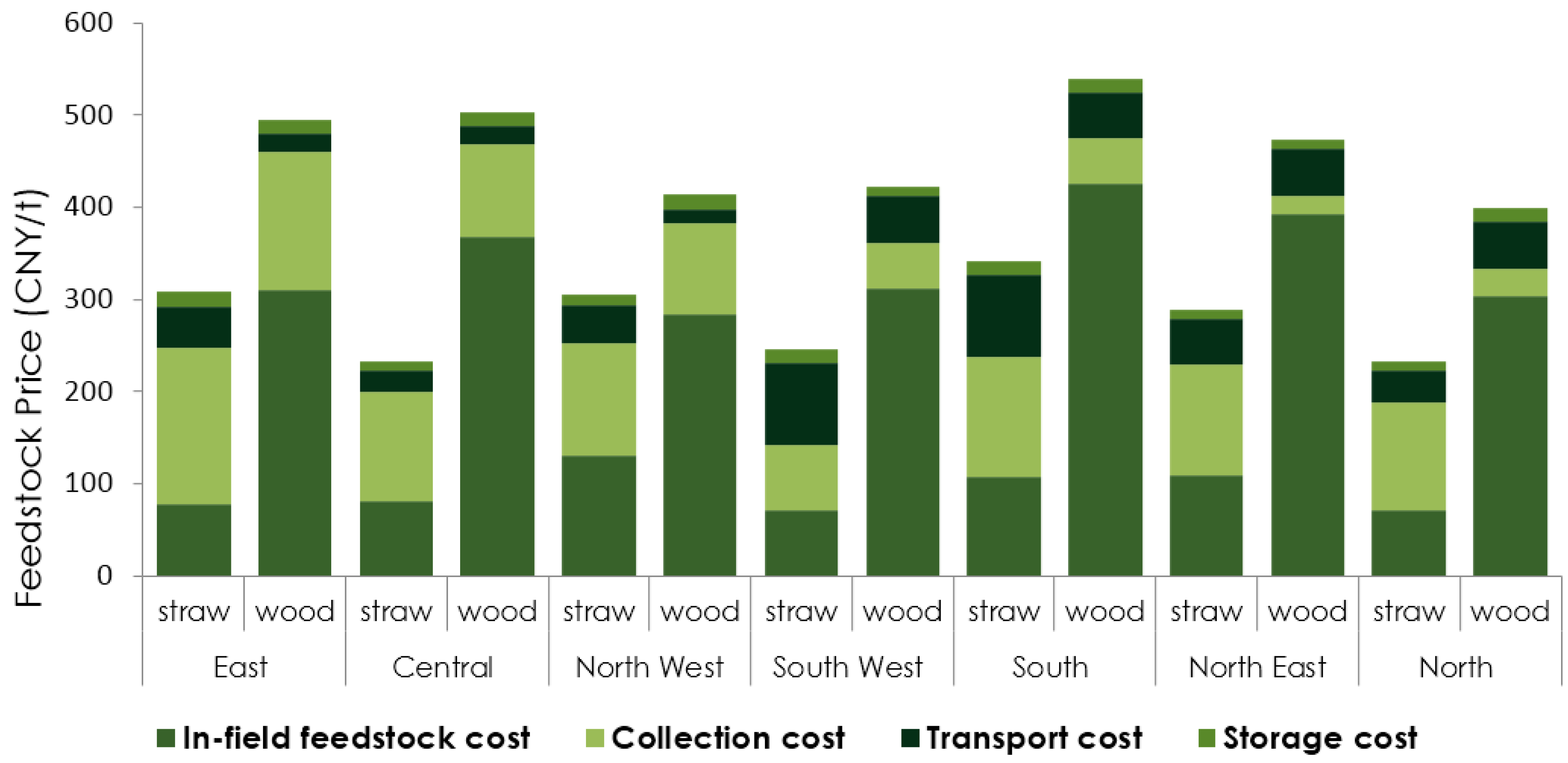

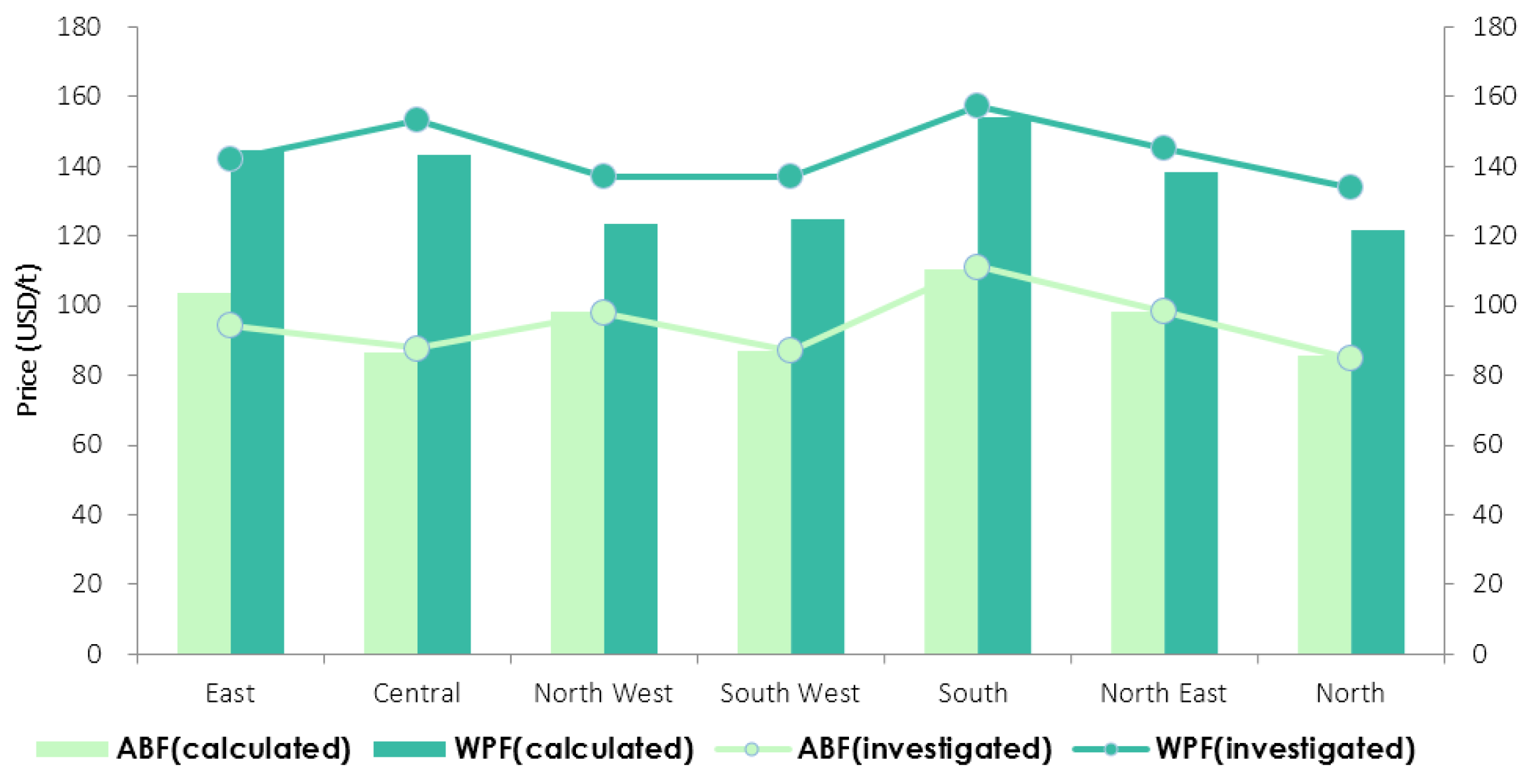

5.1. Calculated Production Cost

Table 7 shows the calculated BMF production costs in each region. In order to validate these results, we compared that data to the local selling prices of the 117 BMF companies that we investigated.

Figure 8 demonstrates that the actual average prices of each region show a high degree of consistency with the simulation results.

Table 7.

Calculated BMF production costs in each region (USD/t). Woody pellet fuel: WPF; agricultural briquette fuel: ABF.

Table 7.

Calculated BMF production costs in each region (USD/t). Woody pellet fuel: WPF; agricultural briquette fuel: ABF.

| BMF | East | Central | Northwest | Southwest | South | Northeast | North |

|---|

| ABF (calculated) | 104 | 86 | 98 | 87 | 110 | 98 | 86 |

| WPF (calculated) | 145 | 143 | 124 | 125 | 154 | 138 | 122 |

Figure 8.

Calculated and investigated regional production costs of BMF in China.

Figure 8.

Calculated and investigated regional production costs of BMF in China.

