Is It Possible to Make Money on Investing in Companies Manufacturing Solar Components? A Panel Data Approach

Abstract

:1. Introduction

2. Data and Methodology

- With a set of K objects, determine that they belong to the same class. If so, end the algorithm.

- Otherwise, consider all possible divisions of set K into subsets K1, K2,... Kn so that they are as homogeneous as possible.

- Assess these divisions according to the adopted criteria and select the best one.

- Divide set K in the chosen way.

- Perform steps 1–4 recursively for each subset.

- We calculate the distance between w and each training object x.

- We find the k training facilities closest to .

- We vote among the decision values corresponding to these objects.

- We assign the most common decision value to object .

3. Results

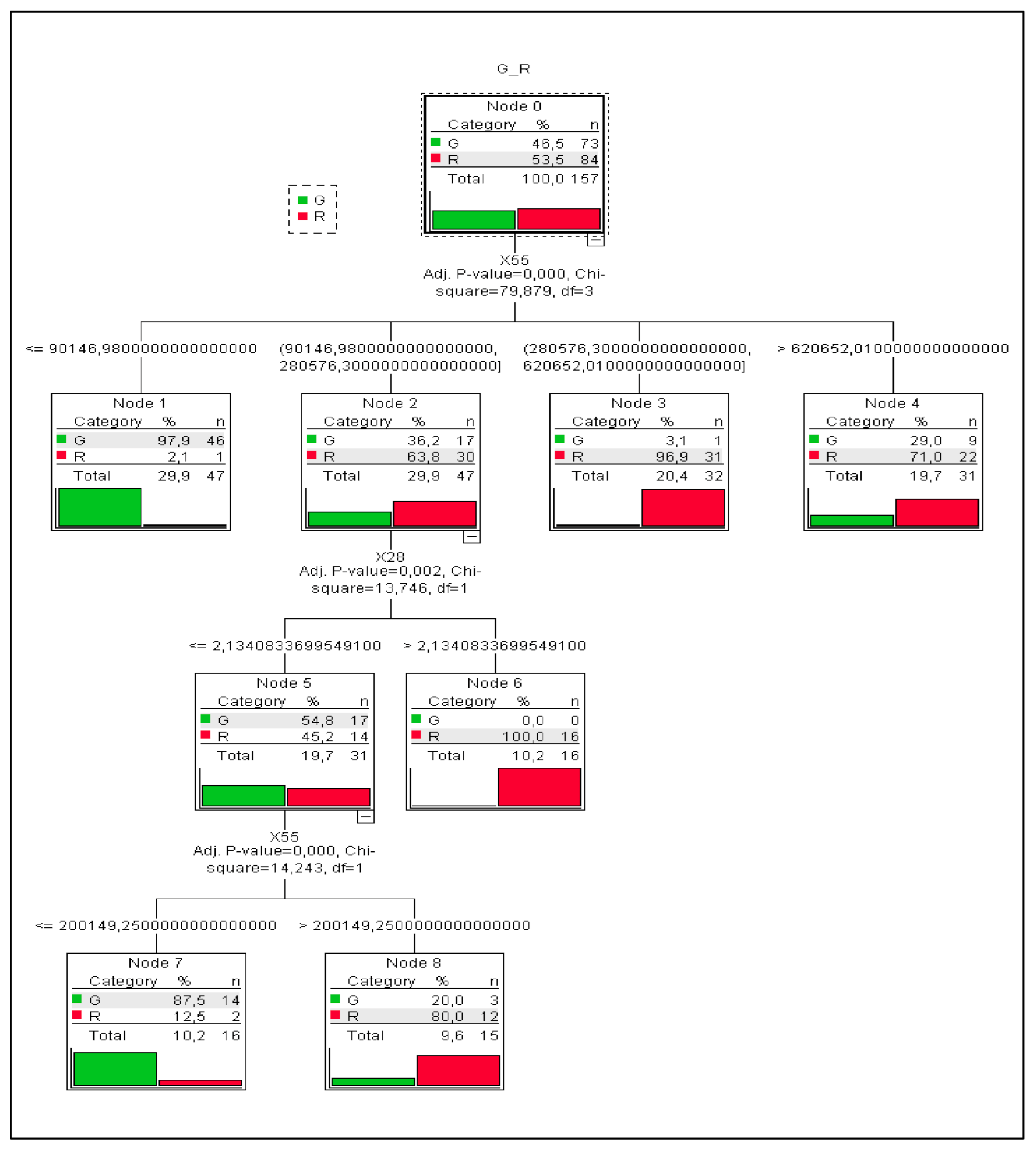

3.1. Classification Trees and k-Nearest Neighbors

3.2. Altman’s Model Analysis and T-Test Sample Comparisons

3.3. Analysis of Crucial Ratios

4. Discussion

- extending the sample period, taking into account the period of 2015–2018, and including businesses operating in Taiwan,

