Adoption Intention of Fintech Services for Bank Users: An Empirical Examination with an Extended Technology Acceptance Model

Abstract

:1. Introduction

- Most existing research mainly studies the application model from the supply side of Fintech services to improve the efficiency and user experience of banks—that is to say, scholars’ concern about how and what kind of Fintech services are provided. Even if someone studies the adoption problems, they focus on a specific Fintech service, such as mobile banking or internet banking service, but the existing research rarely pays attention to a more empirical extension of previous studies in TAM applied in Fintech from the demand side.

- This paper comprehensively and concretely analyzes the influencing factors and their relationship with the adoption of Fintech services, and it extends the applicability of traditional TAM models as we consider more factors influencing the users’ adoption.

- The research results provide valuable information for the adjustment of bank marketing strategies and the implementation of strategic goals. How to change users’ behavioral intentions through the adjustment of influencing factors when providing users with financial and technological products is of great significance for the development of banks in the digital age.

2. Literature Review and Conceptual Framework

2.1. Fintech

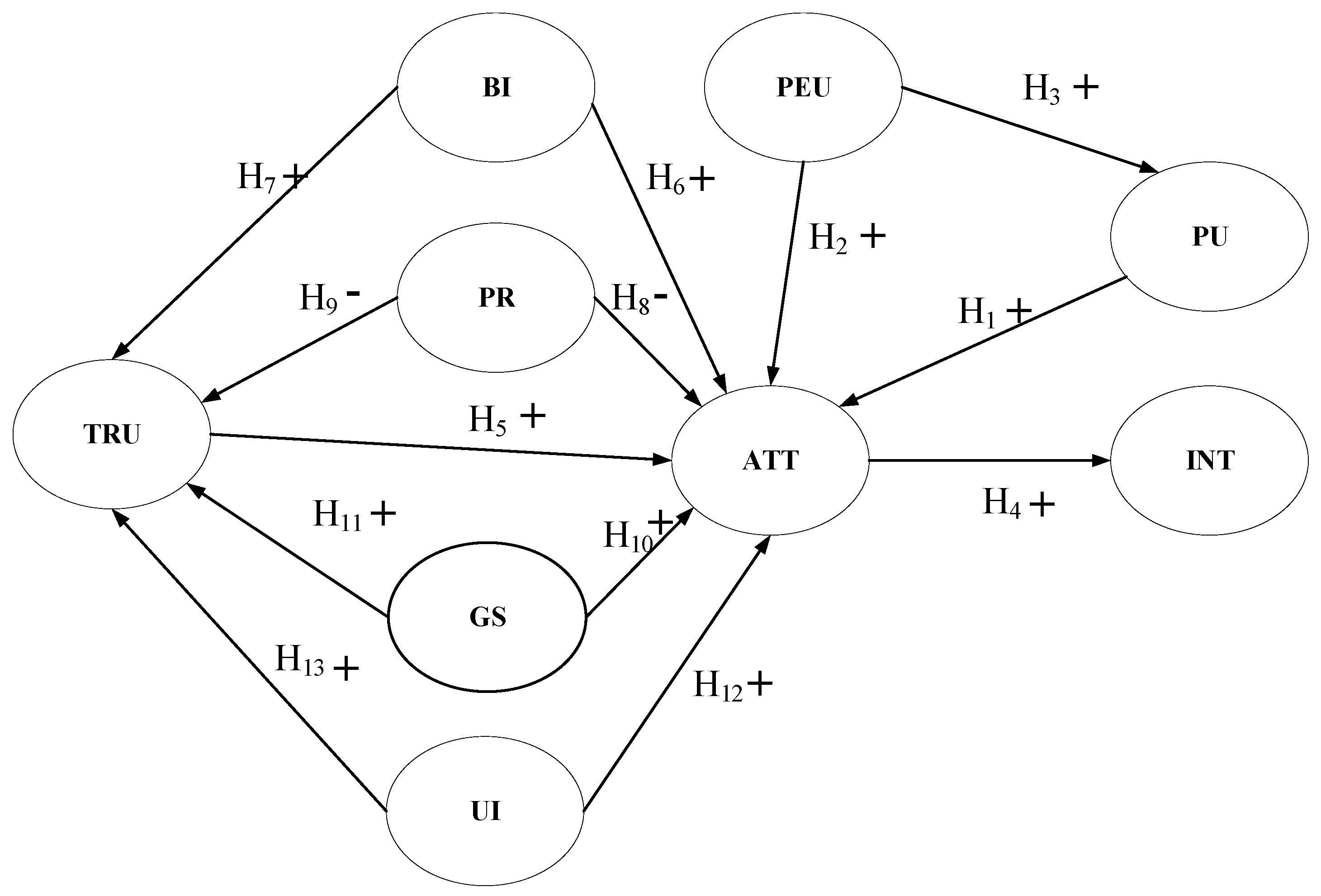

2.2. Hypotheses Development for the Proposed Model

2.2.1. Perceived Usefulness

2.2.2. Perceived Ease of Use

2.2.3. Attitudes

2.2.4. Trust

2.2.5. Brand Image

2.2.6. Perceived Risk

2.2.7. Government Support

2.2.8. User Innovativeness

3. Methodology

3.1. Data Collection

3.2. Instrument Development

4. Results

4.1. Scale Validity and Reliability

4.2. Structural Equation Model: Hypotheses Testing

5. Discussion and Conclusions

