CSR Reporting Practices in Visegrad Group Countries and the Quality of Disclosure

Abstract

:1. Introduction

2. Literature Review

3. Research Methodology

- What is the current state of CSR reporting in V4 countries? (What types of companies publish CSR reports? What types of reports are these? According to which guidelines are these reports prepared? Are the data in these reports subject to external verification?)

- What is the quality level of CSR reports published in V4 countries?

- What are the quality differences between reports prepared according to the GRI guidelines and those not prepared according to the GRI guidelines?

- What are the quality differences between reports externally verified and those not externally verified?

3.1. Data Collection

3.2. Assessment Tool

3.3. Quality Indicators of CSR Reports

- R—relevance of information indicator,

- C—credibility of information indicator.

4. Results

4.1. Current State of CSR Reporting in V4 Countries

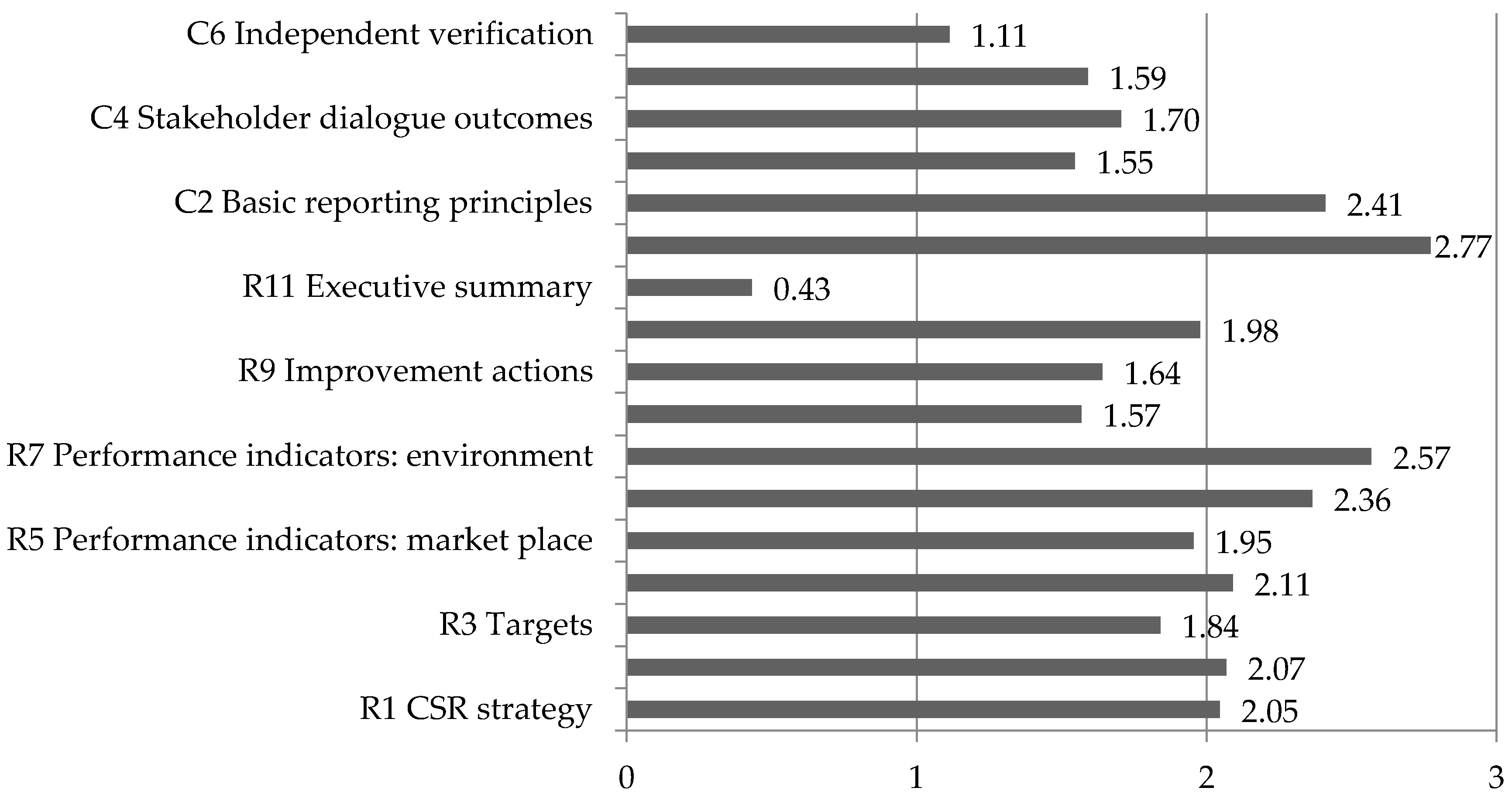

4.2. Quality Level of CSR Reports from the Visegrad Group Countries

4.3. Factors Influencing the Level of Quality of CSR Reports

5. Discussion

6. Conclusions

Conflicts of Interest

References

- Kołodziej, S.; Maruszewska, E.W. Economical Effectiveness and Social Objectives in Corporate Social Reports—A Survey among Polish Publicly Traded Companies. Available online: https://www.researchgate.net/profile/Ewa_Maruszewska/publication/307875171_Economical_effectiveness_and_social_objectiveness_in_corporate_social_reports_-_a_survey_among_Polish_publicly_traded_companies/links/582b376b08ae102f07208568/Economical-effectiveness-and-social-objectiveness-in-corporate-social-reports-a-survey-among-Polish-publicly-traded-companies.pdf (accessed on 7 December 2017).