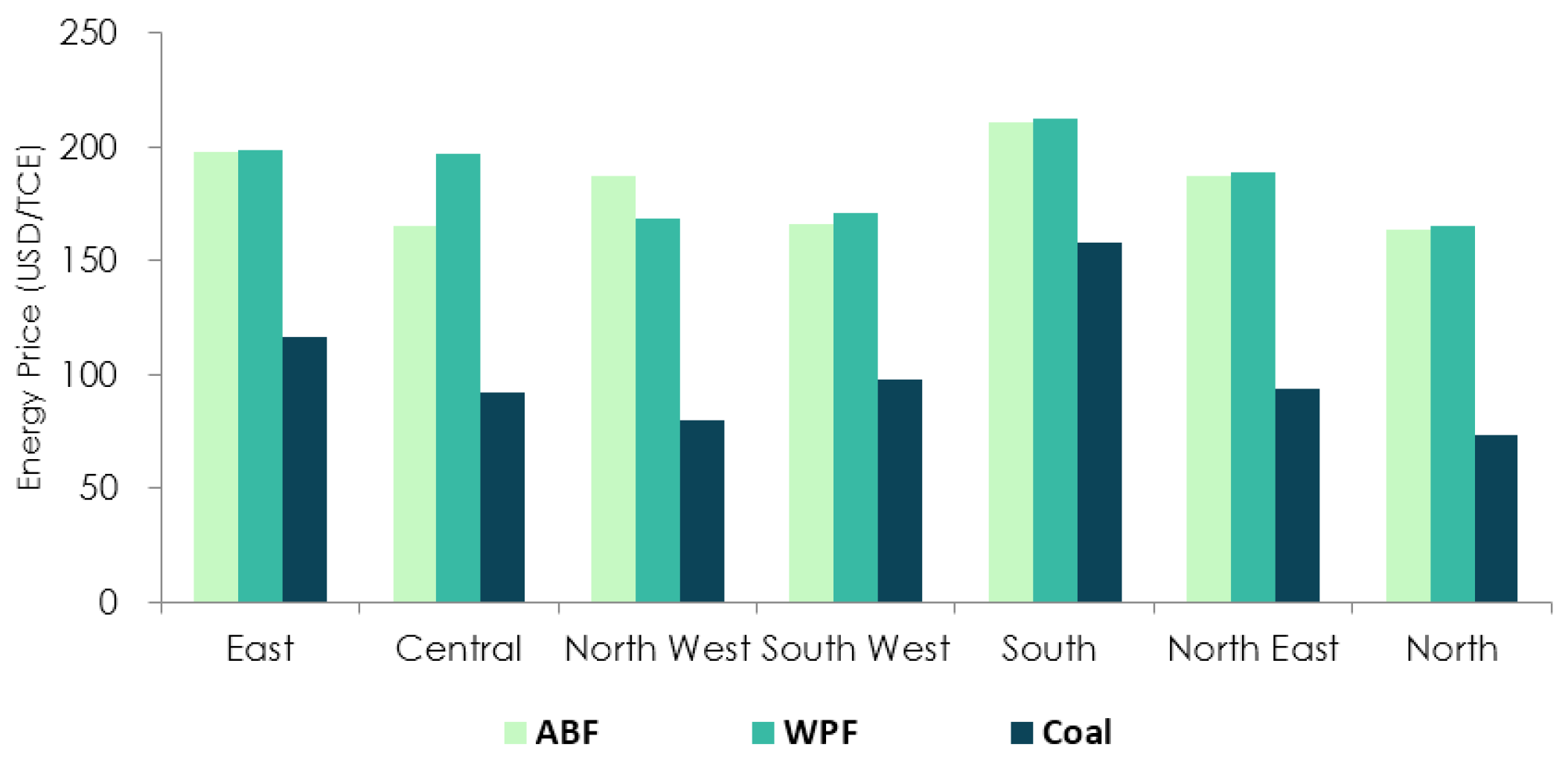

Due to its lower energy density, the average cost of ABF is 40 USD/t less than that of WPF. In order to compare different BMFs equitably, we also calculated the regional unit energy cost of ABF and WPF based on one ton standard coal equivalent.

Figure 9 gives the results. In most regions, the energy costs of ABF and WPF are almost equal, but in central China, the energy cost of ABF is lower than that of WPF, whereas in northwest China, WPF’s energy cost is lower. For ABF, south China has the highest prices, followed by east, northeast, northwest and southwest China, north and central China have the lowest prices. For WPF, south China again has the highest prices, followed by east, central, northeast, southwest, northwest China, north China has the lowest WPF price.

Figure 9.

Energy cost of BMF and coal in China’s regions.

Figure 9.

Energy cost of BMF and coal in China’s regions.

The reason for this price disparity for BMF in China is the unbalanced regional development. In most regions, BMF is replacing coal for both distributed and centralized heating. However, in developed regions like the south and east, due to a high degree of urbanization, less local feedstock is locally available; in addition, the local governments attach high importance to environmental protection, strictly implementing measures like coal ban regulations. Accordingly, BMF is shipped to these regions to replace natural gas at a higher price. However, natural gas presents only a small part of China’s energy consumption and it will be too expensive to provide natural gas heating all over China. From the prospective of mainstream of heating patterns, coal will continue to be the most commonly used fossil fuel in the long run and thus the main competitive target that BMF will seek to replace in most regions in China. From

Figure 9 we can observe that in all regions BMF’s energy cost is higher than that of coal, especially in the current context of decreasing coal prices, so some incentives should be adopted to protect the BMF industry and maintain BMF’s commercial competitiveness.

