1. Introduction

It is widely agreed that the quality of governance matters for economic prosperity [

1,

2,

3], but the linkage between specific aspects of governance quality and economic prosperity has not been sufficiently studied in the literature yet. In the World Bank’s first series of publications that stress “governance matters for development”, the notion of “good governance” was built on four components that include the competence of the public sector to manage the economy and deliver public services, accountability of public officials, transparency of policy frameworks, and a legal framework for development [

4,

5,

6]. However, the literature has not reached a consensus on what type of legal framework performs better in facilitating development [

7,

8]. In the World Bank’s publication, only the legal framework satisfying the principle of “the rule of law” can create a sufficient stable setting for efficient use of resources and productive investment [

5]. Nevertheless, “the rule of law is notoriously difficult to define and measure” [

9]. Meanwhile, the connection between the rule of law and economic prosperity is still under extensive debate [

10,

11]. In several emerging economies, a low or even, sometimes, a negative association between the rule of law and economic development is observed [

12,

13]. In addition, as far as the authors are aware, to date, all the existing analyses on the law–development nexus have been conducted at a national level and none have been based on subnational or city-level data.

Over the last few decades, the Chinese ruling party (Chinese Communist Party, CCP) has made constant efforts towards “governing the country according to the law” [

14]. Just recently, the fourth plenary session of the 19th CCP Central Committee that ended in Oct. 2019 again reiterated the importance of “ensuring law-based governance in all areas, building a country of socialist rule of law” [

15]. However, several scholars have stressed that the Chinese state’s attempts to use laws as a means to exercise the rule do not fit the universal notion of the “rule of law” but instead are better interpreted as pursuing a governance model of “rule by law” [

16,

17,

18,

19]. In this paper, we do not plan to get involved in the debate on whether and how the Chinese institutionalization efforts in its legal framework are different from the universal notion of the “rule of law”. We hereby use the term “law-based governance” to refer to the law aspect of governance, as this term is the standard word used in the English versions of the Chinese government’s official documents for promoting legal development [

20] and also the translated copy of President Xi Jinping’ related works [

21]. While “law-based governance” appears to mainly emphasize the functional use of law in the spirit of “governing according to law” [

22] or “rule-based regulation” and “law-based control” [

17], it is, however, open to wider interpretations. For example, we presume that the notion of law-based governance is compatible with the World Bank’s Worldwide Governance Indicators project team’s conception of the rule of law: “perceptions of the extent to which agents have confidence in and abide by the rules of the society, and in particular the quality of contract enforcement, property rights, the police, and the courts, as well as the likelihood of crime and violence” [

23].

This paper describes the relationship between average city-level housing prices and law-based governance, or the law aspect of governance, in Chinese cities. In this analysis, housing prices are chosen as a proxy to reflect both contemporary prosperity and people’s confidence in future economic prosperity [

24]. According to classical urban economics literature, people choose where to dwell by “voting with their feet” and their competition for desirable urban amenities including the quality of urban governance is well capitalized in housing prices [

25,

26,

27]. Exploring the cross-city variations of the linkage between housing prices and law-based governance in China can provide rich information on how Chinese people value the law aspect of governance quality in their location choices. Such work will then contribute to bridging the knowledge gap regarding the heterogeneous associations between legal development and economic prosperity within a given political regime.

Our research work is premised on three unique advantages. First, we have the chance to utilize city-level indicators of law-based governance, which are rarely available in the empirical literature. The rule of law or quality of law-based governance is generally assessed on the country level but its city-level variations within a country are rarely explored in the literature. Second, compared to advanced economies, the Chinese housing market is still nascent and sensitive to the quality of the law aspect of governance. Launched formally in 1998 on the basis of the abolishment of a welfare housing system that served the needs of the central planning economy, the Chinese housing market has just roughly two decades of development history and many institution buildings are still evolving [

24,

28]. It will thus be of great interest to discover how people’s confidence in the future prospects of local property is associated with the law aspect of governance in a nascent housing market. Third, China is a vast country with significant regional variations in both housing market development and the quality of governance, particularly its law aspect. These significant regional variations make it possible to detect the detailed heterogeneity of the relationship between housing market booms and law-based governance.

