2.1. Definition and Interdependence of Stakeholders and Organisations

The definition of the concept of “stakeholder” within organisational theories, the boundaries of their interrelationship with those stakeholders, and even their origin and meaning have always been difficult to define [

3,

4,

5]. Originally, in the definition of the Stanford Research Institute’s internal memo in 1963 [

3], the term included those entities that supported the survival of organisations.

This first approach to the definition of the term “stakeholder” divided opinions, differentiating and complementing each other depending on the discipline and the approach from which the content and validity of the term was studied. From the perspective of organisational planning, the contingent nature of stakeholders was emphasised [

3,

6], so their identification and number could change over time, depending on the circumstances affecting the organisations. The authors of systems theory renewed the views of Chester Barnard [

7], arguing that the “support and interaction” of stakeholders could solve various social problems [

8]. From the perspective of social responsibility, the shift in the orientation of stakeholder action towards participatory rather than influential positions was emphasised [

9], and from organisational theory, stakeholders were restricted to those groups that could make claims on firms and those on whom the firm might have claims [

10]. Freeman [

3], from a strategic management perspective, sought a broader definition of the term to include in his famous description all groups that could affect or be affected by the “purpose of an organisation”.

In the context of sustainability, the various definitions of the term that have been proposed since then agree in pointing out the interdependence of the interests of the groups or individuals that make up the system [

11,

12], whether they belong to organisations or not, in an interconnected model or system of relationships [

4,

12,

13].

At a corporate level, there is a widespread view that stakeholders drive the sustainability strategies of organisations and that their influence is a function of, among others, the degree of mutual influence that can be exerted [

14,

15] and their level of power [

16], with power being understood as the predictable ability to impose one’s will on a social action, even against the opposition of the other participants [

17]. The intensity and direction in which both manifest themselves will depend on the degree of dependence of one party on the other to achieve the expected results [

11,

12]. Other authors link stakeholder relations to resource dependency theory, according to which the survival of organisations depends on their ability to acquire critical resources from the external environment [

18].

The widespread but also controversial stakeholder theory [

19,

20] has established an internal division of stakeholders according to the type of interdependence they have with organisations [

3,

21]. This division groups together, firstly, stakeholders without whose participation the organisation could not survive, which are referred to as “primary stakeholders”, and secondly, those who maintain a degree of mutual influence but are not directly involved in the organisations’ transactions and are, therefore, not dependent on or essential for their survival, which are referred to as “secondary stakeholders”.

Organisations can be seen as a “nexus of contracts” between themselves and stakeholders, with each party seeking to maximise its utility in the relationship [

22,

23,

24]. From this perspective, stakeholders have also been distinguished between those whose relationship is contractual in nature, who have been called “primary”, and those who do not have a contractual relationship but who nevertheless have some kind of power over the organisations, referred to as “secondary” [

21,

25,

26]. In stakeholder theory, this distinction categorises the ways in which relationships between organisations and stakeholders are managed, with those defined as primary focusing on managing the interests of both parties, and those defined as secondary focusing on achieving a form of equilibrium in which relationships with them are relational rather than contractual.

Stakeholder theory implicitly contains a theory of the instrumental dimension [

27,

28], which links the interests of organisations to those of their environment, extending the boundaries of the organisation to all stakeholders [

19,

29]. All of them, in proportion to their capacity for intervention or pressure, are given the quality of modulating the structures and decisions of the organisations themselves. The instrumental perspective of stakeholder theory answers the question “what happens if?” [

28] and aims to describe what happens when corporate managers make differentiated decisions in the context of their relationships with stakeholders.

In addition to the instrumental theory mentioned above, there are also descriptive and normative theories [

27] that implicitly coexist with it and that try to explain the behaviour of corporate managers and the way in which they should behave towards stakeholders, answering the questions “what happens?” and “what should happen?”, respectively [

28]. Both, together with instrumental theory, comprise a way of describing the behaviour of organisations towards stakeholders or a group of them.