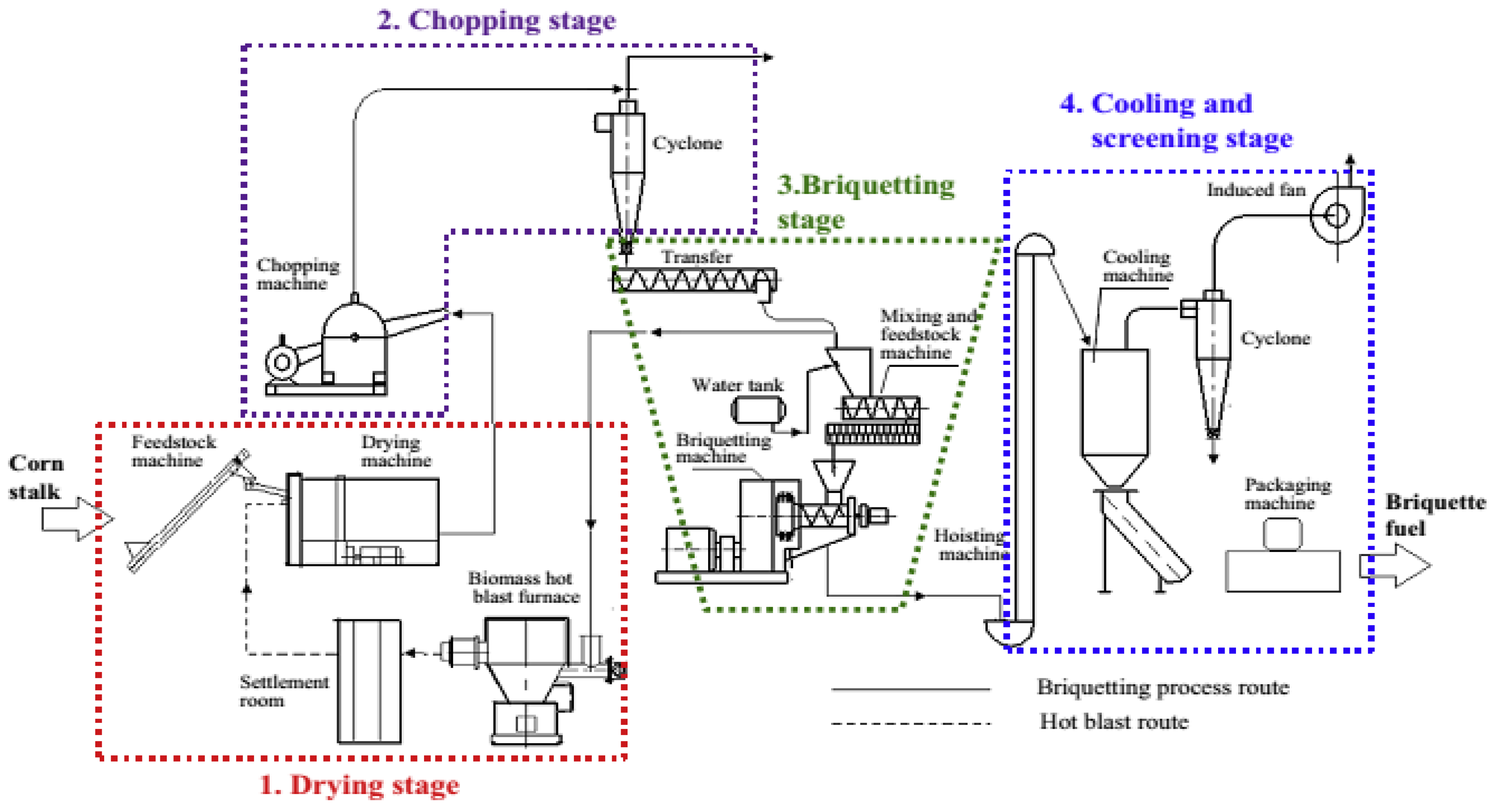

5.2. Energy Consumption

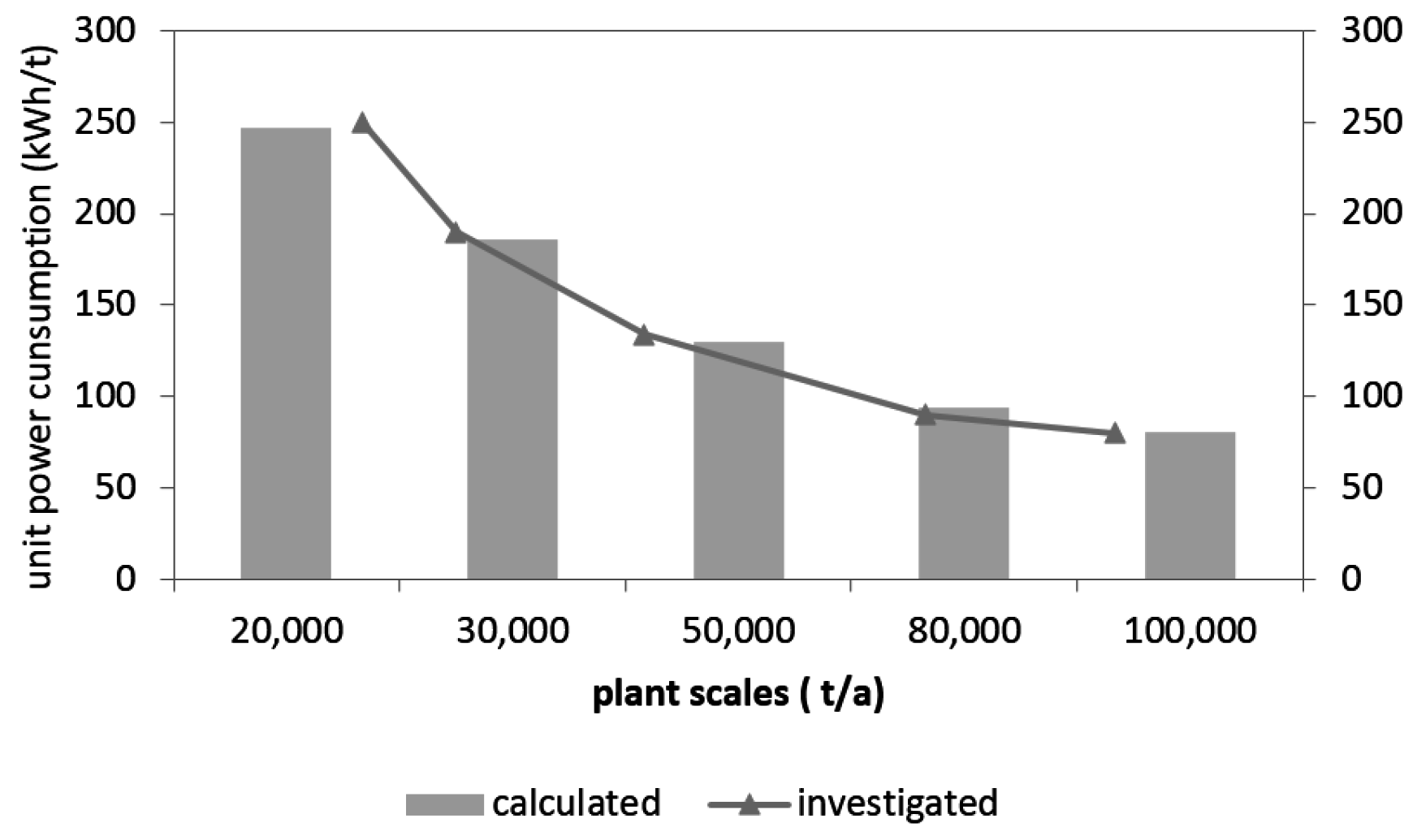

Figure 10 depicts the relationship between the calculated energy consumption to produce a ton of BMF and the actual values that we obtained from the nationwide investigation. The result shows a high degree of consistency, and that means our assumption of the proportionality factor in economy of scale function is valid. From

Figure 10 we also observe that along with the increase of BMF production plant scales, the unit energy consumption represents a decreasing tendency and comes close to some value between 50 kWh/t and 80 kWh/t.

Figure 10.

Calculated and investigated energy consumption.

Figure 10.

Calculated and investigated energy consumption.

