Are Delay and Interval Effects the Same Anomaly in the Context of Intertemporal Choice in Finance?

Abstract

:1. Introduction

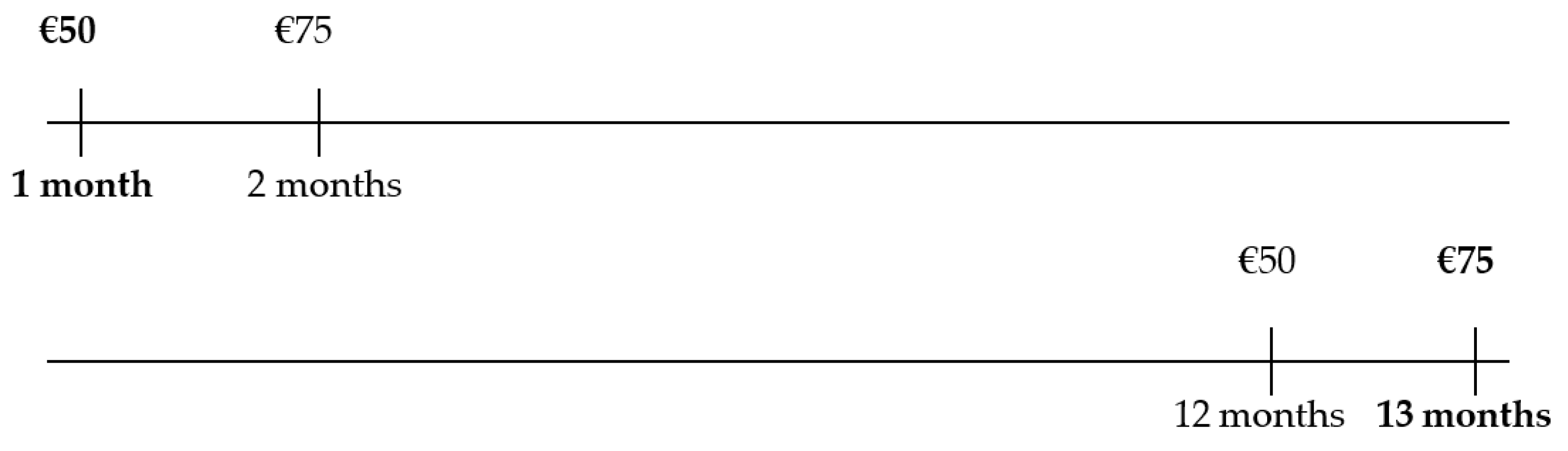

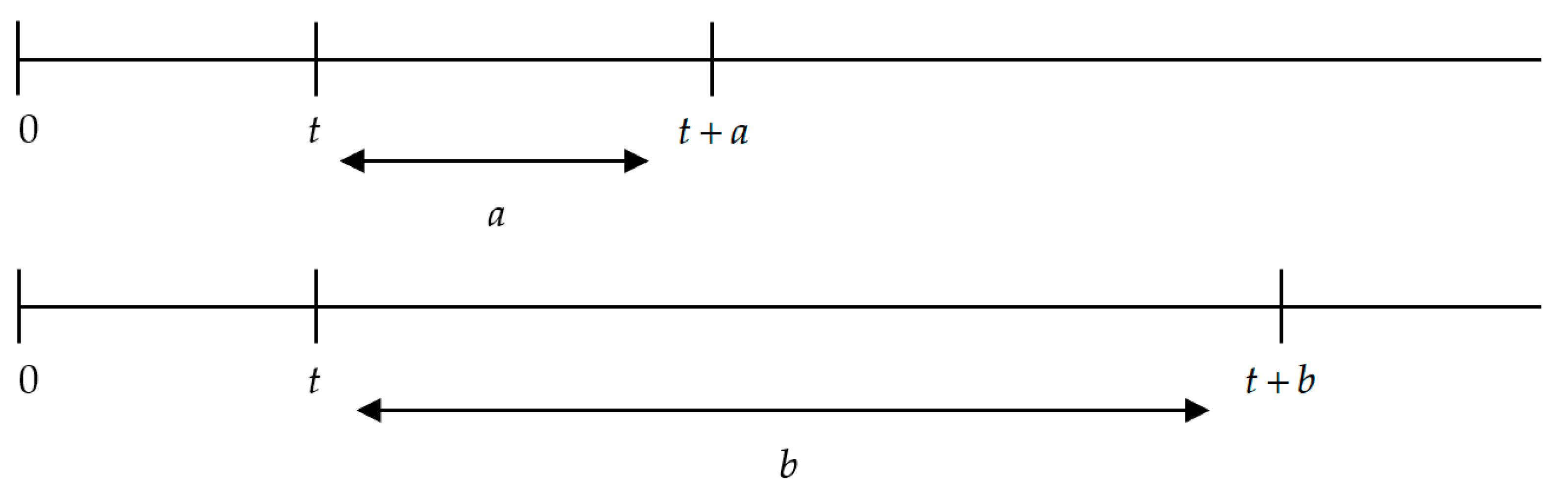

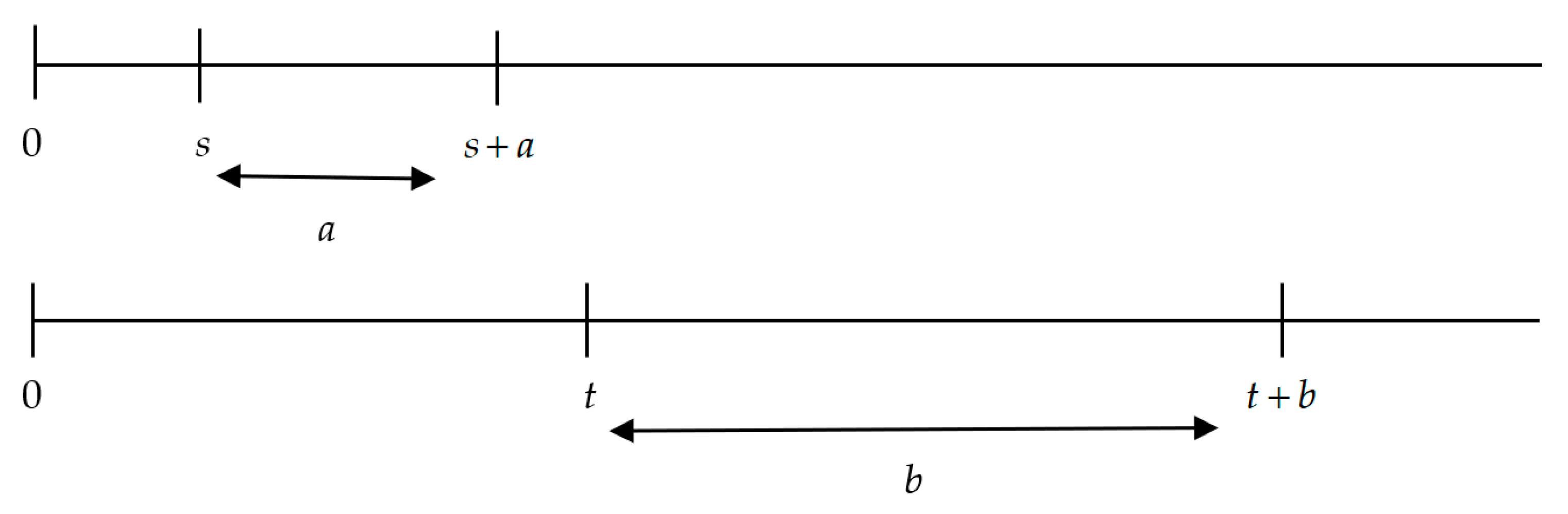

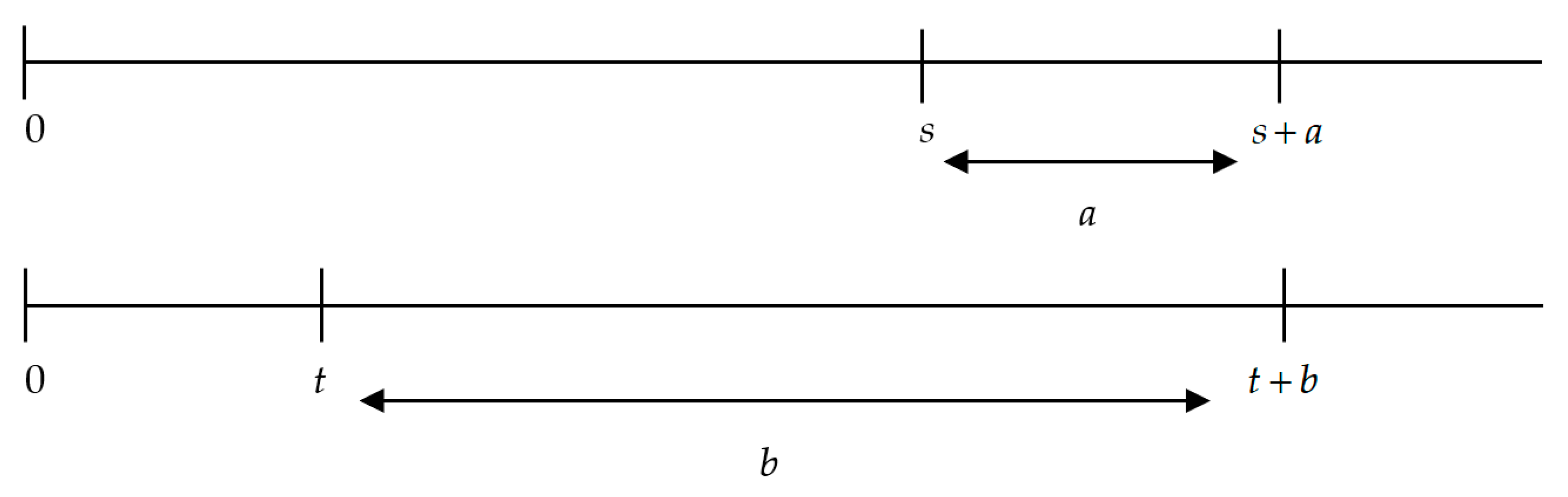

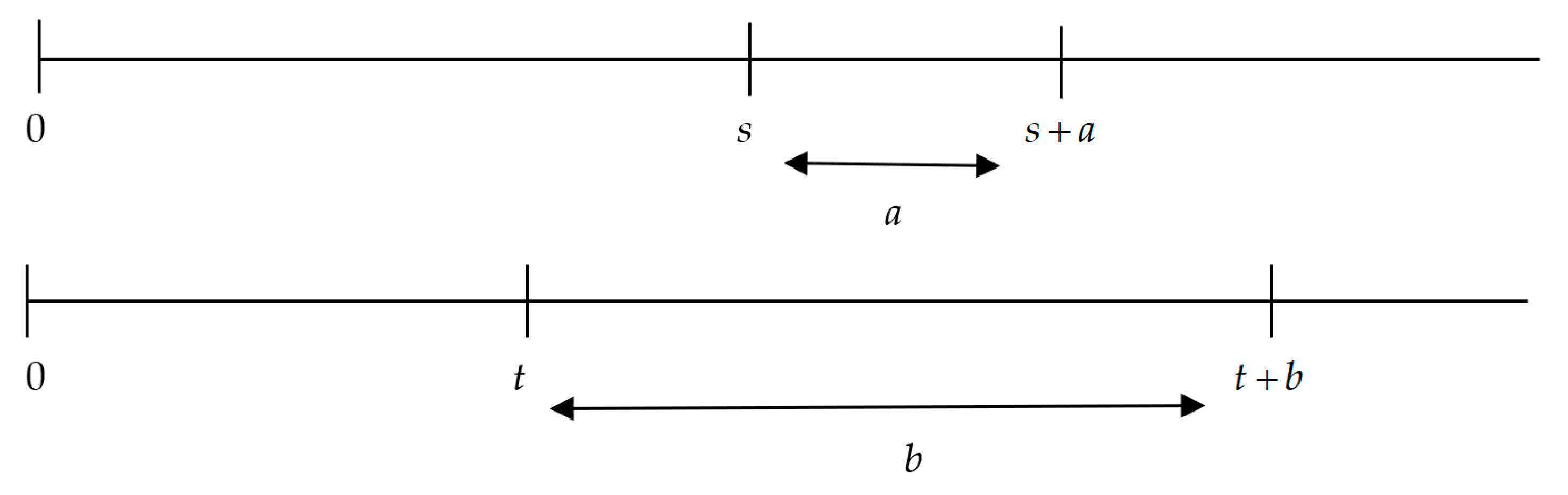

2. The Delay Effect

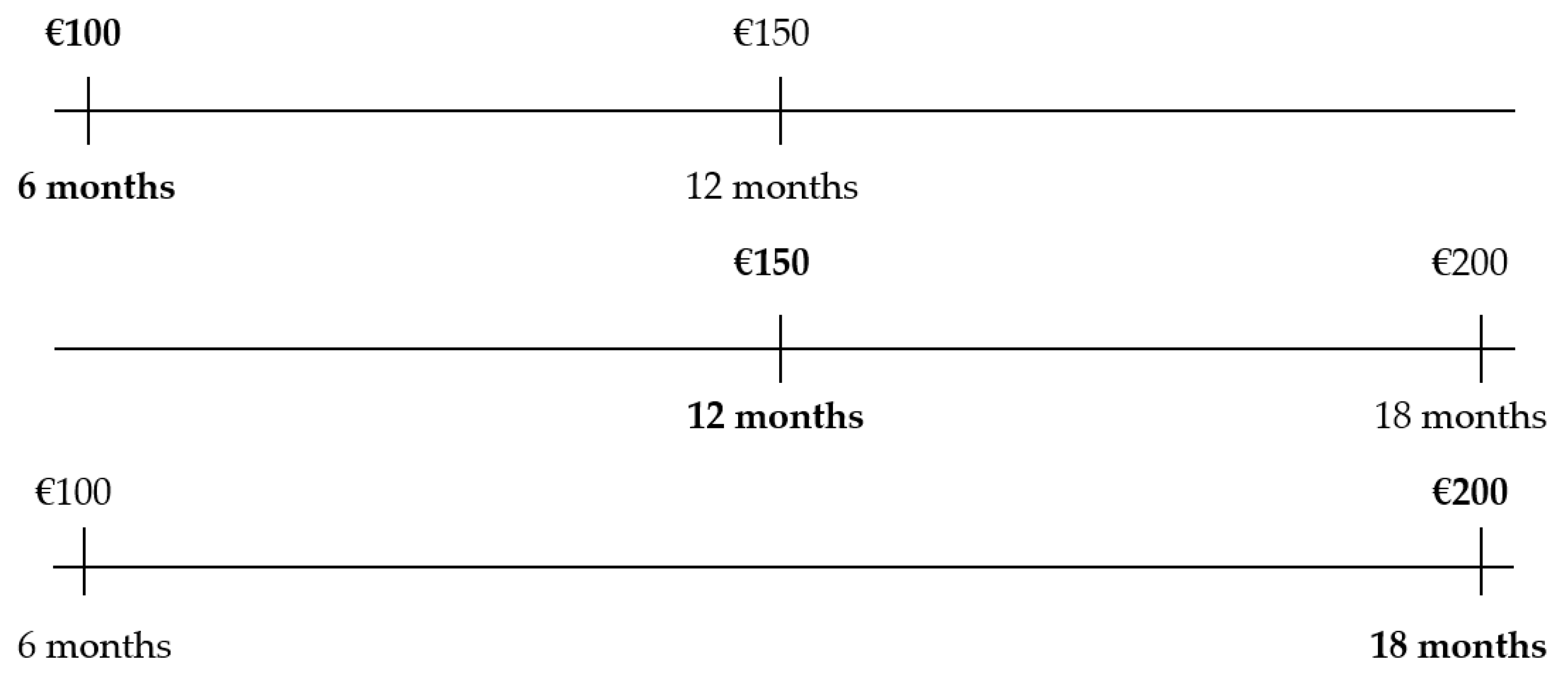

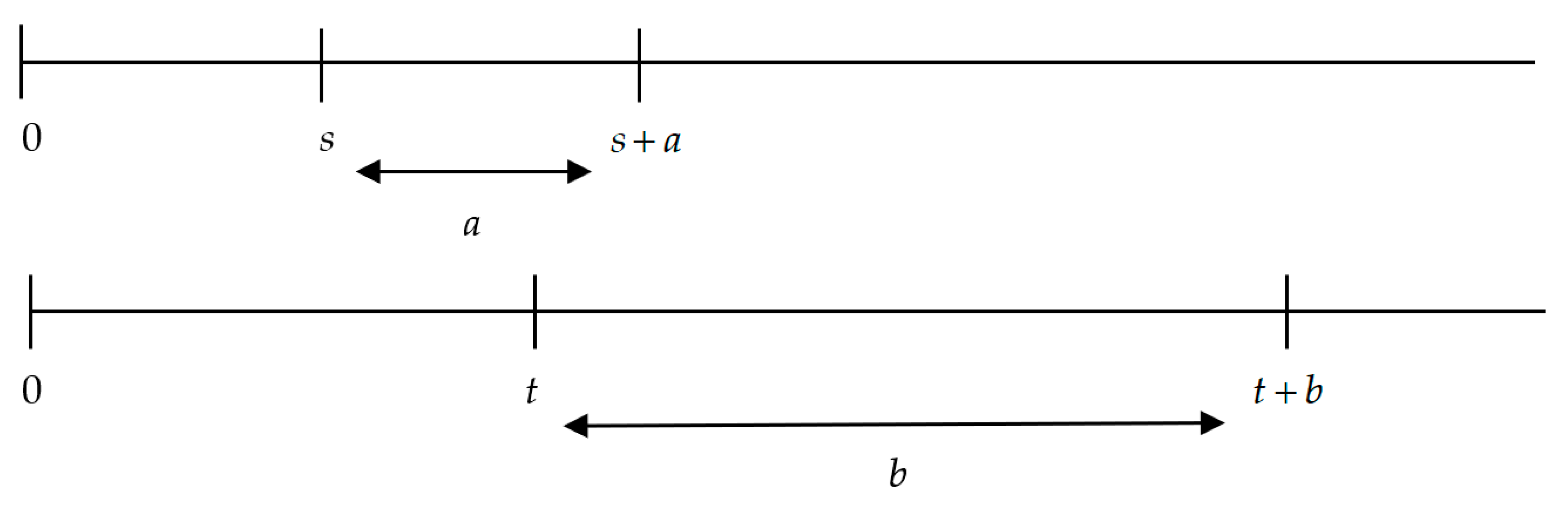

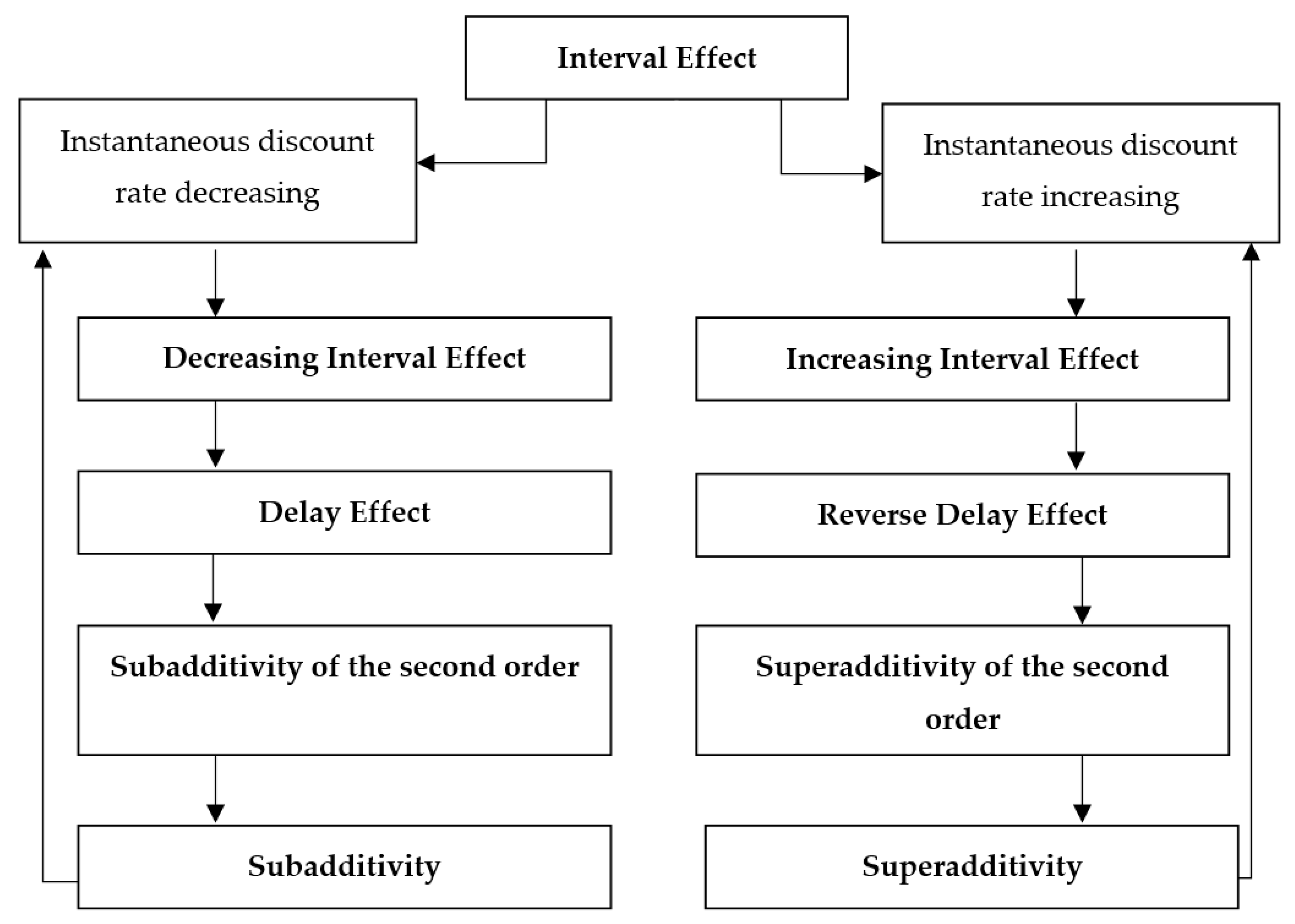

3. The Interval Effect

- 1.

- , whereis the mean discount rate in the interval;

- 2.

- , whereis the instantaneous discount rate at time t.

