Determining Environmental Costs: A Challenge in A Governmental E-Waste Recycling Scheme

Abstract

:1. Introduction

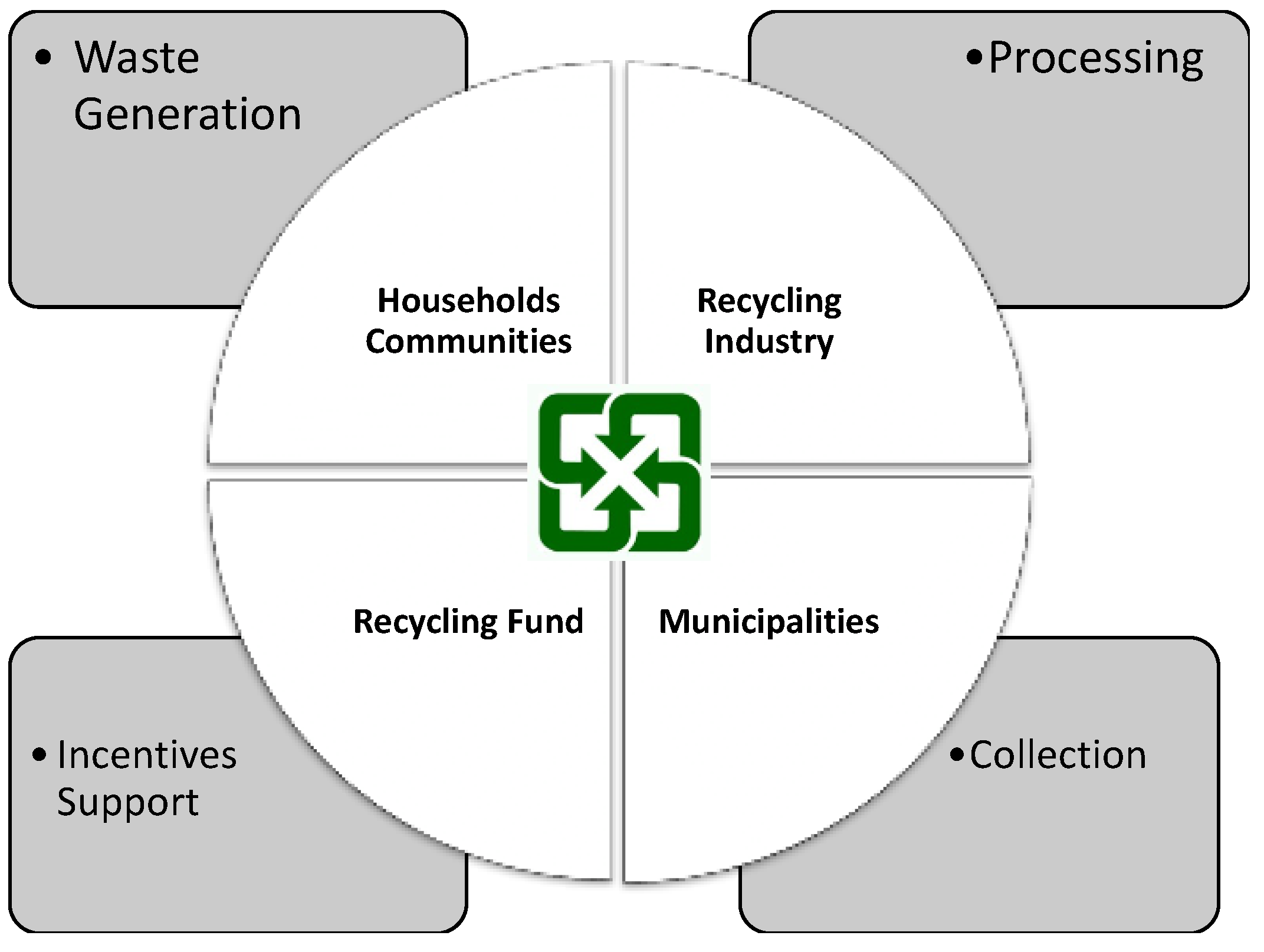

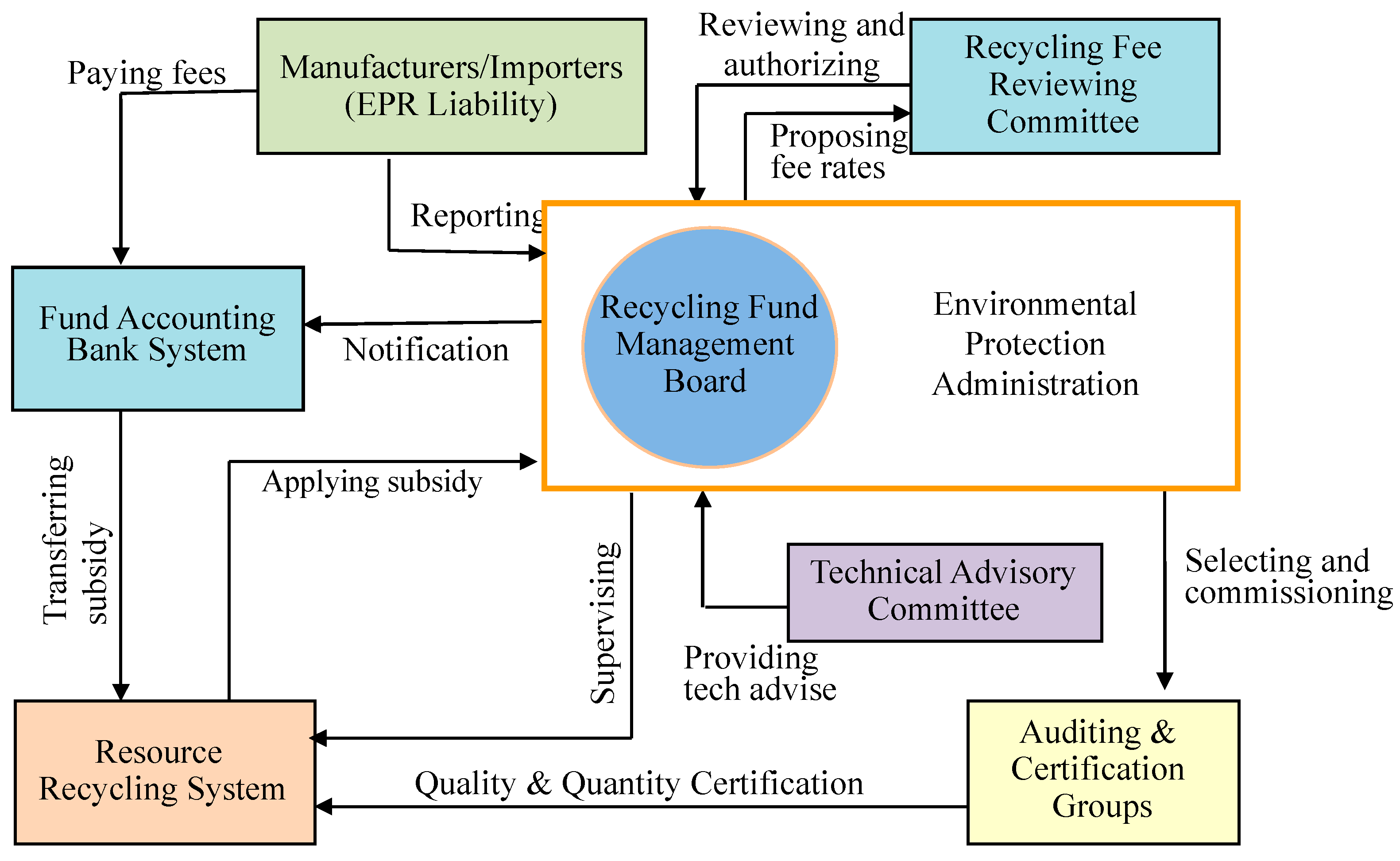

2. The Structure of EPR in Taiwan

3. Evolution of the Recycling Fee Equation

3.1. Recycling Fee Calculation Equation V.1 (1998)

- R: recycling fee ($/unit)

