IC was identified as a critical component for managing logistics service providers [

52]. Nevertheless, the IC benchmarking research in the logistics domain has still never been studied, even in Thailand [

7]. Therefore, in 2017, this study used a case from four commercial logistics companies that are well-known express courier organizations operating in Thailand. The research focuses on a specific type of logistics business, express couriers, because the courier sector of Thailand has been identified as one of the most crucial sectors. It had the biggest growth among all logistics businesses [

53] in Thailand, and, moreover, the IC management in the courier sector has also never been studied in any academic research before. The benchmarking results obtained through this case study are expected to provide in-depth information that would demonstrate advantages and disadvantages of the proposed method and, moreover, would suggest improvement opportunities as well as priorities for all logistics service providers, especially to local Thai firms. Therefore, to properly highlight the differences of benchmarking cases, we included both top international players and local developing players in the market in this study. Moreover, to usefully suggest improvement opportunities and sustainable development to the local firms, we selected two high-potential and local companies to participate in this study. Although this study carried out strategic benchmarking, which mostly involves non-confidential information, participants that are in middle to top management are still unwilling to disclose their identities, neither their individual identities nor those of their organizations. Regarding this agreement, data and information that could present or imply their identities are not presented. Therefore, general information about these organizations is presented in

Table 2. Two companies (Companies A and B) are international organizations and are unofficially classified as the top five express courier companies in the world. The two other firms have their main operating bases in Thailand (Companies C and D), of which one (Company C) is a Thai organization, which has developed from a small and medium-sized enterprise and operates only in Thailand. Since one of these firms (Company A) has been widely accepted as ranking first among the express courier businesses in the world, this player would present the best managerial model or IC management practice for other performers. To provide the current managerial focuses of all firms, their major management strategies are summarized as follows: (1) Company A focused on a broad differentiation strategy, which aimed to serve customers with a high standard of quality internationally; (2) Company B focused on a specific customer segment that required international service quality by having lower costs than other firms; (3) Company C intended to be an overall low-cost service provider; and, finally, (4) Company D concentrated on a focused service quality, which mainly served local Thai customers who required moderate to high service quality with an acceptable price. In the following sections, details of the application of the proposed method are presented.

