1. Introduction

From a financial perspective, the relationship sustainability of firms is closely related to effective supplier management to achieve a stable production structure and sustainable business relationships. In the stock market, many company stakeholders face information asymmetry, having access to different levels of data. For example, investors who have difficulty accessing business information and management who can easily access it face the issue of adverse selection [

1,

2], which is hiding information, and the signaling effect, which is providing information actively [

3,

4].

Overall, the success and failure of a company’s new product development (NPD) can affect the rise and fall of corporate value. If the NDP cost is greater than the effect of sales increases due to a new product launch (NPL), the company’s profit may decrease and its short-term corporate value may decline. However, for the corporate strategy to maximize corporate value, continuous new product preannouncement (NPP) accumulates brand and customer assets, leading to long-term profits and increasing corporate value.

NPP refers to a planned communication in which a company provides consumers with information such as price, quality, and release date before launching a new product [

5]. Moreover, as a strategic signal for companies to influence the behavior of stakeholders, such as competitors, customers, investors, and suppliers, NPP is an effective means of deterring competitors from entering the market and providing information to potential customers and investors [

6,

7]. Research on the effect of NPP on corporate value is being conducted in two directions: the direct effect in which NPP increases corporate value by enhancing financial performance and the signaling effect that influences investors to increase corporate value. Meanwhile, the impact of the NPP signaling effect on corporate value is a change in investors’ perception of future cash flows [

8]. Additionally, the factors that continuously affect the signaling effect of NPP include reliable information [

9,

10], the specificity of NPP content [

11], high innovation capacity [

12], and adequate spare resources [

13].

Apple—the leading American information technology company—is famous for not releasing any information about a new product before the official announcement event. Apple’s “secret marketing” strategy enjoys maximum effectiveness without advertising, which is possible thanks to its strong brand power and consumer loyalty. Thus, creative products such as the iPhone break market expectations, change the rules of the game, and create a new ecosystem to wow consumers. However, more than 10 years have passed since Apple’s iPhone launch, and few papers have studied the market response for parts suppliers according to the type of investors in the stock market. Therefore, this study examined the effects of signaling the selection and elimination of partnerships for Apple’s parts suppliers from 2007 to 2018 at times of NPP. The mid- to long-term stock price reactions were also analyzed to understand trading patterns by investor type. Moreover, through logit regression analysis, factors influencing the retention or elimination of the partners were analyzed.

The specific purposes of this paper are as follows: first, we examine whether the short-term signaling effect at the time of NPP is useful investment information by dividing the Apple iPhone parts suppliers into new, old, and revocation partners. Second, we examine investment performance through mid- to long-term stock price changes before and after the selection or elimination of Apple’s parts suppliers; this will be investigated through the analysis of the cumulative excess return for 60 trading days and the buy and hold abnormal return (BHAR) for six months, before and after the disclosure of the parts suppliers. Third, by analyzing the trading pattern of each investor type for 40 trading days before and after the partner selection by classifying investors into individuals, institutions, and foreigners, this study identifies whether there is information asymmetry in the selection or elimination of partners and examines whether there are differences by country (the United States (US), Taiwan, Japan, and South Korea).

As described above, this study is different from prior research in that it measures the long- and short-term signaling effect of Apple’s NPP strategy under which a new iPhone model is introduced annually and the parts suppliers that are investigated are expanded to the US, Taiwan, Japan, and South Korea to analyze their trading pattern by investor type in the market.

2. Literature Review

2.1. Information Asymmetry

In capital markets, business stakeholders have different levels of information. There is information asymmetry in which the management of a company has an information advantage over investors who have an information disadvantage, resulting in different levels of information access between the parties. Additionally, such information asymmetry leads to adverse selection and the signaling effect. The difference between the adverse selection and signaling theories, which assume information asymmetry, is that the one with more information tends to hide the information in the former case and tries to reveal more information in the latter case. Adverse selection refers to the problem of making an adverse choice when investors are not aware of information that the management already has, and this can also be found in corporate NPPs. Contrary to the adverse selection that arises from hidden information, the signaling effect provides information voluntarily at the expense of the company. With signaling, companies with superior information deliver information to investors who have insufficient information. This is often used as an NPP strategy [

8]. Therefore, information on a company’s NPD creates a strong signaling effect for investors; this means that when a company pursues NPD, information about partner change is being used as a useful signal to investors.

