1. Introduction

One of the main issues facing large firms in developing economies is whether it pays them to adopt a culture of corporate environmentalism [

1]. Most of these firms would want to adopt a corporate environmental posture if they were certain that such a posture would improve their economic lifeline. If they were sure that while they undertake an intense push for green strategy adoption, their products would maintain high quality and their financial performance would not be threatened, then these firms may consider such a dilemma as an easier issue to deal with. These firms would not want to advance environmental performance targets at the expense of their own financial baseline; being the very essence of their organizational existence. As these firms grow, their existential focus shifts to improving market share and exploring new markets. By so doing, these firms inadvertently get enmeshed in competitive tussles with other global players. Due to these competitive terrains wherein they exist, if they undertake green strategies for any reason that does not improve their product offering, then they really face a prompt existentialism.

It is a fact that the global academic and policy environment is one that now emphasizes the need for firms and societies to adopt policies, strategies, and postures that pitch them as environmentally conscious entities. Studies like those of Al-romeedy [

2]; Dai, Cantor & Montabon, [

3]; Fanasch, [

4]; García-marco & Sánchez, [

5]; Ge et al. [

6]; Liu et al. [

7]; Malviya et al. [

8]; Yu & Han, [

9]; H. Zhang et al. [

10], and W. Zhang et al. [

11] make it clear that environmental posturing is not only important, but remains a contemporary discourse. Also, whether it is the clichés of “green new deal”, “carbon neutrality”, “zero emissions” or even the global effort to deal with climate change per the “Paris Climate Accord”, societies and policies are being designed to make entities appear environmentally responsible, for obvious beneficial reasons. On the organizational side, while large multinational firms may be able to bear the sudden shift in greening, especially those who operate in developed economies, it is a corporate crisis for other large firms in developing economies that are faced with the same levels of expectations, but exist in countries with lax environmental standards and weak alternative infrastructures.

In Nigeria and other developing climes for instance, it is this kind of dilemma that firms have to deal with in answering when it pays to be green. The disincentives for environmental responsibilities are high. The cost of production is increasingly high, the energy production process is poor and inefficient, distribution infrastructure is mostly weak, and most importantly, the regulatory standards are almost inexistent, giving most firms the latitude to relax their environmental posturing. If these firms were merely engaging in green showboating to appeal to the wider academic and global markets, then it would be an easier question, but it is a lot more than that. The assurance that these firms would want to have is that, if they actually become green, it should pay, both financially and environmentally.

The debate that this study is concerned with is therefore competitive. It answers the question of whether the environmental position is enhanced and the financial position of the firm threatened if its green posturing is channeled through improving its product. As for the benefits of green strategies generally, it can hardly be in doubt that green leadership improves employees creativity, green innovation, and other firm outcomes [

11,

12,

13]; green innovation strategy improves competitive advantage and curbs uncertainty [

6]; green human resource management aids environmental performance [

14] and profit maximization being a function of green programming [

15]. A unique position of this study, aside from its focus on a regional multinational consumer-based manufacturing firm, is its simultaneous probe on the dual effects of corporate environmentalism on both financial and environmental outcomes. While most studies, as stated above, have investigated the effects of green strategy on organizational outcomes, this study addresses the issue within the same organization, having a uniform baseline. Also, while Baron and Kenny’s approach has been used in most mediation studies, we adopted an improvement of the Baron and Kenny’s approach, namely the Hayes mediation approach, which makes up for the methodological flaw of the extant Baron and Kenny approach [

16,

17,

18].

As for this study, it intends to investigate this comparative question under the same firm, in an effort to understand if financial positions are compromised when a firm tilts green; the central question of the study. The study also addresses the hypothetical arguments on the direct effects of green strategy on financial and environmental performance and the total effects being mediated by product quality. It goes on to provide empirical mediation tests and provides theoretical and managerial implications

2. Literature Review

2.1. Green Strategy/Corporate Environmentalism

Green management is the management practice that produces environmentally–friendly products and minimizes the impact on the environment through green strategy, green production, green research & development and green marketing [

19]. A green strategy for an enterprise-public or private, government or commercial, is one that complements the business operations and overall business strategies that are already well understood and often well-articulated by the enterprise [

20]. Also known as corporate environmentalism, environmental management, or corporate sustainability [

21,

22], green strategy focuses on firm decision making that positively impacts the environment. Green strategy is a relatively new term, and so a consistent and comprehensive definition of the term is lacking in literature [

23]. However, Banerjee [

24] defines the term as the “integration of environmental concerns into a firm’s decision-making process”. A major consideration in building a green strategy is for enterprises to create a common culture of awareness and action to support environmental responsibility.

2.2. Product Quality

Product quality describes the degree to which the user’s needs are elegantly met and thus should be complete, usable, efficient, and effective [

25]. It has been acknowledged as one of the most promising strategies to compete successfully in the market and a key strategic component of competitive advantage. It is akin to the tetramerous features of specific ingredient (product essence), benefits (product difference), new knowledge (product differentiation), and risk-free knowledge (product risk). Garvin [

26] conceptualized product quality using five different approaches: transcendent approach, product-based approach, user-based approach, manufacturing-based approach, and value-based approach. According to the transcendent approach, quality is defined as the intrinsic features of a product which makes it superior or preferable to substitutes. It is conceived as a simple property that can be recognized only through experience and in this way is consistent with the experimental goods typology. Value-based approach likens quality to performance at an acceptable price or alternatively conformance to an acceptable cost. For product-based approach, differences in the quantity of some ingredient or attribute possessed by the product are considered to reflect difference in quality. For the user-based approach, quality is the extent to which a product/service meets or exceeds customer expectation. Finally, manufacturing-based approach defines quality as conformance to specification. Recently, product quality has been portrayed in terms of brand, design, and customer requirements. The brand gives customers additional value and prestige, and marketers use it as a tool for gaining competitive advantage [

27]. It is effective in creating product quality perceptions and it establishes the intention of buyers towards the product [

28].