The regional energy consumption for BMF production in each region is shown in

Table 8. It is concluded that plants in the east region have the lowest energy consumption to produce a ton of BMF, at about 130 kWh/t, followed by the plants in the northeast region, at about 180kWh/t, while plants in the remaining regions are roughly the same, at about 250 kWh/t. This is because that the energy consumption is mainly related to the plant scales, and east China has more large plants, its integration degree is higher than other regions, and therefore the energy consumption is less.

Table 8.

Regional energy consumption data.

Table 8.

Regional energy consumption data.

| Item | East | Central | Northwest | Southeast | South | Northeast | North |

|---|

| Popular plant scale (t/a) | 50,000 | 20,000 | 20,000 | 20,000 | 20,000 | 30,000 | 20,000 |

| Power consumption (kWh/t) | 130.24 | 247.35 | 247.35 | 247.35 | 247.35 | 186.23 | 247.35 |

5.3. Cost Structure

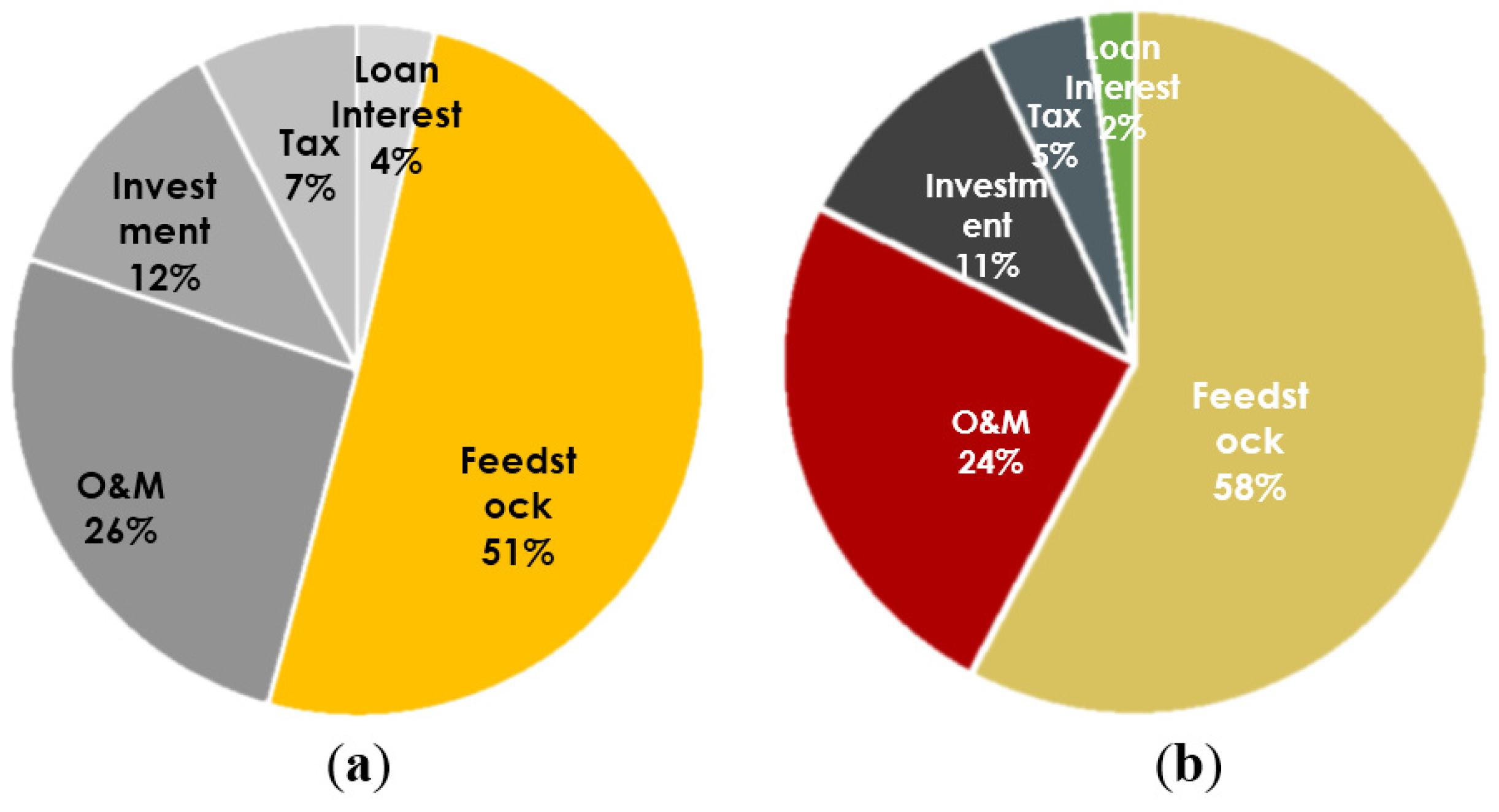

According to our simulation results, the regional cost structures show a high degree of similarity. Here we will take BMF in central China as an example, and its cost structure is shown in

Figure 11. For ABF, feedstock represents the largest share of the total cost, around 51%, with

O &

M costs come second at 26%, followed by investment costs at 12%, tax costs at about 7%, and loan interest costs at 4%. The cost structure for WPF is similar to that for ABF, with a slightly higher feedstock share, about 58%, resulting from the higher energy density and higher price of woody feedstocks.

O &

M costs represent a comparable share as in the ABF case at 24%, the investment costs, tax costs and loan interest costs for WPF are 11%, 5% and 2%, respectively.

Figure 11.

(a) Cost structure for ABF in central China; (b) cost structure for WPF in central China.

Figure 11.

(a) Cost structure for ABF in central China; (b) cost structure for WPF in central China.

Unlike other renewable energies such as PV and wind energy, the initial investment of BMF is not the greatest part of its production cost, it means that it is easier for SMEs to access to this industry because the capital threshold is relatively low.