6. Limitations and Future Directions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Gabor, D.; Brooks, S. The Digital Revolution in Financial Inclusion: International Development in the Fintech Era. New Polit. Econ. 2017, 22, 1–14. [Google Scholar] [CrossRef]

- Leong, C.; Tan, B.; Xiao, X.; Tan, F.T.C.; Sun, Y. Nurturing a Fintech Ecosystem: The Case of a Youth Microloan Startup in China. Int. J. Inf. Manag. 2017, 37, 92–97. [Google Scholar] [CrossRef]

- Alt, R.; Beck, R.; Smits, M.T. Fintech and the Transformation of the Financial Industry. Electron. Mark. 2018, 28, 235–243. [Google Scholar] [CrossRef]

- Zavolokina, L.; Dolata, M.; Schwabe, G. The Fintech Phenomenon: Antecedents of Financial Innovation Perceived by the Popular Press. Financ. Innov. 2016, 2, 16. [Google Scholar] [CrossRef]

- Chang, Y.; Wong, S.; Lee, H.; Jeong, S. What Motivates Chinese Consumers to Adopt Fintech Services: A Regulatory Focus Theory; ACM: New York, NY, USA, 2016. [Google Scholar]

- Priem, R.L.; Li, S.; Carr, J.C. Insights and new directions from demand-side approaches to technology innovation, entrepreneurship, and strategic management research. J. Manag. 2012, 38, 346–374. [Google Scholar] [CrossRef]

- Priem, R.L.; Swink, M. A demand-side perspective on supply chain management. J. Supply Chain Manag. 2012, 48, 7–13. [Google Scholar] [CrossRef]

- Hermes, N.; Lensink, R. Does Financial Liberalization Influence Saving, Investment and Economic Growth? Evidence from 25 Emerging Market Economies, 1973; Palgrave Macmillan: Basingstoke, UK, 2008; pp. 47–57. [Google Scholar]

- Nakashima, T. Creating Credit by Making Use of Mobility with Fintech and IoT. IATSS Res. 2018, 42, 61–66. [Google Scholar] [CrossRef]

- Gai, K.; Qiu, M.; Sun, X. A Survey on Fintech. J. Netw. Comput. Appl. 2018, 103, 262–273. [Google Scholar] [CrossRef]

- Yin, H.; Gai, K. An Empirical Study on Preprocessing High-Dimensional Class-Imbalanced Data for Classification. In Proceedings of the IEEE International Conference on High PERFORMANCE Computing and Communications, New York, NY, USA, 24–26 August 2015. [Google Scholar]