- increasing the number of ratios considered to 92 and by taking not only into account ratios and variables calculated using balance sheet and profit and loss account data but also cash flow and market value data,

- using the k-Nearest Neighbors approach, Altman model, and Student’s t-test to investigate whether companies that manufacture solar modules, solar cells, solar silicon rods, solar wafers, solar power, solar photovoltaic products, and related equipment (green companies) can be differentiated from other enterprises in the sector that are not associated with renewable energy and whether these companies are in a better financial state.

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Hazboun, S.O.; Howe, P.D.; Coppock, D.L.; Givens, J.E. The politics of decarbonization: Examining conservative partisanship and differential support for climate change science and renewable energy in Utah. Energy Res. Soc. Sci. 2020, 70, 101769. [Google Scholar] [CrossRef]

- The International Energy Agency. Available online: https://www.iea.org/statistics (accessed on 30 October 2019).

- Independent Evaluation Group. CHINA Renewable Energy Scale-Up Program: Phase One, Report No. 117156. 2017. Available online: https://ieg.worldbankgroup.org/sites/default/files/Data/pparchinarenewableenergy-10302017.pdf (accessed on 22 December 2019).

- National Institute of Transforming India. Report of Expert Group on 175 GW RE by 2022. 2015. Available online: https://niti.gov.in/writereaddata/files/175-GW-Renewable-Energy.pdf (accessed on 22 December 2019).

- Hongzhan, S.; Qiang, Z.; Yibo, W.; Qiang, Y.; Jun, S. China’s solar photovoltaic industry development: The status quo, problems and approaches. Appl. Energy 2014, 118, 221–230. [Google Scholar]

- Pablo-Romero, M.P. Solar Energy: Incentives to Promote PV in EU27. AIMS Energy 2013, 1, 28–47. [Google Scholar] [CrossRef] [Green Version]

- Solangi, K.H.; Islam, M.R.; Saidur, R.; Fayaz, H.R. A review on global energy policy. Renew. Sustain. Energy Rev. 2011, 15, 2149–2163. [Google Scholar] [CrossRef]

- Sachu, B.K. A study on global solar PV energy developments and policies with a special focus on the top ten solar PV power producing countries. Renew. Sustain. Energy Rev. 2015, 43, 621–634. [Google Scholar]

- Trück, S.; Weron, R. Convenience yields and risk premiums in the EU-ETS—Evidence from the Kyoto commitment period. J. Futures Mark. 2016, 36, 587–611. [Google Scholar] [CrossRef] [Green Version]

- Bohl, M.T.; Kaufmann, P.; Stephan, P.M. From hero to zero: Evidence of performance reversal and speculative bubbles in German renewable energy stocks. Energy Econ. 2013, 37, 40–51. [Google Scholar] [CrossRef] [Green Version]

- Henriques, I.; Sadorsky, P. Oil prices and the stock prices of alternative energy companies. Energy Econ. 2008, 30, 998–1010. [Google Scholar] [CrossRef]

- Inchauspe, J.; Ripple, R.D.; Truck, S. The dynamics of returns on renewable energy companies: A state-space approach. Energy Econ. 2015, 48, 325–335. [Google Scholar] [CrossRef]

- Kumar, S.; Managi, S.; Matsuda, A. Stock prices of clean energy firms, oil and carbon markets: A vector autoregressive analysis. Energy Econ. 2012, 34, 215–226. [Google Scholar] [CrossRef]

- Managi, S.; Okimoto, T. Does the price of oil interact with clean energy prices in the stock market? Jpn. World Econ. 2013, 27, 1–9. [Google Scholar] [CrossRef] [Green Version]

- Maryniak, P.; Trück, S.; Weron, R. Carbon pricing and electricity markets—The case of the Australian Clean Energy Bill. Energy Econ. 2019, 79, 45–58. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Does it really pay to be green? Determinants and consequences of proactive environmental strategies. J. Account. Public Policy 2011, 30, 122–144. [Google Scholar] [CrossRef]

