Do Bitcoin and Traditional Financial Assets Act as an Inflation Hedge during Stable and Turbulent Markets? Evidence from High Cryptocurrency Adoption Countries

Abstract

:1. Introduction

2. Literature Review

2.1. Inflation Hedge Testing

2.2. Inflation Hedge Assets

2.3. Methodology Issues

3. Methodology

4. Data

5. Empirical Results

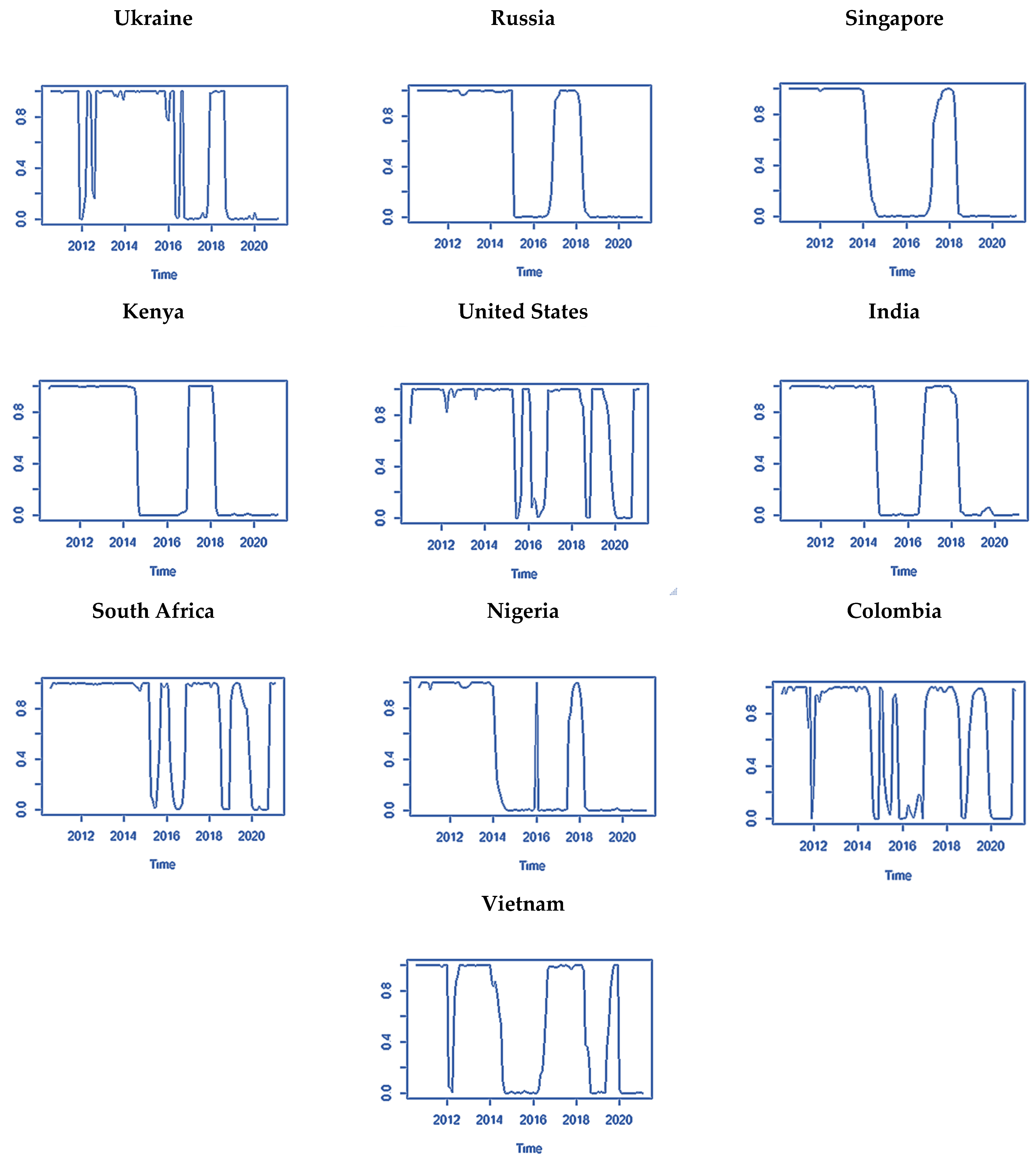

5.1. States of the Market

5.2. Main Results of the Inflation Hedging Property of BITCOIN and Other Assets

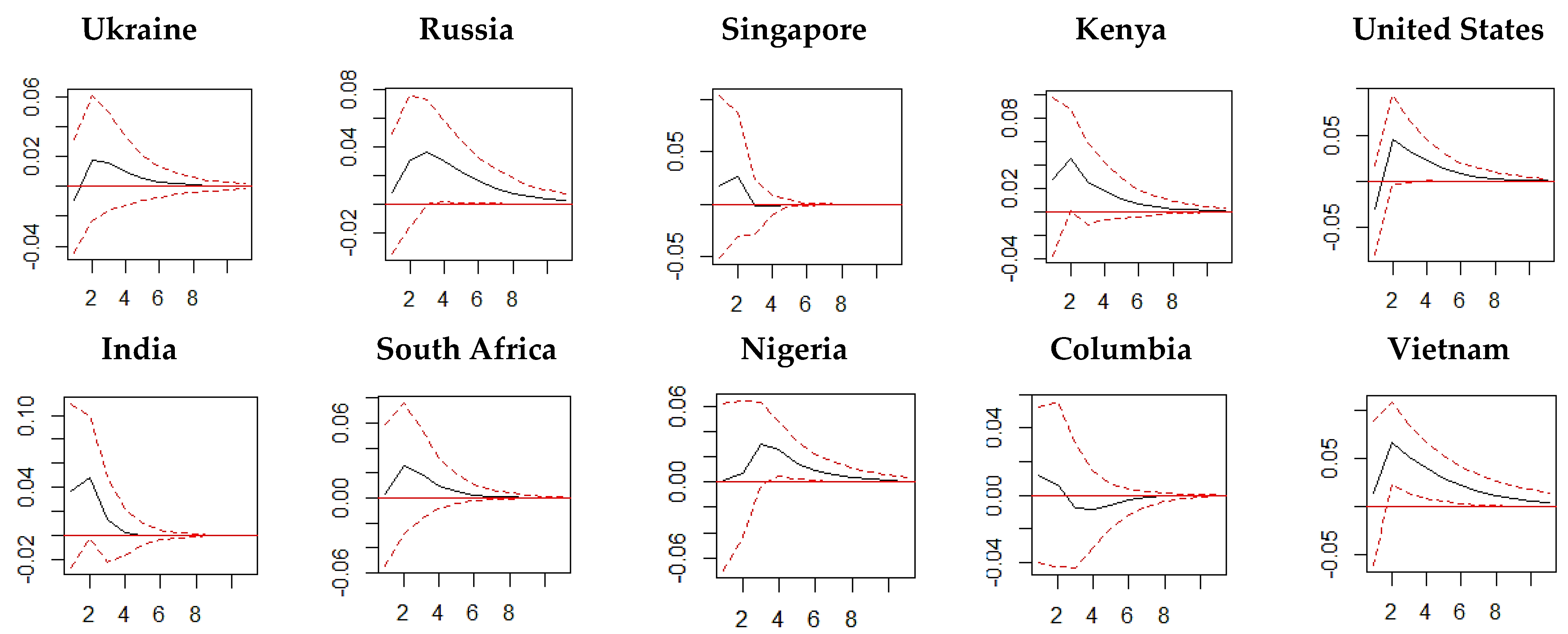