The description of the behaviour of organisations in the field of sustainability has been translated over time into voluntary or mandatory formulas for the communication of non-financial information (now defined in European regulations as sustainability reporting) to all stakeholders, with the aim of being used by them in different areas and for different purposes, ranging from knowledge of the risks and opportunities arising from the actions of organisations and the demand for greater accountability to monitoring environmental and social trends in order to contribute to the modulation of public policies, which has become a fundamental aspect of investment decisions [

30,

31].

2.2. The Treatment of Stakeholders in the CSRD and the Trickle-Down Effect

The traditional division between stakeholder groups has been maintained in European regulatory guidance, both in the proposal to amend the EU Directive 2013/34/EU [

32,

33] on non-financial reporting and in its current text, as amended by the CSRD [

30], which, as a continuation of EU Directive 2014/95/EU [

34], represents the political and societal demand for more information from companies [

35] and, consequently, for a better description of organisations’ sustainability performance.

The CSRD does not explicitly clarify the reasons why it promotes a distinction between stakeholders according to the use and benefit that each stakeholder group makes or derives from the sustainability information it receives or expects to receive. However, it does describe what it expects to happen with the dissemination of sustainability information, understood as a description of organisational behaviour that improves the management of sustainability-related risks and opportunities for both organisations and stakeholders [

30] within the system of interrelationships in which they coexist.

Specifically, the CSRD expects that sustainability information, which should favour the management of risks and opportunities, is carried out from the momentum of the dialogical engagement between organisations and stakeholders, which has previously been described by other authors ([

36,

37,

38], among others). It also allows the foundations to be laid for close collaboration between all parties as a means of preserving the value of organisations [

39], promotes the dissemination of relevant information on sustainability, protects the interests of stakeholders, and describes the way in which this objective is achieved within the framework of “responsible business conduct” [

30], which goes beyond its economic function [

40].

Both the CSRD and its predecessor distinguish between the interests of a first group of stakeholders, consisting of investors and asset managers who are said to “want to better understand the risks and opportunities that sustainability issues pose to their investments and the impacts of those investments on people and the environment” ([

30], p. L322/18), and those of a second group of stakeholders, consisting of non-governmental organisations and social partners and other stakeholders, who are said to expect a form of scrutiny [

33] of the impact of organisations’ activities, with the aim of holding them to a higher level of accountability for their impact on people and the environment [

30,

33].

Other standard setters in the field of sustainability disclosure have followed a similar line of distinction, recognising that the objective of their sustainability reporting frameworks focuses on interconnecting sustainability information that meets the needs of capital markets with the needs of other stakeholders [

2,

41].

In both cases, therefore, the aim was to ensure, on the one hand, that organisations disclose sustainability information to investors according to their specific needs and, on the other hand, to provide other stakeholders with a source of information on the behaviour of organisations, which, in line with the CSRD, should serve as a means of demanding greater accountability for the impact of organisations’ activities on people and the environment. This should be the basis for comparative analysis across and within market sectors, as a source of information on risks and opportunities, and monitoring trends in the context of public policymaking [

30].

EU Directive 2014/95/EU [

34], which first reformed Directive 2013/34/EU [

32], currently amended by the CSRD, aims to reduce the asymmetry between organisations and stakeholders through greater information dissemination while maintaining the perspective of agency models in the management organisation. This was in exchange for greater power and an improvement in terms of the legitimacy potentially provided by the disclosure of their social responsibility [

42], but without a change in the organisational model and, therefore, without a change in behaviour [

35].

The distinction between stakeholder groups in the current European directive and in other non-financial reporting standards now introduces a novel asymmetry or dichotomy [

41] between the different classes that are defined, assigning each of them a differentiated role according to the expected benefits that each of them will obtain from the sustainability information. Thus, investors, despite being one of the least studied groups in terms of sustainability [

43], seem to be at the centre of the requirements to be met by the dissemination of non-financial information, while the other stakeholders are apparently assigned a differentiated role based on making judgements, rather than a central role.