- Ruggiero, S.; Lehkonen, H. Renewable energy growth and the financial performance of electric utilities: A panel data study. J. Clean. Prod. 2017, 142, 3676–3688. [Google Scholar] [CrossRef] [Green Version]

- Sueyoshi, T.; Goto, M. Can environmental investment and expenditure enhance financial performance of US electric utility firms under the Clean Air Act amendment of 1990? Energy Policy 2009, 37, 4819–4826. [Google Scholar] [CrossRef]

- Telle, K. “It pays to be green”—A premature conclusion? Environ. Resour. Econ. 2006, 35, 195–220. [Google Scholar] [CrossRef]

- Pätäri, S.; Arminen, H.; Tuppura, A.; Jantunen, A. Competitive and responsible? The relationship between corporate social and financial performance in the energy sector. Renew. Sustain. Energy Rev. 2014, 37, 142–154. [Google Scholar] [CrossRef]

- Arslan-Ayaydin, Ö.; Thewissen, J. The financial reward for environmental performance in the energy sector. Energy Environ. 2016, 27, 389–413. [Google Scholar] [CrossRef]

- Sueyoshi, T.; Goto, M. Data envelopment analysis for environmental assessment: Comparison between public and private ownership in petroleum industry. Eur. J. Oper. Res. 2012, 216, 668–678. [Google Scholar] [CrossRef]

- Jamasb, T.; Pollitt, M.; Triebs, T. Productivity and eciency of US gas transmission companies: A European regulatory perspective. Energy Policy 2008, 36, 3398–3412. [Google Scholar] [CrossRef] [Green Version]

- Doumpos, M.; Andriosopoulos, K.; Galariotis, E.; Makridou, G.; Zopounidis, C. Corporate failure prediction in the European energy sector: A multicriteria approach and the e_ect of country characteristics. Eur. J. Oper. Res. 2017, 262, 347–360. [Google Scholar] [CrossRef]

- Bobinaite, V. Financial sustainability of wind electricity sectors in the Baltic States. Renew. Sustain. Energy Rev. 2015, 47, 794–815. [Google Scholar] [CrossRef]

- Halkos, G.E.; Tzeremes, N.G. Analyzing the Greek renewable energy sector: A Data Envelopment Analysis approach. Renew. Sustain. Energy Rev. 2012, 16, 2884–2893. [Google Scholar] [CrossRef]

- Paun, D. Sustainability and financial performance of companies in the energy sector in Romania. Sustainability 2017, 9, 1722. [Google Scholar] [CrossRef] [Green Version]

- Tomczak, S.K. Comparison of the Financial Standing of Companies Generating Electricity from Renewable Sources and Fossil Fuels: A New Hybrid Approach. Energies 2019, 12, 3856. [Google Scholar] [CrossRef] [Green Version]

- Rastogi, R.; Jaiswal, R.; Jaiswal, R.K. Renewable Energy Firm’s Performance Analysis Using Machine Learning Approach. Procedia Comput. Sci. 2020, 175, 500–507. [Google Scholar] [CrossRef]

- Tomczak, S.K.; Skowrońska-Szmer, A.; Szczygielski, J.J. Is Investing in Companies Manufacturing Solar Components a Lucrative Business? A Decision Tree Based Analysis. Energies 2020, 13, 499. [Google Scholar] [CrossRef] [Green Version]

- Ciarreta, A.; Espinosa, M.P.; Zarraga, A. Panel Data Analysis, Encyclopedia of Law and Economics; Springer: New York, NY, USA, 2019. [Google Scholar] [CrossRef]

- Ajmani, V.B. Panel Data Analysis; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2008. [Google Scholar] [CrossRef]

- Horbach, J. Determinants of environmental innovation—New evidence from German panel data sources. Res. Policy 2008, 37, 163–173. [Google Scholar] [CrossRef] [Green Version]

- Polzin, F.; Migendt, M.; Täube, F.A.; Flotow, P. Public policy influence on renewable energy investments—A panel data study across OECD countries. Energy Policy 2015, 80, 98–111. [Google Scholar] [CrossRef] [Green Version]

- Aparicio, S.; Urbano, D.; Audretsch, D. Institutional factors, opportunity entrepreneurship and economic growth: Panel data evidence. Technol. Forecast. Soc. Chang. 2016, 102, 45–61. [Google Scholar] [CrossRef] [Green Version]

