1. Introduction

The venture investment market in Korea has experienced unprecedented rapid growth over the past decade. To solve the current problem of long-term low growth and job creation, the Korean government has proposed revitalizing start-ups as an alternative. As a result, the venture investment market has achieved rapid development not only in quantitative aspects, such as an expansion of investment resources and increase in investment scale, but also in qualitative aspects, such as the inflow of human resources into the venture investment market and an increase in private investment [

1].

The amount of capital committed to new venture funds, which was

$572 million in 2012, increased to

$7055 million in 2021, approximately 12 times in 10 years. New venture investments also increased significantly from

$942 million in 2012 to

$5.86 billion in 2021. The expansion in the amount of capital committed into new venture funds and investment scale is the result of an increase in government finances and the entry of various private limited partners (LPs) into the venture investment market [

2].

The proportion of government-related LPs among all venture funds fell from 33% in 2013 to 29.8% in 2021, while the proportion of private LPs increased from 67% in 2013 to 70.2% in 2021. Additionally, the composition of private LPs has diversified, ranging from financial institutions to general corporations, pension funds, mutual aid associations, and individuals [

2].

From an institutional perspective, the venture investment market, which was centered on investment companies for the establishment of small and medium enterprises, has diversified into new technology venture capitalists, limited liability company-type venture investment companies, securities companies, asset management companies, and accelerators.

Investment vehicles in the venture investment market have also diversified from venture investment associations to new technology investment associations, private equity funds specializing in start-ups or venture businesses, and individual investment associations.

The venture investment market has also shown many changes in terms of changes in human resources. In 2012, the number of professionals registered with the Korean Venture Capital Association was 692, which had increased to 1289 by 2021. (The Korean Venture Capital Association is entrusted with the management of professionals in investment companies for the establishment of small and medium enterprises by the Ministry of SMEs and Startups in Korea to establish an efficient manpower management system under Korea’s Venture Investment Promotion Act.) In addition, the education majors and backgrounds in human resources have diversified from business and economics majors and financial institutions backgrounds to engineering, natural science, and medicine based on the Korean Venture Capital Association website’s data. This indicates increased interest of workers with experience in various diverse fields, as the venture investment market grows. The demand for manpower with expertise in each field increases as venture companies’ technology levels and business fields become diversified and specialized [

3].

Amid these changes in the venture investment environment, investors have had to develop evaluation indicators to determine whether to invest, and many studies have been conducted to identify the factors that influence the performance of venture funds to provide primary data. Research on the factors that create the performance of venture funds is largely divided into internal and external environmental factors of funds [

1].

Internal factors refer to studies on the impact of venture funds and general partner (GP) characteristics such as fund period, investment field, fund size, and GPs’ capabilities on fund performance, and have been studied by Kaplan and Schoar [

4], Gompers, Kovner, Lerner, and Scharfstein [

5], Humphery-Jenner [

6], Robinson and Sensoy [

7], Harris, Jenkinson, and Kaplan [

8], Cho and Park [

9], Chae, Kim, and Ku [

10], Oh, Choi, and Park [

11], and others. The results of studies on the effects of internal factors on fund performance often differ from research to study.

External environmental factors include studies on the impact of economic cycles, securities markets, venture investment markets, and exit market environments on fund performance, and have been studied by Gompers and Lerner [

12], Kaplan and Schoar [

4], Diller and Kaserer [

13], Robinson and Sensory [

7], Chae et al. [

10], Oh et al. [

11], Choi and Kim [

1], and others. Most studies on the effect of the external environment on fund performance show similar results, and many results indicate that the securities market and the economic cycle have a positive (+) effect on fund performance, and the venture investment market (scale of venture fund inflow) has a negative (−) effect.

Venture funds are in the form of private equity funds, and their operational performance is defined according to the investor’s purpose, which is not limited to investors’ common goals and financial purposes. In addition, venture funds are also affected by the governance structure and operational purpose of GPs because ownership and management are not completely separated, and GPs also have the status of investors. Moreover, fund managers who manage funds as agents, are paid incentives according to fund performance and become direct stakeholders of the fund because their management performance is used as an individual competency evaluation factor when proposing other venture fund formations to investors. Therefore, GPs, LPs, and fund managers are major stakeholders in venture funds, who have a great influence on fund performance [

14].

Nevertheless, little is known about the impact of venture funds’ human resources and investor composition on their performance. Furthermore, in existing studies, little is known about the impact of fund type or GP governance. Therefore, this study aims to analyze the performance factors of venture funds in terms of human resources of directly operating venture funds and the composition of investors supplying funds to venture funds and further verify the difference in impact based on the fund type or GP governance structure.

This is of theoretical significance in that it analyzes performance factors focusing on stakeholders of venture funds, which were not covered in previous studies. In addition, it provides theoretical implications in that it confirms differences between groups, such as GP’s governance structure and fund types. Moreover, regarding practical values, this study aims to provide the primary data necessary for rational decision-making when the government is establishing a policy for supplying funds to the venture investment market or establishing evaluation standards for investors to decide whether to invest in venture funds.

2. Theoretical Background and Hypothesis Setting

2.1. Human Resources and Fund Performance of Venture Funds

One of the most crucial evaluation factors for LPs in selecting venture fund GPs is fund managers (key persons). Therefore, the personal information of the fund manager is stated in the articles of association, and the dismissal and change of the fund manager (key person) (The fund manager (key person) is a professional in charge of the investment review of venture funds. In the case of venture investment associations, the fund manager is to be specified in the application form when registering the fund under Korea’s Venture Investment Promotion Act.) are limited only through the resolution of the General Assembly. LPs may require minimum manpower depending on the size and types of venture funds and may limit the number and size of funds that can be operated by fund managers. This improves management concentration by restricting the fund manager from concurrently serving as a manager for other funds until the fund is exhausted to a certain percentage. If the fund manager is to be changed during a venture fund operation, investors demand that the GPs’ management fee be reduced through agreement, and replacement fund managers corresponding to existing fund managers be provided. In some cases, fund operations are suspended [

15]. Consequently, fund managers have a significant impact on fund performance; therefore, some regulations limit changes in fund managers in various ways when forming venture funds.