2.3. Environmental Performance

Many organizations seek ways to understand, demonstrate, and improve their environmental performance. This can be achieved by effectively managing those elements of their activities, products, and services that can significantly impact the environment. Environmental performance is defined as the commitment of firms to protect the environment and to demonstrate measurable operational parameters that are within the prescribed limits of environmental care [

29]. A comprehensive measure of environmental performance includes incident reduction, continuous improvement, recycling performance, stakeholder perception, independent audit, waste reduction, resource consumption, and cost-saving. Managers play an essential role in achieving environmental performance objectives through recruitment, training, appraisal, and incentive for an environmentally conscious workplace [

30]. Hiring environmentally conscious employees and establishing a consistent, effective training and measurement system promote environmental awareness across the various functions of the firms [

31,

32]. Environmental performance is evaluated on the basis of objectives, improvements, and the extent of waste reductions in the production process [

30]. Also, peer involvement or environmentally conscious teamwork are vital elements for green integration [

33]. Green human resource management (GRHM) practices offer a practical way for the organization to develop human capital that can enhance the environmental performance and sustainable development of the firm [

34].

2.4. Financial Performance

Financial performance is the extent to which financial objectives have been accomplished. It is the process of measuring the result of a firm’s policies and operation in monetary terms. Financial performance assesses the financial well-being of the overall firm, and is measured with financial statements such as balance sheet, income statement, cash flow statements, and the statements of changes in equity. The balance sheet provides an overview of how the company manages its assets and liabilities and also shows a summary of the financial balances of an organization. The income statement (profit or loss statement) provides a summary of operations for the year showing gross profit margin, cost of goods sold, operating profit margin, and net profit margin. The cash flow statement is a combination of both the income statement and the balance sheet. It provides the sources and the use of cash available to an organization. Lastly, the statement of changes in equity (statement of retained earnings) details the movement of owner’s equity over a period. Financial performance is also concerned with the factors that contribute to profitability and returns such as sales and costs as well as return on assets (ROA), return on equity (ROE), profit margins, etc. ROA measures the net income generated by total assets, i.e., return for every amount invested while ROE measures the profit generated by the total equity [

35].

3. Hypotheses Development

3.1. Green Strategy and Environmental Performance

Recent studies show that green strategy holds various advantages for the firm [

36,

37,

38], and relates positively to environmental performance [

3,

15]. Majid et al. [

36], Fores [

39], and Li et al. [

40] argued that firms will experience an increase in environmental performance when environmental business strategies are developed in line with pollution prevention, regulation compliance, materials recycling, and waste reduction. Laari et al. and others [

38] further argued in their study of logistics service providers that green supply chain management practices would relate positively to environmental performance. Thus, proactive environmental strategies would predicate environmental performance, especially for firms with a high shared vision for corporate environmentalism. More so, Luu [

41] averred that, employee organizational citizenship behaviour is necessary for organizational green performance, which is significantly associated with overall organizational performance. To effect green strategy and green creativity among employees, Zhang et al. [

11] suggest that firms should adopt green transformational leadership, because firms with green innovation strategies promoted by green transformational leaders are likely to enhance process engagements, leading to environmental performance. In fact, green transformational leadership is likely to influence green human resource management practices, which will precipitate green innovation [

13,

42]. Building upon the above discussion, we propose the following hypothesis:

Hypothesis 1 (H1). There is a positive effect of the adoption of green strategy/corporate environmentalism on environmental performance.

3.2. Green Strategy and Financial Performance

Laari and others [

38] suggests that firm financial performance can be measured by normalizing raw financial metrics to assess performance in relation to industry peers. Thus, financial performance is not measured in isolation, but benchmarked against industry performance; although such measurements may not specifically capture gradual changes in the firm’s financial performance over a period of time. It is very unlikely that corporate social responsibility alone would yield financial performance given that green strategies are holistic [

43], and benefits accrue only in the long run [

44]. This explains the possibility that no significant correlation exists between green management practices and financial performance. Similarly, Trumpp & Guenther [

45] argued that a non-linear relationship exists between corporate environmental performance (CEP) and corporate financial performance (CFP), especially for manufacturing industries. They suggest that the relationship between CEP and CFA is such that the impact of the former on the latter is likely to be negative for a range of CEP periods, after which the relationship becomes positive, where more CEP leads to a higher-level CFP. However, Gupta & Zhang [

15] report that the financial returns on green programming in firms would be predicated by the profit maximization motive of the firm and vice-versa [

46]. This means that firms are wont to invest more in green programming if their strategic business model is founded on green policies, and if they possess the required capacity to match these green capabilities to compliment strategic business models. According to Ge et al. [

6], firms that employ green innovative strategies would likely achieve greater sustainable competitive advantage, which will occasion various performance routes and results due to uncertainty levels in turbulent and austere environments. We therefore propose the following hypothesis:

Hypothesis 2 (H2). There is a positive effect of the adoption of green strategy/corporate environmentalism on financial performance.

3.3. The Mediating Role of Product Quality

According to Qasrawi et al. [

47], total quality management is a system that ensures continuous improvements through the development of tools, methods, processes, and values that ensure that products continually meet environmental expectations and satisfy customers. From the green performance perspective, tools and technologies should minimize the adverse effects of firm production on environment [

48,

49,

50]. Chen et al. [

51], suggests that environmental product quality is an offshoot of eco-friendly products stemming from green innovations. It is ascertained by its ability to meet environmental needs through proper integration of environmental concerns at the primary stage of product development. However, this is impossible without corporate environmentalism through green transformational leadership [

11,

13]. Corporate environmentalism entails environmental concern, which is the level of knowledge, awareness, and consciousness an individual or organization possesses about the harmful consequences of non-eco-friendly products which may be adding value to the organization [

52]. We therefore expect, in line with the work of Zhang and his colleagues [

11], that corporate environmentalism will lead to employee green creativity, which ensures the development of quality products that improve environmental performance. Since green strategy will influence product quality [

24,

51,

53], it is likely that environmental performance will be influenced to the extent that green strategies are implemented in the environment. Brady and others [

54] also argue that by integrating environmental issues into concerns for quality products, performance will be improved. Poor product quality has the potential to deface firm reputation and firm performance [

55], while exacerbating the wastage of human resources [

56] and natural resources [

57]. Based on this discourse, the following hypothesis is proposed:

Hypothesis 3 (H3). Product quality mediates the effect of green strategy/corporate environmentalism on environmental performance.

