Environmental Parametric Cost Model in Oil and Gas EPC Contracts

,

,

Abstract

:1. Introduction

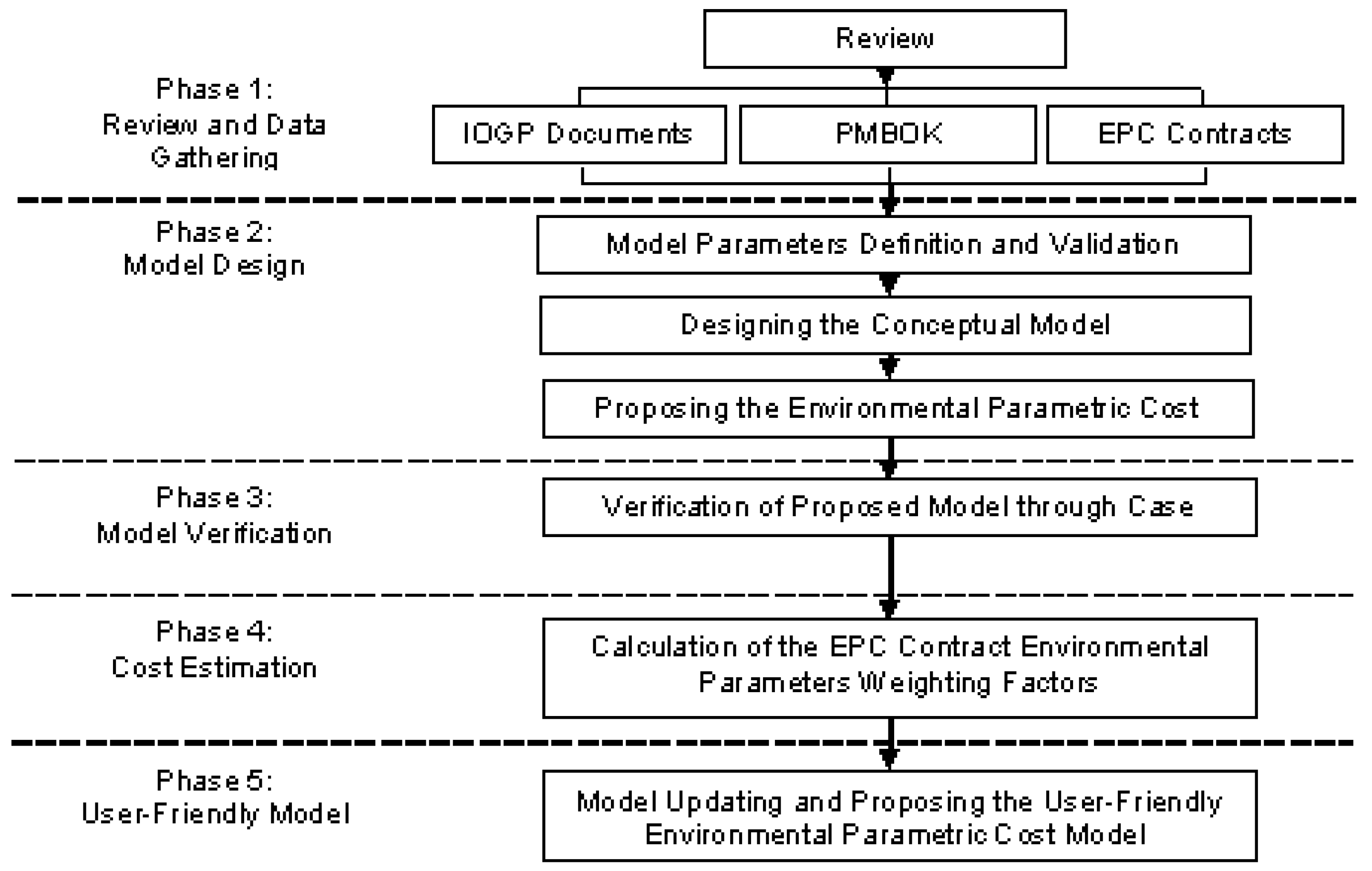

2. Materials and Methods

- The bottom-up cost estimation method was used to calculate the cost of each environmental management parameter (work package), separately;

- The group decision making technique (Delphi technique) was used to validate the identified environmental management parameters (work packages); and

- The parametric modelling was used to design the environmental parametric cost model.

