Uncovering the Impact of Local and Global Interests in Artists on Stock Prices of K-Pop Entertainment Companies: A SHAP-XGBoost Analysis

Abstract

:1. Introduction

2. Literature Review

2.1. Social Network Service Data

2.2. Entertainment Stock

2.3. XAI

3. Methods

3.1. Extreme Gradient Boosting (XGBoost)

3.2. Shapley Value

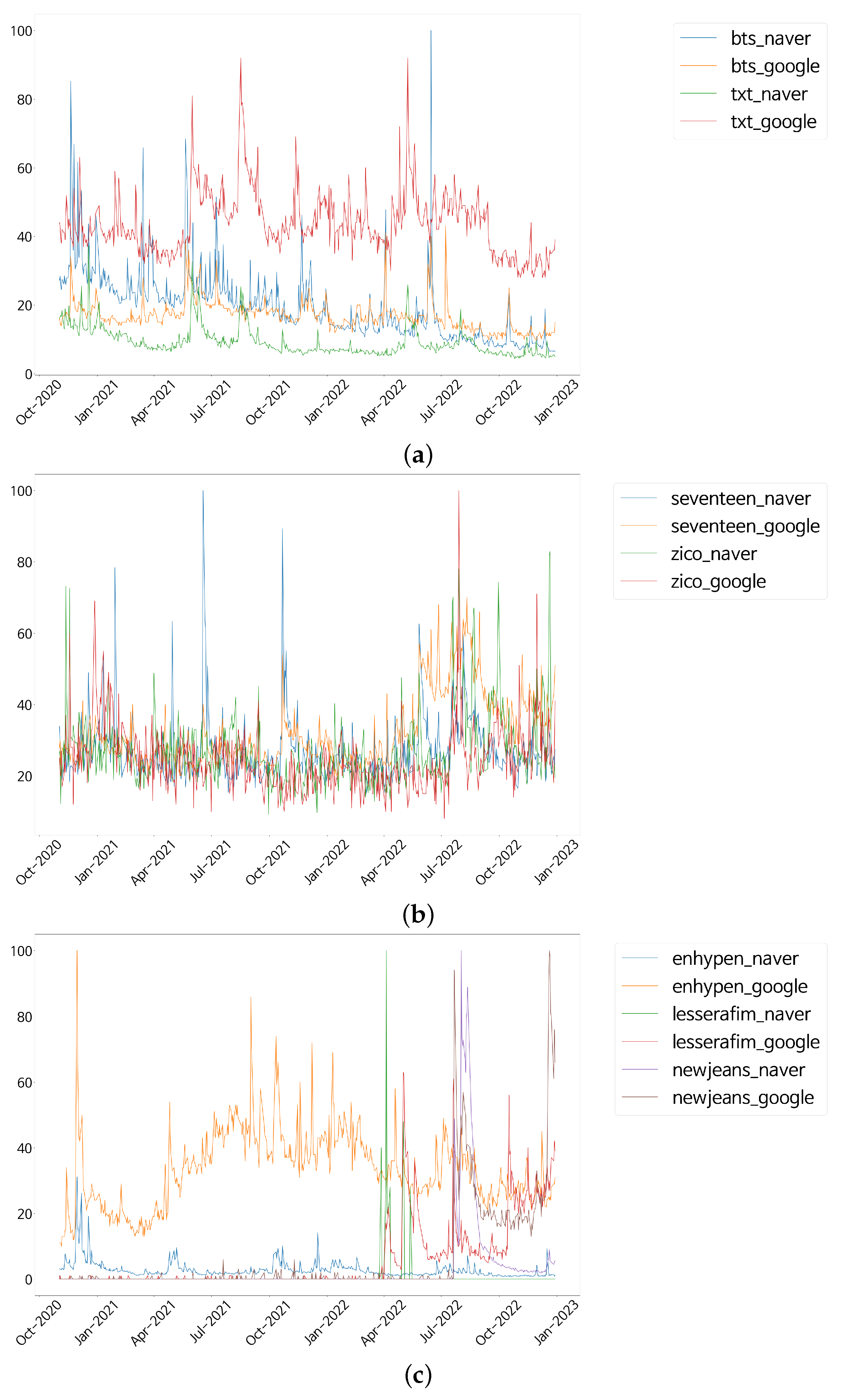

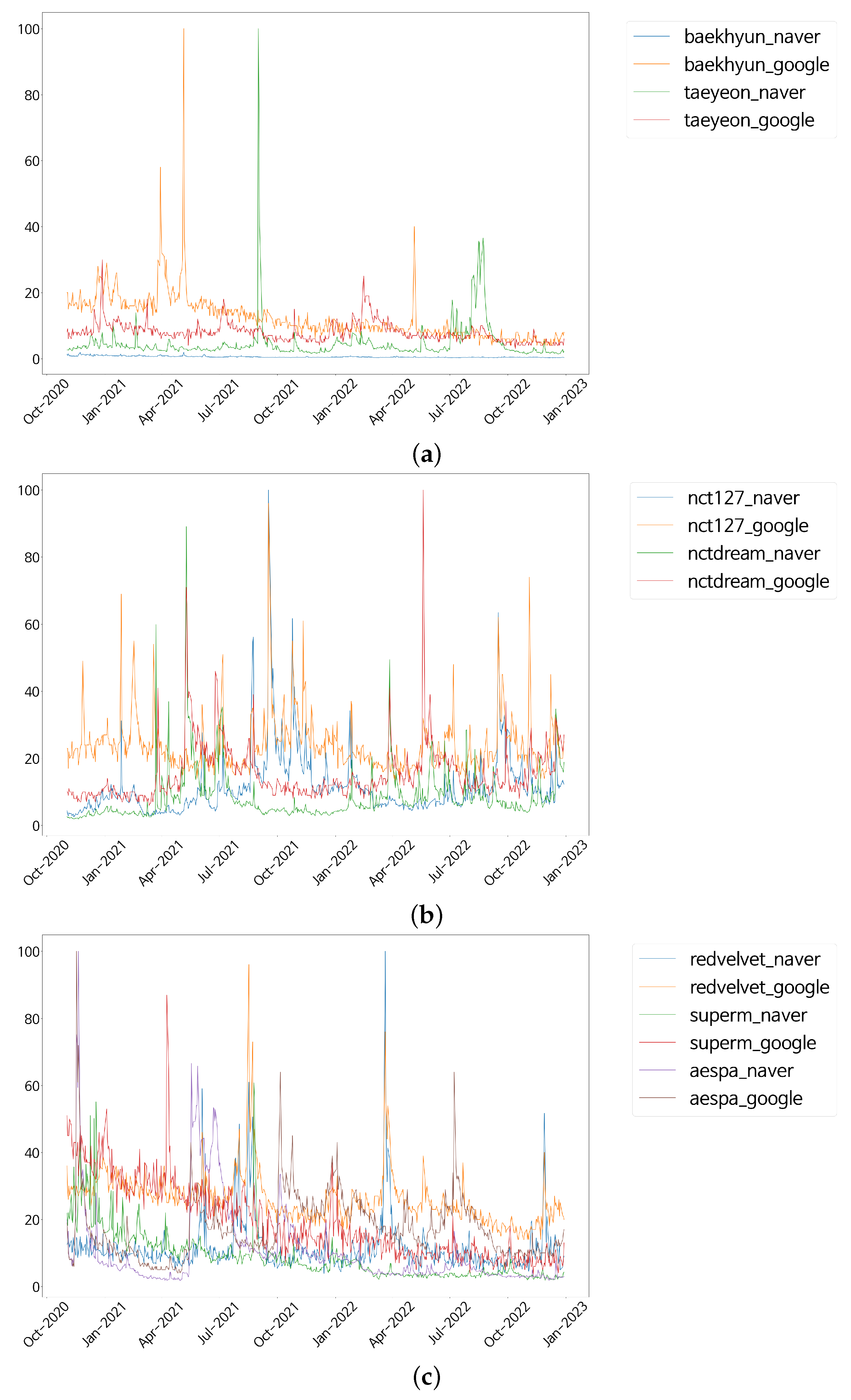

