Ex-Ante Study of Biofuel Policies–Analyzing Policy-Induced Flexibility

Abstract

:1. Introduction

Biofuel Promotion Schemes

2. Methods and Data

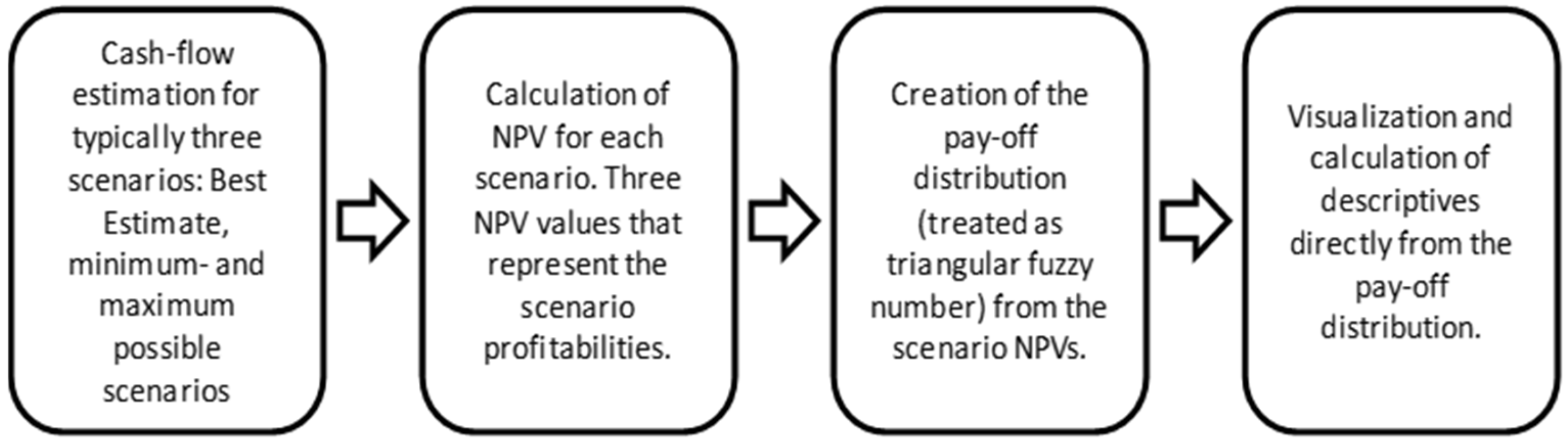

2.1. Pay-Off Method

2.2. Simulation-Based Profitability Analysis and Simulation Decomposition

2.3. Numerical Assumptions

3. Results

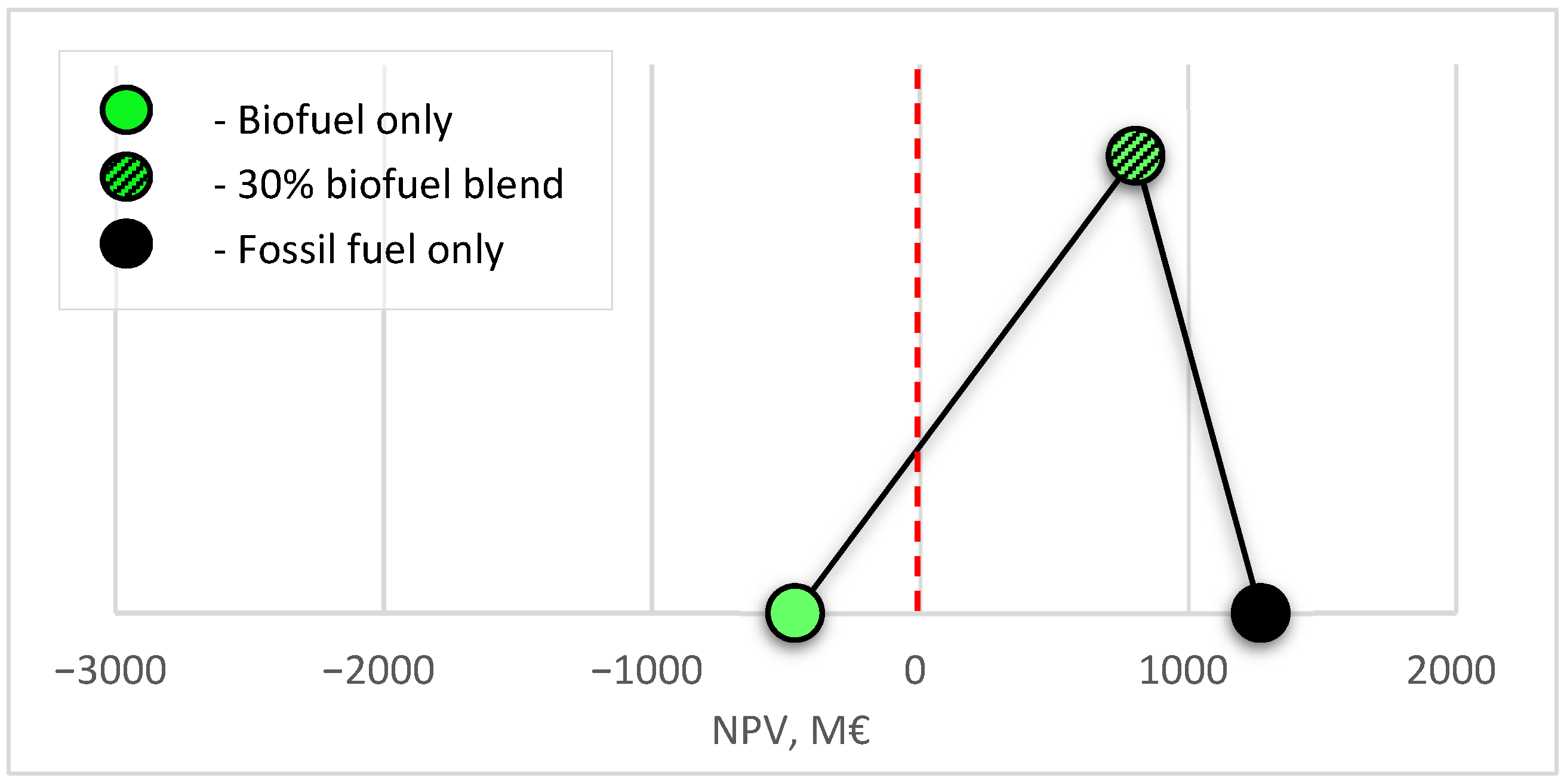

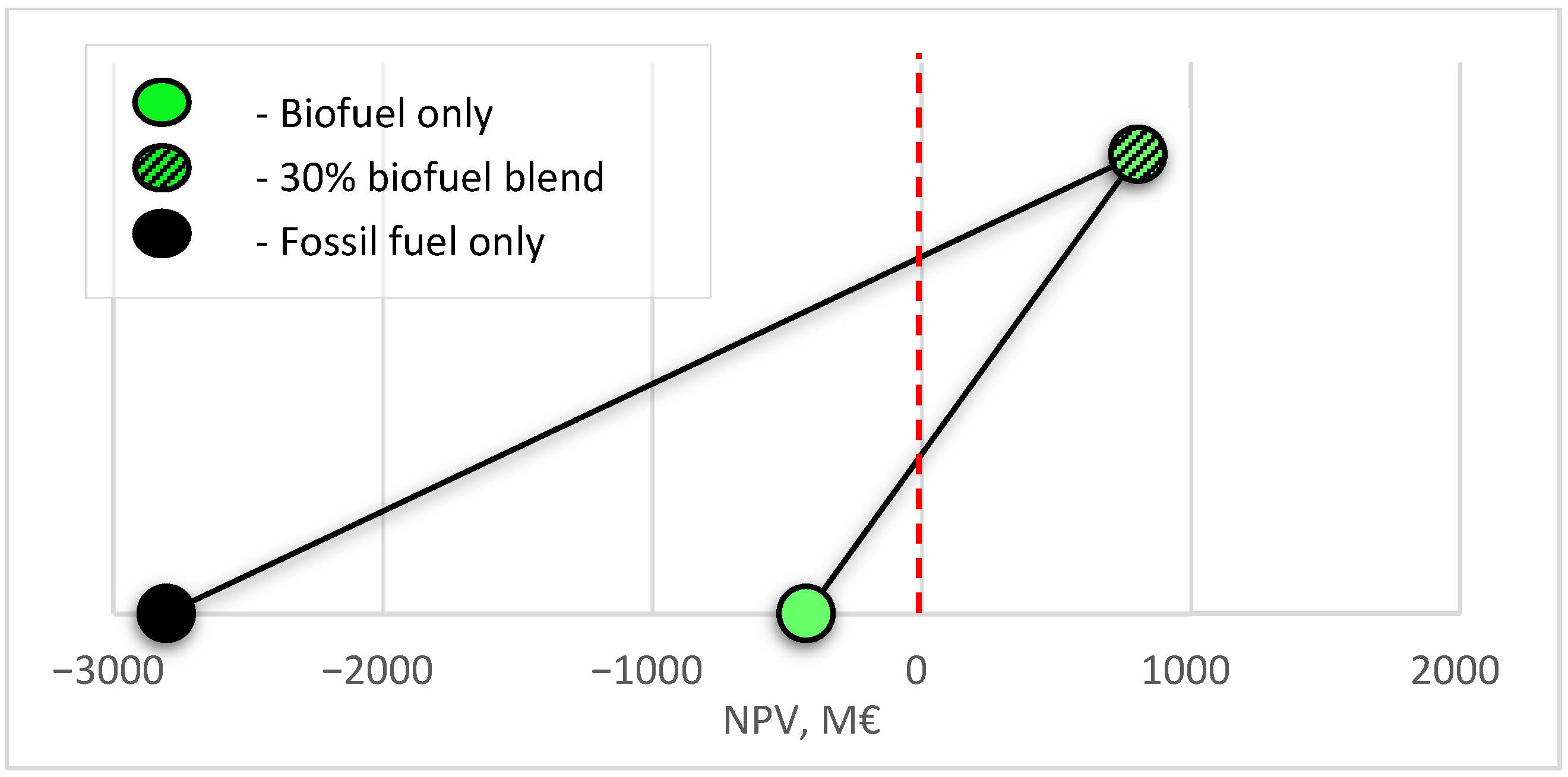

3.1. The Pay-Off Method Based Analysis

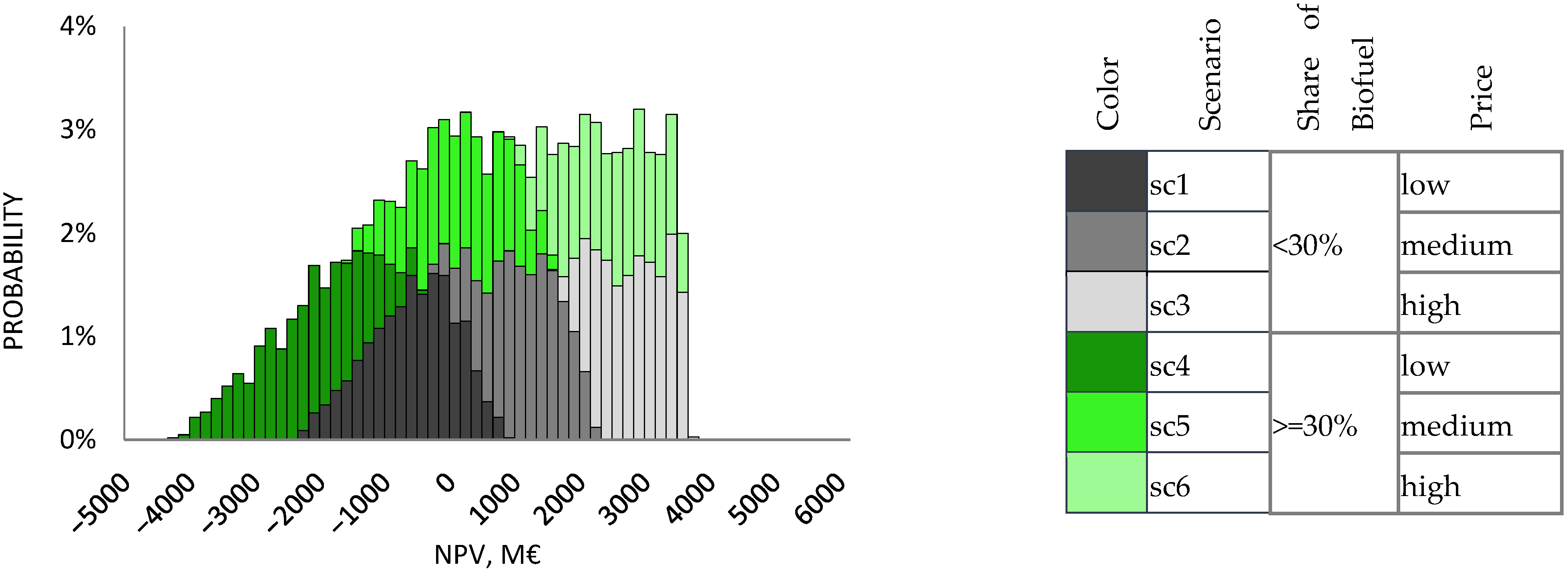

3.2. Simulation Decomposition Based Analysis

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- REN21 Renewables 2020 Global Status Report. 2020. Available online: http://www.ren21.net/wp-content/uploads/2018/06/17-8652_GSR2018_FullReport_web_final_.pdf (accessed on 13 December 2021).

- European Environmental Agency Urban Sustainability: How Can Cities Become Sustainable? Available online: https://www.eea.europa.eu/themes/sustainability-transitions/urban-environment (accessed on 13 December 2021).