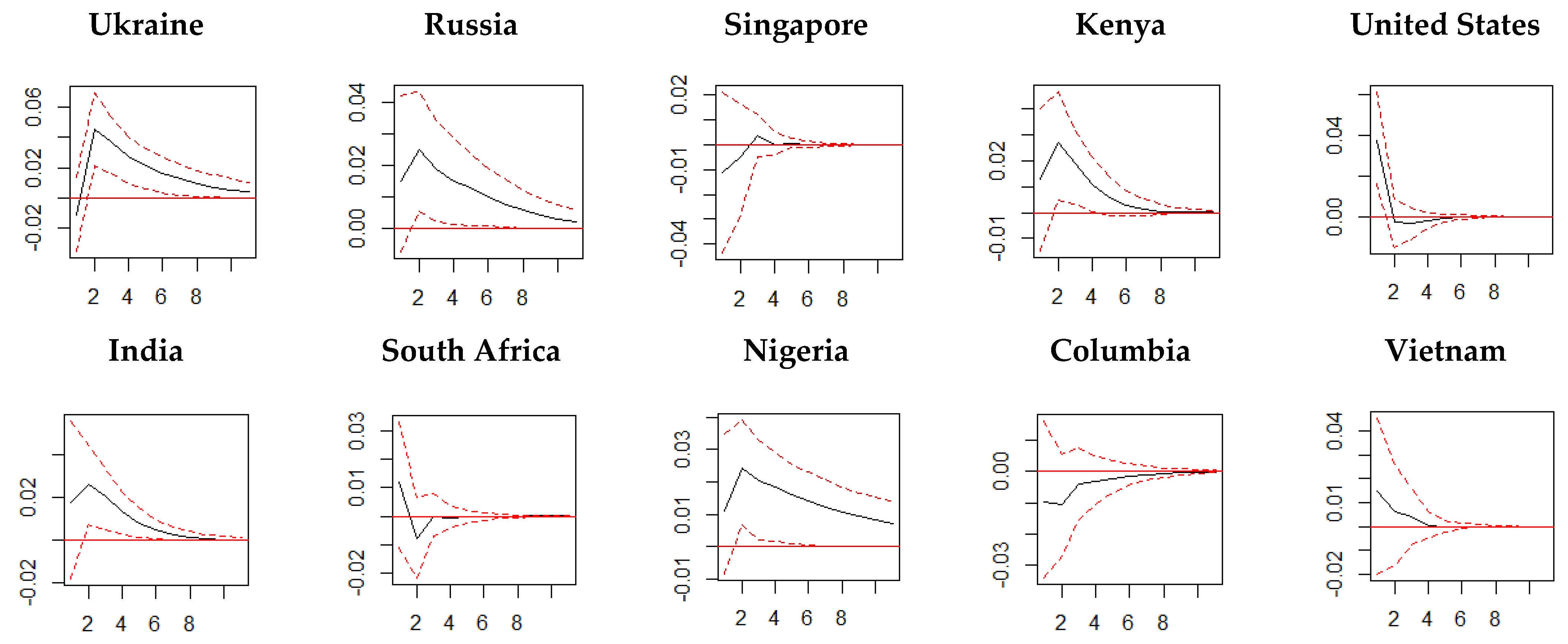

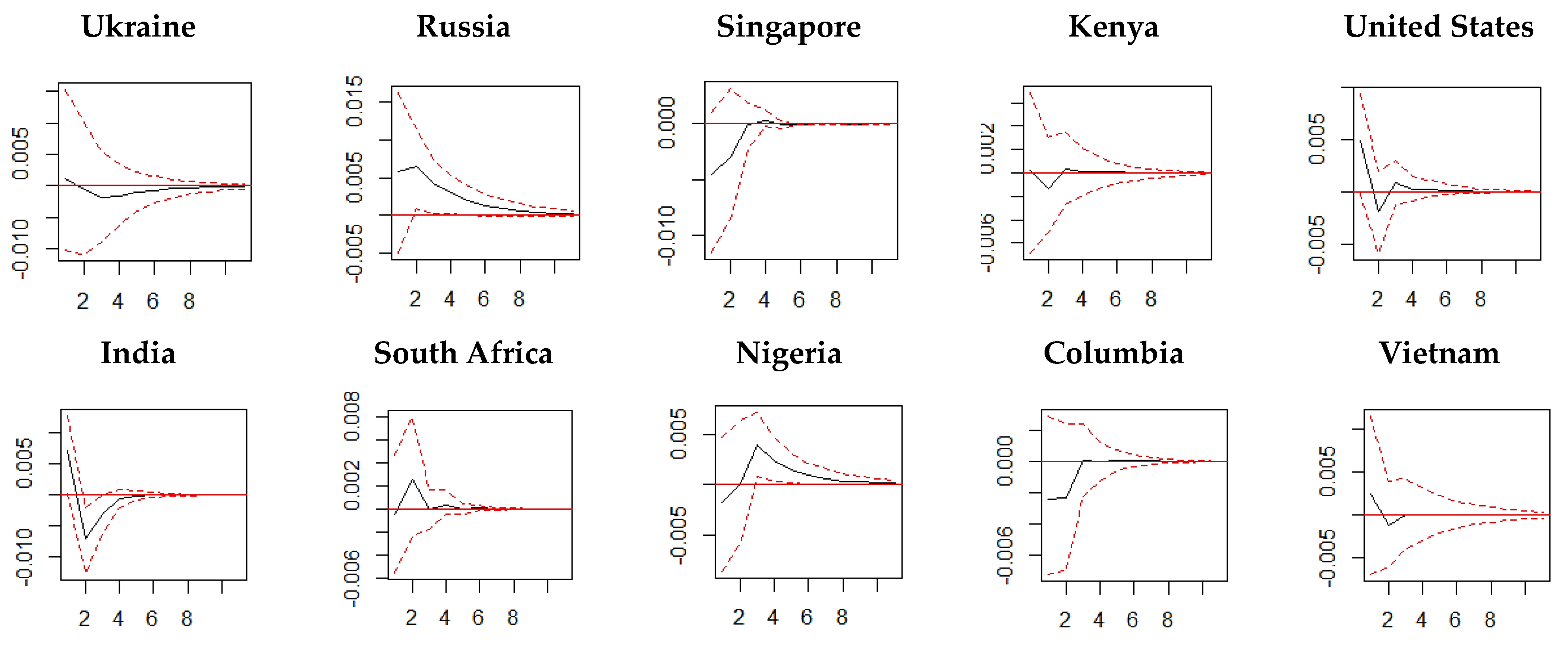

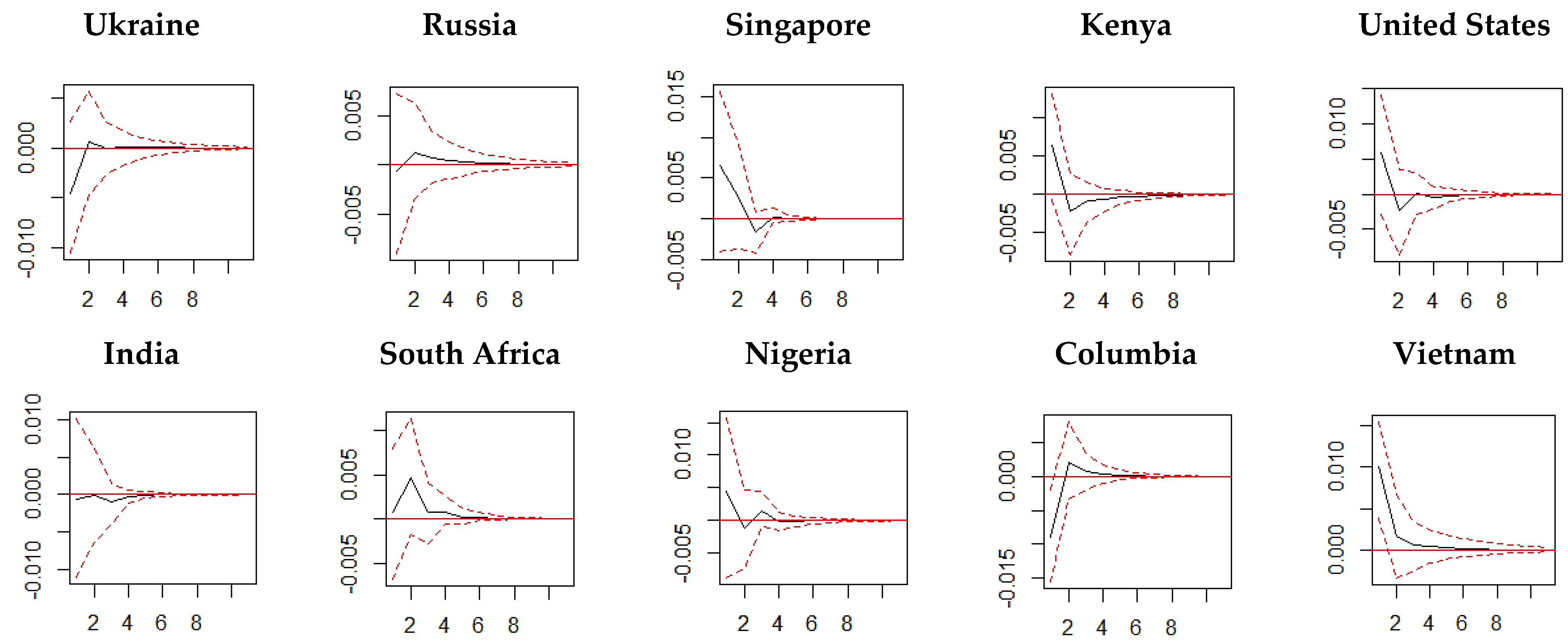

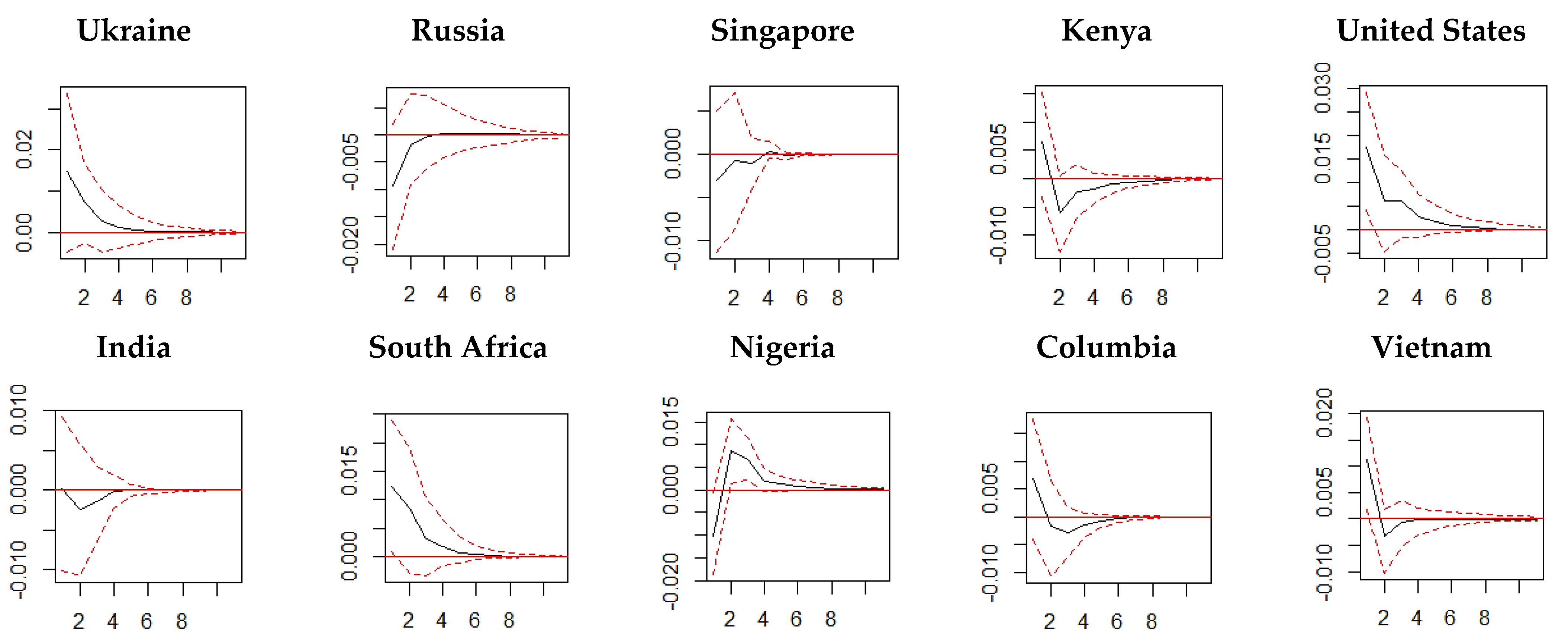

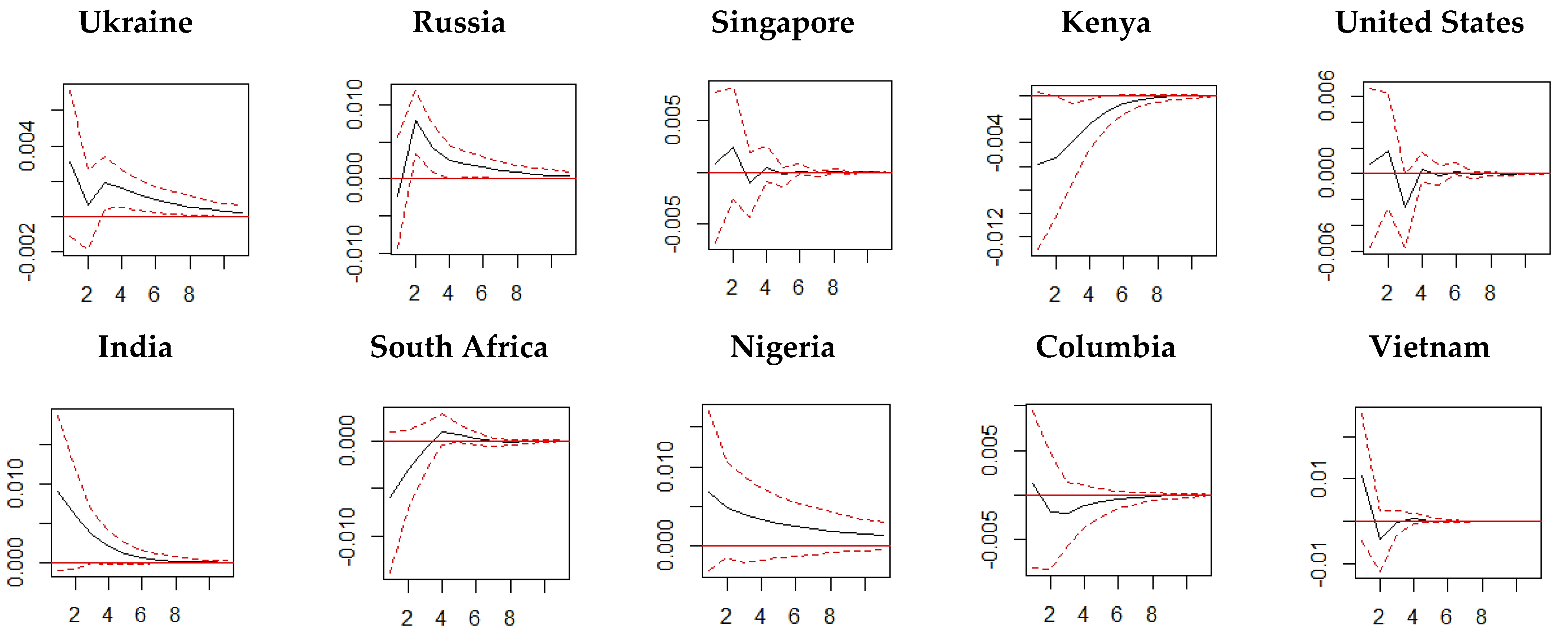

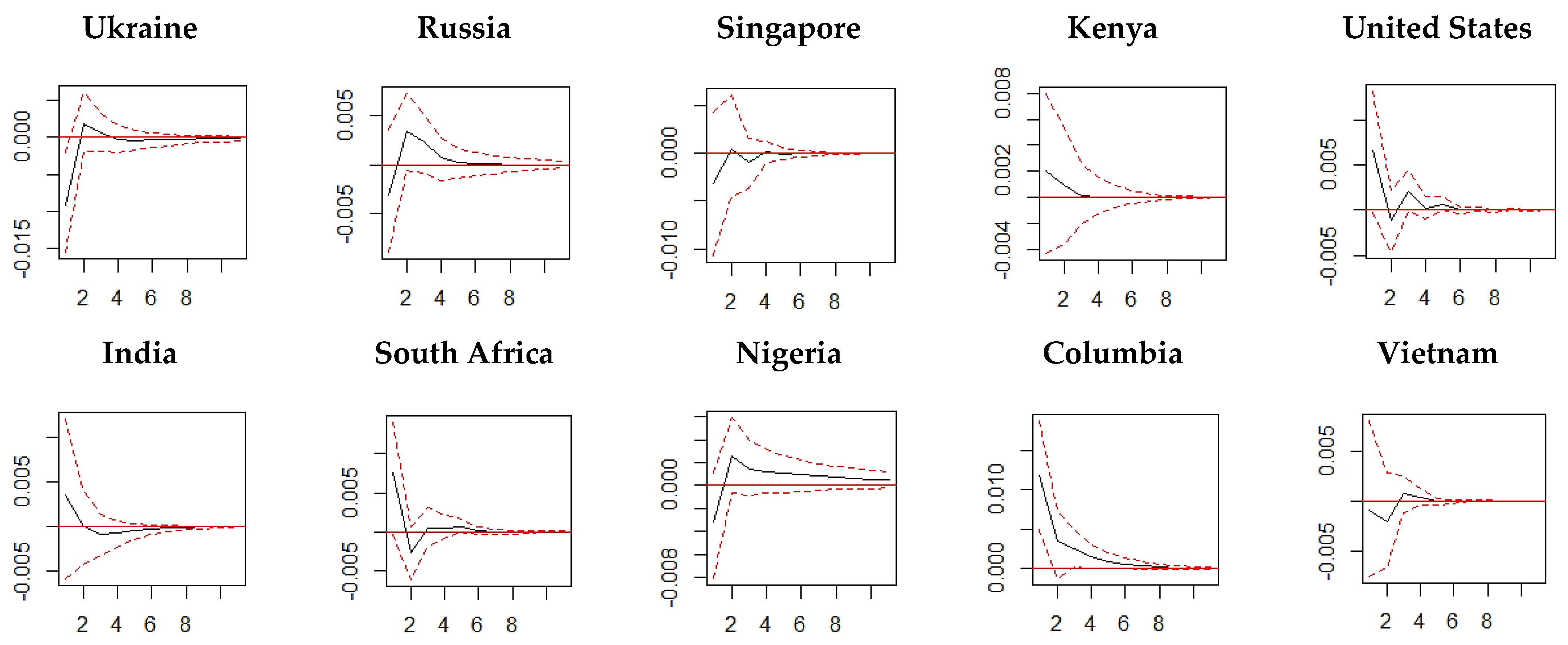

