Predictive Trading Strategy for Physical Electricity Futures

Abstract

:1. Introduction

1.1. Context of This Research

1.2. Literature Review

1.3. Contributions and Structure of This Article

2. Conditional Predictive Trading of Electricity Physical Futures

2.1. Proposed Mid-Term Forecasting Model of Average Spot Prices

- DM: delivery month, with values 1 to 12. It represents the number of the month when the traded electricity will be delivered.

- LagD: period, in days, between the negotiation day (any day, i.e., n) and the last negotiation day before the start of the delivery period corresponding to DM.

- : Average monthly futures settlement price for delivery month DM in the last 7 days before negotiation day n. So, this input variable is calculated by (1):where represents the monthly futures settlement price for delivery month DM on the trading phase of day p, i.e., that established at the end of that phase on the previous negotiation day, and corresponds to the number of futures negotiation days in the last 7 days. Observe that the values for nonmarket days (day p with no futures market) are not included in the summation.

- : Average quarterly futures settlement price for the quarter including the DM in the last 90 days before negotiation day n. This is calculated by (2), where the delivery quarter DQ must include the delivery month DM:where represents the quarterly futures settlement price for the quarter (including the DM) established at the end of the previous negotiation day and corresponds to the number of futures negotiation days in the last 90 days. Observe that values for nonmarket days (day p with no futures market) are not included in the summation.

- : Average spot price in the last 7 days before day n; this is calculated by (3):where represents the spot price for day p hour h. Observe that the spot prices for day n were established on the previous day.

- : variation of the average monthly futures settlement price for delivery month DM in the last 7 days before negotiation day n; this is calculated by (4):where represents the average monthly settlement futures price for delivery month DM in the last 7 days before negotiation day and corresponds to its value 7 days before.

