Electricity Day-Ahead Market Conditions and Their Effect on the Different Supervised Algorithms for Market Price Forecasting †

,

,

Abstract

:1. Introduction

2. Literature Review

3. Market Conditions

3.1. Brief Description of the Nature of Electricity Markets

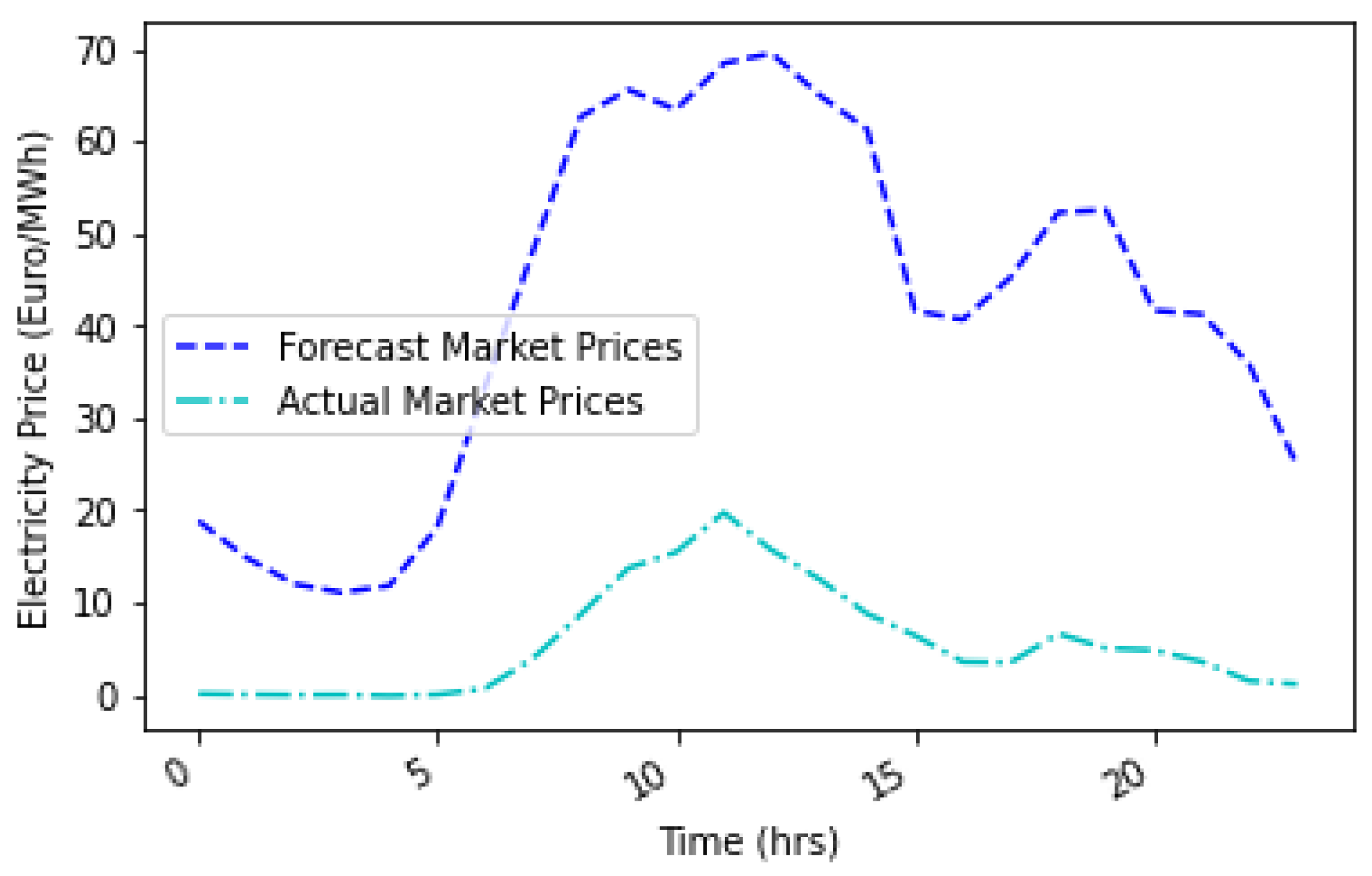

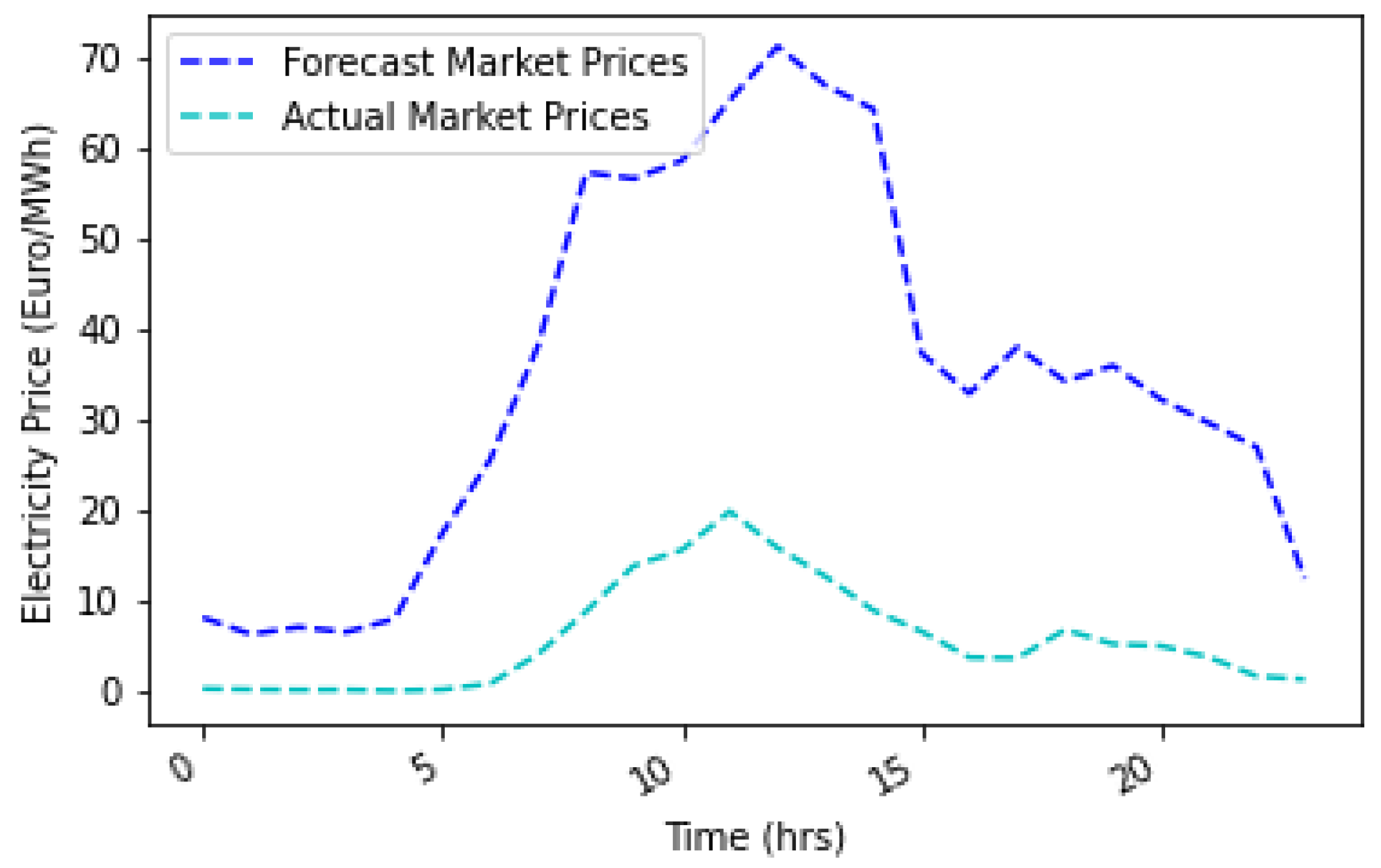

3.2. Day-Ahead German and Finnish Markets: Exploratory Analysis

3.3. Normal Market Price Range Determination

4. Supervised Algorithms for Market Price Forecasting

4.1. Extreme Learning Machine (ELM) Model