By investigating the correlations between law-based governance and housing prices, especially the mediating mechanisms, sensitivity, and heterogeneity of the relationship, this paper contributes to the literature in four aspects. First, for the first time, we demonstrate that a higher degree of law-based governance in one city is on average associated with higher average city-level housing prices. This relationship remains consistent in different subsamples, various model settings, and is robust when applying instrument variable (IV) estimators to alleviate potential endogeneity bias. In particular, we construct a weighted distance as an instrument for law-based governance using distances between different levels of government. Second, we find evidence that the effect of law-based governance can work through expanding the supply of banking loans and stimulating more foreign investment and, further, we find that the mediating role of loans is greater than that of foreign investment. Third, we find that the correlation of law-based governance and housing prices is stronger when the public has higher satisfaction with the quality of the law aspect of governance. This suggests that the extent that the law aspect of governance can be felt and accredited by the public is the key for law-based governance to affect people’s confidence in asset prices. Fourth, the size of the association between law-based governance and housing prices is heterogeneous across different city groups. In particular, we find the association is greater in the first- and second-tier cities, and presume this is because housing is expensive in these cities and thus buyers and investors are more sensitive to the security of property rights and guarantee of contract outcomes.

The remainder of this study is structured as follows.

Section 2 explores the mechanisms through which law-based governance correlates with housing prices, reviews the relevant literature, discusses potential research gaps, and proposes research hypotheses of this paper;

Section 3 displays the methodology and constructs the empirical model used in this study;

Section 4 introduces the variables and data;

Section 5 presents the estimation results and shows robustness checks and other extensions. Finally, we conclude this study with policy suggestions in

Section 6.

2. Analytic Framework and Hypothesis Development

In this section, we first discuss the literature relevant to the general relationship between law-based governance and housing prices, China’s pursuit of law-based governance, and Chinese housing market development. Based on the insights and theoretic arguments from the existing literature, we derive the main hypotheses to be tested in the study.

2.1. Governance, Law, and Economic Development

Since the World Bank’s 1992 publication of the booklet “Governance and Development”, the roles of governance in development and economic prosperity have been extensively studied worldwide [

2,

3,

29,

30,

31]. For example, governance is said to affect economic growth via many direct and indirect channels, but the central role is its function in the formation of an institutional environment that is friendly to investment and capital accumulation [

32]. Alternatively, good governance can be considered as the existence of an appropriate set of institutions that reward efforts to develop economic performance [

33].

From the beginning of the World Bank’s call for “good governance”, the rule of law, alongside accountability and transparency, is one of the central elements of governance institutions [

6]. The World Bank itself deemed that “some elements of rule of law are needed to create a sufficient stable environment for economic actors to make investments and transact business” [

5], and further proposed that “good governance is epitomized … by all behaving under the rule of law” [

6]. The build-up of “good governance” has always been closely blended with the concept of the “rule of law” as they are believed to mutually reinforce each other [

3]. Although with a wide or sometimes, arguably, an all-embracing meaning, the “rule of law” is perhaps one of the most universally appealing political concepts. For example, the principle of the “rule of law” has been interpreted as “man is governed by law, and not by whims of men” [

5]. Meanwhile, the rule of law is also said to mean that “the state should exercise power under the authority of law; government officials should be subject to law just as private citizens” [

5]. As the United Nations put it, “the rule of law is a principle of governance in which all persons, institutions and entities, public and private, including the State itself, are accountable to laws” [

34]. In empirical work, the rule of law is one of the six ingredients in the World Bank’s Worldwide Governance Indicators [

35], and the World Development Report 2017 also stresses the importance of the linkage between governance and law [

36].

However, the connection between the degree of the rule of law and economic prosperity involves much controversy [

10]. Taking the case of China as an example, China’s performance of the rule of law is generally assessed as inferior in Western literature [

37,

38], and consistently ranks low in most international rankings, e.g., China was ranked 100 in 2014 and 87 of 177 countries and regions in 2018 on the Corruption Perceptions Index (CPI). Nonetheless, despite the persistence of low international assessment of its degree of rule of law, China has not only achieved a stunning miracle of economic growth since 1978 but also continued to maintain the economic boom after four decades of rapid development. This phenomenon has been called the China paradox, between the low degree of rule of law and high economic growth, in the literature [

39]. A similar association is also observed in several other new emerging economies [

12,

40]. It has been suggested that in the case of China, the disinterested government, i.e., a government that not captured by any interest group, is impartial towards different sections of the population and prioritizes the long-term welfare of the whole society [

41], acting as a substitute for the rule of law to constrain the pitfalls of “entrenched special interest groups” and underpinning China’s economic success [

42]. However, the exact relationship between Chinese-style rule of law and economic performance has not received much empirical investigation.

