The Influence of Administrative Division Adjustment on Enterprise Earnings Management: A Quasi-Natural Experiment on City–County Consolidation

Abstract

:1. Introduction

2. Literature Review

2.1. Reviews of City–County Consolidation

2.2. Market Competition and Enterprise Earnings Management

2.3. Summary of the Literature

3. Theoretical Mechanism Analysis

3.1. City–County Consolidation Intensified Market Competition among Enterprises

3.2. Intensified Market Competition among Enterprises Improved Level of Enterprises’ Earnings Management

4. Methods

4.1. Date

4.2. Model Design and Description

5. Results

5.1. The Impact of City–County Consolidation on Enterprise Earnings Management

5.2. Transmission Mechanism Test for Market Competition

5.3. Robustness Checks

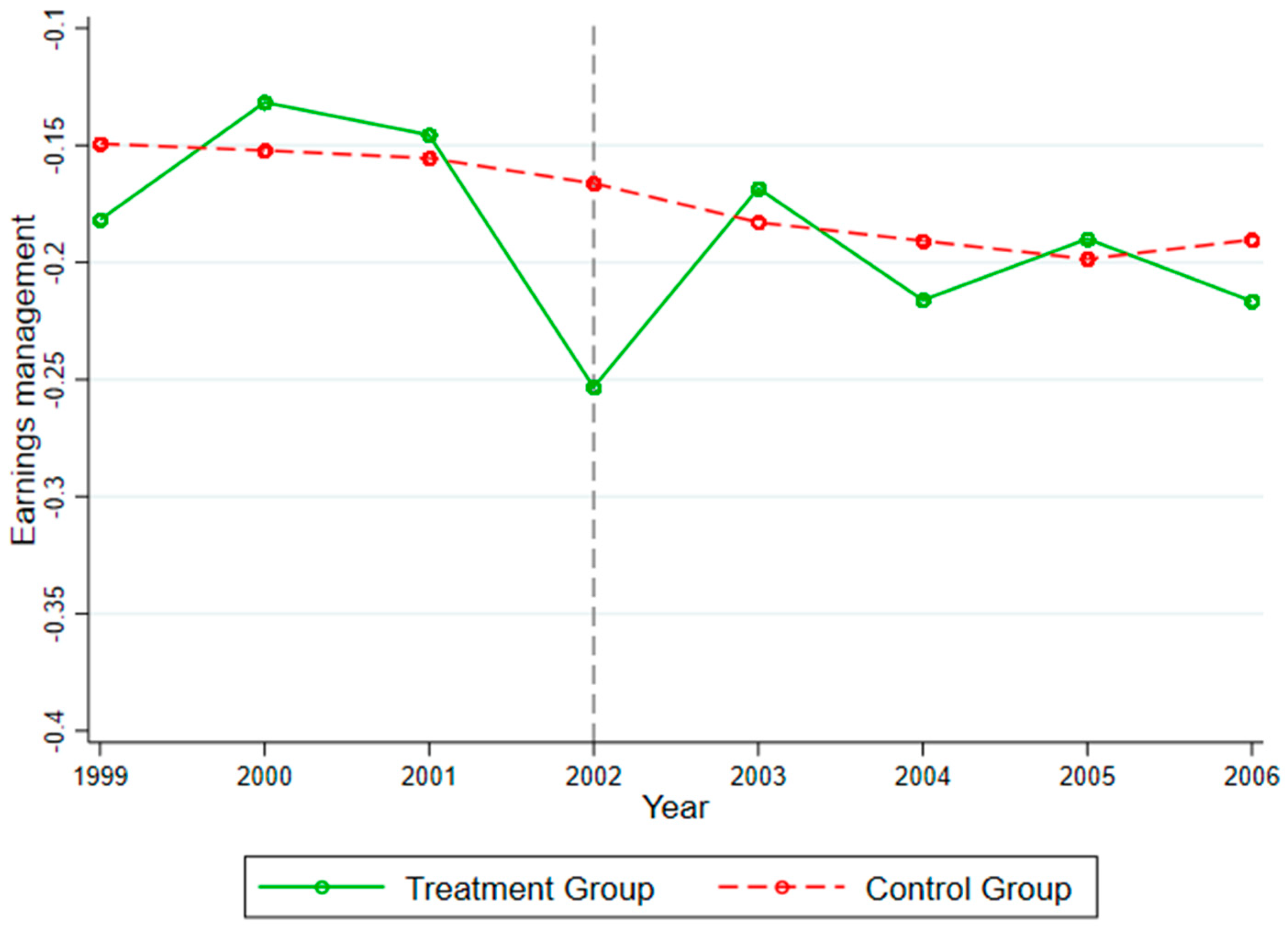

5.3.1. Parallel Trend Test

5.3.2. Clustering by County

5.3.3. Endogeneity Problems

5.3.4. Replace Other Measures of Earnings Management

5.4. Research on Heterogeneity

5.5. Discussion

6. Conclusions and Implications

6.1. Conclusions

6.2. Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Carr, J.B.; Feiock, R.C. Metropolitan government and economic development. Urban Aff. Rev. 1999, 34, 476–488. [Google Scholar] [CrossRef]

- Carr, J.B.; Bae, S.S.; Lu, W. City-county government and promises of economic development: A tale of two cities. State Local Gov. Rev. 2006, 38, 131–141. [Google Scholar] [CrossRef]

- Fan, S.; Li, L.X.; Zhang, X.B. Challenges of creating cities in China: Lessons from a short-lived county-to-city upgrading policy. J. Comp. Econ. 2012, 40, 476–491. [Google Scholar] [CrossRef]

