1. Introduction

As one of the important pillar industries in China, the automotive industry plays a significant role in the national economy and in social development. According to the latest statistics released by the China Association of Automobile Manufactures (CAAM), the total production and sales volume of Chinese cars reached a new high with 28.119 million vehicles produced and 28.028 million vehicles sold. The production and sales showed relatively rapid growth, and have ranked first among world economies since 2009 [

1].

Along with the rapid development of the automotive industry, the existing energy and environmental problems cannot be ignored. First, massive car ownership accelerates the very large demand for crude oil. In 2016, Chinese car ownership reached 295 million. According to the report of the China Energy News, the dependence on foreign oil rose to 65.4% for the year [

2]. Second, there is an urgent demand of preventing and controlling the pollution of motor vehicle emissions. Currently, the automobiles in China are mainly fueled by gasoline and diesel refined from crude oil [

3], and, according to the report of the Ministry of Environmental Protection of the People’s Republic of China (MEPPRC), the vehicle emissions of China in 2016 were estimated to be around 44.725 million tons, becoming a significant source of air pollution in China, resulting in Particulate Matter 2.5 (PM

2.5) pollution and photochemical smog [

4].

Nowadays, the Chinese economy has entered into an era of “New Normal”, the vision of green development has been gradually absorbed into the vehicle industry in the background of the “low-carbon economy”. Moreover, it is an important measure for cultivating new momentum and accelerating the transformation and upgrading of the automotive industry to develop the new energy vehicle (NEV) industry. According to the Energy-Saving and New Energy Automobile Industry Development Plan 2012–2020, new energy vehicle (NEV) refers to automobiles that use a new type of power system (driven completely, or mainly relying on new energy sources). Currently, there are mainly three kinds of NEVs: battery electric vehicles, plug-in hybrid electric vehicles, and fuel cell vehicles [

5]. During the inspection in Shanghai, Chinese President Xi Jinping pointed out that the automobile market was very large, the automotive industry was full of advanced technology and detailed management, and the development of new energy vehicles was the only road for China to transform from a large automobile-manufacturing country to a powerful one [

6]. Premier Li Keqiang also pointed out the green development of China needed green products (i.e., NEVs), and Chinese firms should endeavor to build up global brands with innovation [

7]. To facilitate the healthy development of the NEV industry, the Chinese government has formulated many policies and regulations (e.g., tax incentives, subsidy policies, and national and industrial standards). The policy support has sped up the development of NEVs in China. For enterprises, more and more automotive firms turn to, and concentrate on, the research and development (R&D) of NEVs and their spare parts, and hope to seize the opportunities as soon as possible, e.g., BYD and SAIC [

8,

9]. Some of them have achieved performance improvements and cost reductions. For customers, there has been an increase in choosing NEVs as one of the travel tools for Green Travel, the NEV ownership has exceeded one million in China, which is equivalent to 50% of the world NEV ownership [

10]. Taking Beijing as an example, according to the communique of the Management Office subordinated to Beijing Traffic Management Bureau, the data show that the total quota of personal new energy vehicles of Beijing in 2017 was 51,000. However, city residents had divided up the quota in April. As of 12:00 p.m. on 8 December 2017, there were still 120,376 users wishing to buy a new energy vehicle waiting in line [

11]. Overall, the NEV industry has been in the spotlight.

It has been more than 60 years since the construction of the First Automobile Manufactory in 1953, which was the beginning of the Chinese automotive industry. Based on the data manually collected by the authors, there were 3030 firms listed in China’s A-share stock market by the end of 31 December 2016, and 121 of them were focused on the R&D of vehicles, including automobiles and their spare parts. The number of automotive firms accounted for 3.7% of the number of A-share firms. The research and development of new energy vehicles rose in the early 2000s. In February 2009, the Ministry of Finance of the People’s Republic of China (MFPRC), the Ministry of Science and Technology of the People’s Republic of China (MSTPRC), the National Development and Reform Commission (NDRC), and the Ministry of Industry and Information of the People’s Republic of China (MIITPRC) convened a meeting to discuss the demonstration, promotion, and pilot schemes of NEVs and the cities including Beijing and Shanghai play an active part in that activity [

12]. During the “two sessions” (the National People’s Congress and the National Committee of the Chinese People’s Political Consultative Conference), officers of the MFPRC and MIITPRC said that the pilot schemes produced good results as thousands of NEVs had been promoted. Moreover, people who wish to buy a NEV will get a purchase subsidy up to tens of thousands Renminbi (RMB) [

13]. In 2014, because of the explosive growth of production and sales of the NEV industry, 2014 was called “the first year of new energy vehicle consumption” by the research institute of Ministry of Commerce of the People’s Republic of China (MCPRC) [

14]. The data released by CAAM show that the production and sales volume were 51.7 million and 50.7 million in 2016, respectively [

15].

To sum up, the automotive industry in China has been rapidly growing. However, whether the firms efficiently operated and the efficiency gap between new energy and traditional vehicle sub-industries are vital for the sustainable development of the automotive industry. Thus, we need to find an appropriate model to measure the efficiency of the automotive firms, and the previous studies on the efficiency evaluation are useful guidelines for our research. Some of them are based on the financial ratios, using traditional statistical methods including principal analysis (see [

16,

17]) and factor analysis (see [

18,

19,

20,

21,

22]). However, when it comes to evaluating the performance of firms with multiple inputs and outputs, data envelopment analysis (DEA) is more appropriate to be used in the situation. Moreover, we do not need to predetermine the weights of inputs and outputs in the DEA [

23]. Additionally, the efficiency evaluation based on DEA has no needs of the setting of a production function, which measures the relative efficiency with the efficient frontier built by the sample (see [

24]).

DEA has been applied to the comparative analysis of the efficiency of productive units in various economic sectors, including the automotive industry. González, Cárcaba, and Ventura used DEA to measure the product efficiency of the vehicles in Spain [

25]. By using the DEA and Malmquist model Voltes-Dorta, Perdiguero, and Jiménez made a detailed analysis on the emission efficiency of Spanish cars [

26]. Choi and Oh evaluated the product efficiency of traditional vehicles and hybrid vehicles using DEA [

27].