- Gai, K.; Qiu, M.; Zhao, H. Energy-Aware Task Assignment for Mobile Cyber-Enabled Applications in Heterogeneous Cloud Computing. J. Parallel Distrib. Comput. 2017, 111, 25–38. [Google Scholar] [CrossRef]

- Cuomo, S.; Somma, V.D.; Sica, F. An Application of the One-Factor Hullwhite Model in an Iot Financial Scenario. Sustain. Cities Soc. 2018, 38, 18–20. [Google Scholar] [CrossRef]

- Mishra, S. Financial Management and Forecasting Using Business Intelligence and Big Data Analytic Tools. Int. J. Financ. Eng. 2018, 6, 10–31. [Google Scholar] [CrossRef]

- Du, W.D.; Pan, S.L.; Leidner, D.E.; Ying, W. Affordances, Experimentation and Actualization of Fintech: A Blockchain Implementation Study. J. Strateg. Inf. Syst. 2018. [Google Scholar] [CrossRef]

- Buckley, R.; Arner, D.; Barberis, J. The Evolution of Fintech: A New Post-Crisis Paradigm? Soc. Sci. Electron. Publ. 2015, 47, 1271–1319. [Google Scholar]

- Davis, F.D. A Technology Acceptance Model for Empirically Testing New End-User Information Systems: Theory and Results. Ph.D. Thesis, Massachusetts Institute of Technology, Cambridge, MA, USA, 1986. [Google Scholar]

- Venkatesh, V.; Bala, H. Technology Acceptance Model 3 and a Research Agenda on Interventions. Decis. Sci. 2010, 39, 273–315. [Google Scholar] [CrossRef]

- Zhang, T.; Lu, C.; Kizildag, M. Banking “On-the-Go”: Examining Consumers’ Adoption of Mobile Banking Services. Int. J. Qual. Serv. Sci. 2018, 10, 279–295. [Google Scholar] [CrossRef]

- Stewart, H.; Jürjens, J. Data Security and Consumer Trust in Fintech Innovation in Germany. Inf. Comput. Secur. 2018, 26, 109–128. [Google Scholar] [CrossRef]

- Ryu, H. What Makes Users Willing or Hesitant to Use Fintech?: The Moderating Effect of User Type. Ind. Manag. Data Syst. 2018, 118, 541–569. [Google Scholar] [CrossRef]

- Ng, A.W.; Kwok, B.K.B. Emergence of Fintech and Cybersecurity in a Global Financial Centre: Strategic Approach by a Regulator. J. Financ. Regul. Compliance 2017, 25, 422–434. [Google Scholar] [CrossRef]

- Barakat, A.; Hussainey, K. Bank Governance, Regulation, Supervision, and Risk Reporting: Evidence from Operational Risk Disclosures in European Banks. Int. Rev. Financ. Anal. 2013, 30, 254–273. [Google Scholar] [CrossRef]

- Featherman, M.S.; Pavlou, P.A. Predicting E-Services Adoption: A Perceived Risk Facets Perspective. Int. J. Hum. -Comput. Stud. 2003, 59, 451–474. [Google Scholar] [CrossRef]

- Hong, W.; Zhu, K. Migrating to Internet-Based E-Commerce: Factors Affecting E-Commerce Adoption and Migration at the Firm Level. Inf. Manag. 2006, 43, 204–221. [Google Scholar] [CrossRef]

- Chang, Y.; Wong, S.F.; Lee, H.; Jeong, S.P. What Motivates Chinese Consumers to Adopt Fintech Services: A Regulatory Focus Theory. In Proceedings of the International Conference on Electronic Commerce: E-Commerce in Smart Connected World, Suwon, Korea, 17–19 August 2016. [Google Scholar]

- Carlin, B.; Olafsson, A.; Pagel, M. Technology Adoption across Generations: Financial Fitness in the Information Age; Working Paper Series; National Bureau of Economic Research: Cambridge, UK, 2017. [Google Scholar]