The resource-based view of the firm suggests that firms can enhance competitive advantage by developing unique resources and capabilities through quality products and services [

58,

59]. Three basic issues confront businesses all over the world, and are predicated by the quality of production process: limited resources/inputs, required output, and waste reduction [

48]. By identifying costs associated with improved product quality, firms can eliminate the risks and losses associated with low quality, thereby improving competitive advantage. Also, Dai [

3] suggested that operational performance can be improved through corporate environmental proactive strategy, but that this relationship is mediated by process innovation. Hence, innovative products stem from management anticipation of environmental demands, which increase customer satisfaction and overall firm performance [

60]. Firms with proactive environmental strategies will increase resource efficiency through energy usage reduction, fewer and cheaper raw materials, and staff cost reduction; and are better positioned to leverage their unique products to attract differentiated customers who are willing to pay for the products. We therefore argue that, as product design and quality are influenced by corporate environmentalism through cost reduction and resource identification, financial performance would be enhanced.

Hypothesis 4 (H4). Product quality mediates the effect of green strategy/corporate environmentalism on financial performance.

4. Methodology

4.1. Sampling and Data Collection

To test our hypotheses, we collected data from one of the largest multinational firms operational in Nigeria. The company runs multiple units with semi-autonomous authorities. These units are made up of brands and sections that thrive to improve their contribution to the overall wellbeing of the firm. The semi-autonomous nature of the firm implies that the responses provided by employees could be regarded as having been provided by multiple independent respondents. The firm, like other consumer goods companies with their production facilities in Nigeria, might also be perturbed that environmental performance and financial performance are mutually exclusive, having an impression that firms focused on profit making may not need to pay attention to the effect of their production processes on environmental degradation. It is the operational scope of the firm that informed its selection.

To collect data, having acquired preliminary access, we sent an email with our attached instrument to the management of the company on the 25 February, 2020 requesting that they distribute the questionnaire to their staff. The instrument was to be filled using the logged in Google forms. We followed up on our request few days later, and on the 4 April 2020, we received our first back-end response. After two weeks, precisely on the 18 April 2020, the last response was received. A total of 2763 respondents which make up the staff of the firm were administered the questionnaire, but we received 648 responses. We had about 27 correspondences with the firm from the first day of contact (25 February 2020) to the last day of contact (18 April 2020).

4.2. Measures

Measures adopted for this study were found in extant empirical literature, and had been well validated, even though we adapted them to fit our study context, especially with keen focus on green strategy and performance. Green strategy construct was measured using the four items adopted from Banerjee [

24]. A sample item was: “We always integrate environment issues into our strategic planning process.” We adopted the four scales from Chen and others [

51], to measure product quality. A sample item was: “Continuous improvement in our organization’s product quality is as a result of our environmentally friendly (green) product innovation process.” For environmental performance construct, we adopted the four question items by Judge & Douglas [

61]. A sample item was: “We always comply with environmental regulations”. Finally, we also made use of three items by Judge & Douglas [

61] to measure financial performance. A sample item was: “My department’s contribution to the profitability of the organization has improved over the years.” All the question items for the four constructs were assessed via a 5-point Likert-type scale, ranging from 1 = Strongly disagree to 5 = Strongly agree.

We controlled for a number of firm/departmental- and individual-level variables. They include: Tenure: the length of time the employee has worked for the organization, the length of time worked in a particular unit, staff category (1 = non-management, and 2 = management staff), and direct reporting (number of people reporting directly to an individual employee). These variables are well discussed in literature as factors that affect the opinion of respondents on whether the strategy being adopted is “corporate”, that is, emanating from the top management [

11], while performance is also a function of experience and size [

3].

4.3. Common Method Variance

Since we studied a homogenous sample group, we adopted the Harman’s single factor test to check for the incidence of common method variance [

62]. All the four latent variables were entered into an unrotated factor solution to ascertain the number of factors that are necessary to account for any variance in the variables. The result showed a 44% covariance, which is less than the 50% benchmark, and implies no single factor explained the relationship between the variables more than it should have.

4.4. Data Validity and Reliability

To determine construct validity, we assessed the factor loading of each construct [

63]. Out of the four question items under green strategy construct, we found that the last item has a rather small factor loading, and thus was obfuscated from the analysis. The CFA for green strategy lies between 0.74 and 0.80; that of product quality lies between 0.85 and 0.89; environmental performance lies between 0.66 and 0.68; financial performance lies between 0.79 and 0.90. The results also indicate that the Cronbach’s Alpha for composite reliability were above the ideal standard of 0.6, with 0.765 for green strategy, 0.920 for product quality, 0.773 for environmental performance, and 0.880 for financial performance. Average variance extracted (AVE) for all the constructs surpassed the minimum required standard of 0.5, except for environmental performance with 0.460. See

Table 1.

4.5. Structural Model and Hypothesis Testing

The appropriate fit for the proposed models were assessed using Structural Equation Modelling (SEM). The result of the model fit indicates that to some degree, the structural model was reasonable and no further amendment was needed (i.e., χ

2/df = 1.778, RMR = 1.783, RMSEA = 0.035, GFI = 0.976, AGFI = 0.960, NFI = 0.977, CFI = 0.990, IFI = 0.990). In all, the model fit indices were interpreted using the guidelines stipulated by Hair et al. [

63]. Since RMSEA values less than 0.05 and CFI, GFI, and AGFI values above 0.90 are typically considered good, it means that our structural model fits well.

5. Pieces of Evidence

As seen in

Table 2, the respondent profile shows that the respondents were majorly male, comprising 88.4% of the respondents, the highest age group was 29–36 years, comprising 46.5% of the respondents, those with a Bachelor’s Degree or its equivalent comprised 73.1% of the population, while non-management staff were more than their management counterparts, comprising 73.3% of the respondents.

In addition, we present the means, standard deviations, and inter-variable correlations in

Table 3. The length of time employees spent on the job has statistically significant positive relationship with the length of time they have spent at their present position (r = 0.205), category of the staff (r = 0.272), direct reporting (r = 0.101), green strategy (r = 0.165), product quality (r = 0.170), environmental performance (r = 0.199). However, no statistically significant relationship was found between length of time in the position and financial performance. Length of time spent in a position was found to have a statistically significant negative relationship with staff category (r = −0.305). Conversely, staff category has a positive relationship with direct reporting (r = 0.235). We found a statistically significant positive relationship between green strategy and product quality (r = 0.642); environmental performance (r = 0.630); and financial performance (r = 0.356). in the same vein, product quality was positively related to both environmental performance (r = 0.288); and financial performance (r = 0.316). Finally, a statistically significant relationship was found between environmental performance and financial performance (r = 0.406).

