1. Introduction

Consumption taxes have taken on a major role in terms of their contribution to public sector revenue. In the case of territories in Europe, this phenomenon has been accompanied by the emergence of new products that are supposed to replace those whose tax design is already developed. This is why policymakers are faced with the dilemma of whether to tax these new alternatives and, if so, how to proceed. This also affects land taxation for European tobacco crops. The consumption of certain products has been a crucial source of public revenue in recent years, with taxes on these products playing a significant role. However, the existence of new non-combustion alternatives (RRPs—Risk Reduced Products such as e-cigarettes, heated tobacco products, snus, and nicotine pouches) has prompted the need for an optimal land tax design protocol. This paper aims to establish such a protocol by conducting a theoretical analysis that considers three distinct aspects: the taxpayer profile, health risks, and previous experiences in other countries.

The main objective of this article is to establish a land tax protocol for the optimal design of taxation on products that generate negative externalities. The relative amount of harm produced by the consumption of each product is a fundamental variable to take into consideration. The negative impacts of these products on society, such as health risks or environmental harm, create a need for policy interventions, such as taxation (including land taxation), to nudge consumers toward better consumption patterns. In this context, the article aims to provide a framework for designing taxes that will be able to accomplish this objective while minimizing unintended consequences. Through this protocol, policymakers and researchers can create evidence-based tax policies that balance economic, social, and environmental considerations.

The global market for alternative risk-reduced tobacco products, such as e-cigarettes, heated tobacco products (HTPs), nicotine pouches, and snus, has been rapidly growing [

1,

2]. As these products are relatively new, there is a lack of consensus among policymakers on how to regulate them, particularly in terms of taxation. In some countries, e-cigarettes and HTPs are taxed at the same rate as traditional cigarettes, despite evidence suggesting that they are less harmful to health [

3,

4]. This lack of differentiation in taxation could discourage smokers from switching to these less harmful alternatives, ultimately hindering public health efforts to reduce the prevalence of smoking.

The main motivation for this article is to explore the benefits of differentiating taxation rates between traditional tobacco products and alternative products. By reviewing existing literature on the health effects of different tobacco products and their associated externalities, we aim to provide evidence-based recommendations for policymakers on how to design optimal taxation policies that promote the use of less harmful alternatives. Additionally, we will examine case studies from countries that have successfully implemented differentiated taxation policies to understand their impact on public health outcomes and revenue generation. Through this article, we hope to contribute to the ongoing policy debate on the regulation of alternative tobacco products and promote evidence-based policymaking in the public health domain.

With this work, we aim to suggest that before implementing price regulations or interventions to reduce traditional tobacco prevalence, policymakers should consider the taxpayer’s socio-economic profile and the risks produced by the specific products to their health. Additionally, the article highlights the potential benefits of harm reduction strategies that prioritize less harmful alternatives to smoking, such as vaping, HTPs, nicotine pouches, and so on. The authors suggest that taxation policies able to recognize the reduced harm of these alternatives can encourage smokers to switch to them, reducing the burden of smoking-related health problems. This is a challenge in Europe for fiscal policies.

In addition to addressing externalities, we recognize that tobacco taxation serves multiple objectives, each with its own unique significance. Beyond mitigating negative health externalities, governments utilize tobacco taxes to generate revenue, fund healthcare initiatives, and promote public health campaigns. Moreover, these taxes can act as a deterrent, aiming to reduce tobacco consumption and thereby improve overall public health. These distinct goals should impact the selection of tax mechanisms and the determination of tax rates. In this sense, we include a section that delves into these diverse objectives of tobacco taxation, shedding light on their interplay and influence on policy decisions.

This article will be structured in three distinct parts. The first focuses on a brief review of the literature and proposes an approach to the problem posed above. The second focuses on an overview of the negative externalities of consumption theory. Thirdly, an empirical approach to the optimal design of taxes is proposed. Finally, conclusions and suggestions for the future development of public policies are presented.

2. Brief Literature Review and General Background

Electronic cigarettes and other risk-reduced alternatives to tobacco have been on the rise in recent years. These products are often marketed as a safer alternative to traditional tobacco products, and as a result, they have become popular among both current tobacco users and some non-users. The latest Eurobarometer Report [

5], however, shows that e-cigarette initiation rates hover around 2.5%, while HTPs’ initiation is virtually non-existent. There is still much debate regarding the safety and efficacy of these products, and as such, it is important to consider the potential impact of taxes on their use.

