Application of Canonical Variate Analysis to Compare Different Groups of Food Industry Companies in Terms of Financial Liquidity and Profitability

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

3.1. The Data Collection

3.2. Financial Analyses

3.3. Statistical Analyses

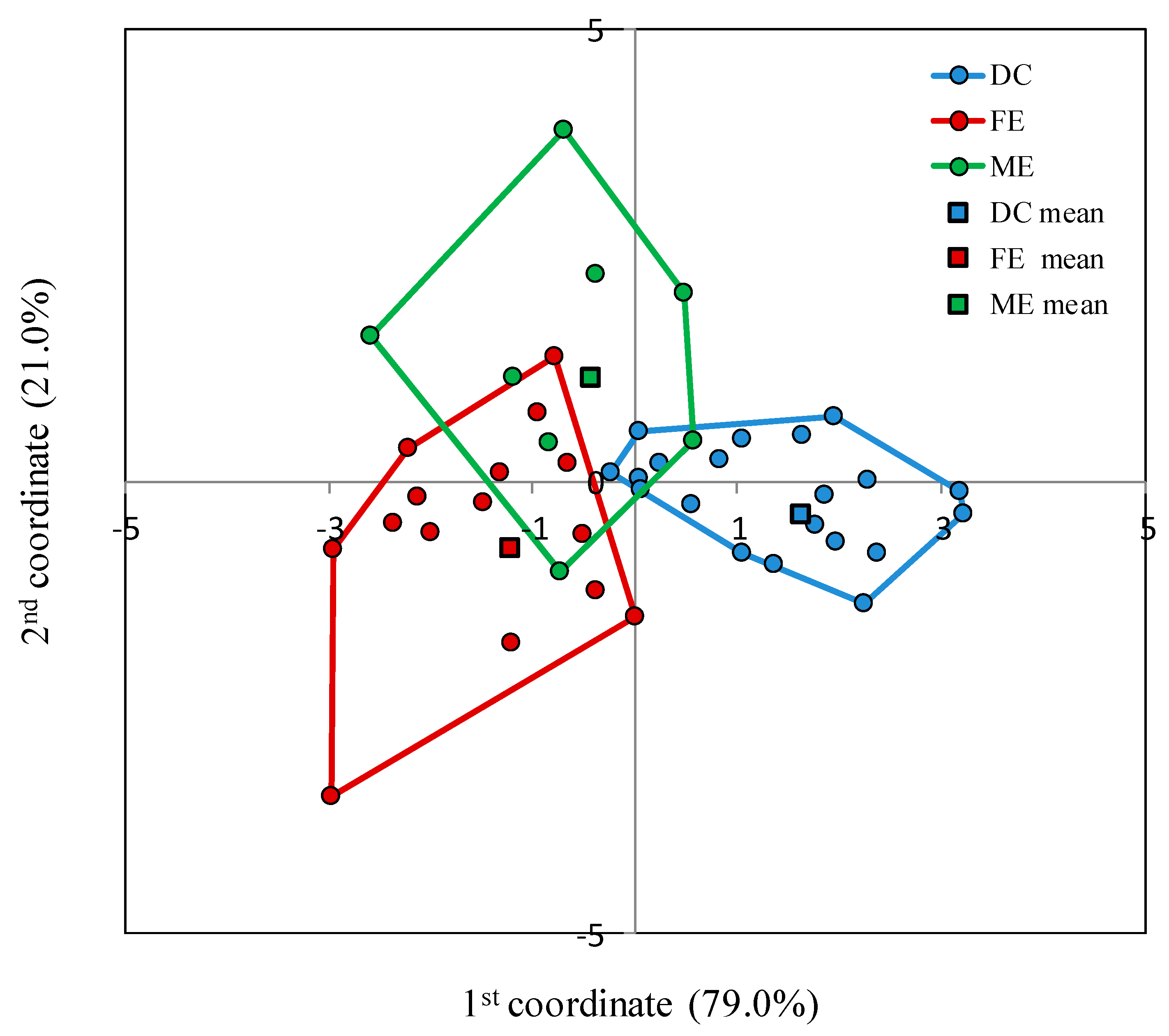

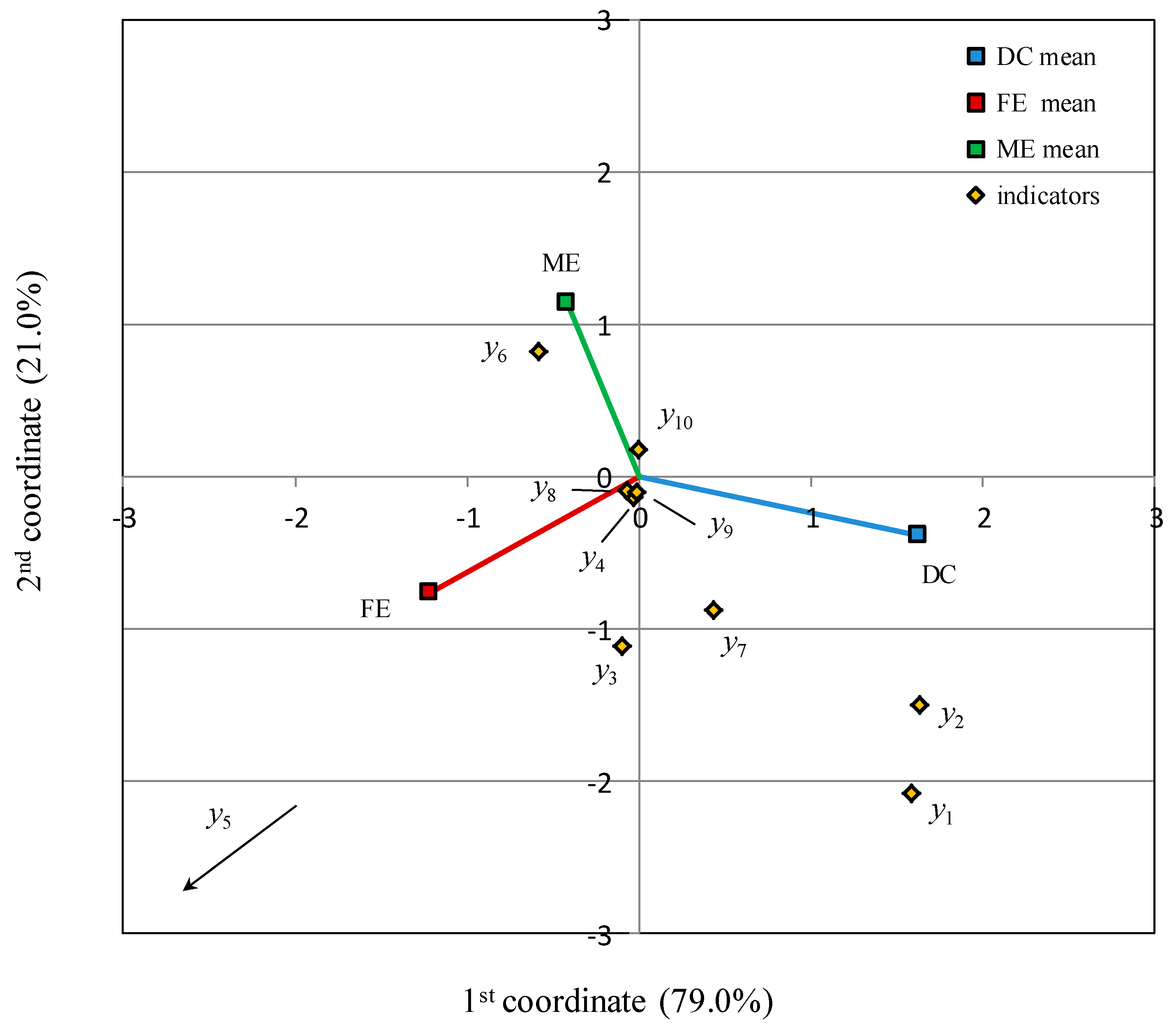

4. Results of Empirical Research

5. Discussion

6. Conclusions

- –

- Financial liquidity ratios are measures that better differentiate business companies compared to profitability ratios;