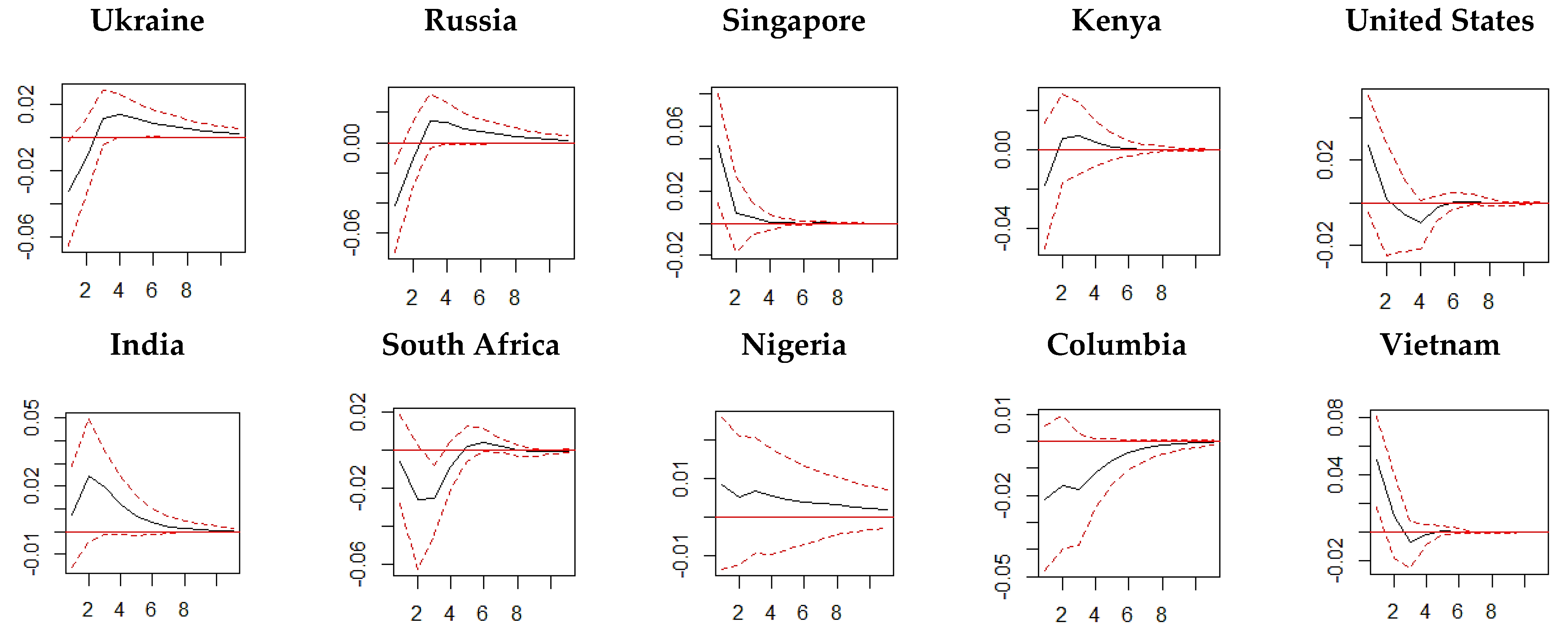

5.3. Impulse Response Function (IRF)

6. Conclusions, Policy Implication and Limitation, and Future Research

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Inflation | Stock | Bitcoin | Gold | Oil | |