As analyzed by the German Federal Institute for Risk Assessment (BfR), non-combustible products have been found to substantially reduce levels of major carcinogens in the emissions of analyzed heat-not-burn products with conventional tobacco cigarettes, thereby reducing the harmfulness of non-combustible products as compared to combustible products [

6]. Furthermore, the UK House of Commons Science and Technology Committee [

7] estimated e-cigarettes to be approx. 95% less harmful than conventional cigarettes, suggesting that both e-cigarettes and additional heat-not-burn products should be used as alternatives to conventional tobacco products.

As the consumption of tobacco has been linked to various health issues, many countries have implemented taxes as a tool for curbing its use. However, the use of alternatives to tobacco—such as electronic cigarettes or heated tobacco products—has become increasingly popular. This is an important (and factual) development to consider when creating the optimal tax design for these products. A tax design that must certainly focus on delivering positive health outcomes. This literature review aims to provide an overview of the research conducted on the optimal design of taxes for alternatives to tobacco.

Several studies have examined the optimal design of taxes for alternatives to combusted tobacco. One such study by ref. [

8] found that taxing RRPs at a lower rate than traditional tobacco products could be an effective way to reduce the use of the latter. This approach is based on the premise that RRPs are a safer alternative to traditional tobacco products and, as such, should be taxed at a lower rate to encourage their use. This idea is also stated in ref. [

9], promoting differential taxation between products based on product harmfulness. Therefore, the use of harm-reduced products in exchange for harmful combustible products is encouraged.

The optimal design of taxes for alternatives to tobacco is a challenge for fiscal policies across countries, and it requires the consideration of a variety of factors in the territory, including the potential harm of the product, the potential impact on public health, and the impact on consumers’ behavior. Research has shown that taxing e-cigarettes and other alternatives to combusted tobacco at a rate that is proportional to their harm could be an effective tool to reduce the use of more toxic products, incentivizing the substitution of harmful products with less damaging alternatives. Ultimately, the optimal design of taxes for alternatives to tobacco will depend on a variety of factors depending on the territory, among others, and further research is needed to fully understand the potential impact of different tax structures.

3. Tobacco Economy and Methodology

This section is divided into the following parts: tobacco cultivation and land taxes, tobacco competitive markets and negative externalities, and tax policies’ measures.

3.1. Tobacco and National Taxes

The cultivation and consumption of tobacco have long been intertwined with European societies, economies, and health systems. As European countries have sought to address tobacco’s economic and health-related challenges, taxation has emerged as a crucial policy instrument. This section aims to explore the relationship between tobacco cultivation taxation and the distribution of consumers in Europe, focusing on how variations in taxation policies influence consumer behaviors, market dynamics, and public health outcomes.

Tobacco cultivation taxation serves as a vital revenue source for many European countries while also acting to regulate tobacco consumption. By levying taxes on the cultivation of tobacco, governments can control the supply chain, influence the pricing of tobacco products, and potentially discourage consumption. However, the effectiveness of taxation policies depends on various factors, including the level of taxation, the presence of alternative tobacco and nicotine products, and the prevalence of illicit trade.

Consumer behavior plays a pivotal role in shaping the demand for tobacco and nicotine products. High tobacco cultivation taxes often lead to increased retail prices, which may deter some consumers from purchasing tobacco products. Consequently, this section examines how varying levels of taxation can influence smoking prevalence rates and patterns of tobacco use across different demographic groups. Analyzing consumer behavior in response to taxation is essential for understanding the potential impact of taxation policies on public health outcomes.

The distribution of tobacco consumers across Europe is not uniform, and taxation policies can contribute to regional disparities in tobacco consumption. Some countries may adopt more aggressive tobacco taxation strategies, resulting in reduced consumption rates, while neighboring countries with lower taxation levels might experience higher tobacco use. Taxation policies can inadvertently create opportunities for the illicit trade of tobacco products (

Table 1). When taxes lead to substantial price differences between neighboring countries, consumers may turn to illegal channels to acquire cheaper tobacco products.