5.4. Sensitivity Analysis

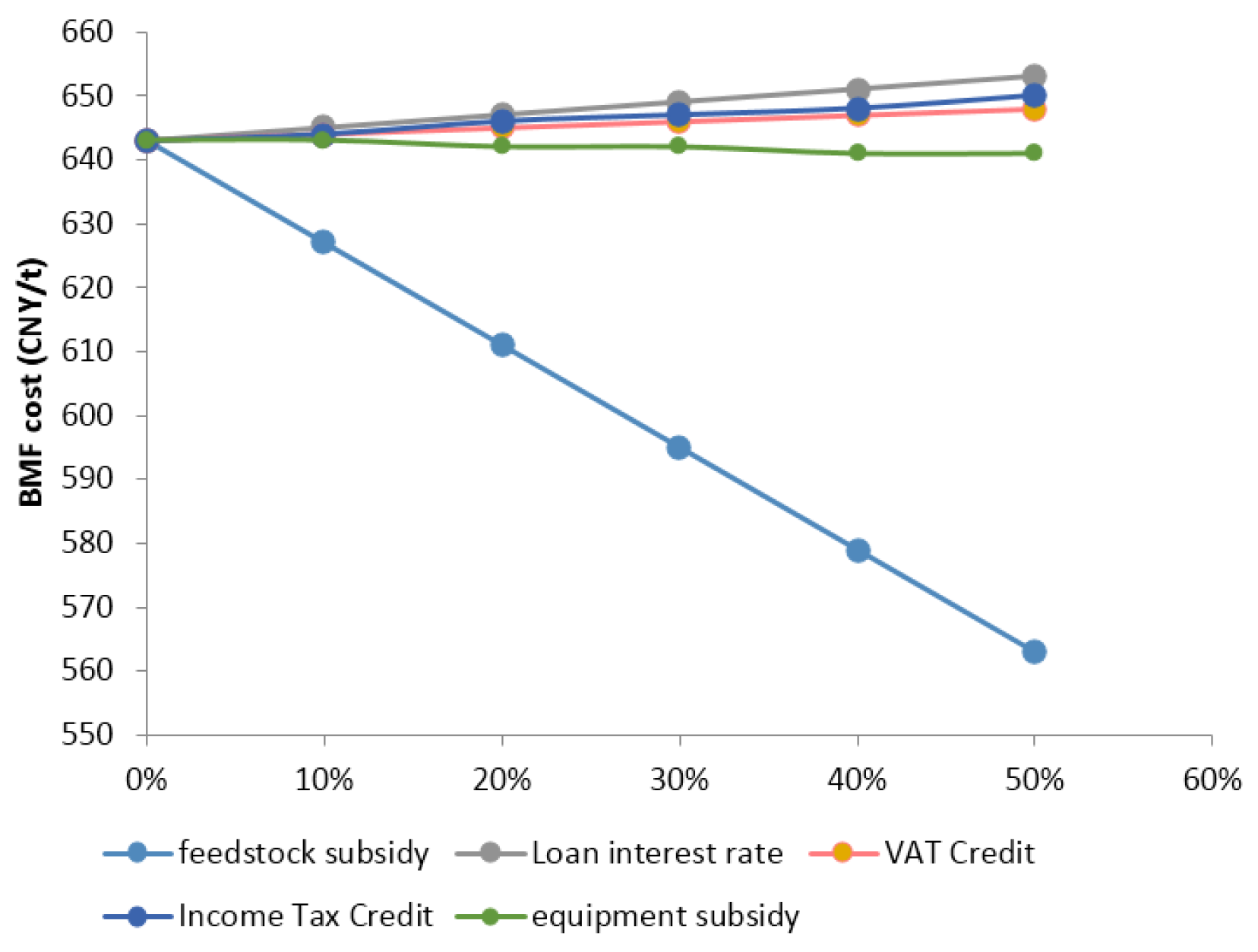

In order to identify the most effective policy factors, we carried out a sensitivity analysis based on current incentive policies. The results show that sensitivity for AMF and WPF are similar. Taking ABF in the east region as an example, the results are shown in

Figure 12. We can see that feedstock subsidies have by far the greatest positive impact on lowering BMF production costs, followed by equipment subsidies. Loan rate, VAT rate and income tax rate changes have a negative impact on lowering BMF production costs. The dramatic impact of feedstock subsidies results from the cost structures. The feedstock subsidies aim at reducing the feedstock costs, while the VAT and income tax credit and the equipment subsidies aim at reducing the tax and investment costs, respectively. However, in ABF cost structure, the sum of the shares of investment, tax and loan interest is 23%, less than the half of the feedstock share, so feedstock subsidies should be considered as the first choice to stimulate this industry.

Figure 12.

Impact of various BMF incentive options. Note: the variation of each policy factor is based on current incentive measures in China: (1) feedstock subsidy: From 0 USD/t to 22 USD/t (in the figure as 0%–100%); (2) loan interest rate: From 0 to 6.5% (in the figure as 0–100%); (3)VAT credit: From 0% to 100% variation on the base of 14% VAT input rate and 17% VAT output rate; (4) income tax rate: From 0% to100% variation on the base of 25% income tax rate; (5) Equipment subsidy: From 0% to 500,000 CNY/t (80,645.16 USD/t, in the figure as 0%–100%).

Figure 12.

Impact of various BMF incentive options. Note: the variation of each policy factor is based on current incentive measures in China: (1) feedstock subsidy: From 0 USD/t to 22 USD/t (in the figure as 0%–100%); (2) loan interest rate: From 0 to 6.5% (in the figure as 0–100%); (3)VAT credit: From 0% to 100% variation on the base of 14% VAT input rate and 17% VAT output rate; (4) income tax rate: From 0% to100% variation on the base of 25% income tax rate; (5) Equipment subsidy: From 0% to 500,000 CNY/t (80,645.16 USD/t, in the figure as 0%–100%).