The studies related to China’s automotive industry were as follows. Jiang and Zhang introduced Charnes Cooper Rhodes (CCR) and Charnes Cooper Golany Seiford Stutz (C

2GS

2) DEA models to measure the research and development (R&D) efficiency of a Chinese automotive firm [

28]. Tan researched the investment effectiveness of automotive firms with DEA, the study showed that most firms were at the stage of increasing returns to scale in 2003, which meant the sizes of firms were smaller than the optimal scales [

29]. Liu and Wu made an efficiency analysis of the listed automotive firms and found that the low level of technical efficiency resulted from the low level of scale efficiency, their results showing that the scale efficiency gap was continuously large in 2005 [

30]. Based on the sample of automotive firms from 2005 to 2007, Huang pointed out the overall technical efficiency decreased over time and some firms in a state of constant returns to scale turned out to be firms with increasing returns to scale [

31]. The study of Wang et al. suggested that there was rapid growth in the scales of inputs and outputs of China’s automobile industry from 2006 to 2010. However, the growth rate of sales and production decreased in 2011, and the scale expansion of the industry should be carefully treated in case of the potential decline of the demand [

32]. Zhou and Liu pointed out that because of the decline of air quality and the demand of achieving carbon reduction targets, NEVs drew public attention. Meanwhile, because there was a long way for people to change consumption habits, the market for NEVs was not mature and the consumption custom needed to be cultivated [

33].

As these DEA models are mainly used in analyzing the efficiency of Decision-Making Units (DMUs) in a static way, the combination of DEA and Malmquist models can measure the growth of the total factor productivity of each DMU year by year [

34]. Moreover, the application of Malmquist models can provide detailed decomposition, which is useful for the dynamic analysis. Therefore, we built DEA and Malmquist models for the efficiency evaluations of the automotive industry and the detailed setting of the models and results are shown in the following section. Gonzalez et al. pointed out that the combination of technology, useful models, and analysis is beneficial to the decision-maker [

35].

The rest of paper is structured as follows:

Section 2 presents the concept of data envelopment analysis (DEA) and Malmquist model, and shows our model setting and data sources. In

Section 3, the descriptive statistics are given in the beginning of the section. By using our DEA and Malmquist models, we make an overall and further analysis of the automotive industry. Based on the data manually collected from the publicly-disclosed financial statement, we present an efficiency comparison in terms of the sub-industry level. Based on the descriptive statistics, we find that the size of each firm is quite different. Further research is presented by dividing the firms into five groups depending on their sizes. Additionally, the robustness based on prior research is given. The discussions and conclusions based on the industry development and the efficiency evaluations are given in

Section 4.

2. Materials and Methods

2.1. Data Envelopment Analysis (DEA)

DEA, as a methodology for the efficiency evaluation of Decision-Making Units (DMUs) with multiple inputs and outputs, is widely used in various areas. The basic idea of DEA is to fit a non-parametric efficient production frontier with DMUs and measure the efficiency relative to the best-performance observations in the sample. This methodology was first put forward by Charnes et al. [

36], which was called CCR-DEA model with the assumption of constant returns to scale. Banker et al. [

37] modified the model with the assumption of variable returns to scale, thus, their Banker Charnes Cooper (BCC)-DEA model could decompose the technical efficiency into the scale efficiency and pure technical efficiency.

In this paper, the China’s listed firms in the automotive industry are seen as the DMUs, and our goal is to measure the efficiency of each DMU and identity the ones that use the inputs more efficiently than the others that have resources over-utilized, namely, the firms can reduce the inputs while the outputs remains constant (input-oriented) rather than the firms can increase the outputs while their inputs remains constant (output-oriented). Therefore, the input-oriented model of DEA is appropriate for our research.

Suppose there are

DMUs,

has

types of inputs

and

types of outputs

. If we want to measure the technical efficiency (

), the linear programming of an input-oriented CCR-DEA model can be expressed as follows, where the input and output data matrices

and

and

are the input and output weights,

The linear form of CCR-DEA model can be written as follows:

The dual form can be written as follows:

In the DEA model, the efficiency value (

) is less than or equal to 1 while it is greater than 0. Farrel pointed out that the technical efficiency measured the quality of inputs [

38]. A DMU is considered to be DEA technical-efficient only if

. In other words, the DMU cannot reduce the inputs while the outputs remain constant, which means it is operating on the efficient production frontier. For the DMU which is not technical efficient, there are redundancy in inputs.

The CCR-DEA model under the assumption of constant returns to scale can be expanded to the model under the assumption of variable returns to scale. Based on [

37], we can further derive the pure technical efficiency and scale efficiency by imposing the condition

, which is called the BCC-DEA model. The pure technical efficiency refers to the efficiency measured under the assumption of variable returns to scale. The scale efficiency reflects whether the DMU is operating at the optimal size. In BCC model, a DMU is considered to be DEA weak-efficient only if the pure technical efficiency or scale efficiency equals 1. Besides, a DMU is considered to be DEA efficient only if both the pure technical efficiency and scale efficiency equal to 1.

2.2. Malmquist Model

The Malmquist total factor productivity index model which is suitable for panel data, is used in our research. The Malmquist index was originally put forward by [

39], which referred to the change of total factor productivity. Farrel defined the measurement of technical efficiency based on the efficient production function [

38]. Caves et al., Färe et al., and Färe et al. introduced the idea into the application of DEA [

40,

41,

42].

The input-oriented Malmquist index, namely, the total factor productivity index, which measures the change in productivity of a DMU

to period

is written as follows:

where

and

refer to the technological feasible production vectors of

and period

,

,

is a distance function of

which is defined as the maximum proportional contraction of the input vector

, given the output vector

, namely,

, which shows that

is feasible with the production technology at time

. We can define

,

, and

similarly. If the Malmquist index is higher than one, or equal one, it refers to the progress of total factor productivity or the total factor productivity remains at the same level as before. If the Malmquist index is lower than one, it refers to the regress of the total factor productivity.

According to [

40,

41,

42], the Malmquist index, which measures the Total Factor Productivity can be decomposed as follows:

where

and

are the distance functions of

and period

, and

and

are the abbreviations of the technical change (the change of efficient frontier between the two periods) and the change in technical efficiency (the increase or decrease of a DMU in technical efficiency). Note that the production technologies used in the distance functions in Equations (3) and (4) are based on the assumption of constant returns to scale. If

and

are greater than, less than or equal to one, there is progress, regress or no change in terms of frontier technology and technical efficiency, respectively.