|---|---|---|---|---|---|

| Ukraine | 0.0049 *** | −0.0017 | 0.0857 ** | 0.0047 | −0.0031 |

| (0.0017) | (0.0095) | (0.0391) | (0.0050) | (0.0085) | |

| Russia | 0.0024 *** | 0.0185 * | 0.0569 | 0.0030 | −0.0036 |

| (0.0006) | (0.0063) | (0.0491) | (0.0062) | (0.0090) | |

| Singapore | 0.0025 *** | 0.0004 | 0.1145 *** | 0.0009 | 0.0124 ** |

| (0.0004) | (0.0046) | (0.0392) | (0.0046) | (0.0060) | |

| Kenya | 0.0034 *** | 0.0120 *** | 0.0834 ** | 0.0047 | 0.0206 *** |

| (0.0007) | (0.0048) | (0.0469) | (0.0056) | (0.0069) | |

| United States | 0.0012 *** | 0.0163 *** | 0.0505 * | 0.0062 | 0.0100 |

| (0.0002) | (0.0031) | (0.0355) | (0.0049) | (0.0080) | |

| India | 0.0047 *** | 0.0247 *** | 0.0822 ** | 0.0007 | 0.0164 *** |

| (0.0007) | (0.0044) | (0.0424) | (0.0053) | (0.0066) | |

| South Africa | 0.0033 *** | 0.0162 *** | 0.0568 | 0.0008 | 0.0043 |

| (0.0004) | (0.0046) | (0.0469) | (0.0062) | (0.0107) | |

| Nigeria | 0.0094 *** | 0.0039 | 0.1212 * | 0.0063 | 0.0142 |

| (0.0010) | (0.0092) | (0.0817) | (0.0100) | (0.0115) | |

| Columbia | 0.0013 *** | 0.0046 | 0.1458 *** | 0.0020 *** | 0.0157 ** |

| (0.0002) | (0.0048) | (0.0463) | (0.0059) | (0.0085) | |

| Vietnam | 0.0020 *** | 0.0118 ** | 0.0654 *** | 0.0076 | 0.0166 *** |

| (0.0005) | (0.0058) | (0.0298) | (0.0051) | (0.0064) |

| Inflation | Stock | Bitcoin | Gold | Oil | |

|---|---|---|---|---|---|

| Ukraine | 0.0019 *** | −0.0119 *** | 0.0364 ** | −0.0228 *** | −0.0795 *** |

| (0.0005) | (0.0019) | (0.0188) | (0.0038) | (0.0192) | |

| Russia | 0.0022 *** | −0.0154 *** | 0.0482 ** | −0.0052 | −0.0419 ** |

| (0.0006) | (0.0063) | (0.0491) | (0.0062) | (0.0090) | |

| Singapore | 0.0002 | −0.0055 * | 0.0427 *** | −0.0031 | −0.0181 |

| (0.0003) | (0.0041) | (0.0168) | (0.0040) | (0.0167) | |

| Kenya | 0.0035 *** | −0.0129 *** | 0.0176 | −0.0032 | −0.0144 |

| (0.0005) | (0.0054) | (0.0207) | (0.0050) | (0.0210) | |

| United States | 0.0004 *** | 0.0065 | 0.0122 | 0.0011 | −0.0033 |

| (0.0481) | (1.7070) | (0.7123) | (1.2834) | (4.3423) | |

| India | 0.0023 *** | 0.0006 | 0.0224 | −0.0064 * | −0.0403 *** |

| (0.0007) | (0.0044) | (0.0424) | (0.0053) | (0.0066) | |

| South Africa | 0.0030 *** | 0.0023 | 0.0412 *** | −0.0086 ** | 0.0508 *** |

| (0.0004) | (0.0066) | (0.0234) | (0.0051) | (0.0224) | |

| Nigeria | 0.0024 *** | −0.0577 *** | −0.0770 ** | −0.0180 *** | −0.0262 |

| (0.0004) | (0.0132) | (0.0347) | (0.0073) | (0.0307) | |

| Columbia | 0.0011 *** | −0.0122 ** | 0.0153 | 0.0063 | 0.0281 |

| (0.0003) | (0.0085) | (0.0219) | (0.0058) | (0.0230) | |

| Vietnam | 0.0014 *** | 0.0078 | 0.0528 *** | 0.0047 | −0.0206 |

| (0.0003) | (0.0072) | (0.0189) | (0.0044) | (0.0185) |

| Inflation | Stock | Bitcoin | Gold | Oil | |

|---|---|---|---|---|---|

| Ukraine | 0.0006 *** | 0.0003 *** | 0.2324 * | 0.0024 | 0.0338 *** |

| (0.0002) | (0.0001) | (0.1222) | (0.0023) | (0.0012) | |

| Russia | 0.00021 ** | 0.0016 | 0.2283 ** | 0.0027 ** | 0.0339 *** |

| (0.00007) | (0.0010) | (0.1022) | (0.0011) | (0.0021) | |

| Singapore | 0.00032 * | 0.0019 | 0.2313 ** | 0.0027 ** | 0.0308 |

| (0.00019) | (0.0050) | (0.1120) | (0.0010) | (0.0230) | |

| Kenya | 0.00024 *** | 0.0021 ** | 0.1305 | 0.0028 | 0.0316 |

| (0.00010) | (0.0011) | (0.2990) | (0.0222) | (0.0231) | |

| United States | 0.00019 *** | 0.0038 *** | 0.2314 * | 0.0026 ** | 0.0181 |

| (0.00006) | (0.0012) | (0.1230) | (0.0012) | (0.0234) | |

| India | 0.00012 *** | 0.0031 | 0.3309 *** | 0.0028 | 0.0258 |

| (0.00004) | (0.0021) | (0.1129) | (0.0021) | (0.0192) | |

| South Africa | 0.00017 | 0.0023 ** | 0.2289 ** | 0.0024 | 0.0264 |

| (0.00012) | (0.0010) | (0.1122) | (0.0022) | (0.0222) | |

| Nigeria | 0.00021 *** | 0.0047 * | 0.2330 ** | 0.0035 * | 0.0257 ** |

| (0.0005) | (0.0023) | (0.1193) | (0.0019) | (0.0109) | |

| Columbia | 0.00010 | 0.0044 ** | 0.2292 *** | 0.0024 | 0.0323 |

| (0.0013) | (0.0019) | (0.0604) | (0.0020) | (0.0213) | |

| Vietnam | 0.00022 *** | 0.0044 *** | 0.1302 | 0.0027 | 0.0290 |

| (0.00014) | (0.0015) | (0.0909) | (0.0039) | (0.0211) |

| Inflation | Stock | Bitcoin | Gold | Oil | |

|---|---|---|---|---|---|

| Ukraine | 0.0004 *** | 0.0083 *** | 0.1401 *** | 0.0023 ** | 0.0067 *** |

| (0.0001) | (0.0021) | (0.0340) | (0.0010) | (0.0022) | |

| Russia | 0.00013 *** | 0.0024 | 0.1444 | 0.0023 | 0.0048 * |

| (0.00007) | (0.0020) | (0.1001) | (0.0022) | (0.0021) | |

| Singapore | 0.00021 *** | 0.0024 | 0.1702 *** | 0.0024 ** | 0.0040 |

| (0.00009) | (0.0023) | (0.0245) | (0.0011) | (0.0044) | |

| Kenya | 0.00023 | 0.0016 | 0.1572 ** | 0.0023 | 0.0034 *** |

| (0.00021) | (0.0011) | (0.0824) | (0.0034) | (0.0016) | |

| United States | 0.00016 *** | 0.0009 *** | 0.1128 *** | 0.0021 | 0.0057 |

| (0.00003) | (0.0003) | (0.0535) | (0.0020) | (0.0031) | |

| India | 0.00011 *** | 0.0016 | 0.1491 | 0.0023 ** | 0.0036 |

| (0.00005) | (0.0022) | (0.1002) | (0.0011) | (0.0030) | |

| South Africa | 0.00007 | 0.0011 *** | 0.1160 *** | 0.0021 | 0.0061 *** |

| (0.0002) | (0.0005) | (0.0245) | (0.0016) | (0.0022) | |

| Nigeria | 0.00015 *** | 0.0023 * | 0.1825 | 0.0028 *** | 0.0036 ** |

| (0.00006) | (0.0011) | (0.9234) | (0.0010) | (0.0017) | |

| Columbia | 0.00006 *** | 0.0014 *** | 0.1309 | 0.0021 ** | 0.0044 |

| (0.00002) | (0.0004) | (0.1092) | (0.0011) | (0.0053) | |

| Vietnam | 0.00017 | 0.0028 | 0.1338 *** | 0.0022 ** | 0.0035 |

| 0.00023 | (0.0022) | (0.0564) | (0.0012) | (0.0031) |

References

- Altissimo, F.; Benigno, P.; Palenzuela, D.R. Inflation differentials in a currency area: Facts, explanations and policy. Open Econ. Rev. 2011, 22, 189–233. [Google Scholar] [CrossRef]

- Tarbert, H. Is commercial property a hedge against inflation? A cointegration approach. J. Prop. Financ. 1996, 7, 77–98. [Google Scholar] [CrossRef]

- Aye, G.C.; Chang, T.; Gupta, R. Is gold an inflation-hedge? Evidence from an interrupted Markov-switching cointegration model. Resour. Policy 2016, 48, 77–84. [Google Scholar] [CrossRef] [Green Version]

- Van Hoang, T.H.; Lahiani, A.; Heller, D. Is gold a hedge against inflation? New evidence from a nonlinear ARDL approach. Econ. Model. 2016, 54, 54–66. [Google Scholar] [CrossRef] [PubMed]

- Kaponda, K. Bitcoin the’Digital Gold’and Its Regulatory Challenges. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3123531 (accessed on 1 February 2022). [CrossRef]

- Salisu, A.A.; Ndako, U.B.; Oloko, T.F. Assessing the inflation hedging of gold and palladium in OECD countries. Resour. Policy 2019, 62, 357–377. [Google Scholar] [CrossRef]

- Wang, K.M.; Lee, Y.M.; Thi, T.B.N. Time and place where gold acts as an inflation hedge: An application of long-run and short-run threshold model. Econ. Model. 2011, 28, 806–819. [Google Scholar] [CrossRef]

- Choi, S.; Shin, J. Bitcoin: An inflation hedge but not a safe haven. Financ. Res. Lett. 2021, 46, 102379. [Google Scholar] [CrossRef]

- Ciaian, P.; Rajcaniova, M.; Kancs, D.A. The economics of BitCoin price formation. Appl. Econ. 2016, 48, 1799–1815. [Google Scholar] [CrossRef] [Green Version]

- Fisher, I. Theory of Interest: As Determined by Impatience to Spend Income and Opportunity to Invest it; Augustusm Kelly Publishers: Wollongong, Australia, 1930. [Google Scholar]

- Bodie, Z. Common stocks as a hedge against inflation. J. Financ. 1976, 31, 459–470. [Google Scholar] [CrossRef]

- Fama, E.F.; Schwert, G.W. Asset returns and inflation. J. Financ. Econ. 1977, 5, 115–146. [Google Scholar] [CrossRef]

- Bekaert, G.; Wang, X. Inflation risk and the inflation risk premium. Econ. Policy 2010, 25, 755–806. [Google Scholar] [CrossRef]

- Salisu, A.A.; Raheem, I.D.; Ndako, U.B. The inflation hedging properties of gold, stocks and real estate: A comparative analysis. Resour. Policy 2020, 66, 101605. [Google Scholar] [CrossRef]