- Michelon, G.; Pilonato, S.; Ricceri, F. CSR reporting practices and the quality of disclosure: An empirical analysis. Crit. Perspect. Account. 2015, 33, 59–78. [Google Scholar] [CrossRef] [Green Version]

- Husillos, J.; Larrinaga, C.; Gil, M.J.A. The emergence of triple bottom line reporting in Spain. Spanish J. Financ. Account. 2011, 40, 195–219. [Google Scholar] [CrossRef]

- Adams, C.A. The ethical, social and environmental reporting—Performance portrayal gap. Account. Audit. Account. J. 2004, 17, 731–757. [Google Scholar] [CrossRef]

- Dando, N.; Swift, T. Transparency and assurance: Minding the Credibility Gap. J. Bus. Ethics 2003, 44, 195–200. [Google Scholar] [CrossRef]

- Gray, R. Is accounting for sustainability actually accounting for sustainability and how would we know? An exploration of narratives of organisations and the planet. Account. Organ. Soc. 2010, 35, 47–62. [Google Scholar] [CrossRef]

- Chen, S.; Bouvain, P. Is Corporate Responsibility Converging? A Comparison of Corporate Responsibility Reporting in the USA, UK, Australia, and Germany. J. Bus. Ethics 2009, 87, 299–317. [Google Scholar] [CrossRef]

- Maignan, I.; Ralston, D.A. Corporate Social Responsibility in Europe and the U.S.: Insights from Businesses’ Self-presentations. J. Int. Bus. Stud. 2002, 33, 497–514. [Google Scholar] [CrossRef]

- Delbard, O. CSR legislation in France and the European regulatory paradox: An analysis of EU CSR policy and sustainability reporting practice. Corp. Gov. Int. J. Bus. Soc. 2008, 8, 397–405. [Google Scholar] [CrossRef]

- Segal, J.P.; Sobczak, A.; Triomphe, C.E. Corporate Social Responsibility and Working Conditions. Available online: http://www.uni-mannheim.de/edz/pdf/ef/03/ef0328en.pdf (accessed on 12 June 2017).