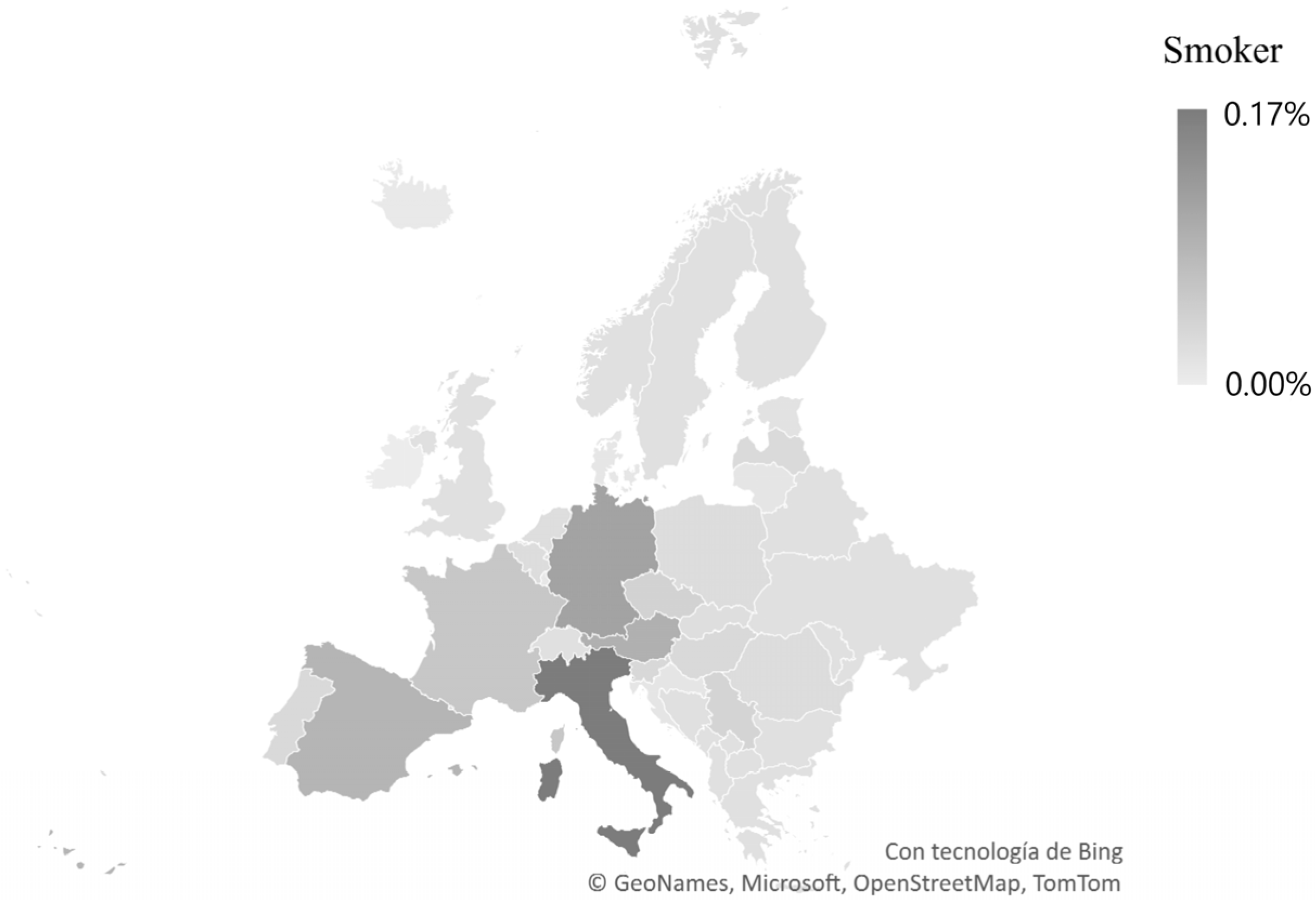

One significant factor contributing to differences in traditional combustible tobacco consumption across Europe lies in its rich history and diverse cultural influences. European countries have distinct tobacco-related traditions dating back centuries. For instance, Mediterranean countries such as Italy and Greece have a long-standing tradition of tobacco cultivation and consumption, often in the form of hand-rolled cigarettes and cigars. In contrast, Northern European nations may have adopted tobacco consumption at different points in history, with varying cultural norms and habits. These historical and cultural differences play a pivotal role in shaping tobacco consumption patterns, with preferences for specific tobacco products deeply embedded in regional identities. Another compelling reason behind the disparities in traditional tobacco consumption in Europe is the socioeconomic diversity among its member states. Countries within the European Union exhibit significant variations in income levels, education, and access to healthcare. Socioeconomic disparities can translate into varying rates of smoking prevalence. In some wealthier European nations, higher incomes and greater access to smoking cessation programs have contributed to lower smoking rates. Conversely, in less economically developed regions, where tobacco may be more affordable and fewer resources are allocated to anti-smoking initiatives, smoking rates tend to be higher. However, the situation is not so clear-cut. Some higher-income countries still show high prevalence rates (and high intensity of use) in adults, such as France and Germany. The simple differentiation between high- and low-income countries does not seem enough to explain the final results. Within-country income level disparities play an important role, too. These disparities highlight some of the complex interplays between economic factors and tobacco consumption behaviors

Figure 1.