- The general expression of a discount function, according to its instantaneous discount rate, leads to and Therefore, as is the average of function in the interval , one haswhich is the required equality;

- , which is an indetermination. Let us solve this indetermination by using the well-known formula to solve this type of indetermination:

4. Mathematical Analysis of the Delay and Interval Effects

4.1. Assessment at a Given Benchmark (Time 0)

- (i)

- If, then;

- (ii)

- The instantaneous discount rate is strictly decreasing;

- (iii)

- If, then;

- (iv)

- The delay effect holds;

- (v)

- The subadditivity of the second order holds.

- The instantaneous discount rate is constant in the interval . This is not possible because by taking and , one has , in contradiction with (i);

- The instantaneous discount rate is not constant in the interval . In this case, there is a subinterval of , where the instantaneous discount rate is increasing and, as such, the reasoning is the same as the case in which .

- (i)

- If, then;

- (ii)

- The instantaneous discount rate is strictly increasing;

- (iii)

- If, then;

- (iv)

- The reverse delay effect holds;

- (v)

- The superadditivity of the second order holds.

4.2. Assesment at Variable Reference (at the Front-End Delay of the Interval)

5. Conclusions and Future Research

- The decreasing interval effect, wherein the discount rate decreases (the FED of the short interval is less than or equal to the FED of the larger interval);

- The increasing interval effect, wherein the discount rate increases (the FED of the larger interval is less than the FED of the shorter interval).

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Reference | Term Used | Definition | Experimental Work? | Mathematical Definition? |

|---|---|---|---|---|

| [20] | Subadditive discounting | Yes | Yes | No |

| [28] | Interval effect and subadditive discounting | Yes | Yes | No |

| [23] | Interval effect | [28] | No | No |

| [21] | Interval effect | Yes | Yes | No |

| [35] | Interval effect | [20] | No | No |