- Antal, A.B.; Sobczak, A. Corporate Social Responsibility in France: A Mix of National Traditions and International Influences. Bus. Soc. 2007, 46, 9–32. [Google Scholar] [CrossRef] [Green Version]

- Hąbek, P.; Wolniak, R. Assessing the quality of corporate social responsibility reports: The case of reporting practices in selected European Union member states. Qual. Quant. 2015, 50, 399–420. [Google Scholar] [CrossRef] [PubMed]

- Ruževičius, J.; Serafinas, D. The Development of Socially Responsible Business in Lithuania. Eng. Econ. 2015, 51, 36–43. [Google Scholar]

- Dočekalová, M. Corporate Sustainability Reporting in Czech Companies—Case Studies. Trends Econ. Manag. 2012, 6, 9–16. [Google Scholar]

- Petera, P.; Wagner, J.; Boučková, M. An Empirical Investigation into CSR Reporting by the Largest Companies with their seat in the Czech Republic. In Proceedings of the 22nd Interdisciplinary Information Management Talks, Podebrady, Czech Republic, 10–12 September 2014; pp. 321–329. [Google Scholar]

- Kunz, V.; Srpová, J. CSR Reporting and its Use by Enterprises in the Czech Republic. Manag. Sci. Educ. 2013, 1, 31–34. [Google Scholar]

- Karcagi-Kováts, A.; Kuti, I. Diversity of Sustainability Performance Indicators and Corporate Reporting in Hungary. In Proceedings of the Corporate Responsibility Research Conference CRRC, Marseille, France, 15–17 September 2010. [Google Scholar]

- Piskóti, I.; Hajdú, N. A Benchmarking Approach to the Situation and Topics in CSR Reports of Hungarian Corporations, Responsibility and Sustainability. Socioecon. Political Legal Issues 2013, 2, 1–13. [Google Scholar]

- Hąbek, P. Evaluation of sustainability reporting practices in Poland. Qual. Quant. 2014, 48, 1739–1752. [Google Scholar] [CrossRef]

- Astupan, D.; Schönbohm, A. Sustainability Reporting Performance in Poland: Empirical Evidence from the WIG 20 and WIG 40 Companies. Pol. J. Manag. Stud. 2012, 6, 68–80. [Google Scholar]

- Szczepankiewicz, E.I.; Mućko, P. CSR Reporting Practices of Polish Energy and Mining Companies. Sustainability 2016, 8, 126. [Google Scholar] [CrossRef]

- Kubaščíková, Z. Sustainable Development Reporting. Manag. Inf. Syst. 2008, 3, 19–23. [Google Scholar]

- Freundlieb, M.; Gräuler, M.; Teuteberg, F. A conceptual framework for the quality evaluation of sustainability reports. Manag. Res. Rev. 2014, 37, 19–44. [Google Scholar] [CrossRef]

- Hąbek, P.; Brodny, J. Corporate Social Responsibility Report—An Important Tool to Communicate with Stakeholders. In Proceedings of the 4th International Multidisciplinary Scientific Conference on Social Sciences & Arts, Albena, Bulgaria, 22–31 August 2017; pp. 241–248. [Google Scholar]

- Daub, C.-H. Assessing the quality of sustainability reporting: An alternative methodological approach. J. Clean. Prod. 2007, 15, 75–85. [Google Scholar] [CrossRef]

- Ching, H.Y.; Gerab, F.; Toste, T. Analysis of Sustainability Reports and Quality of Information Disclosed of Top Brazilian Companies. Int. Bus. Res. 2013, 6, 62–77. [Google Scholar] [CrossRef]

- G4 Sustainability Reporting Guidelines. Reporting Principles and Standard Disclosures. Available online: https://www.globalreporting.org/resourcelibrary/GRIG4-Part1-Reporting-Principles-and-Standard-Disclosures.pdf (accessed on 7 December 2017).

- Sustainable Development Reporting—Striking the Balance. Available online: http://www.wbcsd.org/Projects/Reporting/Resources/Sustainable-Development-Reporting-Striking-the-balance (accessed on 7 December 2017).