Further, the change in technical efficiency in Equation (3) can be expressed as follows:

where

and

are the distance functions of

with the underlying production technology exhibiting variable returns to scale (increasing returns to scale or decreasing returns to scale) and constant returns to scale. Correspondingly,

and

are the distance functions with the underlying period-

production technology exhibiting variable returns to scale (increasing returns to scale or decreasing returns to scale) and constant returns to scale.

and

are the abbreviations of the pure technical efficiency change and the scale efficiency change. Similarly, if

and

are higher than, lower than or equal to one, there is increase, decrease or no change in terms of frontier technology and technical efficiency, respectively.

2.3. Variable Selection and Data Sources

In the automotive industry, the fixed assets (e.g., machinery, equipment, and plants), intangible assets (e.g., patents, non-patented technology, trademarks), and operating expenses, which play an important role in the operation of a company, are chosen as the capital inputs. In this paper, we use the net value of fixed assets and intangible assets, which reflect the real value of assets. The number of employees is chosen as the input in terms of human resources, which is used in most studies. Therefore, four variables including the number of employees and the fixed assets, the intangible, and the operating expenses are chosen as the input indicators.

The operating income, which refers to the income from the main business activities of an automotive firm, is chosen as the output indicator.

All the data are collected from the public disclosed financial reports of the listed firms, and the monetary values of the inputs including the operating expense, the fixed assets, intangible assets and operating income are in million Renminbi. Renminbi (RMB), namely, the Chinese Yuan, is the official currency of the People’s Republic of China. Since the indicators released in the original financial reports were in Renminbi, we do not need to make foreign exchange rate adjustments to the indicators.

3. Results

3.1. Sample Description

The aim of this paper is to make a static and dynamic analysis of the listed automotive firms in China. According to the industry classification of each firm, we select 140 automotive firms mainly engage in the manufacturing of automobiles, automobile parts and accessories, or both. Moreover, in China’s stock market, firms with special treatment in the sample period, which are usually considered to be abnormal in financial conditions or other aspects, are excluded. Furthermore, based on the financial statements, we screen out the firms whose main business had significantly changed in the sample period, and 95 firms are chosen. Additionally, the firms without available and sufficient amounts of financial figures during the sample period are not included in the sample. Finally, 77 firms listed in the form of A-shares and traded on the Shanghai Stock Exchange and the Shenzhen Stock Exchange are selected as the sample. The names and abbreviations of the sample firms are shown in

Table A1. Throughout the rest of the paper, we use the abbreviation (namely, the name of a firm is shortened to a four-digit abbreviation of its Chinese stock’s name in Pinyin) of each firm for conciseness in referring to the name of a company, and the abbreviations are adjusted according to Chinese Pinyin when different firms share the same abbreviations due to the homophone phenomenon in Chinese. The descriptive statistics are shown in

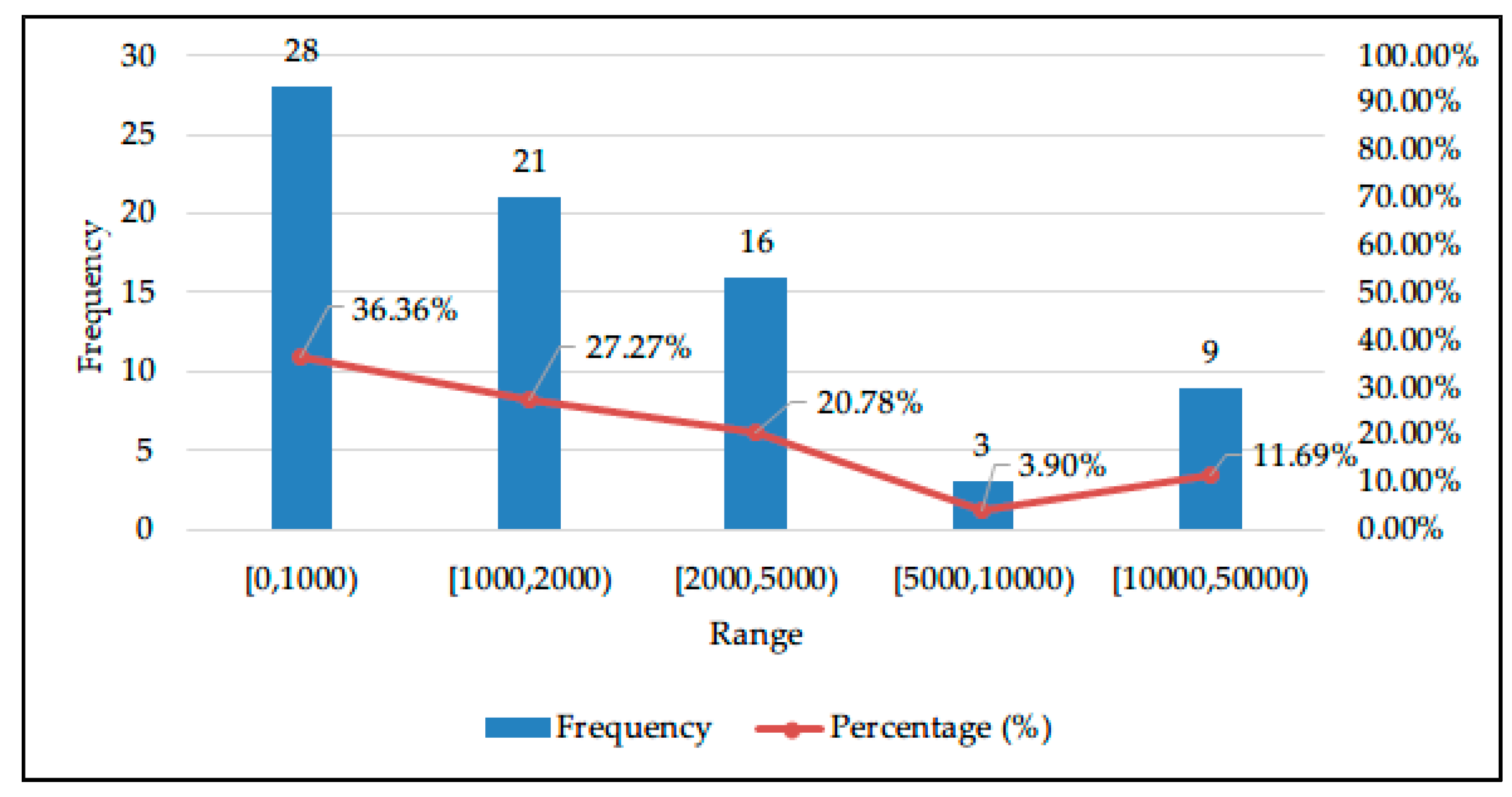

Table 1. Clearly, the distributions of variables are highly skewed. Therefore, we take the data in 2016 as an example and showed the size distribution of the listed automotive firms, and the size of a firm is measured by its fixed assets.