A serial mediation test is conducted in this study using model 4 of Hayes PROCESS macro.

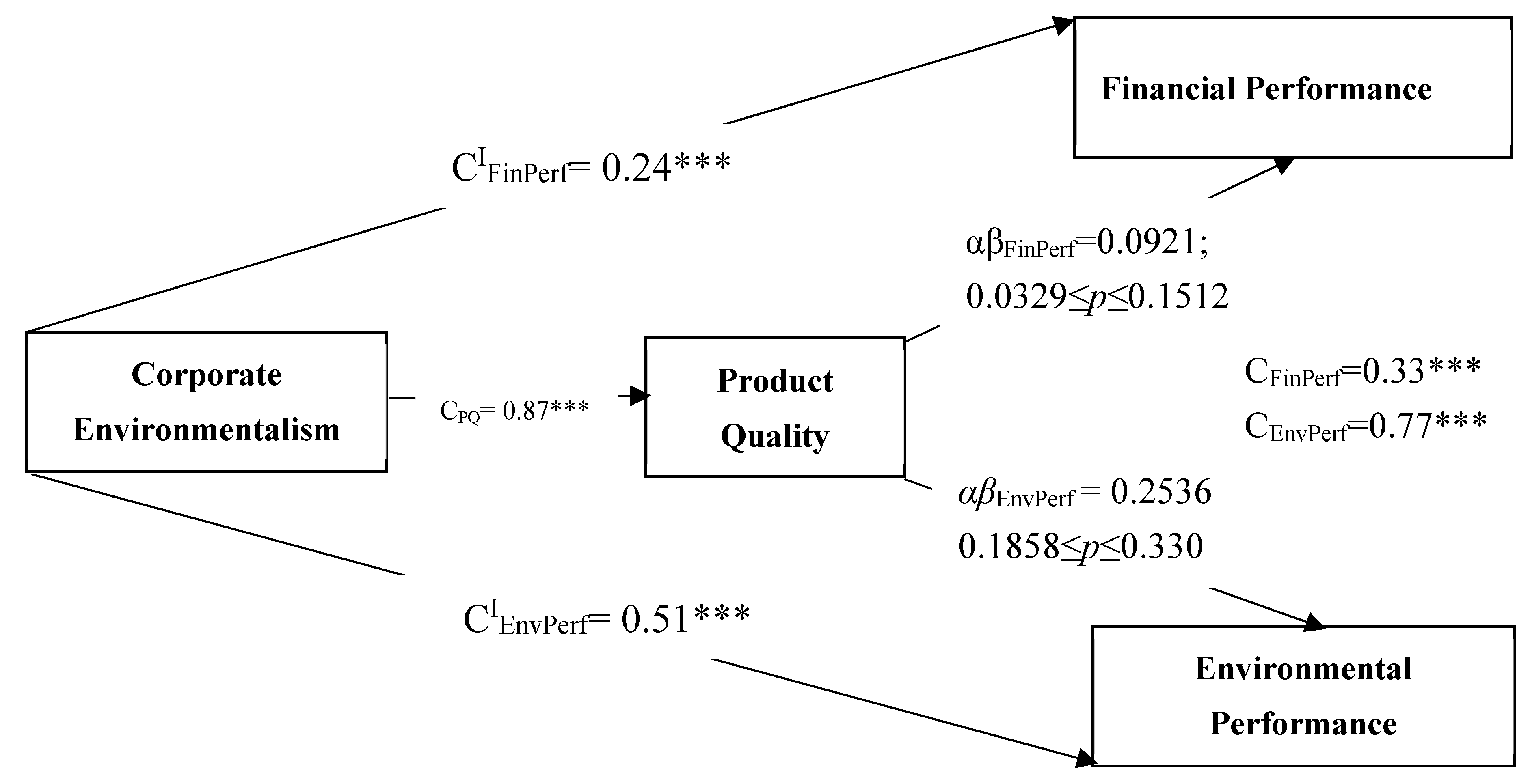

Table 4 shows a summary of key findings. The results show a statistically significant direct effect of green strategy on environmental performance (C

ΙEnvPerf = 0.51,

p < 0.05) which supports hypothesis one. This implies that the use of green strategy directly improves the environmental performance contribution from the firm. While the indirect effects were not a cause for hypothetical inquiry, the results also showed that the total indirect effect was statistically significant (αβ

EnvPerf = 0.2536; 0.1858 ≤

p ≤ 0.330). The result on hypothesis three also showed that the total effect of green strategy on environmental performance through product quality was statistically significant (C

EnvPerf = 0.77,

p < 0.05). This implies that product quality was a strong mediator of the green strategy-environmental performance effect. This result shows that green strategy channeled through improving product quality would not only strongly improve product quality, but would also improve environmental performance. There is little to no risk of adopting a green strategy with the intention of improving product quality and environmental performance.

The other sets of results are shown on

Table 5. The summary shows that there is a statistically significant direct effect of green strategy adoption on the financial performance of the firm (C

ΙFinPerf = 0.24,

p < 0.05). This implies that an improvement in the uptake of green action would only serve to improve the firm’s financial performance. It is also important to state the strong direct effect of green strategy on product quality (C

ΙPQ = 0.87;

p < 0.05), coupled with the total indirect effect (αβ

FinPerf = 0.0921; 0.0329 ≤

p ≤ 0.1512) leading to a statistically significant total effect of green strategy through product quality in affecting financial performance (C

FinPerf = 0.33,

p < 0.05). This implies that the mediation of product quality on the green strategy-financial performance effect does not reduce, but rather improves the financial lifeline of the firm. While the environmental performance effect is stronger, this result shows that the financial performance effect is not weak either. Combined with the controls and mediation, financial performance doubly predicated upon green strategy and product quality is high. All results from

Table 4 and

Table 5 are also presented on

Figure 1 below.

