Reporting of Intellectual Capital Management Using a Scoring Model

Abstract

:1. Introduction

- How to recognise, subjacent to the top-level managers’ answers to the questionnaires, the existence of intangibles with meanings compatible with the ICM (Matos and Lopes, 2009) [2]?

- How to obtain a mathematical model compatible with the ICM (Matos and Lopes, 2009) [2] that accounts for the meaning of intangibles involved in the IC concept and for the implicit or assumed causal relations between those variables?

- How to estimate and validate the ICM (Matos and Lopes, 2009) [2] by using observed data from the available answers to the associated ICM questionnaire, applied a significant number of times in varied and controlled situations?

- How to use the estimated model as a scoring function in order to evaluate the observed SMEs’ IC management?

2. Theoretical Background

3. Support Framework

3.1. Individual Capital (IDC)

3.2. Team Capital (TC)

3.3. Processes Capital (PC)

3.4. Clients Capital (CC)

3.5. NTIC and Network (NET)

3.6. Questionnaire

- Individual Capital Quadrant:

- ▪

- Training/Qualification and Talent Management.

- ▪

- Valuation of Know—How and Innovation.

- ▪

- Investment in Innovation and Development (I & D).

- ▪

- Existence of a Policy for Talent Retention.

- Team Capital Quadrant:

- ▪

- Training/Qualification Team.

- ▪

- Teamwork.

- ▪

- Innovation in Teams.

- ▪

- Leadership in Teams.

- Processes Capital Quadrant:

- ▪

- Processes Systematization.

- ▪

- Registration of Organizational Knowledge.

- ▪

- Existence of Certifications, Environmental, and Social policies.

- ▪

- Partnerships.

- ▪

- Investment in Innovation and Development (I & D).

- ▪

- Brands Creation and Management.

- ▪

- Complaints System.

- ▪

- Existence of Awards.

- Clients Capital Quadrant:

- ▪

- Market Audits.

- ▪

- Management of the Clients’ Satisfaction.

- ▪

- Clients’ Complaints System.

- ▪

- New Markets and Internationalization.

- ▪

- Networks.

- ▪

- New Technologies of Information and Communication.