3. Results and Discussion

3.1. Model Parameters Definition and Validation

3.2. Designing the Conceptual Model

3.3. Designing the Environmental Parametric Cost Model

IRy(n−1))/100) + Cy(n−1))]

El.C + Inst.C + TFC + CCC + SSCC + VSPCC + EMSC

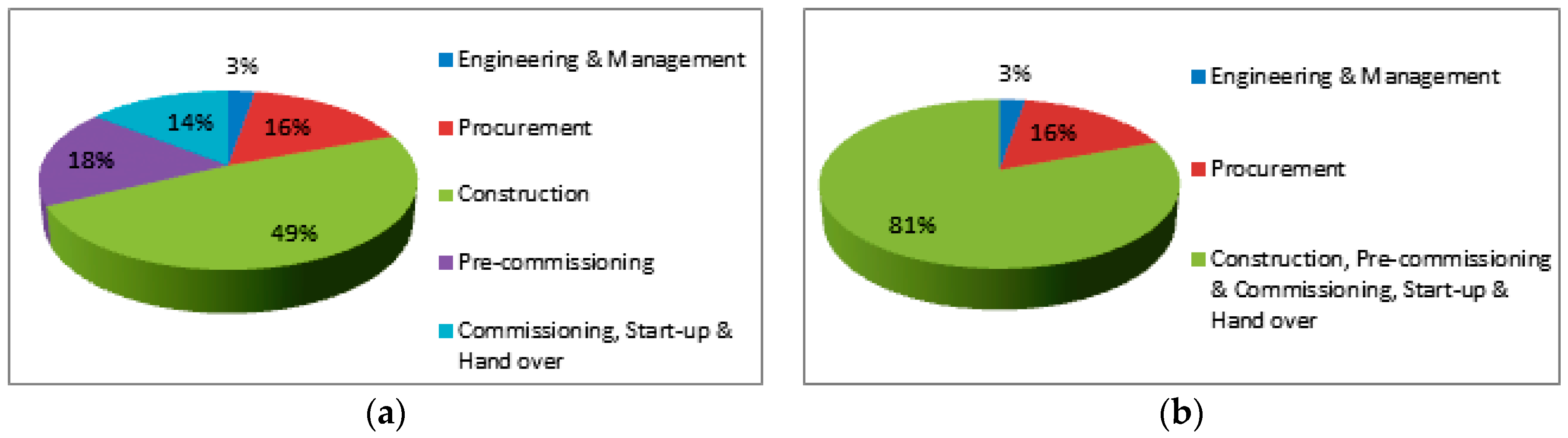

3.4. Verification of the Designed Model by Case Study

3.5. Calculation of the EPC Contract Environmental Management Weighting Factors

4. Conclusions

- Internal costs of projects included:

- Environmental Pollution Prevention Costs: The costs of activities to prevent the production of pollutants including pollution control equipment, designing processes, designing products and carrying out environmental studies.

- Environmental Detection Costs: The costs of compliance with appropriate environmental standards.

- Environmental Internal Costs: The costs of remedial actions to eliminate and manage the wastes produced including the costs for operating pollution control equipment, licensing facilities for producing pollutants and costs resulting from recycling scrap.

- External costs of projects included environmental degradation costs and human impact costs.