- Blau, B.M.; Griffith, T.G.; Whitby, R.J. Inflation and Bitcoin: A descriptive time-series analysis. Econ. Lett. 2021, 203, 109848. [Google Scholar] [CrossRef]

- Arnold, S.; Auer, B.R. What do scientists know about inflation hedging? N. Am. J. Econ. Financ. 2015, 34, 187–214. [Google Scholar] [CrossRef]

- Capie, F.; Mills, T.C.; Wood, G. Gold as a hedge against the dollar. J. Int. Financ. Mark. Inst. Money 2005, 15, 343–352. [Google Scholar] [CrossRef]

- Erb, C.B.; Harvey, C.R. The golden dilemma. Financ. Anal. J. 2013, 69, 10–42. [Google Scholar] [CrossRef]

- Ghosh, D.; Levin, E.J.; MacMillan, P.; Wright, R.E. Gold as an inflation hedge? Stud. Econ. Financ. 2004, 22, 1–25. [Google Scholar] [CrossRef] [Green Version]

- Levin, E.J.; Montagnoli, A.; Wright, R.E. Short-run and long-run determinants of the price of gold. World Gold Counc. Res. Study 2006, 32, 1–68. [Google Scholar]

- McCown, J.R.; Zimmerman, J.R. Is gold a zero-beta asset? Analysis of the investment potential of precious metals. Oklahoma City University Working Paper. SSRN Electron. J. 2006. [Google Scholar] [CrossRef]

- McCown, J.R.; Zimmerman, J.R. Analysis of the investment potential and inflation-hedging ability of precious metals. Oklahoma City University Working Paper. SSRN Electron. J. 2007. [Google Scholar] [CrossRef]

- Rubbaniy, G.; Lee, K.T.; Verschoor, W.F. Metal investments: Distrust killer or inflation hedging? In Proceedings of the 24th Australasian Finance and Banking Conference, Sydney, Australia, 14–16 December 2011. [Google Scholar]

- Worthington, A.C.; Pahlavani, M. Gold investment as an inflationary hedge: Cointegration evidence with allowance for endogenous structural breaks. Appl. Financ. Econ. Lett. 2007, 3, 259–262. [Google Scholar] [CrossRef] [Green Version]

- Baur, D.G. Explanatory mining for gold: Contrasting evidence from simple and multiple regressions. Resour. Policy 2011, 36, 265–275. [Google Scholar] [CrossRef]

- Blose, L.E. Gold prices, cost of carry, and expected inflation. J. Econ. Bus. 2010, 62, 35–47. [Google Scholar] [CrossRef]

- Brown, K.C.; Howe, J.S. On the use of gold as a fixed income security. Financ. Anal. J. 1987, 43, 73–76. [Google Scholar] [CrossRef]

- Mahdavi, S.; Zhou, S. Gold and commodity prices as leading indicators of inflation: Tests of long-run relationship and predictive performance. J. Econ. Bus. 1997, 49, 475–489. [Google Scholar] [CrossRef]

- Aye, G.C.; Carcel, H.; Gil-Alana, L.A.; Gupta, R. Does gold act as a hedge against inflation in the UK? Evidence from a fractional cointegration approach over 1257 to 2016. Resour. Policy 2017, 54, 53–57. [Google Scholar] [CrossRef]

- Batten, J.A.; Ciner, C.; Lucey, B.M. On the economic determinants of the gold–inflation relation. Resour. Policy 2014, 41, 101–108. [Google Scholar] [CrossRef]

- Beckmann, J.; Czudaj, R. Gold as an inflation hedge in a time-varying coefficient framework. N. Am. J. Econ. Financ. 2013, 24, 208–222. [Google Scholar] [CrossRef] [Green Version]

- Chua, J.; Woodward, R.S. Gold as an inflation hedge: A comparative study of six major industrial countries. J. Bus. Financ. Account. 1982, 9, 191–197. [Google Scholar] [CrossRef]

- Jaffe, J.F. Gold and gold stocks as investments for institutional portfolios. Financ. Anal. J. 1989, 45, 53–59. [Google Scholar] [CrossRef]

- Lucey, B.M.; Sharma, S.S.; Vigne, S.A. Gold and inflation (s)–A time-varying relationship. Econ. Model. 2017, 67, 88–101. [Google Scholar] [CrossRef] [Green Version]

- Shahzad, S.J.H.; Bouri, E.; Roubaud, D.; Kristoufek, L.; Lucey, B. Is Bitcoin a better safe-haven investment than gold and commodities? Int. Rev. Financ. Anal. 2019, 63, 322–330. [Google Scholar] [CrossRef]

- Taylor, N.J. Precious metals and inflation. Appl. Financ. Econ. 1998, 8, 201–210. [Google Scholar] [CrossRef]

- Adrangi, B.; Chatrath, A.; Raffiee, K. Economic activity, inflation, and hedging: The case of gold and silver investments. J. Wealth Manag. 2003, 6, 60–77. [Google Scholar] [CrossRef]

- Gupta, P.; Goyal, A. Impact of oil price fluctuations on Indian economy. OPEC Energy Rev. 2015, 39, 141–161. [Google Scholar] [CrossRef]

- Hijazine, R.; Al-Assaf, G. The effect of oil prices on headline and core inflation in Jordan. OPEC Energy Rev. 2022. [Google Scholar] [CrossRef]

- Zaremba, A.; Umar, Z.; Mikutowski, M. Inflation hedging with commodities: A wavelet analysis of seven centuries worth of data. Econ. Lett. 2019, 181, 90–94. [Google Scholar] [CrossRef]

- Gultekin, N.B. Stock market returns and inflation: Evidence from other countries. J. Financ. 1983, 38, 49–65. [Google Scholar] [CrossRef]

- Jaffe, J.F.; Mandelker, G. The” Fisher effect” for risky assets: An empirical investigation. J. Financ. 1976, 31, 447–458. [Google Scholar] [CrossRef]

- Luintel, K.B.; Paudyal, K. Are common stocks a hedge against inflation? J. Financ. Res. 2006, 29, 1–19. [Google Scholar] [CrossRef]

- Nelson, C.R.; Schwert, G.W. Short-term interest rates as predictors of inflation: On testing the hypothesis that the real rate of interest is constant. Am. Econ. Rev. 1977, 67, 478–486. [Google Scholar]

- Rödel, M.G. Inflation Hedging. An Empirical Analysis on Inflation Nonlinearities, Infrastructure, and International Equities. Ph.D. Thesis, Technical University of Munich, Munich, Germany, 2012. [Google Scholar]

- Rödel, M.G. Inflation hedging with international equities. J. Portf. Manag. 2014, 40, 41–53. [Google Scholar] [CrossRef]

- Schotman, P.C.; Schweitzer, M. Horizon sensitivity of the inflation hedge of stocks. J. Empir. Financ. 2000, 7, 301–315. [Google Scholar] [CrossRef]

- Hoesli, M.; Lizieri, C.; MacGregor, B. The inflation hedging characteristics of US and UK investments: A multi-factor error correction approach. J. Real Estate Financ. Econ. 2008, 36, 183–206. [Google Scholar] [CrossRef] [Green Version]

- Simpson, M.W.; Ramchander, S.; Webb, J.R. The asymmetric response of equity REIT returns to inflation. J. Real Estate Financ. Econ. 2007, 34, 513–529. [Google Scholar] [CrossRef]

- Bouri, E.; Molnár, P.; Azzi, G.; Roubaud, D.; Hagfors, L.I. On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier? Financ. Res. Lett. 2017, 20, 192–198. [Google Scholar] [CrossRef]

- Bouri, E.; Gupta, R.; Tiwari, A.K.; Roubaud, D. Does Bitcoin hedge global uncertainty? Evidence from wavelet-based quantile-in-quantile regressions. Financ. Res. Lett. 2017, 23, 87–95. [Google Scholar] [CrossRef] [Green Version]

- Corbet, S.; Meegan, A.; Larkin, C.; Lucey, B.; Yarovaya, L. Exploring the dynamic relationships between cryptocurrencies and other financial assets. Econ. Lett. 2018, 165, 28–34. [Google Scholar] [CrossRef] [Green Version]

- Dyhrberg, A.H. Hedging capabilities of bitcoin. Is it the virtual gold? Financ. Res. Lett. 2016, 16, 139–144. [Google Scholar] [CrossRef] [Green Version]

- Huynh, T.L.D.; Ahmed, R.; Nasir, M.A.; Shahbaz, M.; Huynh, N.Q.A. The nexus between black and digital gold: Evidence from US markets. Ann. Oper. Res. 2021, 1–26. [Google Scholar] [CrossRef]

- Selmi, R.; Mensi, W.; Hammoudeh, S.; Bouoiyour, J. Is Bitcoin a hedge, a safe haven or a diversifier for oil price movements? A comparison with gold. Energy Econ. 2018, 74, 787–801. [Google Scholar] [CrossRef]

- Taskinsoy, J. Bitcoin Nation: The World’s New 17th Largest Economy. Available online: https://www.researchgate.net/publication/349669164_Bitcoin_Nation_The_World%27s_New_17th_Largest_Economy (accessed on 1 February 2022). [CrossRef]

- Matkovskyy, R.; Jalan, A. Bitcoin vs Inflation: Can Bitcoin Be a Macro Hedge? Evidence From a Quantile-on-Quantile Model. SSRN Electron. J. 2020, 7, 1021–1039. [Google Scholar] [CrossRef]

- Smales, L.A. Cryptocurrency as an Alternative Inflation Hedge? 2021. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3883123 (accessed on 20 November 2021).