- IEA Global EV Outlook 2021. Available online: https://www.iea.org/reports/global-ev-outlook-2021 (accessed on 13 December 2021).

- IEA Transport Biofuels. Available online: https://www.iea.org/reports/transport-biofuels (accessed on 13 December 2021).

- IEA Projected Costs of Generating Electricity 2020. Available online: https://www.iea.org/reports/projected-costs-of-generating-electricity-2020 (accessed on 13 December 2021).

- Kozlova, M.; Lohrmann, A. Steering Renewable Energy Investments in Favor of Energy System Reliability: A Call for a Hybrid Model. Sustainability 2021, 13, 13510. [Google Scholar] [CrossRef]

- Kozlova, M.; Overland, I. Combining capacity mechanisms and renewable energy support: A review of the international experience. Renew. Sustain. Energy Rev. 2021; 111878, in press. [Google Scholar] [CrossRef]

- Jakob, P.; Wagner, J. Optimal Allocation of Variable Renewable Energy Considering Contributions to Security of Supply. Energy J. 2021, 42, 1–35. [Google Scholar]

- Sendstad, L.H.; Hagspiel, V.; Mikkelsen, W.J.; Ravndal, R.; Tveitstøl, M. The impact of subsidy retraction on European renewable energy investments. Energy Policy 2022, 160, 112675. [Google Scholar] [CrossRef]

- Boomsma, T.K.; Linnerud, K. Market and policy risk under different renewable electricity support schemes. Energy 2015, 89, 435–448. [Google Scholar] [CrossRef]

- Kitzing, L.; Fitch-Roy, O.; Islam, M.; Mitchell, C. An evolving risk perspective for policy instrument choice in sustainability transitions. Environ. Innov. Soc. Transit. 2020, 35, 369–382. [Google Scholar] [CrossRef]

- Habermacher, F.; Lehmann, P. Commitment Versus Discretion in Climate and Energy Policy. Environ. Resour. Econ. 2020, 76, 39–67. [Google Scholar] [CrossRef] [Green Version]

- Trigeorgis, L.; Tsekrekos, A.E. Real Options in Operations Research: A Review. Eur. J. Oper. Res. 2018, 270, 1–24. [Google Scholar] [CrossRef] [Green Version]

- Kozlova, M. Real option valuation in renewable energy literature: Research focus, trends and design. Renew. Sustain. Energy Rev. 2017, 80, 180–196. [Google Scholar] [CrossRef]

- Savolainen, J.; Collan, M.; Luukka, P. Analyzing operational real options in metal mining investments with a system dynamic model. Eng. Econ. 2016, 62, 54–72. [Google Scholar] [CrossRef]

- De Oliveira, D.L.; Brandao, L.E.; Igrejas, R.; Gomes, L.L. Switching outputs in a bioenergy cogeneration project: A real options approach. Renew. Sustain. Energy Rev. 2014, 36, 74–82. [Google Scholar] [CrossRef]

- Kozlova, M.; Fleten, S.; Hagspiel, V. Investment timing and capacity choice under rate-of-return regulation for renewable energy support. Energy 2019, 174, 591–601. [Google Scholar] [CrossRef]