4. Methodology

4.1. Intellectual Capital as a Vector with Latent Components

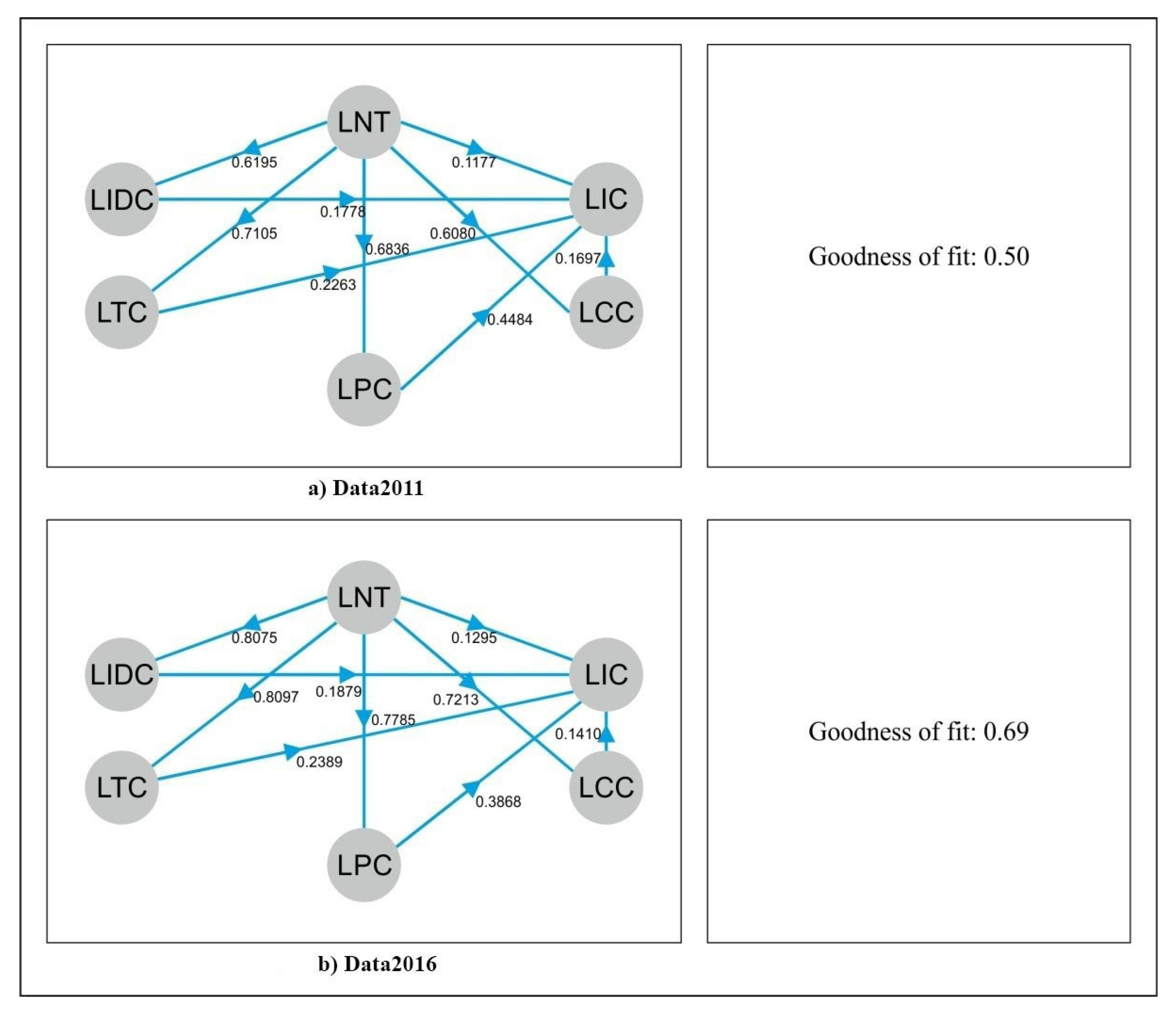

4.2. A Path Model for ICM

- LNT—LV NTIC and Network.

- LIDC—LV Individual Capital.

- LPC—LV Processes Capital.

- LTC—LV Team Capital.

- LCC—LV Clients Capital.

- LIC—LV Intellectual Capital, represented as a scalar value.

5. Data

5.1. Questionnaire

- Parameter 1 (QCIP1)—Training/Qualification and Talent Management (associated with 3 questions—Q1.1, Q1.2, Q1.3).

- Parameter 2 (QCIP2)—Valuation of Know-How and Innovation (associated with 3 questions—Q2.1, Q2.2, Q2.3).

- Parameter 3 (QCIP3)—Investment in Innovation and Development (associated with 8 questions—Q3.1…Q3.8).

- Parameter 4 (QCIP4)—Existence of Policy for Talent Retention (associated with 4 questions—Q4.1, Q4.2, Q4.3, Q4.4).

5.2. Data Organization

6. Data Analysis Results

6.1. Structural Model Estimation

- Mode “A”—Means that all MVs for a LV are of the reflective type: MVs are manifestations of the corresponding LVs. The observed values are caused by the behaviour of the corresponding latent variable.

- Cronbach α—This value measures the coherence and homogeneity of MVs associated with the corresponding LV.

- R2—Quality of fit of the LV by a weighted combination of its MVs.

- First Eigen/Second Eigen—This quotient is an indicator that shows if the first principal component of the MVs group can represent the group. It is the quotient between the first and second eigenvalues for data in each group. The greater the quotient, the greater the importance of the first component; consequently, this quotient indicates the quality of the first principal component as representative of the group.

- TYPE—Variables exogenous or endogenous in relation to the inner model.