2.2. Predictive Trading Strategy of Physical Futures

3. Results of Conditional Predictive Trading of Physical Futures

3.1. Results of the Forecasting Model in the Prediction of the Monthly Average Spot Price

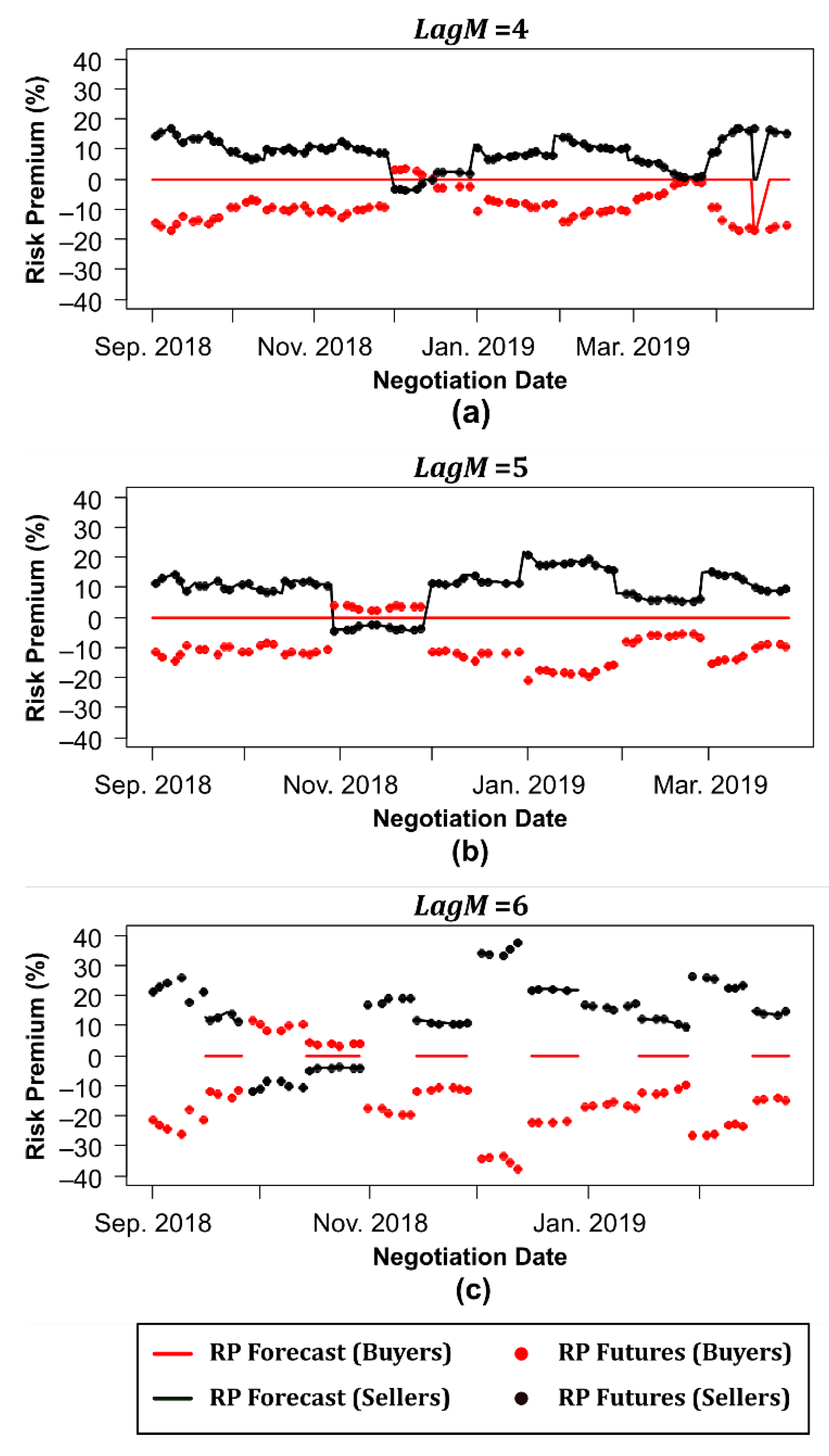

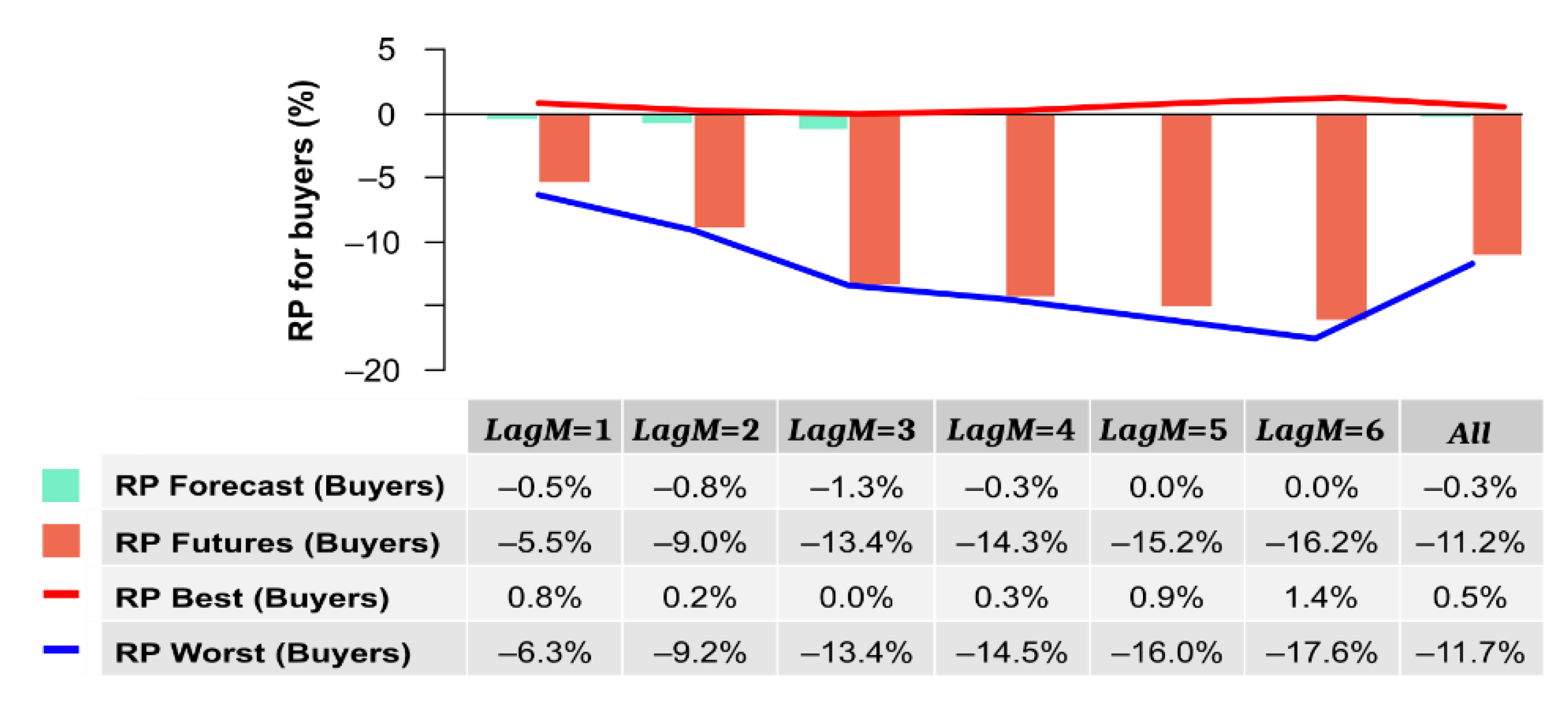

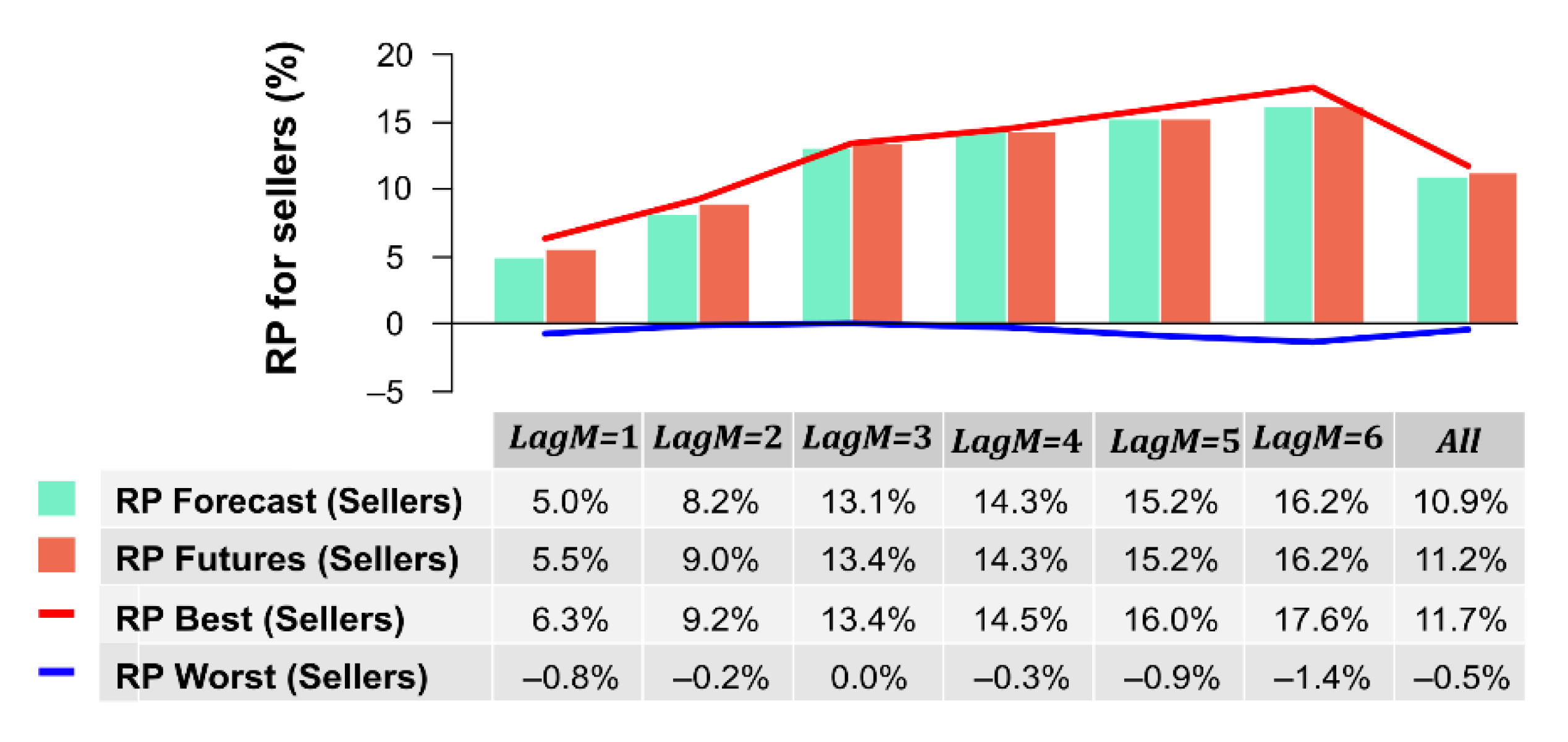

3.2. Results of the Predictive Trading Strategy of Physical Futures with the ELM Neural Network Model

3.3. Results of the Predictive Trading Strategy of Physical Futures with a Simpler Forecasting Model

4. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Nomenclature

| Vector of weights between the input layer and the hidden layer node i | |

| Bias of the hidden layer node i | |

| Output weights vector | |

| Least square estimation of the output weights vector | |

| Weight from the hidden layer node i to the output node | |

| Delivery month | |

| Last delivery month in the testing period | |

| First delivery month in the testing period | |

| D-M | Diebold-Mariano |

| Activation function | |

| Hour Index | |

| Hidden layer output matrix | |

| Moore–Penrose generalized inverse of the hidden layer output matrix | |

| L | Number of nodes in the hidden layer |

| Number of days between the negotiation day and the last negotiation day for the delivery month | |

| Maturity or holding period in months ( = 1,2, …, 6) | |

| Monthly futures settlement price for delivery month on the trading phase of day p, i.e., the established at the end of previous trading day to day p | |

| Average monthly futures settlement price for delivery month in the last 7 days before negotiation day | |

| Variation of the average monthly futures settlement price for delivery month in the last 7 days before negotiation day | |

| Negotiation day | |

| N | Number of samples in the training data set |

| Number of futures negotiation days in the last i days | |

| Total number of negotiation days for delivery month with a maturity | |

| Last negotiation day for delivery month with maturity | |

| First negotiation day for delivery month with maturity | |

| Target vector | |

| Target value for the sample j | |

| Day Index | |

| Average quarterly futures settlement price for the quarter including the established on the last 90 days before negotiation day | |

| Quarterly futures settlement price for the quarter including the established in the last negotiation day before day | |

| Root mean square error | |

| Root mean square error of the variable with respect to the ex post monthly average spot price for a holding period (variable = spot price forecast, Futures price) | |

