The Impact of Women Power on Firm Value

Abstract

:1. Introduction

2. Literature Review

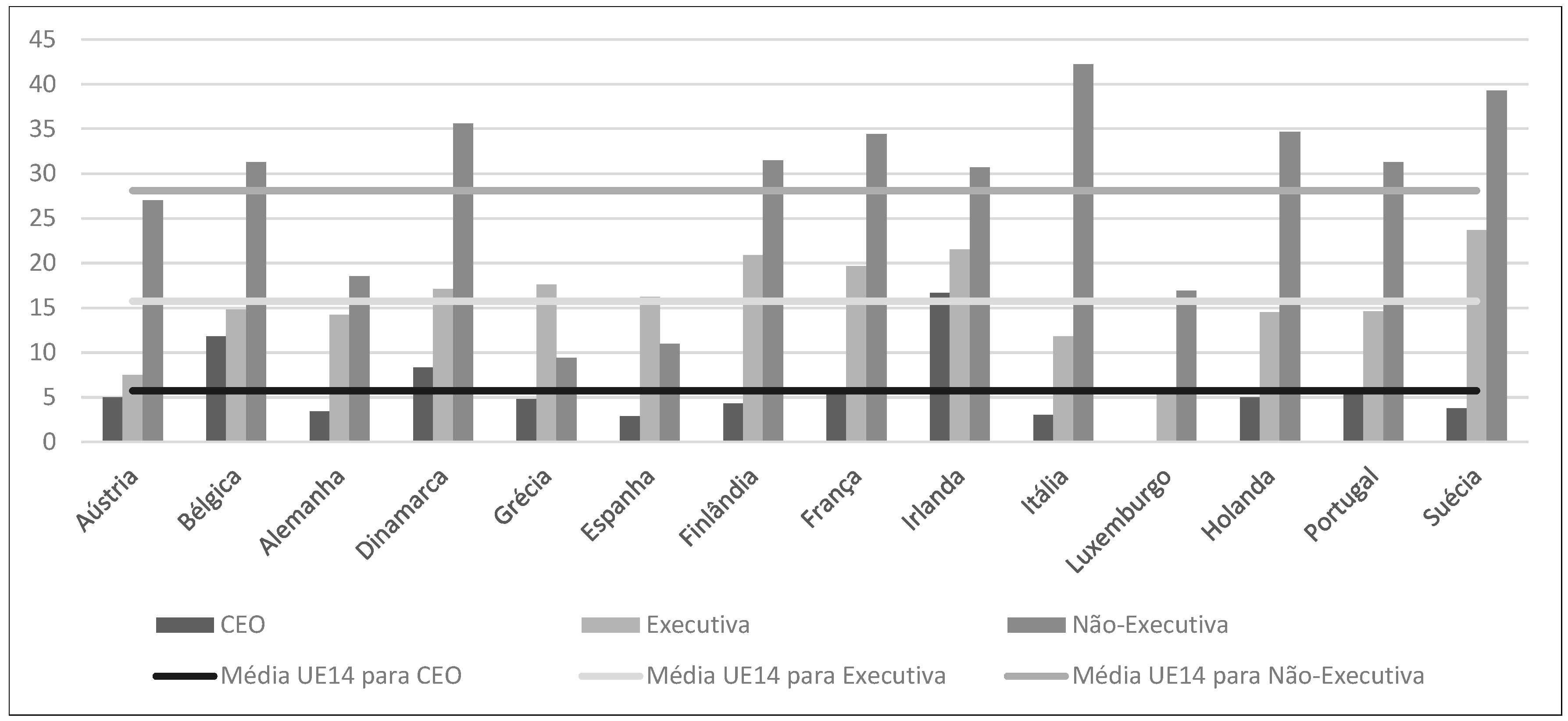

2.1. Gender Diversity in the Largest Companies of the EU14

2.2. Gender Differences and Similarities

2.3. Gender Diversity and Firm Value

- Q1: Is the presence of women on boards positively associated with firm value?

