The Effects of Knowledge Assets and Path Dependence in Innovations on Firm Value in the Korean Semiconductor Industry

Abstract

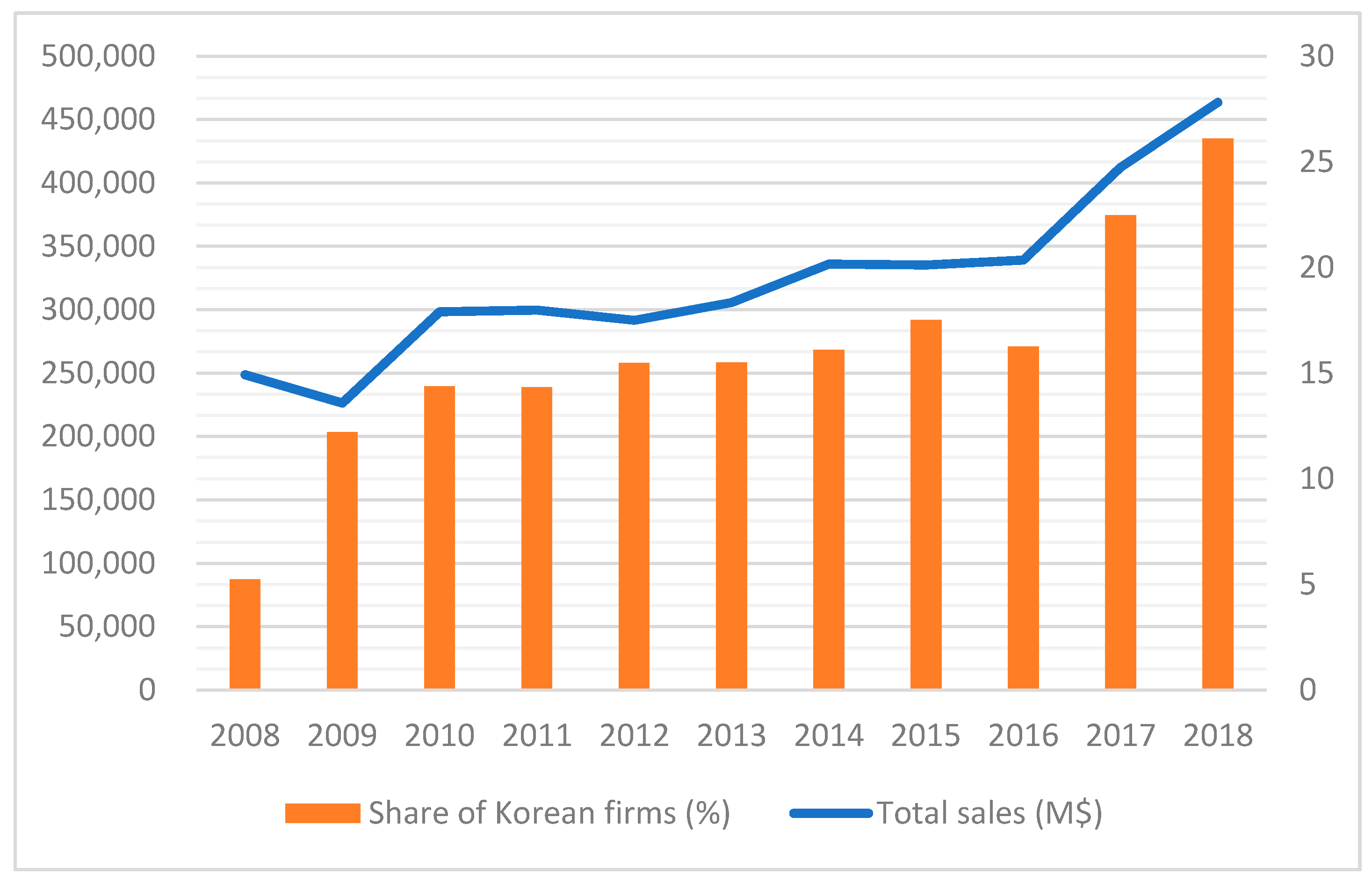

:1. Introduction

2. Theoretical Background and Hypotheses

2.1. Firm Value

2.2. Knowledge Assets

2.3. Technological Innovation by Path Dependence

3. Methodology

3.1. Sample

3.2. Measures

3.2.1. Dependent Variable

3.2.2. Independent Variables

3.2.3. Control Variables

3.3. Estimation

4. Results and Discussion

4.1. Descriptive Statistics

4.2. Main Results

4.3. Robustness Check

5. Conclusions

Funding

Acknowledgments

Conflicts of Interest

References

- O’Reagan, D.; Fleming, L. The FinFET breakthrough and networks of innovation in the semiconductor industry, 1980–2005: Applying digital tools to the history of technology. Technol. Cult. 2018, 59, 251–288. [Google Scholar] [CrossRef] [Green Version]