4.2. Artificial Neural Network (ANN) Model

4.3. Extreme Gradient Boosting (XGBoost) Model

4.4. Random Forest (RF) Model

4.5. Bootstrap Method

4.6. Description of the Training Process

5. Results

5.1. Comparison of the Proposed Methodologies

5.2. Forecasting Results for Each Class

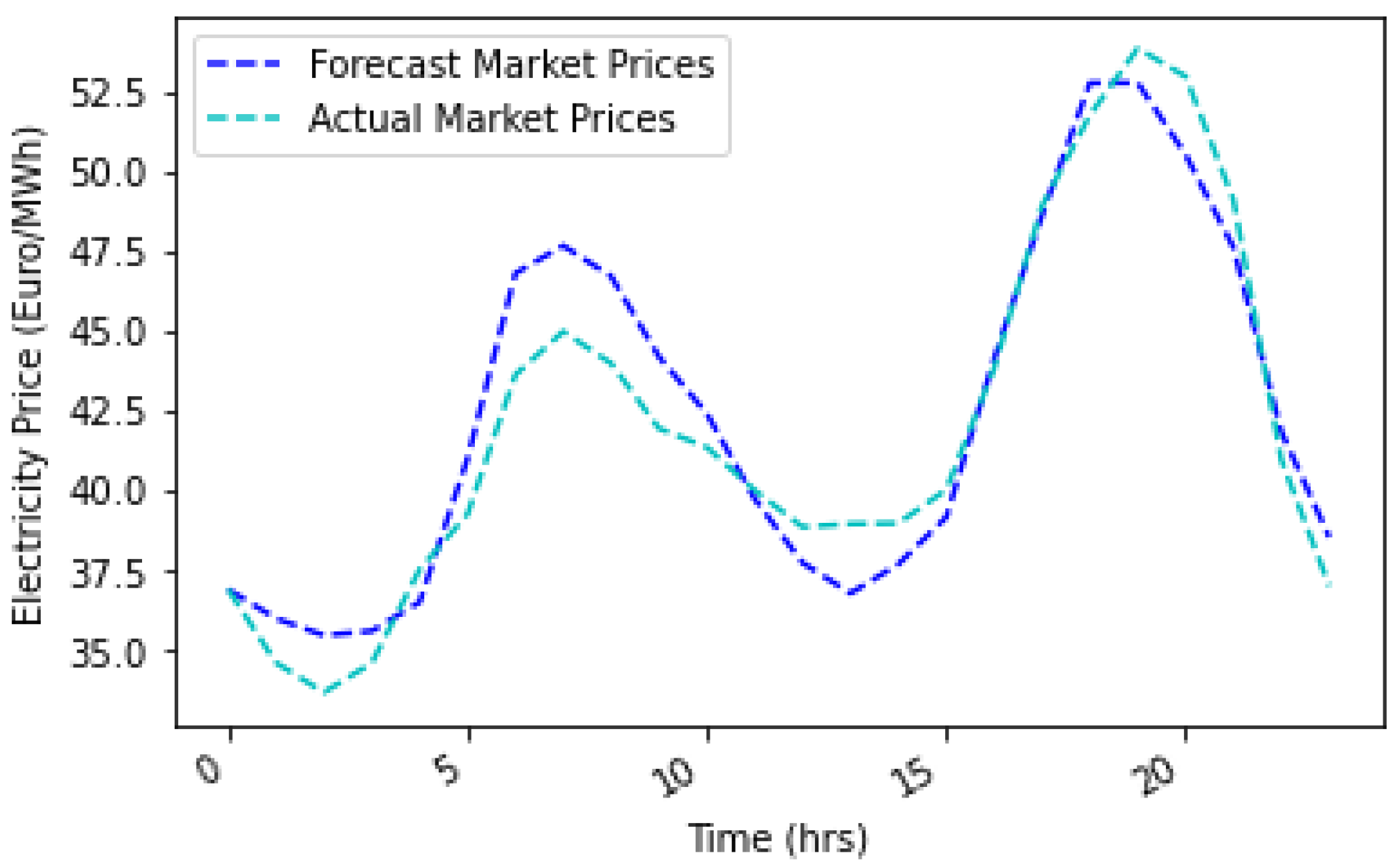

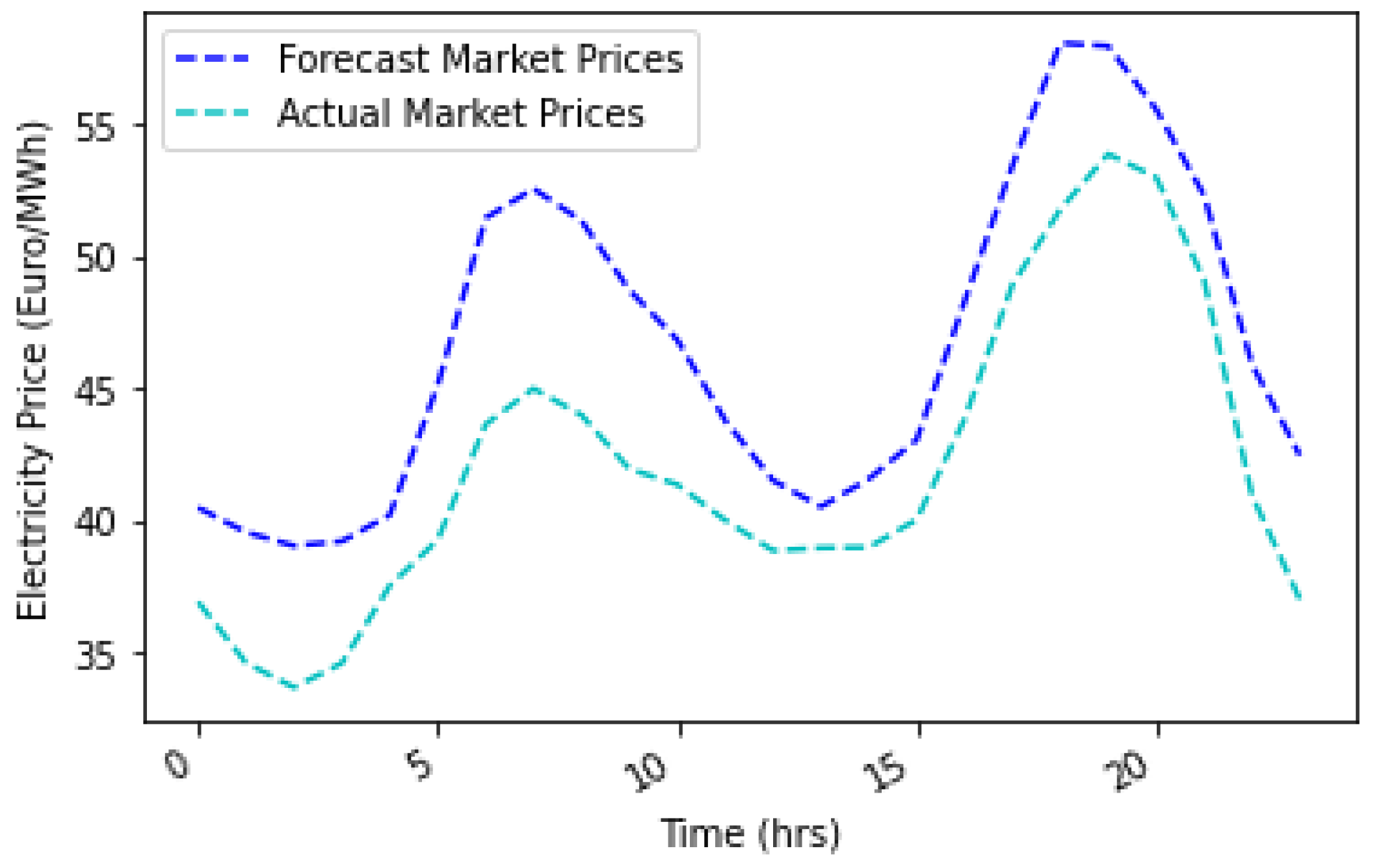

5.2.1. Normal Market Price Class

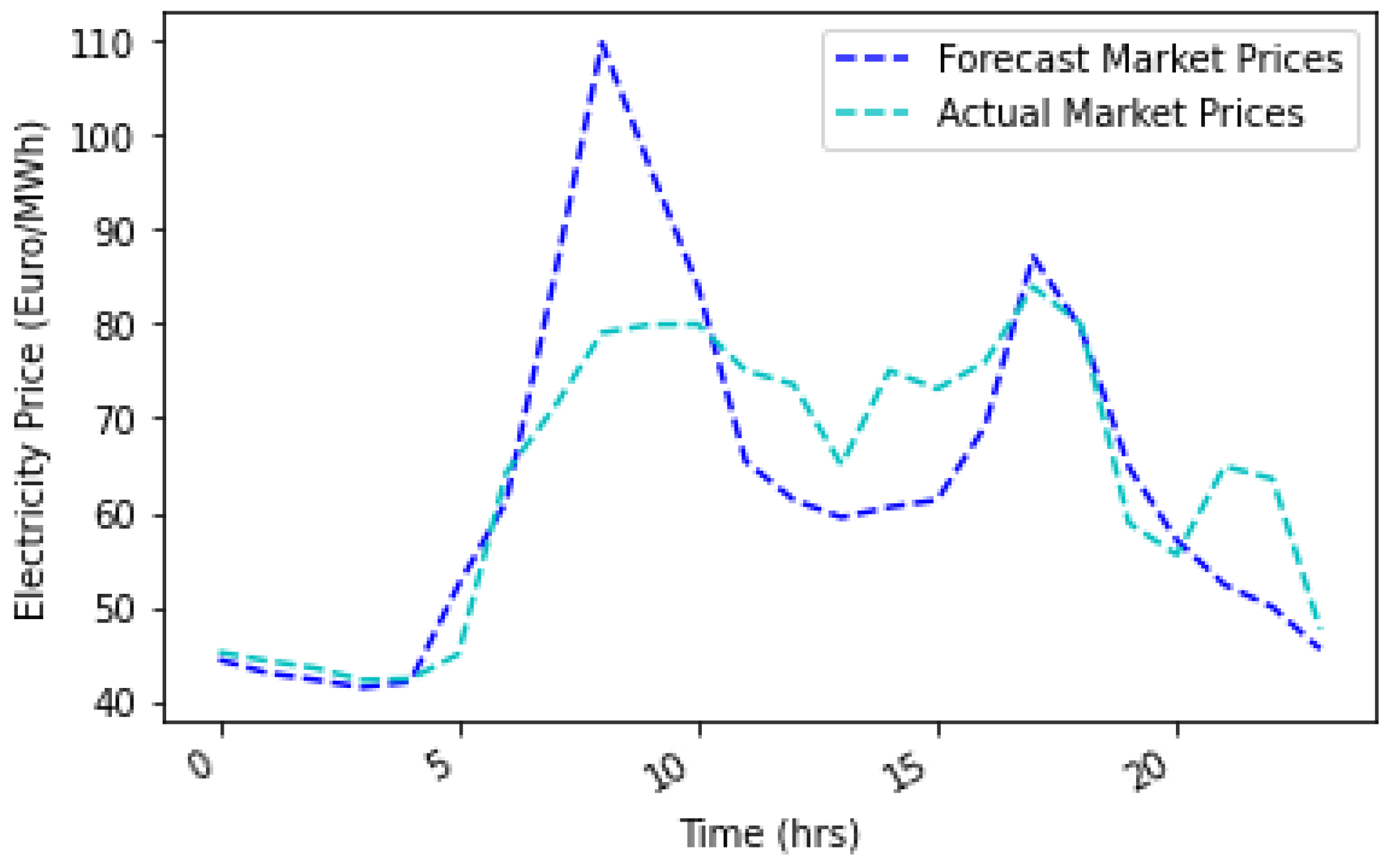

5.2.2. Extremely High Market Price Class

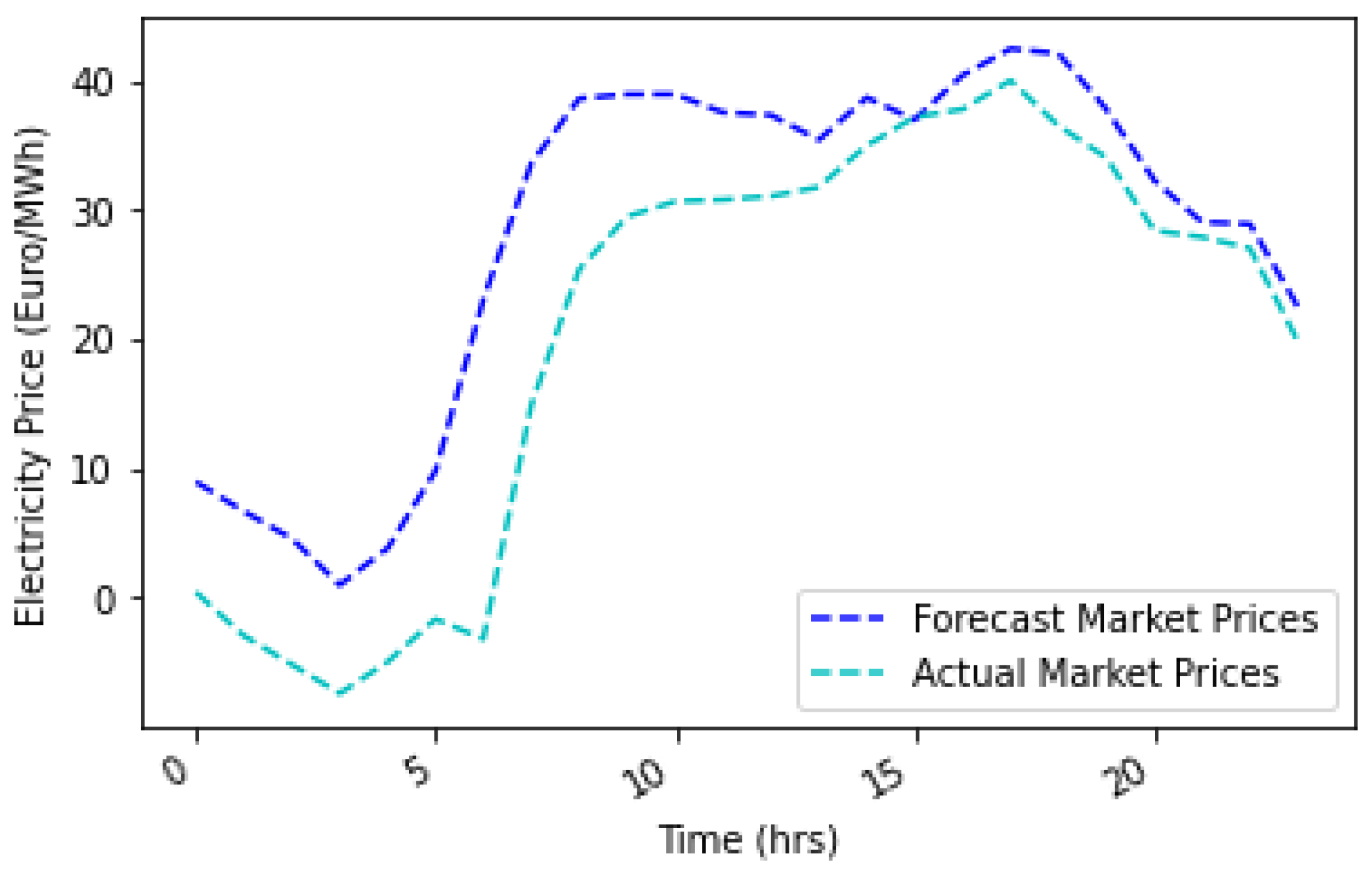