Prior research on NPP includes studies on the timing of NPP [

8], on the content of NPP [

14,

15], and on the effects of NPP [

6,

11]. Among studies on the effect of NPP, Sorescu et al. [

11] viewed NPP as a strategic signal sent to stakeholders, such as investors, shareholders, and suppliers, and proved through an empirical method that companies providing specific information about their products had higher short-term excess returns. In addition, they argued that the continuous provision of new information on the progress of the NPP increases reliability as well as the long-term excess return. Warren and Sorescu [

16] found that recurring NPP strategies reflected positive investor expectations for the company’s future performance, analyzing a sample of 4845 from 826 American companies.

2.2. Relationship between NPP and Corporate Value

For marketing strategies such as NPP, research that estimates corporate value using the event study methodology is being actively undertaken [

11,

17,

18]. For example, Sorescu et al. [

11] argued that investors responded positively to the specificity and reliability of the NPP content in terms of the announcement effect of NPP. Sood and Tellis [

17] revealed, through an empirical analysis, that NPP had the highest return and NPL had the lowest return in the innovative announcement effect of each phase of NPD, NPP, and NPL. Borah and Tellis [

18] found that in the announcement effect, which classified innovative new products into direct production (make), external purchase (buy), and alliance (ally), investors responded positively to direct production (make) and alliance (ally) but negatively to external purchase (buy).

NPP enhances corporate value by increasing sales and profits and acts as a direct signal to inform investors. Under information asymmetry, the NPP signaling effect is that the information provided by the management who has information advantage on a new product to investors who have information disadvantage is recognized as a sign of changes in financial performance and reflected in the stock price. As a corporate value, the NPP signaling effect is identified as a change in investors’ perception of the future cash flows of a company [

8,

19]. Furthermore, factors that continuously and positively affect the NPP signaling effect include reliable information [

10,

20], the specificity of NPP content [

11], high innovation capacity [

12], and adequate spare resources [

13].

In the smartphone industry, adverse selection may occur when information asymmetry exists between a company that announces a new product and investors in its parts supplier; this is because the management has information about a new and innovative product and investors do not. Therefore, the investor assumes that NPP is done only when the management has positive information about innovation. Investors will then invest in new companies that enter the market or have new technologies, which, in turn, will lead to NPP when companies actually think that new products are highly innovative. Consequently, the greater the signaling effect of information about new partners provided by NPP, the greater the investor’s excess return on the information [

11].

3. Materials and Methods

3.1. Data Collection

This study targets parts suppliers who participated in the NPP events for Apple iPhone series products between 2007 and 2018, and the detailed data collection method is as follows. Data were collected based on the supplier list provided in Apple’s annual report as well as based on the vendors list disclosed by Apple. Additionally, to identify parts suppliers only for iPhone, parts suppliers were identified through a website that provided technical information for individual parts after disassembling smartphones.

The final sample selected according to these criteria had 1104 parts suppliers of Apple. In detail,

Table 1 shows the results of classifying all parts suppliers that participated in manufacturing new iPhone products for 13 years from 2007 to 2018 by country. There are 92 Apple iPhone parts suppliers on average, and except for the eight Korean companies that supply core parts, they are evenly distributed among different countries with 30 US companies, 27 Taiwanese companies, and 27 Japanese companies.