- C: collection and treatment cost per unit ($/unit)

- W: estimated obsolete amount (units)

- α: collection rate target (%)

- p: administration cost vs recycling operation cost ratio (%)

- S: forecasted yearly new sales amount (units)

3.2. Recycling Fee Calculation Equation V.2 (2001)

- R: recycling fee ($/unit)

- C: collection and treatment cost per unit ($/unit)

- α: collection rate target (%)

- E: averaged environmental cost of the unrecycled waste products ($/unit)

- F: fund balance amortization ($)

- β: ratio of obsolete vs new sales of product, or W/S (%)

3.3. Recycling Fee Calculation Equation V.3 (2005)

- R: recycling fee ($/unit)

- C: collection and treatment cost per unit ($/unit)

- α: collection rate target (%)

- E1: averaged environmental cost of unrecycled but properly disposed products, such as through sanitarily landfilled or incinerated means ($/unit)

- E2: averaged environmental cost of littering for unrecycled and improperly disposed products ($/unit)

- F: fund balance amortization ($)

- W: estimated obsolete amount (units)

- β: ratio of obsolete vs newly sold products, or, W/S (%)

- The ratio of the unrecyclable but properly disposed products (α1);

- The ratio of littering involving the unrecyclable and improperly disposed products (α2).

- R: recycling fee ($/unit)

- C: collection and treatment cost per unit ($/unit)

- α: collection rate target (%)

- α1: ratio of the waste products properly disposed of but not recycled (%)

- α2: ratio of the waste products littered and not properly disposed of (%)α + α1 + α2 = 1

- E1: averaged environmental cost of unrecycled but properly disposed products, such as through sanitarily landfilled or incinerated means ($/unit)

- E2: averaged environmental cost of littering for unrecycled and improperly disposed products ($/unit)

- W: estimated obsolete amount (units)

- F: fund balance amortization ($)

- L: administration cost of the recycling scheme ($)

- S: forecasted yearly new sales amount (units)

4. Green Recycling Fee Rates: A Discount Factor in Recycling Fees for Environmentally Designed Products

5. Consideration of Environmental Costs in the Fee Equations

6. Findings from the Variation of Recycling Equation and Environmental Cost Consideration

- Consumers do not highly value consumer subsidy or rewards, and instead care more about the convenience of handing over recyclables to collectors.

- Producers care not about how they should physically work on taking back and recycling, but about how much they should pay.

- The government is not able to further achieve better environmental targets simply by managing the recycling fee-charging system. However, the government needs to guide the market towards greener appliances with monetary instruments.

- Establishing a linkage between producers and recyclers to encourage eco-design, as well as a linkage between recyclers and collectors to form a complete alliance.

- Identifying potential profits through innovative and inter-industrial collaboration between manufacturers and recyclers.

- Sharing the subsidy fee with the producers who pay the recycling fees, and executing physical responsibility for recycling.

7. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- OECD. Extended Producer Responsibility: A Guidance Manual for Governments; Organisation for Economic Co-operation and Development: Paris, France, 2001. [Google Scholar]

- European Parliament and of the Council. Directive 2002/96/EC of the European Parliament and of the Council of 27 January 2003 on Waste Electrical and Electronic Equipment (WEEE). Off. J. Eur. Union 2003, No. 96. L 37/24–L 37/39. [Google Scholar]

- Li, J.; Lin, M.; Liu, L. Producer Responsibility Extension System and Electronic Waste Recycling. In 2011 Circular Economy and Energy Saving Carbon Reduction; CTCI Foundation: Taipei, Taiwan, 2011; pp. 71–86. [Google Scholar]

- Wen, L.; Lo, S.F.; Lin, C.H. Assistance to Fee Committee Member’s Meeting Operation and Review of Recycling-and-Treatment Fee Structure; EPA-96-HA14-03-A127; Chung-Hua Institution for Economic Research: Taipei, Taiwan, 2007. [Google Scholar]