- Leitonienea, S.; Sapkauskiene, A. Quality of Corporate Social Responsibility Information. Procedia Soc. Behav. Sci. 2015, 213, 334–339. [Google Scholar] [CrossRef]

- Baviera-Puig, A.; Gómez-Navarro, T.; García-Melón, M.; García-Martínez, G. Assessing the Communication Quality of CSR Reports. A Case Study on Four Spanish Food Companies. Sustainability 2015, 7, 11010–11031. [Google Scholar] [CrossRef]

- Legendre, S.; Coderre, F. Determinants of GRI G3 application levels: The case of the Fortune Global 500. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 182–192. [Google Scholar] [CrossRef]

- Ruhnke, K.; Gabriel, A. Determinants of voluntary assurance on sustainability reports: An empirical analysis. J. Bus. Econ. 2013, 83, 1063–1091. [Google Scholar] [CrossRef]

- Bachoo, K.; Tan, R.; Wilson, M. Firm value and the quality of sustainability reporting in Australia. Aust. Account. Rev. 2013, 23, 67–87. [Google Scholar] [CrossRef]

- Zorio, A.; García-Benau, M.A.; Sierra, L. Sustainability development and the quality of assurance reports: Empirical evidence. Bus. Strategy Environ. 2013, 22, 484–500. [Google Scholar] [CrossRef]

- Lock, I.; Seele, P. The credibility of CSR reports in Europe. Evidence from a quantitative content analysis in 11 countries. J. Clean. Prod. 2016, 122, 186–200. [Google Scholar] [CrossRef]

- Hahn, R.; Kühnen, M. Determinants of sustainability reporting: A review of results, trends, theory, and opportunities in an expanding field of research. J. Clean. Prod. 2013, 59, 5–21. [Google Scholar] [CrossRef]

- Beretta, S.; Bozzolan, S. Quality versus Quantity: The Case of Forward-Looking Disclosure. J. Account. Audit. Financ. 2008, 23, 333–376. [Google Scholar] [CrossRef]

- Kuzey, C.; Uyar, A. Determinants of sustainability reporting and its impact on firm value: Evidence from the emerging market of Turkey. J. Clean. Prod. 2016, 143, 27–39. [Google Scholar] [CrossRef]

- Bluszcz, A. A comparative analysis of selected synthetic indicators of sustainability. Procedia Soc. Behav. Sci. 2016, 220, 40–50. [Google Scholar] [CrossRef]

- Jonek-Kowalska, I.; Zieliński, M. CSR Activities in the Banking Sector in Poland. In Proceedings of the 29th International-Business-Information-Management-Association Conference, Vienna, Austria, 3–4 May 2017; pp. 1294–1304. [Google Scholar]

- Cierna, H.; Sujova, E. Parallels Between Corporate Social Responsibility and the EFQM Excellence Model. MM Sci. J. 2015, 670–676. [Google Scholar] [CrossRef]

- Hąbek, P.; Molenda, M. Using the FMEA Method as a Support for Improving the Social Responsibility of a Company. In Proceedings of the 6th International Conference on Operations Research and Enterprise Systems (ICORES 2017), Porto, Portugal, 23–25 February 2017; pp. 57–65. [Google Scholar]

- Pflugrath, G.; Roebuck, P.; Simnett, R. Impact of assurance and assurer’s professional affiliation on financial analysts’ assessment of credibility of corporate social responsibility information. Audit. J. Pract. Theory 2011, 30, 239–254. [Google Scholar] [CrossRef]

- Park, J.; Brorson, T. Experiences of and views on third-party assurance of corporate environmental and sustainability reports. J. Clean. Prod. 2015, 13, 1095–1106. [Google Scholar] [CrossRef]

- Alavi, H.; Hąbek, P. Addressing Research Design Problem in Mixed Methods Research. Manag. Syst. Prod. Eng. 2016, 21, 62–66. [Google Scholar] [CrossRef]

- GRI’s Sustainability Disclosure Database. Available online: http://database.globalreporting.org (accessed on 17 January 2017).