From 2007 to 2018, companies that were newly selected as a parts supplier for the year as alliance partners of the Apple iPhone were categorized as “new,” and companies that remained as partners after being selected as partners in the previous year were classified as “old.” Companies that were eliminated from the partner list, although they had been selected as partners in the previous year, were categorized as “revoked” in

Table 2. Stock price data and financial data necessary for this study are collected in the following way. Stock prices and financial data of the American, Taiwanese, and Japanese companies were collected from OSIRIS DB and those of Korean companies were collected from KISVALSE and FnGuide.

In this study, the stock price and event date of parts suppliers were classified based on the following criteria. First, adjusted stock prices were used for daily closing prices to maintain the continuity of stock price as there may be discrepancies between past closing stock prices before ex-rights dates and the current prices after ex-rights dates due to market factors such as capital increase with or without consideration, dividends, and stock split. Second, the event dates were adjusted by applying time differences for each country (the US, Taiwan, Japan, and South Korea) based on the preannouncement dates of Apple’s new iPhone. Third, if an event date was not a stock trading date, it was excluded from the sample. Fourth, if the stock price data was less than the estimated period based on the date of the event, it was excluded from the sample.

3.2. Methodology

For this study, we conducted a case study using the market model to estimate and test excess returns. For the estimation of the excess return, regression coefficient (

) of a company’s stock

was estimated according to the OLS of Equation (1) using daily stock price data from −170 to −6 days. Then, we set the period from −5 days to +5 days as event days, which may be influenced by the event, and the change in excess returns was observed. Moreover, the average abnormal return (AAR) and cumulative average abnormal return (CAR) for N sample companies are calculated as Equations (2) and (3) by summing the daily average excess return for the relevant period [

20].

here,

: Individual company i’s return on day

t.

: The market index returns on day

t.

Furthermore, the BHAR model is calculated as Equation (4).

here,

: excess returns in

day(s) for

company stock.

: Individual company i’s return on day t.

: The market index returns on day t.

Additionally, Equation (5) is a model for analyzing the trading patterns by investor type (individual, institutional, and foreign investors) before and after the time of NPP.

here,

:

Daily net purchase ratio by the investor in

day(s).

: Net purchase quantity by investor type (individual, institutional, and foreign) in day(s).

: Number of shares issued in day(s).

4. Results and Discussion

4.1. The Signaling Effects of New, Old, and Revocation Partners

This study analyzed the signaling effects through excess returns by categorizing Apple iPhone parts suppliers into new, old, and revocation partners for 13 years from 2007 to 2018. The results are shown in

Table 3; the table shows excess returns for five days before and after the NPP date for each company selected as Apple’s iPhone parts suppliers categorized as new, old, and revocation partners. First, the excess return of new partners was statistically significant at 1.81% on the event date (t = 0) and had a positive effect on the stock price of the companies. The excess return of the old partners was 0.78% on the date of the event (t = 0), which was also significant at the 10% level. However, the partners that were eliminated from Apple’s partner list showed a negative excess return of −1.11%. This can be interpreted as having a signaling effect that the market perceives being selected as or eliminated from Apple parts suppliers as either positive or negative information in the short term. This implies the NPP of Apple, which uses a secret marketing strategy in the stock market where information asymmetry exists, provides useful information to investors in the short term.

4.2. Signaling Effect by Country

Table 4 demonstrates the analysis results of the signal effect through the excess returns by classifying the parts suppliers of the Apple iPhone by country. Apple’s parts suppliers were divided by country to indicate the excess return for five days before and after the new product preannouncement of an iPhone model. First, the excess return of the US companies was statistically significant at 1.71% on the event date (t = 0) and had a positive effect on the stock price of the companies. The excess returns of Taiwanese companies were 1.61% on the day after the event (t = 1), 1.33% for Japanese companies on the day after the event (t = 1), and 1.87% on the day after the event (t = 1) for Korean companies. They were statistically significant and showed positive market reactions. This can be interpreted as a positive signaling effect in the short term, considering the time difference in the stock markets of the US and Asia (Taiwan, Japan, and South Korea). Interestingly, it was observed that the order of the signal effect was South Korea, the US, Taiwan, and Japan.