- R2—Determination coefficient as in multiple regression.

- Commun.—Communality: Is the percentage of variance of MVs that is explained by the corresponding latent variable.

- Redund.—Redundancy: Given a dependent LV and its independents LVs, it is the percentage of variability of the MVs of those independent LVs that is explained by the dependent LV manifests variance.

- AVE—Average Variance Extracted: the percentage of variance extracted from its indicators in relation to error variance.

6.2. Estimation of the Measurement Model

6.3. Estimating ICM Variants

6.4. Analysis of LVs Scores Using Biplots

7. Results Discussion

8. Conclusions, Limitations, and Future Work

Author Contributions

Funding

Conflicts of Interest

References

- Matos, F. A Theoretical Model for the Report of Intellectual Capital. Electron. J. Knowl. Manag. 2013, 11, 339–360. [Google Scholar]

- Matos, F.; Lopes, A. Intellectual Capital Management—SMEs Accreditation Methodology. In Proceedings of the European Conference on Intellectual Capital, Haarlem, The Netherlands, 28–29 April 2009; Stam, C., Ed.; Academic Publishing Limited: Reading, UK, 2009; pp. 344–354. [Google Scholar]

- Galbraith, J.K. The New Industrial State; Houghton Mifflin Company: Boston, MA, USA, 1967. [Google Scholar]

- Itami, H. Mobilizing Invisible Assets; Harvard University Press: Cambridge, UK, 1987. [Google Scholar]

- Konrad Group. The Invisible Balance Sheet; Sveiby, K., Ed.; Affärsvärlden Förlag: Stockholm, Sweden, 1990; ISBN 91-85804-22-3. [Google Scholar]

- Sveiby, K. The New Organizational Wealth: Managing and Measuring Knowledge-Based Assets; Berrett-Koehler Publishers: San Francisco, CA, USA, 1997; ISBN 1576750140. [Google Scholar]

- Stewart, T.A. Brainpower: How Intellectual Capital is Becoming America’s Most Important Asset. Available online: https://archive.fortune.com/magazines/fortune/fortune_archive/1991/06/03/75096/index.htm (accessed on 1 July 2020).

- Stewart, T.A. Intellectual Capital: The New Wealth of Organizations; Currency Doubleday: New York, NY, USA, 1997; ISBN 0385482280. [Google Scholar]

- Stewart, T.A. The Wealth of Knowledge: Intellectual Capital and the Twenty-First Century Organization; Currency/Doubleday: New York, NY, USA, 2001; ISBN 0385500718. [Google Scholar]

- Bontis, N. World Congress on Intellectual Capital Readings; Elsevier Butterworth Heinemann KMCI Press: Boston, MA, USA, 2002. [Google Scholar]

- Nonaka, I.; Takeuchi, H. The Knowledge-Creating Company: How Japanese Companies Create the Dynamics of Innovation; Oxford University Press: New York, NY, USA, 1995; ISBN 978-0195092691. [Google Scholar]

- Senge, P.M. The Fifth Discipline: The Art and Practice of the Learning Organization; Doubleday/Currency: New York, NY, USA, 1990. [Google Scholar]

- Sullivan, P.H. Profiting from Intellectual Capital: Extracting Value from Innovation; Wiley: Hoboken, NJ, USA, 1998; ISBN 978-0-471-19302-9. [Google Scholar]

- Edvinsson, L. Corporate Longitude: What You Need to Know to Navigate the Knowledge Economy; Financial Times Prentice Hall: London, UK, 2002; ISBN 0273656279. [Google Scholar]

- Edvinsson, L. Developing Intellectual Capital at Skandia. Long Range Plan. 1997, 30, 366–373. [Google Scholar] [CrossRef]

- Edvinsson, L.; Malone, M.S. Intellectual Capital: Realizing Your Company’s True Value by Finding Its Hidden Brainpower; Harper Business: New York, NY, USA, 1997; ISBN 0887308414. [Google Scholar]

