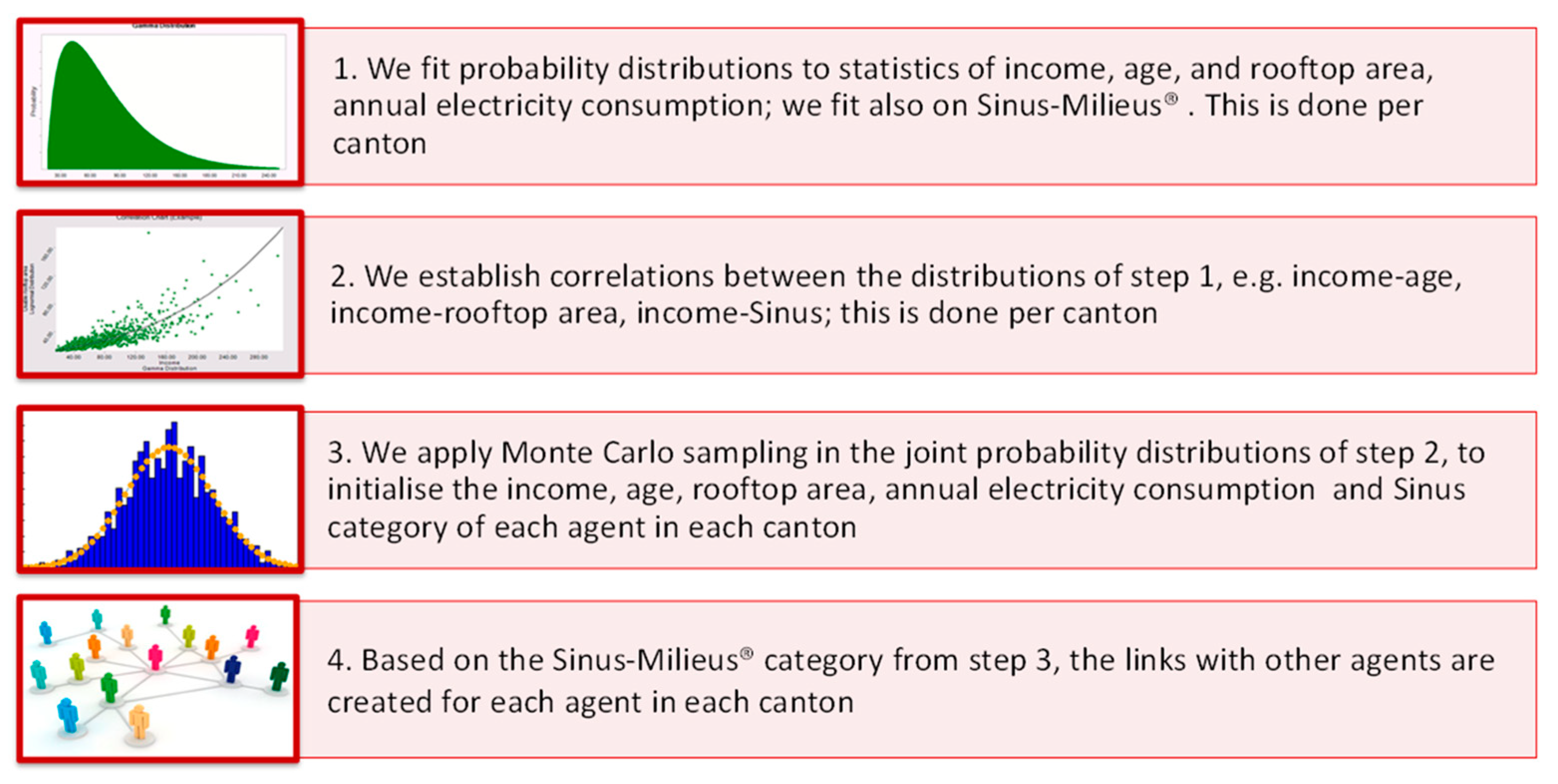

To quantify the key drivers and barriers affecting the diffusion of the rooftop solar PV systems in Switzerland, and especially their dynamics over the time, we apply an agent-based model (ABM) that simulates the decision process, the actions, and interactions of autonomous agents. An agent is a single- or two-family house in Switzerland, with main attributes its location (at a Cantonal level), income, average age, and education level of the adults in the house, social status, average annual electricity consumption, expected annual production from a solar PV system, and usable rooftop area. The decision mechanism is based on a utility function, which considers the financial attractiveness of the investment, the income of the agent, its environmental sensitivity, awareness, and knowledge about the solar PV technology, as well as social norms. Two social norms are modeled, the descriptive social norm (i.e., peer effects from e.g., seeing more solar PV installations in the neighborhood or influence from increased social links with adopters) and the injunctive social norm (i.e., the perception that the adoption of a PV system is the right thing to do for the environment) [

18]. While the peer effects are modeled through the social network component of the model, the injunctive social norm is approximated via a partial utility function. The model represents a synthetic population of more than one million agents, and it runs on an annual basis from 2009 to 2050, with the years 2009–2017 being treated as model calibration and validation datasets.

ABMs are widely used to simulate the inherent complexity of adoption and diffusion process of various energy technologies [

19]. For example, ABMs have been applied to assess the technology penetration of micro-generation in the Netherlands [

20], plug-in hybrids in the USA [

21] and China [

22], heat pumps in the UK [

23], energy-efficient technologies in households in various world regions [

24] and in the UK [

25], smart metering [

26], electric cars in Ireland [

27] in the USA [

28] and in Germany [

29]. The assessment of the adoption of residential solar PV systems with an ABM is examined in a few studies. For example, the impact of different governmental incentives in the USA is evaluated by using a weighted utility function to model the investment decision of the agents [

30]. In [

31], a model based on behavioral rules and the theory of planned behavior [

32] is applied to assess the penetration of solar PV at the city of Austin in Texas. In [

33], a data-driven ABM is implemented to evaluate the diffusion of solar PV in California. In [

34], geospatial information is taken into account to forecast the adoption of solar PV systems in California, but the study does not develop an ABM system. Also, for California, ABMs employing GIS [

35] and social behavior [

36,

37] methodologies have been applied as well. In [

38], an ABM with the geographic information system and logistic regression has been developed to simulate the adoption of the rooftop solar PV system in a district of Gangnam in South Korea. In [

39], an ABM based on logistic regressions with explanatory variables the payback period, eco-friendliness, budget, and peer effects is developed to assess the diffusion of solar PV in Germany. Another study looked at the penetration of solar PV systems in single-family houses in Italy, using a weighted utility function to model the decision based on income, economic and environmental benefits, and communication as partial utilities [

40]. In [

41] an ABM is proposed which uses self-reported data and then it is empirically tuned using historical data, in order to study the adoption of solar PV panels in private households in the Emilia-Romagna region in Italy. In [

42] an ABM is employed to study and contrast the adoption of solar PV and battery systems (combined) in both Ontario, Canada, and Bavaria, Germany, using weighted utility function that includes budget, payback period, environmental sensitivity, social influence, and emotional impressions of PV systems. In [

43] an ABM is described to explore the impact of installers of PV panels on the adoption rate of PV technology in the residential sector, focusing on the maximization of the installers’ profit (while buyers only evaluate the financial viability of their investment before adopting the technology).