| [26] | The effect of interval length | [20] | Yes | No |

| [30] | Interval effect | Yes | No | No |

| [27] | Interval effect | [20,23] | No | No |

| [36] | Interval effect | [23] | Yes | No |

| [37] | Interval effect | [20,28] | Yes | No |

References

- Loewenstein, G.; Prelec, D. Negative time preference. Am. Econ. Rev. 1991, 81, 347–352. [Google Scholar]

- Loewenstein, G.; Prelec, D. Anomalies in Intertemporal Choice: Evidence and an Interpretation. Q. J. Econ. 1992, 107, 573–597. [Google Scholar] [CrossRef]

- Prelec, D. Decreasing Impatience: A Criterion for Non-stationary Time Preference and “Hyperbolic” Discounting. Scand. J. Econ. 2004, 106, 511–532. [Google Scholar] [CrossRef]

- Samuelson, P.A. A Note on Measurement of Utility. Rev. Econ. Stud. 1937, 4, 155–161. [Google Scholar] [CrossRef]

- Keren, G.; Roelofsma, P. Immediacy and Certainty in Intertemporal Choice. Organ. Behav. Hum. Decis. Process. 1995, 63, 287–297. [Google Scholar] [CrossRef] [Green Version]

- Read, D.; Loewenstein, G.; Kalyanaraman, S.; Bivolaru, A. Mixing virtue and vice: The combined effects of hyperbolic discounting and diversification. J. Behav. Decis. Mak. 1999, 12, 257–273. [Google Scholar] [CrossRef]

- Weber, B.J.; Huettel, S.A. The neural substrates of probabilistic and intertemporal decision making. Brain Res. 2008, 1234, 104–115. [Google Scholar] [CrossRef] [Green Version]