2.2. China’s Pursuit of Law-Based Governance

Since 1978, accompanying the shift towards a market-oriented economic system, the Chinese party-state has pledged to move forward with “ruling the country by law”, the professionalization of the judiciary, and the expansion of legal practitioners, and many new laws have been passed [

18,

38,

43].

Table 1 shows the major events in China’s pursuit of law-based governance during the period 1997–2010.

In the Xi Jinping era, in 2012, the 18th Congress of the Chinese Communist Party and two important decisions adopted subsequently in the 3rd and 4th Plenum in 2013 and 2014, respectively, opened new phases of China’s instrumentalist legal-based governance [

38]. Particularly, the fourth plenary session of the 18th CCP Central Committee that convened in Oct. 2014 was exclusively devoted to a theme “concerning comprehensively advancing the law-based governance of China”. The Plenum called for making “coordinated efforts to promote law-based governance, law-based exercise of state power, and law-based administration of government”, and emphasized that “justice is administered impartially, the law is observed by everyone”, in order to “ensure that everyone is equal before the law” [

45]. The Plenum also pointed out that “to exercise state power based on law, the Party not only has to govern the country in accordance with the Constitution and laws, but also has to ensure that its self-governance is in line with its own rules and regulations”, and therefore “to ensure judicial impartiality and improve judicial credibility” [

45]. It was clearly stated at this Plenum that “the law is an instrument of great value in the governance of a country and good laws are a prerequisite for good governance” [

45].

The pronouncements on socialist law-based governance at the Congresses and Plenums, together with the legal dimensions of Xi Jinping’s anticorruption campaign, signify China’s localization of international standard of rule of law discourses including substantial modifications to fit Chinese circumstances and the party-state’s ambitions [

22,

46]. According to the

Implementation Outline for Constructing Law-based Government (2015–2020), jointly issued by the Central Committee of the Communist Party of China (CPC) and the State Council on Dec. 2015, the law-based governance structure that ensures all the government’s work complies with the law should be basically established by 2020. The fulfillment of this aim, however, requires not only major institutional developments but also sufficient legal service capability. The data from China’s Ministry of Justice suggest that, by the end of 2019, in China there were 473,000 practicing lawyers, including 393,300 full-time lawyers, 43,300 public lawyers, and 10,900 corporate lawyers; Beijing, Guangdong, Jiangsu, and Shandong are the four provincial-level region units that host more than 30,000 lawyers [

47]. However, in terms of registered lawyers per capita, the gap between China and the advanced economies is still very large.

2.3. Evolution and Differentiation of Chinese Housing Market

The Chinese housing market plays an important role in the economy and society [

24]. In July 1998, the State Council formally abolished the in-kind distribution of welfare housing in urban areas. Between 1999 and 2016, the Chinese government considered the commodity housing sector as an engine to promote investment, expand domestic demand, and boost economic growth [

48]. During this period, the scale of real estate investment was over-inflated and prices rose fast. According to the data released by the National Bureau of Statistics, the phase of fastest-rising housing prices in China was 2004–2009, with an average annual growth rate of 12.4% and a more pronounced phenomenon of investment and speculation. In November 2008, China proposed an economic stimulus package totaling about four trillion RMB in response to the financial crisis, and housing prices grew by as much as 23.2% in 2009. Since 2010, in order to stabilize housing prices and alleviate the unaffordability crisis that has threatened social stability, the Chinese government has intensively introduced a series of regulatory policies to dampen the speculative demand. During the study period of this paper, 2014–2017, data from the National Bureau of Statistics show that the average annual growth rate of housing prices in China fell to 6.1%, which is lower than the average growth rate of 8% over the past 20 years. Based on this, the regulatory policies during this period were relatively loose, mainly in the form of interest rate and tax rate reductions. Since 2017, the Chinese government emphasized the residential nature of housing and insisted on the position that houses were for living in, not for speculation, and attempted to promote a steady development of the housing market [

49]. This seems to be a return to the original intent of the market-oriented housing reform in 1998.