- Shao, Z.D.; Su, D.N.; Bao, Q. Growth Performance Evaluation of City-County Merger under the Chinese Style Decentralization. J. World Econ. 2018, 41, 101–125. (In Chinese) [Google Scholar]

- Leland, S.M.; Thurmaier, K. When Efficiency Is Unbelievable: Normative Lessons from 30 Years of City–County Consolidations. Public Adm. Rev. 2010, 65, 475–489. [Google Scholar] [CrossRef]

- Lu, S.F.; Chen, S.X. The Value of Governmental Favoritism: Evidence from Export Performance of Chinese Industrial Enterprises. J. Financ. Res. 2016, 7, 33–47. (In Chinese) [Google Scholar]

- Lu, S.F.; Chen, S.X. Does Governmental Favoritism Reduce Financing Constraints of Firms: A Quasi-Natural Experiment from China. Manag. World 2017, 5, 51–65. (In Chinese) [Google Scholar]

- Grossman, S.J.; Hart, O.D. Corporate Financial Structure and Managerial Incentives; University of Chicago Press: Chicago, IL, USA, 1982; pp. 107–140. [Google Scholar]

- Xue, S.; Tinaikar, S. Product Market Competition and Earnings Management: Some International Evidence; Social Science Electronic Publishing: Rochester, NY, USA, 2009; pp. 1–48. [Google Scholar]

- Datta, S.; Mai, I.D.; Sharma, V. Product market pricing power, industry concentration and analysts’ earnings forecasts. J. Bank. Financ. 2011, 35, 1352–1366. [Google Scholar] [CrossRef]

- Hoberg, G.; Phillips, G.M. Real and Financial Industry Booms and Busts. J. Financ. 2010, 65, 45–86. [Google Scholar] [CrossRef]

- Hall, J.C.; Matti, J.; Yang, Z. The economic impact of city–county consolidations: A synthetic control approach. Public Choice 2020, 184, 43–77. [Google Scholar] [CrossRef] [Green Version]

- Feiock, R.C.; Carr, J.B. A reassessment of city/county consolidation: Economic development impacts. State Local Gov. Rev. 1997, 29, 166–171. [Google Scholar] [CrossRef]