We apply the methodology presented in [

30,

40], based on the concept of maximizing a weighted sum of partial utilities representing different decision factors, which we extend in the present study by including: a) dynamic growth of the agents’ population over time; b) changes of key agents’ attributes over time, such as income, age, and electricity consumption; c) optimization models for each agent to decide the support scheme (capital subsidy or feed-in tariff) when applicable; d) a large number of agents based on synthetic populations using Monte Carlo sampling. In our framework, we capture the most influential factors affecting the decision to invest, as these have been identified in the literature. We include economic drivers, budgeting constraints and access to capital, descriptive and injunctive social norms, climate conditions, technology performance, policy schemes and market configurations. We compensate the lack of using surveys and geographical systems with the large sample of agents we include in our analysis and the statistical equivalence of our synthetic population to the actual (and unobserved) population of agents. Thus, the novelty in our approach is that we include the major influencing drivers regarding the decision to adopt a PV in a flexible framework that only requires access to open data published by administrative registers, without the need for conducting a census for a large share of the population. To the best of our knowledge, the ABM applied in this study is the first of its kind that quantitatively assesses the diffusion of solar PV systems in single- and two-family houses in Switzerland. The model can also be extended to include additional solar PV markets, e.g., multi-family houses.

The next section presents the description of the model and its calibration and validation procedures.

Section 3 presents results from different scenarios and sensitivity analyses regarding policy support schemes, technology performance, electricity prices, and discount rates. We conclude with policy implications of our analysis and suggestions for extending the current work.

3. Results

3.1. Reference Scenario

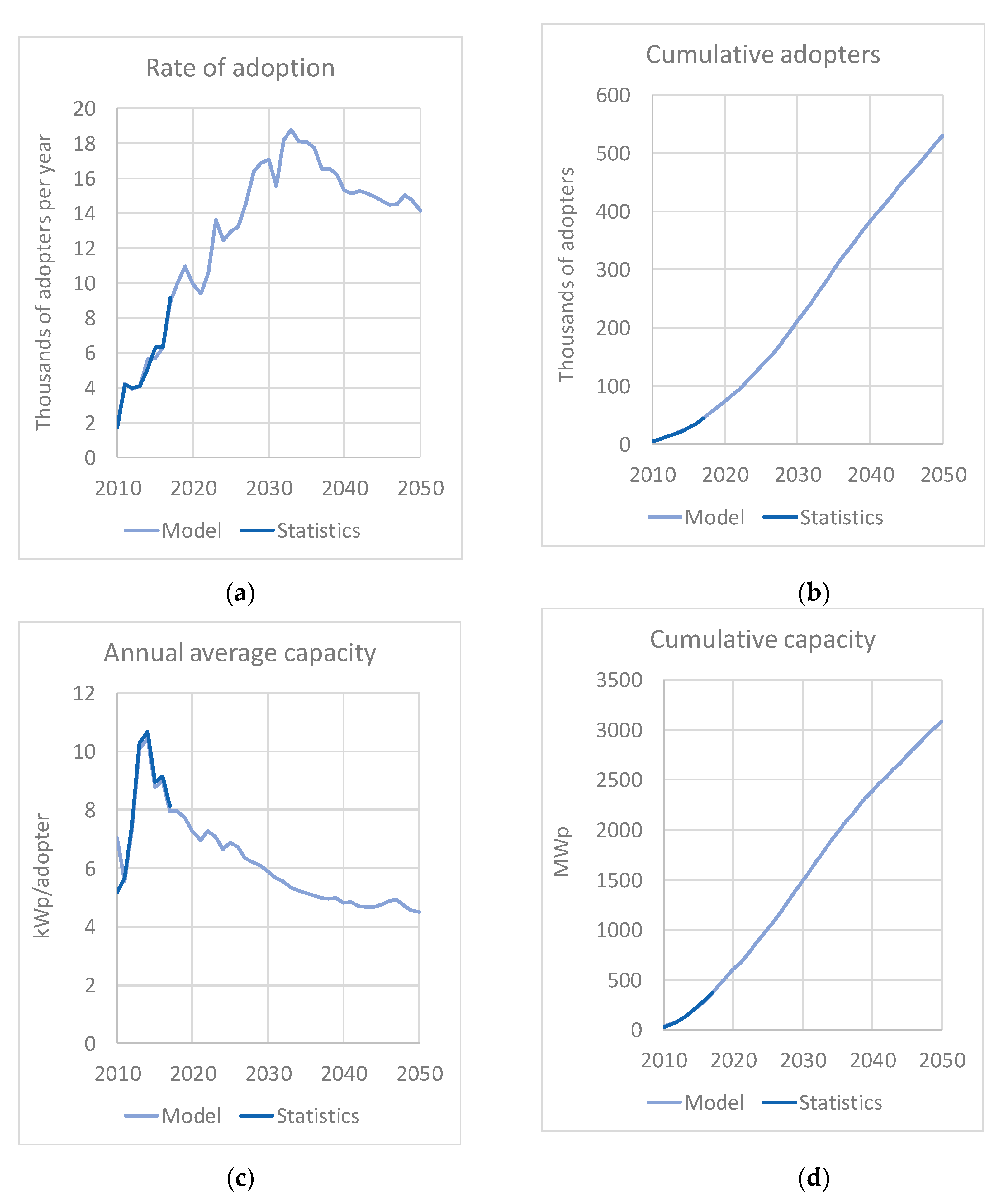

The annual rate of adoption, the cumulative number of adopters and the cumulative installed capacity in the Reference scenario is presented in

Figure 6. In 2050, the total installed capacity is 3083 MWp, from 369 MWp in 2017. The number of installations increases from about 44,000 in 2017 to more than 530,000 in 2050 (

Figure 6b,d). However, the average installed capacity per installation declines over time: from 8 kWp in 2017 to 4.5 kWp in 2050 (

Figure 6c).

There are three main reasons for the reduction in the average installed capacity in the future. The first reason is the assumed market configuration: any excess electricity that an adopter produces from the installed solar PV system can be sold at the average production cost of a nearby utility, after the phase-out of the feed-in tariff. The average cost is significantly lower than the electricity price paid by the end consumer [

81]. As a result, large installations aiming at selling excess electricity are financially less attractive than smaller installations targeting the optimization of the self-consumption. The difference between the end consumer’s electricity price and the selling price of the excess electricity from solar PV broadly defines the operating strategy of the prosumer after the phase-out of the support policies (i.e., focus on self-consumption or focus on selling electricity). The second reason for the smaller, on average, installed capacity in the future is the reduction of the average annual electricity consumption of the households by 2050. The efficiency measures implemented in the Reference scenario render larger systems not cost-effective when the prosumers’ strategy focuses on self-consumption. Finally, the third reason for the reduction in the average installed capacity are budgeting constraints and shifts between consumer classes. These shifts occur as the diffusion process evolves and the pool of high-income classes (innovators, early adopters) is being depleted, while the middle-class (early majority) is starting to adopt the technology (see also

Figure 7).