During both the socialist planned economy era and the early stage of the economic reform era, housing in Chinese cities was considered as part of the welfare provision package, while population mobility was constrained, and thus the spatial differentiation of housing was insignificant [

50]. However, during the market-oriented development process of the housing sector, the widening regional economic inequality amplified by the massive urban–rural migration, as well as increasing city-to-city mobility, has led housing market conditions and institutional settings to rapidly exhibit substantial spatial variations across cities [

24]. In particular, housing prices have shown increasingly significant spatial differences across different tiers of cities [

51].

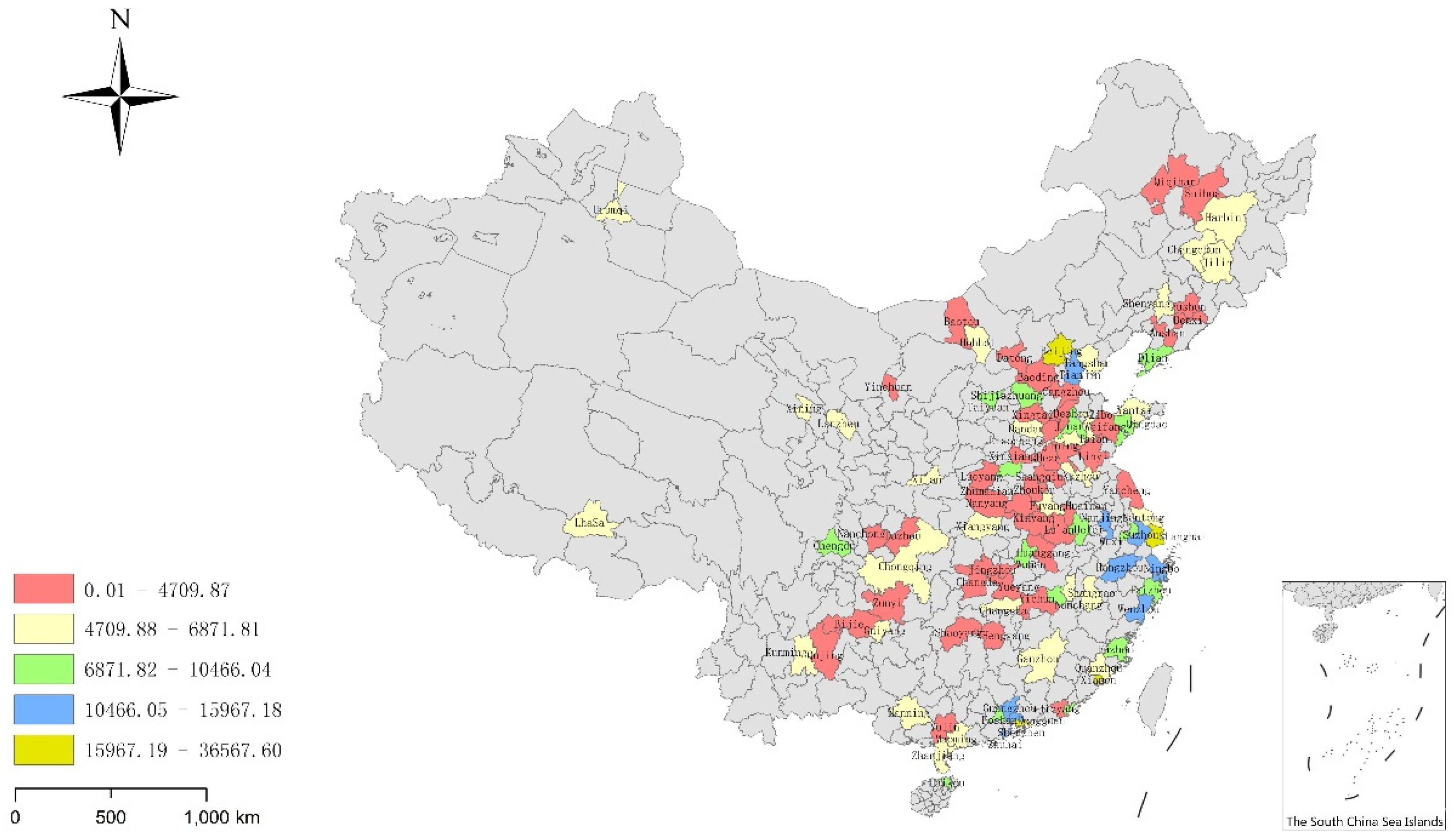

Figure 1 shows the spatial distribution of mean housing prices between 2014 and 2017 in 100 large and medium-sized sample cities.

It can be seen that the cities falling into the two highest housing price categories are mainly concentrated in the eastern region of China, such as Shenzhen, Beijing, Xiamen, Shanghai, Hangzhou, Zhuhai, Guangzhou, etc. Meanwhile, the cities with lower housing prices are primarily located in the central and western regions of China. Therefore, regional differences in housing prices are evident in China’s real estate market.

2.4. Mechanism Discussions and Hypothesis Development

A “fair” legal framework plays an important role in the housing market. Both housing investments made by developers and housing purchases made by households are capital intensive, and thus very sensitive to legal non-transparency or legal uncertainty. A business climate of predictability that features economic agents’ certainty in exercising their rights and high confidence in the restraint of arbitrary behavior of government officials can help greatly to attract stable capital investment and promote a sustainable boom in the housing market. The market confidence would be upheld with the availability of an independent and credible judicial system that can give impartial judgement in conflict solving even when the private agents confront the state. Over the last two decades, significant changes have been made to property-related laws as well as legal procedural frameworks of property-related dispute settlement as the state needs to respond to intensifying conflicts in the booming Chinese real estate market [

52]. There is also a growing awareness among the execution branches of Chinese local authorities of governing the growing rights-based disputes through law [

53], and increasing compliance with the law.