Nevertheless, there are few direct studies on the effects of human resource factors, including the characteristics of fund managers, on venture fund performance.

This is because venture funds are mainly in the form of private equity funds, so it is challenging to secure data and ensure data accuracy [

8]. Therefore, we would like to derive the analytical direction and implications of this study through studies targeting mutual funds (A mutual fund is a fund that invests investment assets in securities after recruiting investors and distributes profits to investors, generally investing in listed stocks, bonds, and derivatives.) that mainly invest in listed companies.

Regarding the experience of replacing mutual funds’ managers, Khorana [

16] found that funds with poor performance showed improvement after replacing fund managers. However, funds with good performance deteriorated after replacement, and Park and Joo [

17] drew the same conclusions. Kim and Chong [

18] analyzed the case of moving to another company after replacing the fund manager and staying at the company. The results showed that when the fund manager moved out, fund performance declined, but when it remained in the same company, the fund’s performance improved.

Taken together, it can be seen that fund performance deteriorated when it changed due to the voluntary movement of fund managers (such as turnover), but when the company took measures to change the fund manager due to poor fund performance, fund performance improved. Mutual funds have daily returns on listed companies as their main investment target. Conversely, venture funds are mainly invested in unlisted companies; therefore, there is a limit to measuring returns during fund operations. In addition, because the replacement of fund managers in venture funds requires the consent of LPs, it is reasonable to view most fund manager changes in venture funds as voluntary transfers.

Previous studies on the human resource factors of funds have indicated different results. Golec [

19] analyzed the relationship between human resource variables such as a fund manager’s career, education period, MBA degree, and operational performance. As a result, it was found that possession of more experience and MBA degrees implied better achievements of the manager. In addition, Chevalier and Ellison [

20], Gottesman and Morey [

21], and Li, Zhang, and Zhao [

22] found that fund managers who graduated from top universities had higher performance. In contrast, Switzer and Huang [

23] found that an MBA degree, age, gender, and investment experience do not affect fund performance, and only the possession of Certified Financial Analyst (CFA) positively affects fund performance. Park and Joo [

24] found no significant relationship between top universities, majors, master’s degrees, and fund performance, but fund operation experience had a significantly positive (+) effect on fund performance. In this study, Hypothesis 1 was proposed based on these discussions.

Hypothesis 1. The human resources of venture funds affect their performance.

Hypothesis 1-1. The fund manager (key person) has a positive (+) effect on fund performance.

Hypothesis 1-2. The fund manager (key person) retention rate has a positive (+) effect on fund performance.

Hypothesis 1-3. The fund size of operations per fund manager (key person) has a negative (−) effect on fund performance.

2.2. Venture Fund Investor (LP) Composition and Performance

Venture funds consist of GPs and LPs, and there may be a conflict of interest between them. This is because not all participants in the venture fund have the same investment purpose and profit system. Conflict of interest between venture fund participants can be divided into conflict of interest between GP and LPs and conflict of interest among LPs.

Conflicts of interest between GPs and LPs arise because GPs aim to maximize management fees according to venture fund operations, whereas LPs aim to maximize fund profits and achieve investment purposes. The way to minimize this conflict is to match the interests of GPs and LPs as much as possible [

25].

As a specific plan, first, the carried interest and incentive system are operated and reflected in the articles of association. It reduces the proportion of management remuneration received in proportion to the size of the fund, designs a paid interest-oriented remuneration structure linked to profits, sets performance indicators according to the purpose of LPs’ investment, and provides incentives when exceeding them. This induces GPs to faithfully achieve the purpose of LP investment by matching the interests between GPs and LPs.

Second, GPs conventionally promise to invest in the fund (GP commitment) to manage the fund faithfully. In other words, GPs have an investor status. In general, more than 1% of the total fund size is invested, and the higher the proportion of GPs’ investment, the more likely it is that the GPs’ and LPs’ profits will coincide [

26]. GPs with insufficient capital invest funds from related companies or fund managers to cause the same effect as GP investments. In this way, the GP commitment rate is used to express GPs’ willingness to manage funds in accordance with the interests of LPs.

Another type of conflict of interest is that among LPs. This is because not all LPs have the same purpose in investing in venture funds. An LP may aim at investment returns, but there are LPs with other purposes as well. These different objectives of the LP can cause confusion in key decisions regarding fund operations, such as GPs’ decisions on investment strategies, selection of investment targets, and exercise of voting rights for invested companies [

14].

LPs are divided into financial investors (FIs) and strategic investors (SIs) according to the investment purpose. FIs seek financial interests first, while SIs have long-term plans and participate in production capital through business links, mergers, and acquisitions to generate production and financial profits [

27]. In addition, the Korean venture fund market was created by the government, and the proportion of government investment was very large. Government investment, which serves as priming water for the creation of venture funds, lands somewhere between FIs and SIs, because it aims to achieve financial profits and policy purposes simultaneously. Kang [

15] found that venture funds that received investment from the leading government investor fund for venture investment (The Fund of Funds for Venture Investment is a fund of funds created based on government finances based on Korea’s Venture Investment Promotion Act. The Fund of Funds for Venture Investment not only serves as priming water for the creation of venture funds through investment in venture funds but also serves as a manager to enhance the compliance and expertise of venture funds.) had higher returns than those that did not because they performed management functions to enhance GP compliance and expertise in addition to the priming water role. In this way, GPs are designed differently from venture fund operation strategies, depending on the LPs’ purpose of investment, which affects fund performance.

To prevent such conflicts of interest among LPs, GPs establish and propose a fund operation strategy that encompasses the purpose of the LPs’ investment, and each LP prepares the articles of association to achieve its investment purpose at the fund formation stage [

14]. For example, an FI may present a remuneration system proportional to financial profits and an SI may require preferential purchase rights and joint investment opportunities for an investment company. Government investors can maximize policy effects by indicating policy purposes, making them mandatory, or by providing incentives.

GPs have the obligation and the right to execute fund affairs in venture fund operations. However, LPs have the authority to monitor and inspect GPs’ work make sure to GPs achieve their investment purposes without a hitch. Furthermore, these powers are specified in the articles of association.