- Kahneman, D.; Tversky, A. On the interpretation of intuitive probability: A reply to Jonathan Cohen. Cognition 1979, 7, 409–411. [Google Scholar] [CrossRef]

- Benzion, U.; Rapoport, A.; Yagil, J. Discount Rates Inferred from Decisions: An Experimental Study. Manag. Sci. 1989, 35, 270–284. [Google Scholar] [CrossRef]

- Thaler, R. Some empirical evidence on dynamic inconsistency. Econ. Lett. 1981, 8, 201–207. [Google Scholar] [CrossRef]

- Green, L.; Myerson, J.; Ostaszewski, P. Amount of reward has opposite effects on the discounting of delayed and probabilistic outcomes. J. Exp. Psychol. Learn. Mem. Cogn. 1999, 25, 418–427. [Google Scholar] [CrossRef] [PubMed]

- Prelec, D.; Loewenstein, G. Decision Making Over Time and Under Uncertainty: A Common Approach. Manag. Sci. 1991, 37, 770–786. [Google Scholar] [CrossRef]

- Loewenstein, G. Anticipation and the Valuation of Delayed Consumption. Econ. J. 1987, 97, 666–684. [Google Scholar] [CrossRef] [Green Version]

- Loewenstein, G.; Sicherman, N. Do Workers Prefer Increasing Wage Profiles? J. Labor Econ. 1991, 9, 67–84. [Google Scholar] [CrossRef]

- Chapman, G.B. Temporal discounting and utility for health and money. J. Exp. Psychol. Learn. Mem. Cogn. 1996, 22, 771–791. [Google Scholar] [CrossRef]

- Chapman, G.B. Preferences for improving and declining sequences of health outcomes. J. Behav. Decis. Mak. 2000, 13, 203–218. [Google Scholar] [CrossRef]

- Ainslie, G. Specious reward: A behavioral theory of impulsiveness and impulse control. Psychol. Bull. 1975, 82, 463–496. [Google Scholar] [CrossRef] [Green Version]

- Christensen-Szalanski, J.J. Discount functions and the measurement of patients’ values. Women’s decisions during childbirth. Med. Decis. Mak. 1984, 4, 47–58. [Google Scholar] [CrossRef]

- Chapman, G.B. Time preferences for the very long term. Acta Psychol. 2001, 108, 95–116. [Google Scholar] [CrossRef]

- Read, D. Is Time-Discounting Hyperbolic or Subadditive? J. Risk Uncertain. 2001, 23, 5–32. [Google Scholar] [CrossRef]

- Scholten, M.; Read, D. Interval Effects: Superadditivity and Subadditivity in Intertemporal Choice; Working Paper No: LSEOR 04.66; The London School of Economics and Political Science: London, UK, 2004; pp. 1–30. [Google Scholar]

- Rambaud, S.C.; Fernández, P.O. Delay Effect and Subadditivity. Proposal of a New Discount Function: The Asymmetric Exponential Discounting. Mathematics 2020, 8, 367. [Google Scholar] [CrossRef] [Green Version]

- Read, D. Intertemporal Choice. In Blackwell Handbook of Judgment and Decision Making; Koehler, D., Harvey, N., Eds.; Blackwell: Oxford, UK, 2004; pp. 424–443. [Google Scholar]

- Mazur, J.E. An Adjusting Procedure for Studying Delayed Reinforcement. In Quantitative Analyses of Behavior; Commons, M.L., Mazur, J.E., Nevin, J.A., Rachlin, H., Eds.; The Effect of Delay and of Intervening Events on Reinforcement Value; Lawrence Erlbaum Associates, Inc.: Mahwah, NJ, USA, 1987; Volume 5, pp. 55–73. [Google Scholar]

- Rachlin, H. Judgment, Decision, and Choice: A Cognitive/Behavioral Synthesis. In A Series of Books in Psychology; WH Freeman/Times Books/Henry Holt & Co.: New York, NY, USA, 1989. [Google Scholar]

- Scholten, M.; Read, D. Discounting by Intervals: A Generalized Model of Intertemporal Choice. Manag. Sci. 2006, 52, 1424–1436. [Google Scholar] [CrossRef]

- Rambaud, S.C.; Torrecillas, M.J.M. Delay and Interval Effects with Subadditive Discounting Functions. In Preferences and Decisions: Models and Applications; Greco, S., Pereira, R.A.M., Squillante, M., Yager, R.R., Eds.; Springer: Berlin, Germany, 2010; pp. 85–110. [Google Scholar]