5.2.3. Negative Market Price Class

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| DA | Day-Ahead |

| MCP | Market Clearing Price |

| SMP | System Marginal Price |

| PaB | Pay-as-Bid |

| TSO | Transmission System Operator |

| COVID | Coronavirus Disease |

| ANN | Artificial neural Network |

| ELM | Extreme Learning Machine |

| XGBoost | Extreme Gradient Boosting |

| RF | Random Forest |

| FCM | Fuzzy C-Mean |

| RNN | Recurrent Neural Network |

| SVM | Support vector Machine |

| PNN | Probabilistic Neural Network |

| HNES | Hybrid Neuro Evolutionary System |

| CART | Classification and Regression Type |

| MAE | Mean Absolute Error |

| RMSE | Root Mean Square Error |

References

- Bichler, M.; Buhl, H.U.; Knörr, J.; Maldonado, F.; Schott, P.; Waldherr, S.; Weibelzahl, M. Electricity Markets in a Time of Change: A Call to Arms for Business Research. Schmalenbach J. Bus. Res. 2022, 74, 77–102. [Google Scholar] [CrossRef]

- Bao, M.; Ding, Y.; Zhou, X.; Guo, C.; Shao, C. Risk assessment and management of electricity markets: A review with suggestions. CSEE J. Power Energy Syst. 2021, 7, 1322–1333. [Google Scholar] [CrossRef]

- Wang, P.; Billinton, R. Reliability assessment of a restructured power system using reliability network equivalent techniques. IET 2003, 150, 555–560. [Google Scholar] [CrossRef]

- Zhao, Q.; Wang, P.; Goel, L.; Ding, Y. Impacts of renewable energy penetration on nodal price and nodal reliability in deregulated power system. In Proceedings of the 2011 IEEE Power and Energy Society General Meeting, Detroit, MI, USA, 24–28 July 2011; pp. 1–6. [Google Scholar] [CrossRef]