- Park, J.H.; Kook, S.H.; Im, H.; Eum, S.; Lee, C. Fabless semiconductor firms’ financial performance determinant factors: Product platform efficiency and technological capability. Sustainability 2018, 10, 3373. [Google Scholar] [CrossRef] [Green Version]

- Seitz, A.; Ehm, H.; Akkerman, R.; Osman, S. A robust supply chain planning framework for revenue management in the semiconductor industry. J. Revenue Pricing Manag. 2016, 15, 523–533. [Google Scholar] [CrossRef]

- Hall, B.H.; Jaffe, A.B.; Trajtenberg, M. The NBER patent citation data file: Lessons, insights and methodological tools. Available online: https://www.nber.org/papers/w8498 (accessed on 4 March 2020).

- Korea International Trade Association. Available online: http://stat.kita.net/stat/kts/pum/ItemImpExpList.screen (accessed on 4 March 2020).

- World Semiconductor Trade Statistics. Available online: www.wsts.org (accessed on 4 March 2020).

- IC Insights. Available online: www.icinsights.com (accessed on 4 March 2020).

- Schumpeter, J.A. Capitalism, Socialism and Democracy; Harper & Brothers: New York, NY, USA, 1942. [Google Scholar]

- Donate, M.J.; de Pablo, J.D. The role of knowledge-oriented leadership in knowledge management practices and innovation. J. Bus. Res. 2015, 68, 360–370. [Google Scholar] [CrossRef]

- Anzenbacher, A.; Wagner, M. The role of exploration and exploitation for innovation success: Effects of business models on organizational ambidexterity in the semiconductor industry. Int. Entrep. Manag. J. 2019. [Google Scholar] [CrossRef]

- Colomo-Palacios, R.; García-Crespo, Á.; Gómez-Berbís, J.M.; Casado-Lumbreras, C.; Soto-Acosta, P. SemCASS: Technical competence assessment within software development teams enabled by semantics. Int. J. Soc. Humanist. Comput. 2010, 1, 232–245. [Google Scholar] [CrossRef]

- Darroch, J. Knowledge management, innovation and firm performance. J. Knowl. Manag. 2005, 9, 101–115. [Google Scholar] [CrossRef]

- Artz, K.W.; Norman, P.M.; Hatfield, D.E.; Cardinal, L.B. A longitudinal study of the impact of R&D, patents, and product innovation on firm performance. J. Prod. Innovat. Manag. 2010, 27, 725–740. [Google Scholar]

- Belderbos, R.; Carree, M.; Lokshin, B. Cooperative R&D and firm performance. Res. Policy 2004, 33, 1477–1492. [Google Scholar]

- Lin, C.; Li, B.; Wu, Y.J. Existing knowledge assets and disruptive innovation: The role of knowledge embeddedness and specificity. Sustainability 2018, 10, 342. [Google Scholar] [CrossRef] [Green Version]

- Thornhill, S. Knowledge, innovation and firm performance in high-and low-technology regimes. J. Bus. Ventur. 2006, 21, 687–703. [Google Scholar] [CrossRef]

- Camagni, R.P. Technological Change, Uncertainty and Innovation Networks: Towards A Dynamic Theory of Economic Space. In Regional Science; Boyce, D.E., Nijkam, P., Shefer, D., Eds.; Springer: Heidelberg, Berlin, 1991; pp. 211–249. [Google Scholar]

- Yayavaram, S.; Srivastava, M.K.; Sarkar, M.B. Role of search for domain knowledge and architectural knowledge in alliance partner selection. Strateg. Manag. J. 2018, 39, 2277–2302. [Google Scholar] [CrossRef]

