Efficiency of Some Predictor–Corrector Methods with Fourth-Order Compact Scheme for a System of Free Boundary Options

Abstract

:1. Mathematical Model

2. Order (1,2) and (2,2) Predictor–Corrector Compact Differencing

2.1. Order (1,2) Euler-CN PC Method with Fourth-Order Compact Scheme

2.2. Stability Analysis

2.3. Order (2,2) Leapfrog-CN PC Method with Fourth-Order Compact Scheme

3. Order (3,3) and (4,4) Predictor–Corrector Compact Differencing

3.1. Order (3,3) PC Method with Fourth-Order Compact Scheme

3.2. Order (4,4) PC Method with Fourth-Order Compact Scheme

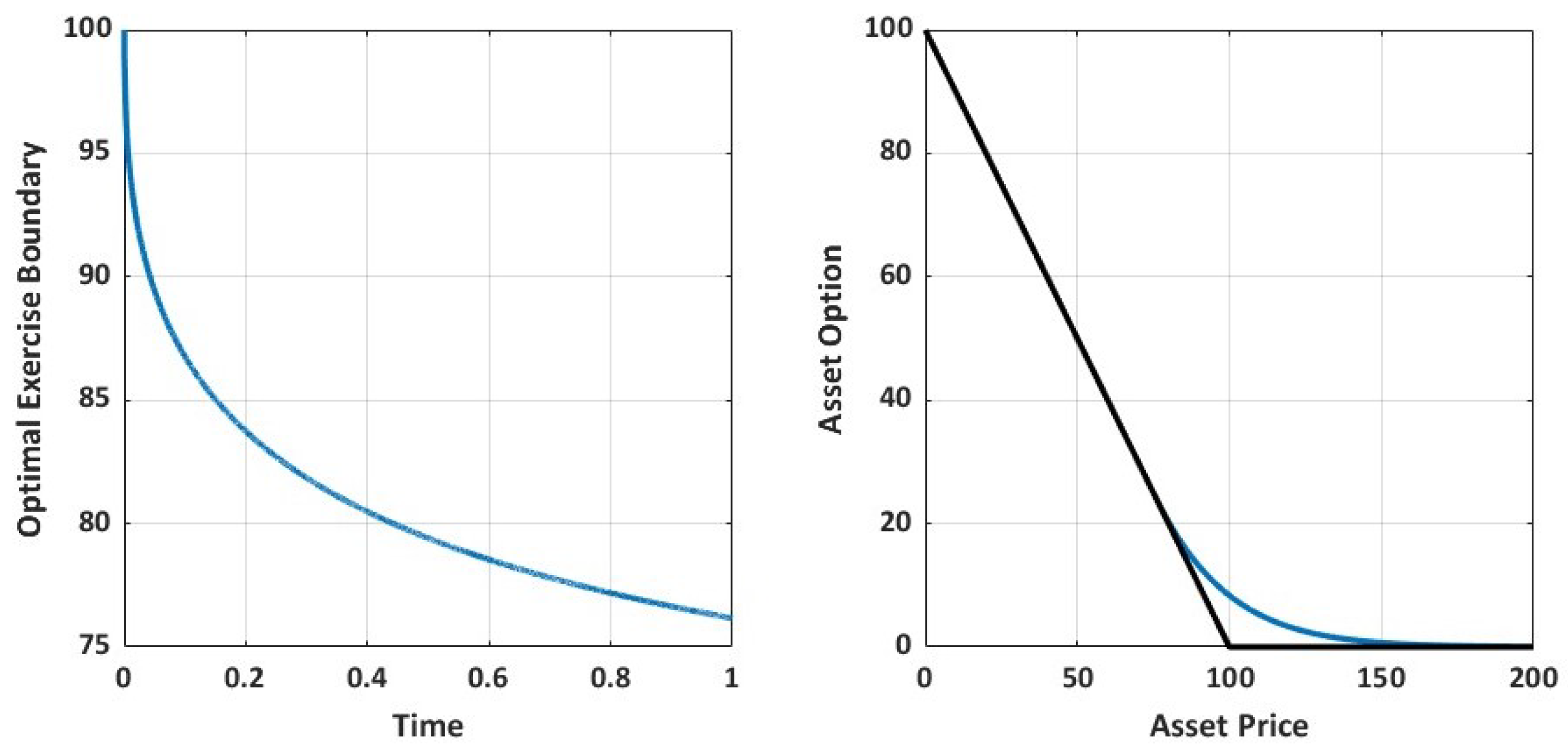

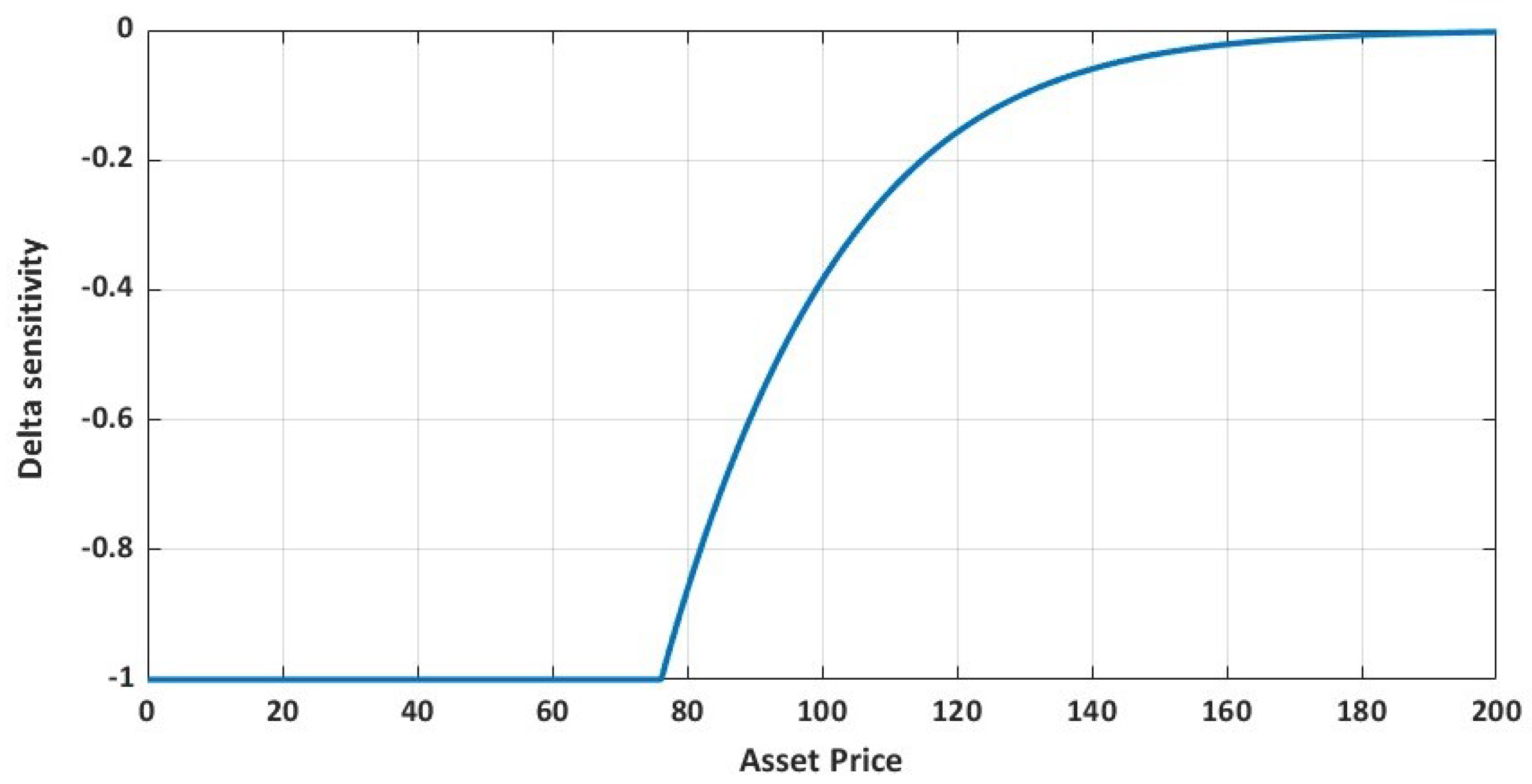

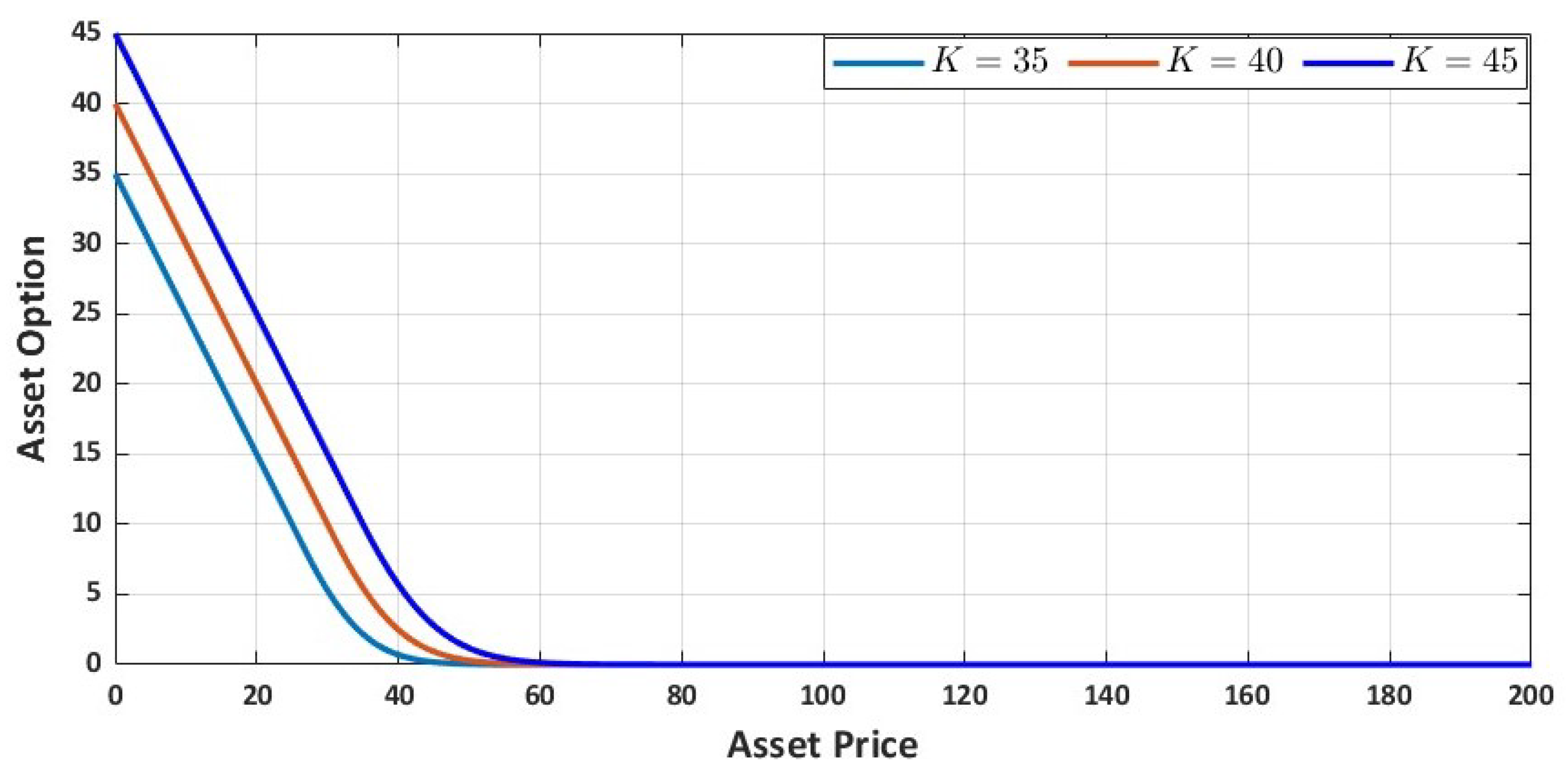

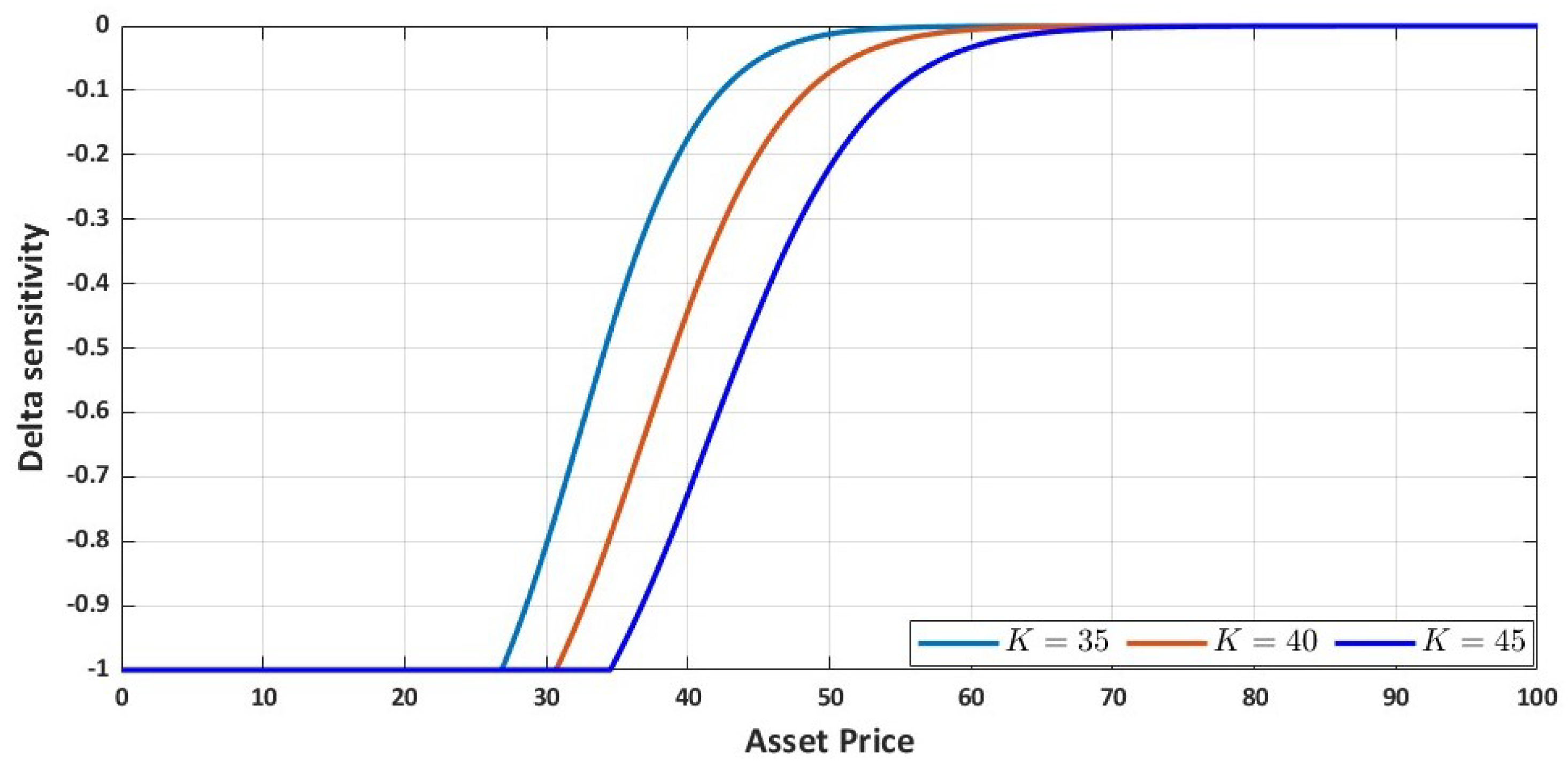

4. Numerical Results

4.1. Order (1,2) and (2,2) Predictor–Corrector Schemes

4.2. Order (3,3) and (4,4) Predictor–Corrector Schemes

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Kazmi, K. An IMEX predictor–corrector method for pricing options under regime-switching jump-diffusion models. Int. J. Comput. Math. 2019, 96, 1137–1157. [Google Scholar] [CrossRef]