While in the Reference scenario, there is a deceleration in the growth of the cumulative installed solar PV capacity in single- and two-family houses in Switzerland (

Figure 6d), there are no signs of saturation. The deceleration is the result of both the reduction of the average installation size and the reduction of the adoption rates after the mid of the 2030 s. As shown in

Figure 6a, the rate of adoption increases until 2030, driven by the innovators (Sinus-Milieus

® category 10) and the early adopters (Sinus-Milieus

® categories 8 and 9). Main characteristics of the innovators are their willingness to take risks, their financial liquidity, and their high social status. Early adopters also have high social status and financial liquidity, but they are more discrete in adoption choices than the innovators. Finally, the early majority (Sinus-Milieus

® categories 5 to 7) adopts innovations after a varying degree of time, which is longer than the innovators and early adopters. The behavior of the model regarding the participation of the different socioeconomic classes in the solar PV diffusion process is consistent with the literature (see for example [

49]).

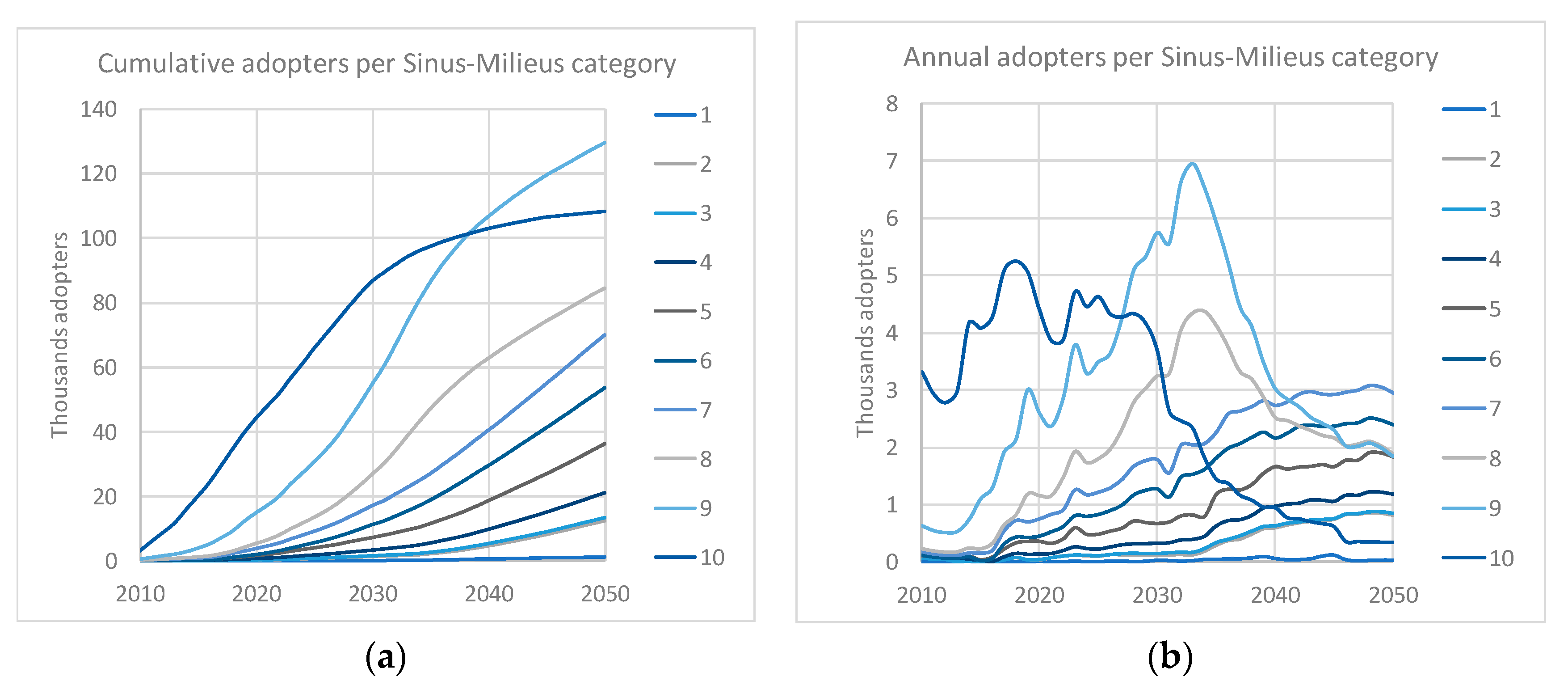

In 2017, innovators installed about 70% of the total solar PV systems in single- and two-family houses (model result from the calibration and validation process). By 2030, the share of adopters belonging to innovators is already 82%, and it further increases to 95% in 2050 (

Figure 7). However, in 2050 the adopters belonging to innovators account for only 20% of the total adopters. This is because, after 2030, the socioeconomic classes belonging to early adopters and the early majority take the driving seat in the diffusion process, as the pool of innovators that are not adopters is being depleted. In 2050, about 94% of the agents in early adopters’ classes install a solar PV system (from only 38% in 2030). At the same time, about 50% of the agents in early majority classes become adopters (from only 12% in 2030). In total, by 2050, 40% of the total adopters are from the early adopters’ classes and another 30% from the early majority. The rest 10% is from the late majority classes. It can be expected that beyond 2050, the early majority classes will continue to drive the diffusion process of the solar PV systems, while the late majority classes will emerge by when the profitability of the investment improves further, and the social network effects increase.

