Entry Mode, Market Selection, and Innovation Performance

Abstract

:1. Introduction

2. Literature Review and Hypothesis Development

2.1. Group Response and Entry Mode Choice

2.2. Host-Country Response and Entry Mode Choice

2.3. Entry Mode Choice and Firm’s Innovation Performance

2.4. Market Selection and Firms’ Innovation Performance

3. Methodology

3.1. Sample

3.2. Dependent Variables

3.3. Independent Variables

3.4. Moderating Variable

3.5. Control Variables

3.6. Model Specification

4. Data Analysis

5. Results

5.1. Descriptive Statistics and Correlation Analysis

5.2. Analysis of Firms’ Entry Mode Choice

5.3. Entry Mode Choice and Innovation Performance

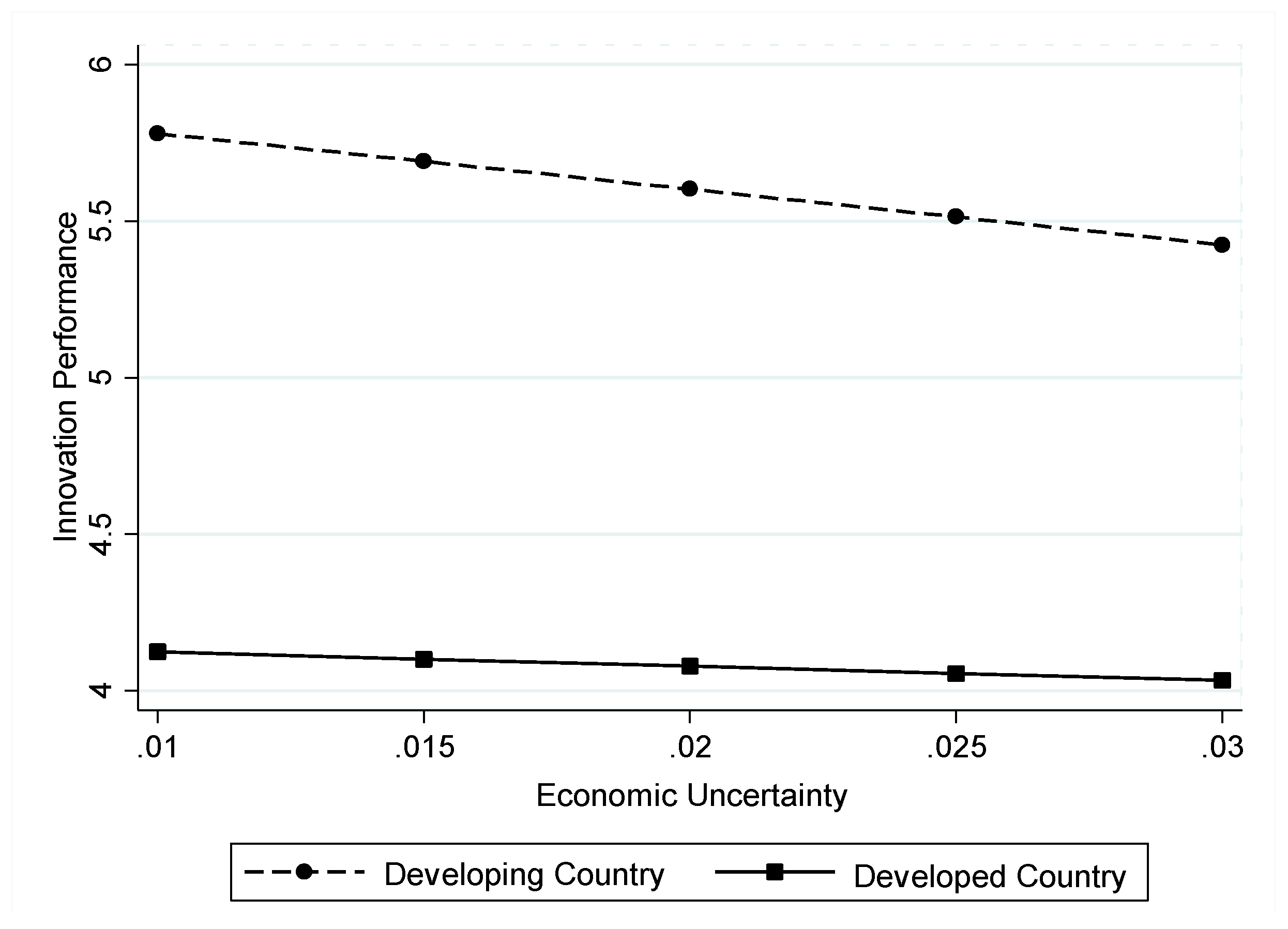

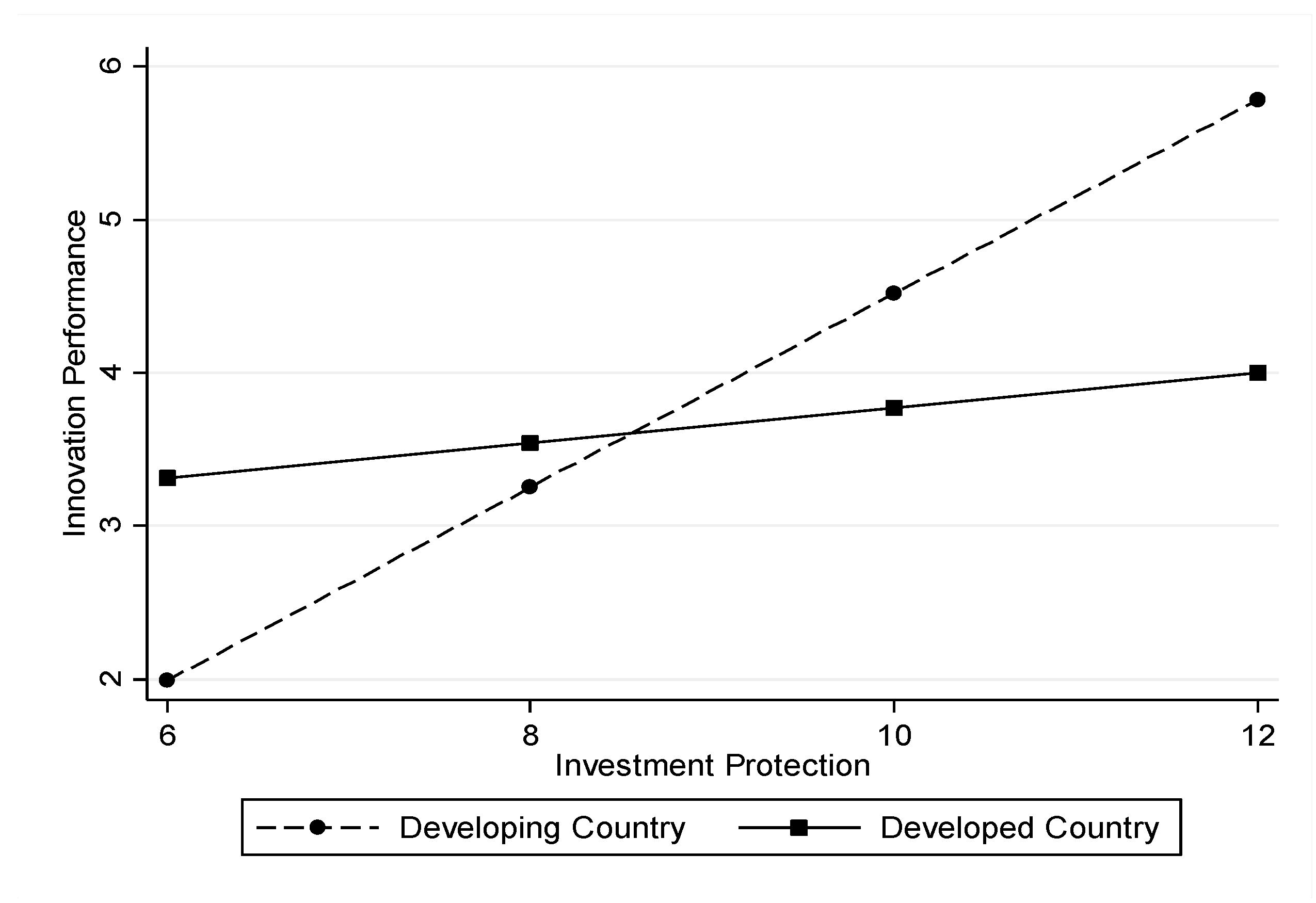

5.4. Market Slection and Inovation Performance: The Moderating Role of the Host Country’s Economic Level

6. Discussion

7. Conclusions and Implications

- (1)

- State-owned firms tend to choose JV modes that have high market entry efficiency, while private firms tend to choose WOS entry modes with intra-group consistency. Asset specificity enhances internal consistency, which has a positive influence on the WOS entry mode. When they accumulate early international experience, firms tend to choose the JV mode with more openness. Economic uncertainty and low investment protection of the host country have a significant positive influence on the choice of the JV mode. The entry mode that integrates group response and host-country response has better results in the prediction of entry modes of Chinese firms. These conclusions are in line with the Western research results based on the IB perspective.

- (2)

- The results of this study on the relationship between the entry mode choice of Chinese firms and performance differ from the results in Western theoretical research. Currently, the entry mode response to the host country unilaterally has a significantly negative influence on EM-MNE performance. That is, when the international environment is complicated, the pressure of host-country legitimacy exerts increasing influence on entry mode choices. As a result, EM-MNEs are unilaterally subject to external environment pressure and choose the entry mode responding to host-country consistency. However, the adjustment of EM-MNEs’ structure and organizational capability generally lags behind the need for international innovation, and the ability to successfully engage in cross-cultural management and innovation network integration cannot be improved in the short term. Correspondingly, the high-level internationalization capability of balancing market development and innovation exploration is also lacking, which negatively affects innovation performance.