Another different approach is the analysis of the percentage of daily smokers in Europe (

Figure 2). The analysis of the percentage of daily smokers in Europe is justified by its specific focus on individuals who maintain a higher and more regular level of tobacco consumption. This is relevant because daily smokers are at greater risk of experiencing the long-term adverse effects of tobacco compared to occasional smokers. Concentrating on this demographic group gives a more detailed understanding of the true burden of smoking in terms of public health. This information is crucial for designing effective public health policies and planning targeted interventions aimed at reducing tobacco consumption and, ultimately, mitigating the severe health consequences associated with smoking for the population.

3.2. Tobacco Competitive Markets and Their Failures

According to classical economic theory, the conditions for considering a market to be competitive are mainly four. First, the existence of many suppliers and demanders must be considered. Second, there must be perfect information, i.e., all market participants must have information about the risks and opportunities that arise. Thirdly, the product must be homogeneous and practically non-differentiable. Finally, there should be no barriers to market entry and exit.

However, despite the guidelines provided by theory, experts know that in practice, markets function in a much more complex way. This is what, in the end, has come to be classified as a market failure. These failures are classified into three types: externalities, imperfect or asymmetric information, public goods, and market power.

In this paper, we will focus on the study of externalities. Externalities are consumption, production, or investment decisions made by individuals, households, or firms that affect third parties that do not necessarily participate in the market. This market failure has indirect effects on the consumption and production opportunities of third parties who do not directly participate in these transactions. However, the price of the product taken into consideration does not reflect this impact. As will be discussed below, such effects may be positive (as in the case of education) or negative (as in the case of sugar, alcohol, and tobacco consumption).

3.3. Negative Externalities Tax Policies’ Measures

The specific case studied here, that of RRPs as a new alternative to traditional combusted tobacco consumption, can be understood as a change in the status of the externality of consumption. The direct health effects will not only affect those who use it but will also have a significant impact on third parties. The question, therefore, arises here: How to optimally correct the costs caused by a negative consumption externality?

The state generally deals with the reduction of the social cost associated with a negative externality of consumption through regulation, taxation, and the education of society. The first two measures are generally the most effective in the short term. However, the design of regulation and taxation is not a simple task. This is why policymakers make use of expert opinions and expertise in carrying out such a task.

Combusted tobacco consumption is widely regarded as a negative externality due to its harmful effects on smokers and non-smokers. According to ref. [

11], the negative health consequences associated with combusted tobacco use extend far beyond the individual smoker and can have significant impacts on broader society. This is because the smoke produced by the combustion of tobacco contains numerous harmful substances that can cause a wide range of health problems, including cancer, heart disease, and respiratory illnesses. Non-smokers who are exposed to second-hand smoke are also at risk of developing these health problems, creating a negative externality for individuals who have not chosen to smoke.

Furthermore, combusted tobacco consumption has a significant economic impact on society. According to a report by the World Health Organization [

12], the costs associated with combusted tobacco use are substantial and include both direct healthcare costs as well as indirect costs related to decreased productivity and increased absenteeism. These costs are borne by society rather than just by individual smokers, making combusted tobacco consumption a negative externality. The World Health Organization (WHO) report notes that the economic burden of combusted tobacco use is particularly high in low- and middle-income countries, where healthcare systems may be less equipped to handle the health consequences of smoking.

Among some of the main steps identified to achieve a good design of the taxes associated with the correction of an externality, we must highlight three: The determination of the risk in comparison with other consumption alternatives already subject to taxation; the knowledge of the taxpayer’s profile; and finally, the tax design.

4. The Empirical Approach

This part of the paper is divided into two sections. The first section presents the basic protocol for establishing and designing optimal consumption taxes for alternatives to traditional combustion tobacco in Spain. Secondly, we present a case where the introduction of new alternatives to traditional cigarettes—such as snus in Sweden—results in a decrease in the prevalence of traditional tobacco products and allows for savings in both health and cost terms. This best practice will therefore allow for obtaining the main guidelines for the design of public policies, both from the point of view of tax design and the needed deregulation of the less-damaging consumption alternatives.

4.1. The Design of Taxes in Spain

As we have observed in the previous section, in the European Union, the tax criteria for regulating new alternatives to traditional tobacco do not always follow a common pattern. However, a vast majority of countries in the EU similarly regulate new products, showing signals of pre-harmonization. Seventeen countries in the EU have opted for tax differentials of various magnitudes in favor of new alternatives. Some countries, such as Spain, have opted for non-regulation. In this section of the work, we will try to carry out a brief simulation of two of the steps that decision-makers ought to take in terms of taxation. To do this, we will take the case of Spain as an example.

