Sustainability of Global Economic Policy and Stock Market Returns in Indonesia

Abstract

:1. Introduction

2. Literature Review

3. Data and Methodology

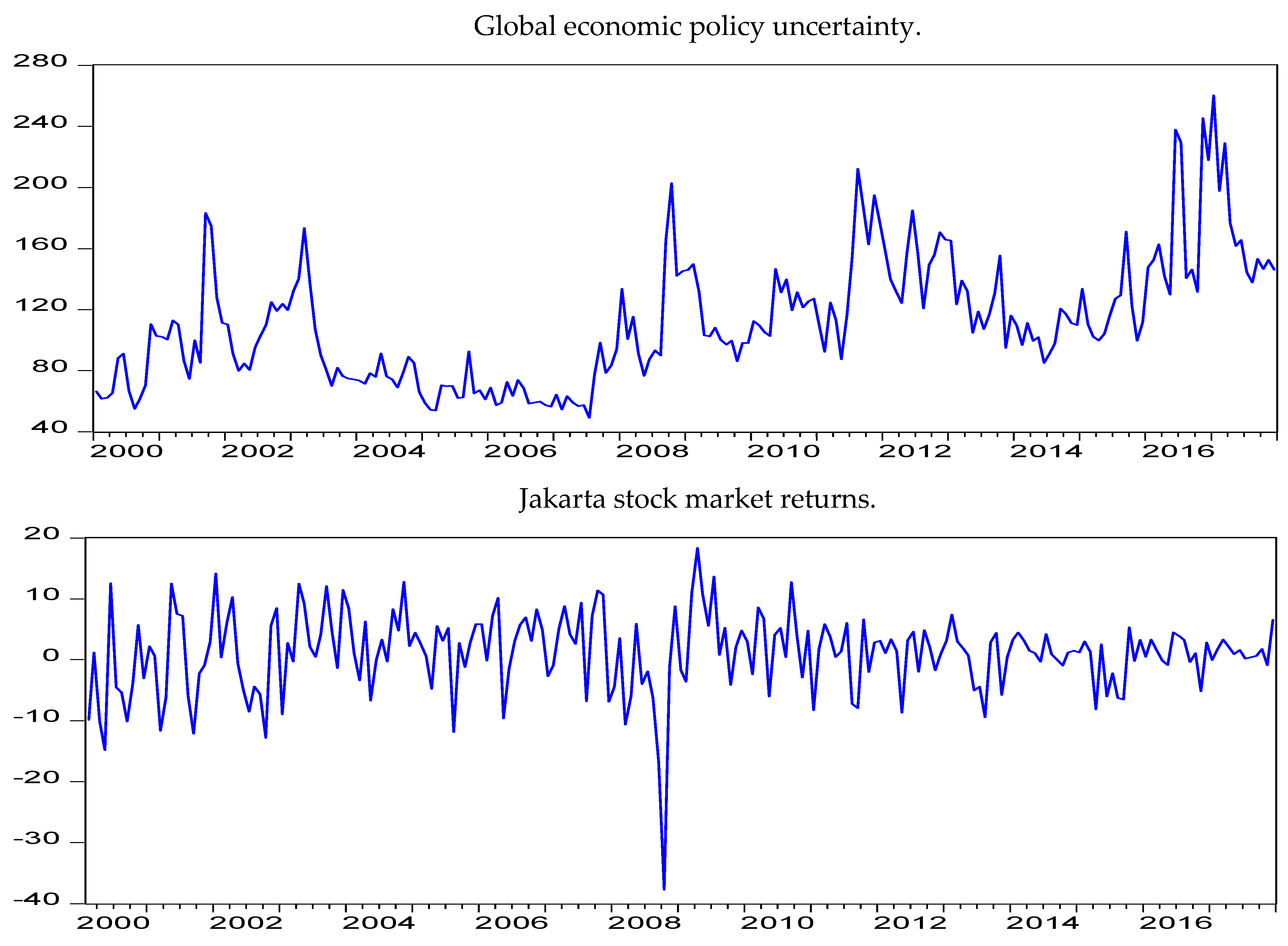

3.1. Data

3.2. Methodology

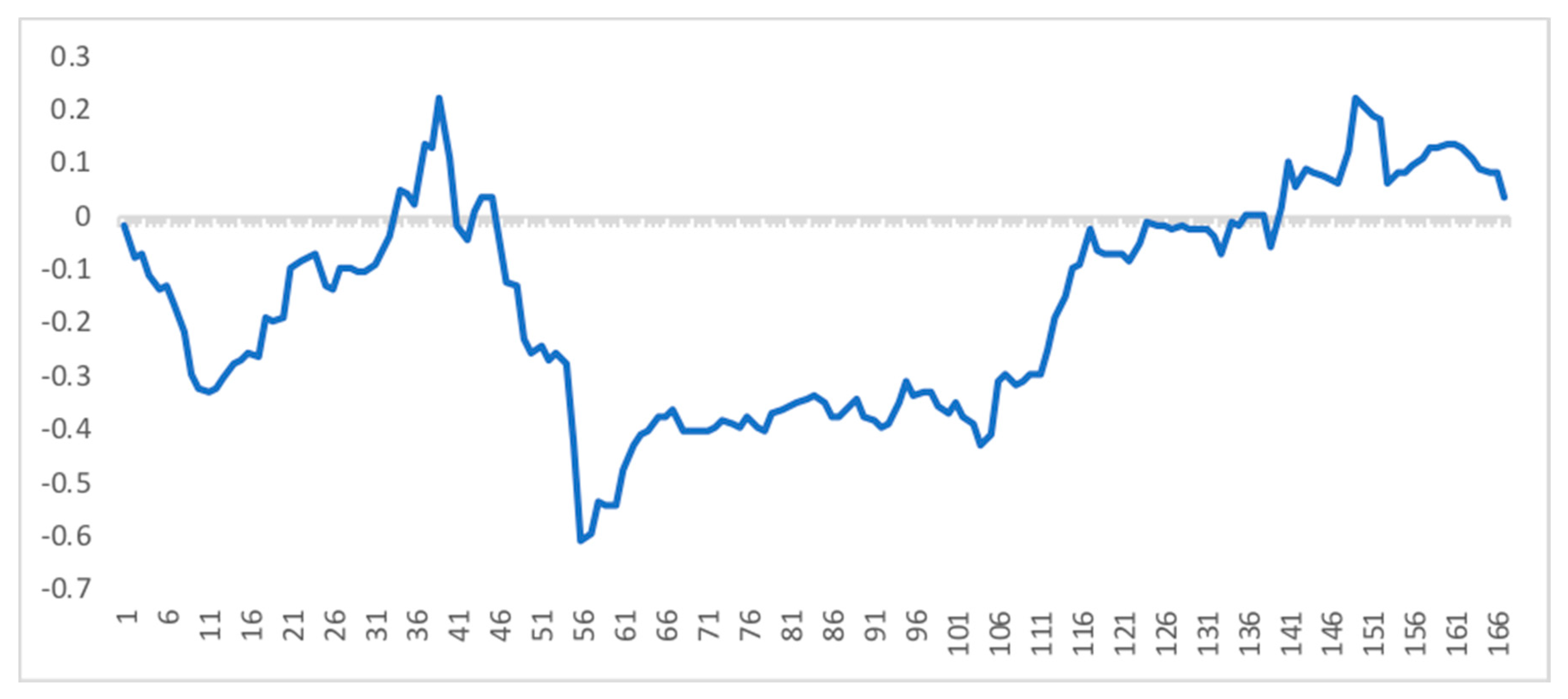

3.2.1. Rolling Window Correlation