- Kalantari, R.; Shahmorad, S.; Ahmadian, D. The stability analysis of predictor–corrector method in solving American option pricing model. Comput. Econ. 2016, 47, 255–274. [Google Scholar] [CrossRef]

- Khaliq, A.Q.M.; Voss, D.A.; Kazmi, S.H.K. A linearly implicit predictor–corrector scheme for pricing American options using a penalty method approach. J. Bank. Financ. 2006, 30, 489–502. [Google Scholar] [CrossRef]

- Chen, W.; Xu, X.; Zhu, S.P. A predictor–corrector approach for pricing American options under the finite moment log-stable model. Appl. Numer. Math. 2015, 97, 15–29. [Google Scholar] [CrossRef]

- Hajipour, M.; Malek, A. Efficient high-order numerical methods for pricing of options. Comput. Econ. 2015, 45, 31–47. [Google Scholar] [CrossRef]

- Zhu, S.P.; Zhang, J. A new predictor–corrector scheme for valuing American puts. Appl. Math. Comput. 2011, 217, 4439–4452. [Google Scholar] [CrossRef]

- Zhu, S.P.; Chen, W.T. A predictor–corrector scheme based on the ADI method for pricing American puts with stochastic volatility. Comput. Math. Appl. 2011, 62, 1–26. [Google Scholar] [CrossRef] [Green Version]

- Wu, L.; Kwok, Y.K. A front-fixing finite difference method for the valuation of American options. J. Financ. Eng. 1997, 6, 83–97. [Google Scholar]

- Zhao, J.; Corless, R.M. Compact finite difference method for integro-differential equations. Appl. Math. Comput. 2006, 177, 271–288. [Google Scholar] [CrossRef]

- Zhao, J. Highly accurate compact mixed methods for two point boundary value problems. Appl. Math. Comput. 2007, 188, 1402–1418. [Google Scholar] [CrossRef]

- Zhao, J.; Davison, M.; Corless, R.M. Compact finite difference method for American option pricing. J. Comput. Appl. Math. 2007, 206, 306–321. [Google Scholar] [CrossRef] [Green Version]

- Egorova, V.N.; Jódar, L. Solving American option pricing models by the front fixing method: Numerical analysis and computing. In Abstract and Applied Analysis; Hindawi: London, UK, 2014; Volume 2014. [Google Scholar]

- Egorova, V.N.; Company, R.; Jódar, L. A new efficient numerical method for solving American option under regime switching model. Comput. Math. Appl. 2016, 71, 224–237. [Google Scholar] [CrossRef]

- Kwok, Y.K. Mathematical Models of Financial Derivatives; Springer: Berlin/Heidelberg, Germany, 2008. [Google Scholar]

- Musiela, M.; Rutkowski, M. Martingale Methods in Financial Modelling; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2006. [Google Scholar]

- Zhang, K.; Song, H.; Li, J. Front-fixing FEMs for the pricing of American options based on a PML technique. Appl. Anal. 2015, 94, 903–931. [Google Scholar] [CrossRef]

- Adam, Y. A Hermitian finite difference method for the solution of parabolic equations. Comput. Math. Appl. 1975, 1, 393–406. [Google Scholar] [CrossRef] [Green Version]

- Adam, Y. Highly accurate compact implicit methods and boundary conditions. J. Comput. Phys. 1977, 24, 10–22. [Google Scholar] [CrossRef]

- Carpenter, M.H.; Gottlieb, D.; Abarbanel, S. The stability of numerical boundary treatments for compact high-order finite-difference schemes. J. Comput. Phys. 1993, 108, 272–295. [Google Scholar] [CrossRef] [Green Version]

- Carpenter, M.H.; Gottlieb, D.; Abarbanel, S. Stable and accurate boundary treatments for compact, high-order finite-difference schemes. Appl. Numer. Math. 1993, 12, 55–87. [Google Scholar] [CrossRef]