From a European regulatory perspective, specific regulations, which embrace specific transparency requirements on the integration of sustainability risks and the description of the negative impacts of investment decisions and financial product disclosures, have been adopted. These regulations affect the stakeholder group, including investors and asset managers [

44]. It follows that this stakeholder group will be affected by the sustainability aspects of investment risk, sustainability opportunities, and the specific regulatory framework, which will logically lead to an ex ante attitude towards the actions of organisations, while the majority of “secondary” stakeholders, which are not affected by specific sustainability regulations, will maintain their critical interest ex post. Thus, it does not appear that the nature and direction of the relationship between the two groups of stakeholders and the organisations described in the European directive are symmetrical, since the first group, the investors, acts ex ante on the action of the organisations, and the second group acts ex post, with the former actively modulating it in defence of its interests, obligations, and for the opportunities that may arise, and the latter critically examining it once the action has been completed.

The main role attributed to investors is related to the fact that this group has previously demanded more high-quality sustainability information [

43,

45] in order to properly assess their investment strategies and related risks, as well as implicitly diffuse, through a trickle-down effect, the ESRS from obligated organisations (listed and larger companies) to small- and medium-sized enterprises (SMEs) integrated in their value chain that are not obligated by the CSRD.

The formal authority of obligated organisations in their value chain, as well as the frequency of interaction and the intra-organisational distance between the two subjects, play a crucial role in the mode of influence and behaviour of organisations [

17,

46], whose “indirect” reporting obligations are subsumed within and driven by the legal obligations of the primary reporter, creating a layered system of influences that may suggest that the quality level of the obligated organisation flows in a trickle [

47] through its value chain when it is not obligated to report.

The consequences of such an effect have been assessed by the European Financial Reporting Advisory Group (EFRAG) in its role as technical advisor to the European Commission on sustainability reporting, from the perspective of the indirect costs for the group of companies (SMEs) that are not subject to annual sustainability reporting under European standards [

48].

As far as we are aware, the EFRAG has not promoted a concrete assessment of this trickle-down perspective in terms of its impact on the behaviour of the value chain of obligated organisations, nor of the extent to which this influence may be appropriate in terms of its homogenising effects, taking into account that a group of stakeholders with sufficient power may be able to influence the behaviour of an organisation in line with its own interests or replace it with other competitors with closer values [

49], regardless of whether or not such behaviour is in line with the law [

50].