- (3)

- The results of this study regarding the effect of a group’s internal factors and the host country’s institutional factors on innovation performance is consistent with results found by Western scholars. R&D input, firm size, the breadth of international experience, economic stability of the host country, and investment protection are positively related to innovation performance; self-selection correction can also enhance the predictive ability of the regression models. However, there are areas of this research that differ from Western research. For example, state ownership, early international experience based on foreign market expansion, and the depth of international experience based on repeated investment in the same region have a significant negative influence on innovation performance.

- (4)

- We also examined and confirmed the moderating effect of different socioeconomic conditions in invested regions on the relationships among economic fluctuation, investment protection, and parent innovation performance. The results enrich studies on the relationship between internationalization and the performance of EM-MNEs, and provide some guidance for EM-MNEs’ practices.

Author Contributions

Funding

Conflicts of Interest

References

- Deng, P. Chinese outward direct investment research: Theoretical integration and recommendations. Manag. Organ. Rev. 2013, 9, 513–539. [Google Scholar] [CrossRef]

- Brouthers, K.D. Institutional, cultural and transaction cost influences on entry mode choice and performance. J. Int. Bus. Stud. 2013, 44, 14–22. [Google Scholar] [CrossRef]

- Shaver, J.M. Do we really need more entry mode studies? J. Int. Bus. Stud. 2013, 44, 23–27. [Google Scholar] [CrossRef]

- Brouthers, K.D.; Brouthers, L.E.; Werner, S. Transaction cost-enhanced entry mode choices and firm performance. Strat. Manag. J. 2003, 24, 1239–1248. [Google Scholar] [CrossRef]

- Madhok, A. Cost, value and foreign market entry mode: The transaction and the firm. Strat. Manag. J. 1997, 18, 39–61. [Google Scholar] [CrossRef]

- Hennart, J.F.; Slangen, A.H. Yes, we really do need more entry mode studies! A commentary on shaver. J. Int. Bus. Stud. 2015, 46, 114–122. [Google Scholar] [CrossRef]

- Gaston-Breton, C.; Martín, O.M. International market selection and segmentation: A two-stage model. Int. Mark. Rev. 2013, 28, 267–290. [Google Scholar] [CrossRef]

- Sakarya, S.; Eckman, M.; Hyllegard, K.H. Market Selection for International Expansion: Assessing Opportunities in Emerging Markets. Int. Mark. Rev. 2007, 24, 208–238. [Google Scholar] [CrossRef]

- Casillas, J.C.; Moreno-Menéndez, A.M. Speed of the Internationalization Process: The Role of Diversity and Depth in Experiential Learning. J. Int. Bus. Stud. 2014, 45, 85–101. [Google Scholar] [CrossRef]

- Anderson, E.; Gatignon, H. Modes of foreign entry: A transaction cost analysis and propositions. J. Int. Bus. Stud. 1986, 17, 1–26. [Google Scholar] [CrossRef]

- Kogut, B.; Zander, U. Knowledge of the firm and the evolutionary theory of the multinational corporation. J. Int. Bus. Stud. 1993, 24, 625–645. [Google Scholar] [CrossRef]

- Allen, L.; Pantzalis, C. Valuation of the Operating Flexibility of Multinational Corporations. J. Int. Bus. Stud. 1996, 27, 633–653. [Google Scholar] [CrossRef]

- Kogut, B.; Kulatilaka, N. Operational Flexibility, Global Manufacturing and the Option Value of a Multinational Networks. Manag. Sci. 1994, 40, 123–139. [Google Scholar] [CrossRef]

- Chetty, S.; Eriksson, K. Mutual commitment and experiential knowledge in mature international business relationship. Upps. Univ. Dep. Bus. Stud. 2002, 11, 305–324. [Google Scholar] [CrossRef]

- Eriksson, K.; Johanson, J.; Majkgård, A.; Sharma, D. Experiential knowledge and costs in the internationalization process. J. Int. Bus. Stud. 1997, 28, 337–360. [Google Scholar] [CrossRef]

- Johanson, J.; Vahlne, J.E. The internationalization process of the firm—A model of knowledge development and increasing foreign market commitments. J. Int. Bus. Stud. 1977, 8, 23–32. [Google Scholar] [CrossRef]

- Barkema, H.G.; Vermeulen, F. What differences in the cultural backgrounds of partners are detrimental for international joint ventures? J. Int. Bus. Stud. 1997, 28, 845–864. [Google Scholar] [CrossRef]

- Mani, S.; Antia, K.D.; Rindfleisch, A. Entry mode and equity level: A multilevel examination of foreign direct investment ownership structure. Strat. Manag. J. 2007, 28, 857–866. [Google Scholar] [CrossRef]