If we had to follow the experience of other European countries in terms of regulation, Spain should be able to decide whether to regulate the market for alternative tobacco devices in the same way as the traditional ones or not. To do this, we must consider two fundamental steps. First, the characterization and differentiation of the taxpayer. We can do so by observing their differences in personal and socioeconomic characteristics. Secondly, once the profile of the consumption-related taxpayer is known, we must analyze the risks for the health system. We do so both in terms of health-related spending and in terms of the health of individuals.

In this microsimulation, we will use a simple econometric methodology rather than offering a solid empirical strategy. This seems to the authors to be the best method to face the research question of this study. Furthermore, we will present a study protocol before moving forward with the material design of the tax.

Brief Methodological Note

As a starting point, it should be considered that the database used in this study is the European Health Interview Survey [

10]. Thanks to its 22,000 observations, it allows us to identify which Spanish citizens among these are traditional (combusted) tobacco consumers and which, instead, have opted for new non-combustion alternatives. In other words, specifically, RRP consumers.

To approach the design of a possible tax, we must first understand the taxpayer’s profile and then consider the risks related to the consumption of the good taken into consideration. To know the taxpayer’s profile, we will carry out the elaboration of two probit models, which will indicate the probability of a. being in the group of consumers of RRPs or b. being in the group of traditional (combusted) tobacco products. This elaboration is based on a set of explanatory variables (personal and socioeconomic). The mathematical form applied to the model is the following:

Here, the variable takes the value 1 if the individual is consuming RRPs and takes the value 0 if not. represents the probability in marginal terms that, given a defined explanatory variable , the individual does or does not belong to the group of RRP users. Firstly, as we have pointed out, represents the set of variables of which we want to discover the incidence in terms of the probability that the individual is part of one or the other group. Secondly, is the error term of the estimated model. In the case of , the only difference is that this variable takes the value of 1 if the individual claims to be a smoker of traditional combusted tobacco or not.

On the other hand, to know the risks, we use two different types of econometric approximations. First, to estimate the effect on the use of health services by vapers or traditional tobacco smokers, we carry out a negative binomial regression model (recommended in health economics for these cases).

This model is used because, on many occasions—as is the case with our data, too—there is a problem of over-dispersion, determined by the possible existence of negative values in the prediction of the dependent variable, in which case the use of the OLS model is not recommended. This negative binomial regression model, or Poisson model, is frequently used in cases such as the one in this paper [

13].

Finally, beyond the social cost and to define the risks to the individual’s health, we elaborate a second round of probit probabilistic regression models that allow us to discover through their marginal effects the probability of suffering from some of the diseases commonly associated with the consumption of this type of substance. These will use the mathematical expression:

where

represents the variable that dichotomously indicates (taking values 1 or 0) whether or not you suffer from the condition; and

represents the type of product you use, i.e., vapers (which is our proxy for all non-combustion alternatives) or smokers of traditional combusted tobacco (also using values 0 or 1 depending on whether or not you use the product).

The objective is to find out , i.e., the effect of the type of consumption on the probability of suffering from the disease.

4.2. Empirical Approach

Once the data and the methodology to be applied are known, first we are going to know the differences, if any, between the groups of “vapers” and “smokers” through the analysis of the results of the probits. As we can see in

Table 1, in the case of vaper consumers, it is observed that their consumption significantly decreases with age. Most of the “vapers” will be comparatively (relatively) younger. Once again, it is important to underline that we use “vapers” as a proxy for all new alternative products. Observing the market penetration of the different products in Spain, this result seems consistent with reality.

Empirically, according to ref. [

14], Spanish combustible smoking prevalence was reported to be highest in the age group 25–34 years, amounting to 30.9%. In general, combustible smoking prevalence rates were reported to be highest among younger consumer groups and higher among men as opposed to women [

15]. Furthermore, combustible smoking prevalence was reported to be highest among less-educated consumer groups and lower-income consumer groups. These reported figures are consistent with the figures in

Table 1, showing that the likeliness to consume combustible tobacco increases for younger consumer groups while decreasing for older consumer groups.

Furthermore, the Spanish government reports switching from combustible products towards RRPs being observable among older consumer groups, not younger consumer groups. The share of older consumers having switched from combustible products towards RRPs was reported at 62.4%, whereas the share of younger consumer groups was reported at only 33.8% [

15]. These findings match the results in

Table 2, as RRPs consumption seems mainly appealing to older consumer groups.

On the one hand, it is easy to notice a higher penetration of e-cigarettes in the Spanish market, which seems to have a larger appeal among the younger cohorts. On the other hand, anecdotal data seems to suggest that HTPs are usually consumed by older groups and have a very small market share in the country. Finally, nicotine pouches are virtually non-existent, and snus is banned.

