Examining Factors Influencing Early Paid Over-The-Top Video Streaming Market Growth: A Cross-Country Empirical Study †

Abstract

:1. Introduction

2. Literature Review

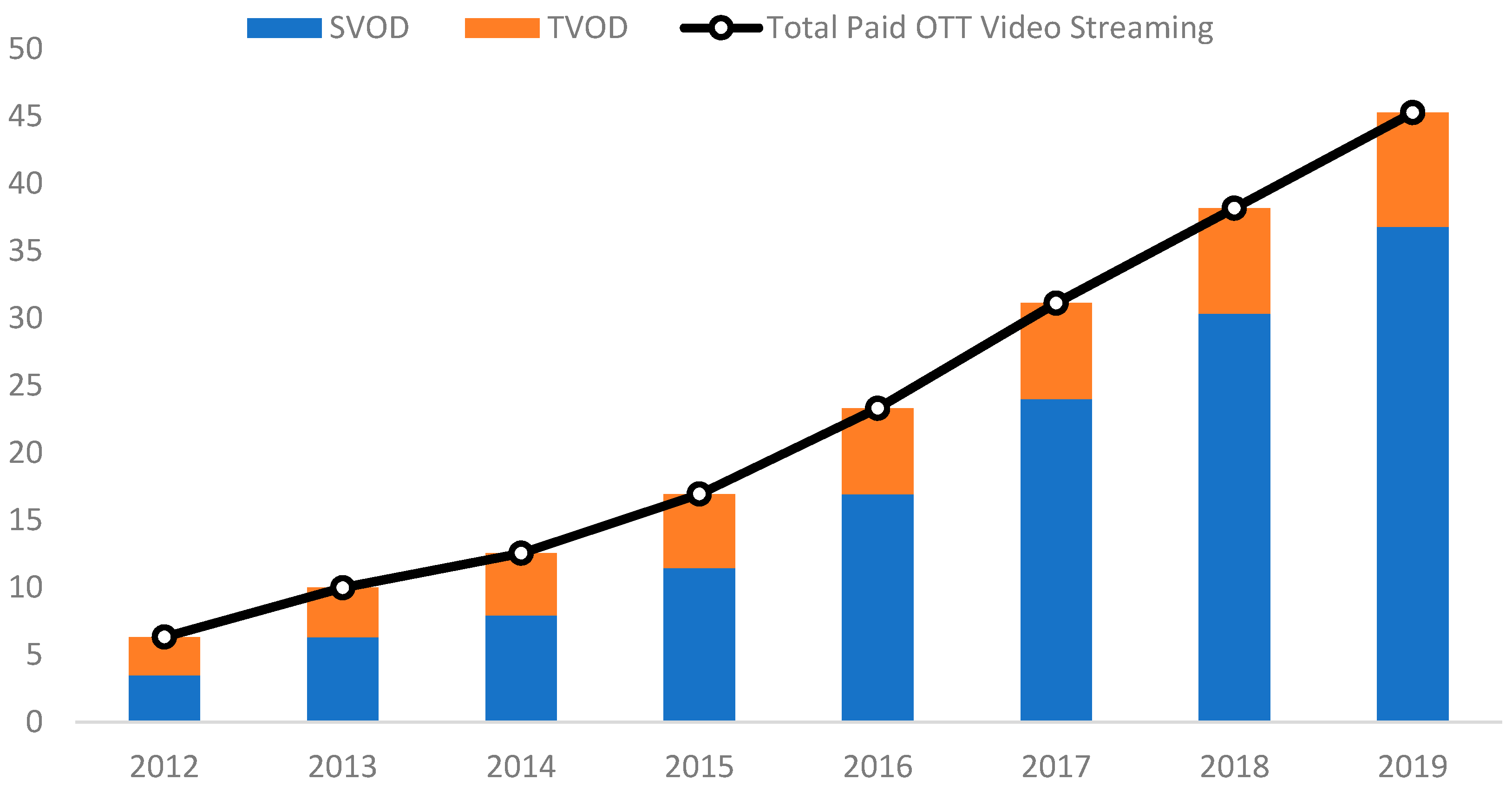

2.1. Global OTT Video Streaming Market Growth

2.2. Complementary Goods and Substitutional Goods

- RQ1:

- Has the paid OTT video streaming market growth rate influenced the traditional pay TV subscription revenue growth rate?