- Faulk, D.; Schansberg, E. An examination of selected economic development outcomes from consolidation. State Local Gov. Rev. 2009, 41, 193–200. [Google Scholar] [CrossRef]

- Egger, P.H.; Koethenbuerger, M.; Loumeau, G. Municipal Megers and economic activity. In Proceedings of the 111th Annual Conference of the National Tax Association, New Orleans, LA, USA, 15–17 November 2018. [Google Scholar]

- Bunch, B.S.; Strauss, R.P. Municipal consolidation: An analysis of the financial benefits for fiscally distressed small municipalities. Urban Aff. Q. 1992, 27, 615–629. [Google Scholar] [CrossRef]

- Dagney, F.; Georg, G. City-county Consolidation and Local Government Expenditures. State Local Gov. Rev. 2012, 44, 196–205. [Google Scholar]

- Gaffney, M.; Marlowe, J. Fiscal Implications of City-City Consolidations. State Local Gov. Rev. 2014, 46, 197–204. [Google Scholar] [CrossRef]

- Taylor, C.D.; Faulk, D.; Schaal, P. Where are the cost savings in city–county consolidation? J. Urban Aff. 2016, 39, 185–204. [Google Scholar] [CrossRef]

- Fan, Z.Y.; Zhao, R.J. Fiscal Responsibilities, Tax Efforts and Corporate Tax Burden. J. Financ. Res. 2020, 55, 101–117. (In Chinese) [Google Scholar]

- Peteraf, M.A. The Cornerstones of Competitive Advantage: A Resource-Based View. Strateg. Manag. J. 1993, 13, 179–191. [Google Scholar] [CrossRef]

- Holmström, B. Moral Hazard in Teams. Bell J. Econ. 1982, 13, 324–340. [Google Scholar] [CrossRef]

- Schmidt, K.M. Managerial Incentives and Product Market Competition. Rev. Econ. Stud. 1997, 2, 191–213. [Google Scholar] [CrossRef]

- Marciukaityte, D.; Park, J.C. Market Competition and Earnings Management; Social Science Electronic Publishing: Rochester, NY, USA, 2009. [Google Scholar]

- Balakrishnan, K.; Cohen, D.A. Competition and Financial Accounting Misreporting. SSRN Electron. J. 2011, 115, 2433–2442. [Google Scholar] [CrossRef]

- Markarian, G.; Santalo, J. Product market competition, information and earnings management. J. Bus. Financ. Account. 2014, 41, 572–599. [Google Scholar] [CrossRef] [Green Version]

- Wu, P.; Gao, L.; Gu, T. Business strategy, market competition and earnings management. Chin. Manag. Stud. 2015, 9, 401–424. [Google Scholar] [CrossRef]

- Baldwin, R.E.; Okubo, T. Heterogeneous Firms, Agglomeration and Economic Geography: Spatial Selection and Sorting. J. Econ. Geogr. 2006, 6, 323–346. [Google Scholar] [CrossRef] [Green Version]

- Melitz, M.J.; Ottaviano, G.I.P. Market Size, Trade and Productivity. Rev. Econ. Stud. 2008, 75, 295–316. [Google Scholar] [CrossRef] [Green Version]

- Gavana, G.; Gottardo, P.; Moisello, A. What Form of Visibility Affects Earnings Management? Evidence from Italian Family and Non-Family Firms. Adm. Sci. 2019, 9, 20. [Google Scholar] [CrossRef] [Green Version]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Shleifer, A. Does Competition Destroy Ethical Behavior? Am. Econ. Rev. 2004, 94, 414–418. [Google Scholar] [CrossRef] [Green Version]

- Brandt, L.; Biesebroeck, J.V.; Zhang, Y. Creative Accounting or Creative Destruction? Firm-level Productivity Growth in Chinese Manufacturing. J. Dev. Econ. 2012, 97, 339–351. [Google Scholar] [CrossRef] [Green Version]

- Dechow, P.M.; Sloan, R.G.; Hutton, A.P. Detecting Earnings Management. Account. Rev. 1995, 70, 193–225. [Google Scholar]