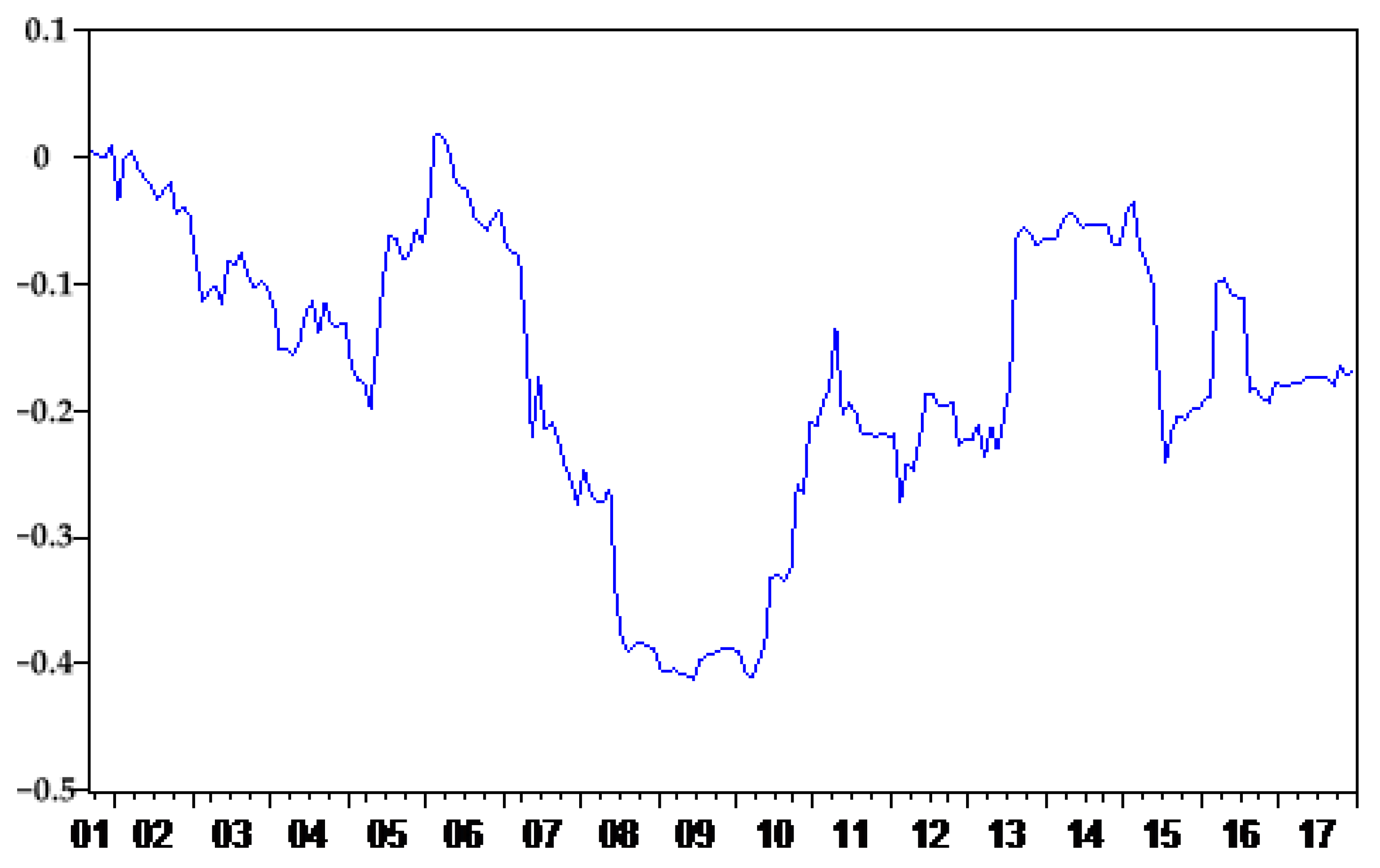

3.2.2. Dynamic Conditional Correlation

3.2.3. Autoregressive Distributed Lag Model

4. Empirical Analysis

4.1. Descriptive Statistics

4.2. Rolling Window Correlation

4.3. Dynamic Conditional Correlation Results

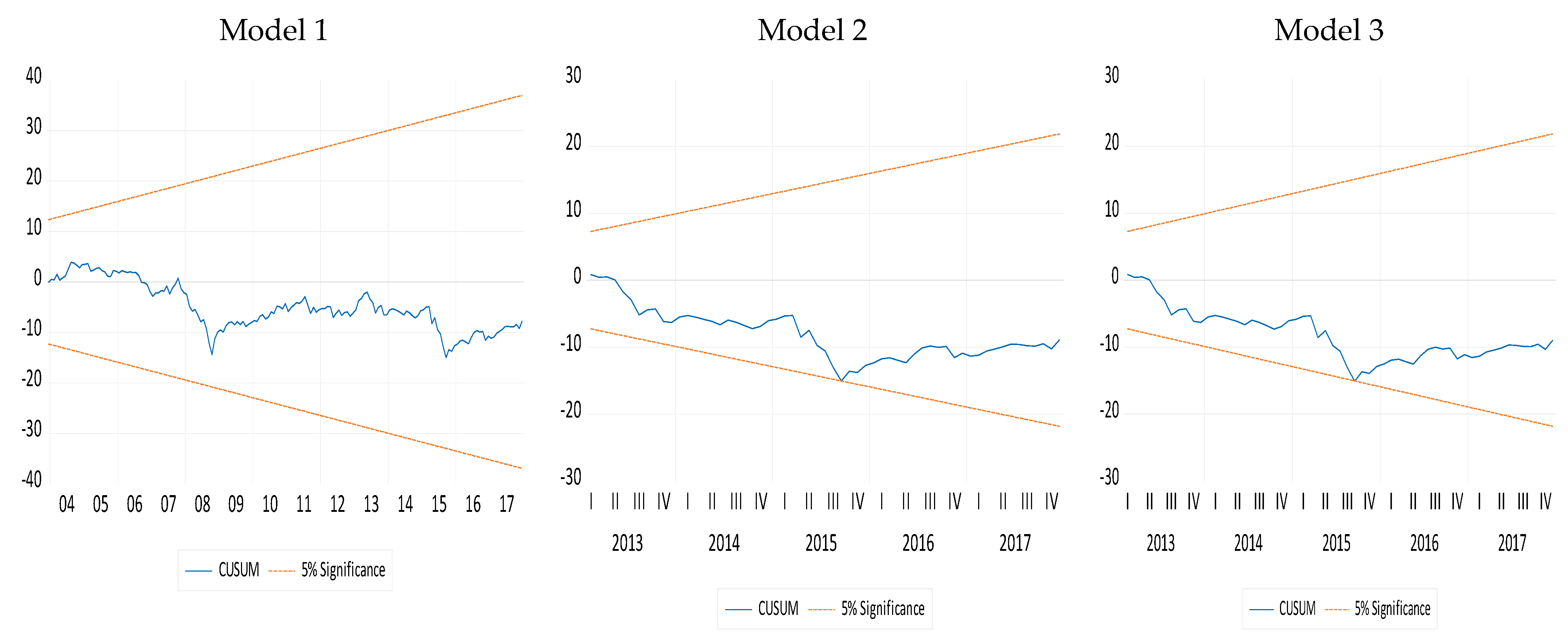

4.4. Autoregressive Distributed Lag Model

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Ethical Approval

References

- World Bank. The World Bank in Indonesia. 2019. Available online: https://www.worldbank.org/en/country/Indonesia/overview (accessed on 25 July 2020).