- –

- The cash conversion cycle was the most important differentiating feature in the group of studied firms;

- –

- The cash conversion cycle was reversely proportional to classical liquidity ratios (i.e., current ratio and quick ratio);

- –

- There was a negative relationship between liquidity measured by current ratio, quick ratio, shareholder equity ratio, and return on assets and equity. Such a direction of relationships was observed in the examined dairy cooperatives and meat companies;

- –

- In the case of feed companies, a positive relationship was observed between studied characteristics;

- –

- No significant relationship was observed between the cash conversion cycle, cash efficiency, and return rates.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Łuczka, W.; Kalinowski, S.; Shmygol, N. Organic Farming Support Policy in a Sustainable Development Context: A Polish Case Study. Energies 2021, 14, 4208. [Google Scholar] [CrossRef]

- Mioduchowska-Jaroszewicz, E. An Analysis of External Cash Flows of Capital Groups. Eur. Res. Stud. J. 2021, 24, 325–340. [Google Scholar] [CrossRef]

- Gentry, J.E. Management Perceptions of the Working Capital Process; Illinois College of Commerce and Business Administration, University of Illinois at Urbana-Champaign: Champaign, IL, USA, 1976; p. 65. Available online: www.archive.org/details/managementpercep352gent (accessed on 15 September 2011).

- Deloof, M. Does working capital management affect profitability of Belgian firms? J. Bus. Finan. Account. 2003, 30, 373–587. [Google Scholar] [CrossRef]

- Eljelly, A.M.A. Liquidity-profitability tradeoff: An empirical investigation in an emerging market. Int. J. Commer. Manag. 2004, 14, 48–61. [Google Scholar] [CrossRef]

- Lazaridis, I.; Tryfonidis, D. The relationship between working capital management and profitability of listed companies in the Athens Stock Exchange. J. Financ. Manag. Anal. 2006, 19, 26–35. [Google Scholar]

- Mensch, G. Finanz-Controlling. Finanzplanung und Kontrolle. Controlling zur Finanziellen Unternehmungsfűhrung, 2nd ed.; Oldenburg Verlag: München, Germany, 2008; p. 417. [Google Scholar]

- Ramachandran, A.; Janakiraman, M. The Relationship between Working Capital Management Efficiency and EBIT. Manag. Glob. Transit. 2009, 7, 61–74. [Google Scholar]

- Bolek, M.; Wiliński, W. The influence of liquidity on profitability of polish construction sector companies. Financ. Int. Q. 2012, 8, 38–52. [Google Scholar]

- Kandpal, V.; Kavidayal, P.C. Implication of working capital management on the profitability: A case of ONGC LTD, India. Commer. Manag. 2013, 4, 49–53. [Google Scholar] [CrossRef]

- Jaworski, J.; Czerwonka, L.; Mądra-Sawicka, M. The relationship between profitability and financial liquidity in food manufacturing industry in Poland. Ann. Pol. Assoc. Agric. Aribus. Econ. 2018, 20, 41–51. [Google Scholar]

- Czerwińska-Kayzer, D. Use of Cash Flow in Assessing the Attainment of the Enterprise’s Fundamental Financial Objectives; Poznań University of Life Sciences: Poznań, Poland, 2018; p. 275. [Google Scholar]

- Kobika, R. Liquidity management and profitability: A case study analysis of listed manufacturing companies in Sri Lanka. Global Sci. J. 2018, 6, 484–494. [Google Scholar]

- Gołaś, Z. Impact of working capital management on business profitability: Evidence from the Polish dairy industry. Agric. Econ. Czech 2020, 66, 278–285. [Google Scholar] [CrossRef]

- Firlej, K. Food Industry in Poland. New Path of Development; PWN: Warszawa, Poland, 2018; p. 382. [Google Scholar]

- Gazdecki, M.; Leszczyński, G.; Zieliński, M. Food Sector as an Interactive Business World: A Framework for Research on Innovations. Energies 2021, 14, 3312. [Google Scholar] [CrossRef]