| Risk Premium | |

| Average value of for the all maturities, agents = (buyers, sellers, both) and strategy = (predictive, conventional, best, worst) | |

| Average value of for maturity , agents = (buyers, sellers, both) and strategy = (predictive, conventional, best, worst) | |

| Risk Premium for agents for negotiation day corresponding to the delivery month following the trading strategy, agents = (buyers, sellers, both) and strategy = (predictive, conventional, best, worst) | |

| Average actual spot price in the delivery month | |

| Average spot price in last 7 days before negotiation day | |

| Forecast of monthly average spot price evaluated in day for delivery month | |

| Spot price for day hour | |

| Input vector for the sample j |

References

- Edwards, D.W. Energy Trading and Investing: Trading, Risk Management and Structuring Deals in the Energy Market; McGraw-Hill: New York, NY, USA, 2009. [Google Scholar]

- Economic Consulting Associates Limited. European Electricity: Forward Markets and Hedging Products—State of Play and Elements for Monitoring 2015. Available online: www.acer.europa.eu (accessed on 28 April 2020).

- Hull, J. Options, Futures, and Other Derivatives, 9th ed.; Prentice Hall: Upper Saddle River, NJ, USA, 2015. [Google Scholar]

- Bessembinder, H.; Lemmon, M.L. Equilibrium pricing and optimal hedging in electricity forward markets. J. Financ. 2002, 57, 1347–1382. [Google Scholar] [CrossRef]

- Wilkens, S.; Wimschulte, J. The pricing of electricity futures: Evidence from the European energy exchange. J. Futures Mark. 2007, 27, 387–410. [Google Scholar] [CrossRef]

- Furio, D.; Meneu, V. Expectations and forward risk premium in the Spanish deregulated power market. Energy Policy 2010, 38, 784–793. [Google Scholar] [CrossRef]

- Umutlu, G.; Dorsman, A.; Telatar, E. The Electricity Market, Day-Ahead Market and Futures Market. In Financial Aspects in Energy; Dorsman, A., Westerman, W., Karan, M.B., Arslan, Ö., Eds.; Springer: Berlin, Germany, 2011; pp. 109–128. [Google Scholar] [CrossRef]

- Steinert, R.; Ziel, F. Short- to mid-term day-ahead electricity price forecasting using futures. Energy J. 2019, 40, 105–127. [Google Scholar] [CrossRef]

- Huisman, R.; Kilic, M. Electricity Futures Prices: Indirect Storability, Expectations, and Risk Premiums. Energy Econ. 2012, 34, 892–898. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. Commodity futures prices: Some evidence on forecast power, premiums, and the theory of storage. J. Bus. 1987, 60, 55–73. [Google Scholar] [CrossRef]