2.3. Market Entry and Growth–Netflix Effect

- RQ2:

- Has Netflix’s market entry positively influenced paid OTT video streaming market growth?

- RQ3:

- Has Netflix’s market entry negatively influenced the pay TV subscription revenue growth rate?

2.4. Broadband Infrastructure and OTT Video Streaming Market Growth

- RQ4:

- Does broadband infrastructure positively influence paid OTT video market growth?

2.5. Market Environmental Factors–Competition, Concentration and Pay TV Market Size

- RQ5:

- Does platform competition among paid OTT types influence paid OTT video streaming market growth?

- RQ6:

- Does pay TV/OTT platform market concentration influence the pay TV subscription revenue growth rate?

- RQ7:

- Does the pay TV market size positively influence paid OTT video streaming market growth?

3. Research Method

3.1. The Paid OTT Video Streaming Market Growth Model

3.2. Traditional Pay TV Subscription Revenue Growth Rate Model

3.3. Measurement and Data Sources

4. Results

5. Discussion and Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Federal Communication Commission. Annual Assessment of the Status of Competition in the Market for the Delivery of Video Programming; MB Docket No. 07-269, FCC 12-81; Federal Communication Commission: Washington, DC, USA, 2012.

- International Data Corporation. Digital Transformation (DX): An Opportunity and an Imperative; IDC: Needham, MA, USA, 2015. [Google Scholar]

- PwC. PwC Global Entertainment and Media Outlook 2019–2024; PwC: London, UK, 2019. [Google Scholar]

- DMR. Netflix Statistics. 2020. Available online: https://www.digitaltvresearch.com/ugc/press/235.pdf (accessed on 28 November 2020).

- Statista Estimated Number of SVOD Subscribers Worldwide in 2020 and 2025, by Service. 2020. Available online: https://www.statista.com/statistics/1052770/global-svod-subscriber-count-by-platform/ (accessed on 2 March 2020).

- Body of European Regulators for Electronic Commerce. Report on OTT Services; BEREC: Riga, Latvia, 2015. [Google Scholar]

- European Union. Over-The Top Players (OTTs); EU: Brussels, Belgium, 2015. [Google Scholar]

- Frieden, R. Next-Generation television and the migration from channels to platforms. In Policy and Marketing Strategies for Digital Media; Liu, Y., Picard, R., Eds.; Routledge: New York, NY, USA, 2014; pp. 60–72. [Google Scholar]

- OECD. Competition Issues in Television and Broadcasting; OECD: Paris, France, 2013. [Google Scholar]

- Ampere Analysis. The UK VOD Market. 2019. Available online: https://www.ofcom.org.uk/__data/assets/pdf_file/0026/149075/ampere-analysis-current-status-future-development.pdf (accessed on 2 January 2020).

- Joo, H.M.; Lee, S. A Study of Factors Affecting Intention to Use Subscription VOD and Paid Advertising VOD. Inf. Soc. Media 2019, 20, 57–92. [Google Scholar]

- World Economic Forum. Digital Transformation Initiative. 2017. Available online: http://reports.weforum.org/digital-transformation/platform-economy (accessed on 23 December 2019).

- Statista Netflix Passes 200 Million Milestone. 2021. Available online: https://www.statista.com/chart/3153/netflix-subscribers/ (accessed on 31 March 2021).

- Statista Video Content Budget of Netflix Worldwide from 2013 to 2020. 2021. Available online: https://www.statista.com/statistics/707302/netflix-video-content-budget/ (accessed on 31 March 2021).

- Statista Netflix Surpasses Major Cable Providers in the U.S. 2017. Available online: https://www.statista.com/chart/9799/netflix-vs-cable-pay-tv-subscribers (accessed on 23 December 2019).