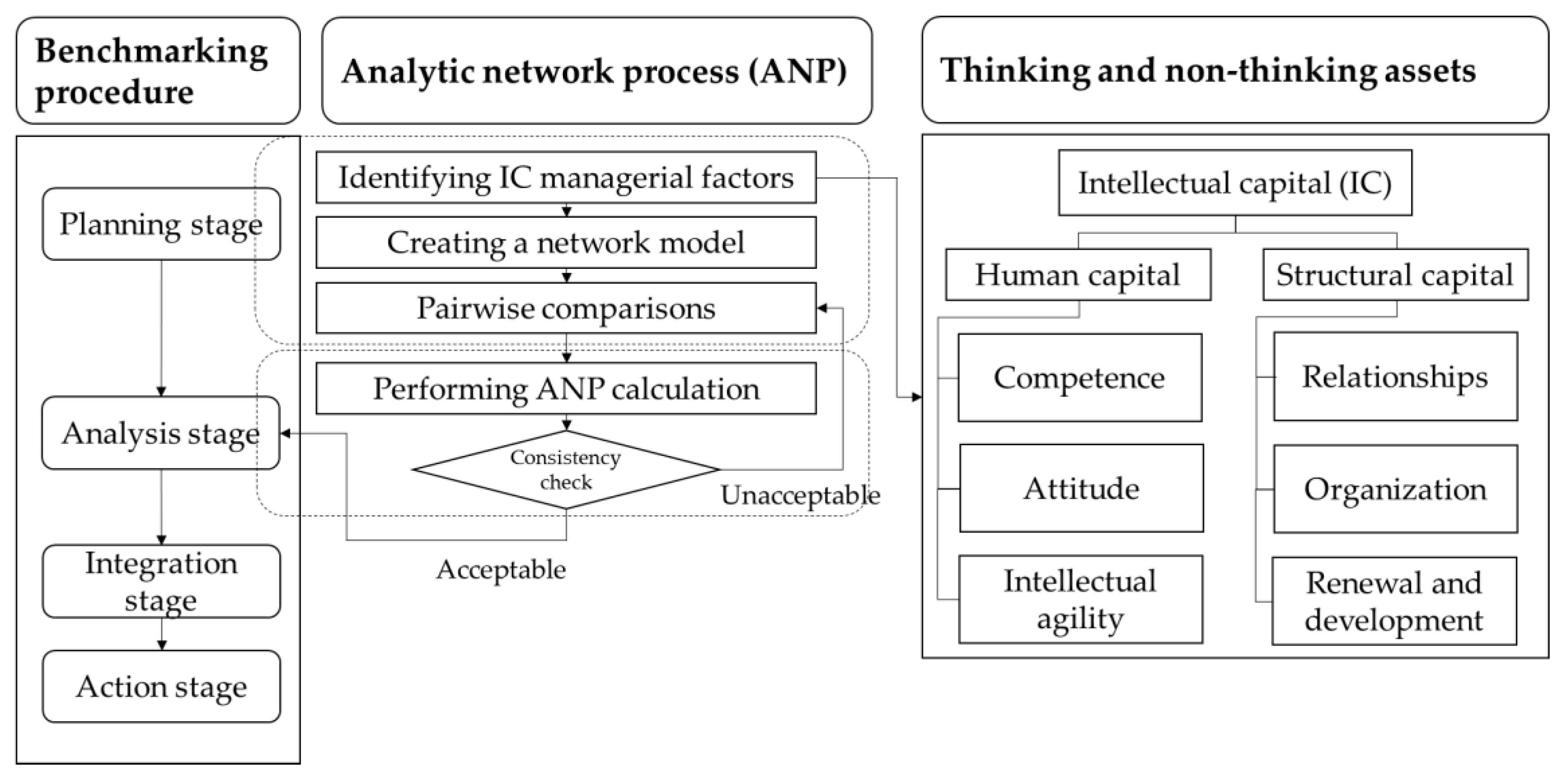

4.1. Stage 1: Planning Phase

First, the objective of this benchmarking is to study and benchmark the strategic management of the IC among four organizations in the logistics domain, as this topic is still underdeveloped, as mentioned above in the prior literature section. The management of IC aspects—human capital and structural capital—that are considered according to the thinking and non-thinking assets concept are divided into six elements—competence, attitude, intellectual agility, organization, relationships, and renewal and development. Most of these IC elements, such as competence, relationships, and renewal and development, were empirically and widely identified as sustainable development factors in several businesses.

As mentioned above, in the second step, Company A was identified as the best performer, since it was broadly acknowledged as ranking first among express courier organizations in the world. Therefore, the IC management and concentration of this firm would be considered best practices for the other players in the comparison.

The last step of this phase is to collect all required data following the requirements of the ANP approach. Specifically, to benchmark the IC management between the logistics firms in focus, in this study, the strategic management of IC was studied using the managerial concentration of the firms’ performance measures. Therefore, the first-round enquiry aimed to collect the current measurements of IC in all the studied organizations. In the first survey form, to clarify IC measures, examples were provided of indicators in logistics that were obtained from previous intensive literature reviews on IC management [

1]. An expert from the middle or top management of each logistics firm was interviewed following the structured questionnaire. In the questionnaire, a comprehensive list of IC performance indicators of logistics businesses was included. The provided indices were obtained from our in-depth literature review in a previous study [

1]. The results of the first-round enquiry indicated the IC management of all firms based on their strategic performance indicators. The obtained measures were then classified according to the thinking and non-thinking assets, as shown in

Table 3.