- Zięba, M.; Tomczak, S.K.; Tomczak, J.M. Ensemble boosted trees with synthetic features generation in application to bankruptcy prediction. Expert Syst. Appl. 2016, 58, 93–101. [Google Scholar] [CrossRef]

- Larose, D.T. Discovering Knowledge in Data. An Introduction to Data Mining, Wiley-Interscience; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2005. [Google Scholar]

- Kass, G.V. An exploratory technique for investigating large quantities of categorical data. J. R. Stat. Soc. Ser. C 1980, 29, 119–127. [Google Scholar] [CrossRef]

- Breiman, L.; Friedman, J.; Olshen, R.; Stone, C. Classification and regression trees. Classif. Regres. Trees 2017, 37, 237–251. [Google Scholar]

- Altman, E.I.; Iwanicz-Drozdowska, M.; Laitinen, E.K.; Suvas, A. Financial distress prediction in an international context: A review and empirical analysis of Altman’s Z-score model. J. Int. Financ. Manag. Account. 2017, 28, 131–171. [Google Scholar] [CrossRef]

- Altman, E.I.; Hotchkiss, E. Corporate Financial Distress and Bankruptcy, 3rd ed.; John Wiley & Sons: Hoboken, NJ, USA, 2006. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| No. | Definition | No. | Definition |

|---|---|---|---|

| 1 | Net profit/total assets | 47 | (Inventory ∗ 365)/cost of goods sold |

| 2 | Total liabilities/total assets | 48 | EBITDA */total assets |

| 3 | Working capital/total assets | 49 | EBITDA */sales revenues |

| 4 | Current assets/short-term liabilities | 50 | Current assets/total liabilities |

| 5 | [(Cash + short-term securities + receivables-short-term liabilities) /(operating expenses-depreciation)] ∗ 365 | 51 | Short-term liabilities/total assets |

| 6 | Retained earnings/total assets | 52 | Short-term liabilities/operating expenses |

| 7 | Gross profit/total assets | 53 | Equity/fixed assets |

| 8 | Book value of equity/total liabilities | 54 | Constant capital/fixed assets |

| 9 | Total operating revenue/total assets | 55 | Working capital |

| 10 | Equity/total assets | 56 | (Total operating revenues-cost of goods sold)/total operating revenues |

| 11 | (Gross profit + financial expenses)/total assets | 57 | Net profit/equity |

| 12 | Gross profit/short-term liabilities | 58 | Long-term liabilities/equity |

| 13 | (Gross profit + depreciation)/sales revenues | 59 | Sales revenues/inventory |

| 14 | EBIT/total costs | 60 | Sales revenues/receivables |

| 15 | (Total liabilities ∗ 365)/(gross profit + depreciation) | 61 | (Short-term liabilities × 365)/sales revenues |

| 16 | (Gross profit + depreciation)/total liabilities | 62 | Sales revenues/short-term liabilities |

| 17 | Total assets/total liabilities | 63 | Sales/fixed assets |

| 18 | EBIT/total liabilities | 64 | (Current assets-inventory-short-term liabilities)/(total operating revenues-profit before income tax-depreciation) |

| 19 | Gross profit/sales revenues | 65 | Net profit/net cash flow from (used in) operating activities |

| 20 | (Inventory ∗ 365)/sales revenues | 66 | Depreciation/net cash flow from (used in) operating activities |

| 21 | Sales revenues (n)/sales revenues (n−1) | 67 | Net cash flow from (used in) operating activities/total assets |

| 22 | EBIT/total assets | 68 | Net cash flow from (used in) operating activities/income |

| 23 | Net profit/sales revenues | 69 | Net cash flow from (used in) operating activities/total liabilities |

| 24 | Gross profit (in 3 years)/total assets | 70 | Net cash flow from (used in) operating activities/long-term liabilities |

| 25 | (Equity-share capital)/total assets | 71 | Net cash flow from (used in) operating activities/short-term liabilities |

| 26 | (Net profit + depreciation)/total liabilities | 72 | Cash conversion cycle (X20 + X44 − X61) |

| 27 | Profit on operating activities/financial expenses | 73 | Net cash flow from (used in) operating activities/net increase (decrease) in cash and cash equivalents |

| 28 | Working capital/fixed assets | 74 | Net cash flow from (used in) operating activities/current assets |