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Description | Abbr. |

|---|---|

| Building Cost | BC |

| Basic Design Cost | BDC |

| Catalyst & Chemicals Cost | Ca.&Che.C |

| Construction Camp Cost | CCC |

| Civil Cost | Ci.C |

| Construction, Pre-comm., Commissioning, Start-up and Hand-Over Cost | CPCSHC |

| Detail Design Cost | DDC |

| Environmental Base Study | EBS |

| Environmental Cost | EC |

| Equipment Erection Cost | EEC |

| Environmental Impact Assessment | EIA |

| Electrical Cost | El.C |

| Engineering & Management Cost | EMC |

| Environmental Management System | EMS |

| Environmental Management System Cost | EMSC |

| Engineering, Procurement and Construction | EPC |

| Environmental Parameters Cost | EPC |

| Equipment Cost | Equ.C |

| Fire Proofing Cost | FPC |

| Health, Safety and Environmental Management System | HSE-MS |

| Insulation Cost | Ins.C |

| Instrument Cost | Inst.C |

| International Association of Oil and Gas Producers | IOGP |

| Inflation Rate | IR |

| Jetty Cost | JC |

| Jetty Construction Cost | JCC |

| Management Cost | MC |

| Parameter | P |

| Painting Cost | Pa.C |

| Procurement Cost | PC |

| Project EMS Cost | PEMSC |

| Piling & Foundation Cost | PFC |

| Piping Cost | Pi.C |

| Project Total Cost | PTC |

| Project Total EMS Cost | PTEMSC |

| Project Total Weighting Factor | PTWF |

| Safety & Fire Fighting Cost | SFFC |

| Site Preparation Cost | Si.Pr.C |

| Support Service to Client Cost | SSCC |

| Storage Tanks Cost | STC |

| Steel Structure Cost | St.St.C |

| Telecommunication Cost | Tc.C |

| Technical | Tech. |

| Temporary Facility Cost | TFC |

| Vendor Staff and Pre-comm. & Commissioning Cost | VSPCC |

References

- Project Management Institute (PMI). A Guide to the Project Management Body of Knowledge (PMBOK Guide), 2000 ed.; Project Management Institute: Newtown Square, PA, USA, 2001; ISBN 1-880410-22-2. [Google Scholar]

- IOGP (International Association for Oil and Gas Producers). HSE Management—Guidelines for Working Together in a Contract Environment; Report No. 423; International Association for Oil and Gas Producers: London, UK, 2014. [Google Scholar]

- Hofer, C.; Cantor, D.; Dai, J. The competitive determinants of a firm’s environmental management activities: Evidence from US manufacturing industries. J. Oper. Manag 2012, 30, 69–84. [Google Scholar] [CrossRef]

- De Burgos-Jimenez, J.; Vazquez-Brust, D.; Plaza-Ubeda, J. Environmental protection and financial performance: An empirical analysis in Wales. Int. J. Oper. Prod. Manag. 2014, 33, 981–1018. [Google Scholar] [CrossRef]

- Muhammad, N.; Scrimgeour, F.; Reddy, K.; Abidin, S. The Relationship between Environmental Performance and Financial Performance in Periods of Growth and Contraction: Evidence from Australian Publicly Listed Companies. J. Clean. Prod. 2015, 102, 324–332. [Google Scholar] [CrossRef]

- Dam, L.; Petkova, B. The impact of environmental supply chain sustainability. Int. J. Oper. Prod. Manag. 2014, 34, 586–609. [Google Scholar] [CrossRef]

- De Giovanni, P. Do internal and external environmental management contribute to the triple bottom line? Int. J. Oper. Prod. Manag. 2012, 32, 265–290. [Google Scholar] [CrossRef]

- Montabon, F.; Sroufe, R.; Narashimhan, R. An examination of corporate reporting, environmental management practices and firm performance. J. Oper. Manag. 2007, 25, 998–1014. [Google Scholar] [CrossRef]

- Rao, P.; Holt, D. Do green supply chains lead to competitiveness and economic performance? Int. J. Oper. Prod. Manag. 2005, 25, 898–916. [Google Scholar] [CrossRef]

- Darnall, N.; Edwards, D. Predicting the cost of environmental management systems adoption: The role of capabilities, resources and ownership structure. Strateg. Manag. J. 2006, 27, 301–320. [Google Scholar] [CrossRef]