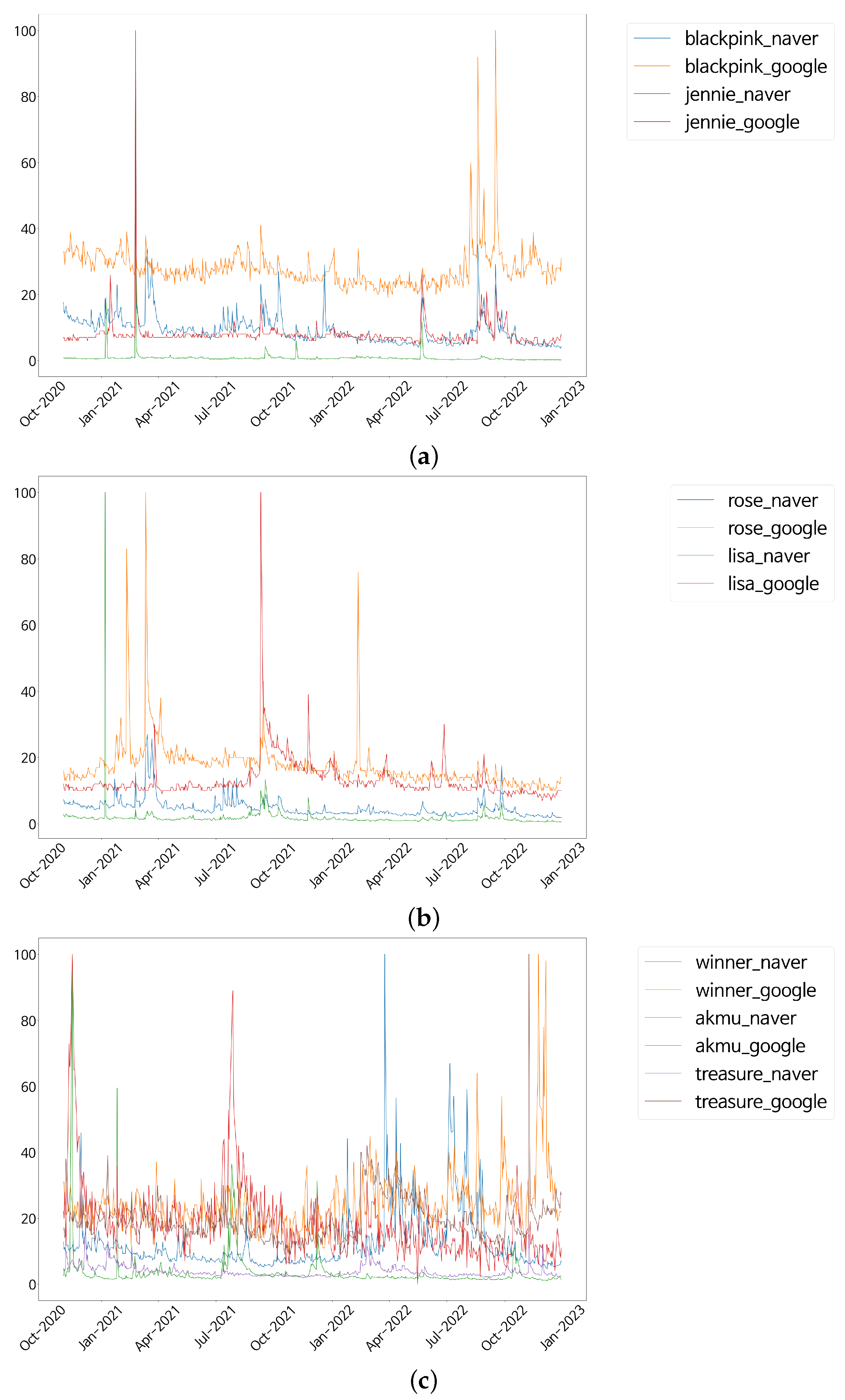

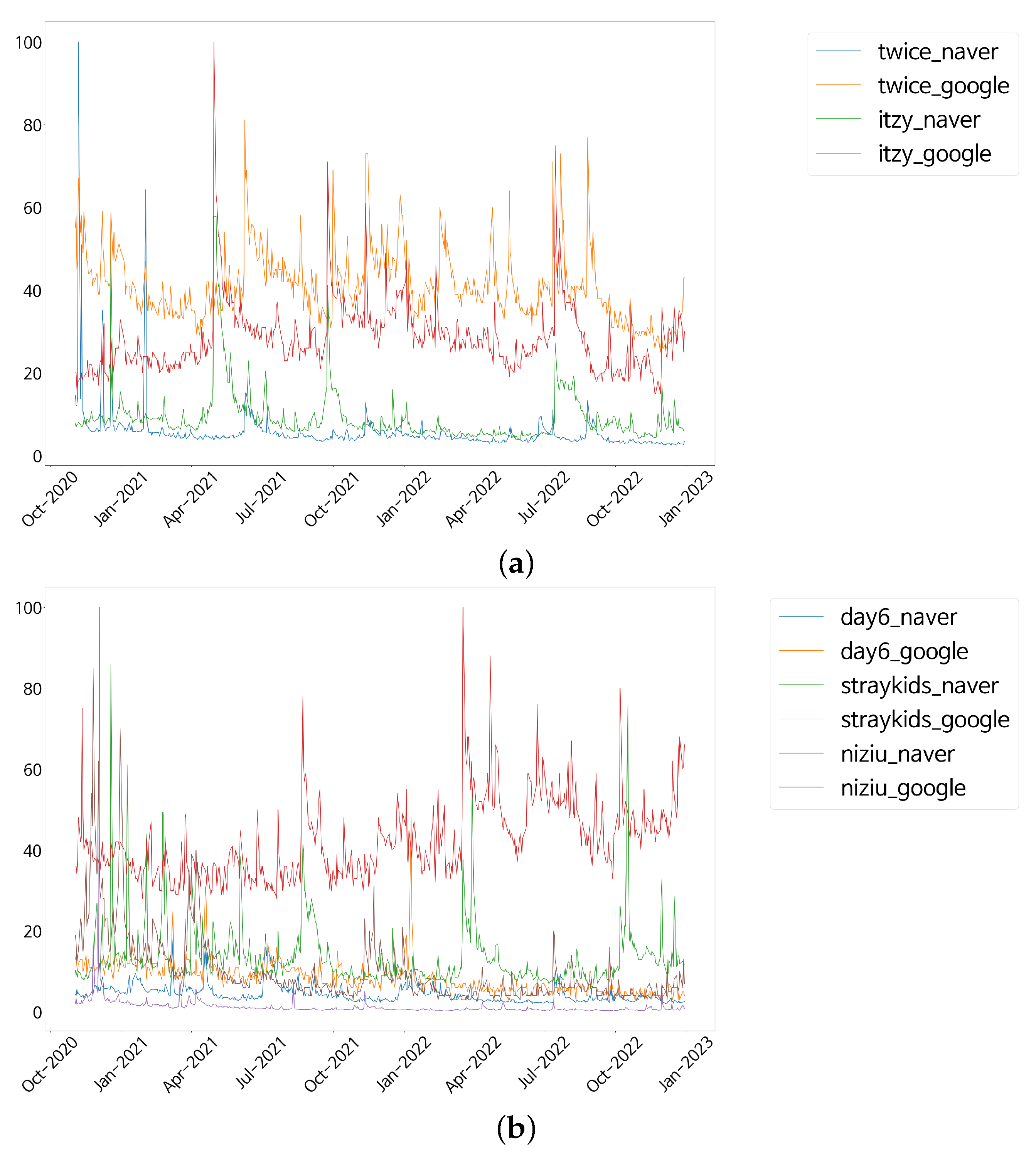

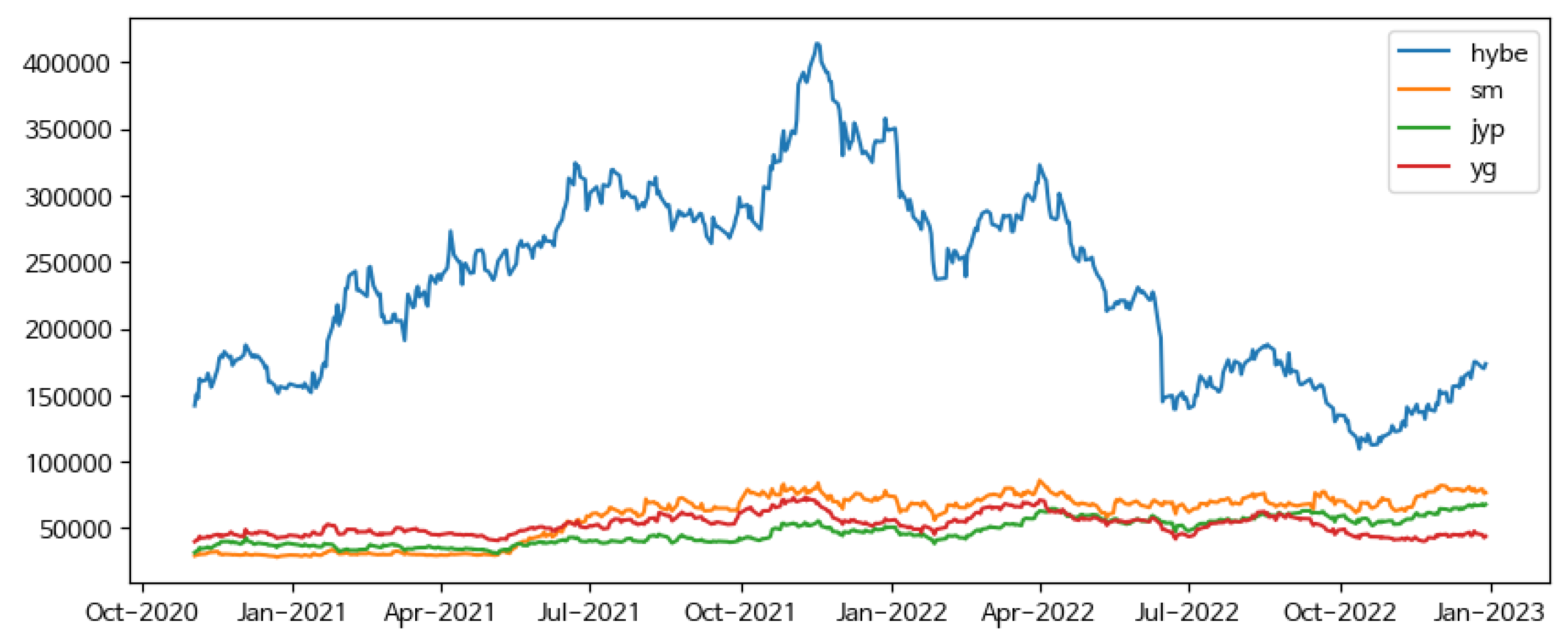

4. Data Description

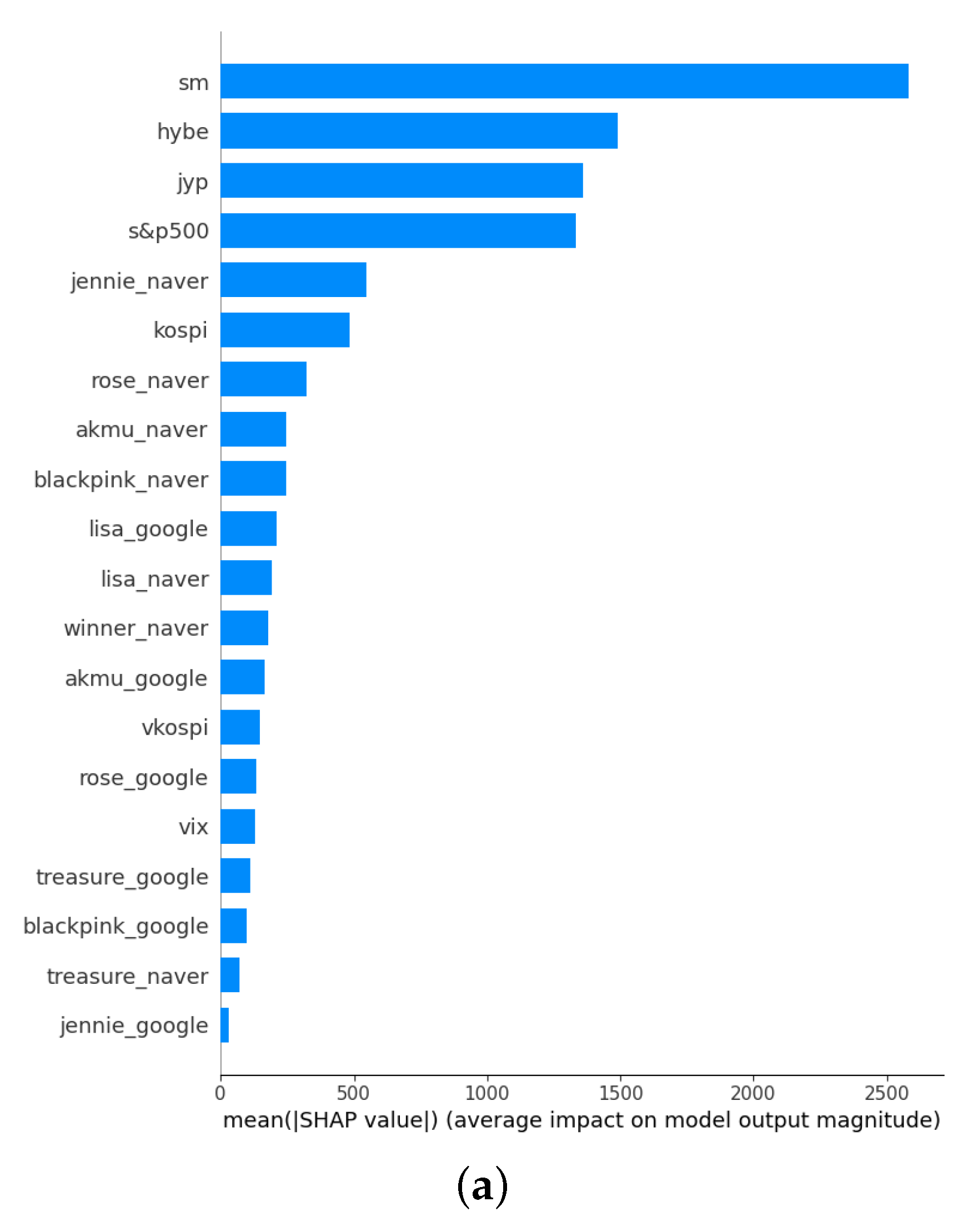

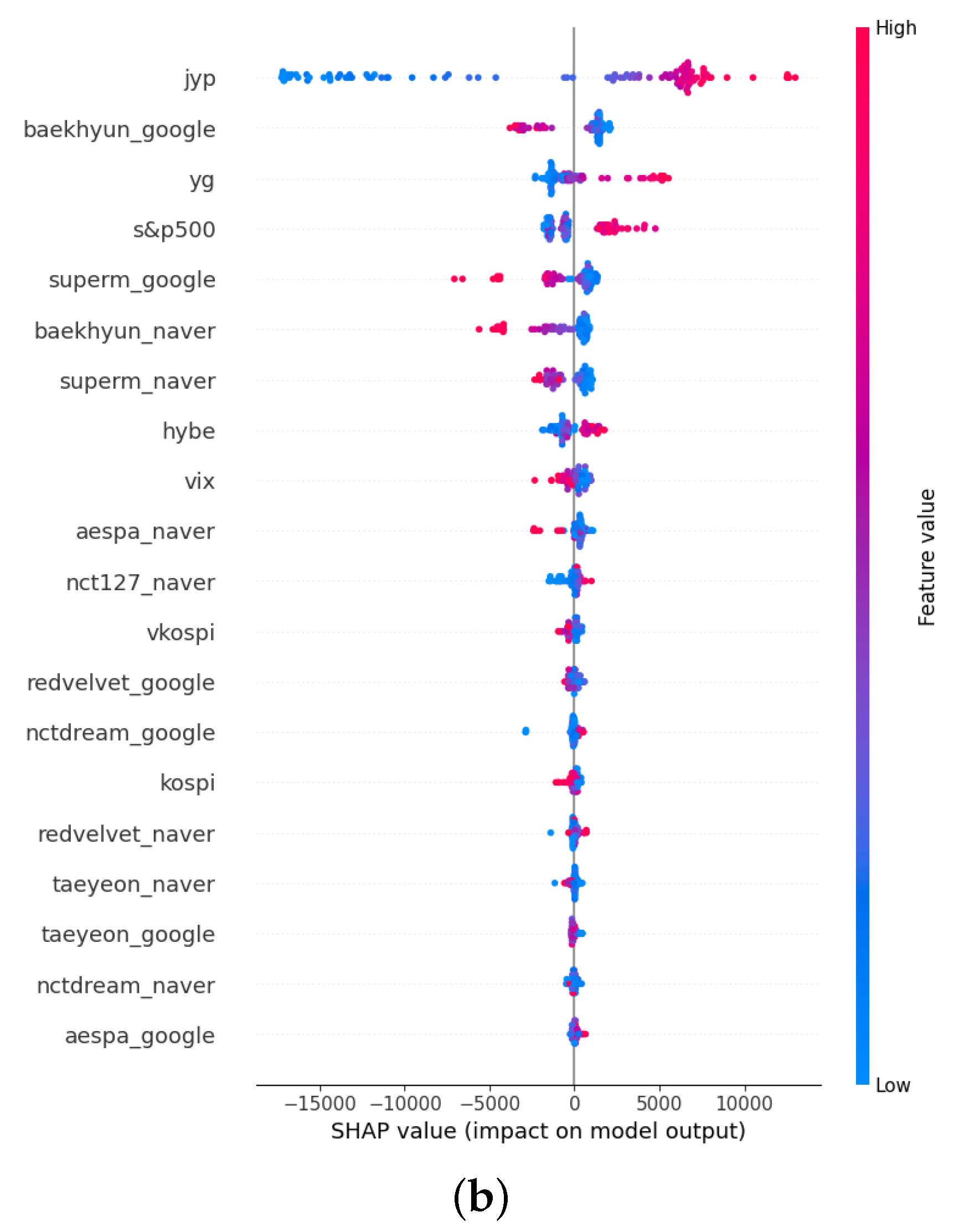

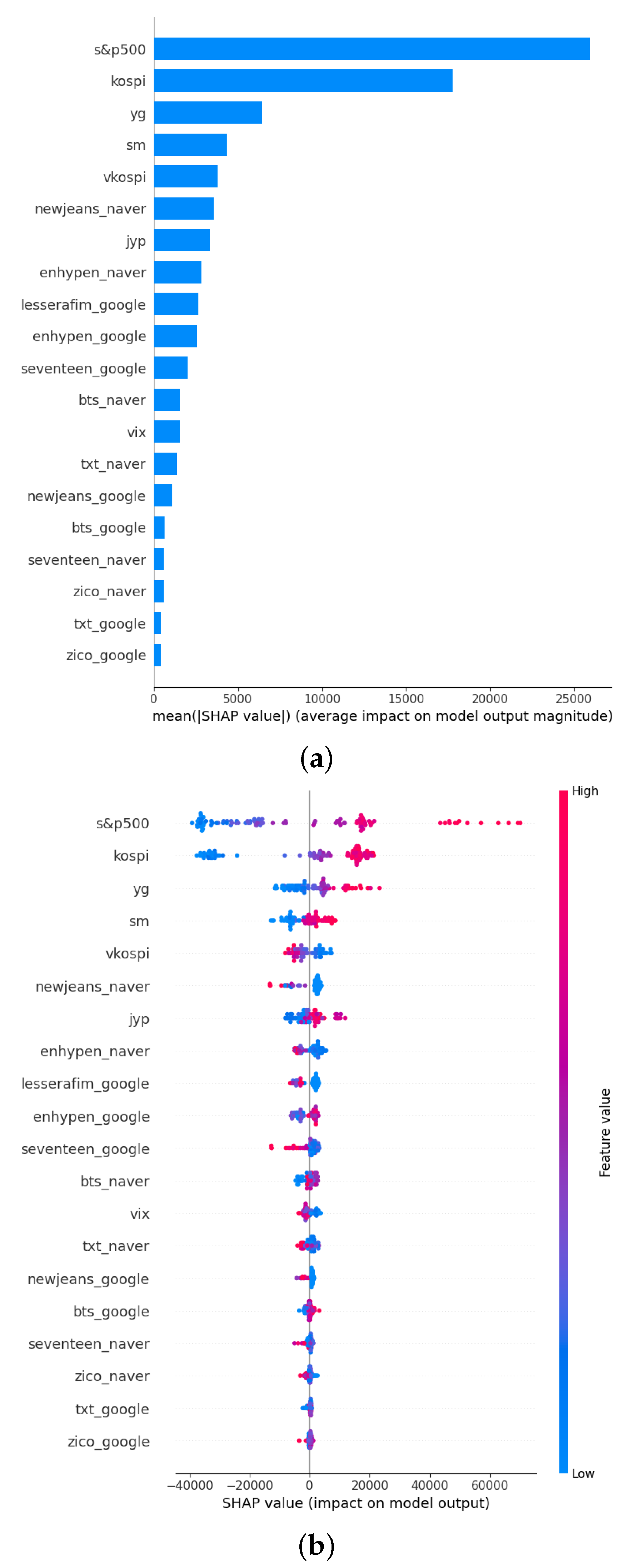

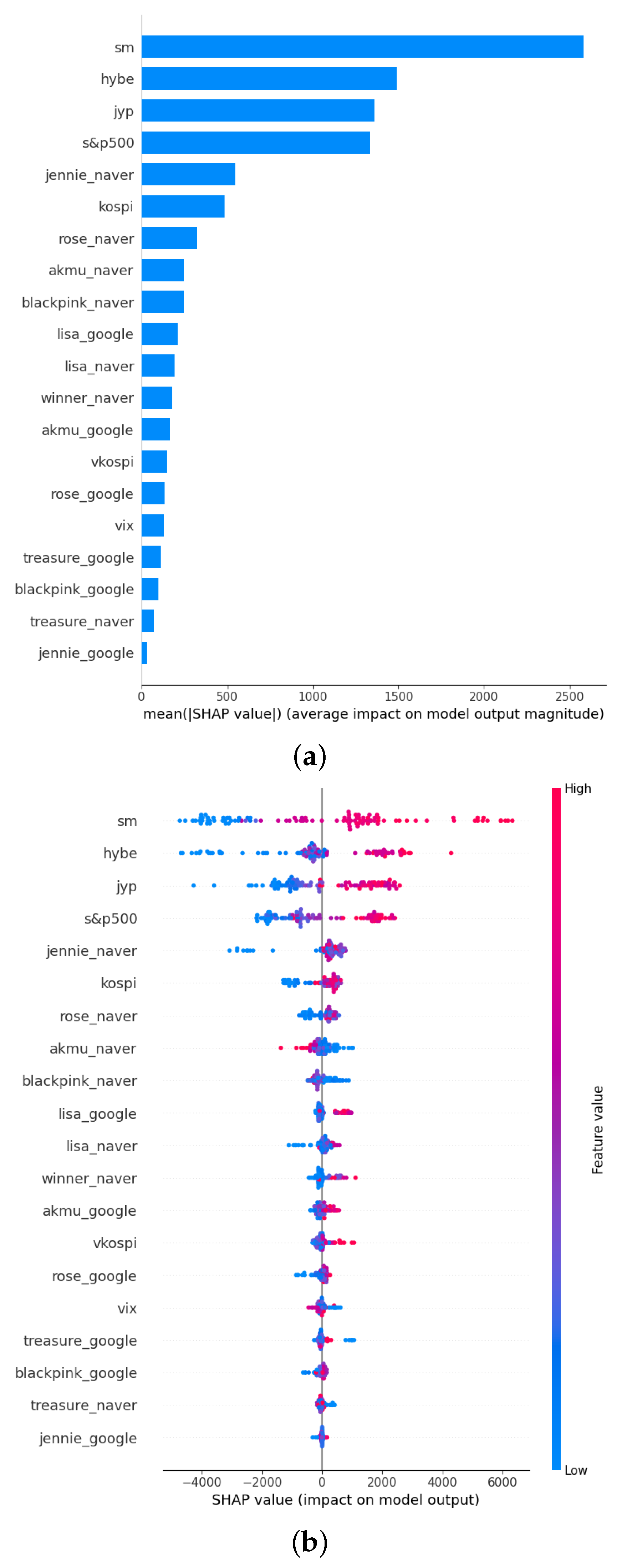

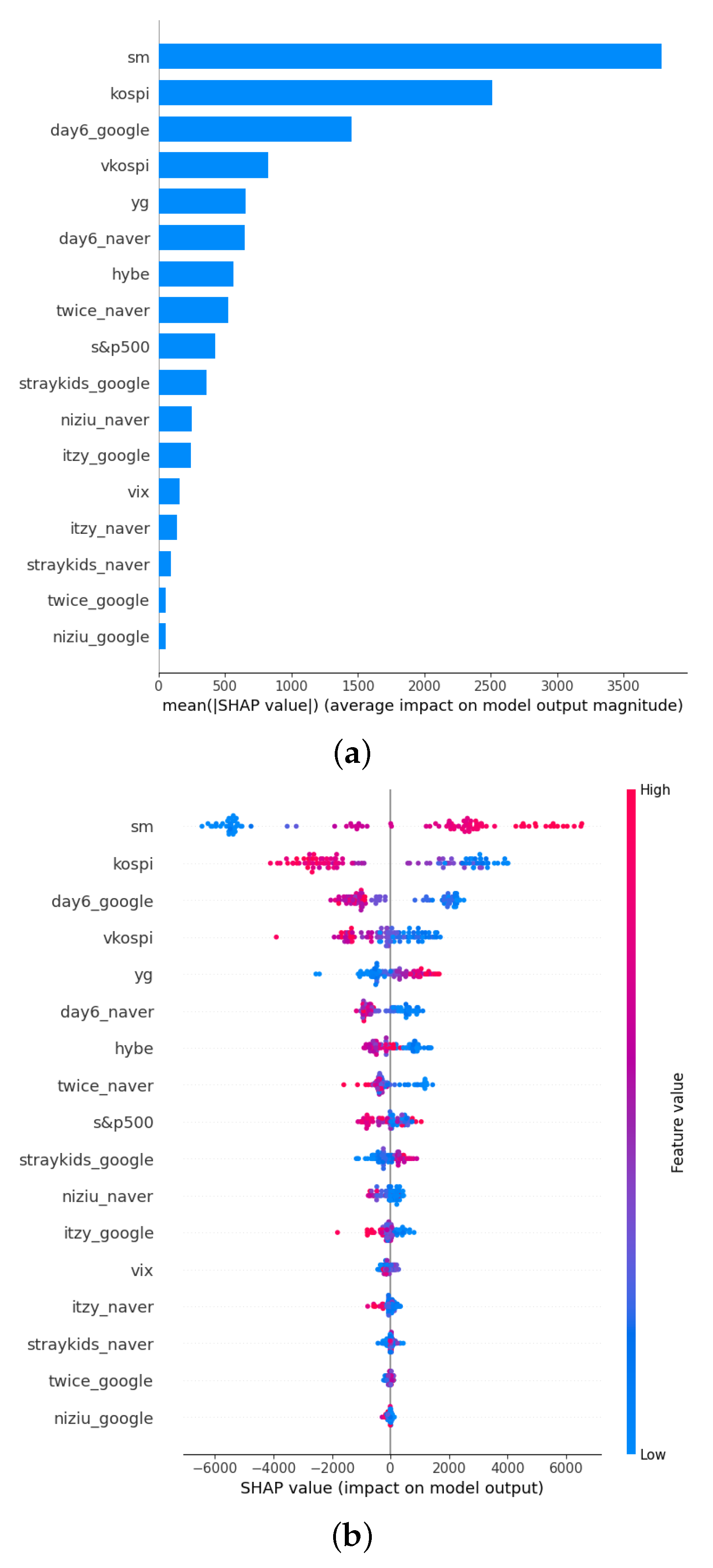

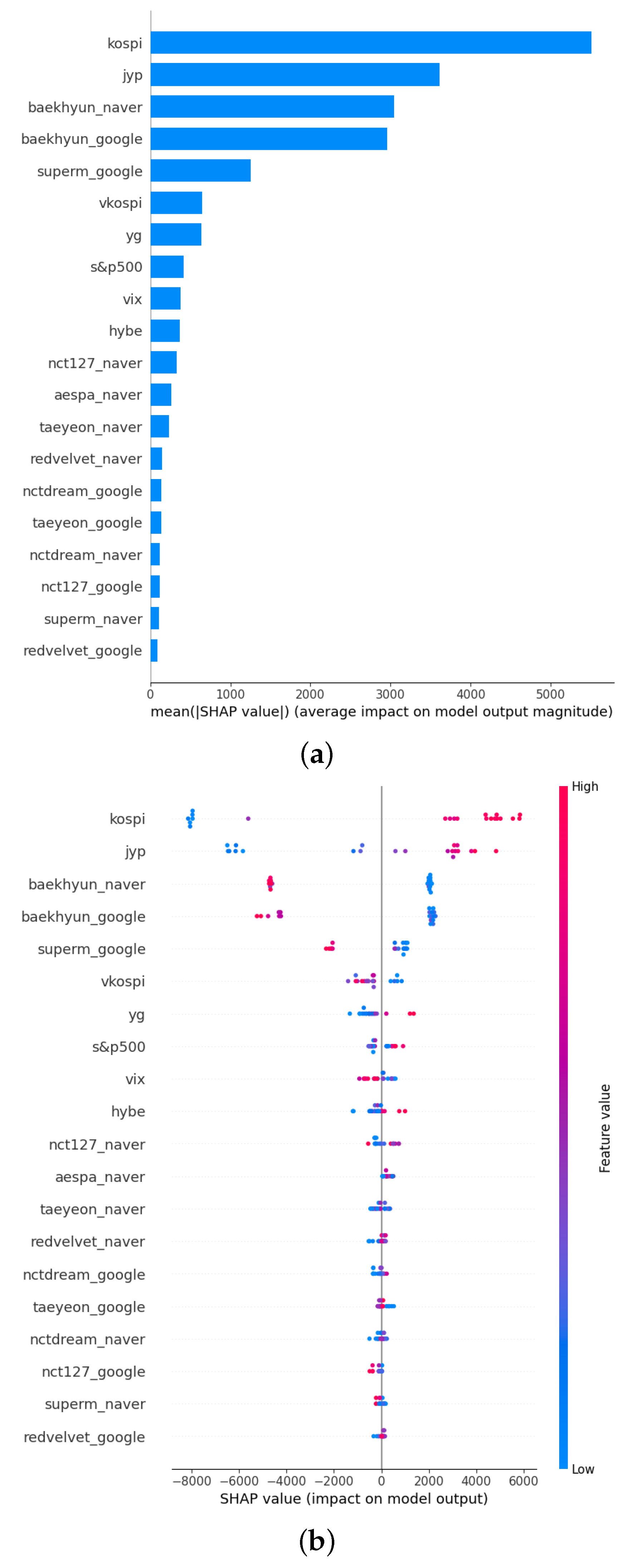