- Zollo, M.; Winter, S.G. Deliberate learning and the evolution of dynamic capabilities. Organ. Sci. 2002, 13, 339–351. [Google Scholar] [CrossRef]

- Paruchuri, S.; Awate, S. Organizational knowledge networks and local search: The role of intra-organizational inventor networks. Strateg. Manag. J. 2017, 38, 657–675. [Google Scholar] [CrossRef]

- Berndt, E.R. The Practice of Econometrics: Classic and Contemporary; Addison Wesley Publishing Company: Boston, MA, USA, 1991. [Google Scholar]

- Chen, M.C.; Cheng, S.J.; Hwang, Y. An empirical investigation of the relationship between intellectual capital and firms’ market value and financial performance. J. Intellect. Cap. 2005, 6, 159–176. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. Linking the balanced scorecard to strategy. Calif. Manag. Rev. 1996, 39, 53–79. [Google Scholar] [CrossRef]

- Boasson, V.; Boasson, E. Firm value, spatial knowledge flow, and innovation: evidence from patent citations. China Financ. Rev. Int. 2015, 5, 132–160. [Google Scholar] [CrossRef]

- Collins, C.J.; Smith, K.G. Knowledge exchange and combination: The role of human resource practices in the performance of high-technology firms. Acad. Manag. J. 2006, 49, 544–560. [Google Scholar] [CrossRef] [Green Version]

- Stewart, T.; Ruckdeschel, C. Intellectual capital: The new wealth of organizations. Perform. Improv. 1998, 37, 56–59. [Google Scholar] [CrossRef]

- Saviotti, P.P. On the dynamics of appropriability, of tacit and of codified knowledge. Res. Policy 1998, 26, 843–856. [Google Scholar] [CrossRef]

- Polanyi, M. The logic of tacit inference. Philosophy 1966, 41, 1–8. [Google Scholar] [CrossRef]

- Agrawal, A. Engaging the inventor: Exploring licensing strategies for university inventions and the role of latent knowledge. Strateg. Manag. J. 2006, 27, 63–79. [Google Scholar] [CrossRef]

- Edvinsson, L. Developing intellectual capital at Skandia. Long. Range. Plann. 1997, 30, 366–373. [Google Scholar] [CrossRef]

- Brooking, A. Intellectual Capital; Cengage Learning EMEA: London, UK, 1998. [Google Scholar]

- Alegre, J.; Sengupta, K.; Lapiedra, R. Knowledge management and innovation performance in a high-tech SMEs industry. Int. Small Bus. J. 2013, 31, 454–470. [Google Scholar] [CrossRef]

- Pater, R.; Lewandowska, A. Human capital and innovativeness of the European Union regions. Innovat. Eur. J. Soc. Sci. Res. 2015, 28, 31–51. [Google Scholar] [CrossRef]

- Zhao, R.; Sheng, X. Innovation-Related Diversification and Firm Value. Eur. Financ. Manag. 2017, 23, 475–518. [Google Scholar]

- Singh, J. Distributed R&D, cross-regional knowledge integration and quality of innovative output. Res. Policy 2008, 37, 77–96. [Google Scholar]

- Bain, J.S. Barriers to New Competition, Their Character and Consequences in Manufacturing Industries; Harvard University Press: Cambridge, MA, USA, 1956. [Google Scholar]

- Cantwell, J. Transnational Corporations and Innovatory Activities; Taylor & Francis: Philadelphia, PA, USA, 1994. [Google Scholar]

- Bell, G.G. Clusters, networks, and firm innovativeness. Strateg. Manag. J. 2005, 26, 287–295. [Google Scholar] [CrossRef]

- Nelson, R.R.; Winter, S.G. Evolutionary theorizing in economics. J. Econ. Perspect. 2002, 16, 23–46. [Google Scholar] [CrossRef] [Green Version]

- March, J.G.; Simon, H.A. Organizations; Wiley: New York, NY, USA, 1958. [Google Scholar]

- March, J.G.; Olsen, J.P. Ambiguity and Choice in Organizations; Universitetsforlaget: Bergen, Norway, 1979. [Google Scholar]

- Ahuja, G.; Morris Lampert, C. Entrepreneurship in the large corporation: A longitudinal study of how established firms create breakthrough inventions. Strateg. Manag. J. 2001, 22, 521–543. [Google Scholar] [CrossRef]