- Read, D.; Roelofsma, P.H. Subadditive versus hyperbolic discounting: A comparison of choice and matching. Organ. Behav. Hum. Decis. Process. 2003, 91, 140–153. [Google Scholar] [CrossRef]

- Kinari, Y.; Ohtake, F.; Tsutsui, Y. Time Discounting: Declining Impatience and Interval Effect. In Behavioral Economics of Preferences, Choices, and Happiness; Ikeda, S., Kato, H.K., Ohtake, F., Tsutsui, Y., Eds.; Springer: Tokyo, Japan, 2016; pp. 49–76. [Google Scholar]

- Kinari, Y.; Ohtake, F.; Tsutsui, Y. Time discounting: Declining impatience and interval effect. J. Risk Uncertain. 2009, 39, 87–112. [Google Scholar] [CrossRef] [Green Version]

- Rachlin, H.; Green, L. Commitment, choice and self-control. J. Exp. Anal. Behav. 1972, 17, 15–22. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Martinez-Garcia, M.; Kalawsky, R.; Gordon, T.J.; Smith, T.; Meng, Q.; Flemisch, F. Communication and Interaction with Semiautonomous Ground Vehicles by Force Control Steering. IEEE Trans. Cybern. 2020, 1–12. [Google Scholar] [CrossRef]

- Rambaud, S.C.; Oller, I.M.P.; Martínez, M.D.C.V. The amount-based deformation of the q-exponential discount function: A joint analysis of delay and magnitude effects. Phys. A Stat. Mech. Appl. 2018, 508, 788–796. [Google Scholar] [CrossRef]

- Zhang, Y.; Martinez-Garcia, M.; Gordon, T. Human Response Delay Estimation and Monitoring Using Gamma Distribution Analysis. In Proceedings of the 2018 IEEE International Conference on Systems, Man, and Cybernetics (SMC), Miyazaki, Japan, 7–10 October 2018; pp. 807–812. [Google Scholar]

- Soman, D.; Ainslie, G.; Frederick, S.; Li, X.; Lynch, J.G.; Moreau, P.; Mitchell, A.; Read, D.; Sawyer, A.; Trope, Y.; et al. The Psychology of Intertemporal Discounting: Why are Distant Events Valued Differently from Proximal Ones? Mark. Lett. 2005, 16, 347–360. [Google Scholar] [CrossRef]

- Xie, S.; Ikeda, S.; Qin, J.; Sasaki, S.; Tsutsui, Y. Time Discounting: The Delay Effect and Procrastinating Behavior. J. Behav. Econ. Financ. 2012, 5, 15–25. [Google Scholar] [CrossRef] [Green Version]

- Shen, S.C.; Huang, Y.N.; Jiang, C.M.; Li, S. Can asymmetric subjective opportunity cost effect explain impatience in intertemporal choice? A replication study. Judgm. Decis. Mak. 2019, 14, 214–222. [Google Scholar]

| Delay | Interval | |

|---|---|---|

| Delay effect | Different | Equal |

| Interval effect | Equal | Different |

| Reference | Definition |

|---|---|

| [20] | “The discount rate will be greater the shorter the interval” |

| [28] | “Shorter intervals lead to more discounting per-time-unit” |

| [29,30] | “The longer the interval, the lower the per-period time discount rate” “The per-period time discount rate decreases as the interval lengthens” |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cruz Rambaud, S.; Ortiz Fernández, P. Are Delay and Interval Effects the Same Anomaly in the Context of Intertemporal Choice in Finance? Symmetry 2021, 13, 41. https://doi.org/10.3390/sym13010041

Cruz Rambaud S, Ortiz Fernández P. Are Delay and Interval Effects the Same Anomaly in the Context of Intertemporal Choice in Finance? Symmetry. 2021; 13(1):41. https://doi.org/10.3390/sym13010041

Chicago/Turabian StyleCruz Rambaud, Salvador, and Piedad Ortiz Fernández. 2021. "Are Delay and Interval Effects the Same Anomaly in the Context of Intertemporal Choice in Finance?" Symmetry 13, no. 1: 41. https://doi.org/10.3390/sym13010041

APA StyleCruz Rambaud, S., & Ortiz Fernández, P. (2021). Are Delay and Interval Effects the Same Anomaly in the Context of Intertemporal Choice in Finance? Symmetry, 13(1), 41. https://doi.org/10.3390/sym13010041