- Fleten, S.; Fram, B.; Ledsaak, M.; Mehl, S.; Røstum, O.E.; Ullrich, C.J. The Effect of Capacity Payments on Peaking Generator Availability in PJM; Local Energy, Global Markets. In Proceedings of the 42nd IAEE International Conference, Montreal, QC, Canada, 29 May–1 June 2019. [Google Scholar]

- Savolainen, J.; Pedretti, D.; Collan, M. Incorporating Hydrologic Uncertainty in Industrial Economic Models: Implications of Extreme Rainfall Variability on Metal Mining Investments. Mine Water Environ. 2019, 38, 447–462. [Google Scholar] [CrossRef] [Green Version]

- Kitzing, L.; Juul, N.; Drud, M.; Boomsma, T.K. A real options approach to analyse wind energy investments under different support schemes. Appl. Energy 2017, 188, 83–96. [Google Scholar] [CrossRef]

- Collan, M. The Pay-off Method: Re-Inventing Investment Analysis; CreateSpace Inc.: Charleston, NC, USA, 2012. [Google Scholar]

- Kozlova, M.; Collan, M.; Luukka, P. Simulation decomposition: New approach for better simulation analysis of multi-variable investment projects. Fuzzy Econ. Rev. 2016, 21, 3. [Google Scholar] [CrossRef]

- Collan, M.; Haahtela, T.; Kyläheiko, K. On the usability of real option valuation model types under different types of uncertainty. Int. J. Bus. Innov. Res. 2016, 11, 18–37. [Google Scholar] [CrossRef]

- Kozlova, M.; Collan, M.; Luukka, P. New investment decision-making tool that combines a fuzzy inference system with real option analysis. Fuzzy Econ. Rev. 2018, 23, 63–92. [Google Scholar] [CrossRef]

- Kozlova, M.; Yeomans, J.S. Multi-Variable Simulation Decomposition in Environmental Planning: An Application to Carbon Capture and Storage. J. Environ. Inform. Lett. 2019, 1, 20–26. [Google Scholar] [CrossRef] [Green Version]

- Hietanen, L.; Kozlova, M.; Collan, M. Analyzing Renewable Energy Policies–Using the Pay-off Method to Study the Finnish Auction-Based Renewable Energy Policy. J. Environ. Inform. Lett. 2020, 4, 50–56. [Google Scholar] [CrossRef]

- European Commission European Green Deal. Available online: https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal_en (accessed on 15 June 2021).

- European Commission Renewable Energy—Recast to 2030 (RED II). Available online: https://ec.europa.eu/jrc/en/jec/renewable-energy-recast-2030-red-ii (accessed on 15 June 2021).

- Finnish Parliament Act on the Use of Biofuels in Transport 2007/446 [in Finnish]. 2007. Available online: https://finlex.fi/fi/laki/ajantasa/2007/20070446 (accessed on 19 December 2021).

- International Council on Clean Transportation Advanced Biofuel Policies in Select EU Member States. 2018. Available online: https://theicct.org/sites/default/files/publications/Advanced_biofuel_policy_eu_update_20181130.pdf (accessed on 19 December 2021).

- Finnish Parliament Government Proposal HE 199 /2018 to the Parliament for Laws to Promote the Use of Biofuel [in Finnish]. 2018. Available online: https://www.eduskunta.fi/FI/vaski/HallituksenEsitys/Sivut/HE_199+2018.aspx (accessed on 19 December 2021).

- Finnish Tax Administration Tax Rates on Liquid Fuels. Available online: https://www.vero.fi/yritykset-ja-yhteisot/verot-ja-maksut/valmisteverotus/nestemaiset-polttoaineet/verotaulukot/ (accessed on 15 June 2021).

- Fisher, I. The Rate of Interest: Its Nature, Determination and Relation to Economic Phenomena; Macmillan: New York, NY, USA, 1907. [Google Scholar]

- Collan, M.; Fullér, R.; Mezei, J. A fuzzy pay-off method for real option valuation. J. Appl. Math. Decis. Sci. 2009, 2009, 165–169. [Google Scholar] [CrossRef] [Green Version]

- Stoklasa, J.; Luukka, P.; Collan, M. Possibilistic fuzzy pay-off method for real option valuation with application to research and development investment analysis. Fuzzy Sets Syst. 2021, 409, 153–169. [Google Scholar] [CrossRef]