- Chou, J.S. Generalized linear model-based expert system for estimating the cost of transportation projects. Expert Syst. Appl. 2009, 36, 4253–4267. [Google Scholar] [CrossRef]

- Czarnigowska, A.; Sobotka, A. Time—Cost relationship for predicting construction duration. Arch. Civ. Mech. Eng. 2013, 13, 518–526. [Google Scholar] [CrossRef]

- Hola, B.; Schabowicz, K. Estimation of earth works execution time and cost by means of artificial neural networks. Autom. Constr. 2010, 19, 570–579. [Google Scholar] [CrossRef]

- Kim, D.Y.; Han, S.H.; Kim, H.; Park, H. Structuring the prediction model of project performance for international construction projects: A comparative analysis. Expert Syst. Appl. 2009, 36, 1961–1971. [Google Scholar] [CrossRef]

- Lai, Y.T.; Wang, W.C.; Wang, H.H. AHP-and simulation-based budget determination procedure for public building construction projects. Autom. Constr. 2008, 17, 623–632. [Google Scholar] [CrossRef]

- Magnussen, O.M.; Olsson, N.O.E. Comparative analysis of cost estimates of major public investment projects. Int. J. Proj. Manag. 2006, 24, 281–288. [Google Scholar] [CrossRef]

- Rogalska, M.; Bożejko, W.; Hejducki, Z. Time/cost optimization using hybrid evolutionary algorithm in construction project scheduling. Autom. Constr. 2008, 18, 24–31. [Google Scholar] [CrossRef]

- Wang, Y.R.; Gibson, G.E., Jr. A study of preproject planning and project success using ANNs and regression models. Autom. Constr. 2010, 19, 341–346. [Google Scholar] [CrossRef]

- Curkovic, S.; Sroufe, R. Total Quality Environmental Management and Total Cost Assessment: An exploratory study. Int. J. Prod. Econ. 2007, 105, 560–579. [Google Scholar] [CrossRef]

- Jasinski, D.; Meredith, J.; Kirwan, K. A comprehensive review of full cost accounting methods and their applicability to the automotive industry. J. Clean. Prod. 2015, 108, 1123–1139. [Google Scholar] [CrossRef]

- Henri, J.F.; Boiral, O.; Roy, M.J. Strategic cost management and performance: The case of environmental costs. Br. Account. Rev. 2015, 48, 269–282. [Google Scholar] [CrossRef]

- Pizzini, M.J. The relation between cost-system design, managers’ evaluations of the relevance and usefulness of cost data, and financial performance: An empirical study of US hospitals. Account. Org. Soc. 2006, 31, 179–210. [Google Scholar] [CrossRef]

- Maiga, A.S.; Nilsson, A.; Jacobs, F.A. Assessing the interaction effect of cost control systems and information technology integration on manufacturing plant financial performance. Br. Account. Rev. 2014, 46, 77. [Google Scholar] [CrossRef]

- De Beer, P.; Friend, F. Environmental accounting: A management tool for enhancing corporate environmental and economic performance. Ecol. Econ. 2006, 58, 548–560. [Google Scholar] [CrossRef]

- Frost, G.R. The introduction of mandatory environmental reporting guideline: Australian evidence. ABACUS J. Account. Financ. Bus. Stud. 2007, 43, 190–216. [Google Scholar] [CrossRef]

- Edino, M.O.; Nsofor, G.N.; Bombom, L.S. Perceptions and attitudes towards gas flaring in the Niger Delta, Nigeria. Environmentalist 2010, 30, 67–75. [Google Scholar] [CrossRef]

- Beck, A.C.; Campbell, D.; Shrives, P.J. Content analysis in environmental reporting research: Enrichment and rehearsal of the method in a British–German context. Br. Account. Rev. 2010, 42, 207–222. [Google Scholar] [CrossRef]

- Russell, A.; Jenkins, L. Reflections on the attempt to set a comprehensive international accounting standard for the oil and gas industry. Petrol. Account. Financ. Manag. J. 2010, 29, 16–29. [Google Scholar]