In addition, a high level of law-based governance may promote the housing market through better information disclosure. Evidently, the law aspect of governance strengthens information disclosure by improving the legal system, whereas liquid and credible information disclosure boosts buyers’/investors’ confidence and facilitates capital circulation [

54]. In fact, China has placed a lot of emphasis on the disclosure of government affairs and government information, which can improve public participation in decision making [

55]. For example, the Opinions on Comprehensively Promoting the Government Affairs Disclosure Work, issued by the General Office of the Central Committee of the CPC and the General Office of the State Council in 2016, provide the directions for work on government affairs disclosure. In addition, the Implementation Outline for Constructing Law-based Government (2015–2020) states clearly that information disclosure shall become a regular government practice [

56]. Moreover, the disclosure of government affairs and government information in the pursuit of a law-based government may alleviate the problem of information asymmetry in the housing market.

In a credit market, information asymmetry between transaction parties and the resulting moral hazard is a major obstacle for financial business. Without reliable legal enforcement to punish cheating and curtail opportunistic behaviors, financial institutions have to invest heavily in investigating the creditability quality of potential borrowers before deciding whether to release loans [

57]. The existence of serious information asymmetry and the failure to curb cheating would cause high financing costs, the prevalence of credit constraints, and weaker borrowing capacity. These problems can further accelerate the default of borrowers and in turn reduce the quantities of credit supply. Eventually, reduced availably of financial loans, to both developers and buyers, leads to a more depressed housing market [

58]. In contrast, housing markets that with less information asymmetry through a better legal arrangement for information disclosure can attract more credit inflow and have a greater chance to experience and sustain a boom.

Further, nations with highly transparent legal system can attract more foreign investment because a “level playing field” exists between foreign and local investors [

59]. In international investment, foreign investors particularly demand good local governance and strong law enforcement in the housing market [

60]. Therefore, it is reasonably expected that a nation/region with better law aspect of governance may attract more foreign investment, which may then boost the local housing market through both the direct injection of external demand for properties and indirect but more important shifts from the improvement of the long-term economic outlook.