- Sharma, S.S.; Narayan, P.K.; Thuraisamy, K.; Laila, N. Is Indonesia’s stock market different when it comes to predictability? Emerg. Mark. Rev. 2019, 40, 100623. [Google Scholar] [CrossRef]

- Rhee, S.G.; Wang, J. Foreign institutional ownership and stock market liquidity: Evidence from Indonesia. J. Bank. Financ. 2009, 33, 1312–1324. [Google Scholar] [CrossRef]

- James, G.A.; Karoglou, M. Financial liberalization and stock market volatility: The case of Indonesia. Appl. Financ. Econ. 2010, 20, 477–486. [Google Scholar] [CrossRef]

- Workman, D. Indonesia’s Top Trading Partners. 2019. Available online: http://www.worldstopexports.com/indonesias-top-15-import-partners/ (accessed on 3 March 2020).

- Basri, M.C.; Rahardja, S. The Indonesian Economy amidst the Global Crisis: Good Policy and Good Luck. Asean Econ. Bull. 2010, 27, 77–97. Available online: https://www.jstor.org/stable/41317110?seq=1 (accessed on 28 June 2019). [CrossRef]

- Baker, S.; Bloom, N.; Davis, S. Measuring economic policy uncertainty. Q. J. Econ. 2016, 131, 1593–1636. Available online: https://EconPapers.repec.org/RePEc:oup:qjecon:v:131:y:2016:i:4:p:1593-1636 (accessed on 19 March 2020). [CrossRef]

- Bloom, N. Fluctuations in Uncertainty. J. Econ. Perspect. 2014, 28, 153–176. [Google Scholar] [CrossRef] [Green Version]

- Fernandez-Villaverde, J.; Guerron-Quintana, P.; Kuester, K.; Rubio-Ramirez, J. Fiscal volatility shocks and economic activity. Am. Econ. Rev. 2015, 105, 3352–3384. [Google Scholar] [CrossRef] [Green Version]

- Bernanke, B.S. Irreversibility, Uncertainty, and Cyclical Investment. Q. J. Econ. 1983, 98, 85–106. [Google Scholar] [CrossRef]

- Wang, Y.; Chen, C.R.; Huang, Y.S. Economic policy uncertainty and corporate investment: Evidence from China. Pac.-Basin Financ. J. 2014, 26, 227–243. [Google Scholar] [CrossRef]

- Eberly, J.C. Adjustment of Consumers’ Durables Stocks: Evidence from Automobile Purchases. J. Politi-Econ. 1994, 102, 403–436. [Google Scholar] [CrossRef]

- Jones, P.M.; Olson, E. The time-varying correlation between uncertainty, output, and inflation: Evidence from a DCC-GARCH model. Econ. Lett. 2013, 118, 33–37. [Google Scholar] [CrossRef]

- Colombo, V. Economic policy uncertainty in the US: Does it matter for the Euro area? Econ. Lett. 2013, 121, 39–42. [Google Scholar] [CrossRef] [Green Version]

- Gulen, H.; Ion, M. Policy Uncertainty and Corporate Investment. Rev. Financ. Stud. 2015, 29, 523–564. [Google Scholar] [CrossRef]

- Arellano, C.; Bai, Y.; Kehoe, P. Financial Markets and Fluctuations in Uncertainty. Federal Reserve Bank of Minneapolis Research Department Staff Report. 2010. Available online: https://www.minneapolisfed.org/research/sr/sr466.pdf (accessed on 20 July 2020).

- Masoud, N. The impact of stock market returns on economic growth. Int. J. Econ. Financ. Issues 2013, 3, 788798. [Google Scholar]

- Forbes, K.J.; Rigobon, R. No Contagion, Only Interdependence: Measuring Stock Market Comovements. J. Financ. 2002, 57, 2223–2261. [Google Scholar] [CrossRef]

- Chen, P. Understanding international stock market comovements: A comparison of developed and emerging markets. Int. Rev. Econ. Financ. 2018, 56, 451–464. [Google Scholar] [CrossRef]

- Eiling, E.; Gerard, B. Emerging Equity Market Comovements: Trends and Macroeconomic Fundamentals. Rev. Financ. 2015, 19, 1543–1585. [Google Scholar] [CrossRef] [Green Version]

- Hamao, Y.; Masulis, R.W.; Ng, V. Correlations in Price Changes and Volatility across International Stock Markets. Rev. Financ. Stud. 1990, 3, 281–307. [Google Scholar] [CrossRef]

- Aggarwal, R.; Rivoli, P. The relationship between the U.S. and four Asian markets. ASEAN Econ. Bull. 1989, 6, 110–117. [Google Scholar] [CrossRef]

- Sarwar, G.; Khan, W. Interrelations of U.S. market fears and emerging markets returns: Global evidence. Int. J. Financ. Econ. 2019, 24, 527–539. [Google Scholar] [CrossRef] [Green Version]

- Ashanapalli, B.; Doukas, J. International stock market linkages: Evidence from pre and post-October 1987 period. J. Bank. Financ. 1993, 17, 193–208. [Google Scholar] [CrossRef]

- Chen, J.; Jiang, F.; Xue, S.; Yao, J. The world predictive power of U.S. equity market skewness risk. J. Int. Money Financ. 2019, 96, 210–227. [Google Scholar] [CrossRef]

- Bhuyan, R.; Robbani, M.G.; Talukdar, B.; Jain, A. Information transmission and dynamics of stock price movements: An empirical analysis of BRICS and US stock markets. Int. Rev. Econ. Financ. 2016, 46, 180–195. [Google Scholar] [CrossRef]