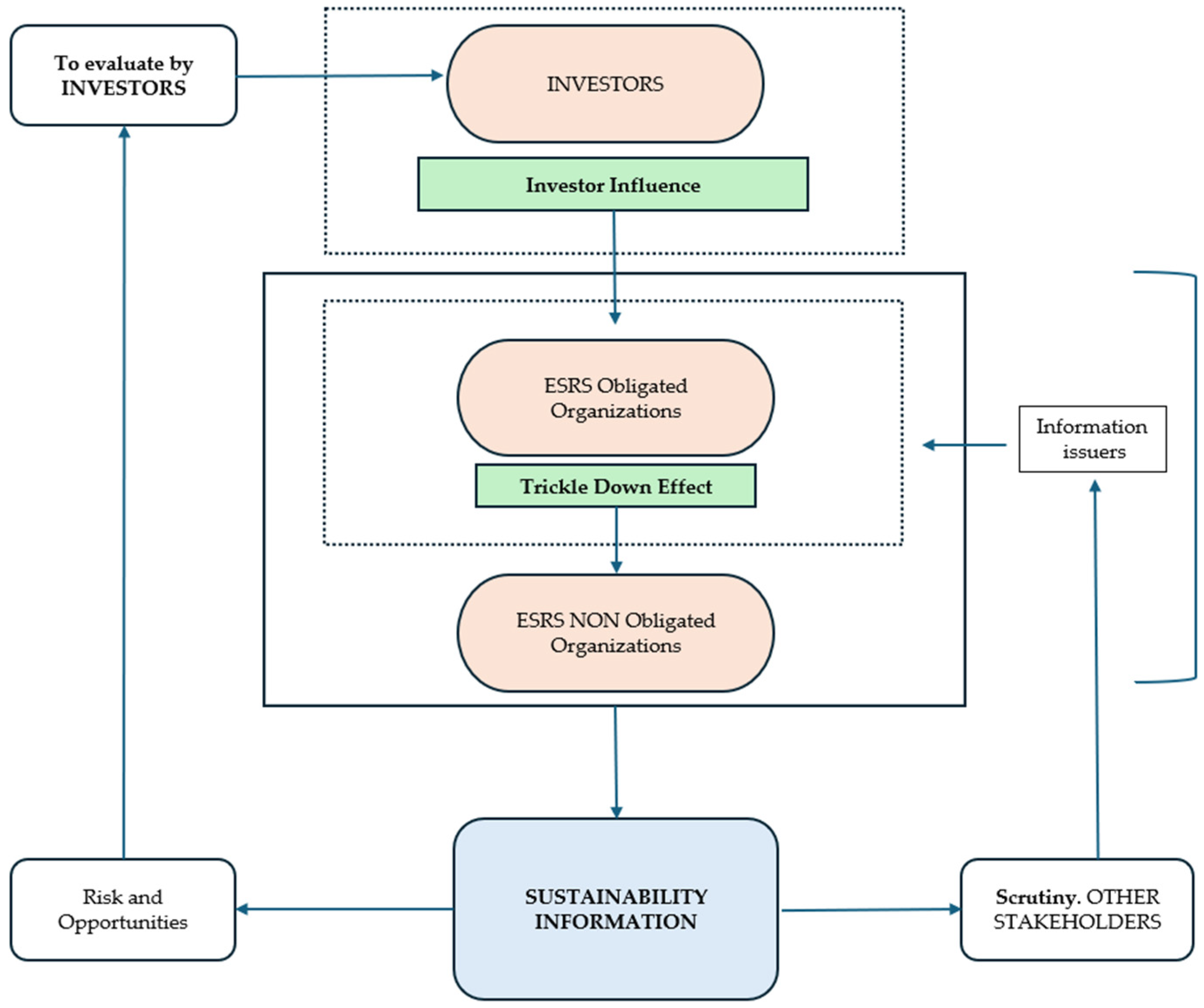

The scheme of relations between the different groups, as well as the sense of mutual influence between investors, stakeholders, and organisations proposed by the European Community legislation, is schematically illustrated in

Figure 1. This scheme represents the mode of transmission of influence from the stakeholder group constituted by investors to the set of organisations legally obliged to disclose sustainability information and, through the trickle-down effect, to the non-obligated ones, both interdependent of the system together with their stakeholders [

13], transferring the characteristics of the behaviour of the influential group to the whole.

Based on the scheme of influences described in

Figure 1, considering that the traditional stakeholder distinction and the one introduced by the CSRD [

30] have not changed the fundamentals of sustainability concerns, it is to be expected that the stakeholder distinction does not affect the extent to which sustainability focuses on material social and environmental aspects but rather the way in which these fundamentals are “filtered” through the interrelationships of organisations.

2.3. Interdependence of Stakeholders, Organisations, and CSRD

If we accept organisations as adaptive individuals, they will tend to behave homogeneously when exposed to similar cues produced in the environment according to the principles of social information processing theory, so they will adapt their attitudes and behaviour to the context of the system [

19,

42] in a form of alignment with external attitudes that reflect ideal or desirable behaviour, becoming more isomorphic over time as they conform to institutionalised norms [

51,

52], even unconsciously [

53].