- Katila, R. New product search over time: Past ideas in their prime? Acad. Manag. J. 2002, 45, 995–1010. [Google Scholar] [CrossRef]

- Gupta, A.K.; Smith, K.G.; Shalley, C.E. The interplay between exploration and exploitation. Acad. Manag. J. 2006, 49, 693–706. [Google Scholar] [CrossRef]

- March, J.G. Exploration and exploitation in organizational learning. Organ. Sci. 1991, 2, 71–87. [Google Scholar] [CrossRef]

- Cohen, W.M.; Levinthal, D.A. Absorptive capacity: A new perspective on learning and innovation. Admin. Sci. Quart. 1990, 35, 128–152. [Google Scholar] [CrossRef]

- Levitt, B.; March, J.G. Organizational learning. Annu. Rev. Sociol. 1988, 14, 319–338. [Google Scholar] [CrossRef]

- DataGuide. Available online: www.dataguide.co.kr (accessed on 4 March 2020).

- WIPS ON. Available online: www.wipson.com (accessed on 4 March 2020).

- Lin, B.W.; Chen, C.J.; Wu, H.L. Patent portfolio diversity, technology strategy, and firm value. IEEE Trans. Eng. Manag. 2006, 53, 17–26. [Google Scholar]

- Galasso, A.; Schankerman, M. Patent rights, innovation, and firm exit. RAND J. Econ. 2018, 49, 64–86. [Google Scholar] [CrossRef]

- Hall, B.H.; Jaffe, A.B.; Trajtenberg, M. Market value and patent citations: A first look. NBER Work. Pap. Ser.. 2000. Available online: https://www.nber.org/papers/w7741 (accessed on 4 March 2020).

- Jaffe, A.B.; Trajtenberg, M. International knowledge flows: Evidence from patent citations. Econ. Innov. New. Technol. 1999, 8, 105–136. [Google Scholar] [CrossRef]

- Carpenter, M.A. The implications of strategy and social context for the relationship between top management team heterogeneity and firm performance. Strateg. Manag. J. 2002, 23, 275–284. [Google Scholar] [CrossRef]

- Thompson, S.B. Simple formulas for standard errors that cluster by both firm and time. J. Financ. Econ. 2011, 99, 1–10. [Google Scholar] [CrossRef]

- Cohen, W.M.; Nelson, R.R.; Walsh, J.P. Protecting Their Intellectual Assets: Appropriability Conditions and Why US Manufacturing Firms Patent (or not) (No. w7552); National Bureau of Economic Research: Cambridge, MA, USA, 2000. [Google Scholar]

- Levin, R.C.; Klevorick, A.K.; Nelson, R.R.; Winter, S.G.; Gilbert, R.; Griliches, Z. Appropriating the returns from industrial research and development. Brook. Pap. Econ. Act. 1987, 3, 783–831. [Google Scholar] [CrossRef] [Green Version]

- Hall, B.H.; Ziedonis, R.H. The patent paradox revisited: An empirical study of patenting in the US semiconductor industry 1979–1995. RAND J. Econ. 2001, 32, 101–128. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

| Variable | Obs. | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| 1. ROA | 37 | 0.0310 | 0.0882 | −0.1905 | 0.1915 |