Firms are divided into five groups depending on the size of their fixed assets: Group A (Extra Small), 0 ≤ Size < 1000; Group B (Small), 1000 ≤ Size < 2000; Group C (Medium), 2000 ≤ Size < 5000; Group D (Large), 5000 ≤ Size < 10,000; Group E (Extra Large), 10,000 ≤ Size < 5000. Note that the unit for fixed assets is one million RMB.

According to

Figure 1 and our calculation, more than 60% of firms belong to the Extra Small group or the Small group, however, they only accounted for 4.97% and 9.3%, respectively, of the industry scale based on our calculation. Nearly a fifth of total firms are in the Medium group, and they account for 15.53% of the industry size. There are three and nine firms in the Large and Extra Large groups, respectively, and their proportions of the total industry in terms of the size are 6.60% and 63.60%. Overall, there is a marked contrast between each group. Further analysis is presented in

Section 3.4.

3.2. Overall Analysis

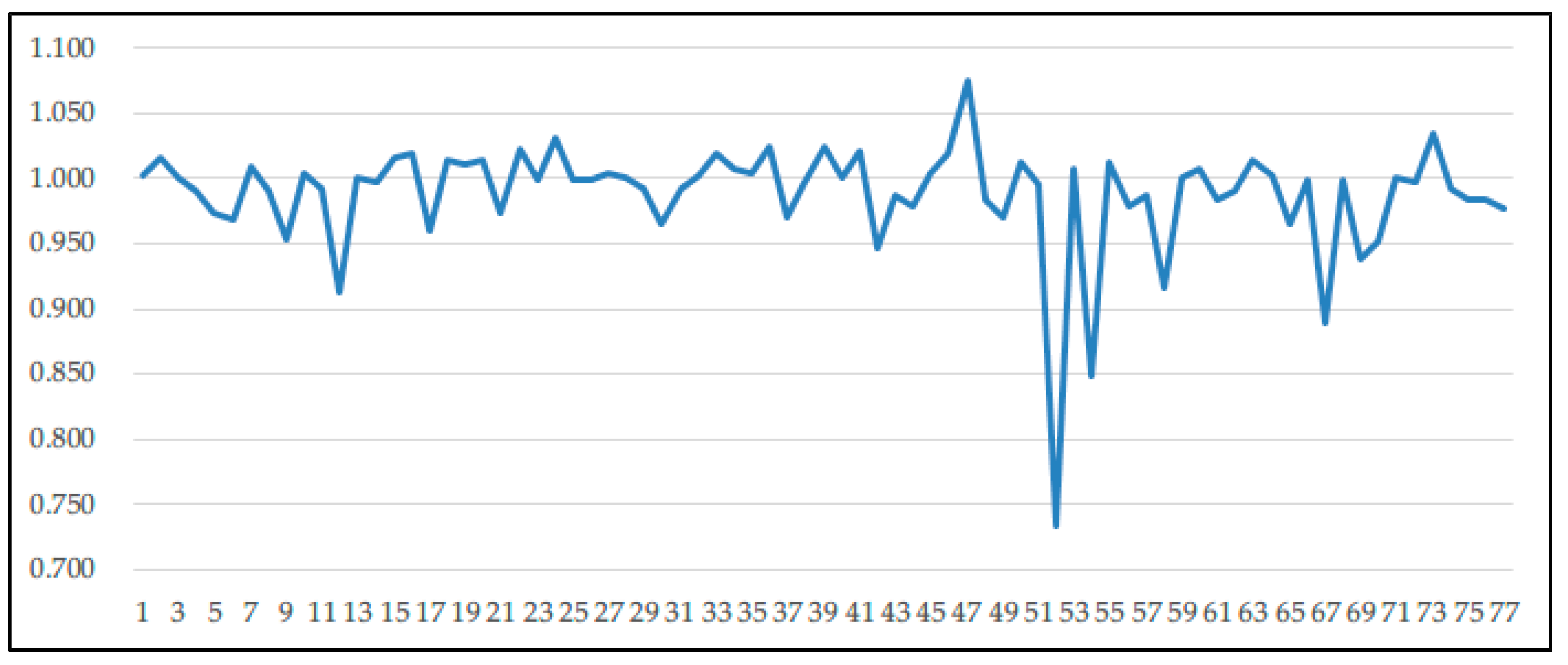

In this section, we report the results of an application of the Malmquist total factor productivity index model to panel data on 77 listed A-share firms for the years 2012–2016.

Table 2 shows the detailed measurement result. The graphical representation of the Malmquist indices is shown in

Figure 2. According to the figure, for different firms in the automotive industry, the change of total factor productivity, which is measured by Malmquist index during the period of 2012–2016, varies considerably.

However, our year-by-year analysis based on the efficiency data shows that the movements of the Malmquist index and its factors are not the same. From 2012 to 2013, the total factor productivity of the whole automotive industry decreased by 3.4%. The main reason was that the industry was faced with a negative technical progress. Meanwhile, the improvement of efficiency change, which was mainly due to increase of scale efficiency, alleviated the influence to some extent. In 2014, the total factor productivity remains decreasing. The technical change index continued to decrease by 4.5%, however, because of 2.2% and 2.0% improvements of pure technical efficiency and scale efficiency, the efficiency change index increased by 4.2%, and the decline narrowed to 0.5%. In the next year, for the whole industry, the efficiency turned to decrease while there was technical progress. In 2016, the total factor productivity of the automotive industry increased by 0.5%, which was benefit from the enlarged technical progress. However, the continuous decline of technical efficiency suggested that there was a certain amount of input slacks or the scale inefficiency of the automotive firms.

3.3. Further Analysis

In the above section, we discuss about the efficiency change of automotive firms based on Malmquist model, and find that the changes of the overall efficiency were quite different from 2012 to 2016. In this section, we make a further analysis of the efficiency change of 77 firms during the sample period. Cte, Tc, Cpe, Cse, and Tfpc refer to the change in technical efficiency, the technical change, the pure technical efficiency change, the scale efficiency change, and the Malmquist total factor productivity index, respectively.

According to

Table 3, the five-year average Malmquist indices of all the listed firms slightly decreased by 1.3%, which was due to the 1.6% decline of the technical change and 0.3% improvement of the efficiency change. Furthermore, the increase of the latter one stemmed from the 0.5% increase of the scale efficiency change and the 0.2% decrease of the pure technical efficiency change.