- Florek, J.; Stanisławska, J.; Czerwinska-Kayzer, D. The financial situation of the food industry in Poland in comparision with 2005 and 2010. Ann. Pol. Assoc. Agric. Agribus. Econ. 2015, 17, 41–48. [Google Scholar]

- Czerwinska-Kayzer, D.; Florek, J.; Stanisławska, J. Assessment of the financial situation of food industry in Poland in 2005 and 2010. Acta Sci. Pol. Oecon. 2014, 13, 43–54. [Google Scholar]

- Pawłowski, K.P.; Czubak, W.; Zmyślona, J. Regional Diversity of Technical Efficiency in Agriculture as a Results of an Overinvestment: A Case Study from Poland. Energies 2021, 14, 3357. [Google Scholar] [CrossRef]

- Odrowaz-Coates, A. Definitions of Sustainability in the Context of Gender. Sustainability 2021, 13, 6862. [Google Scholar] [CrossRef]

- Bielski, S.; Zielińska-Chmielewska, A.; Marks-Bielska, R. Use of Environmental Management Systems and Renewable Energy Sources in Selected Food Processing Enterprises in Poland. Energies 2021, 14, 3212. [Google Scholar] [CrossRef]

- Cyrek, M.; Cyrek, P. Does Economic Structure Differentiate the Achievements towards Energy SDG in the EU? Energies 2021, 14, 2229. [Google Scholar] [CrossRef]

- Collins, R.D.; Selin, N.E.; De Weck, O.L.; Clark, W.C. Using inclusive wealth for policy evaluation: Application to electricity infrastructure planning in oil-exporting countries. Ecol. Econ. 2017, 133, 23–34. [Google Scholar] [CrossRef] [Green Version]

- Zimon, G. Financial Liquidity Management Strategies in Polish Energy Companies. Int. J. Energy Econ. Policy 2020, 10, 365–368. [Google Scholar] [CrossRef]

- Dang, H.T. Determinants of Liquidity of Listed Enterprises: Evidence from Vietnam. J. Asian Financ. Econ. Bus. 2020, 7, 67–73. [Google Scholar] [CrossRef]

- Zimon, G.; Zimon, D. The Impact of Purchasing Group on the Profitability of Companies Operating in the Renewable Energy Sector—The Case of Poland. Energies 2020, 13, 6588. [Google Scholar] [CrossRef]

- Enqvist, J.; Graham, M.; Nikkinen, J. The impact of working capital management on firm profitability in different business cycles: Evidence from Finland. Res. Int. Bus. Financ. 2014, 32, 36–49. [Google Scholar] [CrossRef]

- Ukaegbu, B. The significance of working capital management in determining firm profitability: Evidence from developing economies in Africa. Res. Int. Bus. Financ. 2014, 31, 1–16. [Google Scholar] [CrossRef]

- Hosaka, T. Bankruptcy prediction using imaged financial ratios and convolutional neural networks. Expert Syst. Appl. 2019, 117, 287–299. [Google Scholar] [CrossRef]

- Ajanthan, A. A nexus between liquidity and profitability: A study of trading companies in Sri Lanka. Eur. J. Manag. Bus. Econ. 2013, 5, 221–237. [Google Scholar]

- Hamid, K.; Akhi, R.A. Liquidity and profitability trade-off in pharmaceuticals and chemicals sector of Bangladesh. Int. J. Sci. Res. 2016, 5, 410–423. [Google Scholar]

- Mitra, S.; Kartik, C.N. Linkage between liquidity, risk and profitability: A study with reference to Eastern Coalfields Ltd. J. Inst. Public Enterp. 2013, 36, 29–48. [Google Scholar]

- Gołaś, Z.; Bieniasz, A.; Czerwińska-Kayzer, D. Working Capital Management in the Food Industry. Zagadnienia Ekon. Rolnej 2011, 3, 78–98. [Google Scholar]