- Chau, V.S.; Ngai, L.W.L.C. The Youth Market for Internet Banking Services: Perceptions, Attitude and Behaviour. J. Serv. Mark. 2013, 39, 42–60. [Google Scholar]

- Abbad, M.M. E-Banking in Jordan. Behav. Inf. Technol. 2013, 32, 681–694. [Google Scholar] [CrossRef]

- Akturan, U.; Tezcan, N. Mobile Banking Adoption of the Youth Market. Mark. Intell. Plan. 2012, 30, 444–459. [Google Scholar] [CrossRef]

- Szopiński, T.S. Factors Affecting the Adoption of Online Banking in Poland. J. Bus. Res. 2016, 69, 4763–4768. [Google Scholar] [CrossRef]

- Riquelme, H.E.; Rios, R.E. The Moderating Effect of Gender in the Adoption of Mobile Banking. Int. J. Bank Mark. 2010, 28, 328–341. [Google Scholar] [CrossRef]

- Taylor, S.; Todd, P.A. Understanding Information Technology Usage: A Test of Competing Models. Inf. Syst. Res. 1995, 6, 144–176. [Google Scholar] [CrossRef]

- Zhao, A.L.; Koenig-Lewis, N.; Hammer-Lloyd, S.; Ward, P. Adoption of Internet Banking Services in China: Is It All About Trust? Int. J. Bank Mark. 2010, 28, 26. [Google Scholar]

- Gupta, A.; Arora, N. Consumer Adoption of M-Banking: A Behavioral Reasoning Theory Perspective. Int. J. Bank Mark. 2017, 35, 733–747. [Google Scholar] [CrossRef]

- Shaikh, A.A.; Karjaluoto, H. Mobile Banking Adoption: A Literature Review. Telemat. Inform. 2015, 32, 129–142. [Google Scholar] [CrossRef]

- Hsu, C.L.; Wang, C.F.; Lin, J.C.C. Investigating Customer Adoption Behaviours in Mobile Financial Services. Int. J. Mob. Commun. 2011, 9, 477–494. [Google Scholar] [CrossRef]

- Aboelmaged, M.G.; Gebba, T.R. Mobile Banking Adoption: An Examination of Technology Acceptance Model and Theory of Planned Behavior. Int. J. Bus. Res. Dev. 2013, 2, 35–50. [Google Scholar] [CrossRef]

- Mcknight, D.H.; Chervany, N.L. What Trust Means in E-Commerce Customer Relationships: An Interdisciplinary Conceptual Typology. Int. J. Electron. Commer. 2001, 6, 35–59. [Google Scholar] [CrossRef]

- Lewis, J.D.; Weigert, A. Trust as a Social Reality. Soc. Forces 1985, 63, 967–985. [Google Scholar] [CrossRef]

- Lee, M.K.O.; Turban, E. A Trust Model for Consumer Internet Shopping. Int. J. Electron. Commer. 2001, 6, 75–91. [Google Scholar] [CrossRef]

- Kesharwani, A.; Singh Bisht, S. The Impact of Trust and Perceived Risk on Internet Banking Adoption in India. Int. J. Bank Mark. 2012, 30, 303–322. [Google Scholar] [CrossRef]

- Malaquias, R.F.; Hwang, Y. An Empirical Study on Trust in Mobile Banking: A Developing Country Perspective. Comput. Hum. Behav. 2016, 54, 453–461. [Google Scholar] [CrossRef]

- Koksal, M.H. The Intentions of Lebanese Consumers to Adopt Mobile Banking. Int. J. Bank Mark. 2016, 34, 327–346. [Google Scholar] [CrossRef]

- Basak, S.K.; Govender, D.W.; Govender, I. Examining the Impact of Privacy, Security, and Trust on the Tam and Ttf Models for E-Commerce Consumers: A Pilot Study. In Proceedings of the 14th Annual Conference on Privacy, Security and Trust (PST), Auckland, New Zealand, 12–14 December 2016. [Google Scholar]