- OVUM. 2017: The Year of Peak Triple-Play in the US; OVUM: London, UK, 2017. [Google Scholar]

- PwC. PwC Global Entertainment and Media Outlook 2017–2012; PwC: London, UK, 2017. [Google Scholar]

- Jang, S.; Park, M. Do new media substitute for old media?: A panel analysis of daily media use. J. Media Econ. 2016, 29, 73–91. [Google Scholar] [CrossRef]

- Lee, S.; Lee, S.; Chan-Olmsted, S.M. An empirical analysis of tablet PC diffusion. Telemat. Inform. 2017, 34, 518–527. [Google Scholar] [CrossRef]

- Nie, N.H.; Hillygus, D.S. The impact of internet use on sociability: Time-diary findings. IT Soc. 2002, 1, 1–20. [Google Scholar]

- Tokunaga, R. An examination of functional difficulties from Internet use: Media habit and displacement theory explanations. Human Commun. Res. 2016, 12, 339–370. [Google Scholar] [CrossRef]

- Seo, S. Convergence and diversification in cable industry: An empirical analysis of the deployment pattern of cable telephony in US local telecommunications markets. Telecommun. Policy 2008, 32, 145–155. [Google Scholar] [CrossRef]

- Antonelli, C. A regulatory regime for innovation in the communications industries. Telecommun. Policy 1997, 21, 35–45. [Google Scholar] [CrossRef]

- Koski, H.; Kretschmer, T. Entry, standards and competition: Firm strategies and the diffusion of mobile telephony. Rev. Industrial Organ. 2005, 26, 89–113. [Google Scholar] [CrossRef] [Green Version]

- Economides, N. The economics of networks. Int. J. Ind. Organ. 1996, 14, 673–699. [Google Scholar] [CrossRef]

- Bourreau, M.; Dogan, P. Service-based vs. facility-based competition in local access networks. Inf. Econ. Policy 2004, 16, 287–306. [Google Scholar] [CrossRef]

- Youzhuo, Z.; Jiesheng, F.; Wong, M.; Stewart, S. The “catfish effect” of the private sector on the economy of the people’s republic of China. J. Enterprising Cult. 1996, 4, 331–349. [Google Scholar] [CrossRef]

- Gomez-Uribe, C. The Netflix recommender system: Algorithms, business value, and innovation. ACM Trans. Manag. Inf. Syst. 2016, 6, 13–19. [Google Scholar] [CrossRef] [Green Version]

- Geroski, P. Market Structure, Corporate Performance, and Innovative Activity; Oxford University Press: Oxford, UK, 1995. [Google Scholar]

- Han, J.; Kim, N.; Srivastava, R. Market orientation and organizational performance: Is innovation a missing link? J. Mark. 1998, 62, 30–45. [Google Scholar] [CrossRef]

- O’Cass, A.; Weerawardena, J. Examining the role of international entrepreneurship, innovation and international market performance in SME internationalization. Eur. J. Mark. 2009, 43, 1325–1348. [Google Scholar] [CrossRef]

- e-Marketer. Cord-Cutting Accelerates as OTT Video Keeps Growing. 2018. Available online: https://www.emarketer.com/content/more-than-half-of-us-consumers-watch-subscription-ott-video-2018 (accessed on 23 December 2019).

- Statista Number of Netflix Streaming Subscribers Worldwide from 3rd Quarter 2011 to 2nd Quarter 2018. 2018. Available online: https://www.statista.com/statistics/250934/quarterly-number-of-netflix-streaming-subscribers-worldwide/ (accessed on 23 December 2019).

- Federal Communication Commission. Annual Assessment of the Status of Competition in the Market for the Delivery of Video Programming; MB Docket No. 12-204, FCC 13-99; Federal Communication Commission: Washington, DC, USA, 2013.