- Abrahamsen, D.; Fornberg, B. Solving the Korteweg-de Vries equation with Hermite-based finite differences. Appl. Math. Comput. 2021, 401, 126101. [Google Scholar] [CrossRef]

- Li, M.; Tang, T. A compact fourth-order finite difference scheme for unsteady viscous incompressible flows. J. Sci. Comput. 2001, 16, 29–45. [Google Scholar] [CrossRef]

- Nwankwo, C.; Dai, W. Sixth-order compact differencing with staggered boundary schemes and 3(2) Bogacki-Shampine pairs for pricing free-boundary options. arXiv 2022, arXiv:2207.14379. [Google Scholar]

- Tangman, D.Y.; Gopaul, A.; Bhuruth, M. A fast high-order finite difference algorithm for pricing American options. J. Comput. Appl. Math. 2008, 222, 17–29. [Google Scholar] [CrossRef] [Green Version]

- Leisen, D.P.; Reimer, M. Binomial models for option valuation-examining and improving convergence. Appl. Math. Financ. 1996, 3, 319–346. [Google Scholar] [CrossRef]

- Ikonen, S.; Toivanen, J. Operator splitting methods for American option pricing. Appl. Math. Lett. 2004, 17, 809–814. [Google Scholar] [CrossRef] [Green Version]

- Brennan, M.J.; Schwartz, E.S. The valuation of American put options. J. Financ. 1977, 32, 449–462. [Google Scholar] [CrossRef]

- Bunch, D.S.; Johnson, H. The American put option and its critical stock price. J. Financ. 2000, 55, 2333–2356. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| K | T | r | ||