- Bednyagin, D.; Gnansounou, E. Real options valuation of fusion energy R&D programme. Energy Policy 2011, 39, 116–130. [Google Scholar]

- Borges, R.E.P.; Dias, M.A.G.; Neto, A.D.D.; Meier, A. Fuzzy pay-off method for real options: The center of gravity approach with application in oilfield abandonment. Fuzzy Sets Syst. 2018, 353, 111–123. [Google Scholar] [CrossRef]

- Kozlova, M.; Collan, M.; Luukka, P. Comparison of the Datar-Mathews Method and the Fuzzy Pay-Off Method through Numerical Results. Adv. Decis. Sci. 2016, 2016, 7836784. [Google Scholar] [CrossRef] [Green Version]

- Hassanzadeh, F.; Collan, M.; Modarres, M. A practical approach to R&D portfolio selection using the fuzzy pay-off method. Fuzzy Syst. IEEE Trans. 2012, 20, 615–622. [Google Scholar]

- Collan, M.; Luukka, P. Evaluating R&D projects as investments by using an overall ranking from four new fuzzy similarity measure-based TOPSIS variants. Fuzzy Syst. IEEE Trans. 2014, 22, 505–515. [Google Scholar]

- Collan, M.; Kyläheiko, K. Forward-looking valuation of strategic patent portfolios under structural uncertainty. J. Intellect. Prop. Rights 2013, 18, 230–241. [Google Scholar]

- Ashby, W.R. Requisite variety and its implications for the control of complex systems. In Facets of Systems Science; Springer: Berlin/Heidelberg, Germany, 1991; pp. 405–417. [Google Scholar]

- Mooney, C.Z. Monte Carlo Simulation; Sage Publications: New York, NY, USA, 1997; Volume 116. [Google Scholar]

- Rubinstein, R.Y.; Kroese, D.P. Simulation and the Monte Carlo Method; John Wiley & Sons: Hoboken, NJ, USA, 2016; Volume 10. [Google Scholar]

- Platon, V.; Constantinescu, A. Monte Carlo Method in risk analysis for investment projects. Procedia Econ. Financ. 2014, 15, 393–400. [Google Scholar] [CrossRef] [Green Version]

- Kwak, Y.H.; Ingall, L. Exploring Monte Carlo simulation applications for project management. Risk Manag. 2007, 9, 44–57. [Google Scholar] [CrossRef]

- Kozlova, M.; Yeomans, J.S. Monte Carlo Enhancement via Simulation Decomposition: A “Must-Have” Inclusion for Many Disciplines. In INFORMS Transactions on Education; Institute for Operations Research and the Management Sciences (INFORMS): Catonsville, MD, USA, 2020. [Google Scholar] [CrossRef]

- Hietanen, L. Comparative Analysis of Renewable Energy Policy Schemes of Finland; LUT University: Lappeenranta, Finland, 2020. [Google Scholar]

- Deviatkin, I.; Kozlova, M.; Yeomans, J.S. Simulation decomposition for environmental sustainability: Enhanced decision-making in carbon footprint analysis. Socioecon. Plann. Sci. 2021, 75, 100837. [Google Scholar] [CrossRef]

- Ruponen, I. Profitability Analysis of Biofuels and the Impact of Biofuel Policies in Finland; LUT University: Lappeenranta, Finland, 2021. [Google Scholar]

- Festel, G.; Würmseher, M.; Rammer, C.; Boles, E.; Bellof, M. Modelling production cost scenarios for biofuels and fossil fuels in Europe. J. Clean. Prod. 2014, 66, 242–253. [Google Scholar] [CrossRef] [Green Version]

- Brown, T.R.; Thilakaratne, R.; Brown, R.C.; Hu, G. Regional differences in the economic feasibility of advanced biorefineries: Fast pyrolysis and hydroprocessing. Energy Policy 2013, 57, 234–243. [Google Scholar] [CrossRef] [Green Version]

- Landälv, I.; Waldheim, L.; van den Heuvel, E.; Kalligeros, S. Building Up the Future Cost of Biofuel; European Commission, Sub Group on Advanced Biofuels: Brussels, Belgium, 2017. [Google Scholar]

- IEA Fuel Price Distribution. Available online: https://www.iea.org/data-and-statistics/charts/fuel-price-distribution-2019 (accessed on 19 December 2021).