- Kaplan, R.S.; Norton, D.P. The Balanced Scorecard: Measures that Drive Performance. Harv. Bus. Rev. 1992, 70, 71–79. [Google Scholar] [PubMed]

- Kaplan, R.S.; Norton, D.P. The Balanced Scorecard: Translating Strategy into Action; Harvard Business School Press: Boston, MA, USA, 1996; ISBN 0875846513. [Google Scholar]

- Kaplan, R.S.; Norton, D.P. Using the Balanced Scorecard as a Strategic Management System. Harv. Bus. Rev. 1996, 74, 75–85. [Google Scholar]

- Mouritsen, J.; Larsen, H.T.; Bukh, P.N. Intellectual Capital and the ‘Capable Firm’: Narrating, Visualising and Numbering for Managing Knowledge. Account. Organ. Soc. 2001, 26, 735–762. [Google Scholar] [CrossRef]

- Andriessen, D.; Tissen, R. Weightless Weight—Find Your Real Value in a Future of Intangible Assets; Pearson Education: London, UK, 2000. [Google Scholar]

- Viedma Martí, J.M. ICBS—Intellectual Capital Benchmarking System. J. Intellect. Cap. 2001, 2, 148–165. [Google Scholar] [CrossRef] [Green Version]

- Zhou, A.Z.; Fink, D. The Intellectual Capital Web. J. Intellect. Cap. 2003, 4, 34–48. [Google Scholar] [CrossRef]

- Abeysekera, I.; Guthrie, J. An Empirical Investigation of Annual Reporting Trends of Intellectual Capital in Sri Lanka. Crit. Perspect. Account. 2005, 16, 151–163. [Google Scholar] [CrossRef] [Green Version]

- Andriessen, D.; Stam, C. Intellectual Capital of The European Union. In Proceedings of the 7th McMaster World Congress on the Management of Intellectual Capital and Innovation, Hamilton, ON, Canada, 19–21 January 2005. [Google Scholar]

- Martí, J.M.V. In Search of an Intellectual Capital General Theory. Electron. J. Knowl. Manag. 2003, 1, 213–226. [Google Scholar]

- Abhayawansa, S.A. A review of guidelines and frameworks on external reporting of intellectual capital. J. Intellect. Cap. 2014, 15, 100–141. [Google Scholar] [CrossRef]

- Dumay, J. Reflections on interdisciplinary accounting research: The state of the art of intellectual capital. Account. Audit. Account. J. 2014, 27, 1257–1264. [Google Scholar] [CrossRef]

- Dumay, J. A critical reflection on the future of intellectual capital: From reporting to disclosure. J. Intellect. Cap. 2016, 17, 168–184. [Google Scholar] [CrossRef]

- Subramaniam, M.; Youndt, M.A. The Influence of Intellectual Capital on the Types of Innovative Capabilities. Acad. Manag. J. 2005, 48, 450–463. [Google Scholar] [CrossRef] [Green Version]

- Lo, C.; Wang, C.; Chen, Y.-C. The Mediating Role of Intellectual Capital in Open Innovation in the Service Industries. Sustainability 2020, 12, 5220. [Google Scholar] [CrossRef]

- Martín-de-Castro, G.; Delgado-Verde, M.; López-Sáez, P.; Navas-López, J.E. Towards ‘An Intellectual Capital-Based View of the Firm’: Origins and Nature. J Bus Ethics 2011, 98, 649–662. [Google Scholar] [CrossRef]

- Choong, K.K. Intellectual capital: Definitions, categorization and reporting models. J. Intellect. Cap. 2008, 9, 609–638. [Google Scholar] [CrossRef] [Green Version]

- Chen, J.; Zhu, Z.; Yuan Xie, H. Measuring intellectual capital: A new model and empirical study. J. Intellect. Cap. 2004, 5, 195–212. [Google Scholar] [CrossRef] [Green Version]