Given this market reality, we can draw a natural relationship with income. As this is higher, the probability of being part of the group “vaping” decreases significantly. Conversely, you are more likely to be part of the group “vaper” as your educational level increases.

If we compare it with smokers of traditional combusted tobacco, we also observe a decrease with age. Likewise, it seems that the fact of being an immigrant decreases the probability of being part of the group “vaper”. An increase in income has the same effect. However, a significant difference from “vapers” is related to the educational level. In the case of traditional tobacco smokers, as the educational level increases, the probability of belonging to this group decreases. The opposite is true in the case of “vapers”. In other words, the higher the education level, the higher the probability of being in the group of “vapers”.

Therefore, given the market reality of Spain, we can conclude that the profile of the taxpayer is that of a relatively younger consumer with low income and a relatively higher education level (above the elementary level). This data is meaningful enough so that, when combined with the risk analysis that we will carry out below, it clearly indicates the direction that tax regulation should take.

Once the approximation of the profile of the vaper has been carried out—and considering the taxpayer characteristics—we must now focus on the differences between the traditional smoker of combusted tobacco and the consumer of new alternatives. For this, we have estimated the results obtained in

Table 3. It shows the effects of being part of the group “vaper” on the use of health services. Thus, we can estimate the risk in terms of health spending. As a result, those who decide to consume RRPs do not have significant results in terms of increased use of general practitioner or specialist health services. However, they do seem to visit the hospital less frequently than the consumers of combusted tobacco products (this variable is measured as the number of nights that the subject remains hospitalized).

Regarding patterns of consumption of health services, we are unable to obtain significant conclusions. The same issue occurs in the case of consumers of traditional combustion tobacco.

Let us now look at the individual health risks, which, indirectly, also play an important role in increasing health spending.

Table 2 shows clear and significant differences between those who consume vaping and those who consume traditional combustion tobacco.

For this part of the work, we are going to use three of the most important diseases related to tobacco consumption as dependent variables. In the first place, bronchitis. Evidence shows that the consumption of traditional combusted tobacco increases the marginal probability of suffering from it. However, this is not the case for the group “vapers”, where the effect is not significant. In the case of suffering from coronary and oral diseases, the same pattern seen for bronchitis is repeated.

That is why these latest models yield a much more significant result on the risks and, therefore, will be more useful to obtain our conclusions (

Table 4).

4.3. Health Risk and Cost in Sweden

Snus, a form of smokeless tobacco, has been widely used in Sweden for several decades. Despite being a form of tobacco, snus has been associated with lower health risks compared to smoking, leading to it being perceived as a safer alternative to smoking. The use of snus has been credited with the declining tobacco prevalence rates in Sweden.

4.3.1. A Brief Review of Previous Literature about Snus

The use of snus as a harm reduction alternative to smoking has been a topic of interest in the scientific literature for several decades. [

16] conducted a study to assess the impact of snus use on smoking prevalence in Sweden, where snus has been widely used as an alternative to smoking since the 1970s. The study found that the use of snus was associated with a significant reduction in smoking prevalence, particularly among men. The authors suggested that the availability of a less harmful alternative to smoking, like snus, may have contributed to the decline in smoking prevalence in Sweden.

In 2016, ref. [

17] conducted a similar study in Sweden to assess the impact of snus use on smoking prevalence over time. The study found that snus use had contributed significantly to the decline in smoking prevalence in Sweden since the 1970s. The authors suggested that the widespread availability and acceptance of snus as a less harmful alternative to smoking had played a crucial role in reducing the prevalence of smoking in Sweden.

The findings of these studies suggest that the availability of harm reduction alternatives like snus can contribute to a reduction in smoking prevalence. Careful regulation and education are necessary to ensure that the benefits of snus as a harm reduction tool are maximized while its potential risks are minimized.

Overall, these studies highlight the potential benefits of harm reduction strategies that prioritize less harmful alternatives to smoking, like snus. Further research is needed to better understand its potential role in reducing smoking prevalence in other countries.

4.3.2. The Impact of Snus on Smoking Prevalence in Sweden

As discussed above, tobacco prevalence drops substantially when legislation is introduced in favor of alternatives, in this case, snus. For the analysis of the impact of snus use, we will follow two steps.

