1. Introduction

Maritime transport is, by far, the most cost-effective way to move goods around the world, and despite a slight decline in 2018, it remains the backbone of international trade: More than four-fifths of global trade by volume is carried by sea [

1]. Though shipping is widely known for its overall environmentally friendly performance compared to road and air transport, it remains characterized by several undesirable environmental impacts. Particularly, shipping emissions are coming under increasing attention and scrutiny as a result of growing awareness on climate change and environmental issues. Shipping emits various pollutants, causing a range of issues:

Carbon dioxide (CO2) is the most significant greenhouse gas (GHG) released by ships. The emission of GHGs is the main reason for global warming;

Sulfur oxides (SOx) and nitrogen oxides (NOx) contribute to the formation of acid rain and are highly undesirable, due to their effects on human health;

Carbon monoxide (CO), volatile organic compounds (VOC) and particulate matter (PM) affect human health. PM also includes black carbon (BC), which is not only particularly harmful to humans, but also the second most powerful climate forcer after CO2.

In this study, the focus is on, but not limited to, GHG emissions.

International shipping is considered one of the largest GHG emitting sectors of the global economy, and it is also expected to become one of the fastest-growing sectors concerning GHGs [

2]. In 2014, the Third GHG Study by the International Maritime Organization (IMO) estimated that international shipping accounts for around 2.2% of global annual CO

2 emissions and that emissions from international shipping could grow between 50% and 250% by 2050 mainly due to the growth of the world trade [

3]. Moreover, IMO predictions for 2050 foresee that 15% of total CO

2 emissions will be attributable to maritime transport. Further estimates of 2019 foresee a 39% demand growth for seaborne trade by 2050. Particularly, the deep-sea segment is estimated to account for more than 80% of world fleet CO

2 emissions, thus making clear that it is particularly important to find technically feasible and cost-effective emission reduction solutions for this segment [

4]. In May 2019, IMO’s Marine Environment Protection Committee (MEPC) announced the start of work for the Fourth IMO GHG Study, which will include, among other things, an inventory of global emissions of GHG emissions from international shipping from 2012 to 2018 and scenarios for future international shipping emissions in the period 2018–2050. The final report of the study is expected for Autumn 2020.

With the adoption of the Paris Agreement in December 2015 [

5], 195 countries agreed to keep a global temperature rise this century well below 2 °C above pre-industrial levels and to pursue efforts to limit the temperature increase even further to 1.5 °C. Though shipping has not yet been included in any international climate agreement, it is called upon to make its fair contribution to global commitments on climate change by reducing its emissions. The IMO, as the body responsible for regulating maritime emissions, is expected to lead this process. Following years of internal debate on how and whether the shipping sector should align with the goals of the Paris Agreement, the IMO has finally developed a challenging roadmap for the decarbonization of the sector. A cornerstone of this roadmap is the adoption, in 2018, of the Initial IMO Strategy to achieve reductions in GHG emissions from shipping. With 2008 as a baseline year, the Strategy aims to at least halve total GHG emissions from shipping by 2050, and to reduce the average carbon intensity (CO

2 per ton-mile) by a minimum 40% by 2030, and 70% before mid-century [

6]. The Strategy represents the IMO’s initial contribution to the global goals of the Paris Agreement to respond to climate change.

To meet internationally agreed levels of mitigation, the shipping industry must undertake fundamental changes in its emissions pathway. Policymakers and stakeholders are called to make substantial efforts to find and implement solutions aimed at reducing the carbon footprint of shipping activities. The increasing interest in the environmental impact of shipping is also demonstrated by the growing attention the corresponding transport environmental literature is devoting to measures, policies, and initiatives aimed at mitigating it [

7]. Several recent literature reviews with a focus on sustainability measures across the maritime industry are available. The study by Reference [

8] uses bibliometric tools to offer a systemic mapping of the literature with some sustainability focus in the field of maritime transport published between 1975 and 2014. More recently, the paper by Reference [

9] has proposed a literature review on sustainability in the field of maritime studies using text-mining techniques to provide future research directions concerning topics and co-authorship patterns. Some reviews are more focused on a specific problem, such as bunker consumption optimization methods [

10], while others provide general overviews of emissions reduction measures [

11,

12]. A general overview of the measures with high CO

2 reduction potential can be found in Reference [

13], while a specific focus on emission reduction in the port area is in Reference [

14]. A holistic assessment of the combined potential of fuels, technologies and policies to reduce GHG emissions from international shipping can be found in Reference [

15]. Several quite recent special issues dealing with specific aspects of sustainability in the shipping and port industry are also available [

16,

17,

18,

19], further confirming the strong interest in the topic.

Notwithstanding this significant body of literature, it seems that the complex issue of decarbonizing the maritime industry would benefit from an overall summary framework designed to configure the key elements that are going to characterize the low-carbon transition, both for the industry and research agenda. Two different, but interconnected, perspectives should be considered when dealing with the decarbonization process of the shipping industry: The perspective of the policymakers, which focus on achieving the established decarbonization targets; and the perspective of the ship-owners and maritime operators, which are requested to face in the short-term decisions that will surely have long-term implications on their business. The 50% emission reduction target set by the IMO is ambitious and will likely call for widespread uptake of lower and zero-carbon fuels, in addition to other energy efficiency measures, including operational and market ones. In an attempt to contribute increasing the general understanding of the decarbonization challenge for the shipping industry, this paper provides a critical overview of the main measures available for cutting down shipping emissions and discusses the main organizational, technical, economic and political challenges and barriers to implementation along with the potential facilitators that could foster a wider application. The framework that is outlined is complex and brings to light some important controversies related to shipping’s decarbonization that exist in both the scientific and business communities.

The remainder of this paper is structured in eight sections. Following this introduction,

Section 2 introduces five research questions and outlines the methodology used to give them an answer.

Section 3 focuses on the identified drivers for the adoption of low-carbon practices, while

Section 4 discusses the main measures and initiatives available to the shipping industry to comply with the new decarbonization and desulfurization targets set by the IMO. The main challenges and barriers to implementation are discussed in

Section 5, while some considerations about the technical possibility to achieve the ambitious IMO’s GHG targets by 2050 are in

Section 6.

Section 7 discusses the potential enablers that could facilitate a quicker and successful low-carbon transition for the shipping industry. Finally,

Section 8 summarizes the major findings of the study and points out the potential role of research as a facilitator of the decarbonization process.

2. The Research Approach

This study aims to provide a critical overview of the main measures the shipping industry can apply to reduce its emissions. The overview tries to highlight the strengths and weaknesses of the most popular emission reduction options with reference to the potential contribution they can make to achieving the IMO’s targets. The specific aspects of interest have been formulated into five research questions (RQ):

RQ 1: What are the main drivers that are pushing the shipping industry to undertake major efforts to contain its emissions?

RQ 2: What are the pros and cons of the most popular emission reduction measures the shipping industry can adopt to try to cope with the new IMO’s requirements?

RQ 3: What are the main challenges and barriers to implementing decarbonization measures?

RQ 4: Is there an objective way to assess the technical possibility to achieve the ambitious IMO’s GHG targets?

RQ 5: Towards the IMO’s goals, who are the potential facilitators that could foster a wider and quicker decarbonization process of the shipping industry?

The overview has been built by following the triangulation research approach. In qualitative research, the triangulation approach refers typically to the use of multiple and diverse data sources to develop a comprehensive understanding of complex phenomena. In order to build an overall framework of the complex issue of shipping’s decarbonization that considers the different dimensions and perspectives of the phenomenon, this research has been developed on two fronts:

In a preliminary phase of the study, purely numerical research was carried out using the Scopus database to get a view of the quantitative impact (in terms of the number of works published) the issue of decarbonization, and more generally of the environmental sustainability of shipping, has had in the last decades on the scientific literature. Scopus was chosen as one of the leading research databases, including about 20,000 journals with a focus on physical sciences, health sciences, life sciences, social sciences and humanities. The search on Scopus aimed at identifying maritime-related papers which contained in the title the following keywords:

IMO + strategy/GHG/Greenhouse;

GHG + shipping/maritime/port(s)/ship(s);

Decarbonization/decarbonize + shipping/maritime/port(s);

Low carbon + shipping/maritime/port(s);

Emission(s) + shipping/maritime/port(s)/ship(s);

Green + shipping/maritime/port(s)/ship(s);

Sustainable/sustainability + shipping/maritime/port(s)/ship(s);

Emission Control Areas (ECAs).