- OECD. Digital Convergence and Beyond: Innovation, Investment, and Competition in Communication Policy and Regulation for the 21st Century; OECD: Paris, France, 2015. [Google Scholar]

- ITU. Impact of Broadband on the Economy; ITU: Geneva, Switzerland, 2012. [Google Scholar]

- Lee, S.; Park, E.; Lee, S.; Brown, J. Determinants of IPTV diffusion. Telemat. Inform. 2015, 32, 439–446. [Google Scholar] [CrossRef]

- Church, J.; Gandal, N. Platform competition in telecommunications. In The Handbook of Telemmunications Vol. 2: Technology Evolution and the Internet; Cave, M., Majumdar, S., Vogelsang, I., Eds.; Emerald Group Publishing: Bingley, UK, 2005; pp. 117–153. [Google Scholar]

- Hause, J.C.; DuRietz, G. Entry, industry growth and the microdynamics of industry supply. J. Political Econ. 1984, 92, 733–757. [Google Scholar] [CrossRef]

- Hitt, M.A.; Ireland, R.D.; Hoskisson, R.E. Strategic Management: Competitiveness and Globalization; South-Western Publishing Company: Versailles, OH, USA, 2005. [Google Scholar]

- Seo, S. Triple-play competition in the US telecommunications industry: Exploring cable operators’ adoption pattern of triple-bundled services. Int. J. Media Manag. 2007, 9, 1–8. [Google Scholar] [CrossRef]

- Pindyck & Rubinfeld. Econometric Models and Economic Forecasts, 4th ed.; McGraw-Hill: Boston, MA, USA, 1988. [Google Scholar]

- Bohlin, A.; Gruber, H.; Koutroumpis, P. Diffusion of new technology generations in mobile communications. Inf. Econ. Policy 2010, 22, 51–60. [Google Scholar] [CrossRef]

- Lee, S.; Brown, J.; Lee, S. A cross-country analysis of fixed broadband deployment: Examination of adoptions factors and network effect. J. Mass Commun. Q. 2011, 88, 580–596. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

| Variables | Measurement | Data Sources |

|---|---|---|

| Paid OTT video streaming market size | Paid OTT video streaming revenue (USD) per 100 inhabitants | PwC |

| SVOD market size | SVOD revenue (USD) per 100 inhabitants | PwC |

| Pay TV subscription revenue growth rate | Compound annual growth rate of traditional pay TV subscription revenue | PwC |

| Total broadband infrastructure | Total number of broadband subscribers per 100 inhabitants (including fixed and mobile broadband) | ITU |

| Fixed broadband infrastructure | Number of fixed broadband subscribers per 100 inhabitants | ITU |

| OTT platform competition | Herfindahl–Hirschman Index for different paid OTT types | PwC |

| Population density | Population per km2 | World Bank |

| Netflix market entry | Netflix market entry dummy (0 or 1) | PwC |

| Traditional Pay TV market size | Traditional pay TV subscription revenue (USD) per 100 inhabitants | PwC |

| Income | GDP per capita | World Bank |

| Paid OTT video streaming revenue growth rate | Compound annual growth rate of paid OTT video streaming revenue | PwC |

| PayTV/OTT platform market concentration | Herfindahl–Hirschman Index for traditional pay TV and paid OTT platforms | PwC |

| 1 | Argentina | 26 | Korea (R.O.K.) |

|---|---|---|---|

| 2 | Australia | 27 | Malaysia |

| 3 | Austria | 28 | Mexico |

| 4 | Belgium | 29 | Netherlands |

| 5 | Brazil | 30 | New Zealand |

| 6 | Canada | 31 | Nigeria |

| 7 | Chile | 32 | Norway |

| 8 | China | 33 | Pakistan |

| 9 | Colombia | 34 | Peru |

| 10 | Czech Republic | 35 | Philippines |

| 11 | Denmark | 36 | Poland |

| 12 | Egypt | 37 | Portugal |

| 13 | Finland | 38 | Romania |

| 14 | France | 39 | Russia |

| 15 | Germany | 40 | Saudi Arabia |

| 16 | Greece | 41 | Singapore |

| 17 | Hong Kong | 42 | South Africa |

| 18 | Hungary | 43 | Spain |

| 19 | India | 44 | Sweden |

| 20 | Indonesia | 45 | Switzerland |

| 21 | Ireland | 46 | Thailand |

| 22 | Israel | 47 | Turkey |

| 23 | Italy | 48 | United Arab Emirates |

| 24 | Japan | 49 | United Kingdom |

| 25 | Kenya | 50 | United States |

| N | Mean | Min | Max | S.D. | |

|---|---|---|---|---|---|

| Paid OTT video streaming market size | 250 | 408.35 | 0.02 | 3693.59 | 713.10 |