- Andriessen, D. IC valuation and measurement: Classifying the state of the art. J. Intellect. Cap. 2004, 5, 230–242. [Google Scholar] [CrossRef]

- Buenechea-Elberdin, M.; Kianto, A.; Sáenz, J. Intellectual capital drivers of product and managerial innovation in high-tech and low-tech firms. RD Manag. 2018, 48, 290–307. [Google Scholar] [CrossRef]

- Cabrilo, S.; Kianto, A.; Milic, B. The effect of IC components on innovation performance in Serbian companies. Vine J. Inf. Knowl. Manag. Syst. 2018, 48, 448–466. [Google Scholar] [CrossRef]

- Dumay, J.; Guthrie, J.; Rooney, J. Being critical about intellectual capital accounting in 2020: An overview. Crit. Perspect. Account. 2020, 70, 102185. [Google Scholar] [CrossRef]

- Martínez-Torres, M.R. A procedure to design a structural and measurement model of Intellectual Capital: An exploratory study. Inf. Manag. 2006, 43, 617–626. [Google Scholar] [CrossRef]

- Martín-de Castro, G.; Delgado-Verde, M.; Navas-López, J.E.; Cruz-González, J. The moderating role of innovation culture in the relationship between knowledge assets and product innovation. Technol. Forecast. Soc. Chang. 2013, 80, 351–363. [Google Scholar] [CrossRef]

- Martín-de Castro, G. Intellectual capital and the firm: Some remaining questions and prospects. Knowl. Manag. Res. Pract. 2014, 12, 239–245. [Google Scholar] [CrossRef]

- Matos, F.; Vairinhos, V.; Osinski, M. Intellectual capital management as an indicator of sustainability. In Proceedings of the European Conference on Knowledge Management, Academic Conferences International Limited, Barcelona, Spain, 7–8 September 2017; pp. 655–663. [Google Scholar]

- Utama, A.A.G.S.; Mirhard, R.R. The influence of sustainability report disclosure as moderating variable towards the impact of intellectual capital on company’s performance. Int. J. Econ. Financ. Issues 2016, 6, 1262–1269. [Google Scholar]

- Rodrigues, L.L.; Tejedo-Romero, F.; Craig, R. Corporate governance and intellectual capital reporting in a period of financial crisis: Evidence from Portugal. Int. J. Discl. Gov. 2017, 14, 1–29. [Google Scholar] [CrossRef] [Green Version]

- Matos, F.; Vairinhos, V.M. Intellectual capital management as a driver of competitiveness and sustainability. J. Intellect. Cap. 2017, 18, 466–469. [Google Scholar] [CrossRef] [Green Version]

- Matos, F.; Vairinhos, V.; Selig, P.M.; Edvinsson, L. Introduction. In Intellectual Capital Management as a Driver of Sustainability; Matos, F., Vairinhos, V., Selig, P., Edvinsson, L., Eds.; Springer: Cham, Switzerland, 2019; p. 5. [Google Scholar]

- Matos, F.; Lopes, A.; Matos, N.; Vairinhos, V. Testing the Intellectual Capital Model Using Biplots. In Proceedings of the European Conference on Knowledge Management, Cartagena, Spain, 6–7 September 2012; Academic Publishing Limited: Reading, UK, 2012; Volume 1, pp. 717–725. [Google Scholar]

- Abdi, H.; Chin, W.W.; Vinzi, V.E.; Russolillo, G.; Trinchera, L. (Eds.) New Perspectives in Partial Least Squares and Related Methods; Springer: Berlin/Heidelberg, Germany, 2013. [Google Scholar]

- Sanchez, G. PLS Path Modeling with R.; Trowchez Editions: Berkeley, CA, USA, 2013. [Google Scholar]

- Tenenhaus, M.; Vinzi, V.E.; Chatelin, Y.-M.; Lauro, C. PLS Path Modeling. Comput. Stat. Data Anal. 2005, 48, 159–205. [Google Scholar] [CrossRef]

- Trinchera, L.; Russolillo, G. On the Use of Structural Equation Models and PLS Path Modeling to Build Composite Indicators. 2010. Available online: https://core.ac.uk/download/pdf/6471123.pdf (accessed on 1 July 2020).