- Hanafizadeh, P.; Behboudi, M.; Abedini Koshksaray, A. Mobile-Banking Adoption by Iranian Bank Clients. Telemat. Inform. 2014, 31, 62–78. [Google Scholar] [CrossRef]

- Park, E.; Kim, H.; Ohm, J.Y. Understanding Driver Adoption of Car Navigation Systems Using the Extended Technology Acceptance Model. Behav. Inf. Technol. 2015, 34, 741–751. [Google Scholar] [CrossRef]

- Sang, S.; Lee, J.D.; Lee, J. E-Government Adoption in Cambodia: A Partial Least Squares Approach. Transform. Gov. People Process Policy 2010, 4, 138–157. [Google Scholar] [CrossRef]

- Riyadh, A.N.; Bunker, D.; Rabhi, F. Barriers to E-Finance Adoption in Small and Medium Sized Enterprises (Smes) in Bangladesh. In Proceedings of the 5th Conference on Qualitative Research in IT, Brisbane, Australia, 17 November 2010. [Google Scholar]

- Shapiro, S.L.; Reams, L.; So, K.K.F. Is It Worth the Price? The Role of Perceived Financial Risk, Identification, and Perceived Value in Purchasing Pay-Per-View Broadcasts of Combat Sports. Sport Manag. Rev. 2018. [Google Scholar] [CrossRef]

- Saleem, Z.; Rashid, K. Relationship between Customer Satisfaction and Mobile Banking Adoption in Pakistan. Int. J. Trade Econ. Financ. 2014, 2, 537–543. [Google Scholar] [CrossRef]

- Srivastava, S.C.; Chandra, S.; Theng, Y.L. Evaluating the Role of Trust in Consumer Adoption of Mobile Payment Systems: An Empirical Analysis. Commun. Assoc. Inf. Syst. 2010, 27, 561. [Google Scholar]

- Semuel, H.; Lianto, A.S. Analisis E-Wom, Brand Image, Brand Trust Dan Minat Beli Produk Smartphone Di Surabaya. J. Manaj. Pemasar. 2014, 8, 7–54. [Google Scholar]

- Lee, K.C.; Chung, N. Understanding Factors Affecting Trust in and Satisfaction with Mobile Banking in Korea: A Modified Delone and Mclean’s Model Perspective. Interact. Comput. 2009, 21, 385–392. [Google Scholar] [CrossRef]

- Siamagka, N.T.; Christodoulides, G.; Michaelidou, N.; Valvi, A. Determinants of Social Media Adoption by B2B Organizations. Ind. Mark. Manag. 2015, 51, 89–99. [Google Scholar] [CrossRef]

- Sikdar, P.; Kumar, A.; Makkad, M. Online Banking Adoption: A Factor Validation and Satisfaction Causation Study in the Context of Indian Banking Customers. Int. J. Bank Mark. 2015, 33, 760–785. [Google Scholar] [CrossRef]

- Khedmatgozar, H.R.; Shahnazi, A. The Role of Dimensions of Perceived Risk in Adoption of Corporate Internet Banking by Customers in Iran. Electron. Commer. Res. 2018, 18, 389–412. [Google Scholar] [CrossRef]

- Bansal, S.K.; Bansal, A.; Blake, M.B. Trust-Based Dynamic Web Service Composition Using Social Network Analysis. In Proceedings of the IEEE International Workshop on Business Applications of Social Network Analysis, Bangalore, India, 15 December 2010. [Google Scholar]

- Zhou, T.; Lu, Y.; Wang, B. Integrating Ttf and Utaut to Explain Mobile Banking User Adoption. Comput. Hum. Behav. 2010, 26, 760–767. [Google Scholar] [CrossRef]

- Malaquias, F.F.D.O.; Hwang, Y. An Empirical Investigation on Disclosure about Mobile Banking on Bank Websites. Online Inf. Rev. 2018, 42, 615–629. [Google Scholar] [CrossRef]

- Kim, K.; Prabhakar, B. Initial Trust, Perceived Risk, and the Adoption of Internet Banking. In Proceedings of the Twenty First International Conference on Information Systems, Brisbane, Australia, 10–13 December 2000. [Google Scholar]