- Zhou, K.Z.; Chi, K.Y.; Tse, D.K. The effects of strategic orientations on technology- and market-based breakthrough innovations. J. Mark. 2005, 69, 42–60. [Google Scholar] [CrossRef]

- Tallman, S.; Fladmoe-Lindquist, K. Internationalization, Globalization, and Capability-Based Strategy. Calif. Manag. Rev. 2002, 45, 116. [Google Scholar] [CrossRef]

- Chung, C.C.; Xiao, S.S.; Lee, J.Y.; Kang, J. The Interplay of Top-down Institutional Pressures and Bottom-up Responses of Transition Economy Firms on FDI Entry Mode Choices. Manag. Int. Rev. 2016, 56, 699–732. [Google Scholar] [CrossRef]

- Deng, P. The Internationalization of Chinese Firms: A Critical Review and Future Research. Int. J. Manag. Rev. 2012, 14, 408–427. [Google Scholar] [CrossRef]

- Acemoglu, D.; Johnson, S.; Robinson, J.; Thaicharoen, Y. Institutional causes, macroeconomic symptoms: Volatility, crises and growth. J. Monet. Econ. 2003, 50, 49–123. [Google Scholar] [CrossRef]

- Florida, R. The globalization of R&D: Results of a survey of foreign-affiliated R&D laboratories in the USA. Res. Policy 1997, 26, 85–103. [Google Scholar]

- Ahsan, M.; Musteen, M. Multinational enterprises’ entry mode strategies and uncertainty: A review and extension. Int. J. Manag. Rev. 2011, 13, 376–392. [Google Scholar] [CrossRef]

- Meyer, K.E.; Nguyen, H.V. Foreign investment strategies and sub-national institutions in emerging markets: Evidence from Vietnam. J. Manag. Stud. 2005, 42, 63–93. [Google Scholar] [CrossRef]

- Lu, J.W.; Li, W.; Wu, A.; Huang, X. Political hazards and entry modes of Chinese investments in Africa. Asia Pac. J. Manag. 2018, 35, 39–61. [Google Scholar] [CrossRef]

- Kostova, T.; Roth, K. Adoption of an organizational practice by subsidiaries of multinational corporations: Institutional and relational effects. Acad. Manag. J. 2002, 45, 215–233. [Google Scholar]

- Kostova, T. Success of the Transnational Transfer of Organizational Practices within Multinational Firms. Unpublished Ph.D. Thesis, University of Minnesota, Minneapolis, MN, USA, 1996. [Google Scholar]

- Estrin, S.; Baghdasaryan, D.; Meyer, K.E. The impact of institutional and human resource distance on international entry strategies. J. Manag. Stud. 2009, 46, 1171–1196. [Google Scholar] [CrossRef]

- Brouthers, K.D.; Brouthers, L.E.; Werner, S. Real options, international entry mode choice and performance. Soc. Sci. Electron. Publ. 2008, 45, 936–960. [Google Scholar] [CrossRef]

- Masten, S.E. Transaction costs, mistakes, and performance: Assessing the importance of governance. Manag. Decis. Econ. 1993, 14, 119–129. [Google Scholar] [CrossRef]

- Shrader, R.C. Collaboration and performance in foreign markets: The case of young high-technology manufacturing firms. Acad. Manag. J. 2001, 44, 45–60. [Google Scholar]

- Chiles, T.H.; Mcmackin, J.F. Integrating variable risk preferences, trust, and transaction cost economics. Acad. Manag. Rev. 1996, 21, 73–99. [Google Scholar] [CrossRef]

- Ghoshal, S.; Moran, P. Bad for practice: A critique of the transaction cost theory. Acad. Manag. Rev. 1996, 21, 13–47. [Google Scholar] [CrossRef]

- Dyer, J.H. Effective interim collaboration: How firms minimize transaction costs and maximize transaction value. Strat. Manag. J. 1997, 18, 535–556. [Google Scholar] [CrossRef]

- Zajac, E.J.; Olsen, C.P. From transaction cost to transactional value analysis: Implications for the study of interorganizational strategies. J. Manag. Stud. 1993, 30, 131–145. [Google Scholar] [CrossRef]

- Luo, Y. Capability exploitation and building in a foreign market: Implications for multinational enterprises. Organ. Sci. 2002, 13, 48–63. [Google Scholar] [CrossRef]

- Hillman, A.J.; Wan, W.P. The determinants of MNE subsidiaries’ political strategies: Evidence of institutional duality. J. Int. Bus. Stud. 2005, 36, 322–340. [Google Scholar] [CrossRef]

- Lu, J.W.; Xu, D. Growth and survival of international joint ventures: An external-internal legitimacy perspective. J. Manag. 2006, 32, 426–448. [Google Scholar] [CrossRef]

- Nell, P.C.; Puck, J.; Heidenreich, S. Strictly limited choice or agency? Institutional duality, legitimacy, and subsidiaries’ political strategies. J. World Bus. 2015, 50, 302–311. [Google Scholar] [CrossRef] [Green Version]