4.3. Mid- to Long-Term Stock Price Changes before and after Partner Selection or Revocation

Table 5 illustrates the analysis results of the mid- to long-term stock price changes before and after Apple iPhone partner selection in addition to retention and revocation through CAR and BHAR. The table shows the CAR for 60 trading days before and after the partner selection and revocation of iPhone parts suppliers by period, and calculated the BHAR for three and six months before and after the partner selection.

First, the results of partner selection, retention, and revocation in Panel A showed that values of CAR for 60 days before the selection had no significance in all sections of the period for new partners and these companies experienced drops in stock prices before the selection. The case of BHAR (−3 months) and BHAR (−6 months) were statistically significant at 2.65% and 3.34%, respectively, thereby indicating that companies with higher investment performance have been newly selected as Apple’s partners. This implies that these companies had exerted efforts to increase corporate value through technology development. Meanwhile, reselected companies generally showed positive CAR before the selection, and BHAR (−3 months) and BHAR (−6 months) were also statistically significant at 1.47% and 2.82%, respectively. Additionally, companies that had been eliminated showed continuous drops in the stock price movement before the selection day.

Next, Panel B shows that values of CAR 60 days after the selection, retention, and revocation had significance in all sections of the period for new partners. After the selection, these companies experienced a rise in stock prices. BHAR (+3 months) and BHAR (+6 months) were statistically significant at 3.85% and 7.24%, respectively, thereby indicating that companies with higher investment performance compared to the market have been newly selected as Apple’s partners. This is the result of cultivating positive responses in the market by applying new technologies developed by new partners. Meanwhile, reselected companies generally showed positive CAR after the selection, and BHAR (+3 months) and BHAR (+6 months) were also statistically significant at 2.64% and 3.21%. The companies eliminated from the partnership had a negative market reaction in the stock price movement, continuously declining compared to the market.

In general, the positive (+) excess return appeared for new and old partners, and the negative (−) excess return appeared for revoked partners. These results suggest that companies that have been selected or retained as Apple’s partners show significant investment results in the future. Particularly, in the case of new partners, the low excess return before the selection turned to high investment performance after the selection. This implies that the new partners meet the expectations of the market.