Table 3 shows that the five-year average Malmquist total factor productivity index of all the firms in the automotive industry spanning from 2012 to 2016. In terms of the total factor productivity of firms in the automotive industry, on the one hand, MCKJ, GQJT, XPGF, WAKJ, and BYD are the top five fastest-growing firms with growth rates of 7.6%, 3.5%, 3.2%, 2.5%, and 2.5%, respectively, which is primarily due to the increase of efficiency. On the other hand, there are significant drops in terms of Malmquist index for SQJT, YXKC, HYQC, AKKC, and FSGF, with the decrease of 26.7%, 15.1%, 11.1%, 8.8%, and 8.4%, respectively, and they are the result from the considerable negative technical progress or the decreasing efficiency, especially the former.

3.4. Sub-Industry Analysis

In this section, by manually collecting the data of main business from the public disclosed financial statements of the sample, we subdivide the automotive industry into the traditional vehicle industry and the NEV industry.

Table 4 and

Table 5 show the efficiency evaluations of 22 NEV firms and 55 traditional vehicle firms in 2016. As shown in the following tables, 81.8% and 90.0% of firms in the NEV industry and traditional vehicle industry were not DEA-efficient in 2016, respectively. Furthermore, 83.3% and 82.0% of the above firms were neither scale efficient nor pure technical efficient. Therefore, for most automotive firms, no matter the sub-industry a firm belonged to, there was room for the efficiency enhancement.

According to

Table 4, In the NEV industry, four NEV firms (JDKJ, SQJT, JLQC, and HYQC) were DEA-efficient, as they were both scale-efficient and pure technical-efficient. Benefiting from the growth of supporting business of the firm’s major customers, JDKJ realized the sales growth of main products, and the export sales increased by 42.19%. Additionally, JDKJ produced the spare parts of the Volkswagen NEV Project, which could support the growth of its main business. Currently, SQJT is not only the largest automobile production and marketing group in China, but also the largest automotive firms listed in the A-share stock market. In 2016, the NEV sales of SQJT exceeded 25,000 units with the models of e550 and e950, which was an increase of 85% over the same period of last year. The sales of NEVs produced by JLQC were at the forefront of the industry in 2016, and the firm took advantage of its own network layout and actively participated in the “the Belt and Road” initiative and the export sales continued to grow (e.g., JLQC obtained the order of all-aluminum electric buses in Paris). HYQC accelerated the international operation of automotive interior and the other main business, established contacts with international automobile manufacturers including Volkswagen and General Motors, and promoted the coverage of main business in regional markets of North America, Europe, and Southeast Asia, which brought 44.75% of the operating income in 2016.

In

Table 4, three NEV firms (YYDQ, YXKC, and YTKC) were DEA weak-efficient in 2016, as they were only efficient in terms of pure technical efficiency. YYDQ and YXKC were in a state of increasing returns to scale, indicating that the reasonable scale expansion was likely to realize the enhancement of the scale efficiency. However, the efficiency evaluation shows that the size of YTKC was bigger than the optimal level, which meant the expansion of inputs did not results in the same amount of outputs. Additionally, it is clearly shown in

Table 4 that the gap between pure technical efficiency of firms results in the difference of technical efficiency because of the smaller of the scale efficiency gap.

According to

Table 5, in the traditional vehicle industry, there are five DEA-efficient firms (NFZC, MCKJ, ZGQY, FSGF, and FYBL) in 2016. NFZC takes a leading position in the manufacturing and R&D of needle bearing and the product quality has been generally recognized in the domestic and foreign markets. MCKJ achieved the operating revenue of 2950.15 million RMB in 2016 with an increase of 63.61% over the same period of the previous year, which was mainly due to the optimization of the customer structure and the upgrading and replacement of products and the pick-up of the automotive market. ZGQY actively explored the market and made a full use of the capacity of the new base. In 2016, ZGQY realized the revenue of 792 million yuan with an increase of 16.99%. FSQF was one of the largest all-steel radial tire manufacturing enterprises and one of the largest tire manufacturer of construction machinery in China. Over 40% of the products were sold in more than 150 countries and regions. In 2016, the sales volume of FYBL automotive glass increased by 3007.57 million RMB with the growth rate of 22.89%, the firm strengthened the development of functional products and high value-added products, realized the goal of energy saving plan and therefore the revenue increased.

Apart from the five firms, nine firms were DEA weak-efficient in 2016. SCGF, CCQC, TEJ and TXYB were in a state of pure technical efficiency, and the optimal sizes of three of them were higher than the current size, especially TXYB. XYGF, YTGF, MSuKJ, XMZT, and MShKJ were scale efficient in 2016, which meant there was a certain degree of input slacks of these firms. According to

Table 4, we find that the characteristics of the traditional vehicle industry was similar to that of NEV industry, the scale efficiency of a firm was closed to another firm in most cases, and the variation of pure technical efficiency caused the technical efficiency gap. This implies that the slacks of inputs had been the common phenomena in both sub-industries, i.e., the firms could realize efficiency improvements by reducing their inputs to some extent. Additionally, in

Section 3.1, we find the high skew phenomenon in the distributions of automotive firms. Moreover, 15.58% of firms in the Extra Large or Large group account for 63.60% of the industry size while 63.64% of firms in the Extra Small or Small group only account for 14.28% of the industry size. More importantly, which group performs better is a key element of the industry sustainability. Based on the measurement of firms in 2016, the result is shown in

Table 6. For the NEV industry, firms in the Extra Large or Extra Small groups perform better than the other groups. For the traditional vehicle industry, the Extra Large and Large group outperform the other groups.

In

Table 7, for the traditional automotive industry, the overall technical efficiency from 2012 to 2016 is 0.875, and the scale efficiency is 0.970, which is larger than the pure technical efficiency (0.903). For the NEV industry, the technical efficiency is 0.902, which is slightly higher than that of the traditional vehicle industry, and so does the pure technical efficiency of NEV industry. The difference of scale efficiency of NEV and traditional automotive industry is quite small.

Then we analyze in detail, it is found that the pure technical efficiency and scale efficiency of the NEV industry are almost continuously larger than that of the traditional vehicle industry during the sample period, which results in the higher efficiency of the NEV industry than that of traditional vehicle industry. The efficiency gap was wide in 2012, and became narrow in the next two years. During the past two years, the gap turned to be wider than before, due to the higher pure technical efficiency, which means the NEV industry performs better than the traditional vehicle industry on the whole.