- Gołaś, Z.; Bieniasz, A.; Czerwińska-Kayzer, D. The relationship between working capital and profitability in food industry firms in Poland. J. Cent. Eur. Agric. 2013, 14, 52–63. [Google Scholar] [CrossRef] [Green Version]

- Jaworski, J.; Czerwonka, L. Determinants of Enterprises’ Capital Structure in Energy Industry: Evidence from European Union. Energies 2021, 14, 1871. [Google Scholar] [CrossRef]

- Brealy, R.A.; Myres, S.C. Fundamentals of Corporate Finance; PWN: Warszawa, Poland, 1999; p. 195. [Google Scholar]

- Niresh, J.A. Trade-off between liquidity & profitability: A study of selected manufacturing firms in Sri Lanka. J. Arts Sci. Commer. 2012, 3, 34–40. [Google Scholar]

- Jerzak, M.A.; Śmiglak-Krajewska, M. Globalization of the Market for Vegetable Protein Feed and Its Impact on Sustainable Agricultural Development and Food Security in EU Countries Illustrated by the Example of Poland. Sustainability 2020, 12, 888. [Google Scholar] [CrossRef] [Green Version]

- Szczepanik, I.; Firlej, K. Food Industry—Macro-Environment, Investments, Foreign Expansion; Foundation of the University of Economics: Kraków, Poland, 2015; p. 247. [Google Scholar]

- Florek, J.; Czerwińska-Kayzer, D. Financial efficiency of the industry producing fodder in Comparison with other food industry sectors. In Proceedings of the 2018 International Conference Economic Science for Rural Development, Riga, Latvia, 9–11 May 2018; Volume 49, pp. 1691–3078. [Google Scholar]

- Malak-Rawlikowska, A.; Gębska, M.; Hoste, R.; Leeb, C.; Montanari, C.; Wallace, M.; de Roest, K. Developing a Methodology for Aggregated Assessment of the Economic Sustainability of Pig Farms. Energies 2021, 14, 1760. [Google Scholar] [CrossRef]

- Pitera, R. Financial Ratios as a Source of Information about the Company’s Financial Condition; Silva Rerum: Poznań, Poland, 2015; p. 112. [Google Scholar]

- Panova, E. Determinants of capital structure in Russian small and medium manufacturing enterprises. Equilibrium. Q. J. Econ. Econ. Policy 2020, 15, 361–375. [Google Scholar]

- Kirkham, R. Liquidity analysis using cash flow ratios and traditional ratios: The telecommunications sector in Australia. J. New Bus. Ideas Trends 2012, 10, 1–13. [Google Scholar]

- Atieh, S.H. Liquidity Analysis Using Cash Flow Ratios as Compared to Traditional Ratios in the Pharmaceutical Sector in Jordan. Int. J. Financ. Res. 2014, 5, 146–158. [Google Scholar] [CrossRef] [Green Version]

- Cheng, C.S.; Liu, C.; Schaefer, T. Earnings permanence and the incremental information content of cash flow from operations. J. Account. Res. 1996, 34, 173–181. [Google Scholar] [CrossRef]

- Cheng, C.S. The incremental information content of earnings and cash flow from operations affected by their extremity. J. Bus. Financ. Account. 2003, 30, 73–116. [Google Scholar] [CrossRef]

- Sharma, D.S. The role of cash flow information in predicting corporate failure: The state of the literature. Financ. Manag. 2001, 27, 3–28. [Google Scholar] [CrossRef]

- Mills, J.; Yamamura, J. The power of cash flow ratios. J. Account. 1998, 186, 53–62. [Google Scholar]

- Barua, S.; Saha, A.K. Traditional Ratios vs. Cash Flow based Ratios: Which One is Better Performance Indicator? Adv. Econ. Bus. 2015, 3, 232–251. [Google Scholar] [CrossRef]

- Jagels, M.G.; Coltman, M.M. Hospitality Management Accounting, 8th ed.; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2004; p. 612. [Google Scholar]

- Giacomino, D.E.; Mielke, D. Cash flow: Another approach to ratio analysis. J. Account. 1993, 175, 55–58. [Google Scholar]