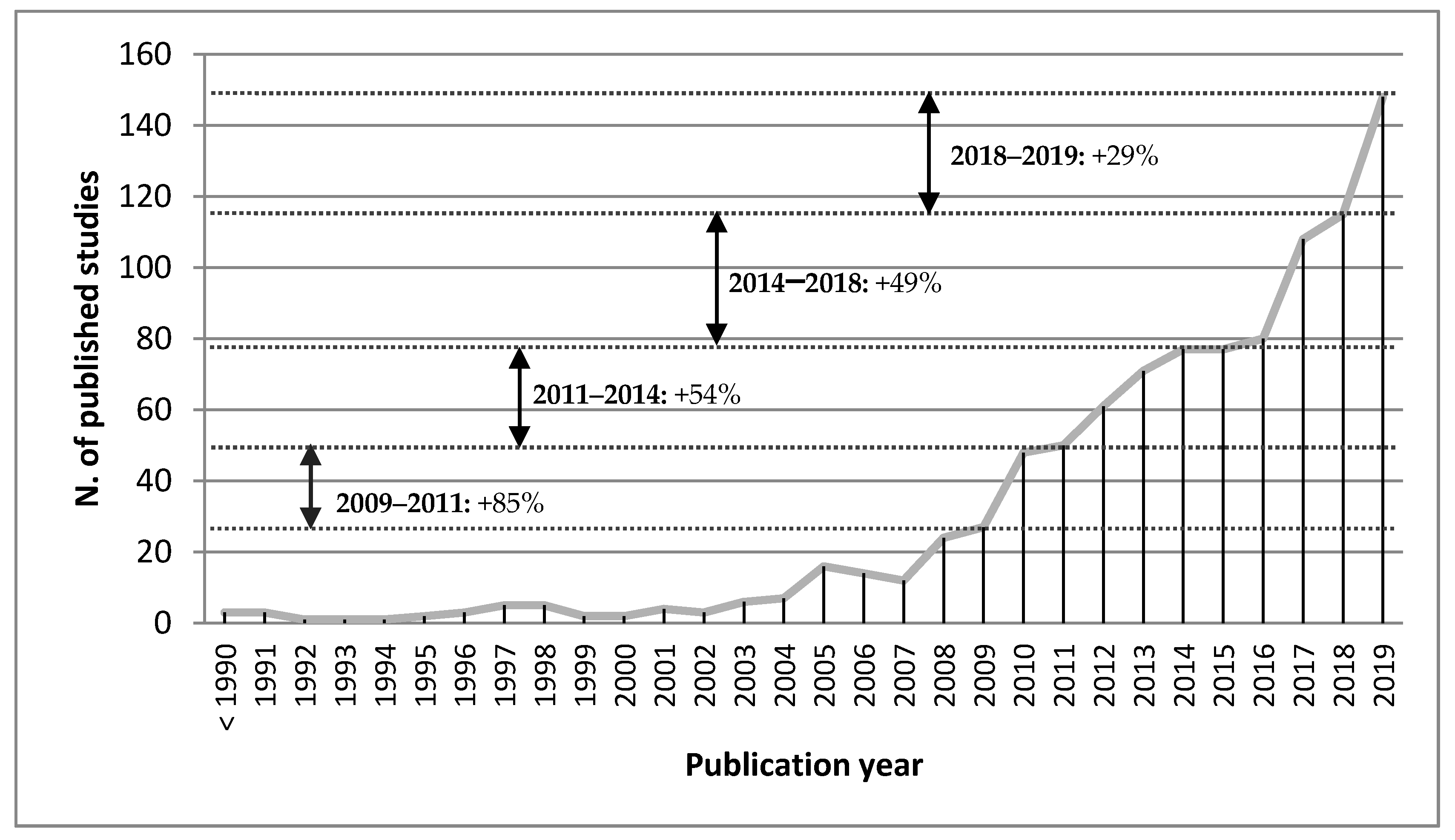

The keyword search was performed in October 2019, and updated in March 2020 to include the studies published in 2019. The search covered the 30 years from 1990 to 2019 resulting in 958 works, including journal articles, conference papers, books and book chapters. This general search is not meant to be complete or all-encompassing, as there may be several studies that the search by keywords in the title has not captured and not all journals and studies appear in the Scopus database. Nevertheless, it offers a quantitative indication of the rise of papers covering sustainability issues in the field of shipping and port industry. Looking at the distribution of the studies concerning the year of publication (

Figure 1), the trend shows a significant increase in the number of papers published starting in 2009 (840 out of 958 studies were published after 2009). Although the environmental issue first emerged in the early sixties, it is especially in the last decade that it has imposed itself with greater force on the attention of institutions and the conscience of public opinion. Particularly, looking at the graph, it seems possible to identify four main growth stages in the annual number of published studies: 2009–2011 (+85%), 2011–2014 (+54%), 2014–2018 (+49%) and 2018–2019 (+29% in just one year).

The start dates of the four phases do not seem random as they coincide with four milestones of the IMO regulation:

2009—publication of the Second GHG Study of the IMO [

20];

2011—mandatory measures to enhance energy efficiency for international shipping adopted by Parties to MARPOL Annexe VI [

21];

2014—publication of the Third GHG Study of the IMO [

3];

2016—setting of the limit for sulfur in fuel oil used onboard ships of 0.50% (mass by mass) from 1 January 2020 [

22];

2018—Initial IMO Strategy on reduction of GHG emissions from ships [

6].

These and other regulatory aspects will be discussed in depth in

Section 3.

Regarding the geographical origin of the studies analyzed, the largest number of them are related to China and the US. This is not surprising considering that the two countries are considered the two biggest emitters in the world and the need for emission reductions is acute for both [

18]. The top 20 countries by the number of studies are listed in

Table 1.

To answer the five RQs by capturing the most recent research developments, the analysis has focused on studies published after the Second IMO GHG Study (2009). The studies published as of 2009 and identified through the keyword search were preliminarily filtered by reading the titles and abstracts to understand if they could fall within the scope of the analysis. Only those deemed more adherent to the purpose were reviewed more in detail, giving priority to the most recent ones. Sixty-seven studies were selected through this process. In addition, 51 academic works that were not captured by the keyword search but considered relevant for the analysis were identified through the authors’ personal knowledge, suggestions from the editor, anonymous reviewers, and by identifying additional key publications from the reference lists of the papers already selected. In total, the review of the academic literature converged on 118 studies whose contents are used in this paper to answer the five RQs. Moreover, to offer an up-to-date framework of the context of decarbonization in shipping, the literature review was completed with the study of technical reports and bulletins of trusted sector experts. This was necessary to capture the latest developments in the sector and to include in the analysis of the contemporary factors that nowadays may influence operators’ priorities and actions.

3. RQ1: What Are the Main Drivers that Are Pushing the Shipping Industry to Undertake Major Efforts to Contain Its Emissions?

In the age of climate change and sustainable development, shipping has been forced to become more environmentally friendly by increasingly stricter regulation and external pressures which are directly derived from environmental concerns. Furthermore, considering that fuel is by far the single largest cost to the sector, there can also be clear economic incentives to improve energy efficiency in shipping and invest in cleaner technology. Although the reasons behind implementing emission reduction measures may be manifold, it seems possible to identify at least three crucial factors that push shipping to lower its environmental impact:

Regulatory and institutional pressures;

Market factors and resource availability issues;

Social pressures and ecological awareness and responsiveness.

The order follows somehow the importance they play in the operators’ choice.