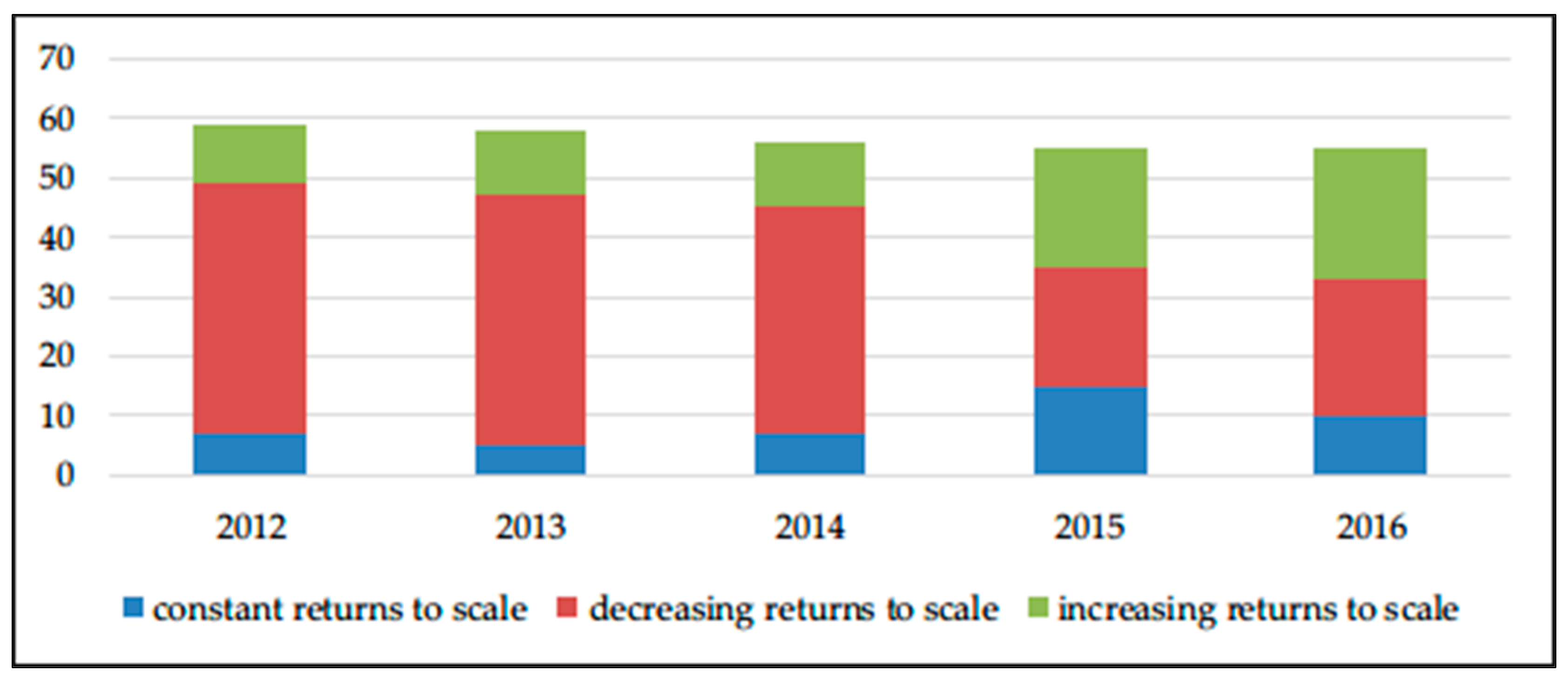

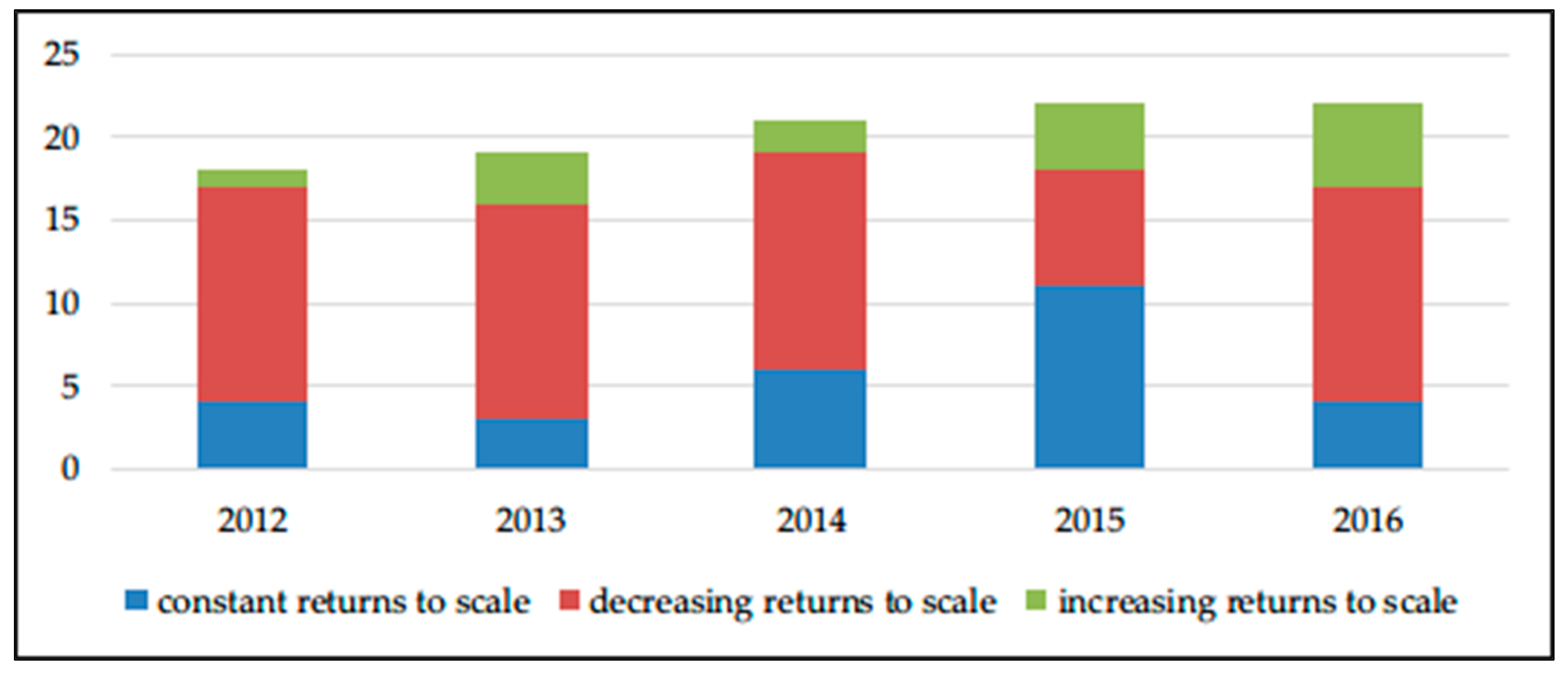

Figure 3 and

Figure 4 show the returns to scale of the traditional vehicle and the NEV industry. By using our DEA model, a large proportion of both the firms in the NEV and traditional vehicle industry were in a state of decreasing returns to scale during the period of 2012–2014. Meanwhile, the numbers of firms in two sub-industries with constant returns to scale and increasing returns to scale increased in the next year, especially the NEV firms. In 2016, the firms faced with decreasing returns to scale accounted for the largest proportion of the total. NEV firms operating at the efficient frontier sharply decreased by more than 30% while that of traditional vehicle firms dropped only by 9.0%. It is clear from the figure that, in 2016, the proportion of both the traditional vehicle and NEV firms with increasing returns to scale continued to increase, and the former one reached more than 40% while the latter reached by nearly 22%. This implies that the situation of NEV and traditional vehicle industry was same in 2012, but different in 2016. First, many firms are still in a state of decreasing returns to scale in both industries, especially the NEV firms, which indicates their scales were too large to maintain effective operation. Second, the number of NEV firms with constant returns to scale decreased steeply, indicating the resources of some firms were not efficiently used. Third, for the traditional vehicle industry, there were a certain number of firms with increasing returns to scale, which meant there was significant room for efficiency improvement after reasonable expansion.

3.5. Robustness Analysis

In the section, we conduct a robustness analysis based on the research of Delimiro et al. [

43]. We can know how robust our measurements are by excluding some variables that are highly correlated with the other variables in the model, and it is found that the fixed assets are highly correlated with the intangible assets and the number of employees. Therefore, we build three models by excluding one of them respectively, and make an efficiency comparison between the base model in

Section 3.4 and the model for robustness analysis (see

Table A2). As shown in

Table A2, for most firms, the technical efficiency difference between the base model and the robust model is slight. Additionally, another robust model is built (see

Table A3) by excluding the firm (SQJT) with the maximum size and the firm (TEJ) with the minimum size, and the result shows that our measurement are robust for most firms. Overall, data envelopment analysis is an effective way to measure the efficiency of listed automotive firms, and our model shows good robustness.

4. Discussion

Our research using the DEA model and Malmquist index approach makes a static and dynamic efficiency measurement of China’s listed automotive industry consisting of traditional and NEV firms. The summary and implications of the results are shown below.

First, the year-by-year Malmquist analysis shows that the influences of the factors on the Malmquist index are different. During the periods of 2012–2013 and 2013–2014, with the increasing concerns of air quality, PM