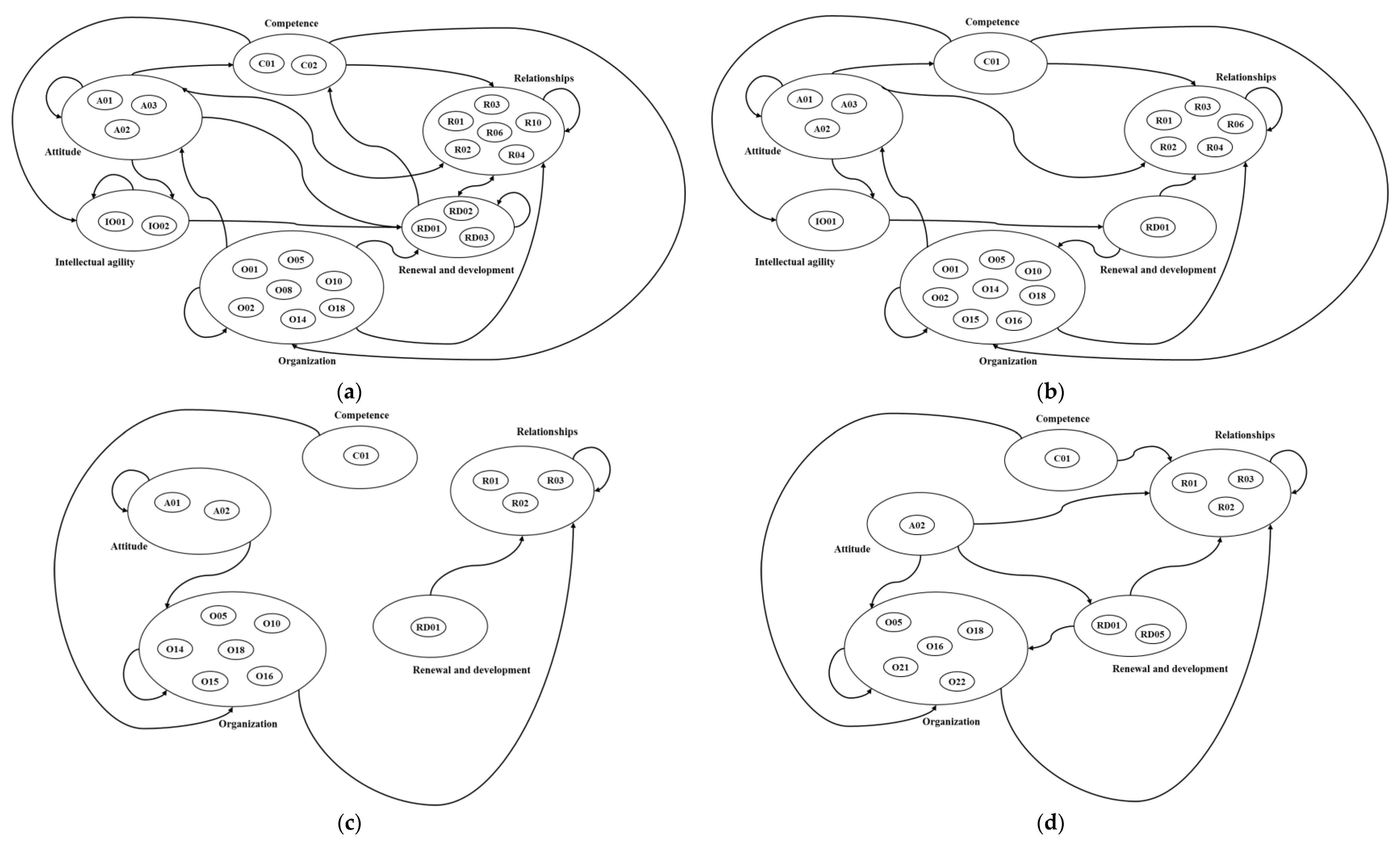

After the measurable indicators were already identified by the participating management, in the second-round enquiry, to create a relational network of IC management following the ANP concept, experts were asked, based on their experience, to identify dependencies among the measures applied in their related organization. Therefore, the obtained results provided visualized networks of the IC management of the firms, as depicted in