3.1. Regulatory and Institutional Pressures

To meet internationally agreed levels of mitigation, the shipping industry has to play its part in reducing its carbon emissions, and to do so, it must undertake fundamental changes in its emissions pathway [

23]. The regulatory preserve of international shipping resides mainly with the IMO, which is the United Nations specialized agency responsible for the prevention of marine pollution by ships and the safety and security of shipping activities. The IMO has traditionally addressed the environmental impact of maritime activities by introducing international conventions and laws to regulate them. In 1997, it was designated by the UNFCCC (United Nations Framework Conference on Climate Change) as the body responsible for regulating maritime emissions. The main measure implemented by the IMO is the International Convention for the Prevention of Pollution from Ships (MARPOL), which came into force in 1983 intending to prevent and minimize pollution caused by ships for both operational and accidental reasons. The MARPOL convention includes six technical Annexes, of which Annexe VI, regulates air pollution generated by ships [

21]. Specifically, Annexe VI establishes the limits of SO

x, NO

x and PM global emissions and introduces Emission Control Areas (ECAs) in which more stringent emission policies apply. Annexe VI seeks a progressive reduction of sulfur content in marine fuel oils to achieve the target value of 0.5% by weight by 2020 [

22]; it also includes progressively restrictive policies regarding NO

x applicable only to ships built after January 2016. IMO established also certain SO

2 Emission Control Areas (SECAs) in which the sulfur limit is 0.01 since 2015 (Baltic Sea, North Sea, North American, United States Caribbean Sea). Furthermore, in January 2019, amendments to MARPOL Annexe VI designate the North Sea and the Baltic Sea as ECAs for NO

X, both will take effect on 1 January 2021.

At the European level, the European Union (EU) has adopted directives for the abatement of shipping emissions which further limit the maximum sulfur content in marine fuels to 0.1% by weight for ships at berth in several EU ports [

24]. Member States are also required to build liquefied natural gas (LNG) refueling points in all ports and install infrastructures for shore-side electricity by the end of 2025 [

25].

In April 2018, the IMO agreed on the Initial IMO Strategy to reduce GHG emissions in the shipping sector to meet the Paris Agreement goals [

6]. Though the Strategy suggests an indicative framework of measures to be implemented in the short- (2018–2023), medium- (2023–2030) and long-term (after 2030), a final plan is not expected until 2023. The Strategy includes a target to “

reduce the total annual GHG emissions by at least 50 per cent by 2050 from 2008 levels whilst pursuing efforts towards phasing them out”. This suggests the IMO will probably implement further and more stringent emissions regulations in the years to come.

Being able to meet the ambitious decarbonization and desulfurization IMO’s targets is probably the major challenge the maritime industry has to face in decades.

3.2. Market Factors and Resource Availability Issues

Market factors have traditionally been the main drivers of innovation in shipping. In particular, the constant fluctuation of fuel prices, due to market forces and the cost of crude oil, has always led to explore alternative energy options or operational practices, such as slow steaming. The global consumption of ship fuel today is estimated in around 400 million tons of oil equivalent [

26]. The crucial role assumed by financial aspects becomes evident when considering that energy costs represent on average between 50% and 70% of operating costs of a vessel [

27]. This percentage is expected to increase further as heavy fuel oil costs increase, making attractive the adoption of alternative fuels.

As for fuel availability and related costs, precise information concerning the location and amount of global fuel reserves are difficult to obtain, and the available estimates are often controversial or difficult to verify [

28]. Moreover, the political instability of several regions holding important oil reserves raises important concerns about security and availability of fuel resources leading several countries to explore and invest in the development of alternative fuels. Diversification of energy alternatives seems to be the key in the future of shipping.

3.3. Social Pressures and Ecological Awareness (Be Green)

The environmental and climate issue is every day in the spotlight and the agendas of governments all over the world. Pressures to adopt “greener” behavior constantly come from various stakeholders, including institutions, customers, citizens, investors and others. In the shipping industry, customers’ and investors’ demands may be strong drivers for the adoption of more environmentally friendly practices as companies need their approval and legitimacy to stay in business [

29,

30]. The study by Reference [

31] stresses that actors in a maritime supply chain should adhere to customers’ expectations and identifies four main customer requirements, including competitive costs, pollution reduction, efficient use of fuel, and health and safety. Nowadays, it is particularly evident how citizen groups, NGOs and other environmental organizations can also influence this change through local activism. By disregarding from what is socially accepted, a company risks losing customers, and thus profits. It is not a case if an ever-increasing number of shipping companies and port operators are progressively investing in communication campaigns and initiatives aimed at promoting their green image to increase their environmental legitimacy. It can also happen that the threat of strictest regulatory actions can become a driving factor for operators to be proactive by taking pre-emptive green moves aimed at increasing their advantage to competitors [

29]. A proactive environmental strategy that exceeds regulations is also believed to produce some benefits in terms of recognition from communities and institutions [

32]. Sometimes, although not frequently, it can also happen that the implementation of energy efficiency measures is directly influenced by the company’s environmental values and moral commitments to adopt “greener” measures [

33].

4. RQ 2: What Are the Pros and Cons of the Most Popular Emission Reduction Measures the Shipping Industry Can Adopt to Try to Cope with the New IMO’s Requirements?

Achieving the sustainability targets defined by the IMO is not straightforward and depends on the widespread adoption of low-carbon technologies and measures. To comply with new regulations, the world of shipping must implement fundamentals changes in fuels, technologies, operations and business practices. In order to discuss the main measures that the shipping industry can undertake to reduce its environmental footprint, this paper uses a scholarly classification based on the following four groups and related sub-groups:

The focus of the analysis is on the decarbonization measures that can contribute to reaching the IMO’s GHG targets, but there are also some insights on the desulfurization options necessary to cope with the IMO 2020 sulfur cap.

4.1. Technological Measures

Emissions from the shipping industry are strongly related to fuel consumption. Around 95% of the global fleet is reported to run on diesel, usually referred to as bunker oil [

17]. Bunker oil is not only much cheaper than that used in road transport, but it is also much lower quality. Bunker oil results in high emissions per power output, even when the most modern marine engines are used. The stringent regulations under MARPOL are main drivers to explore the adoption of alternative measures to comply with IMO’s desulfurization requirements. In October 2019, the IMO clarified that ships would be liable for any non-compliance with IMO sulfur regulation [

34]. Currently, ship-owners and maritime operators seem to have four main technological options to comply with the new IMO desulfurization and decarbonization requirements:

A description of the four options is provided below.

4.1.1. Change the Fuel Quality by Using Low-Sulfur Fuel Oil

It is the simplest way to comply with the new IMO 2020 requirements on marine fuels. Ships can use low-sulfur fuel oil, such as marine gas oil (MGO), instead of heavy fuel oil (HFO). According to several projections built on a market consensus that many ship-owners will switch to MGO to comply with the IMO’s 0.5% sulfur limit, a gas oil supply shortfall of 500,000 barrels per day might emerge unless refineries increase their crude runs by 1.1 m bpd [

35]. As expected, the price of compliant low-sulfur fuels skyrocketed in the first week of January 2020, immediately after the IMO 2020 sulfur cap came into force. According to CME Group, in early January 2020, the average spread between high-sulfur and low-sulfur fuel prices reached

$234/MT [

36]. Since then, after the first days of sharp rise, low-sulfur fuel prices have come down, and the spread has had a fluctuating trend. From January 2020, extraordinary uncertainty has come to the market as a result of the coronavirus epidemic and its negative impact on shipping and global crude oil demand. To date, it is impossible to predict what the effects of this disruption will be in the medium and long-term.

4.1.2. Switch to Alternative Fuel Options

To meet the new IMO’s decarbonization and desulfurization targets a large-scale use of carbon-neutral fuels and/or exhaust gas abatement equipment will be required. Potential alternatives to conventional marine fuels are diverse and identifying the preferable one is not easy [

37]. This section provides an overview of the most famous or promising alternatives.