- Kothari, S.P.; Leone, A.J.; Wasley, C.E. Performance matched discretionary accrual measures. J. Account. Econ. 2005, 39, 163–197. [Google Scholar] [CrossRef]

- Li, G.Z.; Jia, F.S. Government Fiscal Incentives, Tax Enforcement, and Enterprise Earnings Management: A Study Based on the Natural Experiment of Fiscal PMC Reform. J. Financ. Res. 2019, 2, 78–97. (In Chinese) [Google Scholar]

- Baker, A.C.; Larcker, D.F.; Wang, C.C.Y. How much should we trust staggered difference-in-differences estimates? J. Financ. Econ. 2022, 144, 370–395. [Google Scholar] [CrossRef]

- Hanlon, M.; Hoopes, J.L.; Shroff, N. The Effect of Tax Authority Monitoring and Enforcement on Financial Reporting Quality; Social Science Electronic Publishing: Rochester, NY, USA, 2014; p. 36. [Google Scholar]

- Ali, A.; Zhang, W. CEO Tenure and Earnings Management. J. Account. Econ. 2015, 59, 60–79. [Google Scholar] [CrossRef]

- Gaspar, J.M.; Massa, M. Idiosyncratic Volatility and Product Market Competition. J. Bus. 2004, 79, 3125–3152. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Description of Variables | Mean | S. D | Observation |

|---|---|---|---|---|

| EM | Take the negative value of discretionary accruals’ absolute value | −0.179 | 0.190 | 653,636 |

| Total liability/total assets | 0.554 | 0.244 | 653,636 | |

| ROA | Net profit/total assets | 0.061 | 0.118 | 653,636 |

| Growth | (Current period sales—last period sales)/last period sales | 0.372 | 3.221 | 653,636 |

| Scale | The logarithm of assets | 10.208 | 1.331 | 653,636 |

| Age | Current year—year of establishment + 1 (in log) | 2.176 | 0.807 | 653,636 |

| IEM | Except the enterprise itself, the current year average earnings management level of other companies in the industry (3-digit code) | −0.179 | 0.027 | 653,636 |

| Dependent Variable | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| EM | Upward | Downward | Market Competition | |

| CCC | −0.053 *** (0.017) | 0.031 (0.025) | −0.071 ** (0.029) | −0.006 ** (0.003) |

| ROA | 0.008 *** (0.005) | 0.010 (0.006) | −0.004 (0.008) | −0.006 * (0.003) |

| LEV | −0.035 *** (0.003) | −0.221 *** (0.003) | −0.351 *** (0.005) | 0.001 (0.001) |

| Age | 0.025 *** (0.001) | −0.018 *** (0.001) | 0.028 *** (0.001) | −0.001 ** (0.001) |

| IEM | 0.371 *** (0.022) | −0.439 *** (0.027) | 0.300 *** (0.042) | 0.188 *** (0.038) |

| Scale | −0.062 *** (0.001) | 0.021 *** (0.001) | −0.087 *** (0.002) | −0.002 ** (0.001) |

| Growth | −0.002 *** (0.001) | 0.002 (0.001) | −0.003 ** (0.001) | 0.000 (0.000) |

| Constant | 0.484 *** (0.011) | −0.018 (0.014) | 0.894 *** (0.020) | 0.152 *** (0.000) |