Figure 2. In this figure, the line with the arrowhead denotes the dependence between the connected clusters. The one-way arrowhead indicates the influence of the beginning cluster on the ending cluster. For instance, regarding the example of Company A (

Figure 2a), the line starting from the organization cluster and ending with the arrowhead at the relationship cluster implies that the organization element affects the relationship element. Similarly to the two-way arrowhead, this denotes the influences between the two connected clusters. For example, the two-way arrowhead for the case of Company A implies the influences between the renewal and development and the relationships.

However, the network model could only demonstrate relationships from the cluster perspective (IC component level). It is still unable to provide in-depth details at the performance indicator level. Hence, the interrelationships at this level are presented in the zero–one matrix depicted in

Table 4. According to the values in the matrix, there are two values, one and zero, and one sign, the hyphen (-). The value of one implies that the measure in the vertical axis influences the indicator in the horizontal axis, the zero value indicates the irrelevance between paired measures, and the hyphen denotes that the indicator in either the vertical or horizontal axis did not exist or was not applied in that organization. On the other hand, the value in each segment can be separated into four digits. The first digit implies the influence between the indicators of Company D, and the second, third, and fourth digits of the value denote the relationships of Companies C, B, and A, respectively. For example, the segment of O01 in the vertical axis and A01 in the horizontal axis shows the value of “10--”. The first (-) and second (-) digits indicate that both indicators (O01 and A01) were not applied together at Companies C and D. At the same time, in the case of Company B, the value of the third digit is zero, which implies that the expert found that O01 did not influence A01. Moreover, the fourth digit with the value of one denotes that the management of Company A found that O01 affected A01.

To identify the influences among all related IC elements and IC performance measures, all indicated interrelationships in

Figure 2 and

Table 4 were further input into the Super Decisions software (version Windows 2.80, The Creative Decisions Foundation, Pittsburgh, PA, USA) to create the third-round questionnaire specific to each organization. The generated questions, which are pairwise comparisons, consist of two major parts: comparative questions at the IC element level and the IC performance measure level. The numbers of the questions created are identified in

Table 5.

In this questionnaire, the management members were asked to indicate the magnitude of influences between the related clusters and nodes following the 1–9 ANP scales. After the experts answered all comparative questions in the related questionnaires that were specifically created for each organization, as shown in

Table 5, the obtained answers were applied for calculating further results, which will be explained in the following.

4.2. Stage 2: Analysis Phase

All the answers obtained from the second enquiry were input into the Super Decisions software to calculate the supermatrix, weighted supermatrix, and limit supermatrix of each organization. However, between the calculations, the inspection of nonconformity was concurrently carried out throughout sets of pairwise comparisons, and there were some inconsistent results wherein CRs were higher than 0.10. In the first-round enquiry of pairwise comparisons, regarding the number of indicators and comparative questions, three organizations (Companies A, B, and C) still presented inconsistent results, as shown in

Table 6. Therefore, to address this inconsistency issue, pairwise comparison questions related to the unreliable results were sent to the respective experts for reassessment.

Regarding the decrease in the number of questions, this round of enquiry could improve the confusion of experts in making comparisons. Therefore, after the reassessment process, all the CR results, as presented in

Table 6, are lower than 0.10, which implies the consistency of all answers. The results conforming to an acceptable level were further used for calculating the supermatrix, weighted supermatrix, and limit supermatrix with the Super Decisions software. The results computed from the limit supermatrix interestingly presented weights of strategic concentration on the IC management of each firm, which can be benchmarked at the IC element level and IC indicator level, as shown in

Table 7 and

Table 8, respectively.