- Czerwińska-Kayzer, D.; Florek, J.; Kayzer, D. Canonical variate analysis applied to determine factors influencing the financial situation of feed enterprises. Ann. Pol. Assoc. Agric. Aribus. Econ. 2020, 22, 21–31. [Google Scholar] [CrossRef]

- Richards, V.D.; Laughlin, E.J. A Cash Conversion Cycle Approach to Liquidity Analysis. Financ. Manag. 1980, 9, 32–38. [Google Scholar] [CrossRef]

- Bieniasz, A.; Czerwińska-Kayzer, D. The length of cash conversion cycle—Result of different construction ratios. Rocz. Akad. Rol. Pozn. 2008, 7, 36–45. [Google Scholar]

- Kramoliš, J.; Dobeš, K. Debt as a financial risk factor in SMEs in the Czech Republic. Equilibrium. Q. J. Econ. Econ. Policy 2020, 15, 87–105. [Google Scholar]

- Kajananthan, R.; Velnampy, T. Liquidity, solvency and profitability analysis using cash flow ratios and traditional ratios: The telecommunication sector in Sri Lanka. Res. J. Financ. Account. 2014, 5, 163–171. [Google Scholar]

- Preiβler, P.R. Beriebswirtschaftliche Kennzahlen. Formeln, Aussagekraft, Sollwere, Ermittlungsintervalle; Oldenbourg Wissenschaftsverlag: München, Germany, 2008; p. 331. [Google Scholar]

- Robinson, T.; Henry, E.; Pirie, W.; Broihahn, M. International Financial Statement Analysis, 3rd ed.; John Wiley & Sons Inc.: Hoboken, NJ, USA, 2015; p. 1072. [Google Scholar]

- Kamar, K. Analysis of the Effect of Return on Equity (Roe) and Debt to Equity Ratio (Der) On Stock Price on Cement Industry Listed In Indonesia Stock Exchange (Idx) In the Year of 2011–2015. Int. J. Bus. Manag. 2017, 19, 66–76. [Google Scholar] [CrossRef]

- Campbell, N.A.; Atchley, W.R. The geometry of canonical variate analysis. Syst. Biol. 1981, 30, 268–280. [Google Scholar] [CrossRef]

- Mitteroecker, P.; Bookstein, F. Linear discrimination, ordination, and the visualization of selection gradients in modern morphometrics. Evol. Biol. 2011, 38, 100–114. [Google Scholar] [CrossRef]

- Xagoraris, M.; Revelou, P.-K.; Alissandrakis, E.; Tarantilis, P.A.; Pappas, C.S. The Use of Right Angle Fluorescence Spectroscopy to Distinguish the Botanical Origin of Greek Common Honey Varieties. Appl. Sci. 2021, 11, 4047. [Google Scholar] [CrossRef]

- Krzanowski, W.J. Principles of Multivariate Analysis: A User’s Perspective, 2nd ed.; Oxford University Press: New York, NY, USA, 2000; p. 608. [Google Scholar]

- Martinet, J.-P.; Ferté, H.; Sientzoff, P.; Krupa, E.; Mathieu, B.; Depaquit, J. Wing Morphometrics of Aedes Mosquitoes from North-Eastern France. Insects 2021, 12, 341. [Google Scholar] [CrossRef]

- Staniszewski, R.; Frankowski, P.; Kayzer, D.; Zbierska, J.; Achtenberg, K. Reconstruction of Ancient Lake After Peat Excavation—A Case Study About Water Quality. Appl. Sci. 2021, 11, 4213. [Google Scholar] [CrossRef]

- Lejeune, M.; Caliński, T. Canonical analysis applied to multivariate analysis of variance. J. Multivar. Anal. 2000, 72, 100–119. [Google Scholar] [CrossRef] [Green Version]

- Kayzer, D.; Borowiak, K.; Budka, A.; Zbierska, J. Study of interaction in bioindication research on tobacco plant injuries caused by ground level ozone. Environmetrics 2009, 20, 666–675. [Google Scholar] [CrossRef]