- Ji, Q.; Liu, B.-Y.; Cunado, J.; Gupta, R. Risk spillover between the US and the remaining G7 stock markets using time-varying copulas with Markov switching: Evidence from over a century of data. N. Am. J. Econ. Financ. 2020, 51, 100846. [Google Scholar] [CrossRef] [Green Version]

- Su, Z.; Fang, T.; Yin, L. Understanding stock market volatility: What is the role of U.S. uncertainty? N. Am. J. Econ. Financ. 2019, 48, 582–590. [Google Scholar] [CrossRef]

- Pastor, L.; Veronesi, P. Uncertainty about government policy and stock prices. J. Financ. 2012, 67, 1219–1264. [Google Scholar] [CrossRef]

- Bansal, R.; Yaron, A. Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles. J. Financ. 2004, 59, 1481–1509. [Google Scholar] [CrossRef] [Green Version]

- Smith, R. The world’s Biggest Economies in 2018. 2018. Available online: https://www.weforum.org/agenda/2018/04/the-worlds-biggest-economies-in-2018/ (accessed on 30 February 2020).

- Forbes, K.J.; Chinn, M.D. A decomposition of global linkages in financial markets over time. Rev. Econ. Stat. 2004, 86, 705–722. [Google Scholar] [CrossRef] [Green Version]

- Ehrmann, M.; Fratzscher, M. Global Financial Transmission of Monetary Policy Shocks. Oxf. Bull. Econ. Stat. 2009, 71, 739–759. [Google Scholar] [CrossRef] [Green Version]

- Bank Indonesia. 2008 Economic Report on Indonesia; Bank of Indonesia: Jakarta, Indonesia, 2008. [Google Scholar]

- Wu, T.-P.; Liu, S.-B.; Hsueh, S.-J. The Causal Relationship between Economic Policy Uncertainty and Stock Market: A Panel Data Analysis. Int. Econ. J. 2016, 30, 109–122. [Google Scholar] [CrossRef]

- Li, T.; Ma, F.; Zhang, X.; Zhang, Y. Economic policy uncertainty and the Chinese stock market volatility: Novel evidence. Econ. Model. 2020, 87, 24–33. [Google Scholar] [CrossRef]

- Yu, H.; Fang, L.; Sun, W. Forecasting performance of global economic policy uncertainty for volatility of Chinese stock market. Phys. A Stat. Mech. Appl. 2018, 505, 931–940. [Google Scholar] [CrossRef]

- Chuliá, H.; Gupta, R.; Uribe, J.M.; Wohar, M.E. Impact of US uncertainties on emerging and mature markets: Evidence from a quantile-vector autoregressive approach. J. Int. Financ. Mark. Inst. Money 2017, 48, 178–191. [Google Scholar] [CrossRef]

- Chen, J.; Jiang, F.; Tong, G. Economic policy uncertainty in China and stock market expected returns. Account. Financ. 2017, 57, 1265–1286. [Google Scholar] [CrossRef]

- Dakhlaoui, I.; Aloui, C. The interactive relationship between the US economic policy uncertainty and BRIC stock markets. Int. Econ. 2016, 146, 141–157. [Google Scholar] [CrossRef]

- Xiong, X.; Bian, Y.; Shen, D. The time-varying correlation between policy uncertainty and stock returns: Evidence from China. Phys. A Stat. Mech. Appl. 2018, 499, 413–419. [Google Scholar] [CrossRef]

- Yang, M.; Zhi-Qiang, J. The dynamic correlation between policy uncertainty and stock market returns in China. Phys. A 2016, 461, 92–100. Available online: https://EconPapers.repec.org/RePEc:eee:phsmap:v:461:y:2016:i:c:p:92-100 (accessed on 19 March 2020). [CrossRef]

- Ahmad, W.; Sharma, S.K. Testing output gap and economic uncertainty as an explicators of stock market volatility. Res. Int. Bus. Financ. 2018, 45, 293–306. [Google Scholar] [CrossRef]

- Christou, C.; Cunado, J.; Gupta, R.; Hassapis, C. Economic policy uncertainty and stock market returns in PacificRim countries: Evidence based on a Bayesian panel VAR model. J. Multinatl. Financ. Manag. 2017, 40, 92–102. [Google Scholar] [CrossRef]

- Tiwari, A.K.; Mutascu, M.I.; Albulescu, C.T. Continuous wavelet transform and rolling correlation of European stock markets. Int. Rev. Econ. Financ. 2016, 42, 237–256. [Google Scholar] [CrossRef]

- Engle, R. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. J. Bus. Econ. Stat. 2002, 2020, 339–350. [Google Scholar] [CrossRef]

- Longin, F.; Solnik, B. Extreme Correlation of International Equity Markets. J. Financ. 2001, 56, 649–676. [Google Scholar] [CrossRef]

- Caggiano, G.; Castelnuovo, E.; Groshenny, N. Uncertainty shocks and unemployment dynamics in U.S. recessions. J. Monet. Econ. 2014, 67, 78–92. [Google Scholar] [CrossRef] [Green Version]

- Bekiros, S.D.; Gupta, R.; Kyei, C. On economic uncertainty, stock market predictability and nonlinear spillover effects. N. Am. J. Econ. Financ. 2016, 36, 184–191. [Google Scholar] [CrossRef] [Green Version]