- Q2: When countries are governed by women, does the positive association between the presence of women on boards and firm value hold?

3. Methodology

3.1. Data and Sample

3.2. Models

4. Results and Discussion

4.1. Descriptive Statistics

4.2. The Association between Women on Boards and Firm Value

4.3. Additional Analysis

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Variable | Definition | |

|---|---|---|

| Tobin’s Q | Firm value | Sum of the market value of equity (share price multiplied by the number of ordinary shares in issue at fiscal year-end) and the book value of debt divided by the book value of total assets. |

| ROA | Return on assets | Net income divided by total assets. |

| Operating Margin | Operating Margin | Operating income divided by the total sales. |

| Chair_W | Chairperson | Dummy variable that takes the value of 1 if the position is occupied by a woman and 0, otherwise. |

| CEO_W | Chief Executive Officer | Dummy variable that takes the value of 1 if the position is occupied by a woman and 0, otherwise. |

| CFO_W | Chief Financial Officer | Dummy variable that takes the value of 1 if the position is occupied by a woman and 0, otherwise. |

| Size | Firm size | Natural logarithm of total assets. |

| Lev | Financial leverage | Total liabilities divided by total assets. |

| Growth | Sales growth | Annual variation of sales (%) |

| Age | Firm age | Natural logarithm of the number of years of the firm |

| Gov_W | Political or monarchical representative of the country | Dummy variable that takes the value of to 1 if the position is occupied by a woman and 0, otherwise. |

| Ind | Industry | Binary variable that takes the value of 1 if the company belongs to the sector in question and 0, otherwise. |

| Country | Country | Binary variable that takes the value of 1 if the company belongs to the country in question and 0 otherwise. |

| Year | Year | Binary variable that takes the value of 1 if the observation belongs to the year in question and 0, otherwise. |

References

- Abdelzaher, Angie, and Dina Abdelzaher. 2019. Women on Boards and Firm Performance in Egypt: Post the Arab Spring. The Journal of Developing Areas 53: 225–41. [Google Scholar] [CrossRef]

- Acker, Joan. 2012. Gendered organizations and intersectionality: Problems and possibilities. Equality, Diversity and Inclusion: An International Journal 31: 212–24. [Google Scholar] [CrossRef]

- Adams, Renée B., and Daniel Ferreira. 2009. Women in the boardroom and their impact on governance and performance. Journal of Financial Economics 94: 291–309. [Google Scholar] [CrossRef] [Green Version]

- Adams, Renée B., Jakob de Haan, Siri Terjesen, and Hans van Ees. 2015. Board diversity: Moving the field forward. Corporate Governance: An International Review 23: 77–82. [Google Scholar] [CrossRef]

- Becker, Gary S. 2009. Human Capital: A Theoretical and Empirical Analysis, with Special Reference to Education. Chicago: University of Chicago Press. [Google Scholar]

- Bennouri, Moez, Tawhid Chtioui, Haithem Nagati, and Mehdi Nekhili. 2018. Female board directorship and firm performance: What really matters? Journal of Banking & Finance 88: 267–91. [Google Scholar]

- Burke, Ronald J. 2000. Company size, board size and numbers of women corporate directors. In Women on Corporate Boards of Directors. Dordrecht: Springer, pp. 157–67. [Google Scholar]

- Campbell, Kevin, and Antonio Mínguez-Vera. 2008. Gender diversity in the boardroom and firm financial performance. Journal of Business Ethics 83: 435–51. [Google Scholar] [CrossRef]

- Campbell, Kevin, and Antonio Mínguez Vera. 2010. Female board appointments and firm valuation: Short and long-term effects. Journal of Management & Governance 14: 37–59. [Google Scholar]

- Carter, David A., Betty J. Simkins, and W. Gary Simpson. 2003. Corporate governance, board diversity, and firm value. Financial Review 38: 33–53. [Google Scholar] [CrossRef]

- Carter, David A., Frank D’Souza, Betty J. Simkins, and W. Gary Simpson. 2010. The gender and ethnic diversity of US boards and board committees and firm financial performance. Corporate Governance: An International Review 18: 396–414. [Google Scholar] [CrossRef]