- Kayzer, D.; Frankowski, P.; Zbierska, J.; Staniszewski, R. Evaluation of trophic parameters in newly built reservoir using canonical variates analysis. In Proceedings of the XLVIII Seminar of Applied Mathematics, Boguszów-Gorce, Poland, 9–11 September 2018; Volume 23, p. 00019. [Google Scholar]

- Kayzer, D. A Note on testing hypotheses concerning interaction with special reference to a graphical presentation in the space of canonical variates. Biom. Lett. 2019, 56, 89–104. [Google Scholar] [CrossRef] [Green Version]

- Sierpińska, M.; Jachna, T. Assessment of Enterprises According to World Standards; PWN: Warszawa, Poland, 2007; p. 406. [Google Scholar]

- Sukiennik, M. The analysis of mining company liquidity indicators. J. Min. Geoengin. 2012, 36, 339–344. [Google Scholar]

- Tóth, M.; Čierna, Z.; Serenčéš, P. Benchmark values for liquidity ratios in Slovak agriculture. Acta Sci. Pol. Oecon. 2013, 12, 83–90. [Google Scholar]

- McGowan, C.B.; Stambaugh, A.R. Using disaggregated return on assets to conduct a financial analysis of a commercial bank using an extension of the DuPont system of financial analysis. Account. Financ. Res. 2012, 1, 24–29. [Google Scholar] [CrossRef]

- Doorasamy, M. Using DuPont analysis to assess the financial performance of the top 3 JSE listed companies in the food industry. Invest. Manag. Financ. Innov. 2016, 13, 29–44. [Google Scholar] [CrossRef] [Green Version]

- Gołaś, Z. The effect of inventory management on profitability: Evidence from the Polish food industry: Case study. Agric. Econ. Czech 2020, 66, 234–242. [Google Scholar] [CrossRef]

- Kuś, A.; Grego-Planer, D. A Model of Innovation Activity in Small Enterprises in the Context of Selected Financial Factors: The Example of the Renewable Energy Sector. Energies 2021, 14, 2926. [Google Scholar] [CrossRef]

- Kovacova, M.; Kliestik, T. Logit and Probit application for the prediction of bankruptcy in Slovak companies. Equilib. Q. J. Econ. Econ. Policy 2017, 12, 775–791. [Google Scholar] [CrossRef]

- Prado, J.W.; Carvalho, F.M.; Benedicto, G.C.; Lima, A.L.R. Analysis of credit risk faced by public companies in Brazil: An approach based on discriminant analysis, logistic regression and artificial neural networks. Estud. Gerenc. 2019, 35, 347–360. [Google Scholar] [CrossRef]

- Papana, A.; Spyridou, A. Bankruptcy Prediction: The Case of the Greek Market. Forecasting 2020, 2, 505–525. [Google Scholar] [CrossRef]

- Żelazny, R.; Pietrucha, J. Measuring innovation and institution: The creative economy index. Equilib. Q. J. Econ. Econ. Policy 2017, 12, 43–62. [Google Scholar] [CrossRef]

- Svabova, L.; Michalkova, L.; Durica, M.; Nica, E. Business Failure Prediction for Slovak Small and Medium-Sized Companies. Sustainability 2020, 12, 4572. [Google Scholar] [CrossRef]

- Korol, T. Examining Statistical Methods in Forecasting Financial Energy of Households in Poland and Taiwan. Energies 2021, 14, 1821. [Google Scholar] [CrossRef]

- Wieprow, J.; Gawlik, A. The Use of Discriminant Analysis to Assess the Risk of Bankruptcy of Enterprises in Crisis Conditions Using the Example of the Tourism Sector in Poland. Risks 2021, 9, 78. [Google Scholar] [CrossRef]

- Saleem, Q.; Rehman, R.U. Impacts of liquidity ratios on profitability (case of oil and gas companies of Pakistan). Interdiscip. J. Res. Bus. 2011, 1, 95–98. [Google Scholar]