First, we will take into consideration the calculation of actual and hypothetical cases of disease and death. For this, we will consider data provided by [

18,

19]. This data provides us with information on smoking and snus in terms of prevalence and their relation to some reference diseases such as lung cancer, ischemic heart disease (IHD), chronic obstructive pulmonary disease (COPD), and stroke. Secondly, for this analysis, we will consider the impact in terms of health costs, differentiating between the following direct costs: those related to all services associated with illnesses, treatment costs, hospitalization and medicalization costs, and indirect costs related to productivity losses: costs for morbidity, early retirement, and premature mortality.

4.3.3. Actual and Hypothetical Health Risks

For the calculation, we will essentially start with two different assumptions. The first assumption will answer the following question: How many people would be smoking in Sweden in 2019 if they had not switched to snus and remained cigarette smokers—assuming an EU average prevalence in Sweden? The second assumption will try to explain the differences between snus users and smokers in terms of the risk of suffering from any of the four smoking-related diseases.

To answer the first question, we must assume two scenarios: scenario A and scenario B. To graphically observe the results, let us look at the following

Table 5.

Regarding the second assumption, the one related to the probability of suffering from the four reference diseases, we can say that, according to [

20], the risk for snus is lower for lung cancer and IHD. In the case of COPD and stroke, the risk of snus is also lower than that of traditional combusted tobacco (cigarettes, rolls of your own), as indicated by ref. [

21]. Once the above two premises have been established, the scheme for the analysis of the risk calculation of suffering from a disease (or dying from it) follows

Table 6:

Therefore, we can conclude that if snus had not been introduced and snus users were cigarette smokers, the risk of having one of the four diseases would have been much higher for them, increasing the number of disease cases.

4.3.4. Actual and Hypothetical Health Costs

The second step, as described at the beginning of this section, concerns a rough calculation of the associated costs. Thus, according to the methodology used by ref. [

21], we will estimate the direct and indirect costs following the same scenario scheme as in the previous section (

Table 7).

For the analysis of the indirect costs associated with lost productivity, three different variables will be used:

- -

The number of years a patient suffers from a disease is referred to in health economics as years lived with disability (YLDs).

- -

The number of individuals inactive at work because of suffering from a disease multiplied by the smoking-related shares of YLDs from COPD, IHD, lung cancer, and stroke.

- -

Labor costs are measured by the average labor cost per year combined with smoking-related incapacity to measure productivity loss due to retirement and permanent incapacity.

Although there are several approaches to the calculation, such as the willingness-to-pay approach introduced by ref. [

24], for our study, we will use the human capital approach, considered by ref. [

25], which considers the number of smoking-related deaths per age group multiplied by the present value of lifetime earnings and yields the following results (

Table 8):

As we can see, the differences in the first case, i.e., among cigarette smokers, are about 2.51 bn Euro, while, on the other hand, among the total population, the costs would increase by 1.70 bn Euro. Based on this approximation of the calculation, if snus had not been introduced, the costs for the total population would have increased by 28.76%. The same would occur if we were to analyze the indirect costs with this same approximation. The results show that the loss of productivity associated with morbidity would be 48% higher if snus had not been introduced. The loss associated with premature mortality would be around 45% higher.

These calculations seem to suggest that the introduction of snus has been crucial for the reduction of tobacco consumption in Sweden, generating significant savings in terms of direct and indirect costs and, most importantly, a reduction in the risk of contracting diseases such as lung cancer, COPD, IHD, and stroke.

The case of Sweden should also have a relevant impact when analyzing the prevalence and trends of traditional tobacco consumption. The learnings from the North give some important signals to policymakers when redesigning fiscal policies related to the taxation of these types of products.

In conclusion, the use of snus has significantly contributed to the declining combusted tobacco prevalence rates in Sweden. The perception of snus as a safer alternative to smoking, its social acceptability, availability, affordability, and the reduction in smoking initiation rates among young people are factors that have contributed to this trend. Further research is needed to better understand the potential impact on tobacco prevalence rates in other countries, but the Swedish case seems too strong of an example to overlook.

5. Conclusions

This paper aims to establish a basic protocol for the optimal design of taxes in the European territories on products whose consumption represents a negative externality. However, to do so, we believe it is appropriate to highlight three elementary design stages. The first of these is related to the taxpayer’s socio-economic profile. The second is the knowledge of the risk involved in terms of expenditure for the system and, finally, the determination of the health risk of the individual who consumes it.