6. Discussion

The overarching goal of this study was to advance the literature on corporate environmentalism and both environmental and financial performance. It is a response to the call by previous researchers [

64,

65] for more empirical studies into the antecedents of both environmental and financial performance. Our study also tested the mediating role of product quality on the corporate environmentalism–performance effect. We have developed a model which linked the four main concepts (corporate environmentalism, product quality, environmental, and financial performance), and formulated five hypotheses to explore their relationships. Our hypotheses were supported by the findings of our study as seen on

Figure 1. Regarding H1 and H2, our results show a statistically significant positive direct effect of corporate environmentalism on environmental performance (C

ΙEnvPer = 0.51,

p < 0.05), and financial performance (C

ΙFinPerf = 0.24,

p < 0.05). These findings are consistent with the work of Judge & Douglas [

61], who found that the more environmental management concerns are integrated into firm overall strategy, then both environmental and financial performance will be improved. However, this can only happen when more firm resources are allocated for environmental issues which are incorporated in the firm’s planning process. Hence, with a leadership concerned about environmental issues, green strategy is a veritable tool for gaining competitive advantage, while enjoying market goodwill [

11]. Laari and others [

38] concluded that logistics service providers (LSPs) who make competitive advantage a top priority find it easier to employ green supply chain management strategies (GSCM) than those who do not. Contrary to our findings, GSCM was found to be positively related to environmental performance, but not to financial performance, due to the obvious short-term financial returns of GSCM practices which in the future could yield differentiation opportunities for the firm.

We found a statistically positive direct effect of corporate environmentalism on product quality (C

ΙPQ = 0.87;

p < 0.05). In line with our results, Palacios-Argüello and others [

37] confirm that organic labelled raw materials incorporated in the production process and products placed at close proximity to the stakeholders, would improve product quality. They also found that environmental product quality leads to product demand especially when product quality is an indispensable criterion when choosing business partners and suppliers. Albino and others [

66] also found that green product developing firms would adopt higher levels of different environmental strategic approaches than non-green product developing firms. This implies that green product developing firms are more environmental savvy, and are more poised to deliver green products than the non-green firms. However, the economic sector and geographical perspectives of the firm determine which green strategies are adopted the most by green product developers.

Consistent with our expectations, our results also reveal that product quality mediates the effects of corporate environmentalism on both environmental performance (CE

nvPerf = 0.77,

p < 0.05), and financial performance (C

FinPerf = 0.33,

p < 0.05). Chen [

51] corroborates our findings, by concluding that both environmental quality and employee commitment to environmental performance would predicate environmental performance. Environmental strategy improves product quality, and with employee commitment, environmental performance will also be improved. Our findings also strengthen the argument that the behaviour and attitude of employees are critical for improving environmental performance [

14,

67,

68]. Thus, when employees are motivated through green innovation strategies, then their creative process engagement is improved, leading to green innovative products [

11]. Also, environmental training mediates the relationship between firm environmental ethics and both firm environmental performance and firm competitive advantage, such that the higher firm’s commitment to ethics in quality, the more profits they would make when compared to competitors [

13]. Ninlawan and others [

69] additionally conducted a case study on green strategy chain management practices in Chinese automobile industries and Thailand electronics industries and observed that increasing pressure on employees with the help of top management commitment can improve environmental performance and also lead to economic stability.

7. Conclusions

Our study investigated the mediating role of product quality on the relationship between green strategy/corporate environmentalism and both financial and environmental performance. Since all the hypotheses were supported by the findings, we conclude that the effective formulation of green strategies would not only improve the environmental outlook of the firm, but also yield positive financial returns for the organization, especially in the long run, through the profits that accrue to green innovative products.

8. Limitation and Future Directions

The intention of the authors was to administer both a structured instrument to the respondents and to also undertake a focused group discussion, making this work a meta-analysis. Due to the COVID-19 pandemic, we were proactive enough redesign our tool for data collection to be administer virtually, but the focused group discussion could not materialize. The statistical diagnosis applied on the dataset showed strong valid and reliable indices, meaning that the quantitative collation done virtually was successful, but not the focused group discussion. This implies that we had to redesign the study. It is therefore our suggestion that similar studies on organizational sustainability make attempt to conduct interviews amongst response for phenomenological context, which is relevant for studies that are still nascent within a geographical domain. Understanding these contexts are important as it would have been important to know if the green strategy is driven by the local content requirements of the industry’s policy, the parent firm influence, an internal policy priority or government regulation. Of course, while these concepts were not the subject of our empirical investigation, they would have provided contextual information for further research.

9. Managerial Implications

A firm’s success and survival could be heightened by enhancing corporate environmentalism as a critical strategic goal of the firm. This study suggests that management play a vital role in the achievement of environmental objectives and employees should be involved in environmentally friendly practices that will enhance firm performance. Management should continuously train employees on environmental practices and ethics, and also provide a friendly environment that will in turn improve the environmental performance and recognition of the firm.

Quality is a key component of competitive advantage. Managers should recognize relevant environmentally friendly technological advanced tools that could be used to produce quality products. Products should be designed with excellent ingredients, possess good branding, packaging and be value-oriented. Management should also conduct research and study trends on environmentally accepted products by the customers, get feedback from the customers and seek ways to better improve a product to meet environmental expectations and serve the safety of customers.

Furthermore, for an improved performance and increased productivity, quality should be seen as a vital aspect that should be incorporated at all levels of the organization and integrated into the stages of production. It will suffice to say that management should see quality as a key instrument needed in all aspects/division of the organization to achieve its desired goals and objectives. In addition, corporate environmentalism could be seen as a critical determinant in firms’ evaluation when regulatory bodies monitor firms on a time-to-time basis over their involvements and positive impact on the environment. The government must make available performance guidelines which should be strictly adhered to by the firms, as well as make public policies that support firms’ involvement on the environment.

10. Theoretical Implications

Our study makes two vital theoretical contributions. First, the findings of our study advance the RBV theory of the firm. The RBV theory assumes that firm resources could be heterogenous within an industry in terms of control and mobility. Firm resources include the materials, skills, knowledge, processes, and other firm characteristics with which the firm seeks to gain competitive advantage [

59]. We suggest that a green strategy, which mirrors the external realities of the firm’s environment, could also be employed as an inimitable tool for competitive advantage through environmental and financial performance. Whereas some of the mainline firm resources could be homogenous within an industry or heterogenous across industries, corporate environmentalism, which centers on leadership poised with the unique capabilities to address environmental concerns in a way that uniquely suits the firm’s strategies, may be irreplaceable.