|---|---|---|---|---|

| 100 | 1.00 | 0.10 | 0.30 | 3.00 |

| PC | (1,2) Euler-CN | (2,2) Leapfrog-CN | Zhu and Zhang [6] (N = 400) |

|---|---|---|---|

| 76.163227 | 76.163151 | 76.163742 |

| PC | (1,2) Euler-CN | (2,2) Leapfrog-CN |

|---|---|---|

| Total Runtime (s) | 0.2 s | 0.2 s |

| Methods | |||

|---|---|---|---|

| (1,2) Euler-CN | 24 s | 32 s | 56 s |

| (2,2) Leapfrog-CN | 21 s | 26 s | 51 s |

| Sixth-order compact scheme | 9 s | 180 s | 4785 s |

| Methods | |||

|---|---|---|---|

| (1,2) Euler-CN | 76.163078 | 76.163188 | 76.163226 |

| (2,2) Leapfrog-CN | 76.163059 | 76.163182 | 76.163225 |

| Sixth-order compact scheme | 76.163220 | 76.163226 | 76.163226 |

| No. of Iteration | 1 | 2 | 3 | 4 |

|---|---|---|---|---|

| 76.163841 | 76.163388 | 76.163276 | 76.163268 |

| K | T | r | ||

|---|---|---|---|---|

| 100 | 3.00 | 0.05 | 0.20 | 3.00 |

| S | Euler-CN | Leapfrog-CN | Binomial | WK | OP | BS-1 | BS-2 |

|---|---|---|---|---|---|---|---|

| 80 | 20.2820 | 20.2820 | 20.2797 | 20.2825 | 20.2795 | 20.2785 | 20.2783 |

| 90 | 13.3077 | 13.3077 | 13.3075 | 13.3117 | 13.3074 | 13.3047 | 13.3072 |

| 100 | 8.7107 | 8.7107 | 8.7106 | 8.7135 | 8.7104 | 8.7070 | 8.7102 |

| 110 | 5.6826 | 5.6826 | 5.6825 | 5.6867 | 5.6824 | 5.6791 | 5.6822 |

| 120 | 3.6965 | 3.6965 | 3.6964 | 3.7001 | 3.6963 | 3.6935 | 3.6961 |

| S | Euler-CN | Leapfrog-CN | Binomial | WK | OP | BS-1 | BS-2 |

|---|---|---|---|---|---|---|---|

| 80 | −0.8537 | −0.8537 | −0.8536 | −0.8508 | −0.8536 | −0.8539 | −0.8536 |

| 90 | −0.5619 | −0.5619 | −0.5619 | −0.5600 | −0.5619 | −0.5621 | −0.5619 |

| 100 | −0.3706 | −0.3706 | −0.3706 | −0.3694 | −0.3706 | −0.3707 | −0.3706 |

| 110 | −0.2436 | −0.2436 | −0.2436 | −0.2429 | −0.2436 | −0.2436 | −0.2436 |

| 120 | −0.1594 | −0.1594 | −0.1594 | −0.1589 | −0.1594 | −0.1593 | −0.1594 |

| h | Maximum Errors | Convergence Rate |

|---|---|---|

| 0.2 | ||

| 0.1 | 3.636750127435 | |

| 0.05 | 0.541734921861 | 2.747 |

| 0.025 | 0.169692227237 | 1.675 |

| 0.0125 | 0.026627237617 | 2.672 |

| 0.00625 | 0.001969927462 | 3.757 |

| h | Maximum Errors | Convergence Rate |

|---|---|---|

| 0.2 | ||

| 0.1 | 3.662480988725 | |

| 0.05 | 0.594074051436 | 2.624 |

| 0.025 | 0.153110702238 | 1.956 |

| 0.0125 | 0.032427092114 | 2.239 |

| 0.00625 | 0.001585082185 | 4.355 |

| T | r | |||

|---|---|---|---|---|

| 40 | 4.00 | 0.0488 | 0.30 | 3.00 |

| K | -BDF3 | -BDF3 | - | - | -M3 | -BDF4 | - | BM |

|---|---|---|---|---|---|---|---|---|

| 35 | 0.6978 | 0.6978 | 0.6978 | 0.6977 | 0.6976 | 0.6977 | 0.6975 | 0.6975 |

| 40 | 2.4837 | 2.4836 | 2.4832 | 2.4832 | 2.4833 | 2.4833 | 2.4830 | 2.4825 |

| 45 | 5.7073 | 5.7072 | 5.7067 | 5.7068 | 5.7068 | 5.7069 | 5.7065 | 5.7056 |

| Time (s) | 5.9 | 5.8 | 5.7 | 5.7 | 5.8 | 5.9 | 5.5 | None |

| K | -BDF3 | -BDF3 | - | - | -M3 | -BDF4 | - | BM |

|---|---|---|---|---|---|---|---|---|

| 35 | −0.1740 | −0.1740 | −0.1740 | −0.1740 | −0.1740 | −0.1740 | −0.1740 | −0.1741 |

| 40 | −0.4418 | −0.4418 | −0.4419 | −0.4419 | −0.4419 | −0.4419 | −0.4419 | −0.4420 |

| 45 | −0.7262 | −0.7262 | −0.7263 | −0.7263 | −0.7263 | −0.7263 | −0.7264 | −0.7266 |

| Time (s) | 5.9 | 5.8 | 5.7 | 5.7 | 5.8 | 5.9 | 5.5 | None |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nwankwo, C.; Dai, W. Efficiency of Some Predictor–Corrector Methods with Fourth-Order Compact Scheme for a System of Free Boundary Options. Axioms 2023, 12, 762. https://doi.org/10.3390/axioms12080762

Nwankwo C, Dai W. Efficiency of Some Predictor–Corrector Methods with Fourth-Order Compact Scheme for a System of Free Boundary Options. Axioms. 2023; 12(8):762. https://doi.org/10.3390/axioms12080762

Chicago/Turabian StyleNwankwo, Chinonso, and Weizhong Dai. 2023. "Efficiency of Some Predictor–Corrector Methods with Fourth-Order Compact Scheme for a System of Free Boundary Options" Axioms 12, no. 8: 762. https://doi.org/10.3390/axioms12080762

APA StyleNwankwo, C., & Dai, W. (2023). Efficiency of Some Predictor–Corrector Methods with Fourth-Order Compact Scheme for a System of Free Boundary Options. Axioms, 12(8), 762. https://doi.org/10.3390/axioms12080762