4.4. Analysis of Trading Patterns by Investor Type before and after Partner Selection, Retention, and Revocation

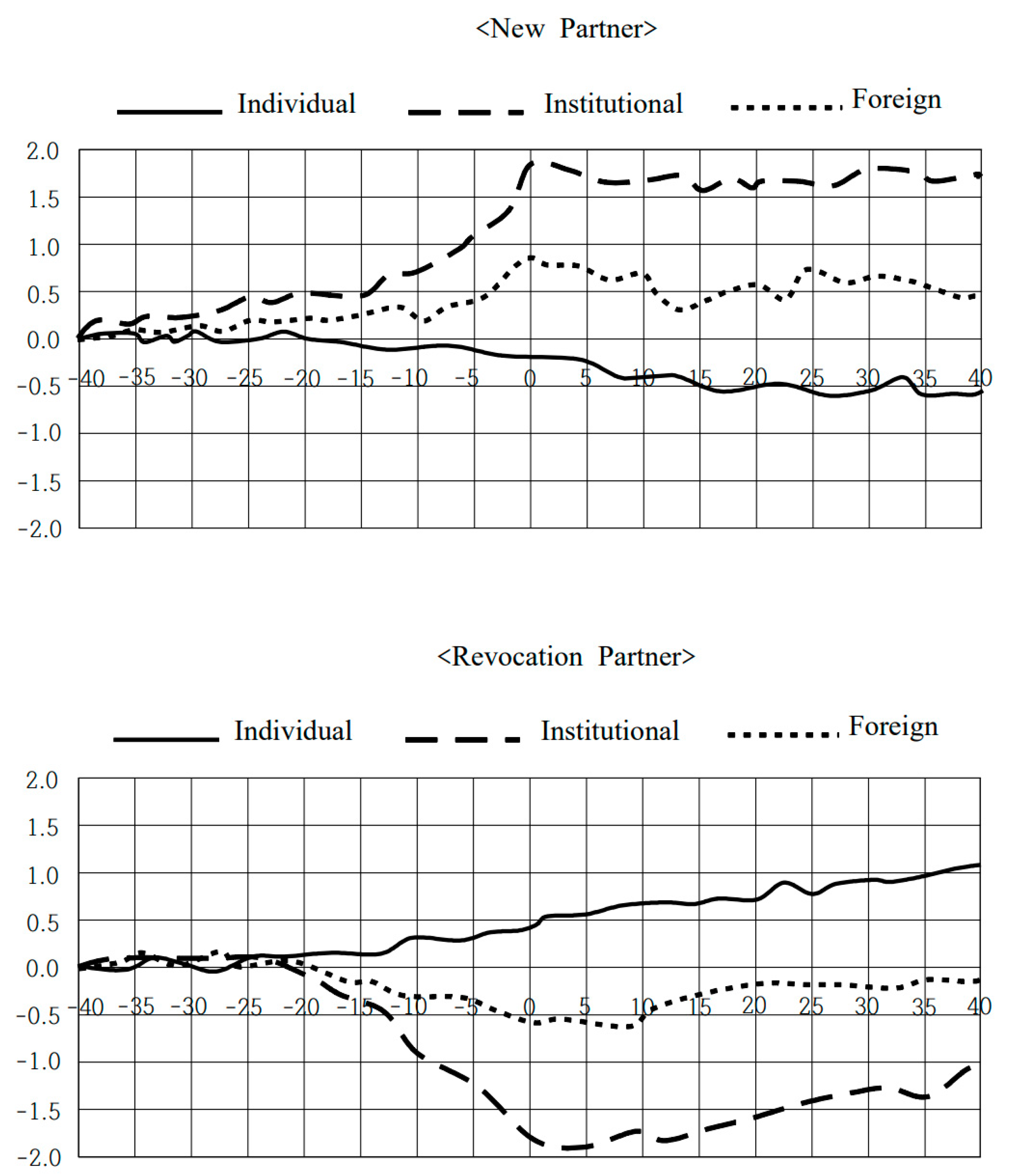

Figure 1 illustrates the analysis result of the trading patterns by each investor type categorized as individual, institution, and foreigner before and after Apple’s partner selection, retention, and revocation.

First, the trading pattern of each investor type for 40 trading days before and after selection and revocation showed that individual investors’ trading pattern is characterized as net selling, institutional investors as net buying, and foreign investors as net buying. Considering that newly selected companies had maintained high investment performance for a long time prior to the selection and that the announcement of new partner selection resulted in a positive excess return, these results indicate that institutional investors and foreigners have favorable trading outcomes while individual investors experience a negative outcome. Similarly, in the case of revocation partners, individual investors showed a net buying pattern while institutional and foreign investors showed a net selling pattern. Individual investors still presented a disadvantageous trading pattern compared to institutional and foreign investors.

These results can be explained by the information asymmetry between individual investors and foreign and institutional investors related to Apple’s partner selection. In other words, institutions and foreign investors have the power of information that the companies that have steadily increased their corporate value through new technology but are not widely known in the market are likely to be selected as new partners. As a result, they net buy in the stock market by recognizing the value of these companies. Conversely, individual investors with less information advantage net sell corresponding to contrarian trading behavior in the process of rising stock prices. In contrast, for revocation partners, the declined stock price in the process of selling the stock by institutional investors, who judged that the company’s technological power and corporate value do not meet the selection criteria, were seen as an opportunity to buy for individual investors.