5.5. Subsidy and Development Strategy for Each Region

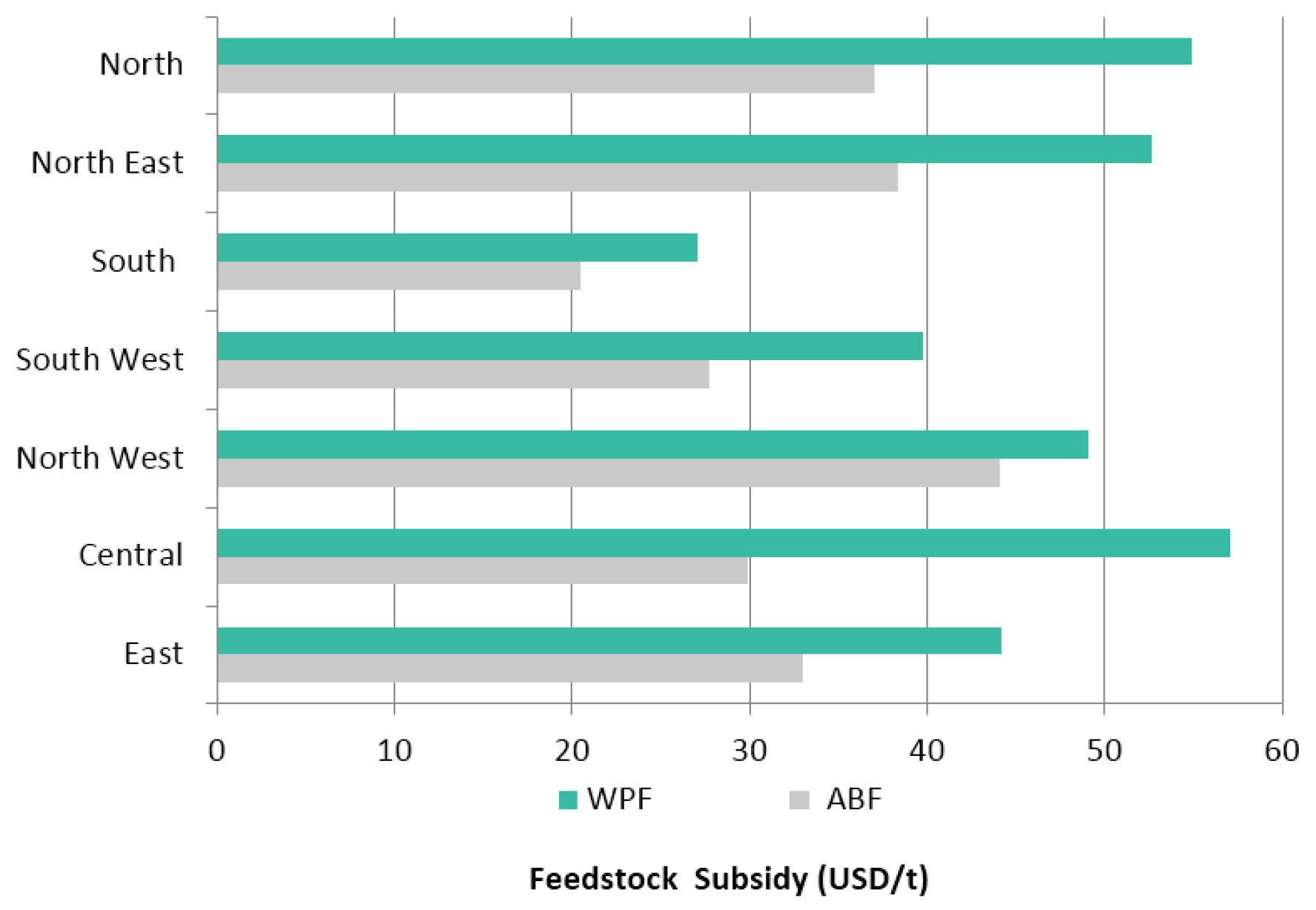

As shown in the aforementioned analysis, feedstock subsidies are the most effective policy, but in different regions, the price of BMF and the price of the target energy to be replaced vary, so the current uniform subsidy standard would not be suitable for all regions. Therefore we calculated how much the local government should subsidize BMF in each region in order to sustain its economic viability.

Figure 13 gives the results. For ABF, the subsidy in south is the lowest, at about 20 USD/t, followed by 28 USD/t in southwest China, 30 USD/t in central China, 33 USD/t in east China and 37 USD/t in north China; as it can be seen, the required subsidies in the northeast and northwest are the highest, at around 38 USD/t and 44 USD/t, respectively.

For WPF, the subsidy in south is again the lowest, at about 27 USD/t, followed by 40 USD/t in southwest China, 44 USD/t in east China, 49 USD/t in northwest China, 53 USD/t in northeast China, 55 USD/t in north China and 57 USD/t in central China.

These results are caused by both the local fossil energy prices and BMF production costs. The reason why south China has the highest production costs but needs the least subsidies is that this region is short of coal and its coal prices are relatively high due to the expensive transportation expenses (its coal price is two times of that in north China). Another factor is the local feedstock conditions, as some regions, like north and central China, are rich in agricultural feedstock due to the fact they are covered by massive arable plains and have few mountains where trees grow, so their agricultural feedstock is much cheap than woody ones, even when the energy density is factored into the calculations. Therefore in these regions ABF are recommended to be extensively promoted, but WPF are suggested as subordinate products.

Figure 13.

Required feedstock subsides for each region.

Figure 13.

Required feedstock subsides for each region.