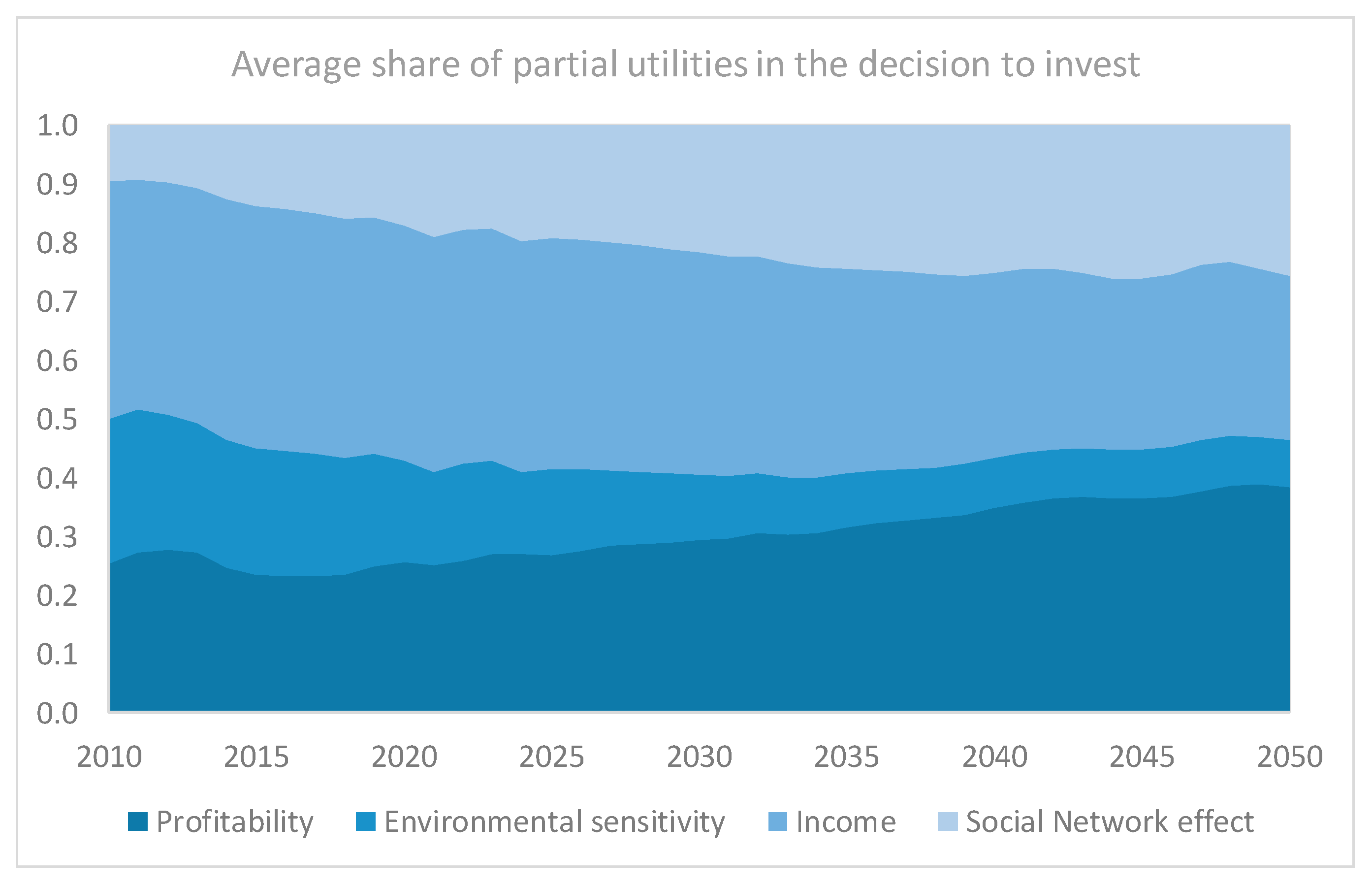

Figure 8 presents the share of each partial utility in the total utility of agents that have installed a solar PV system, which is a key component of the innovation-decision mechanism of the model. In the near-term period until 2030, the decision to invest in solar PV technology is mostly influenced by the level of agent’s income and the profitability of the investment. In this regard, the financial support schemes, implemented by the government, play an important role. The environmental sensitivity and level of knowledge and awareness about the PV technology also have a significant weight in the adoption decision in the near-term period, driven by the ecological values of the innovators and early adopters.

As an increasing number of agents belonging to innovators and early adopters’ classes install a solar PV system over time, the weight of the income utility in the decision is gradually reduced. This is because lower income classes are starting to become adopters too, and the improvement in the production costs of solar PV system mitigates the barriers related to limited budgets. The weight of the environmental sensitivity lessens over time, because of the continuous decline in the average installed capacity per adopter. Following the alternative interpretation of the environmental utility as the level of awareness and knowledge about the solar PV technology, when more agents become familiar with the technology and adopt it then a point is reached beyond which the impact of the increased technology awareness and knowledge of the investment decision lessens over time. By when the lower income classes are starting to become adopters, the profitability of the investment and financial liquidity are important investment criteria. The influence from the social network is constantly increasing during the projection horizon, as an increasing number of links with adopters is established. The peer effects become of equal importance with the income in the investment decision by 2050. However, there is a slowdown in the increase of the weight of the social network in the decision to invest, due to the reduction in the adoption rate.

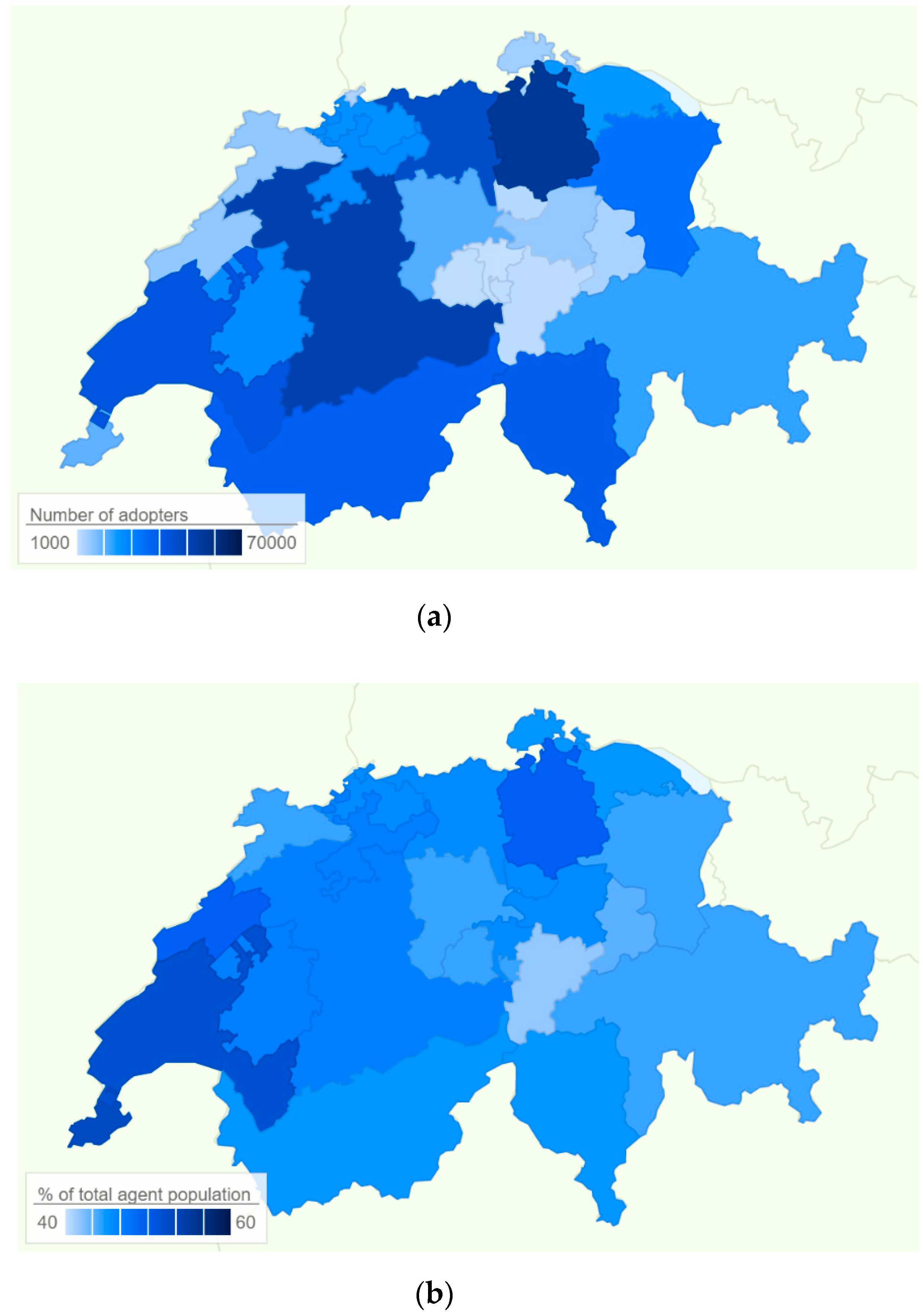

Figure 9 presents the geographical distribution of adopters per Swiss Canton, both as absolute values and as a share of the total population of the agents in 2050. Adoption rates of more than half of the total population of agents are achieved in the Cantons of Zürich, Neuchâtel, Vaud, and Genève. These high rates are attributable to the high average irradiation levels and high average incomes.