- Fan, K.S.; Lin, C.H.; Chang, T.C. Management and performance of Taiwan’s waste recycling fund. J. Air Waste Manag. Assoc. 2005, 55, 574–582. [Google Scholar]

- Wen, L.; Lee, C.H.; Chang, S.L.; Lin, C.H. Due-Recycling Articles Recycle Rate of Clearance and Disposal Fees Evaluation, Effectiveness and Review Program; EPA-91-HA31-03-A173; Chung-Hua Institution for Economic Research: Taipei, Taiwan, 2003. [Google Scholar]

- Wu, C.-L.; Wang, C.-H.; Wu, J. The Innovaton of Recycling System for Waste Household Appliances and Waste Electronics IT Objects; EPA-98-HA14-03-A177; SGS Taiwan Corporation: Taipei, Taiwan, 2009. [Google Scholar]

- Cheng, C.-P.; Chang, T.-C. The development and prospects of the waste electrical and electronic equipment recycling system in Taiwan. J. Mater. Cycles Waste Manag. 2017, 20, 667–677. [Google Scholar]

- Wang, C.-H.; Lee, Y.-W. Waste Home Appliance and IT Equipment Industrial Investigation and Fee Rate Structure Assessment Project; EPA-103-HA14-03-A058; E-Titanium International Inc.: Taipei, Taiwan, 2014. [Google Scholar]

- Wen, L.; Liao, L.-Q. Project on Investigating the Flow and Improving the Recycling Technology of Waste Home Appliances and IT Equipment Recycling; EPA-106-HA14-03-A066; Chung-Hua Institution for Economic Research: Taipei, Taiwan, 2017. [Google Scholar]

- Xu, Y.; Li, J.; Liu, L. Current Status and Future Perspective of Recycling Copper by Hydrometallurgy from Waste Printed Circuit Boards. Procedia Environ. Sci. 2016, 31, 162–170. [Google Scholar] [Green Version]

- Chang, T.-C.; Ku, Y. A Strategy and Analysis of E-Waste in Taiwan; EPA-105-H103-02-A295; National Taipei Technology University: Taipei, Taiwan, 2016. [Google Scholar]

- Recycling Fund Management Board Website. Available online: https://recycle.epa.gov.tw/en/index.html (accessed on 20 June 2019).

- Jiang, K.Y. Project of Planning Resource Recycling System and Promoting Design for Environment; EPA-96-H103-02-131; Institute of Environment and Resources: Taipei, Taiwan, 2007. [Google Scholar]

- Lin, C.-H. A model using home appliance ownership data to evaluate recycling policy performance. Resour. Conserv. Recycl. 2008, 52, 1322–1328. [Google Scholar]

- Qiu, X. Project of Management and Elevate Efficacy of Waste Home Appliances and Waste IT Equipment Selling and Recycling System; EPA-103-HA14-03-A037; SGS: Taipei, Taiwan, 2014. [Google Scholar]

- Hecht, J.E. National Environmental Account: Bridging the Gap between Ecology and Economy; Resources for the Future: Washington, DC, USA, 2004. [Google Scholar]

- United Nations; European Union; Food and Agriculture Organization of the United Nations; International Monetary Fund; Organisation for Economic Co-operation and Development; The World Bank. System of Environmental-Economic Accounting 2012—Central Framework; United Nations: New York, NY, USA, 2014. [Google Scholar]

- Eshet, T.; Ayalon, O.; Shechter, M. Valuation of externalities of selected waste management alternatives: A comparative review and analysis. Resour. Conserv. Recycl. 2006, 46, 335–364. [Google Scholar]

- Directorate-General of Budget, Accounting and Statistics (DGBAS). Green National Income (Environmental-Economic Account) for 2017; Directorate-General of Budget, Accounting and Statistics (DGBAS): Taipei, Taiwan, 2019. [Google Scholar]

- Shih, H.-S. Policy analysis on recycling fund management for E-waste in Taiwan under uncertainty. J. Clean. Prod. 2017, 143, 345–355. [Google Scholar]