- Cartea, A.; Villaplana, P. An analysis of the main determinants of electricity forward prices and forward risk Premia. In Quantitative Energy Finance; Benth, F., Kholodnyi, V., Laurence, P., Eds.; Springer: New York, NY, USA, 2014; pp. 215–236. [Google Scholar] [CrossRef]

- Longstaff, F.A.; Wang, A.W. Electricity forward prices: A high-frequency empirical analysis. J. Financ. 2004, 59, 1877–1900. [Google Scholar] [CrossRef] [Green Version]

- Benth, F.E.; Cartea, A.; Kiesel, R. Pricing forward contracts in power markets by the certainty equivalence principle: Explaining the sign of the market risk premium. J. Bank Financ. 2008, 32, 2006–2021. [Google Scholar] [CrossRef] [Green Version]

- Weron, R.; Zator, M. Revisiting the relationship between spot and futures prices in the Nord Pool electricity market. Energy Econ. 2014, 44, 178–190. [Google Scholar] [CrossRef] [Green Version]

- Fleten, S.-E.; Hagen, L.A.; Nygård, M.T.; Smith-Sivertsen, R.; Sollie, J.M. The overnight risk premium in electricity forward contracts. Energy Econ. 2015, 49, 293–300. [Google Scholar] [CrossRef]

- Bunn, D.W.; Chen, D. The forward premium in electricity futures. J. Empir. Financ. 2013, 23, 173–186. [Google Scholar] [CrossRef]

- The Iberian Energy Derivatives Exchange, OMIP. Available online: http://www.omip.pt (accessed on 29 April 2020).

- Ballester, J.M.; Climent, F.; Furió, D. Market efficiency and price discovery relationships between spot, futures and forward prices: The case of the Iberian Electricity Market (MIBEL). Span. J. Financ. Accoun. 2016, 45, 135–153. [Google Scholar] [CrossRef] [Green Version]

- Ferreira, M.; Sebastião, H. The iberian electricity market: Analysis of the risk premium in an illiquid market. J. Energy Markets 2018, 11, 61–82. [Google Scholar] [CrossRef]

- Da Silva, R.R.; Dias, M.F.; Madaleno, M. Iberian electricity market spot and futures prices: Comovement and lead-lag relationship analysis. J. Sustain. Energy Plan. Manag. 2019, 19, 59–68. [Google Scholar] [CrossRef]

- Hong, T.; Pinson, P.; Fan, S.; Zareipour, H.; Troccoli, A.; Hyndman, R.J. Probabilistic energy forecasting: Global energy forecasting competition 2014 and beyond. Int. J. Forecast. 2016, 32, 896–913. [Google Scholar] [CrossRef] [Green Version]

- Yan, X.; Chowdhury, N.A. Mid-term electricity market clearing price forecasting: A hybrid LSSVM and ARMAX approach. Int. J. Electr. Power 2013, 53, 20–26. [Google Scholar] [CrossRef]

- García-Martos, C.; Rodríguez, J.; Sánchez, M.J. Forecasting electricity prices and their volatilities using unobserved components. Energy Econ. 2011, 33, 1227–1239. [Google Scholar] [CrossRef] [Green Version]

- Yan, X.; Chowdhury, N.A. Mid-term electricity market clearing price forecasting: A multiple SVM approach. Int. J. Electr. Power 2014, 58, 206–214. [Google Scholar] [CrossRef]

- Kristiansen, T. A time series spot price forecast model for the Nord Pool market. Int. J. Electr. Power 2014, 61, 20–26. [Google Scholar] [CrossRef]

- Torbaghan, S.S.; Motamedi, A.; Zareipour, H.; Tuan, L.A. Medium-term electricity price forecasting. In Proceedings of the 2012 North American Power Symposium (NAPS), Champaign, IL, USA, 9–11 September 2012; pp. 1–8. [Google Scholar] [CrossRef]

- Cheng, C.; Luo, B.; Miao, S.; Wu, X. Mid-term electricity market clearing price forecasting with sparse data: A case in newly-reformed Yunnan electricity market. Energies 2016, 9, 804. [Google Scholar] [CrossRef] [Green Version]

- Vehviläinen, I.; Pyykkönen, T. Stochastic factor model for electricity spot price—the case of the Nordic market. Energy Econ. 2005, 27, 351–367. [Google Scholar] [CrossRef]

- Maciejowska, K.; Weron, R. Short-and mid-term forecasting of baseload electricity prices in the UK: The impact of intra-day price relationships and market fundamentals. IEEE Trans. Power Syst. 2016, 31, 994–1005. [Google Scholar] [CrossRef] [Green Version]

- Chakravarty, S.; Mohapatra, P.; Dash, P.K. Evolutionary extreme learning machine for energy price forecasting. Int. J. Knowl.-Based Intell. Eng. Syst. 2016, 20, 75–96. [Google Scholar] [CrossRef]

- Windler, T.; Busse, J.; Rieck, J. One month-ahead electricity price forecasting in the context of production planning. J. Clean Prod. 2019, 238, 117910. [Google Scholar] [CrossRef]

- Ziel, F.; Steinert, R. Probabilistic mid- and long-term electricity price forecasting. Renew. Sustain. Energ. Rev. 2018, 94, 251–266. [Google Scholar] [CrossRef] [Green Version]

- Ghoddusi, H.; Creamer, G.G.; Rafizadeh, N. Machine learning in energy economics and finance: A review. Energy Econ. 2019, 81, 709–727. [Google Scholar] [CrossRef]

- Moreno, J. Trading strategies modeling in Colombian power market using artificial intelligence techniques. Energy Policy 2009, 37, 836–843. [Google Scholar] [CrossRef]

- Pinto, T.; Sousa, T.M.; Praça, I.; Vale, Z.; Morais, H. Support Vector Machines for decision support in electricity markets’ strategic bidding. Neurocomputing 2016, 172, 438–445. [Google Scholar] [CrossRef]

- Santos, G.; Pinto, T.; Praça, I.; Vale, Z. MASCEM: Optimizing the performance of a multi-agent system. Energy 2016, 111, 513–524. [Google Scholar] [CrossRef] [Green Version]