Renewable energy. Wind and solar energy may have some potential to reduce carbon emissions and are useful to supplement existing power generating systems. The potential CO

2 reduction for solar energy generation onboard is reported to be between 0.2 and 12%, while wind-solar hybrid systems may achieve up to 40% of fuel savings [

13]. Despite their GHG reduction potential, they are not yet considered as a viable alternative for commercial shipping [

38], and it is shared the opinion that the shift from fossil fuels to renewable ones is still far from being achieved [

28].

An interesting emerging trend in the modern maritime industry is the use of large kites to increase propulsion efficiency in navigation, while reducing fuel consumption and related emissions. Especially in the high sea, where winds are generally more powerful, kites can allow significant fuel savings, while maintaining full speed [

39]. This solution has some potential for saving fuel and is characterized by very low installation costs.

Electrification, batteries, fuel cells and hydrogen with fuel cells. Electrification has been gaining strong interest in maritime shipping as it improves energy management onboard and reducing emissions in port areas [

40,

41]. Electrification opportunities are exploited both to produce energy to power berthing ships (cold ironing) and to charge batteries for full-electric or hybrid ships [

42,

43,

44]. The power system of full-electric ships is based on batteries charged from the onshore grid while at berth, whereas battery hybrid ships do not bunker electricity from shore but use batteries to improve the energy efficiency. Several degrees of hybridization using batteries can be realized between a full-electric system and a traditional system. Hybrid solutions are believed to have significant potential for energy efficiency and are suitable for applications on different types of ships. More than 320 hybrid ships were reported in operation or on order in 2019, and it is expected that almost every newbuild ship will use batteries in the short-term [

4]. In the next years, the cost-effectiveness of electric propulsion ships will depend largely by battery costs and technology [

45]. As for most alternative energy sources, the technical and commercial applicability of the electric option will vary extremely for deep-sea and short-sea shipping. The full-electric operation seems currently relevant only for the short-sea shipping segment where the shorter distances can make electric or hybrid propulsion systems more efficient than traditional ones. Conversely, deep-sea shipping looks unlikely to use a significant level of onshore power shortly but can already install batteries for energy optimization [

4]. The potential of electrification to reduce GHG emissions depends heavily on the source of electricity. According to DNV GL forecast, 30% of all global electricity production will come from wind energy by 2050—12% from offshore wind and 18% from onshore wind. Today’s levels are 0.2% and 4.1%, respectively, of global electricity production [

46].

Fuel cells can efficiently produce electricity by using the chemical energy of hydrogen or another fuel and are more efficient than traditional reciprocating engines, since their fuel to electricity conversion efficiency can reach up to 60%, instead of 40% of conventional engines [

47,

48]. Hydrogen is the most promising option to power fuel cells on board. However, its use as fuel raises several challenges concerning not only its production, transport, storage and related costs, but also important safety concerns [

49]. It is a shared opinion that much work must be done before hydrogen can be considered a competitive alternative to traditional fossil fuels. An overview of different fuel cell technologies with possible application to shipping is provided in the report commissioned by the European Maritime Safety Agency—EMSA [

50]. The report recognizes that fuel cell technology is still a diminutive business on a global scale, and several hurdles must be overcome before it can become a viable and realistic alternative for future energy solutions.

Biofuels (biodiesel, liquefied biogas, etc.). They have the potential to contribute to reducing GHG emissions and the advantage to be rapidly biodegradable. Biofuels are flexible fuel alternatives as they can be blended with conventional fuels or used as drop-in fuels in existing installations without requiring significant technical modifications. While several demonstration projects have been testing the technical feasibility of various biofuels [

51], the main challenge for their adoption on a large scale concerns the possibility to secure the necessary production volume [

38]. There are also some skeptical opinions about their GHG reduction potential. Several studies state that biofuels may have the potential for air pollution during cultivation and are not fully carbon-neutral, due to the sacrifice of forests required for their production [

15].

Liquefied Natural Gas (LNG). There is a large interest in the use of LNG as a marine fuel. In regards to conventional marine fuels, LNG reduces CO

2 emissions by around 20–30% (even compared to low-sulfur fuels), the almost complete removal of SO

x and PM emissions and a reduction of NO

x emission of up to 85%, while emissions of CO

2 -equivalents do not necessarily favor LNG [

14,

52]. For example, the fugitive emission of methane during bunkering can bring down its environmental potential [

53].

LNG is commercially attractive and available worldwide in quantities able to meet the fuel demand of shipping in the coming decades. The number of ships using LNG as fuel is growing rapidly. By the end of 2018, the global LNG fleet totaled 525 LNG-burning vessels in operation, including LNG carriers and floating storage units [

54]. According to ship certification experts, in 2018, there were 125 merchant ships around the world using LNG as a fuel, with between 400 and 600 expected to be delivered by 2020. Some of the world’s largest container shipping companies already own or are reported to have ordered mega container vessels powered by LNG [

26]. In 2019, the world’s largest cruise company welcomed the first LNG-powered cruise ship to the fleet. Further estimates foresee that around 1,000 non-LNG carrier vessels running on LNG will be reached in 2020 or shortly thereafter, even if this is still a small part of a commercial world fleet of more than 60,000 vessels [

28].

Research into the application of LNG as a ship fuel has seen strong growth in the past 15 years. A systematic review of the studies published since 2003 on the use of LNG as a ship fuel can be found in Reference [

55]. In this review, the authors analyze 33 studies by identifying several crucial barriers to the widespread adoption of LNG as a ship fuel. On the one hand, the lack of bunkering facilities and international standards are recognized as important barriers for the faster deployment of LNG as a ship fuel; whereas, on the other hand, its widespread application is supported by the competitive environment (LNG supply chains are already in place, and alternative fuel options are expected to face greater obstacles) and the abundant global natural gas reserves. Furthermore, LNG is currently the only green fuel that is scalable commercially and globally for the deep-sea segment. According to some forecasters, LNG bunker annual demand from the shipping sector is expected to be between 20 to 30 million tons by 2030, while today it is estimated in less than one million tons per annum. It should be noted that the adoption of LNG on a large scale may happen as a consequence of some drivers, including an increase in the price of conventional fuels and development of the necessary bunkering facilities at a global level [

56]. It is reported that the EU has already invested over

$500 million USD for marine bunkering LNG projects and many European ports are investing heavily to offer upgraded LNG refueling points for ships as a result of the adoption of the EU Directive 2014/94/EU [

57].

In contrast to these factors of growth of LNG as a marine fuel, there are now more than a few skeptical opinions about its actual GHG reduction value as a replacement of conventional fuels. Several studies agree that, concerning the CO

2 reduction required by the IMO’s 2050 objectives, there does not seem to be significant CO

2-equivalent reduction achievable using LNG [

58]. The life cycle assessment of LNG as a marine fuel shows an impact on climate change of the same order of magnitude as with the use of HFO [

37], if not higher [

53]. Furthermore, depending on the fuel’s supply chain used, a switch to LNG can even increase GHG emissions related to conventional fuels [

56].

Methanol. Methanol is in an earlier stage of market introduction, but some large-scale tests have already been implemented [

4]. It is easier to store and distribute than LNG because it is liquid at room temperature. It can be mainly used in dual-fuel engines and offer several advantages in terms of reductions of NO

x and PM emissions, it is sulfur-free and can be used in compliance with SECAs regulations. Methanol is available in volume today, but due to the limited availability of related global infrastructure and bunkering facilities for shipping, it is not expected it will shortly play a key role as an alternative fuel in the shipping sector [

59,

60].

Ammonia (NH3). Although no marine engine currently on the market is capable of burning ammonia, several studies consider ammonia as a potential shipping fuel [

61,

62]. The use of ammonia as a marine fuel brings several technological challenges, and much work has to be done before NH

3 engines will be ready on the market.

Several researchers and classification societies now agree that halving shipping emissions by 2050 can be possible only with a consistent switch to non-fossil fuel sources [

56]. DNV GL forecasts that, by 2050, only 47% of energy for shipping will derive from oil-based fuels, gas-fuels will account for 32%, and the remaining part will be provided by alternative energy sources, mainly biofuels and electricity [

59]. In 2019, Maersk and Lloyd’s Register published a study that selects alcohol (ethanol/methanol), biomethane and ammonia as the three most promising net-zero fuels on which the shipping industry should focus to have all shipping decarbonized by 2050 [

63].