| Enterprise fixed effect | Yes | Yes | Yes | Yes |

| Year fixed effect | Yes | Yes | Yes | Yes |

| Observations | 653,636 | 366,751 | 286,885 | 609,140 |

| R2 | 0.470 | 0.610 | 0.655 | 0.849 |

| Dependent Variable | (1) | (2) | (3) |

|---|---|---|---|

| EM | EM | EM | |

| CCC | −0.053 *** (0.014) | −0.047 *** (0.017) | −0.051 *** (0.017) |

| ROA | 0.008 (0.006) | 0.012 *** (0.005) | −0.009 * (0.005) |

| LEV | −0.035 *** (0.004) | −0.036 *** (0.003) | −0.034 *** (0.003) |

| Age | 0.025 *** (0.001) | 0.023 *** (0.001) | 0.025 *** (0.001) |

| IEM | 0.371 *** (0.024) | 0.324 *** (0.022) | 0.351 *** (0.021) |

| Scale | −0.062 *** (0.001) | −0.062 *** (0.001) | −0.063 *** (0.001) |

| Growth | −0.002 * (0.001) | −0.002 * (0.001) | −0.002 * (0.001) |

| Constant | 0.484 *** (0.019) | 0.482 *** (0.011) | 0.494 *** (0.011) |

| Clustered by enterprise | Yes | Yes | Yes |

| Clustered by county | Yes | No | No |

| Cross-fixed effects of provinces and years | No | Yes | No |

| Enterprise fixed effect | Yes | Yes | Yes |

| Year fixed effect | Yes | Yes | Yes |

| Replace other measures | No | No | Yes |

| Observations | 653,636 | 653,636 | 653,636 |

| R2 | 0.470 | 0.471 | 0.471 |

| Dependent Variable | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| State-Owned Enterprises | Non-State-Owned Enterprises | Belonging to the Central, Provincial, and City Governments | Belonging to the Central, Provincial, and City Governments | |

| CCC | −0.052 (0.049) | −0.054 *** (0.020) | −0.031 (0.024) | −0.065 ** (0.025) |

| ROA | −0.017 (0.021) | 0.010 ** (0.005) | −0.071 *** (0.015) | 0.018 *** (0.005) |

| LEV | 0.005 (0.010) | −0.038 *** (0.003) | −0.038 *** (0.007) | −0.034 *** (0.003) |

| Age | 0.009 *** (0.002) | 0.022 *** (0.001) | 0.017 *** (0.002) | 0.023 *** (0.001) |

| IEM | 0.251 *** (0.050) | 0.351 *** (0.024) | 0.264 *** (0.040) | 0.357 *** (0.025) |

| Scale | −0.032 *** (0.004) | −0.068 *** (0.001) | −0.027 *** (0.003) | −0.068 *** (0.001) |

| Growth | −0.000 *** (0.000) | −0.005 *** (0.001) | −0.001 ** (0.000) | −0.007 ** (0.002) |

| Constant | 0.248 *** (0.047) | 0.539 *** (0.012) | 0.199 *** (0.033) | 0.528 *** (0.012) |

| Enterprise fixed effect | Yes | Yes | Yes | Yes |

| Year fixed effect | Yes | Yes | Yes | Yes |

| Observations | 58,797 | 594,839 | 85,936 | 567,700 |

| R2 | 0.525 | 0.475 | 0.479 | 0.476 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xu, Y.; Ge, Y.; Bao, H. The Influence of Administrative Division Adjustment on Enterprise Earnings Management: A Quasi-Natural Experiment on City–County Consolidation. Buildings 2022, 12, 951. https://doi.org/10.3390/buildings12070951

Xu Y, Ge Y, Bao H. The Influence of Administrative Division Adjustment on Enterprise Earnings Management: A Quasi-Natural Experiment on City–County Consolidation. Buildings. 2022; 12(7):951. https://doi.org/10.3390/buildings12070951

Chicago/Turabian StyleXu, Yueling, Yijiu Ge, and Haijun Bao. 2022. "The Influence of Administrative Division Adjustment on Enterprise Earnings Management: A Quasi-Natural Experiment on City–County Consolidation" Buildings 12, no. 7: 951. https://doi.org/10.3390/buildings12070951

APA StyleXu, Y., Ge, Y., & Bao, H. (2022). The Influence of Administrative Division Adjustment on Enterprise Earnings Management: A Quasi-Natural Experiment on City–County Consolidation. Buildings, 12(7), 951. https://doi.org/10.3390/buildings12070951