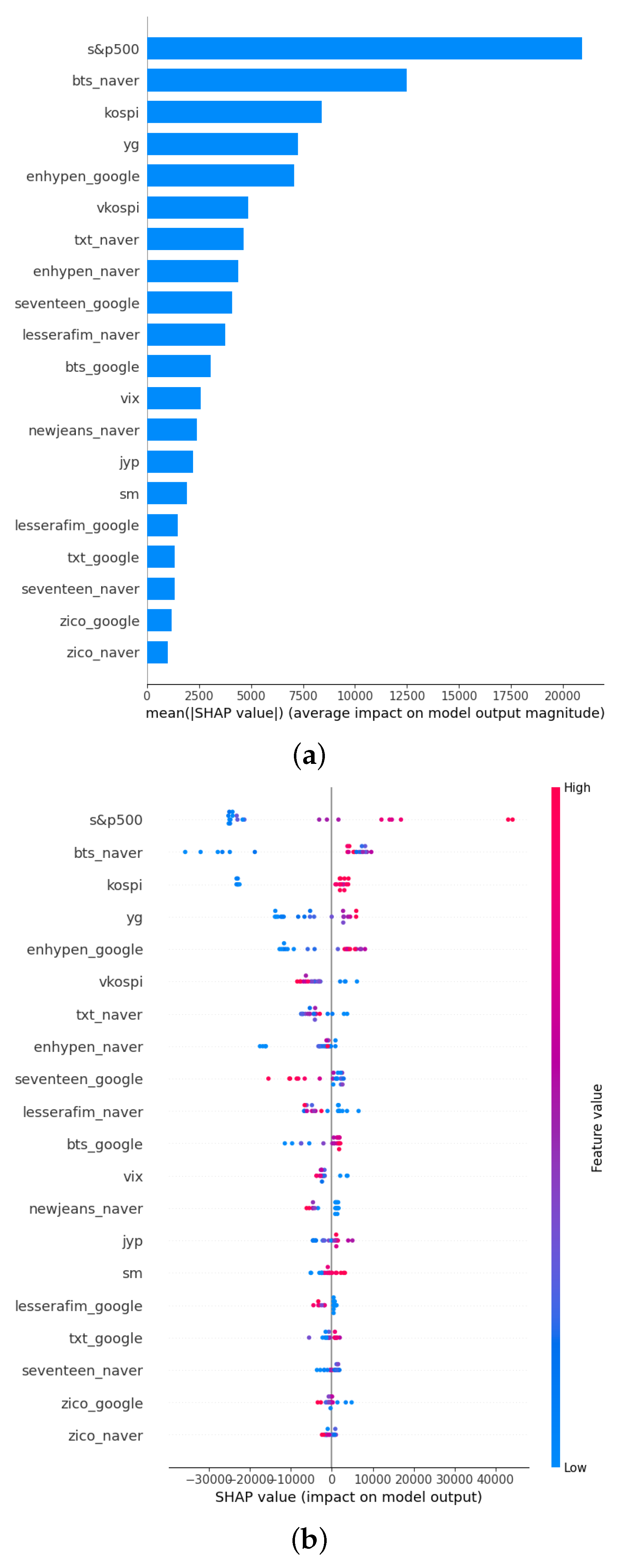

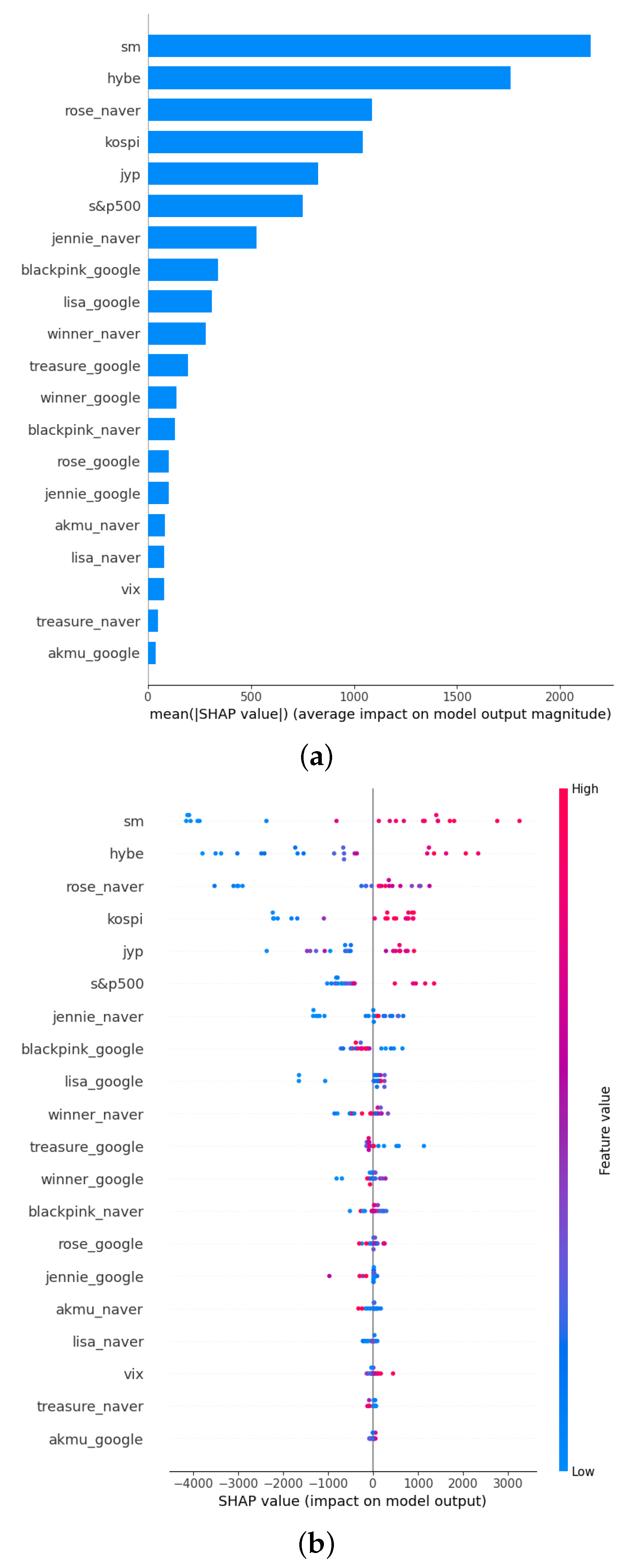

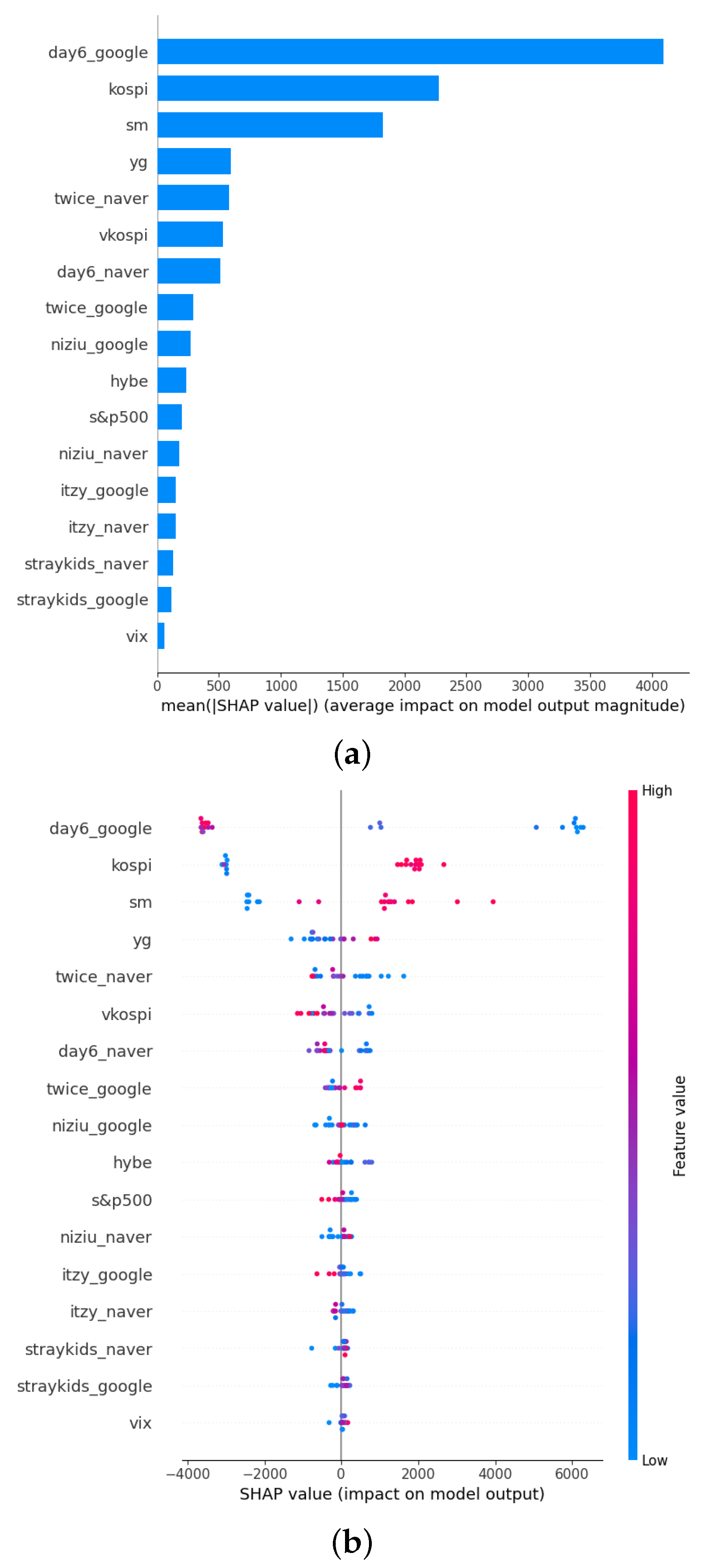

5. SHAP-XGBoost Analysis Results

6. Concluding Remarks

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Moussa, F.; BenOuda, O.; Delhoumi, E. The use of open source internet to analysis and predict stock market trading volume. Res. Int. Bus. Financ. 2017, 41, 399–411. [Google Scholar] [CrossRef]