- Greenwood, R.; Raynard, M.; Kodeih, F.; Micelotta, E.R.; Lounsbury, M. Institutional complexity and organizational responses. Acad. Manag. Ann. 2011, 5, 317–371. [Google Scholar] [CrossRef]

- Kostova, T.; Roth, K.; Dacin, M.T. Institutional theory in the study of multinational corporations: A critique and new directions. Acad. Manag. Rev. 2008, 33, 994–1006. [Google Scholar] [CrossRef]

- Pache, A.C.; Santos, F. Inside the hybrid organization: Selective coupling as a response to competing institutional logics. Acad. Manag. J. 2013, 56, 972–1001. [Google Scholar] [CrossRef]

- Xu, D.; Meyer, K.E. Linking theory and context: ‘strategy research in emerging economies’ after Wright et al. (2005). J. Manag. Stud. 2013, 50, 1322–1346. [Google Scholar] [CrossRef]

- Hedge, D.; Hicks, D. The maturation of global corporate R&D: Evidence from the activity of U.S. foreign subsidiaries. Res. Policy 2008, 37, 390–406. [Google Scholar]

- Lu, J.W.; Beamish, P.W. International diversification and firm performance: The s-curve hypothesis. Acad. Manag. J. 2004, 47, 598–609. [Google Scholar]

- Kafouros, M.; Wang, C.; Piperopoulos, P.; Zhang, M. Academic collaborations and firm innovation performance in china: The role of region-specific institutions. Res. Policy 2015, 44, 803–817. [Google Scholar] [CrossRef]

- Mingo, S.; Junkunc, M.; Morales, F. The interplay between home and host country institutions in an emerging market context: Private equity in Latin America. J. World Bus. 2018, 53, 653–667. [Google Scholar] [CrossRef]

- Luo, Y.; Xue, Q.; Han, B. How emerging market governments promote outward FDI: Experience from China. J. World Bus. 2010, 45, 68–79. [Google Scholar] [CrossRef]

- Dunning, J.H. Location and the multinational enterprise: A neglected factor? J. Int. Bus. Stud. 1998, 29, 45–66. [Google Scholar] [CrossRef]

- Wu, J.; Wang, C.; Hong, J.; Piperopoulos, P.; Zhuo, S. Internationalization and innovation performance of emerging market enterprises: The role of host-country institutional development. J. World Bus. 2016, 51, 251–263. [Google Scholar] [CrossRef] [Green Version]

- Kotabe, M.; Dunlap-Hinkler, D.; Parente, R.; Mishra, H.A. Determinants of Cross-National Knowledge Transfer and Its Effect on Firm Innovation. J. Int. Bus. Stud. 2007, 38, 259–282. [Google Scholar] [CrossRef]

- Hitt, M.A.; Hoskisson, R.E.; Kim, H. International diversification: Effects on innovation and firm performance in product-diversified firms. Acad. Manag. J. 1997, 40, 767–798. [Google Scholar]

- Jacobides, M.G.; Knudsen, T.; Augier, M. Benefiting from innovation: Value creation, value appropriation and the role of industry architectures. Res. Policy 2006, 35, 1200–1221. [Google Scholar] [CrossRef]

- Kafouros, M.I.; Buckley, P.J.; Clegg, J. The effects of global knowledge reservoirs on the productivity of multinational enterprises: The role of international depth and breadth. Res. Policy 2012, 41, 848–861. [Google Scholar] [CrossRef]

- Folta, T.B.; Miller, K.D. Real options in equity partnerships. Strat. Manag. J. 2010, 23, 77–88. [Google Scholar] [CrossRef]

- Tung, R.L. The human resource challenge to outward foreign direct investment aspirations from emerging economies: The case of China. Int. J. Hum. Resour. Manag. 2007, 18, 868–889. [Google Scholar] [CrossRef]

- Birkinshaw, J.; Hood, N. Multinational Corporate Evolution and Subsidiary Development; Macmillan: London, UK, 1998. [Google Scholar]

- Wan, H.P. Country Resource Environments, Firm Capabilities, and Corporate Diversification Strategies. J. Manag. Stud. 2005, 42, 161–182. [Google Scholar] [CrossRef]

- Meyer, K.E.; Estrin, S.; Bhaumik, S.K.; Peng, M.W. Institutions, resources, and entry strategies in emerging economies. Lse Res. Online Doc. Econ. 2009, 30, 61–80. [Google Scholar] [CrossRef] [Green Version]

- Shaver, J.M. Accounting for endogeneity when assessing strategy performance: Does entry mode choice affect FDI survival? Manag. Sci. 1998, 44, 571–585. [Google Scholar] [CrossRef]

- Fang, V.W.; Tian, X.; Tice, S. Does stock liquidity enhance or impede firm innovation? J. Financ. 2014, 69, 2085–2125. [Google Scholar] [CrossRef]

- Cornaggia, J.; Mao, Y.; Tian, X.; Wolfe, B. Does banking competition affect innovation? J. Financ. Econ. 2015, 115, 189–209. [Google Scholar] [CrossRef]

- Williamson, O.E. The Economic Institution of Capitalism; Free Press: New York, NY, USA, 1998. [Google Scholar]

- World Bank. The Worldwide Governance Indicators (WGI). Available online: http://info.worldbank.org/governance/wgi/index.aspx#home (accessed on 27 July 2018).