On the other hand, adoption rates of less than 45% occur in the Cantons of Appenzell, Uri, Glarus, Sankt Gallen, and the Cantons of Unterwalden. The lower rates in these Cantons are mostly attributable to the lower irradiation levels and, to a lesser degree, to lower average incomes. In the rest of the Cantons, about 45% to 48% of the single- and two-family houses have installed a rooftop solar PV system by 2050.

The Cantons of Zürich, Bern, Aargau account for one third of the total adopters in Switzerland in 2050 (about 11% each, on average). In contrast, the three Cantons with the highest adoption rates, Vaud, Neuchâtel, and Genève, account together for only 13% of the total adopters in 2050, since the number of single- and two-family houses in these Cantons is much lower than in Zürich, Bern, and Aargau. It can be argued that the southern Cantons benefit from higher solar irradiation levels that partly compensate for the lower number of single- and two-family houses compared to the northern Cantons. Hence, Ticino, Vaud, Wallis and Genève (i.e., south- and south-west Switzerland) have together 27% of the total adopters in 2050. Eastern Switzerland (Sankt Gallen, Thurgau, Appenzell, Glarus, Schaffhausen and Graubünden) accounts for 17% in the total number of adopters in 2050. Central Switzerland (Uri, Schwyz, Obwalden, Nidwalden, Lucerne and Zug) contributes only by 6% in the total number of adopters, mainly due to the lower solar irradiation levels compared to the other regions. The share of north-western Switzerland (Basel-Stadt, Basel-Land, and Aargau) in total adopters is 15% in 2050. The region of Espace Mittelland (Bern, Solothurn, Fribourg, Neuchâtel and Jura) contributes with another 24% in total adopters in 2050. Zürich alone accounts for the rest 12% of the adopters.

The results obtained in the Reference scenario are benchmarked against two studies regarding the future development of solar PV in Switzerland. The first study is the short-term outlook of the solar PV market in Europe from solar power [

82]. The outlook for Switzerland estimates a total capacity between 2.8 GWp and 4.1 GWp by 2021. The application of today’s share of single- and two-family houses in the total market (which is about 19%) to the total capacity estimated from solar power for Switzerland results in installed capacity between 480 and 700 MWp. This figure is in-line with the estimation of 741 MWp in the Reference scenario in 2021. The second benchmarking study is the NEP scenario from the Swiss energy strategy [

44], which implements the objectives of the Swiss energy and climate policy. In the NEP scenario, about 15 GWp of solar PV power are installed by the end of 2050, which implies that the share of the installed capacity in single- and two-family houses in the Reference scenario accounts for 20% of the total installed capacity projected in the NEP scenario (which is slightly higher than the today’s share of 19%).

3.2. Variants

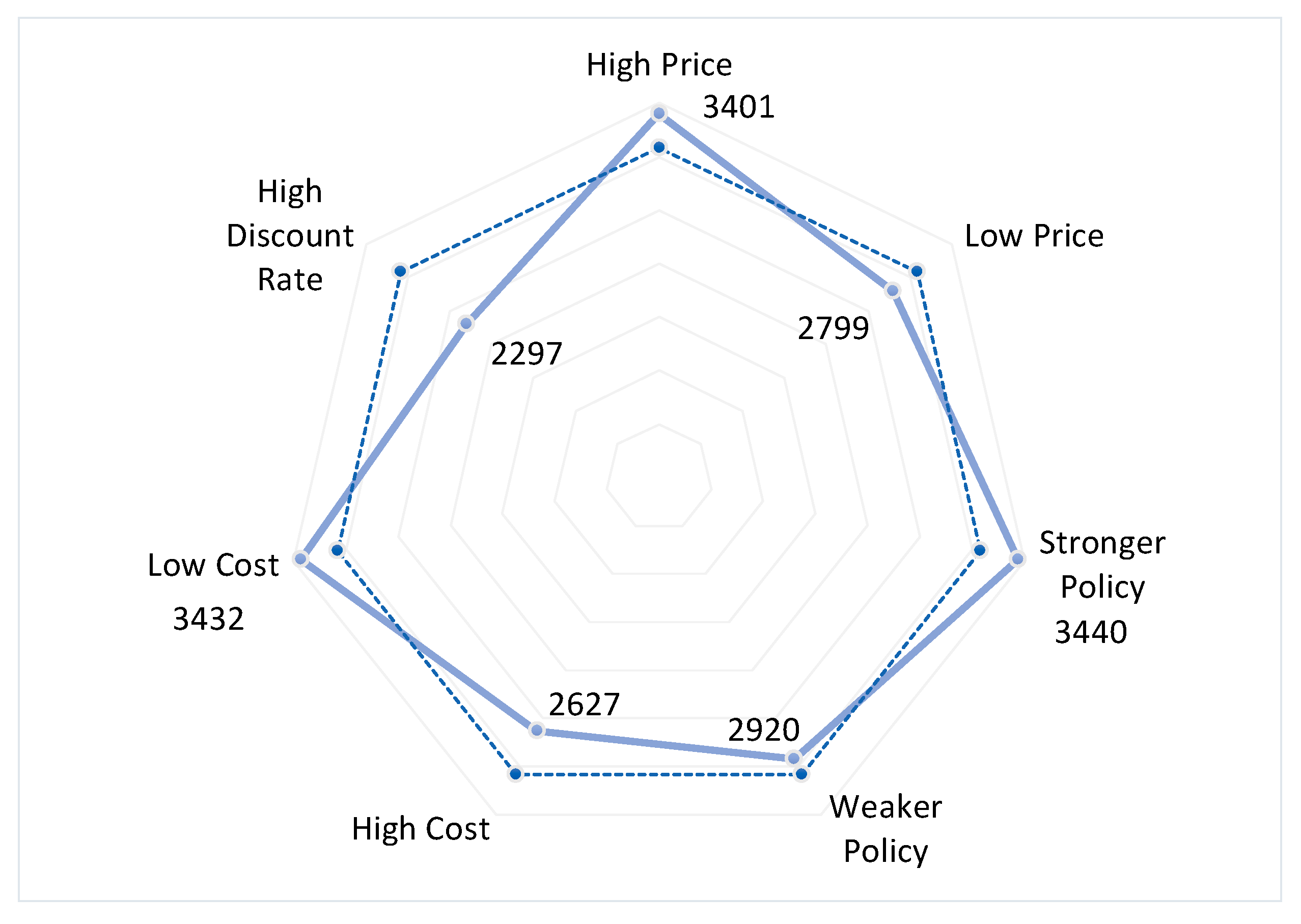

Figure 10 presents a comparison of all variants, and with the Reference scenario, regarding the total installed solar PV capacity in single- and two-family houses in 2050. In the Weaker Policy variant, the diffusion process delays about 3 to 4 years compared to the Reference scenario. The number of adopters in the Weaker Policy in 2050 is already achieved by 2046/7 in the Reference scenario. In total, there are about 505,000 houses with a solar PV system in 2050 (−5% than in Reference). The cumulative installed capacity amounts to 2.9 GWp in the same year, also 5% less compared to the Reference scenario. It can be therefore argued that the government support schemes are necessary to stimulate a particular segment of agents from the early majority classes (which are about 25,000 single- and two-family houses), to become adopters.