- Wang, Y.; Ding, Y. Nodal price uncertainty analysis considering random failures and elastic demand. In Proceedings of the IEEE PES Power Systems Conference and Exposition, New York, NY, USA, 10–13 October 2004; Volume 1, pp. 174–178. [Google Scholar] [CrossRef]

- Feuerriegel, S.; Strüker, J.; Neumann, D. Reducing price uncertainty through demand side management. In Proceedings of the Thirty Third International Conference on Information Systems, Orlando, FL, USA, 16–19 December 2012; pp. 1–20. [Google Scholar]

- Hong, Y.Y.; Hslao, C.Y. Locational marginal price forecasting in deregulated electricity markets using artificial intelligence. IEEE Trans. Power Syst. 2002, 149, 621–626. [Google Scholar] [CrossRef]

- Chen, X.; Dong, Z.Y.; Meng, K.; Xu, Y.; Wong, K.P.; Ngan, H.W. Electricity Price Forecasting With Extreme Learning Machine and Bootstrapping. IEEE Trans. Power Syst. 2012, 27, 2055–2062. [Google Scholar] [CrossRef]

- Wang, P.; Xiao, Y.; Ding, Y. Nodal market power assessment in electricity markets. IEEE Trans. Power Syst. 2004, 19, 1373–1379. [Google Scholar] [CrossRef]

- Lakić, E.; Medved, T.; Zupančič, J.; Gubina, A.F. The review of market power detection tools in organised electricity markets. In Proceedings of the 2017 14th International Conference on the European Energy Market (EEM), Dresden, Germany, 6–9 June 2017; pp. 1–6. [Google Scholar] [CrossRef]

- Zhang, F.-Q.; Zhou, H. Research on Economic Withholding in Wholesale Markets Based on Incremental Heat Rate. In Proceedings of the 2005 IEEE/PES Transmission & Distribution Conference & Exposition: Asia and Pacific, Dalian, China, 18 August 2005; pp. 1–7. [Google Scholar] [CrossRef]

- Wholesale. Wholesale Electricity Market Rules. 2020. Available online: https://www.erawa.com.au/rule-change-panel/wholesaleelectricity-market-rules (accessed on 30 March 2020).

- Yu, Z.; Razzaq, A.; Rehman, A.; Shah, A.; Jameel, K.; Mor, R.S. Disruption in global supply chain and socio-economic shocks: A lesson from COVID-19 for sustainable production and consumption. Oper. Manag. Res. 2022, 15, 233–248. [Google Scholar] [CrossRef]

- Cali, U.; Çakir, O. Energy Policy Instruments for Distributed Ledger Technology Empowered Peer-to-Peer Local Energy Markets. IEEE Access 2019, 7, 82888–82900. [Google Scholar] [CrossRef]

- Bampoulas, A.; Saffari, M.; Pallonetto, F.; Mangina, E.; Finn, D.P. A fundamental unified framework to quantify and characterise energy flexibility of residential buildings with multiple electrical and thermal energy systems. Appl. Energy 2021, 282, 116096. [Google Scholar] [CrossRef]

- Tahersima, F.; Stoustrup, J.; Meybodi, S.A.; Rasmussen, H. Contribution of domestic heating systems to smart grid control. In Proceedings of the 2011 50th IEEE Conference on Decision and Control and European Control Conference, Orlando, FL, USA, 12–15 December 2011; pp. 3677–3681. [Google Scholar] [CrossRef] [Green Version]

- Kalfa, V.R.; Arslan, B.; Ertuğrul, İ. Determining the Factors Affecting the Market Clearing Price by Using Multiple Linear Regression Method. Alphanumeric 2021, 9, 35–48. [Google Scholar] [CrossRef]

- Baumeister, C.; Korobilis, D.; Lee, T.K. Energy Markets and Global Economic Conditions. Rev. Econ. Stat. 2022, 104, 828–844. [Google Scholar] [CrossRef]

- Halkos, G.E.; Tsirivis, A.S. Energy Commodities: A Review of Optimal Hedging Strategies. Energies 2019, 12, 3979. [Google Scholar] [CrossRef] [Green Version]

- Huang, G.-B.; Zhu, Q.-Y.; Siew, C.-K. Extreme learning machine: Theory and applications. Neurocomputing 2006, 70, 489–501. [Google Scholar] [CrossRef]

- Alshejari, A.; Kodogiannis, V.S. Electricity price forecasting using asymmetric fuzzy neural network systems. In Proceedings of the 2017 IEEE International Conference on Fuzzy Systems (FUZZ-IEEE), Naples, Italy, 9–12 July 2017; pp. 1–6. [Google Scholar] [CrossRef] [Green Version]

- Amjady, N.; Daraeepour, A. Design of input vector for day-ahead price forecasting of electricity markets. Expert Syst. Appl. 2009, 36, 12281–12294. [Google Scholar] [CrossRef]

- Ghayekhloo, M.; Azimi, R.; Ghofrani, M.; Menhaj, M.; Shekari, E. A combination approach based on a novel data clustering method and Bayesian recurrent neural network for day-ahead price forecasting of electricity markets. Electr. Power Syst. Res. 2019, 168, 184–199. [Google Scholar] [CrossRef]