- Lopes, F. MATREM: An Agent-based Simulation Tool for Electricity Markets. In Electricity Markets with Increasing Levels of Renewable Generation: Structure, Operation, Agent-Based Simulation and Emerging Designs; Springer: Cham, Switzerland, 2018; pp. 189–225. [Google Scholar] [CrossRef]

- Krečar, N.; Benth, F.E.; Gubina, A.F. Towards Definition of the Risk Premium Function. IEEE Trans. Power Syst. 2020, 35, 1085–1098. [Google Scholar] [CrossRef]

- Browell, J. Risk Constrained Trading Strategies for Stochastic Generation with a Single-Price Balancing Market. Energies 2018, 11, 1345. [Google Scholar] [CrossRef] [Green Version]

- Bunn, D.W.; Gianfreda, A.; Kermer, S. A Trading-Based Evaluation of Density Forecasts in a Real-Time Electricity Market. Energies 2018, 11, 2658. [Google Scholar] [CrossRef] [Green Version]

- MIBEL Board of Regulators. Estudio Sobre Comparativa de los Precios MIBEL (Contado y Plazo) con otros Mercados Europeos y su Relación con el Mercado único. Internal Report. July 2019. Available online: https://www.mibel.com/wp-content/uploads/2020/03/20190705SE_ESb.pdf (accessed on 12 June 2020).

- Huang, G.-B.; Zhu, Q.-Y.; Siew, C.-K. Extreme learning machine: Theory and applications. Neurocomputing 2006, 70, 489–501. [Google Scholar] [CrossRef]

- Huang, G.-B.; Wang, D.H.; Lan, Y. Extreme learning machines: A survey. Int. J. Mach. Learn. Cybern. 2011, 2, 107–122. [Google Scholar] [CrossRef]

- Li, S.; Wang, P.; Goel, L. Short-term load forecasting by wavelet transform and evolutionary extreme learning machine. Electr. Power Syst. Res. 2015, 122, 96–103. [Google Scholar] [CrossRef]

- Chen, Y.; Kloft, M.; Yang, Y.; Li, C.; Li, L. Mixed kernel based extreme learning machine for electric load forecasting. Neurocomputing 2018, 312, 90–106. [Google Scholar] [CrossRef]

- Rafiei, M.; Niknam, T.; Aghaei, J.; Shafie-Khah, M.; Catalao, J.P.S. Probabilistic load forecasting using an improved wavelet neural network trained by generalized extreme learning machine. IEEE Trans. Smart Grid 2018, 9, 6961–6971. [Google Scholar] [CrossRef]

- Hossain, M.; Mekhilef, S.; Danesh, M.; Olatomiwa, L.; Shamshirband, S. Application of extreme learning machine for short term output power forecasting of three grid-connected PV systems. J. Clean Prod. 2017, 167, 395–405. [Google Scholar] [CrossRef]

- Wan, C.; Xu, Z.; Pinson, P.; Dong, Z.Y.; Wong, K.P. Probabilistic forecasting of wind power generation using extreme learning machine. IEEE Trans. Power Syst. 2014, 29, 1033–1044. [Google Scholar] [CrossRef] [Green Version]

- Behera, M.K.; Nayak, N. A comparative study on short-term PV power forecasting using decomposition based optimized extreme learning machine algorithm. Eng. Sci. Technol. Inter. J. 2020, 23, 156–167. [Google Scholar] [CrossRef]

- Wu, C.; Wang, J.; Chen, X.; Du, P.; Yang, W. A novel hybrid system based on multi-objective optimization for wind speed forecasting. Renew. Energy 2020, 146, 149–165. [Google Scholar] [CrossRef]

- Chen, X.; Dong, Z.Y.; Meng, K.; Xu, Y.; Wong, K.P.; Ngan, H. Electricity price forecasting with extreme learning machine and bootstrapping. IEEE Trans. Power Syst. 2012, 27, 2055–2062. [Google Scholar] [CrossRef]

- Shrivastava, N.A.; Panigrahi, B.K. A hybrid wavelet-ELM based short term price forecasting for electricity markets. Int. J. Electr. Power 2014, 55, 41–50. [Google Scholar] [CrossRef]

- Wang, G.; Wei, Y.; Qiao, S. Generalized Inverses: Theory and Computations; Springer: Singapore, 2018. [Google Scholar]

- Ding, S.; Zhao, H.; Zhang, Y.; Xu, X.; Nie, R. Extreme learning machine: Algorithm, theory and applications. Artif. Intell. Rev. 2015, 44, 103–115. [Google Scholar] [CrossRef]

- Botterud, A.; Kristiansen, T.; Ilic, M.D. The relationship between spot and futures prices in the Nord Pool electricity market. Energy Econ. 2010, 32, 967–978. [Google Scholar] [CrossRef]

- Diebold, F.X.; Mariano, R.S. Comparing predictive accuracy. J. Bus. Econ. Stat. 1995, 13, 253–263. [Google Scholar] [CrossRef] [Green Version]

- Harvey, D.; Leybourne, S.; Newbold, P. Testing the equality of prediction mean squared errors. Int. J. Forecast. 1997, 13, 281–291. [Google Scholar] [CrossRef]

- Nowotarski, J.; Raviv, E.; Trück, S.; Weron, R. An empirical comparison of alternative schemes for combining electricity spot price forecasts. Energy Econ. 2014, 46, 395–412. [Google Scholar] [CrossRef]

- Kath, C.; Ziel, F. The value of forecasts: Quantifying the economic gains of accurate quarter-hourly electricity price forecasts. Energy Econ. 2018, 76, 411–423. [Google Scholar] [CrossRef] [Green Version]

- Lago, J.; De Ridder, F.; De Schutter, B. Forecasting spot electricity prices: Deep learning approaches and empirical comparison of traditional algorithms. Appl. Energy 2018, 221, 386–405. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Statistic | Spot (Daily) | Futures (All) | ||||||