In the Stronger Policy variant, the diffusion process accelerates about 4 years compared to the Reference scenario. The number of adopters is about 26,000 higher than in Reference in 2050 (or +5%) and reaches 556,000. The cumulative capacity is 3.5 GWp in 2050 or +12% from the Reference scenario, implying that the average installation size per adopter is also higher in Stronger Policy than in Reference. From the analysis of the Weaker and Stronger Policy variants, it can be concluded that about 51,000 agents from the early majority classes are sensitive to the financial incentives provided by the government. However, this number is only 10% of the total number of adopters in the Reference scenario, which implies that the diffusion of the solar PV technology in single- and two-family houses has already gained momentum.

In the High Cost variant, the diffusion process delays about 5 years compared to the Reference scenario. The total number of adopters is about 470,000 in 2050 (–11% from Reference). The cumulative installed capacity is about 2.6 GWp (–15% from Reference). Hence, the average installation size per adopter also declines, compared to Reference, due to the higher upfront investment costs. To bring the diffusion of solar PV systems to the level of the Reference scenario, increased support schemes are required in this variant.

In the Low Cost variant, the total number of adopters reaches 557,000 in 2050 (or +5% from the Reference scenario). The cumulative installed capacity is 3.4 GWp in the same year (+10% from the Reference scenario). This result also implies that the average installation size per adopter is higher in this variant than in the Reference scenario due to the favorable economics of the investment. From the analysis of both the High and Low Costs variants, it can be concluded that the financial incentives provided by the government need to be constantly adjusted for the learning rate of the technology and they constitute an administrable and tractable option to accelerate the penetration of the solar PV system.

In the High Price variant, the increase in the electricity price has a backwards-shifting impact on the adoption. The higher electricity prices act retroactively, and the diffusion process accelerates by about 5 to 6 years compared to the Reference scenario. The number of adopters is 585,000 in 2050 (+10% from the Reference scenario), and the cumulative installed capacity amounts to 3.4 GWp (+10% form the Reference scenario). Higher electricity prices enable increased rates of self-consumption, and the installed systems are mostly dimensioned to fit the household’s electricity needs, which in turn translates to a (slightly) lower average installation size per adopter compared to Reference.

In contrast, the Low Price variant displays a slowdown in the diffusion process compared to the Reference scenario. The total number of adopters is about 502,000 in 2050, and the cumulative installed capacity is 2.9 GWp. The average installation size is only slightly higher than in the Reference scenario, which can be associated with slightly lower rates of self-consumption. From the analysis of both the High and Low Prices variants, it can be concluded that the level of electricity price is an important enabler for the penetration of solar PV in single- and two-family houses, while the adopters mainly follow self-consumption strategies (i.e., naïve prosumers). However, this depends on the configuration of the market and the ability of smaller market players to participate in the electricity trading schemes.

Finally, the cost and access to capital, risk, and time preferences are important factors for the timing of the investment. In the High DRate variant, the decision to invest is postponed by almost 10 years compared to the Reference scenario. In addition, the average size of investment per adopter is smaller because higher discount rates do not favor capital-intensive projects. As a result, the total number of adopters is about 417,000 in 2050 (−22% from Reference), and the cumulative installed capacity reaches 2.3 GWp (−25% from Reference).

4. Discussion

A key pillar of the Swiss Energy Strategy is the increase of non-hydro-based renewable generation by 2050. Solar PV systems are envisaged to expand further, but currently, it is unclear if this expansion will have the same pace in all market segments. In this study, we have developed and applied an ABM to understand the dynamics of the diffusion process of the rooftop solar PV systems in the market of single- and two-family houses. We have selected this particular market segment because of three main reasons: 1) it has been quite sensitive to financial incentives provided by the government, 2) it has experienced a slowdown in its growth in the recent past, and 3) it counts for more than two thirds of the total residential building stock in Switzerland.

We apply the model in a Reference scenario, which reflects the objectives of the Swiss energy and climate policy, in-line with the implementation of the country’s commitments to the Paris Agreement. We find that in the market of single- and two-family houses the installed systems can be smaller in the future than in the past if: a) there are low rates of return from selling excess power to the grid; b) the focus of investors are on self-consumption strategies; and c) strong efficiency measures are implemented that reduce the overall electricity consumption.

We also find that by 2050, more than 50% of the modeled agents install a solar PV system, and the cumulative installed capacity increases to 3083 MW from 369 MW in 2017. Enabling factors in the decision to invest are the continuous technology learning that improves the economic performance of the investment, the higher electricity prices, the time and risk preferences of the investors, as well as peer effects from the social network and injunctive social norms.

The profitability of the investment, a major factor in the investment decision, is influenced by both the technology learning and financial incentives provided by the government. The policy support schemes need to be adjusted continuously to better reflect the economic performance of the technology on the one side and to attract investors from socioeconomic classes with limited financial liquidity on the other side. With the phase-out of the feed-in tariff and capital subsidies, other financial instruments need to be developed to overcome financial barriers from the investors. Schemes such as leasing and crowdfunding are already in place in some countries (e.g., Germany), and complement traditional financial instruments such as equity, debt financing, and energy cooperatives. Leasing is used in business models based on self-consumption (from a legislature’s perspective, when the plant operator and consumer are the same entity). In leasing, the building owner (or tenant) does not have the capital or willingness to invest in a solar PV system, and the investment is made through a utility or company. It can also be the case that the building owner invests in a solar PV system, and then the system is leased to the tenant. Crowd investing is equity-based crowdfunding where the investors become shareholders, i.e., they receive shares in return. This mechanism mainly covers the financing gap of projects, which have difficulties in getting bank credit. It is suitable for the business models considering Power Purchase Agreements and self-consumption (in fact, it is more profitable for self-consumption due to the reduced payment of the surcharge).

Innovators drive the diffusion process until 2030/5, and the diffusion curve has an inflexion point by when most of the innovators have become adopters. At this point, peer effects and the improvement in the economic performance of technology are the key enablers for attracting more agents from the other socioeconomic classes. Although interpersonal communication is an important influencing factor, it comes to saturation by when links with new adopters are being established at continuously low rates. Mass media communication and campaigns can perhaps continue attracting more agents in this case.

The rate of adoption by 2050 exceeds 90% for the agents belonging to innovators, early adopters, and early majority classes. Agents belonging to the late majority and laggards remain at very low adoption rates and do not seem to play a significant role in the Reference scenario until 2050. These socioeconomic classes are expected to drive the diffusion process after 2050, by when the pool of potential adopters from the early majority classes is depleted. The adoption rate in the early majority classes is characterized by increased volatility and uncertainty compared to the adoption rates of innovators and late majority until 2050, and it depends on the income distribution.

The cross comparison of the sensitivity analysis regarding different levels of policy support schemes, prices and technology costs shows that the diffusion process of solar PV in single- and two-family houses is starting to gain its momentum, but in the near-term is still sensitive to the profitability of the investment. To this end, the financial incentives provided by the government constitute an administrable and tractable option to accelerate the penetration of the solar PV system.