4.1.3. Invest in Cleaning Equipment

From January 2020, ships that use fuels with a sulfur content higher than 0.5% [

22] can only operate if equipped with Exhaust Gas Cleaning Systems (EGCS). EGCS, also called scrubbers, are desulfurization pieces of equipment that remove the excess pollution from the exhaust gas and then flush it into the sea (open-loop mode). Closed-loop EGCS retain the pollution onboard, but they are feasible only for short-distance travels. Although continuous developments in scrubber technology, ship-owners are reluctant to invest in EGCS, since they are extremely costly (between

$1–5 million USD, per ship), require up to 20 days for installation (yielding consequent revenue losses for out-of-service) and do not actually reduce sulfur, as they mainly transfer it from the atmosphere to the sea. Moreover, several states are reported to have banned the use of open-loop scrubbers within their territorial waters [

64]. In May 2018, DNV GL reported just 817 ships ordered or installed with scrubbers out a global commercial fleet of 60,000 vessels. Moreover, considering that at present IMO is still implementing emissions regulations, there is also the risk that flushing the pollution into the sea will be prohibited soon as additional regulations come into force.

There is now a lively debate on open-loop scrubbers prompted by fears that they clean air emissions at the expense of polluting the sea. In 2014, the study by Reference [

52] evaluated the impact of an open-loop seawater scrubber combined with HFO showing that it does not seem able to significantly reduce the life cycle impact on climate change, while it can reduce the impact on particulate matter. In February 2019, a study investigating the environmental impact of marine scrubbers was submitted to the IMO by a group of MIT researchers. The MIT study raised concerns about this technology, stating that scrubbers may not be as efficient in removing small particulate that is harmful to human health, while they are effective for gaseous sulfur oxides [

65]. Similarly, saying there is scientific evidence for the potential toxicity of water discharges, in 2019, the EU asked the IMO to review its guidelines on scrubbers and take appropriate measures. The EU request heavily disappointed the Clean Shipping Alliance 2020, a group of shipping companies that have invested in scrubbers, which said the EU was creating unnecessary worries. An alternative Japanese study, presented to the IMO only one week before the MIT report, stated that there are no unacceptable effects from the use of open-loop scrubbers [

66]. Such conflicting opinions make clear that research is far from conclusive in this area, and more work is needed to effectively and objectively quantify the effects of scrubbers.

4.1.4. Ship Design-Related Measures

They can include the optimization of hull shape and superstructure, the improvement of propulsion systems or, more in general, the development of energy-efficient designs. The shape of a ship’s hull directly impacts the performance efficiency of the vessel. According to some estimates, the optimization of the hull shape and super-structures can reduce fuel consumption and CO

2 emissions up to 15% for large vessels and design-related measures can potentially reduce ships’ CO

2 emissions by up to 50% [

20]. Nevertheless, this huge potential can be only achieved if ships operate according to design specifications and at a relatively slow speed [

14,

20].

The first mandatory regulatory instrument for GHG emissions reduction has been the Energy Efficiency Design Index (EEDI) adopted by the IMO in 2011. All new ships built from 1 January 2013 onwards and of 400 gross tonnage and above are obliged to indicate an EEDI to comply with minimum mandatory energy efficiency performance levels, increasing over time through different phases (phase 1: 2015–2020; phase 2: 2020–2025; phase 3: 2025–2030). The adoption of the EEDI by IMO’s MEPC marked the end of the non-regulation era for shipping GHGs. The EEDI depends on the installed engine power and the expected power at design speed and gives an estimate of CO

2 emissions per dwt*NM. It is based on sea trials at delivery in which observed values are adjusted to “calm water conditions”. There are now opinions according to which the current sea-trial procedures may not be representative of real conditions at sea, and without adjusting the testing results, the desired reductions will be short on targets [

67]. Several scholars have discussed some potential problems associated with EEDI, such as reduced maneuverability, increased inventory cost, modal shift to land-based modes, etc., [

68]. Particularly, the study by Reference [

69] detects some critical issues in the formulation of the index which, in the quest for EEDI compliance, could involve potential risks in terms of inefficient and less safe design.

Considering that the EEDI affects only newbuild ships, it is expected that most commercial ships would be covered by EEDI only by 2040.

In May 2019, IMO’s MEPC approved amendments to MARPOL Annexe VI, for adoption in 2020, to strengthen the existing EEDI requirements for some categories of new ships, including containerships, gas carriers, general cargo ships and LNG carriers. The enhancement of the EEDI and the development of a Ship Energy Efficiency Management Plan (SEEMP) to reduce the energy consumption of ships are the main measures on which the IMO Initial Strategy focuses on the short-term (2018–2023).

4.2. Operational Measures

They typically concern eco-navigation, i.e., the practice of navigating more economically, and the adoption of slow steaming to reduce fuel consumption and related pollutant emissions. Generally speaking, among the various potential fuel reduction measures, operational measures are easier to adopt as they do not require major investments, are readily implementable and can yield significant benefits in a short time [

70,

71].

4.2.1. Speed Management

It is well established that the relationship between fuel consumption and sailing speed is not linear. Bunker fuel consumption is recognized as being proportional to the third power of the vessel sailing speed so that a small decrease in speed entails a significant reduction in fuel consumption [

72,

73]. Speed reduction can be made through both technological and operational measures. The first concern the construction of ships with reduced installed horsepower, the second the adoption of slow steaming. Some data can help to understand how much the size and design speed of ships have changed over the years:

The first cellular containerships of the 1960s reached up to 33 knots;

The Maersk Triple-E containerships (18,270 TEU) have a design speed of 17.8 knots and emit 50% less CO

2 per container moved than the industry average [

74];

The Maersk Second Generation Triple-E containerships (20,568 TEU) have a design speed of 16 knots;

The OOCL containerships, currently the world’s biggest containerships by carrying capacity (21,413 TEU), have a design speed of 14.6 knots.

Slow steaming refers to the practice of large ships sailing at reduced speed to reduce fuel consumption. This practice spread widely during the 2007 global economic crisis among the main shipping companies to counteract rising fuel costs [

75,

76,

77,

78]. By 2010 almost all global shipping companies made slow steaming a regular practice. In this regard, note that ships are built to operate within a given range of service speed, as such the potential savings related to slow steaming depend on the design speed, and further speed reductions could even damage the engines. Slow steaming helps reduce the amount of CO

2 emissions [

79], whereas it is not always useful to reducing the operating costs unless an optimal voyage speed and a strategic range of voyage speed are used [

80]. Slow steaming can also contribute to reducing the shipping overcapacity, which today is the norm, but it can also have negative side-effects. Especially for short-sea trade, it could cause the shift towards alternative land-based transport alternatives, with a consequent increase of GHG emissions.

Many operators are now reported to focus at the same time on slow steaming and gigantism trend to enjoy the benefits of slow steaming and the economies of ship size. However, some research results seem to suggest that, because of a negative correlation between the two strategies, this is not a good strategy and operators are required to select one of two strategies based on their own strategic goals [

80].

4.2.2. Route Planning and Voyage Optimization

Modern technologies allow predicting the weather and maritime conditions with remarkable accuracy to select the most energy-efficient navigation routes. The practice of voyage optimization is very cost-effective as it allows shipping companies to reduce both their costs and their carbon footprint simply bypassing routes in which the ship may not run as efficiently, due to bad weather conditions. The greatest potential is achievable on long routes [

81], which makes route planning more interesting for deep-sea shipping rather than short-sea shipping.

4.3. Market-Based Measures

Recently, the interest in market-based measures (MBMs) has become strong [

82]. Differently from command-and-control measures, such as legislation, MBMs are based on economic incentives to achieve a more sustainable pollution control [

83]. Generally speaking, MBMs can act in two main ways:

The former can be pursued through the application of emissions price-control or quantity-control approaches. Both measures implement the “

polluter pays” principle and can help internalize the external costs of shipping emissions [

84,

85].