In

Section 2.1, we described the way in which the division between stakeholder types has traditionally been maintained. Moreover, in

Section 2.2, we pointed out the way in which the stakeholders have been dealt with in the CSRD, and how a kind of separation has also been maintained between stakeholders who want to know the scope of the risks and opportunities that directly affect their interests (fundamentally investors) and those who are expected to maintain an attitude of verification regarding the impact of the organisations on sustainability-related factors.

On the other hand, the CSRD excludes 98% of the total of 31 million companies operating in the European Union in 2021 from reporting on sustainability matters, representing 35% of the added value generated [

54], but it assumes the existence of a cost arising from such organisations as a consequence of the need to report that affects large companies with regard to their own chain of value, and investors due to the requirements arising from regulations related to sustainable investments (i.e., [

44]). The mechanism imposed by the CSRD thus reasonably supposes an indirect means of transmission of sustainability-related information by the organisations excluded.

However, the CSRD has not specifically appraised the possibility that the trickle-down effect may not only affect the cost borne by the non-obliged organisations but may also influence the trend that large companies and investors may exert in relation to a specific way of approaching the content and scope of the sustainability-related information, which may contribute to uniformity in the information disseminated according to the degree of influence of both.

For these reasons, in this work, we ask in what way sustainability-related aspects have been dealt with in the context of the group of stakeholders who constitute the investors prior to the CSRD coming into force and, thus, what are the aspects one might expect to be transmitted to the overall system through the trickle-down effect.

2.4. Research Hypothesis

Based on the CSRD guidelines [

30] and the differentiated role and specific expectations they identify for the first group of stakeholders (mainly investors but also asset managers), we would like to know what sustainability-related aspects have been associated with this group of stakeholders in the scientific literature, which could be extended to obligated organisations and the rest of the system through the interrelationships on which it is based and through the trickle-down mechanism.

Firstly, it should be noted that, in the scientific literature, the group of stakeholders who have control over financial resources, with current or potential contractual relationships with organisations, may have received more attention between 2014 and 2022 than the univocal set of individuals represented by the term “stakeholder”. This may be an intention to address, with greater intensity and attention, the examination of their interests, expectations, and influence on sustainability issues considering the relevance of their role in the context of organisational management.