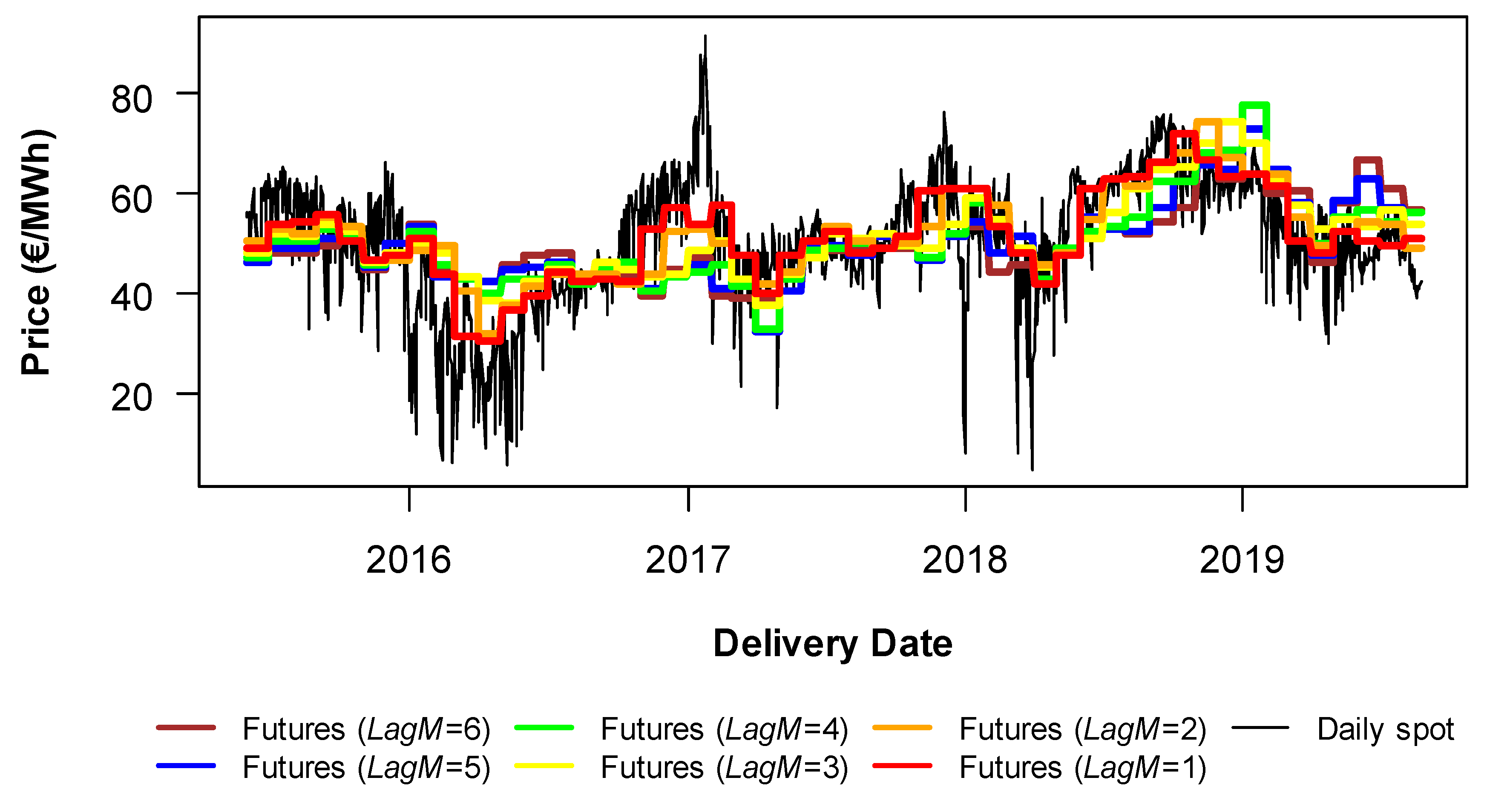

|---|---|---|---|---|---|---|---|---|

| Maximum | 91.88 | 67.40 | 65.40 | 67.40 | 65.21 | 60.02 | 56.30 | 55.44 |

| Minimum | 4.50 | 27.48 | 27.48 | 29.10 | 33.82 | 31.50 | 32.05 | 30.57 |

| Mean | 48.51 | 47.52 | 49.02 | 48.37 | 47.34 | 46.82 | 46.88 | 46.50 |

| SD | 12.43 | 6.09 | 8.10 | 6.75 | 5.72 | 5.26 | 4.62 | 4.59 |

| Skewness | −0.594 | 0.05 | −0.16 | 0.14 | 0.12 | −0.37 | −0.52 | −0.69 |

| Kurtosis | 0.969 | 0.61 | −0.28 | 0.12 | 0.12 | 0.39 | 0.62 | 1.02 |

| Statistic | Spot (Daily) | Futures (All) | ||||||

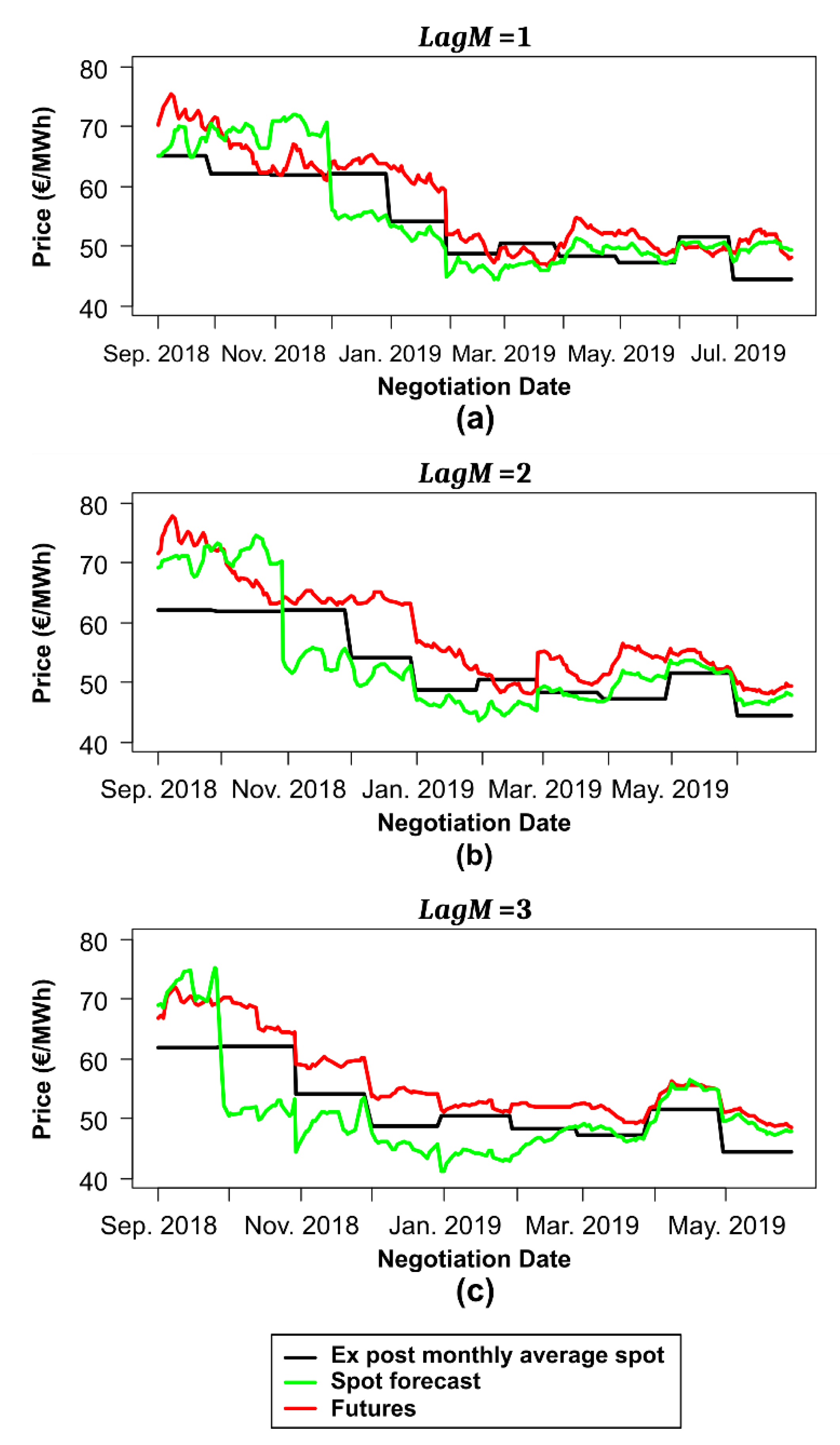

|---|---|---|---|---|---|---|---|---|

| Maximum | 75.93 | 81.00 | 75.50 | 77.75 | 78.81 | 81.00 | 78.87 | 71.42 |

| Minimum | 26.69 | 44.78 | 46.60 | 48.00 | 50.40 | 47.35 | 46.85 | 44.78 |