- Rebitzer, G.; Nakamura, S. Environmental Life Cycle Costing. In Environmental Life Cycle Costing; Chapter 3; Hunkeler, H., Lichtenvort, K., Rebitzer, G., Eds.; CPC Press: Webster, NY, USA, 2008; pp. 35–58. [Google Scholar]

- Steen, B.; Hoppe, H.; Hunkeler, D.; Lichtenvort, K.; Schmidt, W.-P.; Spindler, E. Integrating External Effects into Life Cycle Costing in Environmental Life Cycling. In Environmental Life Cycle Costing; Chapter 4; Hunkeler, H., Lichtenvort, K., Rebitzer, G., Eds.; CPC Press: Webster, NY, USA, 2008; pp. 59–76. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Recycling Fee (NT$/Unit *) | |||||||

|---|---|---|---|---|---|---|---|

| PC a | Monitor | Laptop | Printer | Keyboard | |||

| Notebook | Panel | Laser | Ink-Jet | Dot-Matrix | |||

| 111 | 127 | 39 | 25.3 | 159 | 144 | 155 | 14 |

| 78 b | 89 b | 27b | 18 b | 151 b | 137 b | 147 b | 10 b |

| Recycling Fee (NT$/Unit) | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Television | Refrigerator | Washing Machine | Air Conditioner | Electrical Fan | |||||

| ≤27” | >27” | ≤250 L | 250 L | ≤12” | >12” | ||||

| CRT | LCD | CRT | LCD | ||||||

| 247 | 127 | 371 | 233 | 392 | 588 | 307 | 241 | 19 | 34 |

| 222 b | 114 b | 334 b | 210 b | 333 b | 500 b | 261 b | 205 b | 16 b | 29 b |

| Factors | Principles of Estimation/Calculation |

|---|---|

| C | The costs from the collection, transportation and recycling processes needed for both labor and equipment, minus revenue generated from the sales of secondary materials. |

| W | Substituted by the actual yearly sales amount of the mandatory recycling product, in the supposed year when the product was introduced to the market. |

| α | The target set by the RFMB and the EPAT. |

| E1 xα1 | The cost of collecting mandatory recycling products which are incorrectly or illegally disposed of into the municipal waste collection. Since residents are currently required to cover municipal waste collection through a unit pricing scheme, this cost is set to be 0 for producers in calculations. |

| E2 xα2 | The cost of the environmental impact from the improper disposal of mandatory recycling products, currently substituted by a planned budget, which is the annual amount of funding given by the RFMB to local municipal cleaning teams. |

| L | Administration cost including the expense for the work done by the Auditing and Certification Groups, the support of online reporting and auditing systems, and other administrative costs associated with research, auditing, and certification. |

| F | Fund balance amortization equal to: (Cumulative trust fund surplus—Amount set aside from the previous year’s surplus for the future management of the fund)/life span of the mandatory recycling product. |

| S | Forecasted annual sales amount estimated by the averaged actual sales in the previous three years. |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cheng, C.-p.; Lin, C.-h.; Wen, L.-c.; Chang, T.-c. Determining Environmental Costs: A Challenge in A Governmental E-Waste Recycling Scheme. Sustainability 2019, 11, 5156. https://doi.org/10.3390/su11195156

Cheng C-p, Lin C-h, Wen L-c, Chang T-c. Determining Environmental Costs: A Challenge in A Governmental E-Waste Recycling Scheme. Sustainability. 2019; 11(19):5156. https://doi.org/10.3390/su11195156

Chicago/Turabian StyleCheng, Chii-pwu, Chun-hsu Lin, Lih-chyi Wen, and Tien-chin Chang. 2019. "Determining Environmental Costs: A Challenge in A Governmental E-Waste Recycling Scheme" Sustainability 11, no. 19: 5156. https://doi.org/10.3390/su11195156

APA StyleCheng, C. -p., Lin, C. -h., Wen, L. -c., & Chang, T. -c. (2019). Determining Environmental Costs: A Challenge in A Governmental E-Waste Recycling Scheme. Sustainability, 11(19), 5156. https://doi.org/10.3390/su11195156