- The PRS Group. The International Country Risk Guide (ICRG). Available online: http://epub.prsgroup.com/products/icrg/international-country-risk-guide-icrg# (accessed on 10 July 2018).

- Tihanyi, L.; Griffith, D.A.; Russell, C.J. The Effect of cultural distance on entry mode choice, international diversification, and MNE performance: A meta-analysis. J. Int. Bus. Stud. 2005, 36, 270–283. [Google Scholar] [CrossRef]

- Kotabe, M.; Kothari, T. Emerging market multinational companies’ evolutionary paths to building a competitive advantage from emerging markets to developed countries. J. World Bus. 2016, 51, 729–743. [Google Scholar] [CrossRef]

- Prange, C.; Verdier, S. Dynamic Capabilities, Internationalization Processes and Performance. J. World Bus. 2011, 46, 126–133. [Google Scholar] [CrossRef]

- Child, J.; Rodrigues, S.B. The Internationalization of Chinese Firms: A Case for Theoretical Extension? Manag. Organ. Rev. 2005, 1, 381–410. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variable | Definition |

|---|---|

| Entry mode | 1 for JV mode and 0 for WOS mode |

| Innovation performance | Natural logarithm of the number of annual patent applications for new inventions by the parent company in the three years after OFDI |

| R&D input | Ratio of R&D expenditures to the firm’s total operation income in three years after OFDI |

| Asset specificity | Ratio of fixed assets to total assets of a sample firm the year before OFDI |

| Ownership | 1 for state-owned firm and 0 for private firm |

| Innovation orientation | Ratio of the number of R&D personnel to the number of all staff in the firm the year before OFDI |

| Early international experience | Ratio of overseas operational revenue to total income in the year prior to OFDI |

| Breadth | Number of foreign countries in which a firm has subsidiaries the year before OFDI |

| Depth | The number of times that the firm set up a subsidiary in the same country the year before OFDI |

| Economic uncertainty | Rolling variance of GDP growth rate over a seven-year period the year before OFDI |

| Rule of law | Indicator of “rule of law” in the WGI of the World Bank |

| Investment protection | Host country’s investment profile the year before OFDI; data were obtained from the ICRG published by the PRS Group |

| Culture distance | Square root of the sum of the squared differences of the score for each cultural dimension; this value was arithmetically averaged |

| Self-selection correction | Inverse Mills ratio calculated from the estimated parameters of the entry mode choice equation, see Section 3.1 of this paper |

| Predicted Fitn (n = 1, 2, or 3) | 1 if the firm used the entry mode predicted by one of three theoretical models, otherwise, the value is 0. |

| Variables | Mean | SD | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Entry mode | 0.26 | 0.44 | 1 | ||||||||||||||

| Innovation Performance | 3.91 | 1.87 | −0.121 * | 1 | |||||||||||||

| R&D input | 0.04 | 0.03 | −0.006 | 0.143 ** | 1 | ||||||||||||

| Ownership | 0.39 | 0.49 | 0.187 *** | 0.129 ** | −0.056 | 1 | |||||||||||

| Asset specificity | 0.23 | 0.13 | −0.093 | −0.216 *** | −0.298 *** | −0.067 | 1 | ||||||||||

| Innovation orientation | 0.19 | 0.12 | −0.037 | 0.012 | 0.411 *** | 0.144 ** | −0.248 *** | 1 | |||||||||

| Early international experience | 0.27 | 0.29 | 0.048 | −0.155 ** | −0.073 | −0.353 *** | 0.063 | −0.154 ** | 1 | ||||||||

| Breadth | 1.48 | 2.35 | 0.037 | 0.331 *** | 0.054 | 0.106 * | −0.147 ** | 0.015 | −0.037 | 1 | |||||||

| Depth | 0.94 | 1.58 | 0.051 | 0.200 *** | 0.178 *** | 0.04 | −0.255 *** | 0.036 | −0.062 | 0.586 *** | 1 | ||||||

| Economic uncertainty | 0.07 | 0.05 | 0.198 *** | 0.022 | 0.058 | 0.026 | −0.081 | 0.019 | −0.032 | 0.222 *** | 0.152 ** | 1 | |||||

| Rule of law | 82.13 | 18.87 | −0.206 *** | −0.088 | 0.065 | −0.046 | −0.043 | 0.086 | −0.024 | −0.161 ** | 0.033 | −0.420 *** | 1 | ||||