- Conlon, T.; Corbet, S.; McGee, R.J. Inflation and cryptocurrencies revisited: A time-scale analysis. Econ. Lett. 2021, 206, 109996. [Google Scholar] [CrossRef]

- Ghazali, M.F.; Lean, H.H.; Bahari, Z. Is gold a good hedge against inflation? Empirical evidence in Malaysia. J. Malays. Stud. 2015, 33, 69–84. [Google Scholar]

- Le Long, H.; De Ceuster, M.J.; Annaert, J.; Amonhaemanon, D. Gold as a hedge against inflation: The Vietnamese case. Procedia Econ. Financ. 2013, 5, 502–511. [Google Scholar] [CrossRef] [Green Version]

- Maneejuk, P.; Pirabun, N.; Singjai, S.; Yamaka, W. Currency Hedging Strategies Using Histogram-Valued Data: Bivariate Markov Switching GARCH Models. Mathematics 2021, 9, 2773. [Google Scholar] [CrossRef]

- Kim, J.H.; Ryoo, H.H. Common stocks as a hedge against inflation: Evidence from century-long US data. Econ. Lett. 2011, 113, 168–171. [Google Scholar] [CrossRef]

- Ihle, R.; von Cramon-Taubadel, S. A comparison of threshold cointegration and Markov-switching vector error correction models in price transmission analysis (No. 1314-2016-102645). In Proceedings of the 2008 NCCC-134 Conference on Applied Commodity Price Analysis, Forecasting, and Market Risk Management, St. Louis, MI, USA, 21–22 April 2008. [Google Scholar]

- Hondroyiannis, G.; Papapetrou, E. Stock returns and inflation in Greece: A Markov switching approach. Rev. Financ. Econ. 2006, 15, 76–94. [Google Scholar] [CrossRef]

- Krolzig, H.M. The markov-switching vector autoregressive model. In Markov-Switching Vector Autoregressions; Springer: Berlin/Heidelberg, Germany, 1997; pp. 6–28. [Google Scholar]

- Hamilton, J.D. A new approach to the economic analysis of nonstationary time series and the business cycle. Econom. J. Econom. Soc. 1989, 57, 357–384. [Google Scholar] [CrossRef]

- Shi, S.P. Specification sensitivities in the Markov-switching unit root test for bubbles. Empir. Econ. 2013, 45, 697–713. [Google Scholar] [CrossRef]

- Hall, S.G.; Psaradakis, Z.; Sola, M. Detecting periodically collapsing bubbles: A Markov-switching unit root test. J. Appl. Econom. 1999, 14, 143–154. [Google Scholar] [CrossRef]

- Alamgir, F.; Amin, S.B. The nexus between oil price and stock market: Evidence from South Asia. Energy Rep. 2021, 7, 693–703. [Google Scholar] [CrossRef]

- Grigoli, F.; Herman, A.; Swiston, M.A.J. A Crude Shock: Explaining the Impact of the 2014–2016 Oil Price Decline Across Exporters. Int. Monet. Fund 2017, 2017, 3–25. [Google Scholar] [CrossRef]

- Hansen, B.E. Erratum: The likelihood ratio test under nonstandard conditions: Testing the Markov switching model of GNP. J. Appl. Econom. 1996, 11, 195–198. [Google Scholar] [CrossRef] [Green Version]

- Anas, J.; Ferrara, L. Detecting cyclical turning points: The ABCD approach and two probabilistic indicators. J. Bus. Cycle Meas. Anal. 2004, 2004, 193–225. [Google Scholar] [CrossRef]

- Artis, M.; Krolzig, H.M.; Toro, J. The European business cycle. Oxf. Econ. Pap. 2004, 56, 1–44. [Google Scholar] [CrossRef] [Green Version]

- Stocker, M.; Baffes, J.; Some, Y.M.; Vorisek, D.; Wheeler, C.M. The 2014-16 oil price collapse in retrospect: Sources and implications. World Bank Policy Res. Work. Pap. 2018, 1, 8419. [Google Scholar]

- Chong, T.T.L.; Li, X. Understanding the China–US trade war: Causes, economic impact, and the worst-case scenario. Econ. Political Stud. 2019, 7, 185–202. [Google Scholar] [CrossRef]

- Bampinas, G.; Panagiotidis, T. Are gold and silver a hedge against inflation? A two century perspective. Int. Rev. Financ. Anal. 2015, 41, 267–276. [Google Scholar] [CrossRef] [Green Version]

- Ehrmann, M.; Ellison, M.; Valla, N. Regime-dependent impulse response functions in a Markov-switching vector autoregression model. Econ. Lett. 2003, 78, 295–299. [Google Scholar] [CrossRef] [Green Version]

- Ivanov, S.I. A study of perfect hedges. Int. J. Financ. Stud. 2017, 5, 28. [Google Scholar] [CrossRef] [Green Version]

- Pastpipatkul, P.; Yamaka, W.; Sriboonchitta, S. Effect of quantitative easing on ASEAN-5 financial markets. In Causal Inference in Econometrics; Springer: Cham, Switzerland, 2016; pp. 525–543. [Google Scholar]

| Country | MEAN | MEDIAN | MAX | MIN | STD | MS-ADF Test | |

|---|---|---|---|---|---|---|---|

| Inflation rate | |||||||

| Ukraine | 0.008 | 0.005 | 0.131 | −0.013 | 0.017 | −3.211 * | −5.093 * |

| Russia | 0.005 | 0.004 | 0.037 | −0.005 | 0.005 | −3.224 * | −4.092 * |

| Singapore | 0.001 | 0.000 | 0.016 | −0.014 | 0.004 | −4.664 ** | −3.009 * |

| Kenya | 0.005 | 0.006 | 0.031 | −0.012 | 0.006 | −7.323 *** | −6.039 *** |

| United States | 0.001 | 0.001 | 0.009 | −0.006 | 0.003 | −8.224 *** | −4.003 * |

| India | 0.004 | 0.005 | 0.022 | −0.016 | 0.007 | −3.834 * | −4.339 ** |

| South Africa | 0.004 | 0.003 | 0.013 | −0.006 | 0.003 | −3.290 * | −4.983 ** |

| Nigeria | 0.009 | 0.008 | 0.032 | −0.005 | 0.005 | −2.904 * | −3.053 * |

| Columbia | 0.003 | 0.002 | 0.012 | −0.003 | 0.003 | −4.934 ** | −2.808 * |

| Vietnam | 0.004 | 0.002 | 0.032 | −0.015 | 0.006 | −3.485 * | −5.094 *** |

| Stock return | |||||||

| Ukraine | −0.033 | −0.005 | 0.290 | −0.274 | 0.073 | −8.009 *** | −4.035 * |

| Russia | 0.074 | 0.111 | 0.165 | −0.123 | 0.048 | −10.932 *** | −9.092 *** |

| Singapore | 0.022 | −0.007 | 0.181 | −0.153 | 0.047 | −5.930 ** | −7.033 *** |

| Kenya | −0.069 | 0.003 | 0.086 | −0.172 | 0.046 | −5.709 ** | 3.902 * |

| United States | 0.104 | 0.161 | 0.191 | −0.133 | 0.038 | −3.779 * | −4.024 * |

| India | 0.079 | 0.072 | 0.134 | −0.262 | 0.051 | −4.092 ** | −6.066 *** |

| South Africa | 0.072 | 0.054 | 0.129 | −0.118 | 0.040 | −6.093 *** | −5.210 ** |