Decisions on significant matters in fund operations (change in the articles of incorporation, resolution of dissolution, transfer of shares, the appointment of accounting auditors, replacement of fund managers, etc.) are made through resolutions of investors’ general meetings as prescribed in advance in the articles of association. In general, venture funds have voting rights in proportion to the amount committed by each investor; therefore, if a particular investor holds a large stake or if the investor is a minority, significant decisions can be made with the consent of some investors [

28]. In this study, Hypothesis 2 was proposed based on these discussions.

Hypothesis 2. The investor composition of venture funds affects their performance.

Hypothesis 2-1. Government investors’ investment rates have a negative (−) effect on fund performance.

Hypothesis 2-2. The GP investment rate has a positive (+) effect on fund performance.

Hypothesis 2-3. The number of LPs has a positive (+) effect on fund performance.

2.3. Types of Venture Funds, Human Resources and Investor Composition, and Fund Performance

Venture funds can be divided into blind and project funds according to the formation process. Blind funds recruit LPs based on the GPs’ operational capabilities and select investment target companies after fund formation. Conversely, project funds are a method of selecting investment target companies in advance for each investment, and then recruiting investors to form funds [

28].

According to Korea Financial Supervisory Service and Korea Venture Capital Association website’s data, in the case of private equity funds (PEF) based on Korea’s Financial Investment Services and Capital Markets Act, the proportion of project funds newly established in 2021 was 70.8% (225 funds), higher than that of blind funds 29.2% (93 funds). At the beginning of the introduction of the PEF system, the proportion of blind funds was high; however, since the global financial crisis, the proportion of investment in project funds with relatively low risk has steadily increased [

29]. In venture investment associations based on Korea’s Venture Investment Promotion Act, blind funds account for the largest proportion. This seems to be because funds for venture investment, which serve as the priming water for venture investment associations, are limited to blind funds. However, as the revision of related regulations in 2018 allowed venture investment associations to be formed without investment in funds for venture investment, project funds began to increase to 91 funds (22.5%) in 2021, and project funds using new technology investment associations based on Korea’s Specialized Credit Finance Business Act are gradually increasing.

These fund types affect the LP investment decision-making procedures and evaluation criteria. In the case of blind funds, investment decisions are made by evaluating GPs, fund managers, and investment strategies, whereas project funds have a high proportion of suitability evaluations for companies to invest in and a relatively low proportion of GPs and fund managers. This study proposed Hypotheses 3 and 4 based on these discussions.

Hypothesis 3. The effect of human resources on fund performance varies depending on venture fund type.

Hypothesis 4. The effect of investor composition on fund performance varies depending on venture fund type.

2.4. The Governance Structure of GPs, Human Resources and LP Composition of Venture Funds, and Fund Performance

GPs can be divided into corporate GPs and independent GPs according to their governance structure. Corporate GP is a structure in which capital and management are separated, and there is a parent company that is a shareholder. On the other hand, independent GPs are in a form in which capital and management coincide because human resources provide capital. Depending on the type of GP governance structure, it causes major differences in terms of management strategy and managerial capital. In terms of management strategy, corporate GP establishes management and investment strategies according to the needs of the parent company, which is a capital supplier. In other words, corporate GPs seek not only financial profits but also strategic benefits such as discovering new business opportunities and strategic alliances demanded by their parent company, which is a shareholder. On the other hand, independent GPs focus all managerial capital on maximizing financial profits because capital and management coincide [

30].

In terms of managerial capital, corporate GPs have management capital such as bargaining power and distribution networks for suppliers through their parent companies. Since the managerial capital of such a corporate GP is unique, it can greatly contribute to the business construction of companies invested by the corporate GP. On the other hand, independent GPs have managerial capital centered on human resources. Therefore, it serves as an advisor to companies that independent GPs invested in, such as recruitment, accounting, and organizational composition, and support is limited to fostering companies. As such, the management strategy and managerial capital vary depending on the governance structure of the GP, which also causes considerable differences in the decision-making and value-up capabilities of the GP’s investment targets. It can also affect the growth of companies that GP invested in, and the direction of the fund’s exit strategy, resulting in a difference in fund returns [

30].

GPs that operate venture funds are mainly small- and medium-sized start-up investment companies based on the Venture Investment Promotion Act and new technology venture capitalists based on the Specialized Credit Finance Business Act. In addition, securities companies, asset management companies, accelerators, and Limited Liability Company (LLC)-type venture investment companies have also formed and operated venture funds, and their proportion is gradually increasing. In particular, an LLC-type venture investment company refers to a limited company based on the Commercial Act and needs to acquire professional manpower, as required by the Venture Investment Promotion Act. An LLC-type venture investment company is an organization that is free from agent problems due to consistent interests because the shareholders and fund managers of the company are the same. The LLC-type venture investment company system was introduced in 2005 and started with two companies; a total of nine companies were established in 2015.

This is 7.3% of the total venture capital (9 out of 124), which is a very low utilization system. Since 2016, LLC-type venture investment companies have grown rapidly, accounting for 16.7% (33 of 198) as of 2020, and their proportion is gradually increasing. As the government expanded the supply of funds to the venture investment market in 2016, fund managers began to independently establish LLC-type venture investment companies with little capital. A limited competition contest for LLC-type venture investment companies was established by the Fund of Funds for Venture Investment, which is a major LP.

LLC-type venture investment companies are drawing attention because fund management personnel and the company’s shareholders are the same, thus minimizing the possibility that other stakeholders are involved in fund operations. If GPs’ shareholders and fund management personnel are different, it is possible that the GPs will make decisions that contradict the LPs’ purpose of investment when there is a conflict of interest between the GPs’ shareholders and the fund’s LPs. This is because fund management personnel, who cannot be free from shareholders’ appointment and dismissal rights, are more likely to respond to shareholders’ demands than to the LPs’ demands. Under the current system, the LPs have a limited means of controlling opportunistic behavior and moral risks of agents, so the LPs have a higher preference for GPs in which shareholders and fund management personnel are the same [

31].