- Pastor, L.; Veronesi, P. Political uncertainty and risk premia. J. Financ. Econ. 2013, 67, 1219–1264. [Google Scholar] [CrossRef] [Green Version]

- Friedman, M. The role of monetary policy. Am. Econ. Rev. 1968, 58, 1–17. [Google Scholar]

- Kevin, A.H.; Gilbert, E.M. Investment with Uncertain Tax Policy: Does Random Tax Policy Discourage Investment? Econ. J. 1999, 109, 372–393. [Google Scholar]

- Robert, H. Regime Uncertainty: Why the Great Depression Lasted So Long and Why Prosperity Resumed After the War. Indep. Rev. 1997, 1, 561–590. [Google Scholar]

- Gilchrist, S.; Sim, J.W.; Zakrajsek, E. Uncertainty, Financial Friction and Investment Dynamics; Working paper. 2010. Available online: http://people.bu.edu/sgilchri/research/GSZ_Sept2010.pdf (accessed on 19 May 2019).

- Prüser, J.; Schlösser, A. The effects of economic policy uncertainty on European economies: Evidence from a TVP-FAVAR. Empir. Econ. 2019, 58, 2889–2910. [Google Scholar] [CrossRef] [Green Version]

- Brogaard, J.; Detzel, A. The Asset-Pricing Implications of Government Economic Policy Uncertainty. Manag. Sci. 2015, 61, 3–18. [Google Scholar] [CrossRef] [Green Version]

- Goodell, J.W.; Vahama, S. US presidential elections and implied volatility: The role of political uncertainty. J. Bank. Financ. 2013, 37, 1108–1117. [Google Scholar] [CrossRef]

- Goodell, J.W.; McGroarty, F.; Urquhart, A. Political uncertainty and the 2012 US presidential election: A cointegration study of prediction markets, polls and a stand-out expert. Int. Rev. Financ. Anal. 2015, 42, 162–171. [Google Scholar] [CrossRef]

- Pasquariello, P.; Zafeiridou, C. Political Uncertainty and Financial Market Quality. SSRN Electron. J. 2014. [Google Scholar] [CrossRef] [Green Version]

- Cox, J.S.; Griffith, T. Political Uncertainty and Market Liquidity: Evidence from the Brexit Referendum and the 2016 U.S. Presidential Election. SSRN Electron. J. 2017. [Google Scholar] [CrossRef]

- Kido, Y. On the link between the US economic policy uncertainty and exchange rates. Econ. Lett. 2016, 144, 49–52. [Google Scholar] [CrossRef]

- Antonakakis, N.; Chatziantoniou, I.; Filis, G. Dynamic co-movements of stock returns, implied volatility and policy uncertainty. Econ. Lett. 2013, 120, 87–92. [Google Scholar] [CrossRef]

- Arouri, M.; Estay, C.; Rault, C.; Roubaud, D. Economic policy uncertainty and stock markets: Long-run evidence from the US. Financ. Res. Lett. 2016, 18, 136–141. [Google Scholar] [CrossRef]

- Balcilar, M.; Gupta, R.; Kim, W.J.; Kyei, C. The role of economic policy uncertainties in predicting stock returns and their volatility for Hong Kong, Malaysia and South Korea. Int. Rev. Econ. Financ. 2019, 59, 150–163. Available online: https://repository.up.ac.za/handle/2263/68145 (accessed on 15 February 2020). [CrossRef] [Green Version]

- Chang, T.; Chen, W.-Y.; Gupta, R.; Nguyen, D.K. Are stock prices related to the political uncertainty index in OECD countries? Evidence from the bootstrap panel causality test. Econ. Syst. 2015, 39, 288–300. Available online: https://EconPapers.repec.org/RePEc:eee:ecosys:v:39:y:2015:i:2:p:288-300 (accessed on 3 March 2019). [CrossRef] [Green Version]

- Fang, L.; Chen, B.; Yu, H.; Xiong, C. The effect of economic policy uncertainty on the long run correlation between crude oil and the US stock markets. Financ. Res. Lett. 2018, 24, 56–63. [Google Scholar] [CrossRef]

- Kang, W.; Ratti, R.A. Oil shocks, policy uncertainty and stock market return. J. Int. Financ. Mark. Inst. Money 2013, 26, 305–318. [Google Scholar] [CrossRef]

- Kang, W.; Ratti, R.A. Oil shocks, policy uncertainty and stock returns in China. Econ. Transit. 2015, 23, 657–676. [Google Scholar] [CrossRef]

- Kido, Y. The transmission of US economic policy uncertainty shocks to Asian and global financial markets. N. Am. J. Econ. Financ. 2018, 46, 222–231. [Google Scholar] [CrossRef]

- Li, X.; Peng, L. US economic policy uncertainty and co-movements between Chinese and US stock markets. Econ. Model. 2017, 61, 27–39. [Google Scholar] [CrossRef]

- Li, X.-L.; Balcilar, M.; Gupta, R.; Chang, T. The Causal Relationship between Economic Policy Uncertainty and Stock Returns in China and India: Evidence from a Bootstrap Rolling Window Approach. Emerg. Mark. Financ. Trade 2016, 52, 674–689. [Google Scholar] [CrossRef] [Green Version]

