Consider a government loan guarantee program that guarantees a proportion

L of each private loan made by program-targeted entrepreneurs. In other words, the bank, in case of facing default, is guaranteed

L percent of the loan payment. To facilitate comparison, we assume that only one type of the entrepreneurs is the targeted group at a time. Assume that the government finances loan guarantees through imposition of a lump-sum tax. The government has access to the same information as the banks; therefore, under asymmetric information, each borrower knows its own type, but the bank and government cannot distinguish among borrowers. The bank and government know that a fraction

of these borrowers are high-risk types and that

are low-risk types. The information structure of including government loan guarantees into the model is shown in

Figure 2.

At first, government announces that at which risk type of entrepreneurs the loan guarantee program is targeted. Banks, taking the loan guarantees as consideration, determine the optimal loan contract with the borrowers. To make every borrower truthfully reveal their risk type, the loan contract requires meeting the condition of incentive compatibility. After entrepreneurs’ project returns are realized, if the entrepreneurs cannot pay back the loan, the bank takes their collateral if it is pledged and collects the promised loan payment from the government if the loan is guaranteed.

3.1. Loan Guarantees Target Low-Risk Entrepreneurs

When government announces it will guarantee percent of the loan payment for low-risk entrepreneurs, the zero-profit condition for the bank that makes a loan to low-risk borrowers becomes . The first term is the bank’s gross interest revenues if the entrepreneur’s project succeeds and pays back the debt. The next two terms, , describe that the bank receives collateral and guaranteed loan payment if the entrepreneur’s project fails. Government financing this guarantee program needs to collect lump-sum taxes, , which equals multiplication of the proportion of low-risk borrowers, the probability of granting the loan, the probability of failure of the project, and the guaranteed loan payment.

The equilibrium contract

solves the following problem (We label the equilibrium contract under asymmetric information and unbinding collateral constraints as

; and adding a subscript

L,

, express there are loan guarantees targeted at low-risk borrowers.):

s.

t.

Equations (5a) and (5b) are the incentive compatibility constraints. With asymmetric information, the optimal loan contract obtained under perfect information, , cannot satisfy the incentive compatibility constraints. The reason is that, under perfect information, no collateral is required for either type of borrowers, and high-risk borrowers are charged a higher interest rate, causing them to have an incentive to disguise themselves as low-risk ones. The bank’s contract must, therefore, satisfy these incentive compatibility constraints. Equations (6) and (7) are feasibility conditions. Equation (8a) is the bank’s zero-profit condition when it loans to high-risk borrowers, whereas Equation (8b) is the similar condition when the bank loans to low-risk borrowers who are included in loan guarantees.