Our study also contributes to the literature on TQM. TQM is a management strategy which aims to satisfy customers by enshrining quality throughout the production process, and by so doing produce long term success for the firm. The principles of TQM include identifying and obfuscating production errors, simplifying supply chain management, improving customer experiences, and effective staff training in line with customer demands [

47]. We suggest that beyond these traditional demands of TQM, green performance should form an integral part of TQM objectives, as it will propel management to integrate environmental concerns at every stage of the product cycle. By doing this, quality will become more standardized, results will be controlled the more, and staff training will become more environmentally focused. As eco-friendly products become policy initiatives for the firm at all management levels, overall firm environmental capabilities will continue to improve, leading to improved environmental performance.

Author Contributions

Conceptualization: A.O. (Akintunde Olayeni), A.O. (Anastasia Ogbo)., B.C. and C.E.; Data curation, H.O.; Formal analysis, A.O. (Anastasia Ogbo), B.C, C.I. and C.E.; Funding acquisition, C.I.; Investigation: A.O. (Akintunde Olayeni), H.O. and C.I; Methodology, A.O. (Anastasia Ogbo), H.O. and C.E.; Project administration: A.O. (Akintunde Olayeni), H.O., B.C. and C.E.; Resources: A.O. (Akintunde Olayeni) and C.I.; Software, H.O; Supervision, A.O. (Anastasia Ogbo) and B.C; Writing—original draft: A.O. (Akintunde Olayeni), H.O., B.C. and C.E.; Writing—review & editing, A.O. (Anastasia Ogbo), B.C., C.I. and C.E. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

Data is contained within the article.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Orsato, R. Sustainability Strategies: When Does It Pay to Be Green? 1st ed.; Palgrave Macmillan: London, UK, 2009. [Google Scholar] [CrossRef]

- Al-romeedy, B.S. Green Human Resource Management in Egyptian Travel Agencies: Constraints of Implementation and Requirements for Success Green Human Resource Management in Egyptian Travel Agencies: Constraints of Implementation. J. Hum. Resour. Hosp. Tour. 2019, 18, 529–548. [Google Scholar] [CrossRef]

- Dai, J.; Cantor, D.E.; Montabon, F.L. Examining Corporate Environmental Proactivity and Operational Performance: A Strategy-Structure-Capabilities-Performance Perspective within a Green Context. Int. J. Prod. Econ. 2017, 193, 272–280. [Google Scholar] [CrossRef]

- Fanasch, P. Survival of the Fittest: The Impact of Eco-Certification and Reputation on Firm Performance. Bus. Strateg. Environ. 2019, 611–628. [Google Scholar] [CrossRef]

- García-marco, T.; Sánchez, M. Do Firms with Different Levels of Environmental Regulatory Pressure Behave Differently Regarding Complementarity among Innovation Practices? Bus. Strateg. Environ. 2020, 29, 1684–1694. [Google Scholar] [CrossRef]

- Ge, B.; Yang, Y.; Jiang, D.; Gao, Y.; Du, X.; Zhou, T. An Empirical Study on Green Innovation Strategy and Sustainable Competitive Advantages: Path and Boundary. Sustainability 2018, 10, 631. [Google Scholar] [CrossRef] [Green Version]

- Liu, K.; Hu, C.; Lin, M.; Tsai, T.; Xiao, Q. Brand Knowledge and Non-Financial Brand Performance in the Green Restaurants: Mediating Effect of Brand Attitude. Int. J. Hosp. Manag. 2020, 89, 102566. [Google Scholar] [CrossRef]

- Malviya, R.K.; Kant, R.; Gupta, A.D. Evaluation and Selection of Sustainable Strategy for Green Supply Chain Management Implementation. Bus. Strateg. Environ. 2018, 27, 475–502. [Google Scholar] [CrossRef]

- Yu, W.; Han, R. The Impact of Pollution Taxation on Competitive Green Product Choice Strategies. Comput. Ind. Eng. 2019, 137, 106012. [Google Scholar] [CrossRef]

- Zhang, H.; Zhang, Z.; Pu, X.; Li, Y. Green Manufacturing Strategy Considering Retailers ’ Fairness Concerns. Sustainability 2019, 11, 4646. [Google Scholar] [CrossRef] [Green Version]

- Zhang, W.; Xu, F.; Wang, X. How Green Transformational Leadership Affects Green Creativity: Creative Process Engagement as Intermediary Bond and Green Innovation Strategy as Boundary Spanner. Sustainability 2020, 12, 841. [Google Scholar] [CrossRef]

- Tuan, L.T. Environmentally-Specific Servant Leadership and Green Creativity among Tourism Employees: Dual Mediation Paths. J. Sustain. Tour. 2020, 28, 86–109. [Google Scholar] [CrossRef]

- Singh, S.K.; Del Giudice, M.; Chierici, R.; Graziano, D. Green Innovation and Environmental Performance: The Role of Green Transformational Leadership and Green Human Resource Management. Technol. Forecast. Soc. Chang. 2020, 150, 119762. [Google Scholar] [CrossRef]

- Umrani, A.W.; Channa, A.N.; Yousaf, A.; Ahmed, U.; Pahi, H.M.; Ramayah, T. Greening the Workforce to Achieve Environmental Performance in Hotel Industry: A Serial Mediation Model. J. Hosp. Tour. Manag. 2020, 44, 50–60. [Google Scholar] [CrossRef]

- Gupta, V.; Zhang, Y. Investigating Environmental Performance Management. Rev. Bras. Gest. Negocios 2019, 22, 5–28. [Google Scholar] [CrossRef]

- Hayes, A.F. Beyond Baron and Kenny: Statistical Mediation Analysis in the New Millennium. Commun. Monogr. 2009, 76, 408–420. [Google Scholar] [CrossRef]

- Zhao, X.; Lynch, J.G.; Chen, Q. Reconsidering Baron and Kenny: Myths and Truths about Mediation Analysis. J. Consum. Res. 2010, 37, 197–206. [Google Scholar] [CrossRef]

- Kline, R.B. The Mediation Myth. Basic Appl. Soc. Psychol. 2015, 37, 202–213. [Google Scholar] [CrossRef]

- Peng, Y.; Lin, S. Local Responsiveness Pressure, Subsidiary Resources, Green Management Adoption and Subsidiary’s Performance: Evidence from Taiwanese Manufactures. J. Bus. Ethics 2008, 79, 199–212. [Google Scholar] [CrossRef]

- Olson, E.G. Creating an Enterprise-Level ‘“Green”’ Strategy. J. Bus. Strategy 2008, 29, 22–30. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J.; Lai, K. Confirmation of a Measurement Model for Green Supply Chain Management Practices Implementation. Int. J. Prod. Econ. 2008, 111, 261–273. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J. An Inter-Sectoral Comparison of Green Supply Chain Management in China: Drivers and Practices. J. Clean. Prod. 2006, 14, 472–486. [Google Scholar] [CrossRef]

- Loknath, Y.; Azeem, B.A. Green Management–Concept and Strategies. In Proceedings of the National Conference on Marketing and Sustainable Development, New Delhi, India, 13–14 October 2017; pp. 688–702. Available online: http://www.aims-international.org/myconference/cd/PDF/MSD4-6111-Done.pdf (accessed on 5 May 2020).