- Mei, D.; Zeng, Q.; Zhang, Y.; Hou, W. Does US Economic Policy Uncertainty matter for European stock markets volatility? Phys. A Stat. Mech. Appl. 2018, 512, 215–221. [Google Scholar] [CrossRef]

- Phan, D.H.B.; Sharma, S.S.; Tran, V.T. Can economic policy uncertainty predict stock market returns? Global evidence. J. Int. Financ. Mark. Inst. Money 2018, 55, 134–150. [Google Scholar] [CrossRef]

- Roubaud, D.; Arouri, M. Oil prices, exchange rates and stock markets under uncertainty and regime-switching. Financ. Res. Lett. 2018, 27, 28–33. [Google Scholar] [CrossRef]

- Sum, V. The Impulse Response Function of Economic Policy Uncertainty and Stock Market Returns: A Look at the Eurozone. SSRN Electron. J. 2012, 12, 100–105. [Google Scholar] [CrossRef]

- Sum, V. The Reaction of Stock Markets in the BRIC Countries to Economic Policy Uncertainty in the United States. SSRN Electron. J. 2012. [Google Scholar] [CrossRef]

- Zhang, D.; Lei, L.; Ji, Q.; Kutan, A.M. Economic policy uncertainty in the US and China and their impact on the global markets. Econ. Model. 2019, 79, 47–56. [Google Scholar] [CrossRef]

- Thomas, C. Economic policy uncertainty and stock returns-evidence from the Japanese Market. Quant. Financ. Econ. 2020, 4, 430–458. [Google Scholar]

- Vo, X.V.; Tran, T.T.A. Modelling volatility spillovers from the US equity market to ASEAN stock markets. Pac.-Basin Financ. J. 2020, 59, 101246. [Google Scholar] [CrossRef]

- Arslanturk, Y.; Balcilar, M.; Ozdemir, Z.A. Time-varying linkages between tourism receipts and economic growth in a small open economy. Econ. Model. 2011, 28, 664–671. [Google Scholar] [CrossRef]

- Pesaran, B.; Pesaran, M.H. Time Series Econometrics Using Microfit; OUP Oxford: Oxford, UK, 2009. [Google Scholar]

- Pesaran, M.H.; Shin, Y. An Autoregressive Distributed Lag Modelling Approach to Cointegration Analysis. In Econometrics and Economic Theory in the 20th Century: The Ragnar Frisch Centennial Symposium; Strom, S., Ed.; Cambridge University Press: Cambridge, UK, 1999. [Google Scholar]

- Johansen, S. Estimation and Hypothesis Testing of Cointegration Vectors in Gaussian Vector Autoregressive Models. Econometrica 1991, 59, 1551–1580. [Google Scholar] [CrossRef]

- Davis, S.J. An index of global economic policy uncertainty. Natl. Bur. Econ. Res. Work. Pap. 2016, 22740. Available online: https://ideas.repec.org/p/nbr/nberwo/22740.html (accessed on 15 June 2020).

- Valdés, R.O. Emerging Markets Contagion: Evidence and Theory. SSRN Electron. J. 2000. [Google Scholar] [CrossRef]

- Jarque, C.M.; Berra, A.K. Efficient tests for normality, homoscedasticity and serial independence of regression residuals. Econ. Lett. 1980, 6, 255–259. Available online: https://EconPapers.repec.org/RePEc:eee:ecolet:v:6:y:1980:i:3:p:255-259 (accessed on 15 May 2020). [CrossRef]

- Pesaran, M.H.; Shin, Y.; Smithc, R.J. Bounds testing approaches to the analysis of level relationships. J. Appl. Econ. 2001, 16, 289–326. [Google Scholar] [CrossRef]

- Rejeb, A.B.; Boughara, A. Financial integration in emerging market economies: Effects on volatility transmission and contagion. BorsaIstanb. Rev. 2015, 15, 161–179. [Google Scholar]

- Chambet, A.; Gibson, R. Financial integration, economic instability and trade structure in emerging markets. J. Int. Money Financ. 2008, 27, 654–675. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| JKSE | GEPU | |

|---|---|---|

| Mean | 1.070 | 111.970 |

| Std | 6.498 | 41.324 |

| Skewness | −1.122 | 0.916 |

| Kurtosis | 8.188 | 3.857 |

| JB | 286.250 * | 36.783 * |

| Unconditional correlation between JKSE and GEPU | −0.147 ** (−2.170) | |

| ADF (Constant) | −11.689 * | −3.947 ** |

| DF (Structural Break) | 13.536 * | 5.720 * |

| ARCH (2) LM Test | 3.391 ** | 4.532 ** |

| Mean | Std | Skewness | Kurtosis | JB | |

|---|---|---|---|---|---|

| Rolling Correlation | −0.1633 | 0.1997 | −0.0253 | 1.8647 | 9.9869 |

| Variable | Mean | Std | Skewness | Kurtosis | JB |

|---|---|---|---|---|---|

| DCC | −0.168328 | 0.1154 | −0.567098 | 2.530553 | 12.30539 |

| Parameter | Estimate | Standard Error | T-Ratio [Prob] |

|---|---|---|---|

| 0.92448 | 0.025413 | 36.3783[0.00] | |

| 0.98549 | 0.0095123 | 103.6013[0.00] | |

| Δ | 0.97543 | 0.025228 | 38.6644[0.00] |

| Dof | 5.3871 | 1.3321 | 4.0440[0.00] |

| Variable | Augmented Dickey−Fuller Test | Dickey–Fuller Test with Structural Break | ||