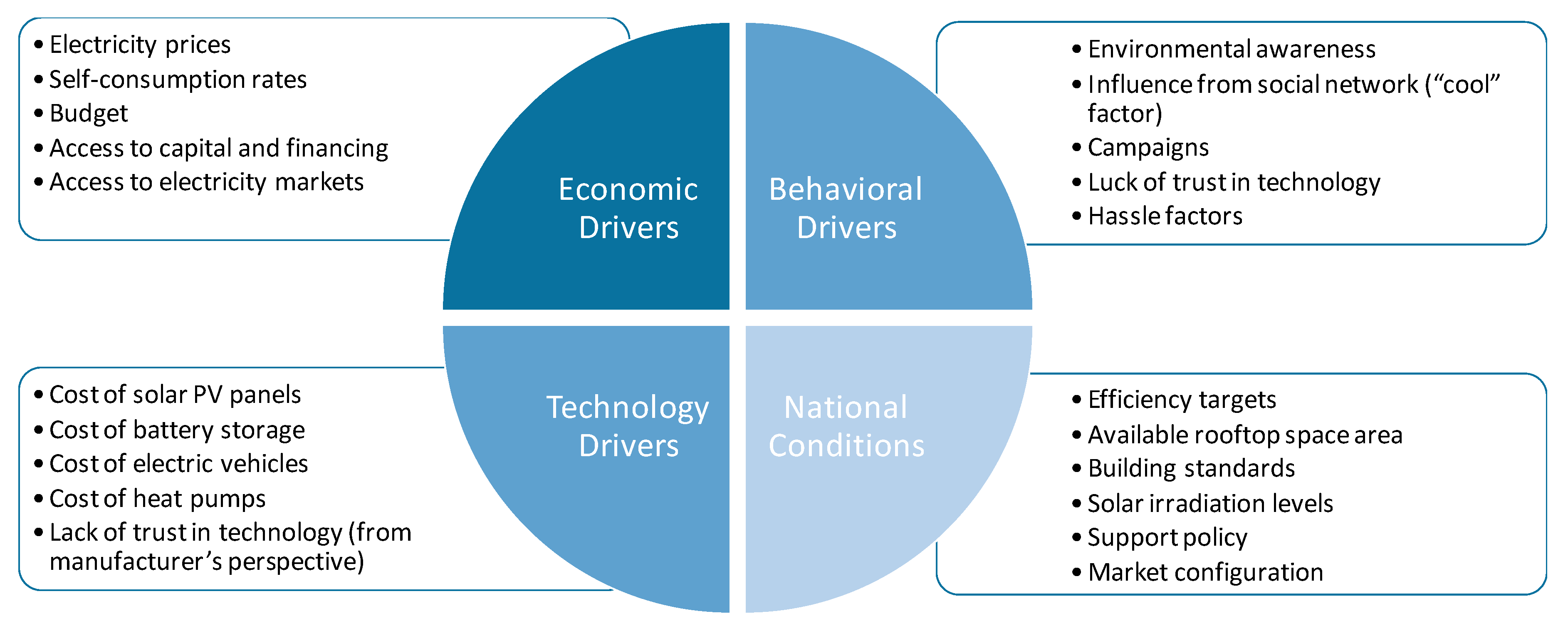

The analysis of the Reference scenario and variants also revealed some of the main drivers that can enable or constrain the prosumers’ uptake, with regards to the market segment of single- and two-family houses. These can be classified as economic drivers, behavioral drivers, technology drivers and drivers stemming from national conditions (

Figure 11).

Low electricity prices and low self-consumption ratios are among the economic drivers that can limit the penetration of solar PV in single- and two-family houses and consequently, the uptake of the prosumers in this market segment. On the other hand, high electricity prices, high self-consumption ratios, and easy access to capital are considered to be favorable economic drivers for the diffusion of the solar PV systems.

Environmental awareness (i.e., the injunctive social norm), knowledge (and awareness) about the technology, and the “cool” factor (or influence from the social network—the descriptive social norm) are behavioral drivers that can accelerate prosumers. Lack of trust in technology and hassle factors (all captured via hurdle rates in our modeling framework) are identified as behavioral drivers that constraint the penetration of small-scale solar PV systems in single- and two-family houses. Viewed another way, low awareness and low knowledge of the small-scale solar PV system technology can be a major barrier in its adoption.

Technology drivers such as low cost of PV and storage, as well as low cost of electric vehicles and heat pumps (which in turn can lead to increased self-consumption ratios), can result in an increased number of prosumers. National conditions such as energy efficiency targets that reduce electricity demand (and consequently the economic benefit of installing a solar PV system) can be limiting factors for the penetration of prosumers. On the contrary, available rooftop space, the intensity of financial support measures, and building standard are national conditions that can act as enablers for accelerated prosumage. Similarly, solar irradiation level is an important national condition for the penetration of solar PV systems.

An increasing number of single- and two-family houses with a solar PV system can reduce the transmission grid investments, but they can also lead to decreased revenues for Transmission System Operators (TSOs) and increased investment in the distribution grid. While prosumers create new business opportunities, as they induce market reforms, they could also lead to increased retail electricity rates for other consumers (which are not prosumers). Prosumers can create economic, social, and environmental benefits and can increase the resilience of energy supply, but they can also reduce the taxable income and increase stranded assets. Therefore, policymakers need to keep all these in mind when considering if, when, why, and how to act. Some drivers are less clear than others are, and while economic drivers are well identified and analyzed, technology drivers can have different impacts (e.g., PV breakthroughs can accelerate prosumers’ uptake, but they can add additional cost in infrastructure).

In this context, decentralized systems with many prosumers require market reforms [

83]. One example is the peer-to-peer market models, in which electricity producers and consumers bid and directly sell and buy electricity and other services (e.g., energy storage), but perhaps at high transaction costs (e.g., the distribution grid is paid a management fee plus a tariff for its distribution function). A second market model is the brokerage systems for prosumers that are connected to a micro-grid. The micro-grid can operate in connection to the main grid or autonomously in isolation. A third market model is the organized prosumer group model, in which a group of prosumers pools resources or forms a virtual power plant. However, all these models are still in the pilot phase, and a possible scale-up would require significant effort from policymakers and stakeholders. To this end, in our analysis, we followed the conventional model of selling excess electricity to the average production cost of a nearby utility. The design of the market is perhaps the most important enabling or constraining factor for scaling up prosumers.

It should be noted that the results obtained in our analysis should be interpreted with some care. There are not forecasts but what-if analyses that are assessing the factors influencing the diffusion of solar PV systems in single- and two-family houses. The Reference scenario does not implement building standards that impose minimum levels of self-sufficiency or renewable energy supply, as well as on emissions. The enforcement of such standards can have a major impact on our results, since not only they can reduce energy consumption but also, they can increase the penetration of renewable, or other low-carbon and efficient technologies.

The methodology we apply is based on several assumptions and simplifications. The parametrization of the model relies on indirect calibration using a rather small sample of years compared to the length of the projection period. However, this issue is common in many frameworks with a long-term perspective, and it is in our aims to extend both the calibration and validation periods of the model when statistical data of later years will be available. Despite these drawbacks, the model displayed a good fitting of the projections obtained with recently published statistics. This is an encouraging sign of the potential of the model.

Apart from improving the parametrization of the model, there are also additional extensions that can be considered in the framework. At first, the agents can be expanded to include multi-family houses, industrial facilities, and commercial buildings. Secondly, the spatial resolution of the model can be increased below the Cantonal level, for example, at the degree of a city or community. Third, the communication component can be expanded to include indirect communication as well. A fourth extension in the model would be the implementation of different market configurations that would help in assessing effective market designs for prosumers. Moreover, the availability of surveys evaluating the investors’ perception of the factors affecting their adoption decision would allow us to base the definition of utility functions on empirical evidence. Finally, the introduction of stochastic solar PV profiles and the option to install also a battery is also in our plans regarding the extension of the current framework.