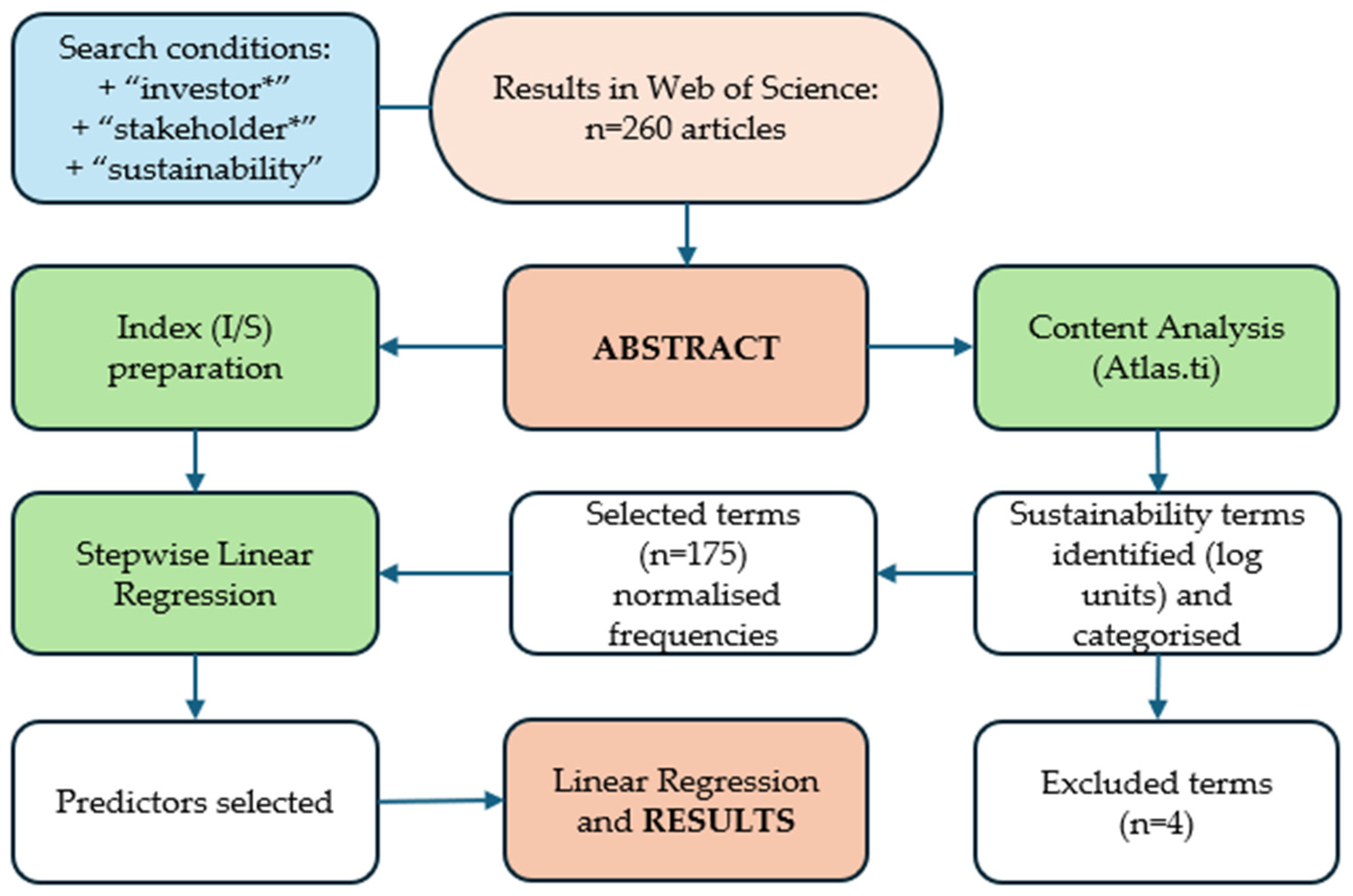

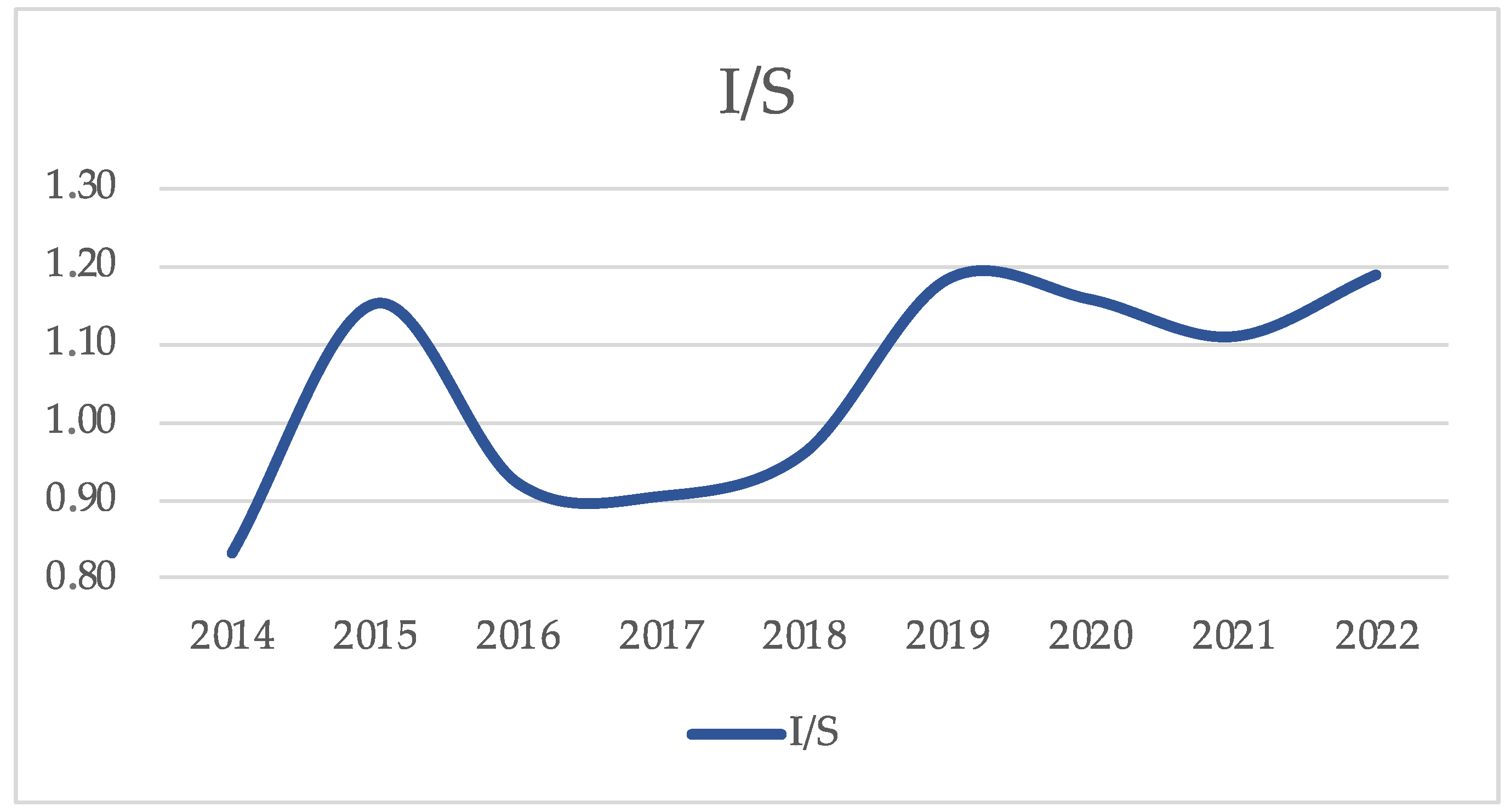

In this context, this research has its origin in the observation of the increasing and separate use of the term “investor” with respect to the term “stakeholder” in scientific articles when, concurrently, the term “sustainability” is present (

Table 1). The same circumstance occurs in other informative publications or in regulatory language, where it is common to find expressions describing conditions affecting investors as the main group, with the generic term “other stakeholders” being added to describe the rest of the stakeholder groups that may be affected.

This growth can be measured by the rate of variation in the occurrence of the first term in relation to the second (investors/stakeholders—I/S) and can be correlated with the other sustainability-related terms identified in the selected scientific literature review. As far as we are aware, there is no measurement in the sense we propose in the scientific literature, so it should be considered a contribution of this article.

Furthermore, we would expect the literature to relate the main interests of investors to the above-mentioned aspects of sustainability, considering that this stakeholder group will maintain their usual attention and interest in this matter [

55], to protect the interests of their investments, alleviate the associated risks, and maintain the existing opportunities and the regulatory requirements to which they are subject.

Hence, the purpose of this research is to determine whether, in the context of sustainability, the separate and growing presence of the term “investor” in the scientific literature is due to the fact that this primary group of stakeholders is establishing new relationships with terms related to the vocabulary of sustainability, understood as a set of customs or words that contain meanings that enable interlocutors to understand each other [

56].

We, therefore, propose the following hypotheses:

H1. The growth of the I/S index is directly related to those concepts having traditionally been linked to the control group of financial resources.

H2. The growth of the I/S index is related to an increased and generalised use of the sustainability lexicon.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}