- Wolniak, R. The role of Grenelle II in Corporate Social Responsibility Integrated Reporting. Manag. J. 2013, 18, 109–119. [Google Scholar]

- Eurostat Data—Business Demography by Size Class (NACE Rev. 2) in 2014, Business Economy except Activities of Holding Companies. Available online: http://ec.europa.eu/eurostat/statistics-explained/index.php/Business_demography_regional_analysis (accessed on 11 January 2017).

- UNGC Website. Available online: https://www.unglobalcompact.org/what-is-gc/participants (accessed on 29 December 2016).

- Hąbek, P. How do companies in European Union disclose their non-financial data? In Proceedings of the International Masaryk Conference for Ph.D. Students and Young Researchers, Hradec Kralove, Czech Republic, 9–13 December 2013; pp. 92–100. [Google Scholar]

{kind=link}

| Authors | Methods/Sample | Quantity Analysis | Quality Analysis | Findings |

|---|---|---|---|---|

| Michelon, G.; Pilonato, S.; Ricceri, F. (2015) | Content analysis, Global Reporting Initiative framework used to assess CSR information disclosures,112 UK companies | x | x | On average, companies that use CSR reporting practices do not provide a higher quality of information. |

| Ching, H.Y.; Gerab, F.; Toste, T. (2013) | Content analysis, 60 listed Brazilian companies, the Global Reporting Initiative framework used to assess the reports | x | Sustainability reports still have a big room for improvement. Companies need to disclose their information in a more integrated way, addressing sustainability issues under the scope of business strategy. | |

| Daub, C.-H.J. (2007) | 76 companies/33 individual criteria, benchmark study, Swiss companies ranked according to the total score, | x | An evaluation of the performance of the reporting company resulted in a clear weakness in reporting performance indicators. | |

| Leitonienea, S.; Sapkauskiene, A. (2015) | Quality index/48 reports of socially responsible Lithuanian companies | x | The results of the quality of information showed that the quality index of joint stock companies is higher, which belong to those sectors which have a significant impact on the environment, i.e., manufacturing, energy and telecommunications. | |

| Baviera-Puig, A.; Gómez-Navarro, T.; García-Melón, M.; García-Martínez, G. (2015) | Multi-criteria methodology, using the Analytic Network Process, large food Spanish companies | x | Results show varying degrees of quality in the communication of different enterprises from the same sector. This assessment highlights the weaknesses and areas for improvement of each of the reports analyzed from a multi-stakeholder point of view. | |

| Lock, I.; Seele, P. (2016) | Quantitative content analysis, the credibility of 237 European CSR reports is studied, human as well as software coding was applied, listed companies from Austria, Belgium, France, Germany, Italy, The Netherlands, Poland, Spain, Sweden | x | CSR reports are credible at a mediocre level, leaving much room for improvement. Reports must be understandable, before truth, sincerity, appropriateness are addressed. | |

| Hąbek, P.; Wolniak, R. (2015) | Quality disclosure index/507 CSR reports assessed from UK, France, The Netherlands, Sweden, Denmark, Poland | x | The quality level of the studied reports is generally low, and there is space for improvement in all studied countries. Referring to the components of the quality indicator, the relevance of the information provided in the assessed reports is at a higher level than its credibility. |

| Country | No. of Reports in the GRI Sustainability Disclosure Database Published in 2014 | CSR Reports Admitted to Analysis of Current CSR Reporting Practices in V4 Countries | No. of CSR Reports Admitted to Quality Assessment (Reports only in English) |

|---|---|---|---|

| Czech Republic | 20 | 20 | 7 |

| Hungary | 30 | 22 | 14 |

| Poland | 36 | 36 | 20 |

| Slovakia | 4 | 4 | 3 |

| Assessment Criteria: Relevance of Information | Scale | |||||

| 0 | 1 | 2 | 3 | 4 | ||

| R1 | Corporate social responsibility strategy The report presents the business strategy which relates to the aspects of CSR | |||||

| R2 | Key stakeholders The report contains identification of organization’s stakeholders, their expectations and a way of engagement with individual groups | |||||