| SVOD market size | 250 | 270.06 | 0.01 | 2906.23 | 559.36 |

| Pay TV subscription revenue growth rate | 235 | 0.15 | −0.44 | 1.00 | 0.11 |

| Total broadband infrastructure | 249 | 87.46 | 1.18 | 183.42 | 44.94 |

| OTT platform competition | 248 | 6864.06 | 5000.00 | 10,000.00 | 1565.80 |

| Population density | 250 | 425.88 | 2.96 | 7908.72 | 1415.73 |

| Netflix market entry | 250 | 0.50 | 0.00 | 1.00 | 0.50 |

| Traditional Pay TV market size | 250 | 6433.10 | 20.04 | 31,585.74 | 6866.39 |

| Income | 250 | 31,846.86 | 2650.44 | 87,832.59 | 18,500.06 |

| Paid OTT video streaming revenue growth rate | 229 | 1.57 | −0.64 | 34.00 | 3.64 |

| PayTV/OTT platform market concentration | 250 | 9185.79 | 6904.87 | 10,000.00 | 741.06 |

| Fixed broadband infrastructure | 250 | 21.56 | 0.01 | 45.13 | 13.11 |

| Total Broadband Infrastructure | OTT Platform Competition | Population Density | Netflix Market Entry | Traditional Pay TV Market Size | Income | Paid OTT Revenue Growth Rate | PayTV/OTT Platform Market Concentration | |

|---|---|---|---|---|---|---|---|---|

| OTT platform Competition | −0.2681 | |||||||

| Population Density | 0.2900 | −0.0174 | ||||||

| Netflix market Entry | 0.2944 | −0.2157 | −0.128 | |||||

| Traditional pay TV market size | 0.5756 | −0.1414 | −0.0228 | 0.3981 | ||||

| Income | 0.7948 | −0.1760 | 0.4171 | 0.1841 | 0.6015 | |||

| Paid OTT revenue growth rate | −0.1611 | 0.2308 | −0.0228 | −0.1100 | −0.1132 | −0.0630 | ||

| PayTV/OTT platform market concentration | −0.6120 | 0.2378 | −0.2479 | −0.3566 | −0.2869 | −0.5556 | 0.1334 | |

| Fixed broadband infrastructure | 0.7684 | −0.2154 | 0.1483 | 0.2432 | 0.6798 | 0.7254 | −0.1098 | −0.4626 |