In addition to LLC-type venture investment companies, the number of GPs with a governance structure centered on fund management personnel is increasing. As the legal minimum capital required to establish an investment company for the establishment of small and medium enterprises was lowered from $3.82 million to $1.52 million in 2017, more GPs, with fund management personnel as their major shareholders, are increasing. Moreover, independent private equity GPs centering on fund management personnel are actively forming venture funds.

Previous studies have mainly analyzed the direct effect of GPs’ governance structure on fund performance. Cho and Park [

9] found that venture funds operated by GPs, in which individuals are major shareholders, have lower performance than venture funds operated by GPs, in which financial institutions or companies are major shareholders. However, Oh et al. [

11] explained that whether the major shareholders are individuals, financial institutions, or companies, they do not show a significant difference in fund performance. As such, research results on the effect of major shareholders of GP on fund performance differ from case to case. Rather than analyzing the direct effect of GPs’ governance structure on fund performance, this study aims to find out whether the function of excluding the effects of other interest factors on fund performance is significant when the fund management personnel are major shareholders, through a comparison between groups.

Korea’s Venture Investment Promotion Act defines in detail the requirements of major shareholders of investment companies for the establishment of small and medium enterprises and strictly restricts major shareholders’ intervention in fund operations for their interests. Nevertheless, it is difficult to exclude the influence of major shareholders on the fund operation process completely. Therefore, a fundamental solution is to completely exclude the possibility of a conflict of interest between GP and venture fund LP by taking the form of a governance structure in which fund management personnel have the status of major shareholders. This study proposed Hypotheses 5 and 6 based on these discussions.

Hypothesis 5. The impact of venture funds’ human resources on fund performance varies depending on the GPs’ governance structure.

Hypothesis 6. The effect of investor composition of venture funds on fund performance varies depending on the governance structure of the GPs.

3. Research Method

3.1. Research Model

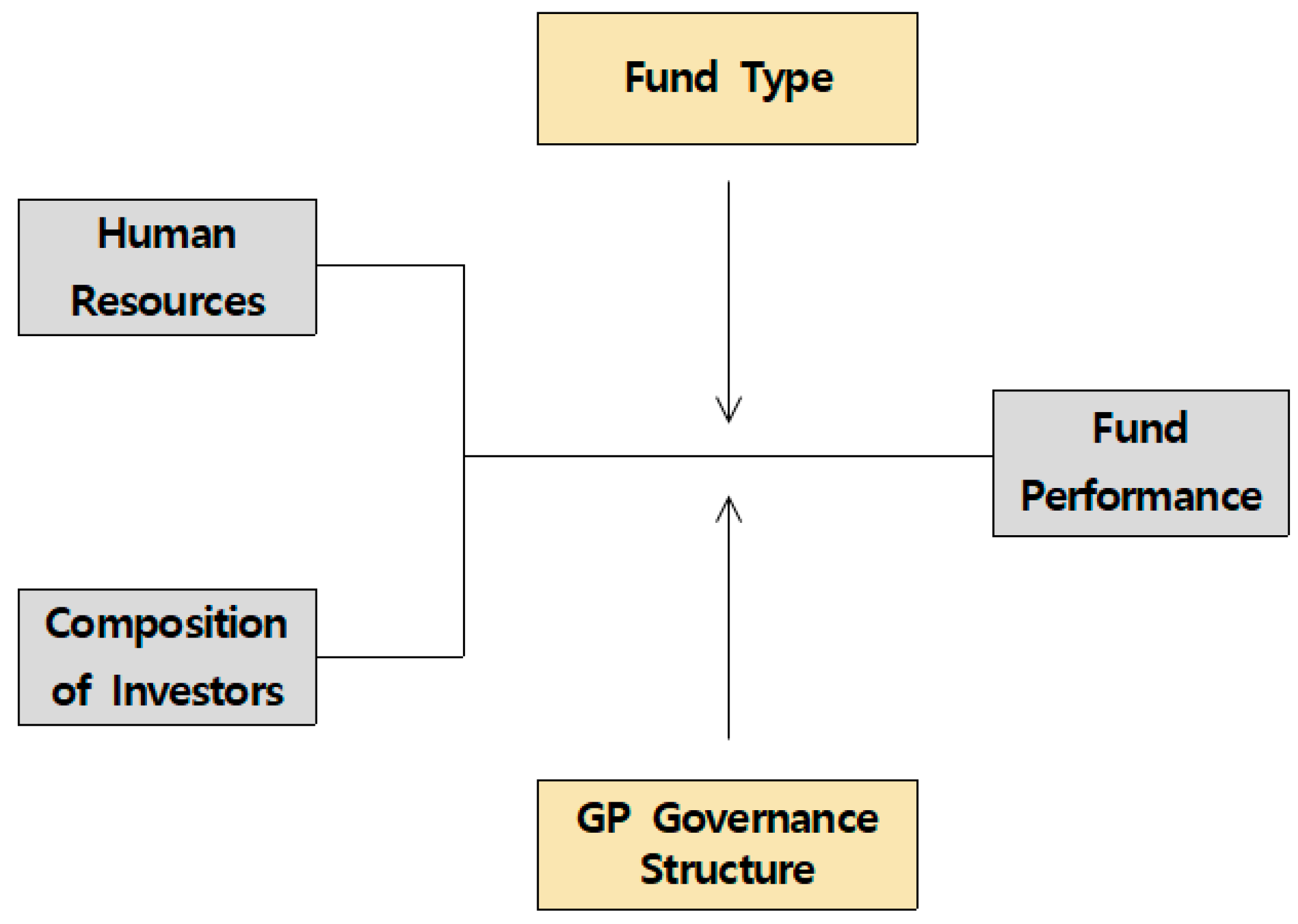

This study aims to understand the impact of venture funds’ human resources and investor composition on fund performance and empirically analyze differences according to fund types and GP governance structures. To this end, the theoretical background and previous studies on human resources, investor composition, fund type, and GP governance structure of venture funds were reviewed, based on which the framework was designed as shown in

Figure 1.

3.2. Defining and Measuring Variables

The independent variable was set as a fund’s human resource factor and investor component. The human resource factor was composed of the fund manager retention period, the fund manager retention rate, and the operation size per fund manager.