Price-control approaches concern bunker levy schemes, such as the carbon tax or the GHG Fund. Ship-owners and operators pay a fixed levy based on their fuel consumption, and part of this money can be used to finance future projects for CO

2 reduction. Although these types of approaches have a theoretical efficiency in both economic and environmental terms, they also have the potential risk to cause the shift from maritime to higher-carbon transport modes and the risk of carbon leakage [

15]. Furthermore, this type of tax can be easily bypassed by taking fuel onboard from countries where it is not applied [

86]. To avoid competitive distortion, they must be applied globally rather than locally [

87], thus, requiring the intervention of independent external bodies.

Emissions quantity-control approaches, such as cap-and-trade programs or emission trading schemes (ETS), issue a limited number of annual allowances that allow companies to emit a certain amount of CO

2. Once the total cap on emissions is set, companies can trade their unused allowances or can be taxed if they produce higher emissions than their permits allow. The cap should be carefully set: A too cautious cap may lead to skyrocketing prices when the availability of allowances is low on the market, whereas a too generous cap may undermine the original goal of the ETS. The expected emission reduction brought by ETSs can be divided into long-term and short-term effects [

88]. In the long-term, an effective ETS can push the shipping companies to invest more in technological innovation to reduce their CO

2 emissions and save money. In the short-term, the shipping companies may slow down their vessels to reduce fuel consumption, and thus, related emissions and allowances. Although the emission reduction effect of ETS in the short-term is generally taken for granted, some scholars have demonstrated that this is not always true. The implementation of ETS can even increase CO

2 emissions depending on other factors, such as charter rate and bunker price [

88].

At the IMO level, the discussion on the possible adoption of MBMs started in 2010 when an IMO Expert Group was tasked to evaluate 11 MBM proposals submitted by various Member States and organizations. In 2013, after three years of work, the MEPC decided to suspend the work of the Group with nothing done. One of the main obstacles to the progress of the discussion was reported to be the objection raised by developing countries about the compatibility of MBMs with the “Common But Differentiated Responsibilities” (CBDR) principle. Another issue of political disagreement was the way of using the funds raised by the MBM [

69].

The discussion on MBMs resumed in December 2019, when the European Commission presented their Green New Deal (aimed at creating the first continent to reach zero carbon emissions by 2050) [

89]. The Deal includes fifty policies, to be implemented over the next three years, in order to meet ambitious climate goals, and unveils plans to regulate shipping emissions by including the maritime sector in the EU ETS. The EU proposal to include shipping in the ETS was met found strong opposition from the shipping industry, which claimed it may create distortions for efficient trade and hinder the global decarbonization process started by the IMO.

No MBM has been applied on an international level so far, and it seems unlikely it will happen shortly [

90]. However, in the framework of the IMO’s Strategy, the implementation of MBMs seem to be expected in the long-term [

91].

As for incentive mechanisms, they can take several forms: Favorable tax systems, low-interest loans for environmentally friendly interventions, the provision of subsidies, etc. Ports have also recently started implementing initiatives aimed at reducing the amount of maritime in-port emissions from ships [

2,

92], and following a more environmentally caring path [

93]. Port initiatives can include discounts to port fees for ships fulfilling certain environmental criteria or the promotion of effective voluntary programs to improve air quality surrounding port areas. The study by Reference [

29] explores the reasons why a voluntary program for vessels speed reduction at the ports of Los Angeles, and Long Beach succeeded identifying three main determinant factors: social pressures given by community about environmental concerns; regulatory pressures by regulatory threats; economic motivations with financial incentives given by the program. The program included incentive funding to use cleaner fuel in main engines and reduced dockage fees. To receive the incentives operators were required to take part in the VSR program; the participation rate reached 86%.

Several shipping firms have begun to respond to environmental concerns by voluntarily embracing green shipping practices (GSPs) to make their operations “greener”. Examples of such practices include counting the carbon footprint of shipping routes and using alternative transportation equipment to reduce environmental damage in performing shipping activities. So far, the adoption of GSPs by shipping firms is not widespread and very little is known about the motivation behind these environmental management initiatives [

94].

4.4. Management and Logistic Measures

The growing interest among researchers and practitioners to reduce the environmental impact of maritime activities can also be witnessed by the increasing number of studies focusing on optimization models, computerized simulation and decision support systems to support more sustainable maritime activities. The paper by Reference [

95] analyzes more than 50 studies published from 2004 to 2015 in the fields of environmental sustainability, decision support systems and multi-objective optimization in maritime shipping. Most of the available studies propose mathematical models or computerized simulation for optimizing specific maritime operations: Among the others, fleet deployment [

96,

97], berth allocation [

98], scheduling optimization and vessels routing [

99,

100,

101]. A low-level operational problem regarding the optimization of vessel speeds and fleet size in response to ECA regulations is discussed in Reference [

102]. A common objective of these studies is to make maritime and port operations more efficient to reduce related times and costs. A recent study has focused on the investigation of the potential role of network design interventions in helping to mitigate GHG emissions of maritime transport chains demonstrating the extent to which shifting freight flows to an integrated and optimized transport scheme could reduce environmental impacts and help to mitigate the emissions of Mediterranean transport chains [

103].

Structural measures (fleet planning, enhanced logistics, etc.) are believed to have a significant potential to reduce emissions but are difficult to implement [

71,

81], because they typically involve two or more counterparts working together to reduce emissions. It is now recognized that improving sustainability in maritime shipping requires a multi-disciplinary approach [

18], and makes it desirable the adoption of multi-objective optimization. The potential of multi-objective optimization to facilitate informed decision making by shipping operators has been investigated in References [

95,

104] indicating its viability to the modeling and optimization of operational and strategic decisions in sustainable shipping.

4.5. A Few Considerations on the Analyzed Measures

Each measure or action analyzed poses both risks and opportunities, and it seems almost impossible to anticipate which solutions will prove most valid. Furthermore, the overview has brought to light some important disputes or disagreements that exist in both the scientific and business communities related to shipping’s decarbonization. Main controversies seem to concern the actual effectiveness or reduction potential of various emission reduction options, the way they are conceived and applied, their economic impact, etc. Particularly, the main disputes seem to concern four popular measures: speed reduction, EEDI, MBMs, and LNG as a marine fuel.

Speed reduction: Although it is one of the short-term measures identified by the Initial IMO Strategy and there is a broad consensus that it is conducive to reducing emissions, it poses important challenges related to the optimal speed design, commercial considerations for just in time delivery, transparency, competition in the shipping market, safety, etc., [

105,

106]. It is also argued that, despite the achievable emission reductions, a regulated global speed restriction may be unpopular and lead to perverse results [

107]. Furthermore, as slow steaming is already widely adopted, it is believed that its potential for further emission reduction may be very limited [

90].

EEDI: Although it is the main measures on which the Initial IMO Strategy focuses on the short-term for GHG emissions reduction, some critical opinions emerge from the literature regarding its formulation and effectiveness [

67,

69]. Particularly, the EEDI formulation is reported to suffer from deficiencies that, in the quest for EEDI compliance, could involve potential risks in terms of inefficient and less safe design [

68,

69].

Market-based measures: MBMs probably constitute the most debated and controversial measure to reduce GHG emissions. Broadly speaking, those in favor of MBMs argue that measures, such as cap-and-trade programs offer an incentive for companies to invest in cleaner technologies in order to avoid buying increasingly costly allowances and contribute to investments in low-carbon projects [

15]. Opponents argue that, by creating an exchange value for emissions, MBMs could lead to an overproduction of pollutants up to the maximum levels set by the government each year.