| 29 | Logarithm of total assets | 75 | Net cash flow from (used in) operating activities/EBIT |

| 30 | (Total liabilities-cash)/sales revenues | 76 | Net profit per share |

| 31 | EBIT/equity | 77 | Income/outstanding shares |

| 32 | (Current liabilities ∗ 365)/cost of products sold | 78 | Net profit/outstanding shares |

| 33 | Operating expenses/short-term liabilities | 79 | Price per share/net profit per share |

| 34 | Operating expenses/total liabilities | 80 | Yearly dividend/price per share |

| 35 | Profit on sales/total assets | 81 | Market capitalization/book value |

| 36 | Total revenue/total assets | 82 | Market capitalization/gross profit |

| 37 | (Current assets-inventories)/long-term liabilities | 83 | Market capitalization/EBITDA |

| 38 | Constant capital/total assets | 84 | Market capitalization to EBIT |

| 39 | Profit on sales/sales revenues | 85 | Market capitalization to total assets |

| 40 | (Current assets-inventory-receivables)/short-term liabilities | 86 | Market capitalization/capital employed |

| 41 | Total liabilities/((profit on operating activities + depreciation) ∗(12/365)) | 87 | Enterprise value/sales revenues |

| 42 | EBIT/sales revenues | 88 | Enterprise value/gross profit |

| 43 | Rotation receivables + inventory turnover in days | 89 | Enterprise value/EBITDA * |

| 44 | (Receivables × 365)/sales | 90 | Enterprise value/EBIT |

| 45 | Net profit/inventory | 91 | Enterprise value/total assets |

| 46 | (Current assets-inventory)/short-term liabilities | 92 | Enterprise value/capital employed |