Table 7 depicts the strategic benchmarking results of IC managerial concentration, which are mostly different among the firms in focus. Nevertheless, the top three organizations, which are well-known and high-performance firms (Companies A, B, and D), all considered organization capital as the most crucial IC element. Although Company C, the local Thai firm, did not identify the organization element as having the highest importance, it still considered this type of capital as the second priority. These results highlighted the preference of express courier companies in Thailand for this IC sub-element of structural capital. However, the IC sub-element of attitude was identified as having the second highest importance, especially for the international organizations, that is, Companies A and B. Nevertheless, the logistics firms (Companies C and D) that have major operating bases in Thailand considered this element as being the third priority. Overall, considering the first three priorities, which highlighted the strategic focus on IC management, all logistics firms similarly concentrated on the three elements of organization, competence, and attitude.

Although

Table 7 depicts new and interesting results, including priorities and weights, which are not found in the traditional benchmarking approach, it still cannot provide details or specifically indicate the concentration on the performance indicator level. Therefore, the results of the in-depth investigation into the performance indicator level of IC management are depicted in

Table 8. From

Table 8, considering the rankings of measures in the overall elements (the front numbers indicated in parentheses), it is apparent that the managerial focus of each firm on the level of performance measures is significantly different in either the magnitude of concentration or the number of indicators assigned for the weights.

Regarding the above consideration, the overall analysis of all IC elements presents significant differences in the IC management of logistics firms. Therefore, to narrowly consider the specific perspective, analysis of the major IC elements—human and structural capital—was further carried out. The results from this process are presented by the back numbers in parentheses in

Table 8.

The analysis of

Table 8 demonstrated the magnitude of concentration on IC by each firm, which can provide the differences and gaps in managerial focus between the best player and other competitive firms. This can lead to the creation of an improvement plan for inferior companies. Furthermore, to gain more advantageous information from the survey results, an analysis of the quantitative usage of IC indicators was carried out, as shown in

Table 9.

The results in

Table 9 show that there are differences in the amounts of indicators applied among the benchmarked firms. The number of IC measures used by international firms was higher than that by firms mainly operating in Thailand. Furthermore, the international companies also applied indicators covering all six IC sub-dimensions that were more comprehensive and had higher amounts of applied indicators than local firms. Companies A and B, the international organizations, measured the IC performance through 23 and 19 indicators, respectively, for all six IC elements, while Companies C and D, local firms that have their main operating bases in Thailand, used only 13 and 12 measures, respectively, for all IC elements, except intellectual agility.

Considering the quantitative usage of measures for IC elements, the results apparently show that the top four measured elements were quite similar. All firms had ranked the same indicators as the first and second highest in terms of their application, which are organization and relationships, respectively. Nevertheless, the third rank was slightly different in some companies. Companies A and D ranked the renewal and development element as third, while Companies B and C ranked the amounts of measures of the attitude element as third.

The above results of the analysis phase highlight several differences between the best performers and other players, as well as, especially, between international firms and local companies. Based on these results, there are several managerial approaches of IC, especially for developing organizations that should be improved. Nevertheless, due to the limited resources and time of this research as well as the management authority in all studied firms, this study could not execute the integration and action phase. However, after the acknowledgment of the benchmarked results and recent follow-up, only the developing companies, which are local firms, aimed to apply the analyzed information as well as the benchmark measures to construct future IC improvement and management plans. For instance, Company C planned to include and manage unused IC measures, such as O01and O15, that were applied by the international firm focusing on the cost control strategy, which is similar to the firm’s direction. On the other hand, Company D, which adhered to the service quality, expected to elevate the service quality by utilizing more service-related activities, such as O02 and R04, following the best player in the market.

Therefore, in this study, the findings and their analysis could only reveal the managerial gaps as well as improvement opportunities and plans. Therefore, in the following section, analysis and discussion related to the results and improved method are presented.

{kind=link}

{kind=link}