5. Conclusions

This paper confirmed the signal effects of Apple iPhone partner selection by analyzing the excess returns by dividing each of Apple’s parts suppliers from 2007 to 2018 into new, old, and revocation partners by country. In addition, mid- to long-term stock price movements before and after the selection of partners were analyzed through the cumulative excess return and BHAR. In addition, the trading patterns of each investor before and after the selection of a partner were identified based on the cumulative net purchase rate for individuals, institutions, and foreigners, and factors influencing the selection of new partners were identified through logit regression analysis. The results are as follows:

First, in the case of the newly selected Apple parts suppliers, the excess return on the day of the NPP (t = 0) was 1.81%, whereas that of the eliminated companies was −1.1%. It was confirmed that the selection or the revocation had either a positive or negative signaling effect on the stock market in the short term. In the classification by country, the stock price has continued to rise since the NPP, although the increase rate is rather small. The excess returns were in the order of South Korea (1.87%), the US (1.71%), Taiwan (1.61%), and Japan (1.33%), which is interpreted as having a positive signaling effect.

Second, the analysis result of mid- to long-term stock price changes before and after partner selection, retention, and revocation through CAR and BHAR showed a drop in stock prices for revocation partners. In the case of new partners, the stock prices rose after the selection. This is the result of cultivating positive responses in the market by applying new technologies developed by new partners. It also suggests that the stock price movement before and after the NPP is an important factor in the selection or revocation of partners. In addition, the mid- to long-term excess returns after partner selection or revocation, companies that have been selected as or eliminated from hidden champions generally show clear investment performance.

Third, in the analysis of trading patterns by investor type, before the new selection and retention and revocation of partners, individual investors showed net selling and institutional and foreign investors showed net buying patterns for the newly selected. Conversely, in the case of revocation partners, individual investors showed net buying and foreign and institutional investors showed net selling patterns, revealing a relatively unfavorable trading pattern for individual investors. In contrast, after the selection, retention and revocation of partners, institutional and foreign investors showed a preference for the newly selected by net buying stocks of the newly selected and net selling that of the eliminated. However, individual investors showed a contrarian pattern in which they net sold the stocks of new partners of which stock prices have increased while net buying that of revocation partners of which stock prices have dropped.

The results of this study as described above suggest several important implications in selecting the partners of a company. First, it suggests that companies selected as new partners have a signaling effect as useful information in the market. In addition, it is significant in that it shows clear investment outcomes after the selection. Meanwhile, the country-by-country analysis confirmed that stock prices in the US and Asian countries continued to rise after the NPP date and the day after. Individual investors net sold the stocks of new partners that had been displaying high investment performance before the partner selection, and net purchased those of the revoked partners, which had been showing sluggish movement in the market, even before the selection. This is an opposite and unfavorable trading pattern to that of institutional and foreign investors. This suggests that information asymmetry exists between individual investors and institutional and foreigners regarding partner selection.

Author Contributions

Conceptualization, I.S. and S.K.; methodology, I.S.; validation, I.S. and S.K.; formal analysis, I.S.; data curation, I.S.; writing—original draft preparation, I.S.; writing—review and editing, S.K.; visualization, S.K.; supervision, S.K.; project administration, S.K.; funding acquisition, I.S. All authors have read and agreed to the published version of the manuscript.

Funding

This work was supported by the Ministry of Education of the Republic of Korea and the National Research Foundation of Korea (NRF-2018S1A5B5A07072352).

Data Availability Statement

The data that support the findings of this study are available from the corresponding author, upon request.