- Collan, M.; Fedrizzi, M.; Luukka, P. A multi-expert system for ranking patents: An approach based on fuzzy pay-off distributions and a TOPSIS–AHP framework. Expert Syst. Appl. 2013, 40, 4749–4759. [Google Scholar] [CrossRef]

- Kozlova, M.; Collan, M.; Luukka, P. Renewable Energy in Emerging Economies: Shortly Analyzing the Russian Incentive Mechanisms for Renewable Energy Investments. In Proceedings of the International Research Conference “GSOM Emerging Markets Conference-2015: Business and Government Perspectives”, New York, NY, USA, 15–17 October 2015. [Google Scholar]

- Kozlova, M.; Yeomans, J. Visual Analytics in Environmental Decision-Making: A Comparison of Overlay Charts versus Simulation Decomposition. J. Environ. Inform. Lett. 2021, 4, 93–100. [Google Scholar] [CrossRef]

- Enciso, S.R.A.; Fellmann, T.; Dominguez, I.P.; Santini, F. Abolishing biofuel policies: Possible impacts on agricultural price levels, price variability and global food security. Food Policy 2016, 61, 9–26. [Google Scholar] [CrossRef]

- Moncada, J.A.; Verstegen, J.A.; Posada, J.A.; Junginger, M.; Lukszo, Z.; Faaij, A.; Weijnen, M. Exploring policy options to spur the expansion of ethanol production and consumption in Brazil: An agent-based modeling approach. Energy Policy 2018, 123, 619–641. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter | Value | Comment |

|---|---|---|

| Time horizon | 20 years | Corresponds to the average lifetime of a biofuel plant, see, e.g., [52] |

| Corporate tax | 20% | The corporate tax-rate in Finland |

| Discount rate | 10% | Discount rate, see e.g., [52] |

| Price of fuel (taxes included) | 1.12 €/liter | The average price of Diesel in Finland 2012–2019 |

| Fossil fuel (diesel) | ||

| Plant size | 1166 million liters per year | Calculated to get 30% biofuel blend with 500 Ml/year biofuel plant |

| Operating costs | 0.37 €/liter | Estimated operating costs, [51] |

| Biofuel (renewable diesel) | ||

| Plant size | 500 million liters per year | Estimates from [53] |

| Operating costs | 0.86 €/liter | |

| Investment cost | 430 M€ | |

| Assumptions related to policies | ||

| Tax-relief | 0.26 €/ liter | Based on the Finnish biofuel policy, [32] |

| Penalties | 1.36 €/ liter | Based on the Finnish biofuel policy, [31] |

| Financial incentive | 0.26 €/ liter | The same as tax-relief to provide the exact profitability for the 30% blend scenario |

| Parameter | Range | States | |

|---|---|---|---|

| Biodiesel production size, million liters per year | 0–1000 | <30% | [0, 500) |

| ≥30% | [500, 1000] | ||

| Price of fuel, €/liter | 1.00–1.50 | low | [1.00, 1.17) |

| medium | [1.17, 1.34) | ||

| high | [1.34, 1.50] |

| Pay-Off Method | Simulation Decomposition | |

|---|---|---|

| Fuel mix variation only | Fixed fossil fuel production + variable size of biofuel production + price uncertainty | |

| No support |  |  |

| Financial incentive |  |  |

| Penalties & tax-relief |  |  |

| Legend |  |  |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ruponen, I.; Kozlova, M.; Collan, M. Ex-Ante Study of Biofuel Policies–Analyzing Policy-Induced Flexibility. Sustainability 2022, 14, 147. https://doi.org/10.3390/su14010147

Ruponen I, Kozlova M, Collan M. Ex-Ante Study of Biofuel Policies–Analyzing Policy-Induced Flexibility. Sustainability. 2022; 14(1):147. https://doi.org/10.3390/su14010147

Chicago/Turabian StyleRuponen, Inka, Mariia Kozlova, and Mikael Collan. 2022. "Ex-Ante Study of Biofuel Policies–Analyzing Policy-Induced Flexibility" Sustainability 14, no. 1: 147. https://doi.org/10.3390/su14010147

APA StyleRuponen, I., Kozlova, M., & Collan, M. (2022). Ex-Ante Study of Biofuel Policies–Analyzing Policy-Induced Flexibility. Sustainability, 14(1), 147. https://doi.org/10.3390/su14010147