- Chen, Y.; Zhao, H.; Li, Z.; Lu, J. A dynamic analysis of the relationship between investor sentiment and stock market realized volatility: Evidence from China. PLoS ONE 2020, 15, e0243080. [Google Scholar] [CrossRef] [PubMed]

- Lee, C.C.; Chen, M.P.; Lee, C.C. Investor attention, ETF returns, and country-specific factors. Res. Int. Bus. Financ. 2021, 56, 101386. [Google Scholar] [CrossRef]

- Bijl, L.; Kringhaug, G.; Molnár, P.; Sandvik, E. Google searches and stock returns. Int. Rev. Financ. Anal. 2016, 45, 150–156. [Google Scholar] [CrossRef]

- Swamy, V.; Dharani, M.; Takeda, F. Investor attention and Google Search Volume Index: Evidence from an emerging market using quantile regression analysis. Res. Int. Bus. Financ. 2019, 50, 1–17. [Google Scholar] [CrossRef]

- Costola, M.; Iacopini, M.; Santagiustina, C.R. Google search volumes and the financial markets during the COVID-19 outbreak. Financ. Res. Lett. 2021, 42, 101884. [Google Scholar] [CrossRef]

- Klein, T. A note on GameStop, short squeezes, and autodidactic herding: An evolution in financial literacy? Financ. Res. Lett. 2022, 46, 102229. [Google Scholar] [CrossRef]