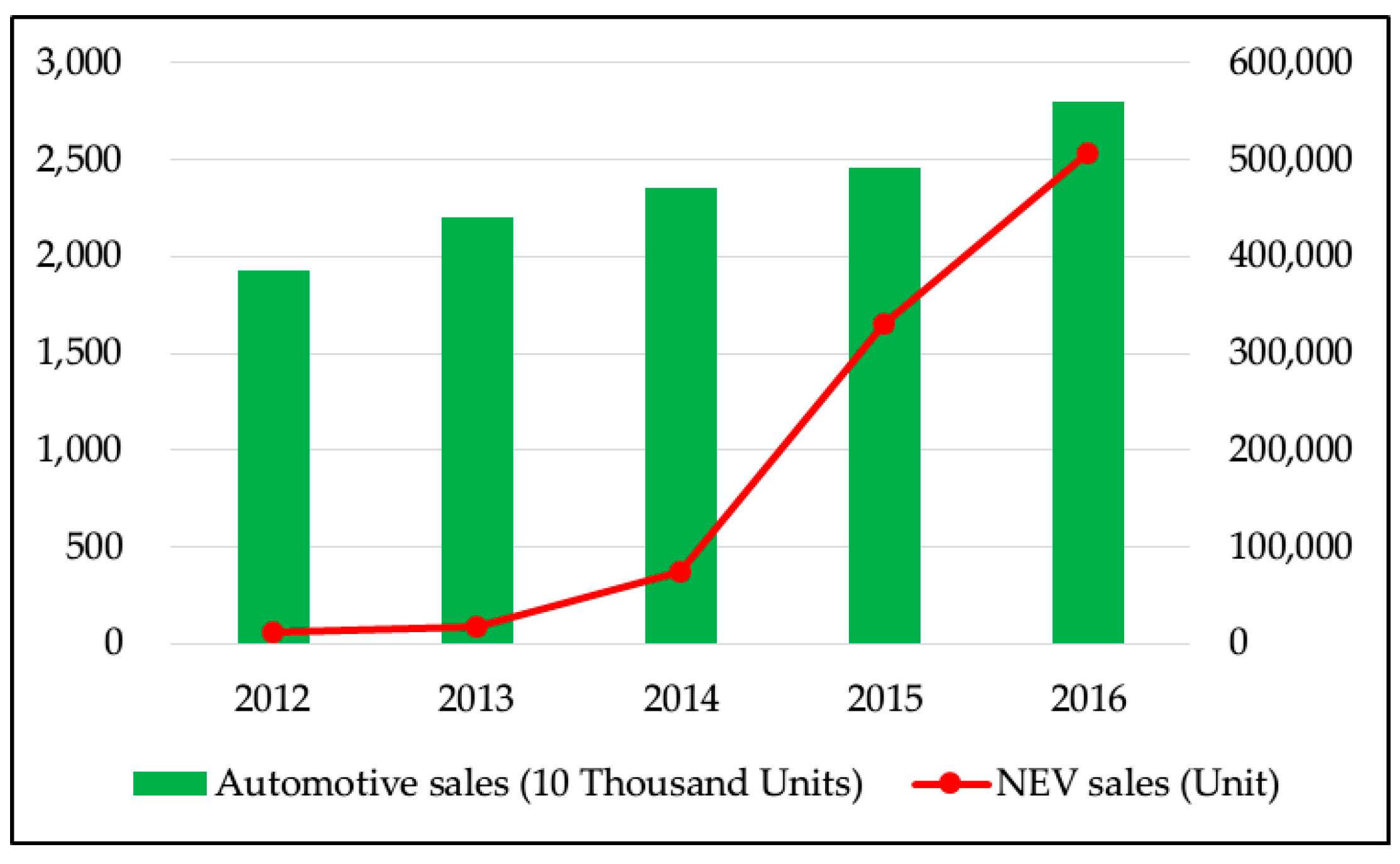

2.5, haze, and traffic congestion, “the restriction policy of car purchase” have been implemented in Beijing since 23 December 2010. Guangzhou issued the policy on 30 June 2012. Tianjin announced the policy on 15 December 2013. Hangzhou implemented a similar policy on 26 March 2014. Shenzhen implemented a car purchase restriction policy on 18 December 2014. Therefore, the sales and production is influenced by the government policy to some extent, which could partly explain the reason the overall technical regress of the automotive industry during the periods. In the background of the increasing demand of NEVs, the improving of charging infrastructures, the expansion of product lines, and government support of NEV purchases, including tax incentives and government subsidies, as is shown in

Figure 5, there is a rapid growth of the NEV sales in China based on the publicly-disclosed data from CAAM (see [

44,

45,

46,

47,

48,

49,

50,

51,

52]), which facilitates the growth of revenue of the whole industry, i.e., the growth of technical change during the periods of 2014–2015 and 2015–2016. The technical change reached a peak from 2015 to 2016. Additionally, the change of technical efficiency from 2014 to 2016 suggested there was room for the improvement of efficiency in the automotive industry.

Second, the average total factor productivity of different firms during the period of 2012–2016 considerably varies and the Malmquist analysis at the firm level proves the point. Therefore, we further discuss the technical efficiency of the firms in 2016. In this paper, the firms are subdivided into two groups: the traditional vehicle and the NEV. From the perspective of technical efficiency, four NEV firms and five traditional vehicle firms were running at the efficient frontier in 2016. In terms of the pure technical efficiency and scale efficiency, our research, based on 77 firms spanning from 2012 to 2016, shows, firstly, that the scale efficiency gap was not as large as in Liu and Wu [

30]. Additionally, the scale efficiency for most firms was higher than 0.9 in 2016. Secondly, the finding that there was a certain number of firms in a state of decreasing returns to scale in both industries was different from [

29], especially the NEV firms, and the characteristics of two sub-industries on returns to scale was the same in 2012 but different in 2016, which indicates that the development stage of China’s automotive firms changed and the firms should pursue for the efficient growth based on the development of the sub-industry, rather than the simple scale expansion. Third, we should notice that the scale efficiency and the pure technical efficiency of the NEV industry was relatively higher than that of the traditional vehicle industry during the sample period, which resulted in the higher efficiency of NEV industry. Besides, during the past two years, the efficiency gap turned out to be wider than before, due to the higher pure technical efficiency, which showed there was a bright future for the NEV industry, while the traditional firms should actively optimize the allocations of inputs and achieve the efficiency improvements.

Third, we find the high skew phenomenon in the distributions of automotive firms in