Regarding human resource factors, Khorana [

16], Park and Joo [

17], Kim and Chong [

18], and Chong [

32] used changes in fund managers, especially those due to voluntary movement (turnover), as core variables in fund performance. Based on these previous studies, the fund manager’s maintenance period was calculated as the period from the date of fund formation to the date of the initial change in the fund manager. If the fund manager has never changed during the fund management period, the fund manager retention rate was calculated as 100%. In the case of a fund manager change, the fund manager retention rate was calculated by subtracting the total fund manager number changes during the fund operation period divided by the fund managers numbers registered for the first time at the time of fund formation from 100%.

This is to prevent errors that occur when analyzing the number of net changes, because the number of fund managers varies depending on the size and character of the fund.

Regarding the fund operation size per fund manager, many previous studies, including Kaplan [

4], Humphery-Jenner [

6], Chae et al. [

10], Oh et al. [

11], and Choi and Kim [

1], dealt with the size of the fund as a major variable but did not consider the number of fund managers. In this study, the size of fund operations according to the number of fund managers was used as a variable, and the size of the operation of one fund manager (i.e., the total amount of venture funds divided by the number of fund managers) was used as a variable.

The variables related to the composition of investors were set as the government investor investment rate, GP investment rate, and the number of investors. Regarding investor composition variables, Kang [

15] analyzed the effect on fund performance by focusing on the participation of government investors. Kim and Lim [

33], Brander, Du, and Hellmann [

34], and Bertoni and Tykvova [

35] study the impact of funds invested by government investors on the performance of companies invested, which could indirectly estimate government investor variables’ effect on fund performance. Through these previous studies, the rate of government investors’ investment was calculated as the rate of investment based on the government budget among the total amount of funds.

Government investors include the Korea Venture Investment, the Korea Development Bank, the Korea Growth Investment Corporation, and local governments.

Regarding the GPs’ investment rate, Lee [

14] and Kim [

26] presented GPs’ investment as variables that positively affect the fund’s performance by lowering its conflict of interest. Based on this, the investment rate of GPs was calculated as the amount invested by GPs compared to the total amount of funds. Although previous studies did not deal with the number of investors as a significant variable, according to Lee [

14], conflicts of interest between investors are presented as a significant factor in fund performance. Therefore, in this study, the number of investors was used as a variable, and it was calculated by including GP if GPs invested in the fund to encompass both GP and investor status.

The dependent variables were set to Internal Rate of Return (IRR) and Abnormal Return. Cho and Park [

9], Chae et al. [

10], and Choi and Kim [

1] used IRR to measure venture fund performance, while Oh et al. [

11] measured it in three ways: IRR, multiple (Multiple is a value obtained by dividing the sum of the distribution by the total investment, which can be easily and intuitively understood, but has limitations in that it does not reflect the concept of cash flow and present value.), and public market equivalent (PME) (PME is an indicator of how much better performance is than listed stocks by assuming and comparing returns when listed stocks are purchased and held at the same time. In other words, a PME greater than 1 means that it showed excellent performance compared to investment in listed stocks.) as performance indicators of venture funds. IRR, a commonly used performance indicator, is a yield calculation method that reflects the concept of time to match the current value of capital inflow and outflow and is the most commonly used performance indicator in the venture investment market. This study uses gross IRR, which is the rate of return before the deduction of performance remuneration. An abnormal return is obtained by subtracting the hurdle rate from the liquidation return rate. Hurdle rate refers to the target rate of return set according to the purpose of the fund creation and investment target when forming a venture fund. Since GPs are paid performance compensation in proportion to profits exceeding the hurdle rate, abnormal returns are an important indicator of venture funds’ performance compared with their goals.

Fund types were classified into blind funds and project funds, depending on whether the investment target companies were confirmed before the formation of venture funds. This was classified based on whether the GP presented a confirmed investment target company in the process of recruiting investors.

The governance structure of GPs was divided into whether the sum of GP shares held by fund management personnel met the conditions of major shareholders defined in Korea’s Venture Investment Promotion Act. If one of the following is satisfied, it is determined that fund management personnel have the status of a major shareholder of the GPs. First, if the fund manager is the largest shareholder and the total stake of fund managers exceeds 10%; second, the total stake of fund managers is more than 30%; and third, the fund managers exercise virtual control over major management matters, such as appointment and dismissal of executives. The definition of each variable is shown in

Table 1.

3.3. Data Collection

This study uses a sample of 235 Korean venture funds formed by 49 GPs between 2004 and 2019 and liquidated between 2011 and 2021. Data were collected through LPs and GPs. The composition of investors and fund managers is specified in the venture fund articles of association, the articles of association are registered with government management agencies such as the Financial Supervisory Service and the Ministry of SMEs and Startups in Korea, and changes are reported if changes occur. Therefore, it can be assumed that the data were highly reliable.

The collected data include fund name, organization date, liquidation date, fund size, investment vehicle, fund type, hurdle rate, liquidation return rate, number of fund managers, number of fund manager changes, fund manager first change date, agreement amount by the investor, GP name, GPs’ legal form, and GP governance structure. The legal forms of GPs include investment companies for the establishment of small and medium enterprises, LLC-type venture investment companies, new technology venture capitalists, securities companies, asset management companies, and independent PEF. Investment vehicles include venture investment associations, new technology investment associations, and PEF specializing in start-up or venture businesses. However, PEF for corporate financial stability for specializing in restructuring companies or funds for project financing such as movies and Intellectual Property (IP) are excluded from the nature of venture investment. In addition, short-term operating funds under 12 months of age, which can show extreme returns, were excluded from the sample.

To confirm the representation of the samples, the proportion of the research sample among the total data was analyzed, as shown in

Table 2 based on Korea’s Financial Supervisory Service and the Korean Venture Capital Association website data.

Table 2 shows the number of venture associations and PEF by liquidation year. The sum of the number of venture associations and PEF, which are major investment vehicles of venture funds liquidated between 2011 and 2021, is 1035. The sample of this study is 235, accounting for approximately 22.7% of the total liquidated venture funds. In addition, the GPs that provided the data for this study is 49 which is about 24.8% of the total GPs (197) registered in Korea as of 2021. Such simple comparison has certain limits, but based on the aforementioned information, it is possible to estimate the representativeness of the study sample to some extent.