| Nigeria | 0.033 | 0.025 | 0.151 | −0.240 | 0.065 | −5.110 *** | −3.992 * |

| Columbia | −0.018 | −0.011 | 0.133 | −0.321 | 0.051 | −6.035 *** | −9.003 *** |

| Vietnam | 0.075 | 0.101 | 0.149 | −0.286 | 0.060 | −9.093 *** | 4.930 * |

| Bitcoin return | −4.024 * | ||||||

| 0.103 | 0.069 | 1.740 | −0.492 | 0.329 | −4.094 ** | −5.093 * | |

| Gold return | |||||||

| 0.002 | 0.000 | 0.110 | −0.120 | 0.046 | −6.903 *** | −9.094 *** | |

| Oil return | |||||||

| −0.001 | 0.009 | 0.413 | −0.844 | 0.149 | −6.003 *** | −7.002 *** | |

| Country | RCM | |

|---|---|---|

| Ukraine | 3.948 (0.000) | 6.935 |

| Russia | 4.934 (0.000) | 3.450 |

| Singapore | 5.309 (0.000) | 4.092 |

| Kenya | 3.829 (0.000) | 3.994 |

| United States | 5.320 (0.000) | 19.934 |

| India | 4.204 (0.000) | 4.220 |

| South Africa | 3.094 (0.000) | 18.988 |

| Nigeria | 5.009 (0.000) | 3.082 |

| Columbia | 3.942 (0.000) | 22.093 |

| Vietnam | 4.492 (0.000) | 6.092 |

| Stock | Bitcoin | Gold | Oil | |

|---|---|---|---|---|

| −0.2427 | −0.4249 | 0.1210 | 0.1376 | |

| (0.4710) | (1.9328) | (0.2483) | (0.4224) | |

| 2.1584 | 0.3052 | 0.9007 | 0.4934 | |

| (0.8836) | (0.8993) | (0.8754) | (1.2599) | |

| −0.8111 | 5.5039 | 1.7141 | 0.1820 | |

| (1.0485) | (8.8383) | (1.0452) | (1.3510) | |

| −0.3131 | 4.6202 | −0.4173 | −1.7791 ** | |

| (0.5400) | (5.3136) | (0.6360) | (0.7840) | |

| −1.2187 | 1.2030 * | −0.9157 | 1.4763 | |

| (0.9542) | (0.4307) | (1.4884) | (2.4430) | |

| −2.2289 *** | 2.5906 | −0.0944 | −0.9876 | |

| (0.5203) | (4.9780) | (0.6233) | (0.7750) | |

| −0.2663 | 5.2000 | 1.3556 | 2.4950 | |

| (0.8172) | (8.3766) | (1.1155) | (1.9136) | |

| 0.6280 | 0.9860 | 0.0233 | 1.4601 *** | |

| (0.8632) | (7.6412) | (0.9397) | (0.7239) | |

| −1.0369 | −13.2560 | 0.2121 | −1.5244 | |

| (1.0822) | (10.5439) | (1.3322) | (1.9283) | |

| −0.4004 | 1.5993 *** | 0.8820 | −0.2940 | |

| (0.7963) | (0.4808) | (0.6977) | (0.8869) |

| Stock | Bitcoin | Gold | Oil | |

|---|---|---|---|---|

| 1.6456 *** | 1.0261 *** | −1.1287 *** | 1.0160 *** | |

| (0.0927) | (0.1298) | (0.1903) | (0.1488) | |

| −1.1493 | 0.0102 | 0.1129 | 3.9073 | |

| (0.7368) | (3.0527) | (0.7541) | (3.3443) | |

| 0.9129 | −6.0139 | 0.5217 | −1.2100 | |

| (0.9292) | (3.7880) | (0.8945) | (3.7585) | |

| −0.9139 | 5.5916 ** | −0.3277 | 0.9669 * | |

| (0.6079) | (2.3422) | (0.5651) | (0.3829) | |

| −1.7553 *** | −1.9102 *** | 0.5243 *** | −0.4122 *** | |

| (0.7070) | (0.7123) | (0.2834) | (0.1423) | |

| 2.0196 *** | 0.4431 ** | −0.3446 | 3.0550 | |

| (0.7133) | (0.2677) | (0.5437) | (2.0699) | |

| −2.3536 ** | −6.3658 | −0.5741 | −1.5535 *** | |

| (1.1803) | (4.1833) | (0.9097) | (0.4987) | |

| 0.2304 *** | 1.5128 *** | 1.9811 *** | 1.6199 | |

| (0.1012) | (0.2475) | (0.6820) | (2.8697) | |

| 0.5433 | 0.8609 | 2.1088 | −1.6255 *** | |

| (1.9297) | (4.9769) | (1.3106) | (0.3400) | |

| −1.6793 * | −0.5713 ** | −0.5945 | −0.6735 *** | |

| (0.9958) | (0.1040) | (0.6110) | (0.1533) |

| Regime 1 | ||||||||

|---|---|---|---|---|---|---|---|---|

| MS-VAR’s Coefficients (Long-Run) | MS-VAR’s Impulse Response (Short-Run) | |||||||

| Stock | BTC | Gold | Oil | Stock | BTC | Gold | Oil | |

| Ukraine | + − | − + | − + | + | ||||

| Russia | + | + | − + | − | ||||

| Singapore | − | + | + − | − | ||||

| Kenya | − | + | + − | + − | ||||

| United States | √ | + − + | − + | + − | + | |||

| India | + − | + | − | − | ||||

| South Africa | + | + | + | + | ||||

| Nigeria | √ | − + | + | + − + | − + | |||

| Colombia | − | + − | − + | + − | ||||

| Vietnam | √ | + − | + | + | + − | |||

| No. of evidence “+” | 0 | 2 | 0 | 1 | 2 | 7 | 2 | 3 |

| Regime 2 | ||||||||

| MS-VAR’s coefficients (Long-run) | MS-VAR’s Impulse Response (Short-run) | |||||||

| Stock | BTC | Gold | Oil | Stock | BTC | Gold | Oil | |

| Ukraine | √ | √ | √ | + | − + | − + | − + | |

| Russia | − + | + | − + | − + | ||||

| Singapore | + − | − + | − | + | ||||

| Kenya | √ | √ | − | + | + | − + | ||

| United States | √ | + − + | + − | + − + | + − | |||

| India | √ | √ | + | + | + − | + | ||

| South Africa | − + | + − | + − | − + | ||||

| Nigeria | √ | √ | √ | + | + | − + | + | |

| Colombia | + − | − | + | − | ||||

| Vietnam | + − | + | − + | + − | ||||

| No. of evidence “+” | 3 | 4 | 2 | 2 | 3 | 5 | 2 | 3 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Phochanachan, P.; Pirabun, N.; Leurcharusmee, S.; Yamaka, W. Do Bitcoin and Traditional Financial Assets Act as an Inflation Hedge during Stable and Turbulent Markets? Evidence from High Cryptocurrency Adoption Countries. Axioms 2022, 11, 339. https://doi.org/10.3390/axioms11070339

Phochanachan P, Pirabun N, Leurcharusmee S, Yamaka W. Do Bitcoin and Traditional Financial Assets Act as an Inflation Hedge during Stable and Turbulent Markets? Evidence from High Cryptocurrency Adoption Countries. Axioms. 2022; 11(7):339. https://doi.org/10.3390/axioms11070339

Chicago/Turabian StylePhochanachan, Panisara, Nootchanat Pirabun, Supanika Leurcharusmee, and Woraphon Yamaka. 2022. "Do Bitcoin and Traditional Financial Assets Act as an Inflation Hedge during Stable and Turbulent Markets? Evidence from High Cryptocurrency Adoption Countries" Axioms 11, no. 7: 339. https://doi.org/10.3390/axioms11070339

APA StylePhochanachan, P., Pirabun, N., Leurcharusmee, S., & Yamaka, W. (2022). Do Bitcoin and Traditional Financial Assets Act as an Inflation Hedge during Stable and Turbulent Markets? Evidence from High Cryptocurrency Adoption Countries. Axioms, 11(7), 339. https://doi.org/10.3390/axioms11070339