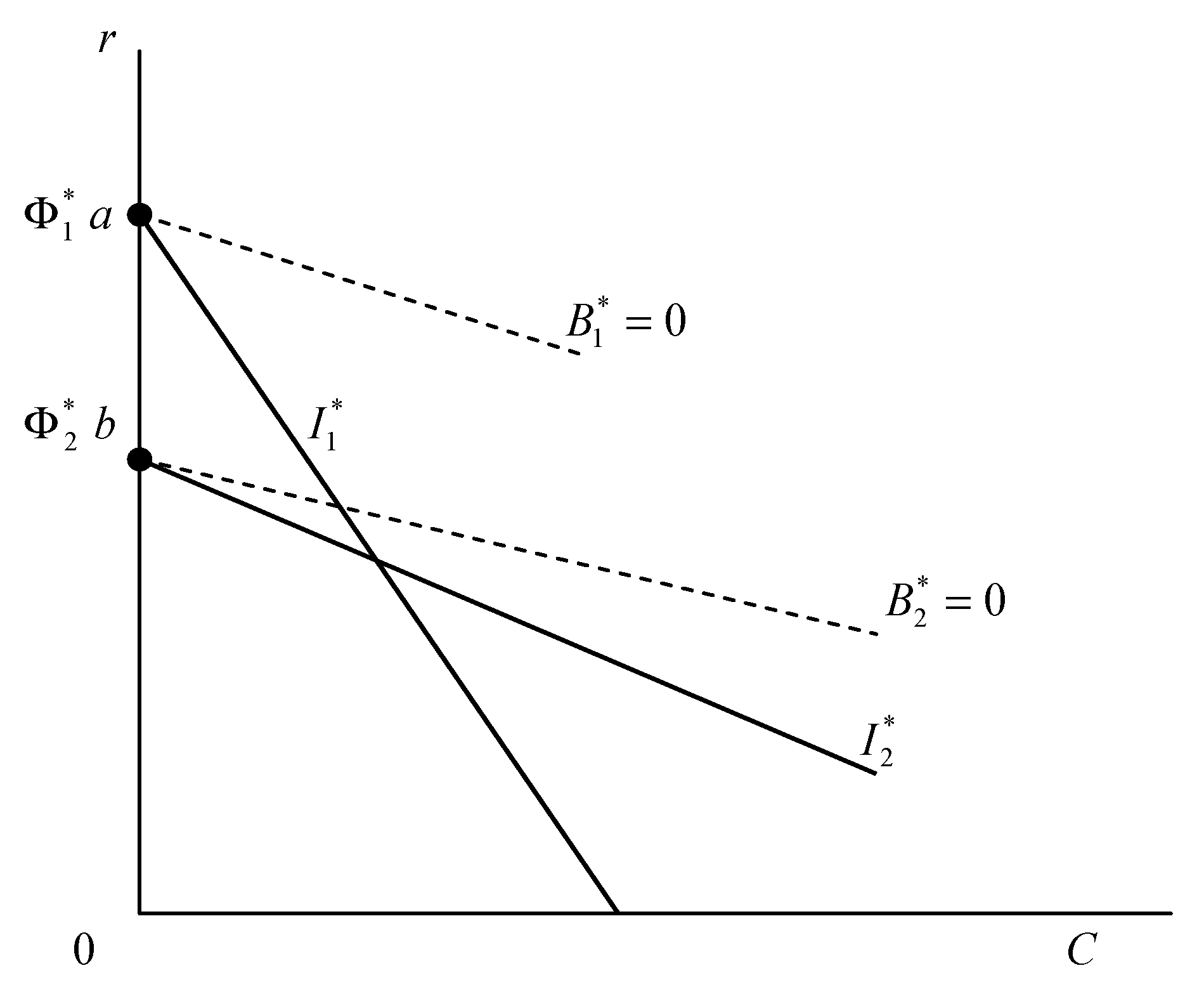

The solution of this contract is as below:

Obviously, without loan guarantees,

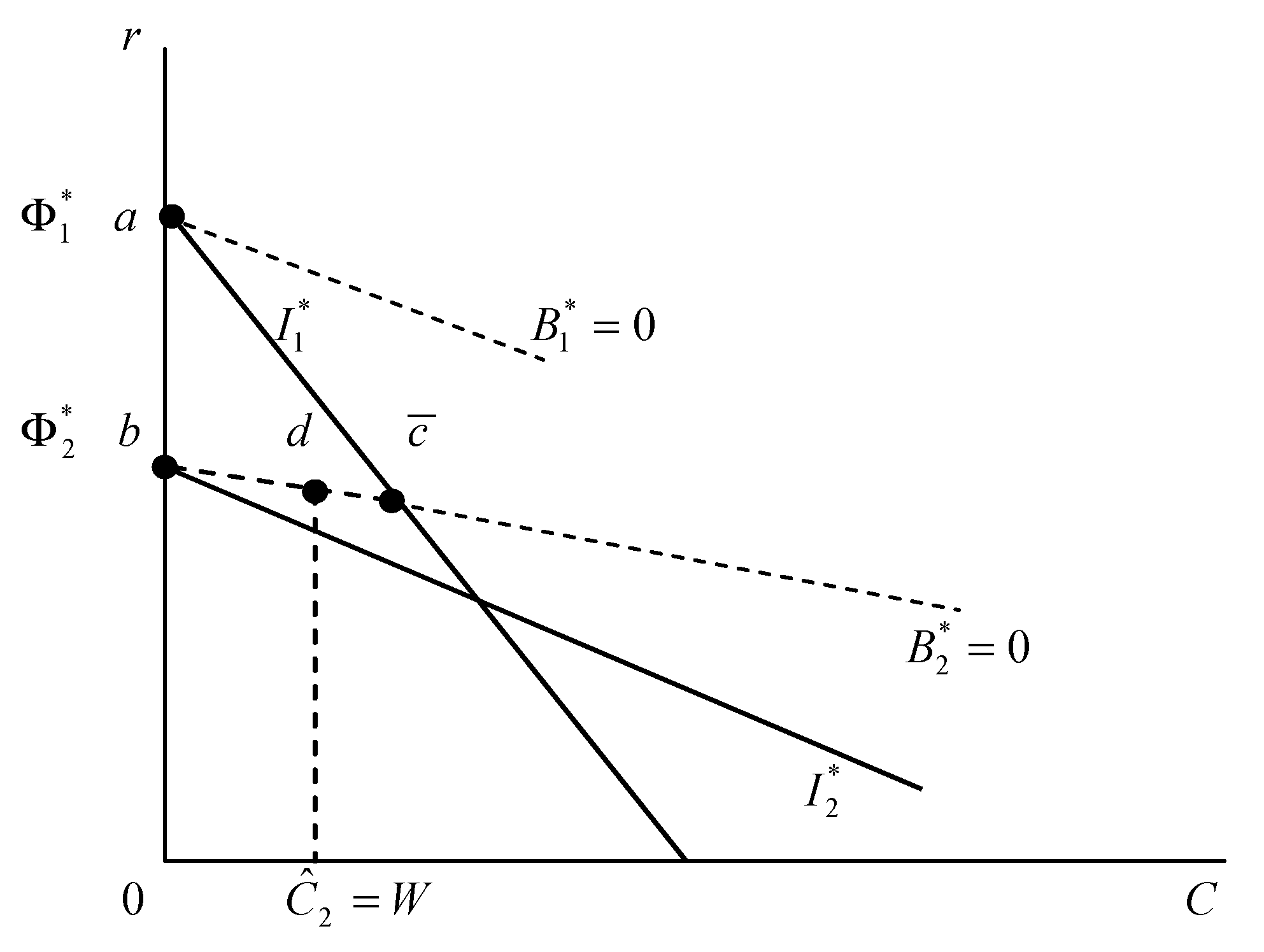

, the equilibrium contract under asymmetric information and unbinding collateral constraints is the same as the one in Besanko and Thakor [

3], denoted by

and depicted in

Figure 3. The separating equilibrium consists of two contracts: one is located at point

a chosen by high-risk borrowers, and the other is located at point

chosen by low-risk borrowers.