- Lin, W.M.; Gow, H.J.; Tsai, M.T. Electricity price forecasting using Enhanced Probability Neural Network. Energy Convers. Manag. 2010, 51, 2707–2714. [Google Scholar] [CrossRef]

- Lago, J.; Marcjasz, G.; De Schutter, B.; Weron, R. Forecasting day-ahead electricity prices: A review of state-of-the-art algorithms, best practices and an open-access benchmark. Appl. Energy 2021, 293, 116983. [Google Scholar] [CrossRef]

- Uniejewski, B.; Weron, R. Efficient Forecasting of Electricity Spot Prices with Expert and LASSO Models. Energies 2018, 11, 2039. [Google Scholar] [CrossRef] [Green Version]

- Uniejewski, B.; Marcjasz, G.; Weron, R. On the importance of the long-term seasonal component in day-ahead electricity price forecasting: Part II — Probabilistic forecasting. Energy Econ. 2019, 79, 171–182. [Google Scholar] [CrossRef] [Green Version]

- Shao, Z.; Zheng, Q.; Liu, C.; Gao, S.; Wang, G.; Chu, Y. A feature extraction- and ranking-based framework for electricity spot price forecasting using a hybrid deep neural network. Electr. Power Syst. Res. 2021, 200, 107453. [Google Scholar] [CrossRef]

- Bissing, D.; Klein, M.T.; Chinnathambi, R.A.; Selvaraj, D.F.; Ranganathan, P. A Hybrid Regression Model for Day-Ahead Energy Price Forecasting. IEEE Access 2019, 7, 36833–36842. [Google Scholar] [CrossRef]

- He, D.; Chen, W.P. A real-time electricity price forecasting based on the spike clustering analysis. In Proceedings of the 2016 IEEE/PES Transmission and Distribution Conference and Exposition (T&D), Dallas, TX, USA, 3–5 May 2016; pp. 1–5. [Google Scholar]

- Wang, Y.; Li, L.; Ni, J.; Huang, S. Feature selection using tabu search with long-term memories and probabilistic neural networks. Pattern Recognit. Lett. 2009, 30, 661–670. [Google Scholar] [CrossRef]

- Wu, W.; Zhou, J.; Mo, L.; Zhu, C. Forecasting electricity market price spikes based on bayesian expert with support vector machines. In Advanced Data Mining and Applications, Proceedings of the International Conference on Advanced Data Mining and Applications, Xi’an, China, 14–16 August 2006; Springer: Berlin/Heidelberg, Germany, 2006; pp. 205–212. [Google Scholar]

- Amjady, N.; Keynia, F. A new prediction strategy for price spike forecasting of day-ahead electricity markets. Appl. Soft Comput. 2011, 11, 4246–4256. [Google Scholar] [CrossRef]

- Dev, P.; Martin, M.A. Using neural networks and extreme value distributions to model electricity pool prices: Evidence from the Australian National Electricity Market 1998–2013. Energy Convers. Manag. 2014, 84, 122–132. [Google Scholar] [CrossRef]

- Shrivastava, N.A.; Panigraphi, B.K.; Lim, M.H. Electricity price classification using extreme learning machines. Neural Comput. Appl. 2016, 27, 9–18. [Google Scholar] [CrossRef]

- Stathakis, E.; Papadimitriou, T.; Gogas, P. Forecasting Price Spikes in Electricity Prices. Rev. Econ. Anal. 2021, 13, 65–87. [Google Scholar] [CrossRef]

- Amjady, N.; Keynia, F. Electricity market price spike analysis by a hybrid data model and feature selection technique. Electr. Power Syst. Res. 2010, 80, 318–327. [Google Scholar] [CrossRef]

- Wang, P.; Goel, L.; Ding, Y. The impact of random failures on nodal price and nodal reliability in restructured power systems. Electr. Power Syst. Res. 2004, 71, 129–134. [Google Scholar] [CrossRef]

- Strategic bidding and rebidding in electricity markets. Energy Econ. 2016, 59, 24–36. [CrossRef] [Green Version]

- Liu, Y.; Wu, F.F. Impacts of Network Constraints on Electricity Market Equilibrium. IEEE Trans. Power Syst. 2007, 22, 126–135. [Google Scholar] [CrossRef] [Green Version]

- Chattopadhyay, D. Multicommodity spatial Cournot model for generator bidding analysis. IEEE Trans. Power Syst. 2004, 19, 267–275. [Google Scholar] [CrossRef]

- Peng, T.; Tomsovic, K. Congestion influence on bidding strategies in an electricity market. IEEE Trans. Power Syst. 2003, 18, 1054–1061. [Google Scholar] [CrossRef]

- Morales, J.M.; Conejo, A.J.; Madsen, H.; Pinson, P.; Zugno, M. Integrating Renewables in Electricity Markets; Springer: New York, NY, USA, 2014; Volume 205. [Google Scholar]

- SMARD. German Market Data. Available online: https://www.smard.de/en/downloadcenter/download-market-data (accessed on 30 March 2020).

- NordPool. Finnish Day-Ahead Market Prices. Available online: https://www.nordpoolgroup.com/en/Market-data1/Dayahead/Area-Prices/ALL1/Hourly/?view=table (accessed on 30 March 2020).