| Variables | VIF |

|---|---|

| Income | 3.66 |

| Total broadband infrastructure | 3.10 |

| Traditional pay TV market size | 1.95 |

| Population density | 1.48 |

| Netflix market entry | 1.25 |

| OTT platform competition | 1.06 |

| Mean VIF | 2.08 |

| Variables | VIF |

|---|---|

| Income | 2.43 |

| Fixed broadband infrastructure | 2.10 |

| PayTV/OTT platform market concentration | 1.57 |

| Netflix market entry | 1.15 |

| Paid OTT revenue growth rate | 1.03 |

| Mean VIF | 1.66 |

| Netflix (No Time-Lag) | Netflix (1- and 2-Year Time-Lag) | |||

|---|---|---|---|---|

| Variable | coef B | p-Value | coef B | p-Value |

| ln_Total broadband infrastructure | 1.0054 | 0.000 | 0.8013 | 0.000 |

| OTT platform competition | 0.0000 | 0.992 | 0.00005 | 0.076 |

| Population density | −0.0004 | 0.831 | 0.0025 | 0.073 |

| Netflix market entry(t) | 0.2642 | 0.030 | -- | -- |

| Netflix market entry(t-1) | -- | -- | 0.3327 | 0.005 |

| Netflix market entry(t-2) | -- | -- | 0.1599 | 0.195 |

| Traditional pay TV market size | 0.0003 | 0.002 | 0.0003 | 0.004 |

| Income | 0.0001 | 0.000 | 0.00003 | 0.000 |

| Constant | −4.3940 | 0.000 | −3.6451 | 0.000 |

| Country impact controlled | yes | yes | ||

| F/R2 | F(6,150) = 43.03/R2 = 0.5748 | F(7,143) = 34.39/R2 = 0.6273 | ||

| Number of observations | 247 | 200 | ||

| Netflix (No Time-Lag) | Netflix (1- and 2-Year Time-Lag) | |||

|---|---|---|---|---|

| Variable | coef B | p-Value | coef B | p-Value |

| ln_Total broadband infrastructure | 1.6336 | 0.000 | 0.68022 | 0.000 |

| OTT platform competition | −0.0008 | 0.000 | −0.00008 | 0.116 |

| Population density | 0.0001 | 0.968 | 0.0044 | 0.042 |

| Netflix market entry(t) | 0.1252 | 0.684 | -- | -- |

| Netflix market entry(t-1) | -- | -- | 0.7841 | 0.000 |

| Netflix market entry(t-2) | -- | -- | 0.1523 | 0.424 |

| Traditional pay TV market size | 0.0004 | 0.144 | 0.0004 | 0.002 |

| Income | 0.0001 | 0.000 | 0.00007 | 0.000 |

| Constant | −5.803 | 0.054 | −6.248 | 0.000 |

| Country impact controlled | yes | yes | ||

| F/R2 | F(6,191) = 49.66/R2 = 0.6094 | F(7,143) = 31.95/ R2 = 0.6100 | ||

| Number of observations | 247 | 200 | ||

| Overall | Reduced | |||

|---|---|---|---|---|

| Variable | coef B | p-Value | coef B | p-Value |

| ln_Paid OTT revenue growth rate | 0.0545 | 0.014 | 0.0544 | 0.013 |

| PayTV/OTT platform market concentration | 0.0002 | 0.005 | 0.00018 | 0.005 |

| Netflix market entry (t) | −0.1776 | 0.006 | −0.1772 | 0.006 |

| Income | −0.0000006 | 0.947 | −0.0000005 | 0.950 |

| Population density | 0.00004 | 0.963 | -- | -- |

| ln_fixed broadband infrastructure | −0.1804 | 0.292 | −0.181 | 0.287 |

| Constant | −3.0747 | 0.004 | −3.0555 | 0.002 |

| Country impact controlled | yes | yes | ||

| F/R2 | F(6,150) = 12.36/R2= 0.3308 | F(5,151) = 14.93/R2 = 0.3308 | ||

| Number of observations | 203 | 203 | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lee, S.; Lee, S.; Joo, H.; Nam, Y. Examining Factors Influencing Early Paid Over-The-Top Video Streaming Market Growth: A Cross-Country Empirical Study. Sustainability 2021, 13, 5702. https://doi.org/10.3390/su13105702

Lee S, Lee S, Joo H, Nam Y. Examining Factors Influencing Early Paid Over-The-Top Video Streaming Market Growth: A Cross-Country Empirical Study. Sustainability. 2021; 13(10):5702. https://doi.org/10.3390/su13105702

Chicago/Turabian StyleLee, Sangwon, Seonmi Lee, Hyemin Joo, and Yoonjae Nam. 2021. "Examining Factors Influencing Early Paid Over-The-Top Video Streaming Market Growth: A Cross-Country Empirical Study" Sustainability 13, no. 10: 5702. https://doi.org/10.3390/su13105702

APA StyleLee, S., Lee, S., Joo, H., & Nam, Y. (2021). Examining Factors Influencing Early Paid Over-The-Top Video Streaming Market Growth: A Cross-Country Empirical Study. Sustainability, 13(10), 5702. https://doi.org/10.3390/su13105702