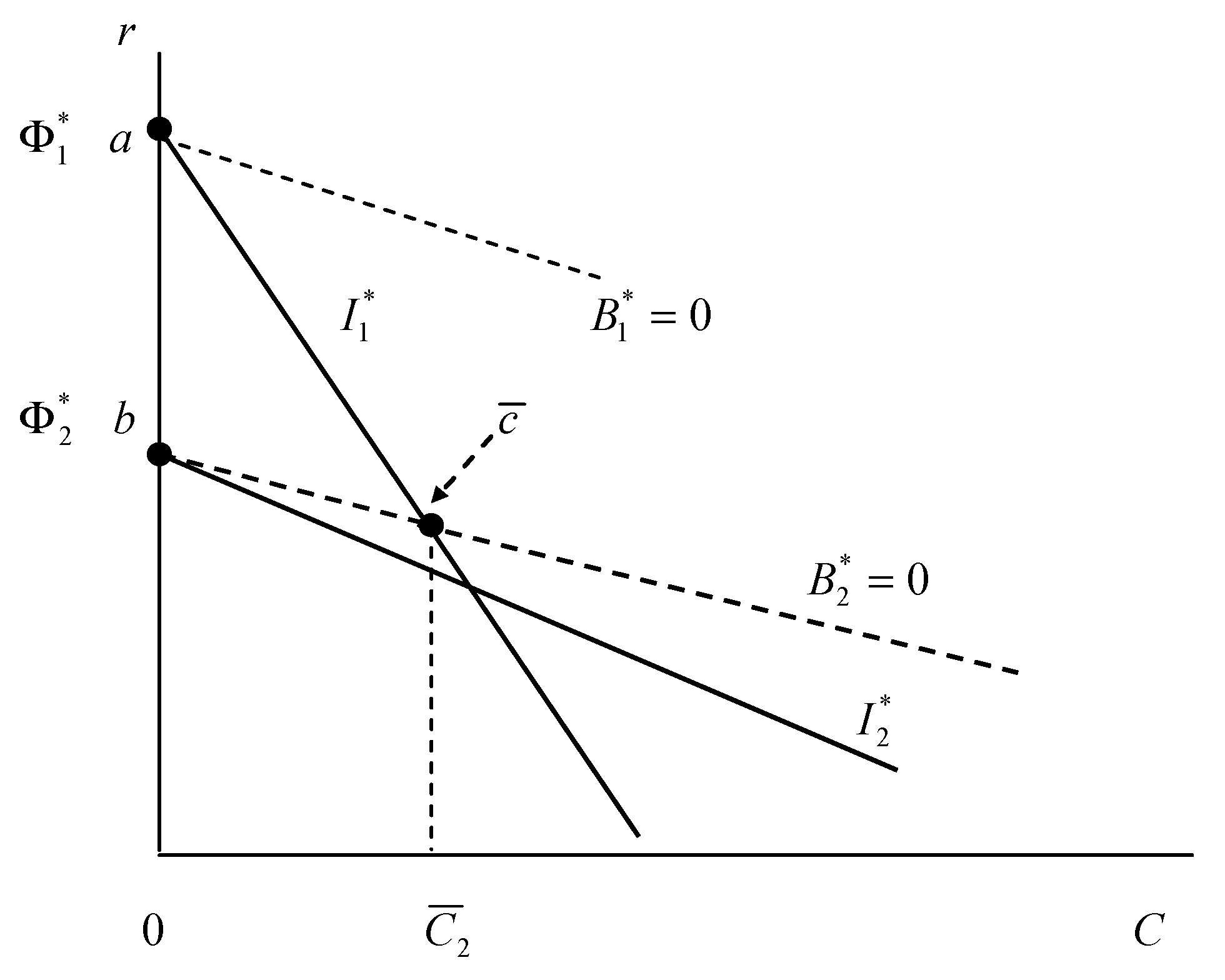

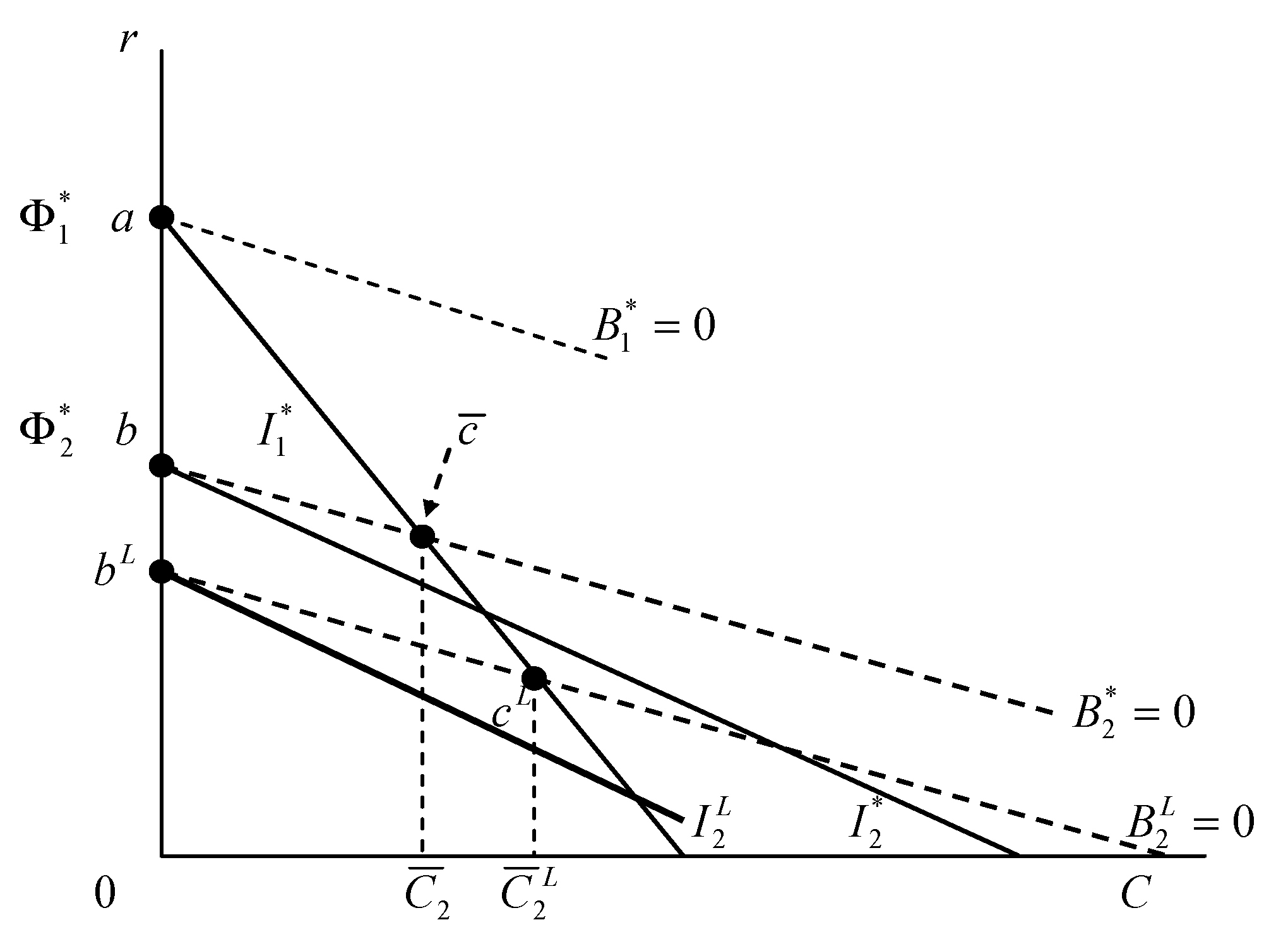

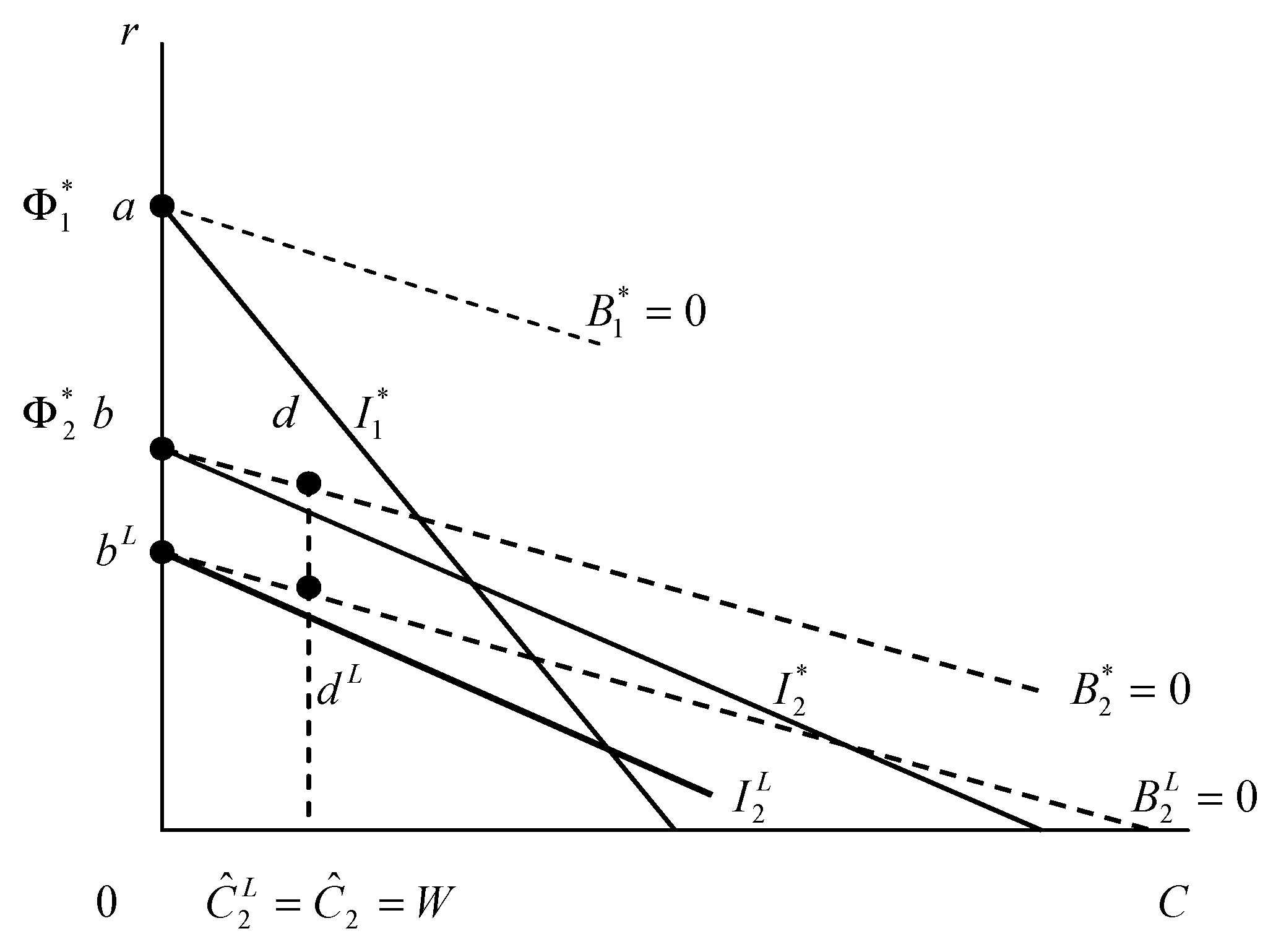

However, when loan guarantees are targeted at low-risk borrowers, the bank’s zero-profit condition, which includes guaranteed loan payment from government, implies that low-risk borrowers can retain greater expected social surplus than they can without government loan guarantees. This can be shown from the inward movement of line

to

and low-risk borrowers’ expected utility line

to

in

Figure 4. Low-risk borrowers take the contract at point

instead of point

, pledging more collateral in exchange for a lower interest rate. Not surprisingly, high-risk borrowers choose the same contract as the one without a government loan program.