3.4. Analysis Method

The SPSS 28.0 program (IBM, Seoul, Republic of Korea) was used to verify the research model and hypotheses presented in this study. First, a multiple linear regression analysis was conducted on the entire sample, and Hypotheses 1 and 2 were verified by analyzing the impact of venture funds’ human resources and investor composition on fund performance. Based on this, the sample was divided into fund types (blind funds and project funds), a multiple linear regression analysis was conducted, and the results were compared to verify Hypotheses 3 and 4. Similarly, based on the governance structure of the GPs, a multiple linear regression analysis was conducted by classifying whether the main shareholders of the GPs were fund management personnel. Hypotheses 5 and 6 were verified by comparing the results.

4. The Results of a Study

4.1. Technical Statistics and Correlation Analysis Results

First, the characteristics of venture funds as research subjects were analyzed through technical statistical analysis, and a correlation analysis was conducted to confirm the relationship between variables.

The results of the basic statistical analysis of the significant variables are presented in

Table 3.

The average of the main variables was 15.49% for IRR and 7.87% for Abnormal Return. The average of human resource-related variables is 2.76 years of fund manager retention, 39.51% of fund manager’s retention rate, and 9.37 million USD of operation size per fund manager. The average of the variables related to the composition of investors is 19.42% of the government’s investment rate, 17.1% of the GP investment rate, and 6.95 of the number of investors. Of the 235 fund samples, 131 were blind funds, 104 were project funds, 84 were operated by GPs in which fund management personnel were major shareholders, and 151 were operated by GPs with other governance structures.

Prior to the regression analysis, Pearson’s correlation analysis was performed to confirm the correlation of the significant variables, and the results are shown in

Table 4. Through correlation analysis, the correlation between the fund performance which is the dependent variable, and human resource and the investor composition which are the independent variable was verified.

Firstly, the correlation between the IRR which is a fund performance variable, and hu-man resource variables were verified. IRR showed a significantly positive (+) correlation with the fund manager retention rate (r = 0.212, p < 0.001) and a negative (−) correlation with the fund manager retention period (r = −0.215, p < 0.001). Meanwhile, IRR had not a significant correlation with the size of fund operations per fund manager. Next, the correlation be-tween IRR and the variables of the investor component was confirmed. IRR showed a significantly positive (+) correlation with the number of investors (r = 0.229, p < 0.001) and a negative (−) correlation with the government investor investment rate (r = −0.153, p < 0.05). On the other hand, IRR had not a significant correlation with the GP investment rate.

The abnormal returns, another variable representing the fund performance, showed the same result. As a result of verifying the correlation between abnormal returns and human resource variables, Abnormal returns were also found to have a significantly positive (+) correlation with the fund manager retention rate (r = 0.204, p < 0.01) and a negative (−) correlation with the fund manager retention period (r = −0.205, p < 0.01). However, Abnormal returns had not a significant correlation with the size of fund operations per fund manager. Next, the correlation between Abnormal returns and the variables of the investor com-ponent was confirmed. Abnormal returns showed a significant positive (+) correlation with the number of investors (r = 0.222, p < 0.001) and a negative (−) correlation with the government investor investment rate (r = −0.128, p < 0.05). Meanwhile, Abnormal returns had not a significant correlation with the GP investment rate.

4.2. Verification of Hypotheses 1 and 2: Venture Funds’ Human Resources, Investor Composition and Fund Performance

A multiple linear regression analysis was conducted to verify the impact of venture funds’ human resources and investor composition on fund performance. The results are shown in

Table 5. First, as a result of verifying the effect of human resources and investor composition on the IRR, the regression model was statistically significant (DF = 234, F = 6.506,

p < 0.001), and the explanatory power of the regression model was approximately 14.6% (modified R squared is 12.4%). Meanwhile, the Durbin-Watson statistic was 1.953, which was evaluated because no issues were found in the assumption of residual independence. In addition, the variance inflation factor (VIF) was less than 1.5; therefore, it was considered that there was no multicollinearity problem. As a result of verifying the significance of the regression coefficient, it was found that the fund manager retention period (β = −0.271,

p < 0.001) had a negative (−) effect on IRR, while the fund manager retention rate (β = 0.269,

p < 0.001) and the number of investors (β = 0.137,

p < 0.05) had a positive (+) effect on IRR. In other words, the shorter the fund manager retention period, the higher the fund manager retention rate, and the higher the number of investors, the more significant the IRR improvement.

Next,

Table 6 shows the results of verifying the effect of venture funds’ human resources and investor composition on abnormal returns. The regression model was statistically significant (DF = 234, F = 5.938,

p < 0.001), and the explanatory power of the regression model was approximately 13.5% (modified R squared is 11.2%). Meanwhile, the Durbin-Watson statistic was 1.923, and it was determined that there was no issue with the assumption of residual independence. In addition, all VIFs were less than 1.5, so it was judged that there was no multicollinearity problem. As a result of verifying the significance of the regression coefficient, it was found that the fund manager retention period (β = −0.262,

p < 0.001) had a negative (−) effect on abnormal returns, while the fund manager retention rate (β = 0.268,

p < 0.001) and the number of investors (β = 0.140,

p < 0.05) had a positive (+) effect on abnormal returns. This showed the same results as those previously analyzed for human resources and investor composition on IRR.

Based on this, Hypotheses 1 and 2 were verified. In contrast to Hypothesis 1-1, the result of the analysis shows that the fund manager retention period had a negative (−) effect on venture fund performance. This is because fund manager replacement occurs in most venture funds, so the stable operation of the fund, after the fund manager is replaced in the early stages of venture fund operation, has a more positive effect on the fund’s performance than the change after a considerable period of fund operation. Hypothesis 1-2, that the fund manager’s retention rate would have a positive (+) effect on venture fund performance, was adopted as a result of verification, and Hypothesis 1-3, that the size of operation per fund manager would have a negative (−) effect on venture fund performance, was rejected. Thus, Hypothesis 1 was partially supported.