In sum, a high level of the law aspect of governance can reduce uncertainty and ambiguousness in conflict solving, strengthen information disclosure to mitigate information asymmetry, and attract foreign investors. Further, reducing uncertainty and ambiguity in conflict resolution can guarantee housing-related rights, such as access to public services in China, which boosts the desire to buy houses. Additionally, strengthening information disclosure enables homebuyers to obtain more loans, which, combined with foreign investment, ultimately increases demand for home ownership. Finally, these aspects can raise housing demand and then cause housing prices to rise. Based on the analysis, we propose hypothesis 1 as follows:

Hypothesis 1. Higher level of law-based governance is associated with higher housing prices, holding other things equal.

Nevertheless, if the public is not cognitively aware of the exact level of law-based governance, then the relationship between law-based governance and housing prices may not be strong. It is quite likely that there may exist a large gap between the public’s awareness of governance quality and researchers’ measurements of such quality. We thus explore the satisfaction level of the public with respect to law-based governance as it is based on the public’s perspective of the quality of law-based governance. Thus, we propose hypothesis 2 as follows:

Hypothesis 2. The more satisfied the public is with law-based governance, the greater the positive association between law-based governance and housing prices.

In addition, it is reasonable to expect that the relationship between law-based governance and housing prices could be very heterogeneous across city groups. For example, housing is much more expensive in first- and second-tier cities, which thus implies great asset value and requires a significant amount of financial credit; both investors and buyers in these cities are thus more sensitive to local law-based governance. On the contrary, investors and buyers of housing in small and less developed cities may give less attention to the quality of local law-based governance. Based on these arguments, hypothesis 3 is proposed as follows:

Hypothesis 3. The correlation between the law-based governance and housing prices is greater in the first- and second-tier cities.

4. Variables and Data

In this study, we are interested in how the law aspect of governance of one city is related to housing prices in that city. The housing price indicator uses the average annual price of new residential housing sold in a city, because there are is no reliable price data for second-hand housing unit sales for a large number of cities in China. A reliable measure of law-based governance is crucial for the credibility of the estimation results. While there is a large number of efforts measuring the degree of rule of law globally [

9,

65], few studies have attempted to assess the rule of law or law-based governance at the city level. In this paper, the data of city-level indicators of the quality of the law aspect of governance are collected from the Annual Assessment Report on China’s Law-based Government that issued by the School of Law-based Government, China University of Political Science and Law (CUPL) [

66]. Since 2014, the report has been successively released five times with annual assessment results for 100 cities, which include four major municipalities that are under the state’s direct administration, twenty-seven provincial capitals, twenty-three large cities (according to the category set by the State Council), and forty-six medium-sized cities. These cities have a good representation of the levels of law-based governance in China. The report’s assessment index system has nine first-level indicators, including “comprehensively performing government functions by law”, “organizational leadership”, “system construction”, “administrative decision”, “administrative law enforcement”, “government information disclosure”, “supervision and accountability”, “solving social conflicts and administrative disputes”, and “public satisfaction”, of local law-based administration. Due to its professionality and independence, the assessment report has earned a good reputation in Chinese society and is widely cited in the media as well as Chinese academic research [

66].

As “comprehensively performing government functions by law” has been placed at the most prominent position in the Implementation Outline for Constructing Law-based Government (2015–2020), we use the scores of this indicator in the assessment report to measure the quality of law-based governance. This core indicator is specified to capture the situation of administration by law including aspects of institution setting, leadership design, public services, administrative approval, emergency response, etc. [

66]. It has a full score of 100 in the annual assessment report, and the score can be expressed as:

where LAWGOV is the score of “comprehensively performing government functions by law”, IS denotes the score of “institution setting”, LD is the score of “leadership design”, PS is the score of “public services”, AA denotes the score of “administrative approval”, and ER is the score of “emergency response”.