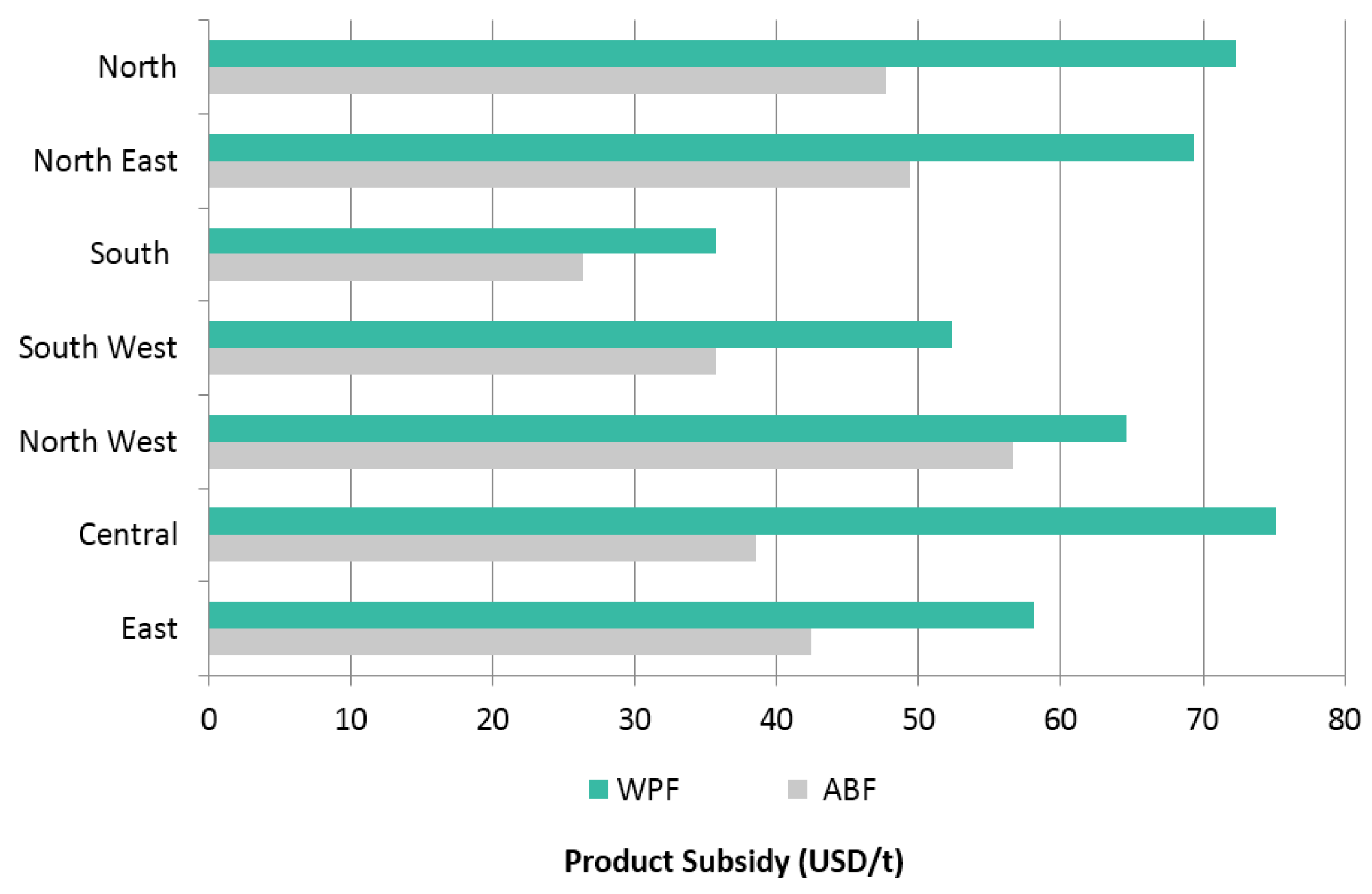

However, actual policy implementation is difficult and complex, because it is easy for recipients of the feedstock subsidy to cheat and hard to incentivize BMF consumption. According to our investigation, in order to maximize their subsidy, some plant owners cheat with regard to the total amount of feedstock they purchase, and did not produce as much as BMF they claimed for the subsidy. Therefore, it is better to change the feedstock subsidy to a product-based subsidy, credited only for the BMF actually produced and utilized by consumers. The regional product subsidies are shown in

Figure 14: For ABF, the product subsidies are 26 USD/t, 36 USD/t, 39 USD/t, 42 USD/t, 48 USD/t, 49 USD/t and 57 USD/t in the south, southwest, central, east, north, northeast and northwest regions, respectively; for WPF, the product subsidies are 36 USD/t, 52 USD/t, 58 USD/t, 65 USD/t, 69 USD/t, 72 USD/t and 75 UDS/t in south, southwest, east, northwest, northeast, north and central China, respectively.

Figure 14.

Production-based subsidy for each region.

Figure 14.

Production-based subsidy for each region.

Also from the subsidy results we can sketch a desired development strategy for BMF in each region. A high subsidy requirement means that it is not economical to develop BMF in that region,

Table 9 indicates which regions should develop each type of BMF and at what level: ABF should be developed with priority in the south region, then in the southwest, central, east, north region, and is not recommended in the northeast, northwest; WPF should be developed first in the south, southwest region, then in the east, northwest and northeast region, and is not recommended in the north and central regions.

Table 9.

Development strategy of BMF for each region.

Table 9.

Development strategy of BMF for each region.

| BMF | Priority development | Modest development | Not recommended |

|---|

| ABF | South | Southwest, Central, East, North | Northeast, Northwest |

| WPF | South, Southwest | East, Northwest, Northeast | North, Central |

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}