| 2. Patents | 37 | 5.1351 | 9.7016 | 1 | 59 |

| 3. Self citation | 37 | 0.2265 | 0.3627 | 0 | 1.25 |

| 4. Other citation | 37 | 1.0038 | 0.8210 | 0 | 3 |

| 5. Firm age | 37 | 25.8378 | 16.8218 | 5 | 78 |

| 6. R&D expenditure | 37 | 0.0425 | 0.0478 | 0.0003 | 0.2778 |

| 7. Firm size | 37 | 6.0943 | 1.5247 | 4.3175 | 11.4700 |

| Variable | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

|---|---|---|---|---|---|---|---|

| 1. ROA | 1 | ||||||

| 2. Patents | 0.2373 | 1 | |||||

| 3. Self citation | 0.3906 | 0.2681 | 1 | ||||

| 4. Other citation | 0.0130 | −0.0513 | 0.1064 | 1 | |||

| 5. Firm age | 0.0064 | 0.3678 | −0.1364 | −0.0569 | 1 | ||

| 6. R&D expenditure | −0.4951 | −0.009 | −0.1252 | −0.1939 | −0.1823 | 1 | |

| 7. Firm size | 0.2268 | 0.5669 | −0.0125 | −0.0881 | 0.4365 | 0.0077 | 1 |

| Model | Model | Model | Model | Model | |

|---|---|---|---|---|---|

| VARIABLES | 1 | 2 | 3 | 4 | 5 |

| Independent variables | |||||

| Patents | 0.00179 * | 0.000587 | |||

| (0.000902) | (0.00108) | ||||

| Self citation | 0.0751 ** | 0.0720 * | |||

| (0.0344) | (0.0396) | ||||

| Other citation | −0.00858 | −0.0110 | |||

| (0.0194) | (0.0179) | ||||

| Control variables | |||||

| Firm age | −0.00125 ** | −0.00141 ** | −0.000928 | −0.00128 ** | −0.00103 |

| (0.000602) | (0.000574) | (0.000587) | (0.000612) | (0.000616) | |

| R&D expenditure | −0.998 *** | −1.003 *** | −0.906 *** | −1.028 *** | −0.950 *** |

| (0.152) | (0.153) | (0.163) | (0.172) | (0.183) | |

| Firm size | 0.0194 ** | 0.0137 | 0.0180 ** | 0.0191 ** | 0.0159 |

| (0.00777) | (0.00990) | (0.00770) | (0.00783) | (0.00996) | |

| Constant | −0.0123 | 0.0175 | −0.0334 | −0.0000937 | −0.00709 |

| (0.0511) | (0.0589) | (0.0468) | (0.0532) | (0.0596) | |

| Observations | 37 | 37 | 37 | 37 | 37 |

| R-squared | 0.342 | 0.368 | 0.433 | 0.348 | 0.446 |

| Model | Model | Model | Model | Model | |

|---|---|---|---|---|---|

| VARIABLES | 1 | 2 | 3 | 4 | 5 |

| Independent variables | |||||

| Patents | 0.00130 | 0.00117 | |||

| (0.000908) | (0.00118) | ||||

| Self citation | 0.0147 | 0.00932 | |||

| (0.0171) | (0.0194) | ||||

| Other citation | 0.0107 | 0.0117 | |||

| (0.0116) | (0.0113) | ||||

| Control variables | |||||

| Firm age | −0.000928 | −0.00104 | −0.000785 | −0.00107 | −0.00110 |

| (0.000939) | (0.000994) | (0.000960) | (0.000991) | (0.00108) | |

| R&D expenditure | −0.0790 | −0.0793 | −0.0459 | −0.0625 | −0.0403 |

| (0.158) | (0.173) | (0.157) | (0.155) | (0.178) | |

| Firm size | 0.0162 * | 0.0119 | 0.0159 * | 0.0175 * | 0.0136 |

| (0.00798) | (0.00751) | (0.00784) | (0.00894) | (0.00860) | |

| Constant | −0.0243 | −0.00157 | −0.0344 | −0.0467 | −0.0347 |

| (0.0437) | (0.0448) | (0.0429) | (0.0542) | (0.0596) | |

| Observations | 37 | 37 | 37 | 37 | 37 |

| R-squared | 0.133 | 0.161 | 0.154 | 0.159 | 0.199 |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cho, Y. The Effects of Knowledge Assets and Path Dependence in Innovations on Firm Value in the Korean Semiconductor Industry. Sustainability 2020, 12, 2319. https://doi.org/10.3390/su12062319

Cho Y. The Effects of Knowledge Assets and Path Dependence in Innovations on Firm Value in the Korean Semiconductor Industry. Sustainability. 2020; 12(6):2319. https://doi.org/10.3390/su12062319

Chicago/Turabian StyleCho, Yoonkyo. 2020. "The Effects of Knowledge Assets and Path Dependence in Innovations on Firm Value in the Korean Semiconductor Industry" Sustainability 12, no. 6: 2319. https://doi.org/10.3390/su12062319

APA StyleCho, Y. (2020). The Effects of Knowledge Assets and Path Dependence in Innovations on Firm Value in the Korean Semiconductor Industry. Sustainability, 12(6), 2319. https://doi.org/10.3390/su12062319