According to the literature, it is still controversial whether it is time to consider MBMs, such as carbon levy or cap-and-trade schemes, in furthering the reduction of shipping GHG emissions. To date, the main opposition to the adoption of MBMs has come from developing countries. The main reasons for this opposition regard the form in which MBMs are applied, their economic impact, and lack of the “common but differentiated responsibility” (CBDR) principle. While most developing countries ask for adequately incorporating the CBDR principle into future MBMs, many developed countries assert that only the “no more favorable treatment” (NMFT) principle should be applied [

91]. The debate on applying these principles has been a constant theme into the IMO regulatory process, but it is believed that well-designed mechanisms could potentially address these barriers.

Moreover, the implementation of an ETS, unless it is set globally, raises important controversies regarding the scope of a ship’s emission liability. Some scholars argue that the ship must be charged for its emission during the whole voyage between two ports as long as one of them is within the ETS area [

108]. Others propose a geographical-based approach where the ship only needs to submit the allowances for the CO

2 emitted inside the territorial waters and economic zone of the regulating authorities [

88,

109]. Both approaches pose important challenges: The former may be easily evaded, and countries not included in the ETS can question the legitimacy of the ETS authority to charge the emissions outside its territorial space [

110], the latter requires careful monitoring of emissions.

LNG: The environmental and economic benefits of using LNG as a marine fuel have created, especially in the last decade, much interest in both the business and research community. However, though there are undeniable environmental benefits of using LNG as a fuel for shipping, there are also important controversies associated with its actual decarbonization potential. Multiple studies have shown that the total GHG savings of LNG are reduced by upstream emissions that may arise within the LNG supply chain and during operation. According to several estimates of life-cycle GHG emissions from using LNG as a marine fuel, its global warming potential would be the same of HFO and MGO, or even higher [

15,

37,

111]. LNG appears to be a good option for complying with the IMO’s sulfur cap and currently has large advantages for those ships that operate for the highest proportion of their sailing times within ECAs. However, as it cannot enable the required IMO’s GHG reductions, its role as a marine fuel, it is likely to be only transitory [

56]. In this regard, the economic risks for those who in recent years have been investing heavily in assets for the use of LNG as a marine fuel are potentially catastrophic. The duration of LNG as a marine fuel will depend both on the possibility to achieve the needed returns on the made investments over the period it remains in demand, and on the extent to which non-fossil fuel sources will penetrate in shipping. In scenarios where there is significant penetration of non-fossil fuels to meet the GHG targets from 2030, there seems to be no space for the development of LNG as a marine fuel [

56]. Such a scenario would likely entail the premature obsolescence of LNG assets and consequent negative cashflows for their financiers.

5. RQ3: What Are the Main Challenges and Barriers to Implementing Decarbonization Measures?

Continuous and widespread deployment of emission reduction measures is reported not to happen at the required speed [

13]. The reasons for this slow implementation can be different—and may concern obstacles relating to both the complex combination of factors that characterize the decision-making process in the shipping industry and the maturity of the measures. For example, measures that may first appear very promising in practice could need to overcome a number of barriers to fully exploit their emission reduction potential on a large scale [

112].

Moreover, several surveys have shown that although some reduction measures may seem cost-effective, their level of implementation remains low and what can be called an “

efficiency gap” exists between the actual level of implementation and the higher level which would be expected based on techno-economic analysis [

27,

113]. Cost considerations, which typically represent the main part of the decision process, are thus not the only elements at stake and additional technical, operational and market factors must necessarily be considered. Fragmented and diverse ambitions of stakeholders in the sector are reported to further contributing to slowing-down the implementation process of emission reduction [

114].

References [

33] and [

115] categorize barriers to energy efficiency into three broad categories: economic, organizational, and behavioral. By extending and further expanding the existing classifications, this section discusses the main implementation barriers and obstacles to wide diffusion and adoption of emission reduction measures for a transition toward a lower-carbon (and lower-sulfur) shipping industry.

5.1. Economic Barriers

According to industry experts estimates, the new IMO regulations will cost the shipping industry about

$60 billion USD per annum [

116]. MGO is currently around 60% more expensive than conventional HFO [

117]. Considering that bunker costs represent around 47% of the vessel’s operating costs [

77], IMO regulations will yield significantly higher costs for the shipping industry. This higher cost will result in an increase in transportation rates estimated at 10% per TEU for customers and the question regarding who will bear these higher costs is not small [

118]. However, the cost of fuel is not the only significant cost—there are also capital and operating costs to be considered when evaluating alternative energy options.

Restricted access to the capital market is widely recognized as a barrier to investing in emission reduction solutions [

27]. Most shipping companies are relatively small and with limited resources to invest in scrubbers or retrofitting and the payback time of the various alternatives is a crucial factor in the decision-making of ship-owners [

52]. Furthermore, ships have a second-hand value that does not reflect investments in energy efficiency equipment [

12]. Scrubbers appear to be a more attractive option for new builds compared to retrofits, and old ships seem not suitable for scrubber installations when their remaining lifespan is less than four years [

119].

For those interested in using LNG as a marine fuel, the transition to LNG not only needs relevant investments to build the required refueling points, but it also involves the purchase of new powered LNG ships that on average cost 10%–30% more than equivalent diesel-fueled ships conventional ships [

59]. Retrofitting can also be extremely expensive, as it requires much space to install bigger fuel tanks [

120]. The cost of converting conventional engines so they can be fueled with methanol is estimated to be lower [

121].

Full-electric solutions are also unlikely to pay back investments alone. Although battery costs are reported to be in sharp decline [

45], their installation and replacement cost (an expected lifetime of 10 years is currently the marine industry standard) is significantly higher than for traditional engines [

4]. Moreover, investments in essential shore-based charging facilities are far from negligible. The study by Reference [

41] has investigated the economic feasibility of shore side facilities investment in ports founding that the overall investment can be economically viable only when the port could make a net profit by selling electricity. A multi-objective model for strategic planning regarding whether and when to retrofit ships to use shore side electricity has been provided by Reference [

122].

Likewise, fuel-cell powered ships are currently much more expensive than comparable diesel ships. Capital costs for a newbuild fuel-cell powered ship are estimated to be 1.5 to 3.5 times higher than a comparable diesel vessel while operating costs are up to eight times higher [

123].

A financial evaluation of alternative approaches to the abatement of NO

x and SO

x emissions can be found in Reference [

124]. The study considers a sample of real ships that operate within the ECA of Northern Europe and accounts for revenue that might be generated from emissions trading within a cap-and-trade market. The use of LNG is found to be the most financially attractive measure for reducing SO

x emissions; alternative distillates do not appear to be an economical solution to meeting regulatory requirements, while scrubbers and selective catalytic reduction systems can constitute financially attractive abatement options.

5.2. Technological Barriers

Alternative energy options are not available in large quantities today, and LNG seems currently the only green fuel that is scalable commercially and globally for the deep-sea segment in the short-term. However, and despite its benefits for reducing SO

x emissions, numerous scholars agree that, as it cannot enable the required IMO’s GHG reductions, its role as a marine fuel will be only transitory. Over the period it will remain in demand, the main limitation to the shift from conventional fuels to LNG is identified in the lack of availability of bunkering facilities at ports. This barrier is a typical “

chicken-and-egg” problem: On the one hand, bunker suppliers are unwilling to invest in bunkering points until there is sufficient demand for LNG as a marine fuel, on the other hand, ship-owners are unwilling to invest in LNG vessels if LNG refueling opportunities are not easy to obtain [

55].

Storage capacity is another technological barrier to several alternative fuels. As an example, LNG fuel tanks require two to three times the volume of fuel-oil tanks with the same energy content. In the comparison between liquid and gaseous fuels, the former require storage tanks that are more easily integrable onboard. Conversely, storage tanks for gas fuels are typically more costly, space-consuming and challenging to integrate onboard.

Similarly, the electrification of modern ships brings a number of challenges concerning the need for more shore-based facilities for battery charging and more. Despite major technological advances in battery capacity and efficiency, batteries must still become considerably more efficient and less heavy to meet the needs of large ocean-going ships. While several mature applications of battery-electric propulsion can be found in the short-sea-shipping segment (the first battery-electric short-sea ferry headed out in 2015) [

125,

126], much work is still needed before similar applications in the deep-sea market. This does not exclude the successful application of batteries on large ocean-going ships for specific purposes [

127]. As an example, several shipping companies are pioneering the use of hybrid marine propulsion systems in ECAs [

128].