- Koch, S.; Dimpfl, T. Attention and retail investor herding in cryptocurrency markets. Financ. Res. Lett. 2023, 51, 103474. [Google Scholar] [CrossRef]

- Han, J.; Miao, S.; Li, Y.; Yang, W.; Yin, H. Faulted-Phase classification for transmission lines using gradient similarity visualization and cross-domain adaption-based convolutional neural network. Electr. Power Syst. Res. 2021, 191, 106876. [Google Scholar] [CrossRef]

- Bhatnagar, M.; Yadav, A.; Swetapadma, A. Enhancing the resiliency of transmission lines using extreme gradient boosting against faults. Electr. Power Syst. Res. 2022, 207, 107850. [Google Scholar] [CrossRef]

- Bentéjac, C.; Csörgő, A.; Martínez-Muñoz, G. A comparative analysis of gradient boosting algorithms. Artif. Intell. Rev. 2021, 54, 1937–1967. [Google Scholar] [CrossRef]

- Nasiri, H.; Homafar, A.; Chelgani, S.C. Prediction of uniaxial compressive strength and modulus of elasticity for Travertine samples using an explainable artificial intelligence. Results Geophys. Sci. 2021, 8, 100034. [Google Scholar] [CrossRef]

- Fatahi, R.; Nasiri, H.; Dadfar, E.; Chehreh Chelgani, S. Modeling of energy consumption factors for an industrial cement vertical roller mill by SHAP-XGBoost: A “conscious lab” approach. Sci. Rep. 2022, 12, 7543. [Google Scholar] [CrossRef] [PubMed]

- Yang, Y.; Huang, Q.; Li, P. Online prediction and correction control of static voltage stability index based on Broad Learning System. Expert Syst. Appl. 2022, 199, 117184. [Google Scholar] [CrossRef]

- Zhang, J.; Ma, X.; Zhang, J.; Sun, D.; Zhou, X.; Mi, C.; Wen, H. Insights into geospatial heterogeneity of landslide susceptibility based on the SHAP-XGBoost model. J. Environ. Manag. 2023, 332, 117357. [Google Scholar] [CrossRef]

- Rathnayaka, R.K.T.; Jianguo, W.; Seneviratna, D.N. Geometric Brownian motion with Ito’s lemma approach to evaluate market fluctuations: A case study on Colombo Stock Exchange. In Proceedings of the 2014 International Conference on Behavioral, Economic, and Socio-Cultural Computing (BESC2014), Shanghai, China, 30 October–1 November 2014; pp. 1–6. [Google Scholar]

- Agustini, W.F.; Affianti, I.R.; Putri, E.R. Stock price prediction using geometric Brownian motion. J. Phys. Conf. Ser. 2018, 974, 012047. [Google Scholar] [CrossRef] [Green Version]

- Liu, Z.; Huang, S. Carbon option price forecasting based on modified fractional Brownian motion optimized by GARCH model in carbon emission trading. N. Am. J. Econ. Financ. 2021, 55, 101307. [Google Scholar] [CrossRef]

- Hu, H.; Zhao, C.; Li, J.; Huang, Y. Stock prediction model based on mixed fractional Brownian motion and improved fractional-order particle swarm optimization algorithm. Fractal Fract. 2022, 6, 560. [Google Scholar] [CrossRef]

- Kim, W.J.; Jung, G.; Choi, S.Y. Forecasting Cds term structure based on nelson–siegel model and machine learning. Complexity 2020, 2020, 2518283. [Google Scholar] [CrossRef]

- Shin, S.; Austin, P.C.; Ross, H.J.; Abdel-Qadir, H.; Freitas, C.; Tomlinson, G.; Chicco, D.; Mahendiran, M.; Lawler, P.R.; Billia, F.; et al. Machine learning vs. conventional statistical models for predicting heart failure readmission and mortality. Esc Heart Fail. 2021, 8, 106–115. [Google Scholar] [CrossRef]

- Grendas, L.N.; Chiapella, L.; Rodante, D.E.; Daray, F.M. Comparison of traditional model-based statistical methods with machine learning for the prediction of suicide behaviour. J. Psychiatr. Res. 2022, 145, 85–91. [Google Scholar] [CrossRef] [PubMed]

- Chae, S.C.; Choi, S.Y. Analysis of the Term Structure of Major Currencies Using Principal Component Analysis and Autoencoders. Axioms 2022, 11, 135. [Google Scholar] [CrossRef]

- Barber, B.M.; Odean, T. All that glitters: The effect of attention and news on the buying behavior of individual and institutional investors. Rev. Financ. Stud. 2008, 21, 785–818. [Google Scholar] [CrossRef] [Green Version]

- Da, Z.; Engelberg, J.; Gao, P. In search of attention. J. Financ. 2011, 66, 1461–1499. [Google Scholar] [CrossRef]

- Li, J.; Yu, J. Investor attention, psychological anchors, and stock return predictability. J. Financ. Econ. 2012, 104, 401–419. [Google Scholar] [CrossRef]

- Zhang, W.; Shen, D.; Zhang, Y.; Xiong, X. Open source information, investor attention, and asset pricing. Econ. Model. 2013, 33, 613–619. [Google Scholar] [CrossRef]

- Han, L.; Lv, Q.; Yin, L. Can investor attention predict oil prices? Energy Econ. 2017, 66, 547–558. [Google Scholar] [CrossRef]

- Halousková, M.; Stašek, D.; Horváth, M. The role of investor attention in global asset price variation during the invasion of Ukraine. Financ. Res. Lett. 2022, 50, 103292. [Google Scholar] [CrossRef]

- Bank, M.; Larch, M.; Peter, G. Google search volume and its influence on liquidity and returns of German stocks. Financ. Mark. Portf. Manag. 2011, 25, 239–264. [Google Scholar] [CrossRef]

- Alexander Dietzel, M.; Braun, N.; Schäfers, W. Sentiment-based commercial real estate forecasting with Google search volume data. J. Prop. Invest. Financ. 2014, 32, 540–569. [Google Scholar] [CrossRef] [Green Version]

- Liu, Y.; Chen, Y.; Wu, S.; Peng, G.; Lv, B. Composite leading search index: A preprocessing method of internet search data for stock trends prediction. Ann. Oper. Res. 2015, 234, 77–94. [Google Scholar] [CrossRef]

- Li, X.; Ma, J.; Wang, S.; Zhang, X. How does Google search affect trader positions and crude oil prices? Econ. Model. 2015, 49, 162–171. [Google Scholar] [CrossRef]

- Hu, H.; Tang, L.; Zhang, S.; Wang, H. Predicting the direction of stock markets using optimized neural networks with Google Trends. Neurocomputing 2018, 285, 188–195. [Google Scholar] [CrossRef]

- Huang, M.Y.; Rojas, R.R.; Convery, P.D. Forecasting stock market movements using Google Trend searches. Empir. Econ. 2020, 59, 2821–2839. [Google Scholar] [CrossRef]

- Fan, M.H.; Chen, M.Y.; Liao, E.C. A deep learning approach for financial market prediction: Utilization of Google trends and keywords. Granul. Comput. 2021, 6, 207–216. [Google Scholar] [CrossRef]

- El Ouadghiri, I.; Guesmi, K.; Peillex, J.; Ziegler, A. Public attention to environmental issues and stock market returns. Ecol. Econ. 2021, 180, 106836. [Google Scholar] [CrossRef]

- Dharani, M.; Hassan, M.K.; Abedin, M.Z.; Ismail, M.A. Does a search attention index explain portfolio returns in India? Borsa Istanb. Rev. 2022, 22, 226–239. [Google Scholar] [CrossRef]

- Joshi, A.M.; Hanssens, D.M. Movie advertising and the stock market valuation of studios: A case of “great expectations?”. Mark. Sci. 2009, 28, 239–250. [Google Scholar] [CrossRef] [Green Version]

- Joshi, A. Movie stars and the volatility of movie revenues. J. Media Econ. 2015, 28, 246–267. [Google Scholar] [CrossRef]

- Ltaifa, M.B.; Jamel, L.; Elnagar, A.K.; Derbali, A. Which is Determining in the Fluctuation of Stock Market Risk of Entertainment Compagnies in Viet Nam: Financial and Economic Crisis or Low Inflation Rate? Risk Financ. Manag. 2020, 2, p76. [Google Scholar] [CrossRef]

- Edwards Barros, C.M.; França Lopes, I.; Simão Kaveski, I.D. Pokémon Go!: Stock valuation and disruptive innovation in entertainment industry. Rev. Contemp. Contab. 2021, 18, 47–63. [Google Scholar] [CrossRef]