|---|---|---|---|---|

| Level | 1st Difference | Level | 1st Difference | |

| −0.1424 | −11.350 * | −5.787 * | −14.823 * | |

| −2.279 | −10.611 * | −4.356 | −11.196 * | |

| −2.797 | −3.019 | −4.013 | −21.352 * | |

| −2.871 | −12.537 * | −3.969 | −14.169 * | |

| 1% Critical values | −4.006 | −4.006 | −5.347 | −5.347 |

| Model 1 | Model 2 | Model 3 | ||||

|---|---|---|---|---|---|---|

| Calculated F Statistic | 4.548 | 4.008 | 4.629 | |||

| Significance Level | Pesaran et al. (2001) [87] | Pesaran et al. (2001) [87] | Pesaran et al. (2001) [87] | |||

| LB | UB | LB | UB | LB | UB | |

| 1 percent | 3.29 | 4.37 | 3.29 | 4.37 | 3.29 | 4.37 |

| 5 percent | 2.56 | 3.49 | 2.56 | 3.49 | 2.56 | 3.49 |

| 10 percent | 2.2 | 3.09 | 2.2 | 3.09 | 2.2 | 3.09 |

| Variable | Model 1 | Model 2 | Model 3 |

|---|---|---|---|

| Constant | 15.344 (2.281) ** | 17.528(2.558) ** | 17.479(2.572) ** |

| 1.862(4.094) ** | 2.075(3.821) ** | 2.051(3.794) ** | |

| 0.30(6.293) ** | 0.311(6.341) ** | 0.306(6.329) ** | |

| −0.892(−4.185) ** | −0.941(−4.126) ** | −0.935(−4.010) ** | |

| 1.691(3.571) ** | 1.461(2.530) ** | 1.450(2.720) ** |

| Variable | Model 1 | Model 2 | Model 3 |

|---|---|---|---|

| 0.189(2.73) ** | 0.167(2.353) ** | 0.169(2.421) ** | |

| −0.829(−2.489) ** | −0.761(2.297) ** | −0.779(−2.359) ** | |

| 0.380(0.938) | 0.406(1.004) | 0.392(0.974) | |

| −0.830(−2.360) ** | −0.801(−2.282) ** | −0.807(−2.303) ** | |

| −0.259(−0.984) | −0.242(−0.920) | −0.248(−0.948) | |

| −0.048(−0.186) | −0.026(−0.10) | −0.030(−0.117) | |

| −0.666(−2.755) ** | −0.632(−2.617) ** | −0.638(−2.650) ** | |

| 0.018(0.073) | 0.041(0.169) | 0.035(0.144) | |

| −0.730(−3.118) ** | −0.685(−2.920) ** | −0.696(−2.971) ** | |

| −0.442(−2.720) ** | −0.423(−2.611) ** | −0.432(−2.682) ** | |

| 0.412(2.132) ** | 0.420(2.179) ** | 0.416(2.165) ** | |

| −0.281(−1.685) | −0.272(−1.641) | −0.273(−1.647) | |

| −0.003(−2.166) ** | |||

| 0.002(0.518) ** | |||

| −0.008(−1.891) | −0.006(−2.055) ** | ||

| −0.004(−2.459) ** | −0.004(−2.494) ** | ||

| −0.115(−5.300) ** | −0.114(−4.977) ** | −0.115(−5.348) ** | |

| 0.22 | 0.23 | 0.23 | |

| DW | 2.03 | 2.02 | 2.04 |

| F statistic LM test | 0.69[0.69] | 0.552[0.7] | 0.62[0.65] |

| F statistic ARCH test | 3.331[0.012] | 3.15[0.02] | 3.098[0.02] |

| F statistic Ramsey RESET test | 0.809[0.6] | 1.091[0.372] | 1.032[0.414] |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hashmi, S.M.; Gilal, M.A.; Wong, W.-K. Sustainability of Global Economic Policy and Stock Market Returns in Indonesia. Sustainability 2021, 13, 5422. https://doi.org/10.3390/su13105422

Hashmi SM, Gilal MA, Wong W-K. Sustainability of Global Economic Policy and Stock Market Returns in Indonesia. Sustainability. 2021; 13(10):5422. https://doi.org/10.3390/su13105422

Chicago/Turabian StyleHashmi, Shabir Mohsin, Muhammad Akram Gilal, and Wing-Keung Wong. 2021. "Sustainability of Global Economic Policy and Stock Market Returns in Indonesia" Sustainability 13, no. 10: 5422. https://doi.org/10.3390/su13105422

APA StyleHashmi, S. M., Gilal, M. A., & Wong, W. -K. (2021). Sustainability of Global Economic Policy and Stock Market Returns in Indonesia. Sustainability, 13(10), 5422. https://doi.org/10.3390/su13105422