- Vinzi, V.E.; Russolillo, G. Partial Least Squares Algorithms and Methods. Wiley Interdiscip. Rev. Comput. Stat. 2012, 5, 1–19. [Google Scholar] [CrossRef]

- Sanchez, G.; Trinchera, L.; Russolillo, G. R Package “plspm”: Tools for Partial Least Squares Path Modeling (PLS-PM). 2015. Available online: https://rdrr.io/cran/plspm/f/inst/doc/plspm_introduction.pdf (accessed on 1 July 2020).

- Hwang, H.; Takane, Y. Generalized Structured Component Analysis: A Component-Based Approach to Structural Equation Modeling; Chapman and Hall/CRC: London, UK, 2014; ISBN 978-0-429-16845-1. [Google Scholar]

- Gabriel, K.R. The Biplot Graphic Display of Matrices with Application to Principal Component Analysis. Biometrika 1971, 58, 453–467. [Google Scholar] [CrossRef]

- Vairinhos, V.; Galindo Villardón, M.P. Biplots PMD—Data Mining Centrada em Biplots. Apresentação de um Protótipo. 2004. Available online: https://www.academia.edu/25177669/Biplots_PMD_Data_Mining_Centrada_em_Biplots_Apresenta%C3%A7%C3%A3o_de_um_Prot%C3%B3tipo (accessed on 1 July 2020).

- Alvarenga, A.; Matos, F.; Godina, R.; C. O. Matias, J. Digital Transformation and Knowledge Management in the Public Sector. Sustainability 2020, 12, 5824. [Google Scholar] [CrossRef]

- Karier, T. Intellectual Capital: Forty Years of the Nobel Prize in Economics; Cambridge University Press: New York, NY, USA, 2010; ISBN 978-0-521-76326-4. [Google Scholar]

- Vairinhos, V.M. BiplotsPMD—Un programa para Análisis Multivariante Centrada en Biplots. In Proceedings of the Congreso Internacional de Estadística y Medio Ambiente (EMA4), Salamanca, Spain, 24–26 September 2003. [Google Scholar]

- Henseler, J.; Dijkstra, T.K.; Sarstedt, M.; Ringle, C.M.; Diamantopoulos, A.; Straub, D.W.; Ketchen, D.J., Jr.; Hair, J.F.; Hult, G.T.M.; Calantone, R.J. Common Beliefs and Reality About PLS: Comments on Ro nkko and Evermann (2013). Organ. Res. Methods 2014, 17, 182–209. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Latent Variable | Number of Manifest Variables | Mode | Cronbach α | R2 | First Eigen/Second Eigen |

|---|---|---|---|---|---|

| LNT | 2 | A | 0.72 | 0.87 | 3.6 |

| LIDC | 4 | A | 0.83 | 0.89 | 4.1 |

| LTC | 4 | A | 0.79 | 0.87 | 5.6 |

| LPC | 8 | A | 0.81 | 0.86 | 2.9 |

| LCC | 4 | A | 0.49 | 0.60 | 1.2 |

| LIC | 22 | A | 0.92 | 0.93 | 3.5 |

| Latent Variable | Number of Manifest Variables | Mode | Cronbach α | R2 | First Eigen/Second Eigen |

|---|---|---|---|---|---|

| LNT | 2 | A | 0.94 | 0.97 | 15.5 |

| LIDC | 4 | A | 0.92 | 0.94 | 7.9 |

| LTC | 4 | A | 0.92 | 0.94 | 6.9 |

| LPC | 8 | A | 0.83 | 0.87 | 2.6 |

| LCC | 4 | A | 0.80 | 0.87 | 2.3 |

| LIC | 22 | A | 0.96 | 0.96 | 5.9 |

| Data2011 | Data2016 | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| LV | TYPE | R2 | Commun. | Redund. | AVE | R2 | Commun. | Redund. | AVE |