- Chong, A.Y.L.; Ooi, K.B.; Lin, B.; Tan, B.I. Online Banking Adoption: An Empirical Analysis. Int. J. Bank Mark. 2010, 28, 267–287. [Google Scholar] [CrossRef]

- Kiwanuka, A. Acceptance Process: The Missing Link between Utaut and Diffusion of Innovation Theory. J. Theor. Appl. Inf. Technol. 2015, 46, 11–16. [Google Scholar]

- Marakarkandy, B.; Yajnik, N.; Dasgupta, C. Enabling Internet Banking Adoption: An Empirical Examination with an Augmented Technology Acceptance Model (Tam). J. Enterp. Inf. Manag. 2017, 30, 263–294. [Google Scholar] [CrossRef]

- Leicht, T.; Chtourou, A.; Youssef, K.B. Consumer Innovativeness and Intentioned Autonomous Car Adoption. J. High Technol. Manag. Res. 2018, 29, 1–11. [Google Scholar] [CrossRef]

- Adeiza, A.; Ismail, N.A.; Malek, M.A. An Empirical Examination of the Major Relationship Factors Affecting Franchisees’ Overall Satisfaction and Intention to Stay. Iran. J. Manag. Stud. 2017, 10, 21–40. [Google Scholar]

- Kim, C.; Mirusmonov, M.; Lee, I. An Empirical Examination of Factors Influencing the Intention to Use Mobile Payment. Comput. Hum. Behav. 2010, 26, 310–322. [Google Scholar] [CrossRef]

- Lockett, A.; Littler, D. The Adoption of Direct Banking Services. J. Mark. Manag. 1997, 13, 791–811. [Google Scholar] [CrossRef]

- Huh, H.J.; Kim, T.; Law, R. A Comparison of Competing Theoretical Models for Understanding Acceptance Behavior of Information Systems in Upscale Hotels. Int. J. Hosp. Manag. 2009, 28, 121–134. [Google Scholar] [CrossRef]

- Wang, Y.S.; Wang, Y.M.; Lin, H.H.; Tang, T. Determinants of User Acceptance of Internet Banking: An Empirical Study. Manag. Sci. Lett. 2014, 4, 501–519. [Google Scholar] [CrossRef]

- Cheng, T.C.E.; Lam, D.Y.C.; Yeung, A.C.L. Adoption of Internet Banking: An Empirical Study in Hong Kong. Decis. Support Syst. 2007, 42, 1558–1572. [Google Scholar] [CrossRef]

- Sánchez-Torres, J.A.; Canada, F.A.; Sandoval, A.V.; Alzate, J.S. E-Banking in Colombia: Factors Favouring its Acceptance, Online Trust and Government Support. Int. J. Bank Mark. 2018, 36, 170–183. [Google Scholar] [CrossRef]

- Ha, H. Factors Influencing Consumer Perceptions of Brand Trust Online. J. Prod. Brand Manag. 2004, 13, 329–342. [Google Scholar] [CrossRef]

- Ruparelia, N.; White, L.; Hughes, K. Drivers of Brand Trust in Internet Retailing. J. Prod. Brand Manag. 2010, 19, 250–260. [Google Scholar] [CrossRef]

- Grabner-Kr Uter, S.; Faullant, R. Consumer Acceptance of Internet Banking: The Influence of Internet Trust. Int. J. Bank Mark. 2008, 26, 483–504. [Google Scholar] [CrossRef]

- Patel, K.J.; Patel, H.J. Adoption of Internet Banking Services in Gujarat. Int. J. Bank Mark. 2018, 36, 147–169. [Google Scholar] [CrossRef]

- Poolthong, Y.; Mandhachitara, R. Customer expectations of CSR, perceived service quality and brand effect in Thai retail banking. Int. J. Bank Mark. 2009, 27, 408–427. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Ruvio, A.; Shoham, A.; Brenčič, M.M. Consumers’ Need for Uniqueness: Short-Form Scale Development and Cross-Cultural Validation. Int. Mark. Rev. 2008, 25, 33–53. [Google Scholar] [CrossRef]