| Investment protection | 10.92 | 1.53 | −0.191 *** | −0.012 | −0.045 | 0.006 | −0.038 | 0.057 | −0.026 | −0.158 ** | −0.025 | −0.468 *** | 0.774 *** | 1 | |||

| Culture distance | 3.2 | 1.89 | 0.021 | −0.029 | 0.128 ** | −0.047 | 0.014 | 0.068 | 0.063 | 0.138 ** | 0.138 ** | 0.251 *** | 0.07 | −0.025 | 1 | ||

| Firm size | 21.89 | 1.14 | 0.063 | 0.438 *** | −0.183 *** | 0.410 *** | −0.111 * | −0.06 | −0.292 *** | 0.447 *** | 0.310 *** | 0.189 *** | −0.128 ** | −0.099 | 0.01 | 1 | |

| Self-selection correction | 1.34 | 0.38 | −0.341 *** | −0.088 | 0.043 | −0.568 *** | 0.333 *** | 0.078 | −0.147 ** | −0.06 | −0.129 ** | −0.512 *** | 0.536 *** | 0.444 *** | −0.062 | −0.261 *** | 1 |

| Fit2 | 0.74 | 0.44 | −0.893 *** | 0.028 | −0.005 | −0.151 ** | 0.097 | 0.068 | −0.062 | −0.105 | −0.052 | −0.235 *** | 0.245 *** | 0.166 *** | −0.045 | −0.061 | 0.337 *** |

| Variables | Model 1 | Model 2 | Model 3 |

|---|---|---|---|

| Group response variables | |||

| Ownership | 1.175 *** | 1.238 *** | |

| (0.344) | (0.359) | ||

| Asset specificity | −2.110 * | −2.233 * | |

| (1.244) | (1.296) | ||

| Early international experience | 1.152 ** | 1.242 ** | |

| (0.584) | (0.609) | ||

| Strategic flexibility | −0.056 | −0.264 | |

| (0.199) | (0.217) | ||

| Innovation orientation | −1.488 | −1.170 | |

| (1.309) | (1.333) | ||

| Host-country response variables | |||

| Economic uncertainty | 5.567 * | 6.045 * | |

| (3.174) | (3.278) | ||

| Rule of law | −0.016 ** | −0.019 ** | |

| (0.008) | (0.009) | ||

| Culture distance | −0.005 | 0.024 | |

| (0.087) | (0.092) | ||

| Constant | −1.085 * | −0.164 | 0.039 |

| (0.566) | (0.778) | (1.037) | |

| Number of observations | 242 | 242 | 242 |

| Chi2 | 15.91 | 12.80 | 29.73 |

| Pseudo R2 | 0.058 | 0.047 | 0.108 |

| Likelihood | −129.8 | −131.3 | −122.8 |

| LR test based on Model 1 | 13.82 *** | ||

| LR test based on Model 2 | 16.93 *** | ||

| Overall prediction accuracy | 65.87% | 64.39% | 72.86% |

| Variables | Model 1 | Model 2 | Model 3 | Model 4 |

|---|---|---|---|---|

| Fit1 | 0.381 | |||

| (0.727) | ||||

| Fit2 | −1.171 ** | |||

| (0.524) | ||||

| Fit3 | −0.371 | |||

| (0.353) | ||||

| JV | −0.662 *** | −0.308 | −1.704 *** | −0.924 *** |

| (0.244) | (0.719) | (0.525) | (0.349) | |

| Early international experience | −1.339 ** | −1.341 ** | −1.228 ** | −1.270 ** |

| (0.517) | (0.518) | (0.515) | (0.521) | |

| Breadth | 0.252 *** | 0.252 *** | 0.216 *** | 0.242 *** |

| (0.063) | (0.064) | (0.065) | (0.064) | |

| Depth | −0.197 ** | −0.196 ** | −0.165 * | −0.187 ** |

| (0.087) | (0.087) | (0.087) | (0.087) | |

| Economic uncertainty | −9.156 *** | −9.024 *** | −9.174 *** | −8.590 *** |

| (3.009) | (3.025) | (2.984) | (3.056) | |

| Investment protection | 0.183 ** | 0.179 ** | 0.148 * | 0.177 ** |

| (0.087) | (0.087) | (0.087) | (0.087) | |

| Culture distance | −0.050 | −0.051 | −0.051 | −0.050 |

| (0.056) | (0.056) | (0.056) | (0.056) | |

| R&D input | 15.439 *** | 15.473 *** | 15.210 *** | 15.220 *** |

| (3.603) | (3.610) | (3.574) | (3.609) | |

| Ownership | −1.429 *** | −1.429 *** | −1.284 *** | −1.372 *** |

| (0.411) | (0.412) | (0.413) | (0.415) | |

| Firm scale | 0.711 *** | 0.710 *** | 0.725 *** | 0.711 *** |

| (0.116) | (0.116) | (0.115) | (0.116) | |

| Self-selection correction | −2.359 *** | −2.343 *** | −2.116 *** | −2.229 *** |