| R3 | Targets The report presents targets for the future, targets set in the previous reporting period and the level of their achievements | |||||

| R4 | Trends over time The report contains indicators shown over several reporting periods indicating this way direction of change and ensuring their comparability | |||||

| R5 | Performance indicators: market place The report contains quantitative information concerning organization’s performance achieved in area of market place | |||||

| R6 | Performance indicators: workplace The report contains quantitative information concerning organization’s performance achieved in area of workplace | |||||

| R7 | Performance indicators: environment The report contains quantitative information concerning organization’s performance achieved in area of environment | |||||

| R8 | Performance indicators: community The report contains quantitative information concerning organization’s performance achieved in area of community | |||||

| R9 | Improvement actions The report describes improvement activities undertaken by the organization in the scope of CSR, e.g., programs to increase resource efficiency, reduction of emission, etc. | |||||

| R10 | Integration with business processes The report contains information confirming that the aspects of CSR are included in the decision-making process and implemented in the basic processes (purchasing, sales, marketing, production, etc.) | |||||

| R11 | Executive summary The report provides a concise and balanced overview of key information and indicators from the reporting period | |||||

| Assessment Criteria: Credibility of Information | Scale | |||||

| 0 | 1 | 2 | 3 | 4 | ||

| C1 | Readability The report has a logical structure, uses a graphical presentation of the data, drawings, and explanations where required or uses other tools to help navigate through the document | |||||

| C2 | Basic reporting principles The reporting period, scope and entity are defined in the report as well as limitations and target audience | |||||

| C3 | Quality of data The report describes the processes, procedures of collection, aggregation and transformation of data and determines the source of the data | |||||

| C4 | Stakeholder dialogue outcomes The report contains a description of the stakeholders’ dialogue and the results of this dialogue in relation to aspects of CSR (surveys, consultations, focus groups, round Tables, programs, engagement, etc.) | |||||

| C5 | Feedback The report contains a mechanism that allows a feedback process (contact point for suggestions or questions, hotline, email, reply card, questionnaire, etc.) | |||||

| C6 | Independent verification The report contains a statement of independent body attesting the authenticity of data presented in the report as well as proposals for future improvements | |||||

| Scores | Assessment Requirements |

|---|---|

| 0 | No mention or insufficient information on individual criteria |

| 1 | Some/little/partial mention or coverage |

| 2 | Most important aspects covered, average |

| 3 | Better than average, the report presents detailed information |

| 4 | Best practices and creative approach, innovative disclosure and explanation |

| EU Member State | CSR Report 2014 | Population of Active Enterprises * | No. of Reports per Million Enterprises |

|---|---|---|---|

| Czech Republic | 20 | 1,022,045 | 19.6 |

| Hungary | 30 | 522,058 | 57.5 |

| Poland | 36 | 2,025,270 | 17.8 |

| Slovakia | 4 | 438,067 | 9.1 |

| Country | Czech Republic | Hungary | Poland | Slovakia |

|---|---|---|---|---|

| Number of signatory (type: company and SME) | 14 | 7 | 67 | 4 |

| Country | Organization Size | Organization Type | ||||||

|---|---|---|---|---|---|---|---|---|

| SME | Large | MNE | Listed | Private | Subsidiary | State-Owned | Others | |

| Czech Republic N = 20 | - | 40% | 60% | 40% | 40% | 45% | 10% | 5% |

| Hungary N = 22 | 14% | 36% | 50% | 27% | 23% | 50% | 18% | 9% |

| Poland N = 36 | 8% | 86% | 6% | 44% | 61% | 25% | 11% | 3% |

| Slovakia N = 4 | - | 100% | - | - | 25% | 75% | - | - |

| Total V4 | 7% | 62% | 31% | 37% | 44% | 39% | 12% | 5% |

| Country | Separate CSR Report | Annual Report with CSR Section | Integrated Report | Report according to GRI | Independent Verification | UN Global Compact Signatory |