- Fingrid. Finnish Market Data. Available online: https://data.fingrid.fi/open-data-forms/search/en/ (accessed on 30 March 2020).

- Kubat, M. Neural networks: A comprehensive foundation by Simon Haykin, Macmillan, 1994, ISBN 0-02-352781-7. Knowl. Eng. Rev. 1999, 13, 409–412. [Google Scholar] [CrossRef]

- Wang, Y.; Guo, Y. Forecasting method of stock market volatility in time series data based on mixed model of ARIMA and XGBoost. China Commun. 2020, 17, 205–221. [Google Scholar] [CrossRef]

- Pavlov, Y.L. Random forests. In Random Forests; De Gruyter: Berlin, Germany, 2019. [Google Scholar]

- Christensen, T.M.; Hurn, A.S.; Lindsay, K.A. Forecasting spikes in electricity prices. Int. J. Forecast. 2012, 28, 400–411. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Market Price Ranges (€/MWh) | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|

| German wholesale Day-Ahead Market | ||||

| <−80 | 4 | 3 | - | - |

| [−80–−60) | 11 | 18 | 4 | - |

| [−60–−30) | 30 | 28 | 21 | - |

| [−30–0) | 166 | 249 | 91 | 69 |

| [0–30] | 1700 | 3860 | 409 | 293 |

| (30–60] | 6501 | 4381 | 2449 | 222 |

| (60–90] | 326 | 207 | 2518 | 566 |

| (90–120] | 20 | 32 | 1254 | 710 |

| (120–150] | 2 | 4 | 488 | 694 |

| (150–180] | - | - | 415 | 816 |

| >180 | - | 2 | 1088 | 5390 |

| Finnish wholesale Day-Ahead Market | ||||

| <−80 | - | - | - | - |

| [−80–−60) | - | - | - | - |

| [−60–−30) | - | - | - | - |

| [−30–0) | - | 9 | 5 | 27 |

| [0–30] | 1010 | 5441 | 1748 | 1623 |

| (30–60] | 6570 | 2768 | 2880 | 844 |

| (60–90] | 1125 | 487 | 1983 | 834 |

| (90–120] | 36 | 38 | 1202 | 961 |

| (120–150] | 11 | 19 | 345 | 751 |

| (150–180] | 2 | 5 | 143 | 716 |

| >180 | 5 | 16 | 454 | 3004 |

| 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|

| German Day-Ahead Market | |||

| or | |||

| Finnish Day-Ahead Market | |||

| or | |||

| Normal Prices | Extremely High Prices | Negative Prices | ||||

|---|---|---|---|---|---|---|

| Internal Neurons | Time (mm.ss) | Average RMSE (€/MWh) | Time (mm.ss) | Average RMSE (€/MWh) | Time (mm.ss) | Average RMSE (€/MWh) |

| ELM | ||||||

| 10 | ||||||

| 20 | ||||||

| 30 | ||||||

| 40 | ||||||

| 50 | ||||||

| 60 | ||||||

| ANN | ||||||

| 10 | ||||||

| 20 | ||||||

| 30 | ||||||

| 40 | ||||||

| 50 | ||||||

| 60 | ||||||

| Normal Prices | Extremely High Prices | Negative Prices | ||||

|---|---|---|---|---|---|---|

| Number of Estimators | Time (mm.ss) | Average RMSE (€/MWh) | Time (mm.ss) | Average RMSE (€/MWh) | Time (mm.ss) | Average RMSE (€/MWh) |

| XGBoost | ||||||

| 50 | ||||||

| 100 | ||||||

| 150 | ||||||

| 200 | ||||||

| 250 | ||||||

| 300 | ||||||

| RF | ||||||

| 50 | ||||||

| 100 | ||||||

| 150 | ||||||

| 200 | ||||||

| 250 | ||||||

| 300 | ||||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Loizidis, S.; Konstantinidis, G.; Theocharides, S.; Kyprianou, A.; Georghiou, G.E. Electricity Day-Ahead Market Conditions and Their Effect on the Different Supervised Algorithms for Market Price Forecasting. Energies 2023, 16, 4617. https://doi.org/10.3390/en16124617

Loizidis S, Konstantinidis G, Theocharides S, Kyprianou A, Georghiou GE. Electricity Day-Ahead Market Conditions and Their Effect on the Different Supervised Algorithms for Market Price Forecasting. Energies. 2023; 16(12):4617. https://doi.org/10.3390/en16124617

Chicago/Turabian StyleLoizidis, Stylianos, Georgios Konstantinidis, Spyros Theocharides, Andreas Kyprianou, and George E. Georghiou. 2023. "Electricity Day-Ahead Market Conditions and Their Effect on the Different Supervised Algorithms for Market Price Forecasting" Energies 16, no. 12: 4617. https://doi.org/10.3390/en16124617

APA StyleLoizidis, S., Konstantinidis, G., Theocharides, S., Kyprianou, A., & Georghiou, G. E. (2023). Electricity Day-Ahead Market Conditions and Their Effect on the Different Supervised Algorithms for Market Price Forecasting. Energies, 16(12), 4617. https://doi.org/10.3390/en16124617