| (0.620) | (0.621) | (0.624) | (0.632) | |

| Constant | −9.349 *** | −9.687 *** | −8.530 *** | −9.185 *** |

| (2.841) | (2.918) | (2.841) | (2.845) | |

| Number of observations | 242 | 242 | 242 | 242 |

| F | 10.55 | 9.665 | 10.26 | 9.770 |

| R2 | 0.335 | 0.336 | 0.350 | 0.339 |

| Adjusted R2 | 0.304 | 0.301 | 0.316 | 0.304 |

| Variables | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 |

|---|---|---|---|---|---|---|

| Economic uncertainty | −9.156 *** | −8.923 *** | −15.310 *** | −9.243 *** | −16.082 *** | |

| (3.204) | (3.303) | (4.076) | (3.271) | (3.754) | ||

| Investment protection | 0.183 ** | 0.214 ** | 0.586 *** | 0.589 *** | ||

| (0.089) | (0.095) | (0.197) | (0.187) | |||

| Developed country | −0.246 | −0.765 | 4.130 * | 2.090 | ||

| (0.494) | (0.686) | (2.212) | (2.238) | |||

| Economic uncertainty × developed country | 9.836 * | 11.779 ** | ||||

| (5.061) | (4.702) | |||||

| Investment protection × developed country | −0.482 ** | −0.408 * | ||||

| (0.226) | (0.214) | |||||

| Culture distance | −0.082 | −0.050 | −0.043 | −0.039 | −0.062 | −0.043 |

| (0.054) | (0.054) | (0.056) | (0.056) | (0.056) | (0.055) | |

| JV | −0.701 *** | −0.662 *** | −0.666 *** | −0.656 *** | −0.671 *** | −0.645 *** |

| (0.252) | (0.244) | (0.243) | (0.239) | (0.243) | (0.238) | |

| Early international experience | −0.344 | −1.339 *** | −1.243 ** | −1.189 ** | −1.208 ** | −1.251 ** |

| (0.434) | (0.456) | (0.535) | (0.541) | (0.528) | (0.520) | |

| Breadth | 0.155 *** | 0.252 *** | 0.242 *** | 0.224 *** | 0.235 *** | 0.234 *** |

| (0.060) | (0.064) | (0.074) | (0.074) | (0.073) | (0.072) | |

| Depth | −0.097 | −0.197 *** | −0.184 ** | −0.186 ** | −0.178 ** | −0.201 ** |

| (0.077) | (0.074) | (0.083) | (0.086) | (0.082) | (0.083) | |

| R&D input | 14.405 *** | 15.439 *** | 15.479 *** | 14.760 *** | 15.444 *** | 15.368 *** |

| (2.807) | (2.625) | (2.619) | (2.720) | (2.655) | (2.595) | |

| Ownership | −0.412 | −1.429 *** | −1.352 *** | −1.174 ** | −1.311 *** | −1.314 *** |

| (0.317) | (0.387) | (0.466) | (0.473) | (0.459) | (0.457) | |

| Firm scale | 0.702 *** | 0.711 *** | 0.713 *** | 0.726 *** | 0.707 *** | 0.724 *** |

| (0.125) | (0.121) | (0.122) | (0.119) | (0.122) | (0.119) | |

| Self-selection correction | −0.565 | −2.359 *** | −2.214 *** | −1.821 ** | −2.156 *** | −2.029 *** |

| (0.409) | (0.623) | (0.779) | (0.802) | (0.756) | (0.757) | |

| Constant | −10.686 *** | −9.349 *** | −9.827 *** | −7.950 *** | −12.823 *** | −12.568 *** |

| (2.845) | (2.814) | (3.156) | (2.934) | (3.248) | (3.034) | |

| Number of observations | 242 | 242 | 242 | 242 | 242 | 242 |

| F | 12.96 | 12.62 | 12.41 | 10.61 | 11.35 | 11.47 |

| R2 | 0.296 | 0.335 | 0.336 | 0.337 | 0.347 | 0.364 |

| Adjusted R2 | 0.268 | 0.304 | 0.302 | 0.302 | 0.310 | 0.325 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, C.; Huang, F.; Huang, C.; Zhang, H. Entry Mode, Market Selection, and Innovation Performance. Sustainability 2018, 10, 4222. https://doi.org/10.3390/su10114222

Wu C, Huang F, Huang C, Zhang H. Entry Mode, Market Selection, and Innovation Performance. Sustainability. 2018; 10(11):4222. https://doi.org/10.3390/su10114222

Chicago/Turabian StyleWu, Chong, Fang Huang, Caihong Huang, and Huiming Zhang. 2018. "Entry Mode, Market Selection, and Innovation Performance" Sustainability 10, no. 11: 4222. https://doi.org/10.3390/su10114222

APA StyleWu, C., Huang, F., Huang, C., & Zhang, H. (2018). Entry Mode, Market Selection, and Innovation Performance. Sustainability, 10(11), 4222. https://doi.org/10.3390/su10114222