Section 3. By classifying the firms into five groups according to size, the result clearly shows that the technical efficiency of NEV firms in the Extra Small group stands out among all groups. For instance, YXKC and YYDQ in the Extra Small group performed well in 2016. YXKC has a strong team of experts from the United States, Australia and Europe. They have advanced design concepts, which forms the core technical force. The quality of their products (NEV bus) has been recognized by the market. YXKC seizes the opportunity of the NEV policy from Chinese government. The technical efficiency of YXKC was 0.992 in 2016, and YXKC ranked number 11 in 77 automotive firms for the technical efficiency. YYDQ is a National High-Tech Enterprise in China, which have the ability of independent research, development and innovation. According to the publicly-disclosed information of YYDQ, the cost of research and development accounts for more than 5% of the operating income every year. YYDQ is one of the leading enterprises in terms of the intelligent power controller of the automobiles, and the technical efficiency of YYDQ was 0.998 in 2016, which ranked 10th in the automotive industry for the technical efficiency. Though the sizes of two firms are relatively small, YXKC ranked number 71st of 77 automotive firms and YYDQ ranked 64th in 77 automotive firms in 2016. However, they are outstanding firms with high technical efficiency. Compared with the production of traditional vehicles, which is more routinized and fixed, the production of new energy vehicle is more of an innovative and expansive mode that facilitates efficiency of the small firms.

Currently, there were only 22 China NEV firms in 2016, and we believe that with the increasing concerns of the energy and the environment, there will be more and more firms turn to be NEV firms. Additionally, the market competition will be fiercer. Nowadays, world famous companies such as the Amazon.com Incorporated (Amazon.com Inc., Seattle, Washington State, the United States), the Apple Incorporated (Apple Inc., Cupertino, State of California, the United States), etc. were small at startup; then, being superpowers in innovation, grew from small firms to large firms and even giant firms gradually. Our result shows that, no matter the size of a firm, only the firm which seizes the development opportunity and makes fully use of the resources can succeed, and we believe a few of them (especially the NEV firms) will become leading enterprises similar to Amazon.com Inc. and Apple Inc.

According to the 2016 Annual Report on the National Economy and Social Development, China’s private car ownership reached 165.59 million [

53]. With the increase of car ownership, the automotive market tends toward saturation. In addition, with the support of government and the advantage of NEVs in terms of technical progress, the NEV industry is likely to be a new driving force of the economy, therefore, the competition between NEV firms and traditional firms will be more and more competitive. Thus, the improvement of efficiency is the key for firms to succeed.

Our major contributions were as follows: First, we make an efficiency evaluation based on DEA and Malmquist models, statically and dynamically measuring the efficiency of listed automotive firms. Second, as previous studies concentrated on the firms’ performance before 2012, our research, based on the panel data of 77 listed A-share firms and the period between 2012 and 2016, contributes to the existing literature. Third, we manually collect the data of main businesses from the publicly-disclosed financial statements, and subdivide the automotive industry into the traditional vehicle industry and the NEV industry, the results showing that the characteristics of the whole industry and the sub-industries changed with the development of the industry.

With the rapid development of NEV industry, NEV is likely to be the mainstream and gain more and more profit in the automotive market. Additionally, the development of NEVs will contribute to the reduction of carbon emissions. Further research may include the estimated carbon emission reduction of the automobiles produced by a firm as an output, so the green efficiency of the automotive firm can be measured.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}