- Mendoza, R.R. Financial performance of micro, small and medium enterprises (MSMES) in the Philippines. Int. J. Bus. Financ. Res. 2015, 9, 67–80. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Name of the Indicator | Mark | The Formula of the Indicator |

|---|---|---|

| Current ratio | y1 | |

| Quick ratio | y2 | |

| Cash flow sufficiency ratio | y3 | |

| Cash flow to sale | y4 | |

| Cash conversion cycle | y5 | = |

| Total debt ratio | y6 | |

| Shareholder equity ratio | y7 | |

| Gross profit margin | y8 | |

| Return on assets | y9 | |

| Return on equity | y10 |

| Statistics | y1 | y2 | y3 | y4 (%) | y5 (day) | y6 (%) | y7 (%) | y8 (%) | y9 (%) | y10 (%) |

|---|---|---|---|---|---|---|---|---|---|---|

| DC | ||||||||||

| minimum | 1.04 | 0.67 | 0.00 | 0.0 | −4 | 13.2 | 34.8 | −3.2 | 0.1 | 0.1 |

| maximum | 4.46 | 3.11 | 1.43 | 11.6 | 47 | 57.8 | 78.8 | 7.5 | 22.6 | 32.1 |

| mean | 1.94 | 1.48 | 0.34 | 3.7 | 17 | 37.0 | 54.3 | 1.6 | 4.8 | 8.2 |

| standard deviation | 0.75 | 0.61 | 0.32 | 2.8 | 13 | 12.1 | 11.8 | 2.6 | 5.4 | 8.1 |

| FE | ||||||||||

| minimum | 0.57 | 0.20 | −0.18 | −4.1 | −18 | 11.5 | 4.9 | −0.8 | −5.3 | −32.0 |

| maximum | 3.06 | 2.21 | 1.74 | 23.0 | 86 | 84.0 | 87.4 | 20.2 | 17.7 | 27.6 |

| mean | 1.51 | 1.01 | 0.42 | 5.1 | 40 | 52.1 | 43.7 | 4.2 | 5.6 | 7.4 |

| standard deviation | 0.63 | 0.52 | 0.54 | 6.3 | 30 | 22.4 | 21.6 | 5.0 | 6.1 | 17.0 |

| ME | ||||||||||

| minimum | 0.95 | 0.44 | 0.00 | −0.2 | −5 | 32.7 | 12.0 | −1.6 | −6.1 | −18.9 |

| maximum | 1.87 | 1.36 | 0.71 | 6.5 | 45 | 88.0 | 64.2 | 4.0 | 9.7 | 41.1 |

| mean | 1.20 | 0.84 | 0.17 | 1.8 | 22 | 64.6 | 28.6 | 1.6 | 3.1 | 11.2 |

| standard deviation | 0.30 | 0.30 | 0.24 | 2.4 | 14 | 18.0 | 15.2 | 1.8 | 4.6 | 15.8 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Czerwińska-Kayzer, D.; Florek, J.; Staniszewski, R.; Kayzer, D. Application of Canonical Variate Analysis to Compare Different Groups of Food Industry Companies in Terms of Financial Liquidity and Profitability. Energies 2021, 14, 4701. https://doi.org/10.3390/en14154701

Czerwińska-Kayzer D, Florek J, Staniszewski R, Kayzer D. Application of Canonical Variate Analysis to Compare Different Groups of Food Industry Companies in Terms of Financial Liquidity and Profitability. Energies. 2021; 14(15):4701. https://doi.org/10.3390/en14154701

Chicago/Turabian StyleCzerwińska-Kayzer, Dorota, Joanna Florek, Ryszard Staniszewski, and Dariusz Kayzer. 2021. "Application of Canonical Variate Analysis to Compare Different Groups of Food Industry Companies in Terms of Financial Liquidity and Profitability" Energies 14, no. 15: 4701. https://doi.org/10.3390/en14154701

APA StyleCzerwińska-Kayzer, D., Florek, J., Staniszewski, R., & Kayzer, D. (2021). Application of Canonical Variate Analysis to Compare Different Groups of Food Industry Companies in Terms of Financial Liquidity and Profitability. Energies, 14(15), 4701. https://doi.org/10.3390/en14154701