- Banerjee, S.B. Corporate Environmentalism: The Construct and Its Measurement. J. Bus. Res. 2002, 55, 177–191. [Google Scholar] [CrossRef]

- Cannatelli, B.; Pedrini, M.; Grumo, M. The Effect of Brand Management and Product Quality on Firm Performance: The Italian Craft Brewing Sector. J. Food Prod. Mark. 2015, 23, 303–325. [Google Scholar] [CrossRef]

- Garvin, D.A. What Does “Product Quality” Really Means? Sloan Manag. Rev. 1984, 28, 25–43. Available online: http://www.oqrm.org/English/What_does_product_quality_really_means.pdf (accessed on 5 May 2020).

- Chadwick, S.; Holt, M. Utilising Latent Brand Equity as a Foundation for Building Global Sport. In Proceedings of the 2007 Academy of Marketing Science (AMS) Annual Conference, Coral Cables, Florida, USA, 23–26 May 2007; pp. 90–98. [Google Scholar] [CrossRef]

- Javeed, A.; Mokhtar, S.S.b.M.; Othman, I.b.L.; Khan, M.Y. Perceived Product Quality: Role of Extrinsic Cues. J. Manag. Sci. 2018, 11, 196–220. [Google Scholar]

- Paillé, P.; Mejía-Morelos, J.H. Antecedents of Pro-Environmental Behaviours at Work: The Moderating Influence of Psychological Contract Breach. J. Environ. Psychol. 2014, 38, 124–131. [Google Scholar] [CrossRef]

- Renwick, D.W.S.; Redman, T.; Maguire, S. Green Human Resource Management: A Review and Research Agenda. Int. J. Manag. Rev. 2013, 15, 1–14. [Google Scholar] [CrossRef] [Green Version]

- Roscoe, S.; Subramanian, N.; Jabbour, C.J.C.; Chong, T. Green Human Resource Management and the Enablers of Green Organisational Culture: Enhancing a Firm’s Environmental Performance for Sustainable Development. Bus. Strateg. Environ. 2019, 28, 737–749. [Google Scholar] [CrossRef]

- Daily, B.F.; Bishop, J.W.; Massoud, J.A. The Role of Training and Empowerment in Environmental Performance: A Study of the Mexican Maquiladora Industry. Int. J. Oper. Prod. Manag. 2012, 32, 631–647. [Google Scholar] [CrossRef]

- Glover, W.J.; Farris, J.A.; Van Aken, E.M.; Doolen, T.L. Critical Success Factors for the Sustainability of Kaizen Event Human Resource Outcomes: An Empirical Study. Intern. J. Prod. Econ. 2011, 132, 197–213. [Google Scholar] [CrossRef]

- Jaramillo, J.Á.; Sossa, J.W.Z.; Mendoza, G.L.O. Barriers to Sustainability for Small and Medium Enterprises in the Framework of Sustainable Development—Literature Review. Bus. Strateg. Environ. 2018, 28, 512–524. [Google Scholar] [CrossRef]

- Kumar, V. Evaluating the Financial Performance and Financial Stability of National Commercial Banks in the UAE. Int. J. Bus. Glob. 2016, 16, 109–128. [Google Scholar] [CrossRef]

- Majid, A.; Yasir, M.; Yasir, M.; Javed, A. Nexus of Institutional Pressures, Environmentally Friendly Business Strategies, and Environmental Performance. Corp. Soc. Responsib. Environ. Manag. 2019, 27, 706–716. [Google Scholar] [CrossRef]

- Palacios-argüello, L.; Gondran, N.; Nouira, I.; Girard, M.; Gonzalez-feliu, J. Which Is the Relationship between the Product’s Environmental Criteria and the Product Demand? Evidence from the French Food Sector. J. Clean. Prod. 2019, 244, 118588. [Google Scholar] [CrossRef] [Green Version]

- Laari, S.; Toyli, J.; Ojala, L. The Effect of a Competitive Strategy and Green Supply Chain Management on the Financial and Environmental Performance of Logistics Service Providers. Bus. Strateg. Environ. 2018, 27, 872–883. [Google Scholar] [CrossRef]

- Fores, B. Beyond Gathering the ‘Low-Hanging Fruit’ of Green Technology for Improved Environmental Performance: An Empirical Examination of the Moderating Effects of Proactive Environmental Management and Business Strategies. Sustainability 2019, 11, 6299. [Google Scholar] [CrossRef] [Green Version]

- Li, S.; Qiao, J.; Cui, H.; Wang, S. Realizing the Environmental Benefits of Proactive Environmental Strategy: The Roles of Green Supply Chain Integration and Relational Capability. Sustainability 2020, 12, 2907. [Google Scholar] [CrossRef] [Green Version]

- Luu, T.T. Integrating Green Strategy and Green Human Resource Practices to Trigger Individual and Organizational Green Performance: The Role of Environmentally-Specific Servant Leadership. J. Sustain. Tour. 2020, 28, 1193–1222. [Google Scholar] [CrossRef]

- Nielsen, I.; Majumder, S.; Szwarc, E. Impact of Strategic Cooperation under Competition on Green Product Manufacturing. Sustainbility 2020, 12, 10248. [Google Scholar] [CrossRef]

- Wang, Z.; Sarkis, J. Corporate Social Responsibility Governance, Outcomes, and Financial Performance. J. Clean. Prod. 2017, 162, 1607–1616. [Google Scholar] [CrossRef]