Both Hypothesis 2-1, that the government investor investment rate would have a negative (−) effect on the performance of venture funds, and Hypothesis 2-2, that the GP investment rate would have a positive (+) effect on the performance of venture funds, were rejected as a result of the verification. Only Hypothesis 2-3, that the number of investors would have a positive (+) effect on the performance of venture funds, was adopted as a result of the verification, so Hypothesis 2 was partially adopted.

4.3. Verification of Hypotheses 3 and 4: Venture Funds’ Human Resources, Investor Composition and Fund Performance according to Fund Types

To confirm whether the impact of venture funds’ human resources and investor composition on fund performance differs depending on the fund type, a multiple linear regression analysis was conducted by dividing groups by fund type. The results are shown in

Table 7.

First, as a result of verifying the effect of human resources and investor composition on IRR, blind funds were statistically significant at p < 0.001 (DF = 130, F = 4.895), and project funds were significant at p < 0.05 (DF = 103, F = 2.318). As a result of verifying the significance of the regression coefficient, blind funds were the same as the total verification results, and the fund manager retention period (β = −0.317, p < 0.001) had a negative (−) effect on IRR, while the fund manager retention rate (β = 0.382, p < 0.001) and the number of investors (β = 0.188, p < 0.05) had a positive (+) effect on IRR. However, for project funds, only the fund manager maintenance period (β = −0.289, p < 0.01) had a negative (−) effect on IRR.

Table 8 shows the verification results of the effect of venture funds’ human resources and investor composition on abnormal returns depending on the types of venture funds. Blind funds were significant at

p < 0.001 (DF = 130, F = 4.883). However, the

p-values of the project funds were

p = 0.052 (DF = 103, F = 2.173), which was more than 0.05, indicating that they were not statistically significant. As a result of verifying the significance of the blind fund regression coefficient, it was found that the fund manager retention period (β = −0.311,

p < 0.001) had a negative (−) effect on abnormal returns, and the fund manager retention rate (β = 0.388,

p < 0.001) and number of investors (β = 0.189,

p < 0.05) had a positive (+) effect on abnormal returns. This is the same as the overall verification results.

Based on this, Hypotheses 3 and 4 were verified, and the effect of human resources and investor composition on fund performance in blind funds was the same as the analysis results for the entire fund, but in project funds, only the fund manager retention period affected IRR and was not statistically significant for the remaining variables. Accordingly, Hypothesis 3, which states that the impact of human resources on venture fund performance varies depending on the type of fund, was partially adopted. In addition, Hypothesis 4 states that the effect of investor composition on fund performance would vary depending on the type of fund.

4.4. Human Resources and Fund Performance of Venture Funds

To confirm whether the impact of venture funds’ human resources and investor composition on fund performance differs according to the GP’s governance structure, a multiple linear regression analysis was conducted by dividing the groups into GPs’ governance structures. The results are shown in

Table 9.

First, as a result of analyzing the effect of human resources and investor composition on IRR, funds operated by GPs, in which fund management personnel are major shareholders, were not statistically significant because the p-value was p = 0.050 (DF = 83, F = 2.218), which was more than 0.05. Only funds operated by GPs composed of other shareholders were statistically significant (DF = 150, F = 4.698, p < 0.001). Funds operated by GPs consisting of shareholders, not fund management personnel, had the same results as the overall verification. The fund manager retention period (β = −0.240, p < 0.001) had a negative (−) effect on IRR, and the fund manager retention rate (β = 0.311, p < 0.001) and the number of investors (β = 0.193, p < 0.05) had a positive (+) effect on IRR.

We verified whether the impact of the fund’s human resources and investor composition on abnormal returns according to the GPs’ governance structure changed. The results are shown in

Table 10. Funds operated by GPs, in which fund management personnel are major shareholders, were not statistically significant because the

p-value was

p = 0.064 (DF = 83, F = 2.086), which was more than 0.05. Only funds operated by GPs composed of shareholders other than fund management personnel (DF = 150, F = 4.339,

p < 0.001) were statistically significant. As a result of verifying the significance of the regression coefficient, the funds operated by GPs, in which fund management personnel are not the major shareholders, were the same as the overall verification results. The fund manager retention period (β = −0.226,

p < 0.01) had a negative (−) effect on abnormal returns, while the fund manager retention rate (β = 0.311,

p < 0.01) and the number of investors (β = 0.198,

p < 0.05) had a positive (+) effect on abnormal returns.

Based on this, the results of verifying Hypotheses 5 and 6 showed that funds operated by GPs in which fund management personnel are major shareholders had no statistically significant impact on fund performance. However, funds operated by GPs, which are shareholders and not fund management personnel, were the same as the analysis results for the entire group. Therefore, Hypotheses 5 and 6 were adopted such that the impact of the fund’s human resources and investor composition on venture funds’ performance would vary depending on the governance structure of the GP.

5. Discussion and Implications

This study differs from previous studies in the sense that it analyzes the factors of fund performance centered on stakeholders of venture funds. In addition, by classifying and analyzing each group according to the fund types and governance structure of GPs, it was found that factors related to venture fund stakeholders had different effects on fund performance by group. Based on this, we present the following theoretical implications.

First, it was confirmed that the retention rate of venture fund managers had a positive (+) effect on fund performance. This is similar to the results of Kim and Chong’s [

18] study on mutual funds, and it was proved that the theory that voluntary fund manager change in mutual funds has a negative (−) effect on fund performance applies to venture funds. In addition, it was confirmed that if the fund manager is changed after a considerable period of fund operation, it has a more negative (−) effect on fund performance than the change at the beginning of the fund operation; additionally, the timing of the fund manager change also has a significant effect on fund performance.

Second, it was confirmed that in funds managed by a GP, which has major shareholders of the fund as its management personnel, factors related to the fund’s stakeholders do not affect the fund’s performance. Previous studies have mainly analyzed the direct effect of GPs’ governance structure on fund performance, and the results differed for each study. Cho and Park [

9] found that venture funds managed by GPs that are the major shareholders of individuals have lower performance than venture funds managed by GPs that are the major shareholders of financial institutions or companies. Conversely, Oh et al. [

11] explained that whether major shareholders are individuals, financial institutions, or companies, they do not show a significant difference in fund performance. Therefore, rather than analyzing the direct effect of GPs’ governance structure on fund performance, this study confirms whether it functions to exclude the impact of other funds’ interest factors on fund performance when fund management personnel are major shareholders.