Lemma 1. With unbinding collateral constraints, loan guarantees targeting low-risk entrepreneurs increase the amount of collateral () and reduce the interest rate () for low-risk entrepreneurs in equilibrium contract.

Proof. , . , , . , . , , . □

Lemma 1 shows that the amount of collateral pledged by low-risk borrowers, , is increasing with the L percent of loan guarantees, and the interest rate charged for low-risk borrowers, , is decreasing with L; thus, compared with in the absence of loan guarantees, and .

Under asymmetric information, interest rates alone cannot sort out borrowers of different risk types; collateral requirements serve as an incentive mechanism. Without government credit policy, low-risk borrowers have pledged collateral in exchange for a lower interest rate than that under perfect information. With loan guarantees that make a further lower interest rate possible, the incentive of pledging more collateral becomes even stronger. As long as their wealth is sufficient to pledge collateral, the loan is granted with a lower interest rate.

The social welfare under the economy with loan guarantees targeting low-risk entrepreneurs is labeled as

and is obtained by summation of the expected entrepreneur utility and bank profit, subtracting the cost of the loan guarantee program,

. That is,

Substituting the results of equilibrium contract

into Equation (9), we obtain:

Similarly, the economic welfare without loan guarantees is calculated using the contract

,

Compare economic welfare with loan guarantees targeting low-risk borrowers,

, and that without loan guarantees,

, i.e., Equations (10) and (11):

In addition, we also know:

Proposition 1 summarizes these results of welfare comparison.

Proposition 1. With unbinding collateral constraints, loan guarantees targeting low-risk entrepreneurs increase these entrepreneurs’ utilities and leave high-risk entrepreneurs’ utilities the same. Moreover, this loan guarantee scheme decreases overall economic welfare.

The reason that loan guarantees reduce the overall economic welfare is attributed to their raising of collateral. Pledging collateral is socially costly because of its lower valuation by banks than by entrepreneurs.

3.2. Loan Guarantees Target High-Risk Entrepreneurs

This section turns to the discussion about the effects of loan guarantees if the targeted group that government chooses to assist is the high-risk type of borrowers. From Proposition 1, loan guarantees targeting low-risk borrowers are harmful to the overall economic welfare because they deteriorate asymmetric information problems in the credit market. Low-risk borrowers are forced to pledge more collateral than they ever did to sort themselves out from high-risk borrowers and deter high-risk borrowers from disguising themselves as low-risk ones. Loan guarantees, however, increase a targeted group’s welfare, resulting in putting up too much collateral at a cost of reducing overall economic welfare. Can loan guarantees targeting the other type of borrowers remedy their dilemma on distributive and overall welfare effects?

When loan guarantees target high-risk entrepreneurs, government guarantees

L percent of their loan payment, and the zero-profit condition for the bank that makes a loan to high-risk borrowers becomes

. Similarly, assume that the government finances loan guarantees by collecting

lump-sum taxes,

. The economic welfare associated with this loan program,

, is thus expressed as follows:

The equilibrium contract is similarly derived as that in

Section 3.1, except by replacing Equations (8a) and (8b) with the following two Equations.

We denote the equilibrium contract when loan guarantees targeting high-risk borrowers as

. The solution of this contract is as below:

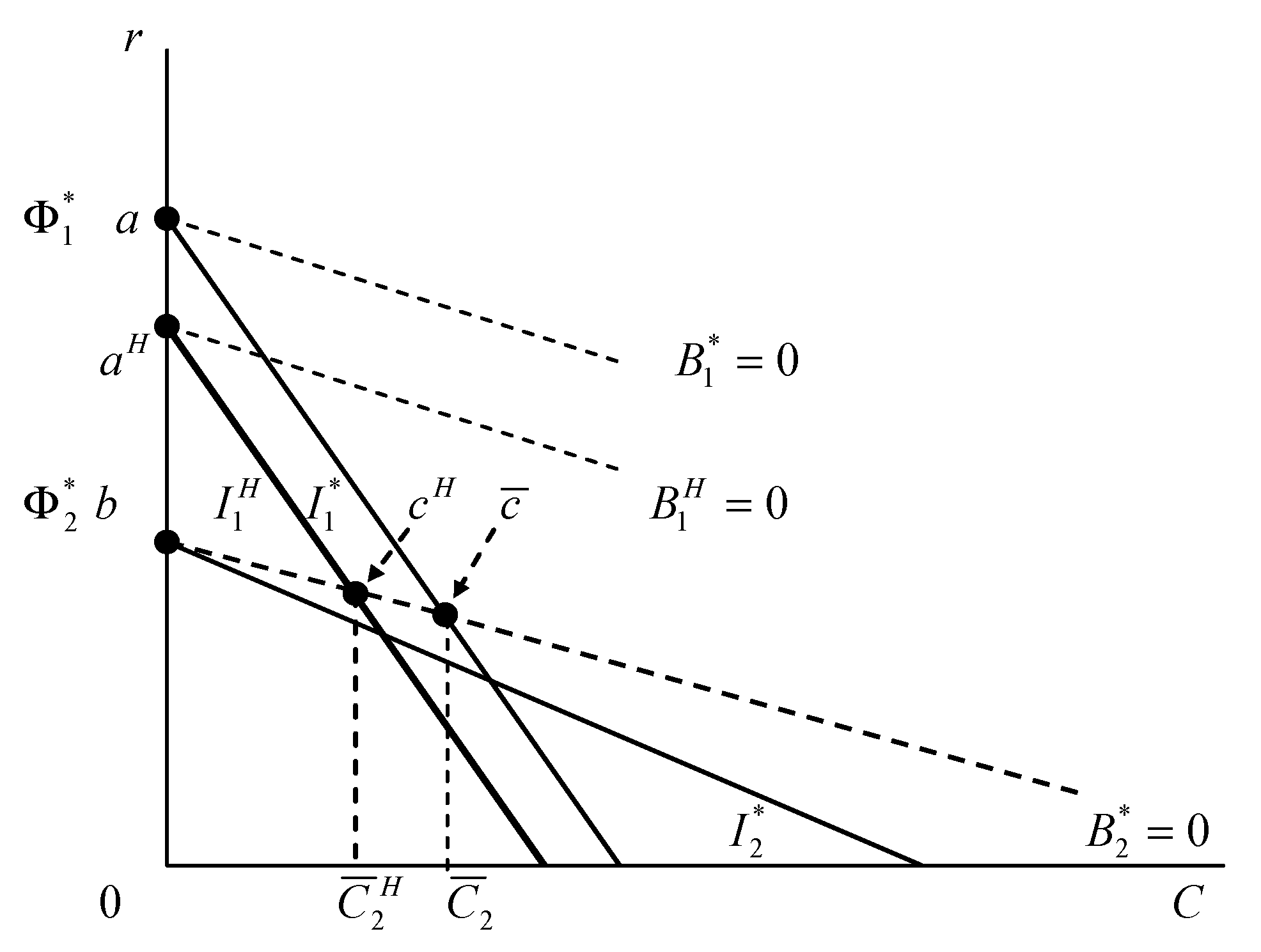

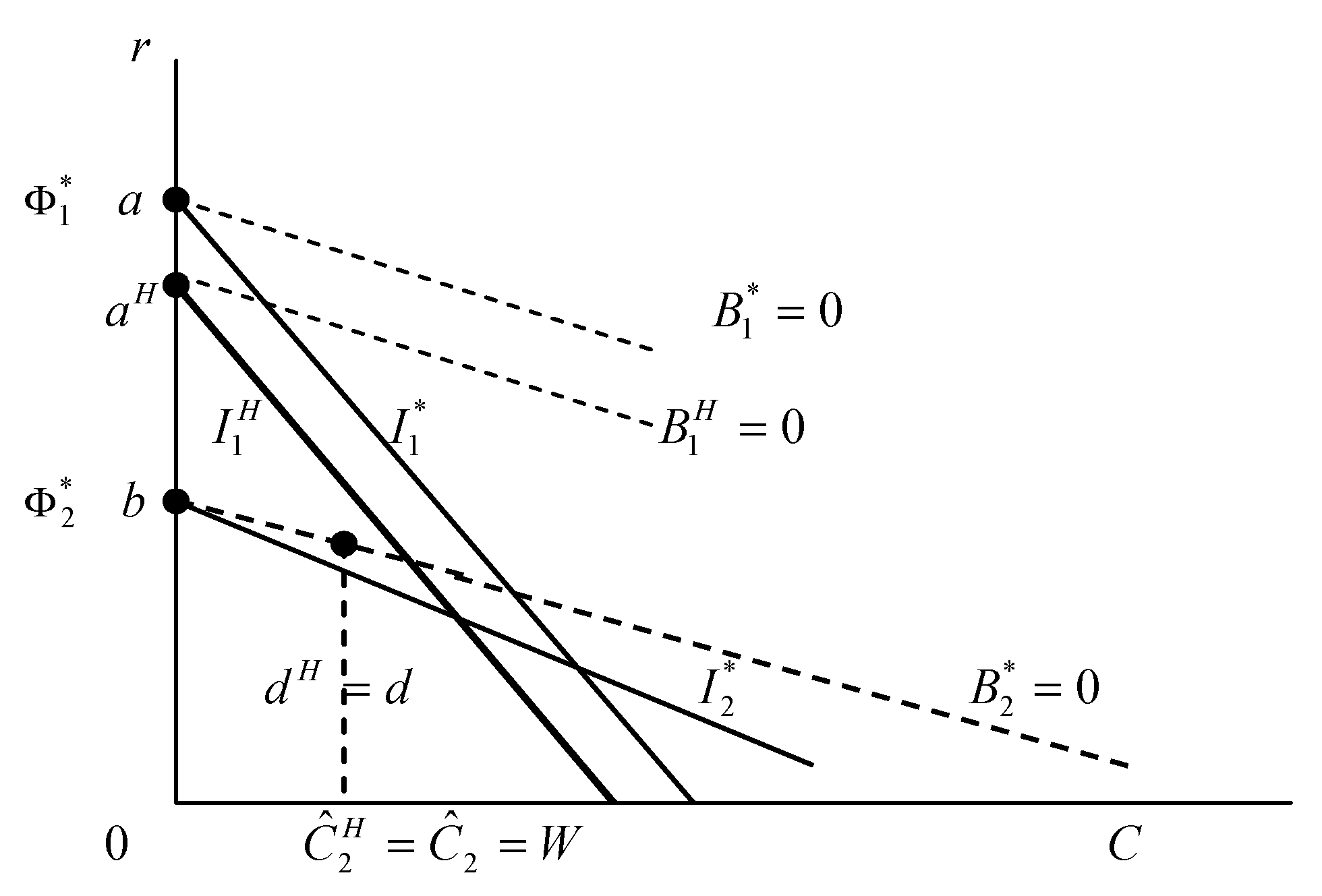

Again, without loan guarantees,

, the equilibrium contract under asymmetric information and unbinding collateral constraints is the same as the one in Besanko and Thakor [

3], labeled by

and depicted in

Figure 3. When loan guarantees are targeted at high-risk borrowers, the bank’s zero-profit condition implies that high-risk borrowers can retain greater expected social surplus than they can without government loan guarantees. This can be shown from the inward movement of line

to

and high-risk borrowers’ expected utility line

to

in

Figure 5. Low-risk borrowers take the contract at point

instead of point

, pledging less collateral than they do without a government loan program. For high-risk borrowers who can apply loan guarantees, they pay less interest and still do not pledge any collateral.

Lemma 2. With unbinding collateral constraints, loan guarantees targeting high-risk entrepreneurs decrease the amount of collateral () and increase the interest rate () for low-risk entrepreneurs in equilibrium contract. The targeted high-risk entrepreneurs pay less interest () and pledge no collateral ().

Proof. , . , , .

, . , , .

, . , , . □

Lemma 2 shows that when loan guarantees target high-risk entrepreneurs, the amount of collateral pledged by low-risk borrowers, , is decreasing with the L percent of loan guarantees; the interest rate charged for low-risk borrowers, , is increasing with L; and the interest rate charged for high-risk borrowers, , is decreasing with L. Thus, compared with in the absence of loan guarantees, and , and the targeted high-risk entrepreneurs pay less interest ().