| LNT | Exog. | 0.00 | 0.77 | 0.00 | 0.78 | 0.00 | 0.93 | 0.00 | 0.93 |

| LIDC | Endog. | 0.38 | 0.67 | 0.26 | 0.67 | 0.65 | 0.80 | 0.52 | 0.80 |

| LTC | Endog. | 0.51 | 0.62 | 0.31 | 0.62 | 0.66 | 0.79 | 0.50 | 0.79 |

| LPC | Endog. | 0.47 | 0.42 | 0.20 | 0.42 | 0.61 | 0.47 | 0.29 | 0.47 |

| LCC | Endog. | 0.37 | 0.37 | 0.14 | 0.38 | 0.52 | 0.60 | 0.31 | 0.60 |

| LIC | Endog. | 1.00 | 0.40 | 0.40 | 0.40 | 1.00 | 0.55 | 0.55 | 0.55 |

| LVs | MVs | Data2011 | Data2016 |

|---|---|---|---|

| LNT | PR | 0.94375 | 0.6388 |

| PNT | 0.60751 | 0.4384 | |

| LIDC | QCI P1 | 0.48770 | 0.3256 |

| QCI P2 | 0.45631 | 0.3398 | |

| QCI P3 | 0.46318 | 0.2950 | |

| QCI P4 | 0.45937 | 0.3384 | |

| LPC | QCP P1 | 0.23514 | 0.1441 |

| QCP P2 | 0.06616 | 0.2054 | |

| QCP P3 | 0.15351 | 0.0342 | |

| QCP P4 | 0.22985 | 0.1803 | |

| QCP P5 | 0.30579 | 0.2492 | |

| QCP P6 | 0.19260 | 0.1410 | |

| QCP P7 | 0.17773 | 0.1578 | |

| QCP P8 | 0.26165 | 0.1153 | |

| LCC | QCC P1 | 0.54626 | 0.4906 |

| QCC P2 | 0.04544 | 0.3185 | |

| QCC P3 | 0.08231 | 0.2433 | |

| QCC P4 | 0.77759 | 0.4100 | |

| LTC | QCE P1 | 0.34871 | 0.2606 |

| QCE P2 | 0.41328 | 0.3172 | |

| QCE P3 | 0.58069 | 0.3630 | |

| QCE P4 | 0.33192 | 0.2260 |

| Hypothesis | Goodness of Fit (Data2011) (Data2016) | |

|---|---|---|

| Basic Model (BM) | 0.50 | 0.69 |

| (BM) + (LIDC → LTC) | 0.52 | 0.66 |

| (BM) + (LPC → LCC) | 0.52 | 0.66 |

| (BM) + {(LIDC → LTC), (LPC → LCC)} | 0.54 | 0.68 |

| (BM) + {(LIDC → LTC), (LPC → LCC), (LIDC → LPC)} | 0.54 | 0.68 |

| Saturated Model | 0.60 | 0.60 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Matos, F.; Vairinhos, V.; Godina, R. Reporting of Intellectual Capital Management Using a Scoring Model. Sustainability 2020, 12, 8086. https://doi.org/10.3390/su12198086

Matos F, Vairinhos V, Godina R. Reporting of Intellectual Capital Management Using a Scoring Model. Sustainability. 2020; 12(19):8086. https://doi.org/10.3390/su12198086

Chicago/Turabian StyleMatos, Florinda, Valter Vairinhos, and Radu Godina. 2020. "Reporting of Intellectual Capital Management Using a Scoring Model" Sustainability 12, no. 19: 8086. https://doi.org/10.3390/su12198086

APA StyleMatos, F., Vairinhos, V., & Godina, R. (2020). Reporting of Intellectual Capital Management Using a Scoring Model. Sustainability, 12(19), 8086. https://doi.org/10.3390/su12198086