Third, when considering fund types, it was confirmed that factors related to the fund’s stakeholders affected the fund’s performance only for blind funds. In previous studies, fund types were not considered when analyzing the performance factors of venture funds. However, from the perspective of the fund’s stakeholders, fund type is one of the main factors determining the possibility of a conflict of interest. This is because stakeholders try to realize their goals through investment targets. Under relevant laws and regulations, the selection of investment targets is a unique right of the GP, and other stakeholders, such as investors, cannot be involved. However, investors may specify the scope of investment in the articles of association to induce investment that is consistent with their interests or indirectly exert influence by utilizing the investor’s right to monitor and consent [

25]. In this respect, because the project fund is formed after the investment company is confirmed, the possibility of conflict of interest between the fund’s stakeholders is largely excluded. Therefore, the results of this study provide a theoretical basis for the derivation of different results when considering fund types while analyzing the performance factors of venture funds.

This study aims to provide the primary data necessary for establishing venture investment policies and several implications in terms of policy.

First, the study finds that the investment rate of government investors does not significantly affect fund performance. This result differs from that of previous studies. Kang [

15] found that the return on venture funds that received investments from the Fund of Funds for Venture Investment, a representative Korean government investor, were higher than those that did not. The reason the results of this study are different from those of previous studies is that previous studies only considered the investment of government investors, and the difference in influence on the fund was not reflected because the investment rate was not considered. Additionally, the samples used in previous studies were funds formed and liquidated between 2000 and 2018, mainly targeting venture associations. In the case of the Korea Venture Investment Association, which comprises the majority of the sample, until 2018, the formation was restricted without the investment of funds for venture investment. Therefore, it is believed that this study contains some data that are difficult to consider as significant investments due to a large number of small investments for formation purposes. Another reason is that, as the manager’s role in enhancing the compliance and expertise of government investors is systematized with the maturity of the venture investment market, minimum compliance and expertise are secured without the investment of government investors. Therefore, the results of this study suggest a need for government investors to strengthen the function of priming water, a unique function of government investors, by expanding investment in non-preferred investment areas that need to be fostered rather than investing in mature markets.

Second, this study provides a basis for government policy needs to actively foster GPs centered on fund management personnel. This study confirmed that if fund management personnel are major shareholders, the possibility of conflicts of interest among fund stakeholders is low because of consistency in fund performance and interests of the GPs, resulting in improved focus on financial profit. The reason for paying attention to the governance structure of GPs when analyzing the performance factors of venture funds is that GPs with fund management personnel as major shareholders prioritize financial motivation, while GPs composed of other shareholders can be motivated by strategic advantages to create new business opportunities for the parent company through strategic relationships with investment companies [

30]. Therefore, this study provides a basis for the promotion of GPs centered on fund management personnel.

This study also provides practical implications for investors to consider when investing in venture funds.

First, project funds target companies that have been determined, and the impact of venture funds’ human resources and investor composition on fund performance is insignificant. However, in blind funds, human resources and investor composition affect fund performance. Therefore, when reviewing investments in a project fund, it is reasonable to judge the target company rather than the funds’ interest factors. In contrast, blind funds should consider their human resources and investor composition as major evaluation factors, and continuous monitoring of conflicts of interest is required in the post-management process.

Second, the fund size of operations per fund manager did not significantly affect fund performance, but factors related to fund manager changes had a significant effect on fund performance. This raises a new point of view for the existing evaluation criteria, which were judged to strengthen fund operational capabilities as the number of fund managers increased. In addition, it was confirmed that better fund performance could be expected to be enhanced by strengthening the evaluation of fund managers’ sustainability and withdrawal prevention measures, which were previously considered only as reference factors.

Third, this study showed that the investment rate of GPs did not significantly affect fund performance. This proves that the existing evaluation criteria for determining responsible operations based on GPs’ investment rate were insignificant. In addition, it provides a basis for confirming that there is a limit to judging the competitiveness of GPs centered on fund management personnel with limited investment capacity due to a small amount of capital. This study suggests the need to review the effectiveness of the existing evaluation system, which judges whether the responsible operation is based on the investment rate of GPs. Rather, it is important to improve fund performance by diversifying the composition of investors and dispersing the authorization of each LP, so that the purpose of fund operations does not change according to the interests of specific investors.

6. Conclusions

This study empirically analyzes the effects of venture funds’ human resources and investor composition on venture fund performance. Existing studies focus on the impact of the internal factors of venture funds (fund period, investment field, fund size, etc.) and external environmental factors (economic cycles, securities market, venture investment market, etc.) on fund performance. However, this study analyzes fund performance factors centering on fund managers and investors, who are stakeholders in venture funds, and provides a differentiated perspective by analyzing differences between groups by dividing them based on fund types and GP governance structure.

This study could not consider the individual capabilities and representativeness of fund managers because of limitations in collecting data on venture funds. In addition, this study could not analyze the differences according to the specific timing of the change of fund managers. Furthermore, differences based on the purpose of the investor’s investment (strategic investor, financial investor) were not analyzed in this study. Moreover, when calculating the GP investment ratio, it was not possible to analyze the case in which the investments of related parties and fund managers were included.

Furthermore, this study verified by consisting of variables deemed to be important factors in fund performance through analysis of previous studies and practical experience. However, the R2 value was slightly lower from 0.13 to 0.19, showing a limitation of insufficient explanatory power. Therefore, there is a need to continue research on finding more important variables in the future.

Moreover, this study is meaningful because it discovered that each variable may or may not affect venture fund performance in some cases by comparing variables that showed different results in previous studies between groups according to GP’s governance structure and fund type. Nevertheless, there are limits in this study including that more diverse variables were not considered in studying the performance factors of venture funds. Therefore, it is necessary to continue research considering more various variables in the future.

Finally, more in-depth research could be conducted with respect to data on liquidated venture funds that were formed after 2019, when venture association-type project funds increased in earnest and PEF-type blind funds were activated.

{kind=link}