| Ratio | Min | Max | Mean | Standard Deviation | Coefficient of Variation |

|---|---|---|---|---|---|

| X1 | −0.44 | 0.33 | 0.03 | 0.09 | 2.96 |

| X2 | 0.17 | 0.81 | 0.50 | 0.17 | 0.34 |

| X3 | −0.15 | 0.62 | 0.23 | 0.16 | 0.71 |

| X4 | 0.49 | 5.81 | 1.84 | 0.94 | 0.51 |

| X5 | −304.41 | 502.54 | 33.53 | 130.79 | 3.90 |

| X6 | −1.31 | 0.51 | 0.06 | 0.26 | 4.52 |

| X7 | −0.43 | 0.41 | 0.04 | 0.09 | 2.33 |

| X8 | 0.24 | 5.01 | 1.35 | 1.09 | 0.81 |

| X9 | 0.23 | 5.91 | 1.12 | 1.02 | 0.91 |

| X10 | 0.19 | 0.83 | 0.50 | 0.17 | 0.34 |

| X11 | −0.43 | 0.42 | 0.05 | 0.10 | 1.87 |

| X12 | −0.96 | 1.71 | 0.16 | 0.35 | 2.12 |

| X13 | −0.55 | 0.68 | 0.12 | 0.15 | 1.29 |

| X14 | −1.26 | 0.29 | −0.08 | 0.17 | −2.11 |

| X15 | −92,233.72 | 55,938.31 | −5562.87 | 9223.37 | −1.66 |

| X16 | −0.50 | 1.69 | 0.24 | 0.31 | 1.28 |

| X17 | 1.24 | 6.01 | 2.35 | 1.09 | 0.47 |

| X18 | −0.37 | 0.98 | 0.12 | 0.24 | 1.90 |

| X19 | −0.69 | 0.54 | 0.05 | 0.14 | 2.82 |

| X20 | 11.35 | 190.43 | 51.81 | 31.63 | 0.61 |

| X21 | 0.41 | 2.66 | 1.05 | 0.25 | 0.24 |

| X22 | −0.26 | 0.40 | 0.04 | 0.08 | 1.81 |

| X23 | −0.69 | 0.43 | 0.03 | 0.13 | 3.60 |

| X24 | −15.46 | 4.94 | 0.29 | 1.70 | 5.79 |

| X25 | −1.29 | 0.68 | 0.27 | 0.29 | 1.08 |

| X26 | −0.51 | 1.58 | 0.21 | 0.28 | 1.33 |

| X27 | −2465.33 | 52.61 | −35.45 | 200.92 | −5.67 |

| X28 | −0.28 | 14.49 | 1.42 | 2.36 | 1.66 |

| X29 | 4.15 | 7.83 | 5.90 | 0.70 | 0.12 |

| X30 | −0.55 | 2.49 | 0.35 | 0.44 | 1.24 |

| X31 | −0.91 | 0.69 | 0.08 | 0.18 | 2.18 |

| X32 | −635.27 | −28.09 | −204.98 | 112.34 | −0.55 |

| X33 | 0.69 | 13.16 | 2.70 | 1.65 | 0.61 |

| X34 | 0.36 | 8.15 | 2.08 | 1.35 | 0.65 |

| X35 | −0.15 | 0.46 | 0.14 | 0.10 | 0.72 |

| X36 | 0.28 | 5.91 | 1.13 | 1.02 | 0.90 |

| X37 | 1.46 | 2128.44 | 39.92 | 173.24 | 4.34 |

| X38 | 0.24 | 0.90 | 0.61 | 0.17 | 0.28 |

| X39 | −0.21 | 0.60 | 0.17 | 0.14 | 0.86 |

| X40 | 0.07 | 3.53 | 0.90 | 0.74 | 0.82 |

| X41 | −4.00 | 6.09 | 0.22 | 0.76 | 3.43 |

| X42 | −0.38 | 0.53 | 0.05 | 0.11 | 2.12 |

| X43 | 48.25 | 296.01 | 133.42 | 50.25 | 0.38 |

| X44 | 12.75 | 185.25 | 81.61 | 35.36 | 0.43 |

| X45 | −13.79 | 6.87 | 0.29 | 1.74 | 5.99 |

| X46 | 0.35 | 4.10 | 1.26 | 0.78 | 0.62 |

| X47 | 9.98 | 198.45 | 55.49 | 33.91 | 0.61 |

| X48 | −0.30 | 0.44 | 0.09 | 0.09 | 0.95 |

| X49 | −0.53 | 0.68 | 0.13 | 0.15 | 1.17 |

| X50 | 0.23 | 4.63 | 1.40 | 0.74 | 0.53 |

| X51 | 0.10 | 0.76 | 0.39 | 0.17 | 0.45 |

| X52 | 0.08 | 1.46 | 0.47 | 0.23 | 0.49 |

| X53 | 0.41 | 14.05 | 2.09 | 2.24 | 1.07 |

| X54 | 0.72 | 15.49 | 2.42 | 2.36 | 0.98 |

| X55 | −9223.37 | 19,906,746.90 | 9223.37 | 9223.37 | 1.00 |

| X56 | 1.40 | 2.25 | 1.83 | 0.14 | 0.08 |

| X57 | −1.54 | 0.56 | 0.04 | 0.22 | 5.46 |

| X58 | 0.00 | 2.44 | 0.27 | 0.33 | 1.20 |

| X59 | 1.92 | 32.16 | 9.31 | 5.19 | 0.56 |

| X60 | 1.97 | 28.62 | 5.88 | 4.33 | 0.74 |

| X61 | 27.55 | 492.88 | 163.15 | 83.21 | 0.51 |

| X62 | 0.74 | 13.25 | 2.86 | 1.66 | 0.58 |

| X63 | 0.33 | 128.73 | 10.17 | 24.13 | 2.37 |

| X64 | −0.72 | 1.66 | 0.20 | 0.38 | 1.86 |

| X65 | −89.41 | 10.16 | −0.87 | 7.94 | −9.11 |

| X66 | −15.88 | 57.92 | 0.87 | 5.48 | 6.27 |

| X67 | −0.39 | 0.41 | 0.08 | 0.09 | 1.23 |

| X68 | −0.20 | 0.63 | 0.12 | 0.14 | 1.21 |

| X69 | −0.51 | 1.42 | 0.22 | 0.29 | 1.34 |