When high-risk borrowers are the targeted group for loan guarantees, banks offer them a lower interest rate, mitigating the problem of misrepresenting themselves as low-risk borrowers. Thus, the role of collateral as a signaling device for deterring high-risk borrowers from choosing a low-risk borrowers’ contract is not as important as that in

Section 3.1 and that without government loan guarantees. Aside from interest rate and collateral, both types of borrowers are granted credit because of their sufficient wealth to pledging collateral.

The economic welfare when loan guarantees target high-risk entrepreneurs,

, is obtained by substituting the results of equilibrium contract

into Equation (12):

Compare Equation (14) with the economic welfare without loan guarantees

in Equation (11) to have:

In addition, the following comparison holds, which leads us to Proposition 2.

Proposition 2. With unbinding collateral constraints, loan guarantees targeting high-risk entrepreneurs increase both types of entrepreneurs’ utilities, as well as overall economic welfare.

Loan guarantees targeting high-risk entrepreneurs are Pareto improving in the sense that they increase overall economic welfare. The reason that loan guarantees improve welfare lies in their effectively reducing the amount of collateral pledged. Even if collateral plays a screening role in the imperfectly informational credit market, pledging collateral is socially costly. With a loan guarantee program carefully designed to target high-risk borrowers, it cures partial imperfect information, and therefore increases the efficiency of the credit market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}