- Duriau, V.K.; Reger, R.K.; Pfarrer, M.D. A content analysis of the content analysis literature in organization studies: Research themes, data source, and methodological refinements. Organ. Res. Methods 2007, 10, 5–34. [Google Scholar] [CrossRef]

- Olalekan, I.O.; Jumoke, O.O. Identifying barriers to environmental management accounting practices: A comparative study of Nigerial and Couth Africa practices. Bus. Manag. Rev. 2017, 9, 168–179. [Google Scholar]

- Bassy, E.B.; Oba, U.E.U.; Onyah, G.E. An analysis of the extent of implication of environmental cost management and its impact on output of oil and gas companies in Nigeria (2001–2010). Eur. J. Bus. Manag. 2013, 5, 110–119. [Google Scholar]

- Can, A.I.M.S.K.; Etale, L.M.; Frank, B.P. The impact of environmental cost on corporate performance: A study of oil companies in Niger Delta states of Nigeria. J. Bus. Manag. 2013, 2, 1–10. [Google Scholar] [CrossRef]

- Ezejiofor, R.A.; Racheal, J.A.; Chigbo, C.B.E.E. Effect of sustainability environmental cost accounting on financial performance of Nigerian corporate organizations. Int. J. Sci. Res. Manag. Stud. 2016, 4, 4536–4549. [Google Scholar] [CrossRef]

- Project Management Institute (PMI). A Guide to the Project Management Body of Knowledge (PMBOK Guide), 5th ed.; Project Management Institute: Newtown Square, PA, USA, 2013; ISBN 978-1-935589-67-9. [Google Scholar]

- Ministry of Petroleum of Iran. Specific Price List for Oil and Gas Facilities—Specific Price for Oil Industries Activities for 2015; Deputy of Engineering: Tehran, Iran, 2014.

- Central Bank of Iran. Total Price List and Consumable Services Index in the Iranian Urban Areas (Inflation Index): Annual Figures of Inflation Rate and Index during 1936–2014; Central Bank of Iran: Tehran, Iran, 2015. Available online: http://www.cbi.ir/datedlist/10807.aspxf (accessed on 16 August 2016).