From the case study presented for Spain, we can derive some of the necessary signals for the design of this kind of taxation. This should be extrapolated to many other countries. On the one hand, it can be observed that the profile of consumers of non-combustion alternatives to traditional tobacco, such as the ones being part of the over-comprehensive group of “vapers” in our case, are young individuals with medium and low income levels. Observing the market penetration of the different products in Spain, this result seems consistent with reality. On the one hand, it is easy to notice a higher penetration of e-cigarettes in the Spanish market, which seems to have a larger appeal among the younger cohorts. On the other hand, anecdotal data seems to suggest that HTPs are usually consumed by older groups and have a very small market share in the country. Finally, nicotine pouches are virtually non-existent, and snus is banned. We can also conclude that “vapers” have lower individual health risks than those who opt for combusted tobacco, although no significant differences have been found in terms of contribution to overall public expenditure yet.

Based on previous literature, RRPs are a less harmful alternative to traditional tobacco smoking. Non-combustible products do not contain tar, which is a major contributor to the health risks associated with smoking. They produce significantly fewer harmful chemicals than traditional cigarettes. Additionally, research suggests that non-combustible products are an effective tool for smokers who wish to quit tobacco smoking.

Given these facts, governments must implement taxation policies that reflect the reduced harm of RRPs compared to combusted tobacco. Imposing lower taxes on RRPs than on combusted tobacco will incentivize smokers to switch to less-damaging products, which would ultimately lead to a positive health outcome for both individuals and society. In countries such as the UK, the House of Commons, or in Germany, the government institution (BfR), has acknowledged the potential entailed in harm-reduced products to reduce health care costs.

Moving in the opposite direction could also lead to an increase in the black market for RRPs, creating additional health and safety risks for consumers.

Additionally, analyzing the experiences of Sweden, we discover that the use of snus has significantly contributed to the reduction in the prevalence of traditional tobacco smoking in the country. Snus is a smokeless tobacco product that is less harmful than traditional cigarettes, and its use has been widely accepted in Swedish society for decades. By promoting snus as a less harmful alternative to smoking, the Swedish government has been able to nudge consumers away from combusted tobacco products, reducing the prevalence of smoking and the associated health risks. The success of snus in Sweden highlights the potential benefits of harm reduction strategies that prioritize less harmful alternatives to smoking. However, it is important to note that the use of snus is not risk-free and can lead to various health issues. Therefore, careful regulation and education are necessary to ensure that the benefits of snus as a harm reduction tool are maximized while its potential risks are minimized. The production of Snus, which requires less tobacco than traditional tobacco products, can have a positive impact on reducing the demand for tobacco cultivation and, consequently, freeing up land for other purposes. This could lead to greater crop diversification, which in turn would help alleviate pressure on water resources since other crops may require less water compared to vast tobacco fields. Furthermore, by encouraging the adoption of other flavoring substances that require less water and resources for production, we can strengthen the agricultural economy by diversifying options for farmers and promoting more sustainable agriculture practices. It is essential to highlight that the focus on the development and promotion of Snus and other flavoring substances should go hand in hand with education and awareness campaigns, informing the public about their benefits and risks while ensuring strict compliance with regulations to safeguard consumers’ health and well-being. Promoting responsible production of snus and other flavoring alternatives is a valuable and promising proposal to reduce tobacco cultivation, preserve natural resources, and enhance agricultural sustainability. Together, we can progress towards a more balanced and healthier future for our planet and future generations.

As main suggestions for policymakers, this article suggests that, before making hasty decisions to reduce the prevalence of traditional combusted tobacco through price regulation or intervention, other academic criteria related to the optimal design of taxation of tobacco and its alternatives should be considered. To this end, the profile of the taxpayer and the risks to his or her health should be considered, avoiding a shift in consumption towards illicit or low-quality products that may be purchased in unregulated secondary markets.

Then, the available evidence supports the implementation of taxation policies that favor harm reduction alternatives like RRPs and snus while discouraging the use of traditional (combusted) tobacco products. RRPs are less harmful alternatives to smoking, and taxation policies that recognize their reduced harm can encourage smokers to switch to these products and reduce the burden of smoking-related health problems.

Higher taxes on traditional tobacco products can discourage their use and reduce the prevalence of smoking, which is the leading cause of preventable death and disease worldwide. Moreover, high taxes on traditional, combusted tobacco products can generate substantial revenue for governments that can be used to fund healthcare programs and tobacco control initiatives. All kinds of combusted tobacco products (cigarettes, roll-your-own, cigars) should be subjected to a relevant increase in their taxation levels to improve both public health and public accounts.

Spain should follow the example of many European countries, which have moved toward a fully specific tax, offering a relevant differential in favor of less-damaging products. In doing so, policymakers will be implementing tax policies that prioritize harm reduction alternatives like RRPs while strongly discouraging the use of traditional tobacco products. Such policies can help reduce the prevalence of smoking and improve public health outcomes while generating increased revenue for public health programs.

{kind=link}

{kind=link}