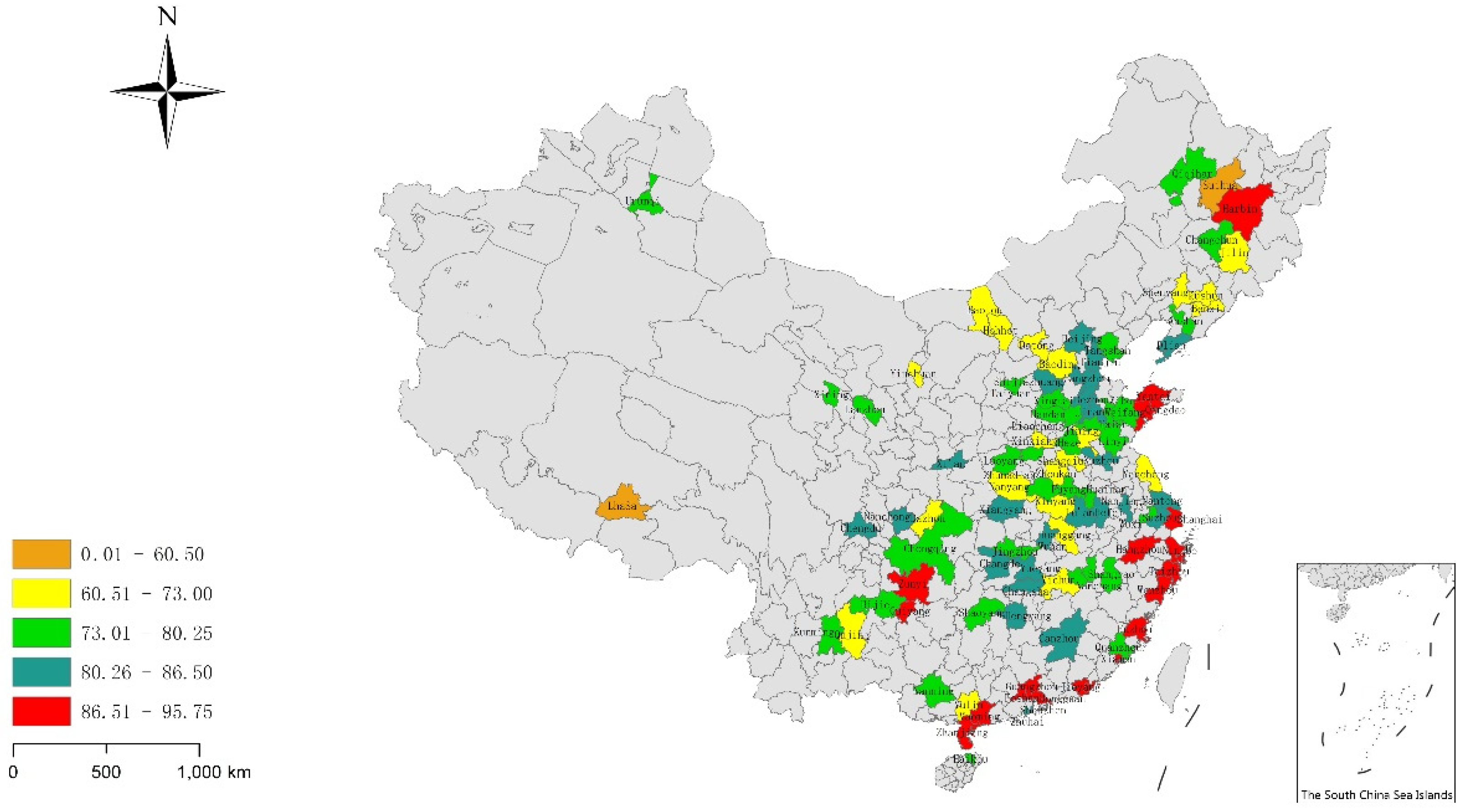

Figure 2 shows the spatial distribution of mean law-based governance quality between 2014 and 2017 across the sample cities. It can be seen that the cities falling into the highest quality category are mainly located in the eastern region of China. To ensure the robustness of our main findings, we also use the sum of the scores of other auxiliary aspects as an alternative indicator of law-based governance. Additionally, the two types of indicators (the core indicator and the mix of auxiliary indicators) enable us to describe the different law-based governance models well.

In addition to the law aspect of governance, many other factors may also affect city-level housing prices. Guided by findings of the existing literature, we select a large number of control variables that reflect the characteristics of the economic, humanistic, ecological, and geographic environment of cities. Two indicators are utilized to reflect the economic environment, including per capita disposable income of urban households and the ratio of tertiary industry’s output value in GDP. For the humanistic environment, we include eight indicators of traffic, educational, medical, and cultural facilities (details in

Table 1). Greenness ratio and the emission ratio of industrial soot and dust are used to reflect the ecological environment. Finally, we apply the distance to the coastline to capture the features of the geographic environment.