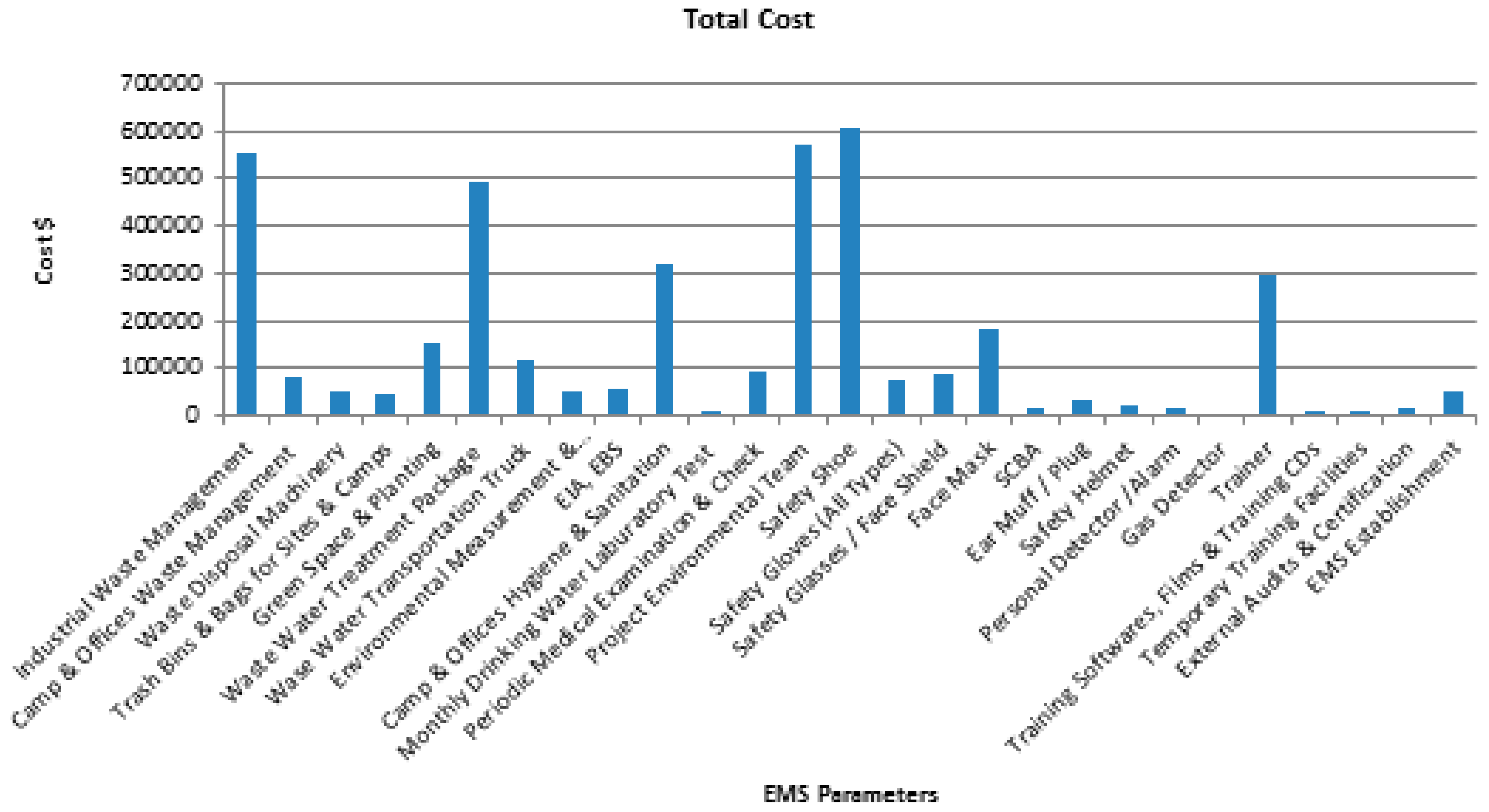

| No. | Environmental Parameter | Project Phases Cost (US $) | Total Costs (US $) | ||||

|---|---|---|---|---|---|---|---|

| Engineering and Management | Procurement | Construction | Precomm. | Comm., Start up and Hand Over | |||

| 1 | Waste Management | ||||||

| 1.1 | Industrial Waste Management | 299,534.4115 | 122,526.4292 | 133,413.8092 | 555,474.65 | ||

| 1.2 | Camp and Offices Waste Management | 45,375.00314 | 18,905.42986 | 18,418.64368 | 82,699.07668 | ||

| 1.3 | Waste Disposal Machinery | 53,430.22013 | 53,430.22013 | ||||

| 1.4 | Trash Bins and Bags for Sites and Camps | 30,504.94724 | 10,907.25144 | 5166.429552 | 465,787.62823 | ||

| 2 | Green Space and Planting | 134,830.9636 | 10,469.82705 | 10,200.24487 | 15,501.0355 | ||

| 3 | Waste Water Treatment Package | 491,558.0252 | 491,558.0252 | ||||

| 4 | Waste Water Transportation Truck | 117,546.4843 | 117,546.4843 | ||||

| 5 | Environmental Measurement and Monitoring | 31,051.5591 | 9576.709443 | 8300.821781 | 48,929.09032 | ||

| 6 | Environmental Impact Assessment (EIA), Environmental Base Study (EBS) | 55,297.50055 | 55,297.50055 | ||||

| 7 | Camp and Offices Hygiene and Sanitation | 173,937.512 | 72,470.81445 | 70,604.80076 | 317,013.1273 | ||

| 8 | Monthly Drinking Water Laboratory Test | 3630.000251 | 1512.434389 | 1473.491494 | 6615.926134 | ||