- Chin, W.W. Commentary: Issues and Opinion on Structural Equation Modeling. Mis Q. 1998, 22, 7–16. [Google Scholar]

- Bagozzi, R.P.; Phillips, L.W. Assessing Construct Validity in Organizational Research. Adm. Sci. Q. 1991, 36, 421–458. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. Mis Q. 1989, 13, 319–340. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Demographic Variable and Category | Frequency | Percentage | |

|---|---|---|---|

| Gender | Male | 182 | 47.03 |

| Female | 205 | 52.97 | |

| Age | 18–25 | 52 | 13.44 |

| 26–35 | 217 | 56.07 | |

| 36–45 | 61 | 15.76 | |

| 46–55 | 52 | 13.44 | |

| ≧56 | 5 | 1.29 | |

| Employ status | Student | 11 | 2.84 |

| Civil service/institution staff | 47 | 12.14 | |

| Business management personnel | 64 | 16.54 | |

| Employee | 200 | 51.68 | |

| Self-employed | 21 | 5.43 | |

| Other | 44 | 11.37 | |

| Education | Less than diploma | 35 | 9.04 |

| Diploma | 79 | 20.41 | |

| Bachelor | 223 | 57.36 | |

| Master or more | 51 | 13.18 | |

| Income (¥) | Less than 2000 | 51 | 13.18 |

| 2000–6000 | 210 | 54.26 | |

| 6001–10000 | 75 | 19.38 | |

| More than 10000 | 51 | 13.18 | |

| Fintech service usage | Never | 8 | 2.07 |

| Occasionally | 67 | 17.31 | |

| Usually | 266 | 68.73 | |

| Frequently in everyday | 46 | 11.89 | |

| Latent Variables | Measurement Items | Sources |

|---|---|---|

| Perceived usefulness (PU) | Using Fintech can meet my service needs. | Lockett et al. [68] and Huh et al. [69] |

| Fintech services can save time. | ||

| Fintech services can improve efficiency. | ||

| Overall, Fintech services are useful to me. | ||

| Perceived ease of use (PEU) | It is easy to use Fintech services. | Cheng et al. [71] and Wang et al. [70] |

| I think the operation interface of Fintech is friendly and understandable. | ||

| It is easy to have the equipment to use Fintech services (cellphone, APP, WIFI, et al.). | ||

| Trust (TRU) | I believe Fintech services keep my personal information safe. | Chong et al. [62] and Sanchez et al. [72] |

| Overall I believe Fintech services are trustable. | ||

| Brand image (BI) | This bank can provide good services and products. | Ha et al. [73] and Ruparelia et al. [74] |

| I think I prefer to accept the services provided by familiar brands. | ||

| The bank has a good reputation. | ||

| Perceived risk (PR) | I believe that the money is easy to be stolen by using Fintech services. | Marakarkandy et al. [64] and Grabner et al. [75] |

| I believe personal privacy will be disclosed by using Fintech services. | ||

| Overall, I feel Fintech services are risky. | ||

| Government support (GS) | I believe the government supports and improve the use of Fintech services. | Marakarkandy et al. [64] |

| I believe the government has introduced favorable legislation and regulations for Fintech services. | ||

| I believe the government is active in setting up all kinds of infrastructure such as the infrastructure telecom network, which has a positive role in promoting Fintech services. | ||

| User innovativeness (UI) | When I hear about a new product, I look for ways to try it | Zhang et al. [19] |

| Among my peers, I am usually the first one to try a new product. | ||

| Attitude (ATT) | I believe using Fintech services is a good idea. | Grabner et al. [75] |

| Using Fintech services is a pleasant experience. | ||

| I am interested in Fintech services. | ||

| Intention (INT) | If I have used Fintech services, I am willing to continue using them. | Marakarkandy et al. [64] and Patel et al. [76] |