- Chen, F.; Ngniatedema, T.; Li, S. A Cross-Country Comparison of Green Initiatives, Green Performance and Financial Performance. Manag. Decis. 2018, 56, 1008–1032. [Google Scholar] [CrossRef]

- Trumpp, C.; Guenther, T. Too Little or Too Much? Exploring U-Shaped Relationships between Corporate Environmental Performance and Corporate Financial Performance. Bus. Strateg. Environ. 2015, 26, 49–68. [Google Scholar] [CrossRef]

- Chen, J.; Liu, L. Profiting from Green Innovation: The Moderating Effect of Competitive Strategy. Sustainbility 2019, 11, 15. [Google Scholar] [CrossRef] [Green Version]

- Qasrawi, B.T.; Almahamid, S.M.; Qasrawi, S.T. The Impact of TQM Practices and KM Processes on Organisational Performance: An Empirical Investigation. Int. J. Qual. Reliab. Manag. 2017, 34, 1034–1055. [Google Scholar] [CrossRef]

- Abbas, J. Impact of Total Quality Management on Corporate Green Performance through the Mediating Role of Corporate Social Responsibility. J. Clean. Prod. 2020, 242, 118458. [Google Scholar] [CrossRef]

- Zhang, D.; Rong, Z.; Ji, Q. Green Innovation and Firm Performance: Evidence from Listed Companies in China. Resour. Conserv. Recycl. 2019, 144, 48–55. [Google Scholar] [CrossRef]

- Cai, W.; Li, G. The Drivers of Eco-Innovation and Its Impact on Performance: Evidence from China. J. Clean. Prod. 2018, 176, 110–118. [Google Scholar] [CrossRef]

- Chen, Y.; Tang, G.; Jin, J.; Li, J.; Paille, P. Linking Market Orientation and Environmental Performance: The Influence of Environmental Strategy, Employee’s Environmental Involvement, and Environmental Product Quality. J. Bus. Ethics 2015, 127, 479–500. [Google Scholar] [CrossRef]

- Armstrong, A.; Stedman, R.C. Understanding Local Environmental Concern: The Importance of Place. Rural Sociol. 2018, 1–30. [Google Scholar] [CrossRef]

- Shu, C.; Zhou, K.Z.; Xiao, Y.; Gao, S. How Green Management Influences Product Innovation in China: The Role of Institutional Benefits. J. Bus. Ethics 2014, 133, 471–485. [Google Scholar] [CrossRef] [Green Version]

- Brady, K.; Henson, P.; Fava, J.A. Sustainability, Eco-Efficiency, Life-Cycle Management and Business Strategy. Environ. Qual. Manag. 1999, 8, 33–41. [Google Scholar] [CrossRef]

- Keszey, T. Environmental Orientation, Sustainable Behaviour at the Firm-Market Interface and Performance. J. Clean. Prod. 2019, 243, 118524. [Google Scholar] [CrossRef]

- Habib, M.S.; Sarkar, B.; Tayyab, M.; Wajid, M.; Hussain, A.; Ullah, M.; Omair, M.; Waqas, M. Large-Scale Disaster Waste Management under Uncertain Environment. J. Clean. Prod. 2019, 212, 200–222. [Google Scholar] [CrossRef]

- Calza, F.; Parmentola, A.; Tutore, I. Types of Green Innovations: Ways of Implementation in a Non-Green Industry. Sustainability 2017, 9, 1301. [Google Scholar] [CrossRef] [Green Version]

- Christmann, P. Effects of “Best Practices” of Environmental Management on Cost Advantage: The Role of Complementary Assets. Acad. Manag. J. 2000, 43, 663–680. [Google Scholar] [CrossRef] [Green Version]

- Barney, J. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Chen, H.; Daugherty, P.J.; Landry, T.D. Supply Chain Process Integration: A Theoretical Framework. J. Bus. Logist. 2009, 30, 27–46. [Google Scholar] [CrossRef]

- Judge, W.Q.; Douglas, T.J. Performance Implications of Incorporating Natural Environmental Issues into the Strategic Planning Process: An Empirical Assessment. J. Manag. Stud. 1998, 35, 241–262. [Google Scholar] [CrossRef]

- Harman, H.H. Modern Factor Analysis, 2nd ed.; The University of Chicago Press: Chicago, IL, USA, 1967. [Google Scholar]

- Hair, J.F.; Sarstedt, M.; Hopkins, L.; Kuppelwieser, V.G. Partial Least Squares Structural Equation Modeling (PLS-SEM): An Emerging Tool in Business Research. Eur. Bus. Rev. 2014, 26, 106–121. [Google Scholar] [CrossRef]

- Chan, R.Y.K. Corporate Environmentalism Pursuit by Foreign Firms Competing in China. J. World Bus. 2010, 45, 80–92. [Google Scholar] [CrossRef]

- Menguc, B.; Auh, S.; Ozanne, L. The Interactive Effect of Internal and External Factors on a Proactive Environmental Strategy and Its Influence on a Firm’s Performance. J. Bus. Ethics 2010, 94, 279–298. [Google Scholar] [CrossRef]

- Albino, V.; Balice, A.; Dangelico, R.M. Environmental Strategies and Green Product Development: An Overview on Sustainability-Driven Companies. Bus. Strateg. Environ. 2009, 96, 83–96. [Google Scholar] [CrossRef]

- Gilal, F.G.; Ashraf, Z.; Gilal, N.G.; Gilal, R.G.; Chaana, N.A. Promoting Environmental Performance through Green Human Resource Management Practices in Higher Education Institutions: A Moderated Mediation Model. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 1–12. [Google Scholar] [CrossRef]

- Kim, Y.J.; Gon, W.; Choi, H.; Phetvaroon, K. The Effect of Green Human Resource Management on Hotel Employees’ Eco-Friendly Behavior and Environmental Performance. Int. J. Hosp. Manag. 2019, 76, 83–93. [Google Scholar] [CrossRef]

- Ninlawan, C.; Seksan, P.; Tossapol, K.; Pilada, W. The Implementation of Green Supply Chain Management Practices in Electronics Industry. In Proceedings of the International MultiConference of Engineers and Computer Scientists, Hong Kong, China, 17–19 March 2010; Volume 3, pp. 1–6. [Google Scholar]

| Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

,

,

{kind=link}