5. Conclusions and Policy Implications

The penetration of solar PV in single- and two-family houses in Switzerland still relies on support measures determined by the design of the energy policy. The share of single- and two-family houses in the Swiss total residential building stock is about two thirds, which underpins its importance for increasing the penetration of solar PV systems in this market segment in order to meet the national climate change mitigation targets. In our analysis, in which we apply an ABM, we quantify the impact of four different socioeconomic and technical drivers on the decision to invest. In this section, we provide policy implications regarding the influence of each driver, as this influence is captured through the partial utilities of the model and their weight in the decision mechanism.

The financial partial utility encapsulates and quantifies the impact of the main economic drivers in the decision to invest in solar PV systems, such as the electricity prices, the rate of self-consumption, the upfront investment cost, as well as financing constraints related to budgeting and capital access. In our analysis, the weight of the financial utility in the investment decision increases over time, which in turn signals the necessity to remove any barriers related to these economic drivers. This implies that consumers need to be aware of their potential of reducing electricity costs, which requires consumers’ knowledge about their consumption patterns as well as suitable measuring and distribution infrastructure to be in place (e.g., smart grids provided by utilities). In addition, market impacts that result in a low electricity price have adverse effects on the consumer’s decision to install PV.

However, increasing the awareness of consumer regarding their electricity costs and saving potentials is not enough. The rate of self-consumption needs to be increased as well, to render the investment in a solar PV system financially attractive. This also implies that electricity needs to enter in new uses, e.g., in heating and mobility. To this end, building efficiency and emissions standards can achieve high electrification rates of the end-use demand. At the same time, bundling of products can be an effective marketing technique: for instance, manufactures and sellers of electric heating equipment or cars can bundle their products with solar PV and storage systems (This practice is followed by the company (

https://www.solarwatt.com/components/heat-pump), or Tesla after the merge with the SolarCity (

https://www.tesla.com/solarpanels?energy_redirect=true).).

On the other hand, the high upfront investment cost can be tackled via purchase agreements and leasing (This practice is followed by the company Vivint. Solar in the US (

https://www.vivintsolar.com/solar-plans).) or crowdfunding. The latter is gaining momentum, facilitated by online platforms (The Mosaic platform in the US (

www.joinmosaic.com)), which act as showcases of the project, and funders can access investment opportunities and financially contribute as they wish. Different types of crowdfunding can be examined, ranging from donation and reward to lending and provision of equity. Other financing models can include community-shared ownership, in which members can purchase a share of the power produced by an array of solar PV panels (e.g., installed on the roofs of series of single- and two-family houses by the construction company) and receive credits on their electricity bills.

In addition, the accessibility to a decentralized peer-to-peer market where the owner of the solar PV system can sell excess electricity is also a crucial factor in determining PV investments. In the present study, we assumed that the market is accessible for all adopters, which in reality might not be the case. Peer-to-peer market models, brokerage systems and organized prosumer group models discussed in the previous section are still in the pilot phase, and their scaling-up needs legislation to be in place. The configuration and design of the market define in a large extent the installation size, i.e., focus on self-consumption or focus on selling electricity. The latter leads to larger installations than the former.

The partial utilities referring to the environmental and social network in the model represent behavioral drivers. The social network utility is used to capture the descriptive social norms (i.e., influence from the social network), and the environmental partial utility captures the injunctive social norm, the awareness and knowledge regarding the solar PV technology. The environmental and social network partial utilities complement each other in the decision process: the results of our analysis show that while the weight of the environmental utility in the decision to invest declines over time, the weight of the social network utility increases. This result also implies that the perceived complexity of the product, often associated with the lack of knowledge about the technology, can be an important barrier regarding its diffusion. Innovative market solutions, e.g., one-stop-shops where customers can buy turnkey solar roofs (e.g., similar to the option offered by Tesla after the merging with the company SolarCity), can help in reducing the perceived complexity of the product.

The environmental sensitivity of the individuals, i.e., the perception that adopting a solar PV system is “the right thing to do” to protect the climate, also needs to be strengthened and reinforced as its weight in the decision process to adopt the technology lessens over time. The marketing of solar PV systems needs to go beyond the expectation that the product is beneficial due to aspects of climate change mitigation. Life-cycle analysis can help in exposing additional co-benefits such as life-cycle cost benefits, independence in supply, human health benefits, reduced land footprint, reduced use of materials during the manufacturing of the panels and others (see also [

3]). The inclusion of life-cycle indicators in campaigns can increase not only the environmental sensitivity of the potential adopters but also it can help in better understanding the complexity, benefits and the true costs of the technology compared to other alternatives in electricity supply.

The research in psychology has long recognized that together with the injunctive social norms, the descriptive norms (i.e., imitating the behavior of the others) is an important decision factor. In our analysis, the influence of the social network gains weight in the investment decision over time. The increasing occurrence of solar PV installations in roofs and their visibility by neighbors and others directly affects intentions and strengthens the adoption of a solar PV system. In this context, government policies with the a priori assumption that investors decide on purely economic grounds, do not fully exploit the influence of the descriptive norms in the decision process. A policy basket that combines the power of peer effects with adequate financing can achieve a fast penetration of solar PV systems in targeted communities, e.g., in areas where the uniform nationwide incentives do not seem to work efficiently. This is of particular importance when solar PV systems enter in the “grid-parity” phase, and the existing financial support schemes are phased-out. For example, the state of Connecticut launched a campaign from 2013 to 2016 to increase the penetration of solar PV systems in houses. The campaign was built around the consumer’s education, consumer’s motivation, and ultimately the conversion of consumer’s interest into a decision to install a solar PV system. The result of the campaign was impressive as the houses with solar PV panels increased from 800 in 2013 to 12,500 in 2016 [

84]. The outcome of this campaign demonstrated that segmentation of consumers in the policy design, targeted campaigns and improved visibility of the technology in areas with low penetration rates can help to increase the overall adoption rates of the solar PV systems in single- and two-family houses.

In addition to the socioeconomic challenges discussed above and related to financial constraints and social norms, there are also important socio-technical barriers that need to be tackled. These include, among others, product quality, complexity, durability, efficiency, and safety, as well as architectural constraints. For example, there is a large number of buildings, which offer little rooftop space for solar PV cells. Moreover, the lack of knowledge about the technology can lead to improper use and poor maintenance of the systems by the adopters. Also, poor after sales service and ineffective marketing represent socio-technical barriers preventing PV deployment. Climatic conditions, i.e., solar irradiation and precipitation, are important determinants for the profitability of PV systems and can make the solar PV panels less suitable in some areas than in others. In such areas, targeted campaigns, also focusing on broader non-financial benefits of the technology, may help in increasing the adoption rates.

In conclusion, we can argue that the diffusion of the solar PV systems in the market segment of single- and two-family houses is gaining its momentum. The reduction in the cost of producing solar PV systems helps in increasing the adoption of technology. While barriers depend on the specific individual context of consumers, various measures can facilitate the solar PV diffusion process. These include collaboration between actors (i.e., manufacturers, consumers, the building construction and the finance sector), as well as dedicated government support with policy segmentation targeting different consumer groups and focus on social norms, and effective marketing to increase product awareness and technology knowledge.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}