As regards clean alternatives (biofuels, methanol, hydrogen, etc.), despite their high potential to reduce CO2 emissions, they are not expected to become feasible on a large scale within a short time because of several technical, economic and safety challenges. The same major concerns exist in using nuclear energy for ship propulsion.

5.3. Time Barriers

Implementing green initiatives needs time and planning. The survey by Reference [

81] finds out that the reasons for the lack of implementation of energy efficiency measures are related to time constraints in decision making, absence of planning and few incentives. By way of example, it takes time to convert ships to LNG or to build new LNG-burning vessels, and it also takes time to install scrubbers. Ship-owners may also have their agenda and objectives, and these can conflict with IMO ones.

5.4. Barriers Related to Unclear and Unfair Regulatory Frameworks

Environmental standards and regulations across the world have to be agreed and adopted in order not to distort competition in international shipping [

129]. A level playing field across the EU and possibly at the international level must be guaranteed. If a country adopts unilaterally more strict measures, the competition is distorted [

130]. As an example, in February 2019, the EU tabled a proposal to the IMO requesting a harmonization of rules relating to scrubber discharge. This comes in the course of concerns on open-loop scrubbers and regional restrictions imposed on their use. It goes without saying that despite strict policies and regulations need to be taken on an international level, complementary action on the regional and national level can still facilitate the low-carbon transition through ad hoc initiatives [

131].

5.5. Side Effects

There are some concerns, according to which some regulations aimed at reducing some problems can exacerbate others [

130]. The introduction of low-sulfur fuels would result in increased CO

2 emissions and a potential modal shift to land transport [

132]. Likewise, the implementation of some measures that are successful from a solely environmental perspective may result in a reduction in the profitability of maritime transport bringing several undesirable side-effects, such as cargo shifts to other modes or reduction of trade [

133]. According to some estimates, the designation of the Mediterranean Sea as an ECA will cause an increase in transport costs of about 6.95 €/ton and will result in a modal shift of 5.2% in favor of the road-only mode [

134,

135]. Similarly, the higher transport costs that will likely result from the implementation of CO

2 mitigation measures is believed to potentially impact not only the modal share of international transport, but also global trade patterns [

114].

5.6. Obstacles Related to Contractual Clauses and Split Incentives

Especially on the spot market, they can be mainly related to the type of charter contracts that may limit the implementation of technical and operational measures. Contracts can contain clauses on speed and bunker consumption or regulations of delays that can make unattractive some practices, such as slow steaming. Another obstacle is related to split incentives that arise when two parties engaged in a contract have different goals. In shipping, they typically occur between ship-owners and charterers, due to divided responsibility for fuel costs [

27]. Ship-owners who make investments to improve the environmental performance of their fleet cannot be able to recover their investments unless they directly operate their ships or have specific long-term agreements with charterers.

5.7. Barriers Related to Incomplete and Non-Transparent Information

Informational problems are relevant obstacles faced by shipping operators to the implementation of emission reduction solutions. More than a few operators complain about the lack of reliable and trusted information concerning costs and efficiency of the measures from independent third parties [

12]. The literature shows several attempts to calculate the techno-economic potential of emission reduction measures for shipping [

136]. The available evaluation methods are mainly based on the use of marginal abatement cost curves (MACCs) that provide the marginal cost of emission abatement for varying amounts of emission reduction [

69,

137]. The paper by Reference [

119] examines the costs and benefits of different reduction measures in connection with the IMO sulfur regulations by integrating the private abatement costs for ship-owners and the social-environmental benefits from emission control. Study results show that the MGO solution is most appealing from a cost perspective, whereas, scrubbers are more efficient in reducing sulfur and particle emissions. Although MACCs can provide some indications about the likelihood of investment, they have several shortcomings concerning the assumptions on which they are based and the impossibility of fully representing the associated costs and risks, including hidden costs [

27]. While the cost-effectiveness of low-carbon measures is usually evaluated on an individual basis, an attempt to evaluate the cost-effectiveness of correlated measures can be found in Reference [

138]. As regards the financing issues related to the implementation of different emission reduction technologies, they are only partially discussed in the literature. A selection criterion for low-carbon technologies in shipping based on the impact of financing concepts on the overall net present value can be found in Reference [

139].

5.8. Barriers Traditionally Inherent to the Sector: Inertia and Risk Appetite

Ship-owners and port operators are typically reported to be conservative and to make resistance to innovation. They generally do not welcome major changes and may be reluctant to implement solutions other than the standard ones. Shipping operators may be skeptical about the implementation of new solutions as a result of the needed large capital investments and the risk of being locked-in in unsuccessful technologies. The perception of risk, both perceived and real, is a traditional barrier to the implementation of innovation in the maritime industry. The risk can be classified into three dimensions—business, technical and external [

115]. Business risk mainly concerns financing risk, due to investments repayments; technical risk concerns unreliability of the measures implemented and their performance; and external risk concerns economic trends, fuel prices, policy and regulations. Particularly, the latter is highly representative of what shipping operators are facing in these years and explains why many shipping operators are adopting a “

wait-and-see” strategy as they consider it risky investing when additional regulations are still being developed.

5.9. Political Barriers

Especially regarding the adoption of MBMs, political obstacles (due to unnecessary fragmentation and complexity of the international scene, combined with factors that relate only to the political sphere) are believed to slow down the decarbonization process of shipping. Removing these obstacles is considered essential to push the decarbonization process forward [

69].

6. RQ4: Is There an Objective Way to Assess the Technical Possibility to Achieve the Ambitious IMO’s GHG Targets?

Reducing shipping emissions implies being able to measure them. The issue of measurability is considered one of the most underrated problems when dealing with maritime emissions [

74]: Is there a reliable way to measure emissions?

Shipping emissions are not measured directly—all the existing data are estimates produced by applying specific methods [

140]. Available methods can be grouped into three main categories depending on the specific estimation approach they use [

103,

141]:

Fuel-based or top-down approaches;

Activity-based or bottom-up approaches;

Hybrid methods that combine fuel-based and top-down approaches.

The first approach combines data on marine fuel sales and fuel-related emission factors, but does not consider actual maritime activities. The second approach uses more detailed information on ship characteristics, as well as operational data for both port and marine activities, combined with emissions and load factors. The third approach is a mix of the first two.

Giving a reliable estimate of the emission reduction potential of the various measures is not easy. The existing body of literature includes broad estimates of emission reduction potential for several measures. In particular, References [

13] and [

114], based on 150 and around 70 studies, respectively, summarize a large portion of the literature on the potential emissions reductions for several green measures. Both reviews highlight a large range in the GHG emission reduction potentials per measure as derived from the available studies, and both suggest a combination of measures would result in larger reduction potentials.

Table 2 reports and compares the GHG reduction potential ranges as derived from the two review papers analyzed. Looking at the numbers, it not only emerges a large range in the emission reduction potentials reported by each study, but also important differences among the potential reported by the two studies for the same measure. The reasons of such differences may be manifold, e.g., the specific application case, how the trial was conducted, the traffic segment (deep-sea or short-sea shipping) and the type of ship considered. However, if on the one hand such variability can be explained by differences in assumptions and baselines across the selected studies, on the other hand, it also indicates limited agreement across studies and estimation methodologies, and thus, significant uncertainty about the reported reduction potentials. These elements make clear the need for more transparent research in the field.

The measurability issue also makes difficult assessing the technical possibility to achieve the ambitious IMO’s goals [

142]. Though several scholars seem to agree that halving shipping emissions by 2050 will require a consistent switch to non-fossil fuel sources [

56], very few studies focus on the quantitative assessment of the technical possibility to reach the IMO’s GHG targets by 2050. Some interesting attempts in this regard can be found in References [

143] and [

144], which examine the technical possibility of decarbonizing international shipping considering a time horizon up to 2035 and 2050, respectively. Particularly interesting is the work by Reference [