| 9 | Periodic Medical Examination and Check | 59,813.62204 | 21,386.76752 | 10,130.25402 | 91,330.64359 | ||

| 10 | Project Environmental Team | 320,171.3714 | 128,263.2446 | 119,756.5535 | 568,191.1695 | ||

| 11 | Personal Protective Equipment (PPE): | ||||||

| 11.1 | Safety Shoe | 398,757.4803 | 142,578.4502 | 67,535.0268 | 608,870.9573 | ||

| 11.2 | Safety Gloves (All Types) | 48,332.0230 | 17,477.5973 | 8648.4741 | 74,458.0944 | ||

| 11.3 | Safety Glasses/Face Shield | 60,856.66731 | 18,535.19852 | 8779.553486 | 88,171.41932 | ||

| 11.4 | Face Mask | 120,265.2561 | 43,001.6606 | 20,368.5641 | 183,635.4807 | ||

| 11.5 | SCBA | 5770.4638 | 8507.4434 | 14,277.9072 | |||

| 11.6 | Ear Muff/Plug | 11,324.7124 | 14,314.8764 | 6789.5167 | 32,420.1055 | ||

| 11.7 | Safety Helmet | 18,176.1340 | 4052.1016 | 22,228.2356 | |||

| 11.8 | Personal Detector/Alarm | 16,883.7567 | 16,883.7567 | ||||

| 12 | Gas Detector | 1068.604403 | 4726.357464 | 5794.961867 | |||

| 13 | Environmental Trainings | ||||||

| 13.1 | Trainer | 167,994.8356 | 66,078.37579 | 61,710.30132 | 295,783.5127 | ||

| 13.2 | Training Software, Films and Training CDs | 10,686.04403 | 10,686.04403 | ||||

| 13.3 | Temporary Training Facilities | 7693.951699 | 7693.951699 | ||||

| 14 | External Audits and Certification | 4150.41089 | 4150.41089 | 4150.41089 | 12,451.23267 | ||

| 15 | EMS Establishment | 53,430.22013 | 53,420.22013 | ||||

| Total Cost of Work packages | 108,727.7207 | 662,534.7296 | 1,953,925.974 | 715,389.2785 | 576,373.7546 | 4,016,951.457 | |

| Project Phases | Contract Value | Environmental Management Value | ||

|---|---|---|---|---|

| Amount (US $) | WF% | Amount (US $) | WF% | |

| Management & Engineering | 20,996,820 | 4.5814% | 108,728 | 0.023724046 |

| Procurement, Supply & Transportation | 280,329,372 | 61.1668% | 662,535 | 0.144562677 |

| Construction, Installation, Commissioning, Start & Hand over | 156,976,747 | 34.2517% | 3,245,689 | 0.70819729 |

| Total | 458,302,940 | 100.0000% | 4,016,952 | 0.876484014 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Abbaspour, M.; Toutounchian, S.; Dana, T.; Abedi, Z.; Toutounchian, S. Environmental Parametric Cost Model in Oil and Gas EPC Contracts. Sustainability 2018, 10, 195. https://doi.org/10.3390/su10010195

Abbaspour M, Toutounchian S, Dana T, Abedi Z, Toutounchian S. Environmental Parametric Cost Model in Oil and Gas EPC Contracts. Sustainability. 2018; 10(1):195. https://doi.org/10.3390/su10010195

Chicago/Turabian StyleAbbaspour, Madjid, Sanaz Toutounchian, Tooraj Dana, Zahra Abedi, and Solmaz Toutounchian. 2018. "Environmental Parametric Cost Model in Oil and Gas EPC Contracts" Sustainability 10, no. 1: 195. https://doi.org/10.3390/su10010195

APA StyleAbbaspour, M., Toutounchian, S., Dana, T., Abedi, Z., & Toutounchian, S. (2018). Environmental Parametric Cost Model in Oil and Gas EPC Contracts. Sustainability, 10(1), 195. https://doi.org/10.3390/su10010195