|---|---|---|---|---|---|---|

| Czech Republic N = 20 | 95% | 5% | - | 20% | 5% | - |

| Hungary N = 22 | 91% | - | 9% | 59% | 23% | 18% |

| Poland N = 36 | 75% | 3% | 22% | 47% | 22% | 28% |

| Slovakia N = 4 | 100% | - | - | 50% | - | 25% |

| Total V4 | 85% | 2% | 12% | 44% | 16% | 18% |

| Country | Number in Sample | Percentage |

|---|---|---|

| Czech Republic | 7 | 15.91 |

| Hungary | 14 | 31.82 |

| Poland | 20 | 45.45 |

| Slovakia | 3 | 6.82 |

| Variable | M | SD | Mdn | Min | Max | S-W | p |

|---|---|---|---|---|---|---|---|

| Relevance of information—R | 1.87 | 0.80 | 1.95 | 0.27 | 3.27 | 0.95 | 0.036 |

| Credibility of information—C | 1.86 | 0.83 | 2.00 | 0.33 | 3.33 | 0.94 | 0.018 |

| Quality of CSR reports—Q | 1.86 | 0.78 | 2.04 | 0.30 | 3.30 | 0.95 | 0.049 |

| Variable | GRI | M | SD | Min | Max | Z | p |

|---|---|---|---|---|---|---|---|

| Relevance of information—R | No (n = 8) | 1.16 | 0.72 | 0.36 | 2.27 | 2.65 | 0.007 |

| Yes (n = 36) | 2.03 | 0.74 | 0.27 | 3.27 | |||

| Credibility of information—C | No (n = 8) | 0.83 | 0.53 | 0.50 | 2.00 | 3.53 | <0.001 |

| Yes (n = 36) | 2.08 | 0.71 | 0.33 | 3.33 | |||

| Quality of CSR reports—Q | No (n = 8) | 1.00 | 0.60 | 0.43 | 2.14 | 3.23 | 0.001 |

| Yes (n = 36) | 2.05 | 0.68 | 0.30 | 3.30 |

| GRI | ||

|---|---|---|

| Spearman’s Rho | p-Value | |

| Quality of CSR reports—Q | 0.49 | 0.001 |

| Variable | Independent Verification | M | SD | Min | Max | Z | p |

|---|---|---|---|---|---|---|---|

| Relevance of information—R | No (n = 31) | 1.72 | 0.86 | 0.27 | 3.27 | 2.05 | 0.040 |

| Yes (n = 13) | 2.23 | 0.48 | 1.45 | 3.00 | |||

| Credibility of information—C | No (n = 31) | 1.57 | 0.80 | 0.33 | 3.33 | 3.80 | <0.001 |

| Yes (n = 13) | 2.54 | 0.43 | 1.83 | 3.33 | |||

| Quality of CSR reports—Q | No (n = 31) | 1.64 | 0.79 | 0.30 | 3.30 | 2.97 | 0.003 |

| Yes (n = 13) | 2.38 | 0.41 | 1.81 | 3.17 |

| Independent Verification | ||

|---|---|---|

| Spearman’s Rho | p-Value | |

| Quality of CSR reports—Q | 0.45 | 0.002 |

© 2017 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hąbek, P. CSR Reporting Practices in Visegrad Group Countries and the Quality of Disclosure. Sustainability 2017, 9, 2322. https://doi.org/10.3390/su9122322

Hąbek P. CSR Reporting Practices in Visegrad Group Countries and the Quality of Disclosure. Sustainability. 2017; 9(12):2322. https://doi.org/10.3390/su9122322

Chicago/Turabian StyleHąbek, Patrycja. 2017. "CSR Reporting Practices in Visegrad Group Countries and the Quality of Disclosure" Sustainability 9, no. 12: 2322. https://doi.org/10.3390/su9122322

APA StyleHąbek, P. (2017). CSR Reporting Practices in Visegrad Group Countries and the Quality of Disclosure. Sustainability, 9(12), 2322. https://doi.org/10.3390/su9122322