| X70 | −26.62 | 225.66 | 3.63 | 18.70 | 5.15 |

| X71 | −0.52 | 2.58 | 0.31 | 0.43 | 1.38 |

| X72 | −313.87 | 108.28 | −29.73 | 74.47 | −2.50 |

| X73 | −172.71 | 177.40 | 0.60 | 23.77 | 39.94 |

| X74 | −0.42 | 0.73 | 0.14 | 0.18 | 1.22 |

| X75 | −555.33 | 143.12 | 0.54 | 47.42 | 88.11 |

| X76 | −0.69 | 1.50 | 0.11 | 0.24 | 2.31 |

| X77 | 0.05 | 14.00 | 2.63 | 2.73 | 1.04 |

| X78 | −0.69 | 1.50 | 0.11 | 0.24 | 2.31 |

| X79 | −189.28 | 662.11 | 17.20 | 62.47 | 3.63 |

| X80 | 0.01 | 0.85 | 0.08 | 0.10 | 1.30 |

| X81 | 0.24 | 5.28 | 1.38 | 0.98 | 0.71 |

| X82 | −529.48 | 362.12 | 7.55 | 59.28 | 7.85 |

| X83 | −559.63 | 893.30 | 9.51 | 87.61 | 9.22 |

| X84 | −2480.13 | 460.32 | −6.82 | 232.80 | −34.13 |

| X85 | 0.09 | 3.15 | 0.69 | 0.60 | 0.87 |

| X86 | 0.15 | 4.62 | 1.12 | 0.82 | 0.73 |

| X87 | −0.01 | 5.69 | 1.06 | 0.99 | 0.94 |

| X88 | −1343.48 | 491.55 | 5.44 | 120.11 | 22.08 |

| X89 | −459.16 | 1755.95 | 15.92 | 146.84 | 9.22 |

| X90 | −3585.83 | 1554.44 | −0.99 | 362.67 | −365.49 |

| X91 | −0.02 | 2.73 | 0.74 | 0.52 | 0.70 |

| X92 | −0.03 | 4.36 | 1.25 | 0.79 | 0.63 |

| Observed | G | R | Percent Correct |

|---|---|---|---|

| G | 60 | 13 | 82.8% |

| R | 3 | 81 | 96.4% |

| Overall Percentage | 40.1% | 59.9% | 89.8% |

| Observed | G | R | Percent Correct |

|---|---|---|---|

| G | 58 | 15 | 79.5% |

| R | 7 | 77 | 91.7% |

| Overall Percentage | 41.4% | 58.6% | 86.0% |

| Partition | Observed | Predicted | ||

|---|---|---|---|---|

| 0 | 1 | Percent Correct | ||

| Training | 0 | 44 | 14 | 75.9% |

| 1 | 5 | 52 | 91.2% | |

| Overall Percent | 42.6% | 57.4% | 83.5% | |

| Holdout | 0 | 13 | 2 | 86.7% |

| 1 | 1 | 26 | 96.3% | |

| Overall Percent | 33.3% | 66.7% | 92.9% | |

| Ratio | Statistical Significance of Differences in the Values of Individual Ratios between Two Groups | Key Ratio * | ||||

|---|---|---|---|---|---|---|

| 2018 | 2017 | 2016 | 2015 | Panel Data | ||

| X29 | Yes | Yes | Yes | Yes | Yes | Yes |

| X53 | Yes | Yes | Yes | Yes | Yes | Yes |

| X55 | Yes | Yes | Yes | Yes | Yes | Yes |

| Ratio | CT | k-Nearest Neighbor | Altman | Student’s t-Test |

|---|---|---|---|---|

| X6 | Yes | – | Yes | No |

| X28 | Yes | – | – | No |

| X29 | No | – | – | Yes |

| X53 | No | – | – | Yes |

| X55 | Yes | – | – | Yes |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tomczak, S.K.; Skowrońska-Szmer, A.; Szczygielski, J.J. Is It Possible to Make Money on Investing in Companies Manufacturing Solar Components? A Panel Data Approach. Energies 2021, 14, 3406. https://doi.org/10.3390/en14123406

Tomczak SK, Skowrońska-Szmer A, Szczygielski JJ. Is It Possible to Make Money on Investing in Companies Manufacturing Solar Components? A Panel Data Approach. Energies. 2021; 14(12):3406. https://doi.org/10.3390/en14123406

Chicago/Turabian StyleTomczak, Sebastian Klaudiusz, Anna Skowrońska-Szmer, and Jan Jakub Szczygielski. 2021. "Is It Possible to Make Money on Investing in Companies Manufacturing Solar Components? A Panel Data Approach" Energies 14, no. 12: 3406. https://doi.org/10.3390/en14123406

APA StyleTomczak, S. K., Skowrońska-Szmer, A., & Szczygielski, J. J. (2021). Is It Possible to Make Money on Investing in Companies Manufacturing Solar Components? A Panel Data Approach. Energies, 14(12), 3406. https://doi.org/10.3390/en14123406