| I would like to use Fintech services soon. | ||

| I will recommend Fintech services to my friends. |

| Constructs | Item | λ | AVE | CR | Cronbach’s Alpha |

|---|---|---|---|---|---|

| PU | PU1 | 0.725 | 0.680 | 0.894 | 0.840 |

| PU2 | 0.878 | ||||

| PU3 | 0.801 | ||||

| PU4 | 0.883 | ||||

| PEU | PEU1 | 0.860 | 0.755 | 0.902 | 0.837 |

| PEU2 | 0.886 | ||||

| PEU3 | 0.859 | ||||

| BI | BI1 | 0.906 | 0.812 | 0.928 | 0.884 |

| BI2 | 0.904 | ||||

| BI3 | 0.893 | ||||

| PR | PR1 | 0.809 | 0.767 | 0.908 | 0.851 |

| PR2 | 0.928 | ||||

| PR3 | 0.886 | ||||

| GS | GS1 | 0.840 | 0.713 | 0.882 | 0.799 |

| GS2 | 0.809 | ||||

| GS3 | 0.883 | ||||

| UI | UI1 | 0.922 | 0.844 | 0.915 | 0.815 |

| UI2 | 0.916 | ||||

| TRU | TRU1 | 0.889 | 0.827 | 0.905 | 0.793 |

| TRU2 | 0.930 | ||||

| ATT | ATT1 | 0.914 | 0.830 | 0.936 | 0.897 |

| ATT2 | 0.902 | ||||

| ATT3 | 0.916 | ||||

| INT | INT1 | 0.884 | 0.737 | 0.894 | 0.822 |

| INT2 | 0.816 | ||||

| INT3 | 0.874 |

| Construct | PU | PEU | BI | PR | GS | UI | TRU | ATT | INT |

|---|---|---|---|---|---|---|---|---|---|

| PU | 0.824 | - | - | - | - | - | - | - | - |

| PEU | 0.741 | 0.869 | - | - | - | - | - | - | - |

| BI | 0.425 | 0.421 | 0.901 | - | - | - | - | - | - |

| PR | −0.205 | −0.168 | −0.244 | 0.876 | - | - | - | - | - |

| GS | 0.504 | 0.508 | 0.502 | −0.184 | 0.844 | - | - | - | - |

| UI | 0.294 | 0.355 | 0.41 | −0.136 | 0.507 | 0.919 | - | - | - |

| TRU | 0.453 | 0.49 | 0.541 | −0.369 | 0.567 | 0.486 | 0.909 | - | - |

| ATT | 0.583 | 0.58 | 0.569 | −0.221 | 0.71 | 0.617 | 0.607 | 0.911 | - |

| INT | 0.518 | 0.547 | 0.582 | −0.234 | 0.591 | 0.552 | 0.572 | 0.793 | 0.858 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hu, Z.; Ding, S.; Li, S.; Chen, L.; Yang, S. Adoption Intention of Fintech Services for Bank Users: An Empirical Examination with an Extended Technology Acceptance Model. Symmetry 2019, 11, 340. https://doi.org/10.3390/sym11030340

Hu Z, Ding S, Li S, Chen L, Yang S. Adoption Intention of Fintech Services for Bank Users: An Empirical Examination with an Extended Technology Acceptance Model. Symmetry. 2019; 11(3):340. https://doi.org/10.3390/sym11030340

Chicago/Turabian StyleHu, Zhongqing, Shuai Ding, Shizheng Li, Luting Chen, and Shanlin Yang. 2019. "Adoption Intention of Fintech Services for Bank Users: An Empirical Examination with an Extended Technology Acceptance Model" Symmetry 11, no. 3: 340. https://doi.org/10.3390/sym11030340

APA StyleHu, Z., Ding, S., Li, S., Chen, L., & Yang, S. (2019). Adoption Intention of Fintech Services for Bank Users: An Empirical Examination with an Extended Technology Acceptance Model. Symmetry, 11(3), 340. https://doi.org/10.3390/sym11030340