- Chen, Y. COVID-19 and the Dynamics of Disney’s Stock Price. In Proceedings of the 2022 7th International Conference on Social Sciences and Economic Development (ICSSED 2022), Wuhan, China, 25–27 March 2022; pp. 1425–1431. [Google Scholar]

- Wu, C.; Chen, Z. Media Coverage and the Noneffective Investment. In Proceedings of the 6th International Conference on E-Commerce, E-Business and E-Government, Plymouth, UK, 27–29 April 2022; pp. 10–14. [Google Scholar]

- Hayduk, T., III. Who Benefitted from the PyeongChang Olympic Announcement? Evidence from the South Korean Stock Market. J. Sport. Econ. 2022, 23, 39–75. [Google Scholar] [CrossRef]

- Yun, K.K.; Yoon, S.W.; Won, D. Prediction of stock price direction using a hybrid GA-XGBoost algorithm with a three-stage feature engineering process. Expert Syst. Appl. 2021, 186, 115716. [Google Scholar] [CrossRef]

- Antwarg, L.; Miller, R.M.; Shapira, B.; Rokach, L. Explaining anomalies detected by autoencoders using Shapley Additive Explanations. Expert Syst. Appl. 2021, 186, 115736. [Google Scholar] [CrossRef]

- Weng, F.; Zhu, J.; Yang, C.; Gao, W.; Zhang, H. Analysis of financial pressure impacts on the health care industry with an explainable machine learning method: China versus the USA. Expert Syst. Appl. 2022, 210, 118482. [Google Scholar] [CrossRef]

- Lin, B.; Bai, R. Machine learning approaches for explaining determinants of the debt financing in heavy-polluting enterprises. Financ. Res. Lett. 2022, 44, 102094. [Google Scholar] [CrossRef]

- Zou, Y.; Gao, C.; Gao, H. Business Failure Prediction Based on a Cost-Sensitive Extreme Gradient Boosting Machine. IEEE Access 2022, 10, 42623–42639. [Google Scholar] [CrossRef]

- Sairam, S.; Seshadhri, S.; Marafioti, G.; Srinivasan, S.; Mathisen, G.; Bekiroglu, K. Edge-based Explainable Fault Detection Systems for photovoltaic panels on edge nodes. Renew. Energy 2022, 185, 1425–1440. [Google Scholar] [CrossRef]

- Feng, Y.; Duan, Q.; Chen, X.; Yakkali, S.S.; Wang, J. Space cooling energy usage prediction based on utility data for residential buildings using machine learning methods. Appl. Energy 2021, 291, 116814. [Google Scholar] [CrossRef]

- Alsahaf, A.; Petkov, N.; Shenoy, V.; Azzopardi, G. A framework for feature selection through boosting. Expert Syst. Appl. 2022, 187, 115895. [Google Scholar] [CrossRef]

- Shapley, L.S. Stochastic games. Proc. Natl. Acad. Sci. USA 1953, 39, 1095–1100. [Google Scholar] [CrossRef] [Green Version]

- Bloch, L.; Friedrich, C.M. Data analysis with Shapley values for automatic subject selection in Alzheimer’s disease data sets using interpretable machine learning. Alzheimer’s Res. Ther. 2021, 13, 1–30. [Google Scholar] [CrossRef]

- Dong, H.; Sun, J.; Sun, X. A multi-objective multi-label feature selection algorithm based on shapley value. Entropy 2021, 23, 1094. [Google Scholar] [CrossRef]

- Rozemberczki, B.; Sarkar, R. The shapley value of classifiers in ensemble games. In Proceedings of the 30th ACM International Conference on Information & Knowledge Management, Gold Coast, Queensland, Australia, 1 November 2021; pp. 1558–1567. [Google Scholar]

- Li, Z. Extracting spatial effects from machine learning model using local interpretation method: An example of SHAP and XGBoost. Comput. Environ. Urban Syst. 2022, 96, 101845. [Google Scholar] [CrossRef]

- Aas, K.; Jullum, M.; Løland, A. Explaining individual predictions when features are dependent: More accurate approximations to Shapley values. Artif. Intell. 2021, 298, 103502. [Google Scholar] [CrossRef]

- Lundberg, S.M.; Lee, S.I. A unified approach to interpreting model predictions. In Proceedings of the Annual Conference on Neural Information Processing Systems 2017, Long Beach, CA, USA, 4–9 December 2017; pp. 4765–4774. [Google Scholar]

- Chang, V.; Li, T.; Zeng, Z. Towards an improved Adaboost algorithmic method for computational financial analysis. J. Parallel Distrib. Comput. 2019, 134, 219–232. [Google Scholar] [CrossRef]

- Chang, V.; Man, X.; Xu, Q.; Hsu, C.H. Pairs trading on different portfolios based on machine learning. Expert Syst. 2021, 38, e12649. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| HYBE | SM | YG | JYP |

|---|---|---|---|

| BTS | Baekhyun (EXO) | BLACKPINK | TWICE |

| Tomorrow X Together (TXT) | Taeyeon (SNSD) | JENNIE | ITZY |

| ENHYPEN | Red Velvet | ROSÉ | NiZiU |

| ZICO | NCT 127 | LISA | DAY6 |

| SEVENTEEN | NCT DREAM | WINNER | Stray Kids |

| NewJeans | aespa | AKMU | |

| LE SSERAFIM | SuperM | TREASURE |

| Mean | Max. | Min. | Std.Dev. | Skewness | Kurtosis | |

|---|---|---|---|---|---|---|

| HYBE | 234,576.05 | 414,000 | 109,500 | 70,962.81 | 0.176 | 2.13 |

| SM | 59,092.88 | 85,900 | 28,100 | 18,078.03 | −0.72 | 1.92 |

| YG | 52,446.08 | 73,100 | 39,850 | 7764.52 | 0.59 | 2.59 |

| JYP | 47,369.40 | 68,200 | 30,950 | 9749.14 | 0.22 | 1.76 |

| KOSPI | 2803.24 | 3305.21 | 2155.49 | 327.40 | −0.20 | −1.30 |

| VKOSPI | 20.06 | 35.73 | 12.55 | 4.31 | 1.08 | 1.09 |

| S&P 500 | 4142.95 | 4796.56 | 3310.24 | 327.77 | 0.03 | −1 |

| VIX | 22.99 | 38.57 | 15.02 | 4.92 | 0.60 | −0.26 |

| Parameter | SM | HYBE | YG | JYP |

|---|---|---|---|---|

| Learning rate | 0.05 | 0.05 | 0.05 | 0.05 |

| Number of gradient-boosted trees | 1000 | 500 | 1000 | 1000 |

| Maximum depth of trees | 7 | 7 | 5 | 5 |

| L1 regularization term on weights | 0.05 | 0 | 0 | 0 |

| L2 regularization term on weights | 0 | 0 | 0 | 0 |

| Subsample ratio of columns for each level | 0.9 | 0.9 | 0.9 | 0.9 |

| Parameter | SM | HYBE | YG | JYP |

|---|---|---|---|---|

| Learning rate | 0.05 | 0.05 | 0.1 | 0.05 |

| Number of gradient-boosted trees | 1000 | 800 | 1000 | 1000 |

| Maximum depth of trees | 7 | 5 | 7 | 3 |

| L1 regularization term on weights | 0.05 | 0.05 | 0.05 | 0 |

| L2 regularization term on weights | 0 | 0 | 0 | 0 |

| Subsample ratio of columns for each level | 0.9 | 0.9 | 0.9 | 0.9 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yu, D.; Choi, S.-Y. Uncovering the Impact of Local and Global Interests in Artists on Stock Prices of K-Pop Entertainment Companies: A SHAP-XGBoost Analysis. Axioms 2023, 12, 538. https://doi.org/10.3390/axioms12060538

Yu D, Choi S-Y. Uncovering the Impact of Local and Global Interests in Artists on Stock Prices of K-Pop Entertainment Companies: A SHAP-XGBoost Analysis. Axioms. 2023; 12(6):538. https://doi.org/10.3390/axioms12060538

Chicago/Turabian StyleYu, Daeun, and Sun-Yong Choi. 2023. "Uncovering the Impact of Local and Global Interests in Artists on Stock Prices of K-Pop Entertainment Companies: A SHAP-XGBoost Analysis" Axioms 12, no. 6: 538. https://doi.org/10.3390/axioms12060538

APA StyleYu, D., & Choi, S. -Y. (2023). Uncovering the Impact of Local and Global Interests in Artists on Stock Prices of K-Pop Entertainment Companies: A SHAP-XGBoost Analysis. Axioms, 12(6), 538. https://doi.org/10.3390/axioms12060538