In addition, as discussed in

Section 2.4, law-based governance affects the housing market through the mediating variables of financial loans and foreign investment. We use per capita personal housing purchase loans from banks and non-bank financial institutions to reflect financial loans. The foreign investment indicator is per capita foreign investment. Additionally, per capita loans from housing provident funds are used as an alternative indicator of financial loans to check the robustness of their mediating role between housing prices and law-based governance. In accordance with the suggestions of [

67], to improve the estimation results, we incorporate economic regional submarket dummy variables into OLS equations, which can also alleviate the problem of heteroscedasticity [

68]. Meanwhile, to control for the time trend effect, we include the time dummy variables for each year.

The data of housing provident fund loans are collected from housing provident fund management centers in each city. The data of the distance to the coastline are calculated by ArcGIS software, which is the shortest straight-line distance from the geometric center of each city to the coastline. The data of city-level housing prices, mediating variables, and control variables are collected from the Bureau of Statistics of each city, the data of the RMB/USD exchange rate come from the People’s Bank of China. As the original unit of foreign investment is the dollar, we need to convert dollars to yuan using the exchange rate. The eastern, central, western, and northeastern economic regions are divided by the National Bureau of Statistics of China. The division of first-, second-, third-, fourth-, and fifth-tier cities is based on a research report from Shanghai YiCai Media Co., Ltd. (

https://www.yicai.com (accessed on 26 April 2021)). It issues the classification of Chinese cities every year based on the commercial store data of mainstream consumer brands, the user behavior data of internet companies, and urban big data. This type of classification changes the traditional classification of cities based on administrative hierarchy. China’s cities are classified according to five dimensional indices: business resource concentration, urban hub, urban activity, lifestyle diversity, and future plasticity, using expert scoring and principal component analysis. The data used in this study cover all the 100 cities in the report over the period 2014–2017 and take their natural logarithm forms in the analysis, except dummy variables.

Table 2 describes details of the variables and shows the descriptive statistics.

6. Conclusions

With the increasing role of law in governance [

75], there is a growing emphasis on law-based governance worldwide, and China expects to build itself into a socialist country with Chinese characteristics under the rule of law. In conventional terms, the rule of law necessarily has a positive correlation with the economic growth and the overall economic prosperity of any country [

76]. For example, law-based environmental governance boosts employment [

77]. Therefore, the pursuit of law-based governance is closely related to economic development, including the real estate market [

53]. Although some studies have noted that a certain law can have a significant impact on housing prices [

54], and the revised “Japanese Tenant Protection Law” affects housing rent [

78], there is still limited knowledge about how the rule of law and housing prices are related across cities in a given country. In the current context of China’s efforts to raise the quality of the law aspect of governance, a lack of awareness of such liaising mechanisms may not contribute maximally to economic development and may lead to less efficient regulation of possible rapid increases in housing prices. Our study bridges this cognitive gap by analyzing the ways in which the law aspect of governance is associated with housing prices, and the focus is the roles played by the factors of public satisfaction and socioeconomic groups.

This study finds that improving the quality of the law aspect of governance can enlarge loans, attract foreign investment, and then significantly raise housing prices. However, the relationship between the rule of law and housing prices is sensitive to public satisfaction. Additionally, considering the geographic and socioeconomic factors, the present paper shows that the correlation between the law aspect of governance and housing prices is greater in the first- and second-tier cities. These findings provide new insights into the pursuit of the rule of law with high quality in contemporary China.

In fact, China has made various efforts to raise the quality of the law aspect of governance in order to establish a socialist state under the rule of law. This pursuit in practice necessarily contributes to economic prosperity. Nevertheless, housing prices may increase additionally in the pursuit, which is an unwanted and concerning outcome for the government. Inspired by our findings, local governments could promulgate measures to reduce financial loans and foreign investment to curb the possible rapid rise in housing prices when improving the law aspect of governance quality, especially for emerging economies in the world.

{kind=link}

{kind=link}