| Mean | 55.75 | 60.18 | 58.04 | 59.88 | 61.58 | 61.12 | 60.59 | 59.87 |

| SD | 9.35 | 7.48 | 8.17 | 8.19 | 7.54 | 7.39 | 6.66 | 6.31 |

| Skewness | 0.010 | 0.20 | 0.25 | 0.20 | 0.37 | 0.68 | −0.02 | −0.37 |

| Kurtosis | −0.559 | −0.60 | −1.38 | −1.16 | −1.02 | 0.11 | 0.03 | 0.02 |

| LagM (Months) | RMSE ELM (€/MWh) | RMSE OLS (€/MWh) |

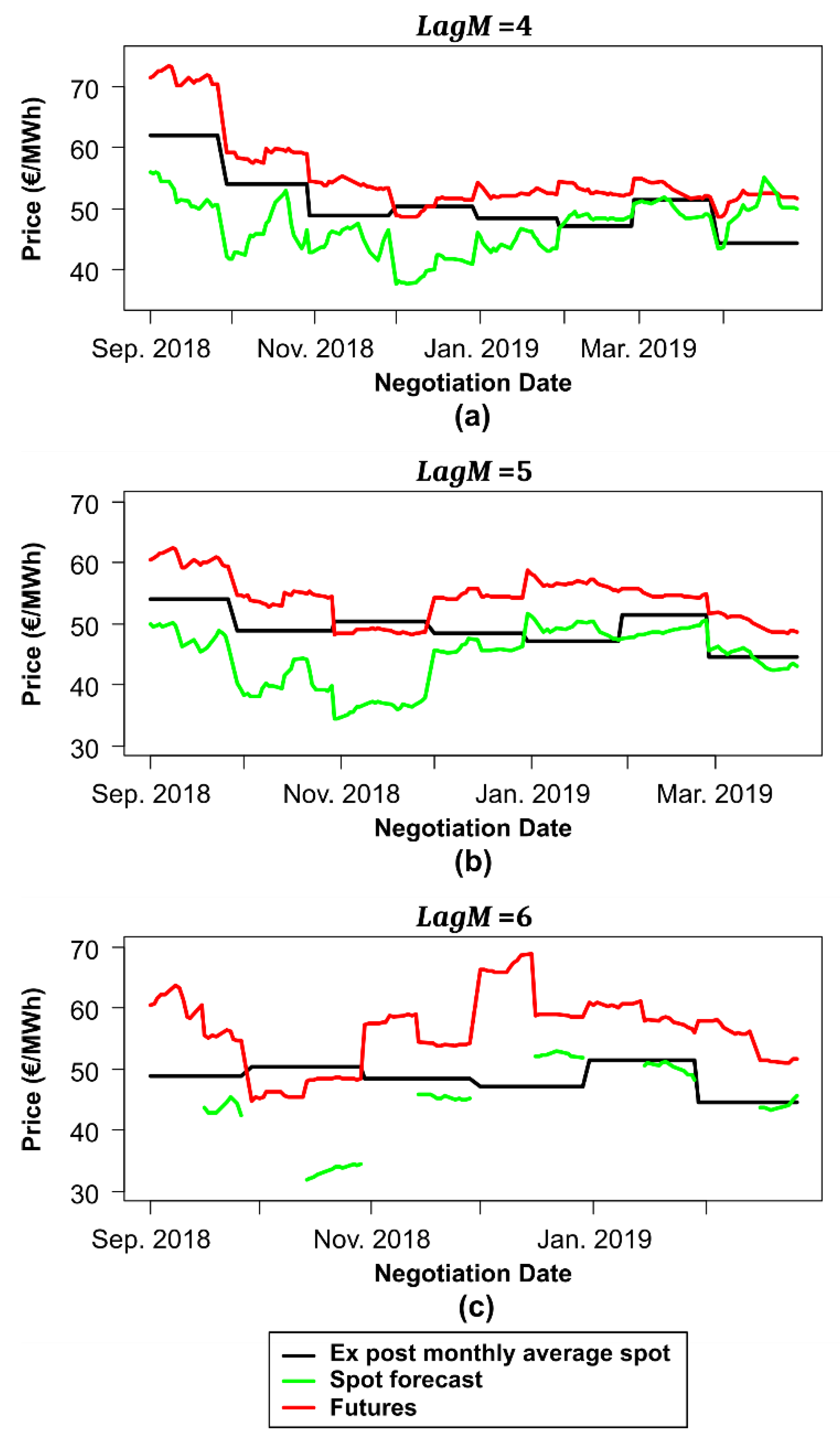

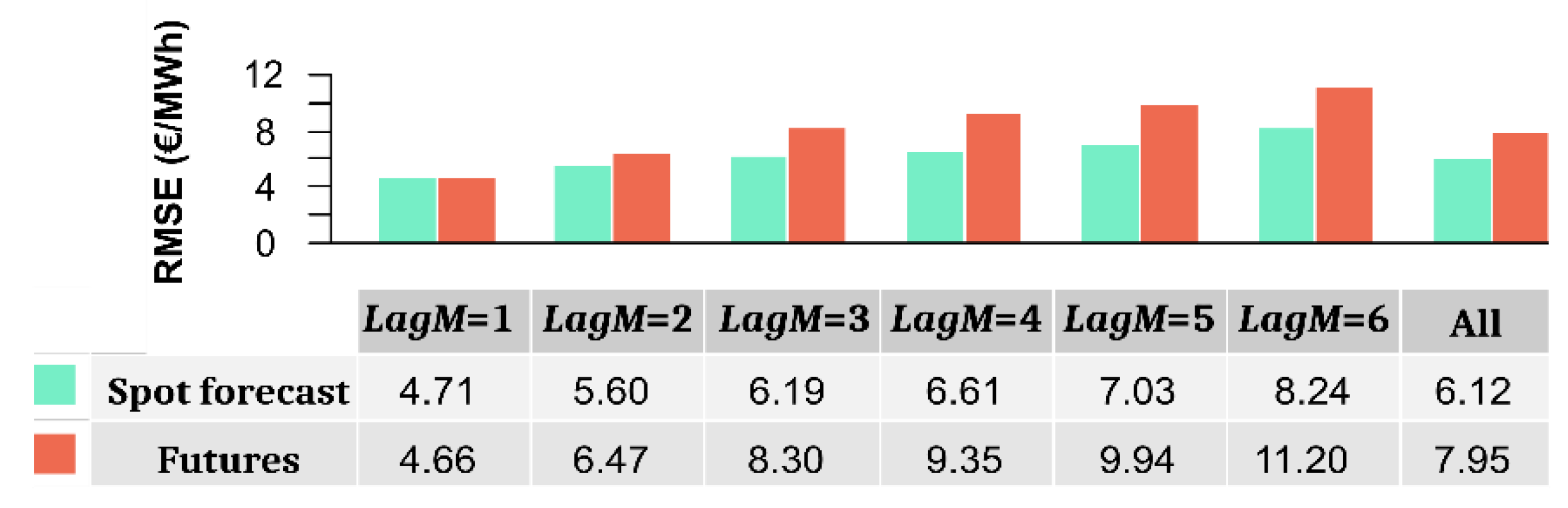

|---|---|---|

| 1 | 4.71 | 7.20 |

| 2 | 5.60 | 6.86 |

| 3 | 6.19 | 5.94 |

| 4 | 6.61 | 5.30 |

| 5 | 7.03 | 4.84 |

| 6 | 8.24 | 4.75 |

| All | 6.12 | 6.15 |

| LagM (Months) | mD-M Statistic | p-Value |

|---|---|---|

| 1 | −7.88 | 0.0000 |

| 2 | −2.13 | 0.0172 |

| 3 | 0.45 | 0.6741 |

| 4 | 1.83 | 0.9658 |

| 5 | 2.26 | 0.9874 |

| 6 | 1.47 | 0.9270 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Monteiro, C.; Fernandez-Jimenez, L.A.; Ramirez-Rosado, I.J. Predictive Trading Strategy for Physical Electricity Futures. Energies 2020, 13, 3555. https://doi.org/10.3390/en13143555

Monteiro C, Fernandez-Jimenez LA, Ramirez-Rosado IJ. Predictive Trading Strategy for Physical Electricity Futures. Energies. 2020; 13(14):3555. https://doi.org/10.3390/en13143555

Chicago/Turabian StyleMonteiro, Claudio, L. Alfredo Fernandez-Jimenez, and Ignacio J. Ramirez-Rosado. 2020. "Predictive Trading Strategy for Physical Electricity Futures" Energies 13, no. 14: 3555. https://doi.org/10.3390/en13143555

APA StyleMonteiro, C., Fernandez-Jimenez, L. A., & Ramirez-Rosado, I. J. (2020). Predictive Trading Strategy for Physical Electricity Futures. Energies, 13(14), 3555. https://doi.org/10.3390/en13143555