Acknowledgments

The authors would like to thank the anonymous reviewers and handling editors for their constructive comments that greatly improved this article from its original form.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Bonnie, F.V.N.; Robert, A.V.N.; Richard, S.W. How well do adverse selection components measure adverse selection? Financ. Manag. 2001, 30, 77–98. [Google Scholar]

- Su, D. Adverse-selection versus signaling: Evidence from the pricing of Chinese IPOs. J. Econ. Bus. 2004, 56, 1–19. [Google Scholar]

- Ross, S. The determination of financial structure: The incentive-signalling approach. Bell J. Econ. 1977, 8, 23–40. [Google Scholar] [CrossRef]

- Kumar, S. Partner characteristics, information asymmetry, and the signaling effects of joint ventures. Manag. Decis. Econ. 2012, 33, 127–145. [Google Scholar] [CrossRef]

- Bayus, B.; Jain, S.; Rao, A. Truth or consequences: An analysis of vaporware and new product announcements. J. Mark. Res. 2001, 3, 3–13. [Google Scholar] [CrossRef] [Green Version]

- Robertson, T.; Eliashberg, J.; Rymon, T. New product announcement signals and incumbent reactions. J. Mark. 1995, 5, 1–15. [Google Scholar] [CrossRef]

- Son, I.; Kim, S. Does partner volatility have firm value relevance? An empirical analysis of part suppliers. Sustainability 2018, 10, 763. [Google Scholar] [CrossRef] [Green Version]

- Su, M.; Rao, V.R. Timing decisions of new product preannouncement and launch with competition. Int. J. Prod. Econ. 2011, 129, 51–64. [Google Scholar] [CrossRef]

- Mishra, D.P.; Bhabra, H.S. Assessing the economic worth of new product pre-announcement signals: Theory and empirical evidence. J. Prod. Brand Manag. 2001, 10, 75–93. [Google Scholar] [CrossRef]

- Lee, R.P.; Chen, Q.; Hartmann, N.N. Enhancing stock market return with new product preannouncements: The role of information quality and innovativeness. J. Prod. Innov. Manag. 2016, 33, 455–471. [Google Scholar] [CrossRef]

- Sorescu, A.; Shankar, V.; Kushwaha, T. New product preannouncements and shareholder value: Don’t make promises you can’t keep. J. Mark. Res. 2007, 44, 468–489. [Google Scholar] [CrossRef]

- Daniel, P.; Pervaiz, K.A. Relationships between innovation stimulus, innovation capacity and innovation performance. R D Manag. 2006, 36, 499–515. [Google Scholar]

- Voss, G.B.; Sirdeshmukh, D.; Voss, Z.G. The effects of slack resources and environmental threat on product exploration and exploitation. Acad. Manag. J. 2008, 51, 147–164. [Google Scholar] [CrossRef] [Green Version]

- Popma, W.T.; Waarts, E.; Wierenga, B. New product announcements as market signals: A content analysis in the DRAM chip industry. Ind. Mark. Manag. 2006, 35, 225–235. [Google Scholar] [CrossRef] [Green Version]

- Homburg, C.; Bornemann, T.; Totzek, D. Preannouncing pioneering versus follower products: What should the message be? J. Acad. Mark. Sci. 2009, 37, 310–327. [Google Scholar] [CrossRef]

- Warren, N.; Sorescu, A. When 1 + 1 > 2: How investors react to new product releases announced concurrently with other corporate news. J. Mark. 2017, 81, 64–82. [Google Scholar] [CrossRef]

- Sood, A.; Gerard, J.T. Do innovations really pay off? Total stock market returns to innovation. Mark. Sci. 2009, 28, 442–456. [Google Scholar] [CrossRef]

- Borah, A.; Gerard, J.T. Make, Buy, or Ally? Choice of and Payoff from Announcements of Alternate Strategies for Innovations. Mark. Sci. 2014, 33, 114–133. [Google Scholar] [CrossRef] [Green Version]

- Koku, P.S.; Aigbe, A.; Thomas, M.S.C. The financial impact of boycotts and threats of boycott. J. Bus. Res. 1997, 40, 15–20. [Google Scholar]

- Brown, S.J.; Warner, J.B. Measuring security price performance. J. Financ. Econ. 1985, 8, 205–258. [Google Scholar] [CrossRef]

| Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

{kind=link}