- Cotter, David A., Joan M. Hermsen, Seth Ovadia, and Reeve Vanneman. 2001. The glass ceiling effect. Social Forces 80: 655–81. [Google Scholar] [CrossRef]

- Eagly, Alice H., and Linda L. Carli. 2003. The female leadership advantage: An evaluation of the evidence. The Leadership Quarterly 14: 807–34. [Google Scholar] [CrossRef]

- Flynn, Patricia M., and Susan M. Adams. 2004. Changes will bring woman oards: Research shows that geography and industry account for considerable discrepancies in the prevalence of women directors, as does company size. But trends are favorable for more women joining corporate boards. Financial Executive 20: 32–35. [Google Scholar]

- Gabrielsson, Jonas, Morten Huse, and Alessandro Minichilli. 2007. Understanding the leadership role of the board chairperson through a team production approach. International Journal of Leadership Studies 3: 21–39. [Google Scholar]

- Gaio, Cristina, and Tiago Cruz Gonçalves. 2022. Gender diversity on the board and firms’ corporate social responsibility. International Journal of Financial Studies 10: 15. [Google Scholar] [CrossRef]

- Galbreath, Jeremy. 2011. Are there gender-related influences on corporate sustainability? A study of women on boards of directors. Journal of Management and Organization 17: 17–38. [Google Scholar] [CrossRef]

- Gonçalves, Tiago, Cristina Gaio, and Frederico Robles. 2018. The impact of Working Capital Management on firm profitability in different economic cycles: Evidence from the United Kingdom. Economics and Business Letters 7: 70–75. [Google Scholar] [CrossRef] [Green Version]

- Gonçalves, Tiago, Cristina Gaio, and Tatiana Santos. 2019. Women on the board: Do they manage earnings? empirical evidence from european listed firms. Revista Brasileira de Gestao de Negocios 21: 582–97. [Google Scholar] [CrossRef]

- Gonçalves, Tiago, Cristina Gaio, and Carlos Lélis. 2020. Accrual mispricing: Evidence from European sovereign debt crisis. Research in International Business and Finance 52: 101111. [Google Scholar] [CrossRef]

- Gonçalves, Tiago, Diego Pimentel, and Cristina Gaio. 2021. Risk and performance of European green and conventional funds. Sustainability 13: 4226. [Google Scholar] [CrossRef]

- Habib, Ahsan, and Mahmud Hossain. 2013. CEO/CFO characteristics and financial reporting quality: A review. Research in Accounting Regulation 25: 88–100. [Google Scholar] [CrossRef]

- Hillman, Amy J., Albert A. Cannella Jr., and Ira C. Harris. 2002. Women and Racial Minorities in the Boardroom: How Do Directors Differ? Journal of Management 28: 747–63. [Google Scholar] [CrossRef]

- Hillman, Amy J., Christine Shropshire, and Albert A. Cannella Jr. 2007. Organizational Predictors of Women on Corporate Boards. Academy of Management Journal 50: 941–52. [Google Scholar] [CrossRef] [Green Version]

- Isidro, Helena, and Márcia Sobral. 2015. The Effects of Women on Corporate Boards on Firm Value, Financial Performance, and Ethical and Social Compliance. Journal of Business Ethics 132: 1–19. [Google Scholar] [CrossRef]

- Jedi, Firas Farhan, and Sabri Nayan. 2018. An empirical evidence on the effect of women board representation on firm performance of companies listed in Iraq stock exchange. Business and Economic Horizons 14: 117–31. [Google Scholar] [CrossRef] [Green Version]

- Kakabadse, Nada K., Catarina Figueira, Katerina Nicolopoulou, Jessica Hong Yang, Andrew P. Kakabadse, and Mustafa F. Özbilgin. 2015. Gender Diversity and Board Performance: Women’s Experiences and Perspectives. Human Resource Management 54: 265–81. [Google Scholar] [CrossRef] [Green Version]

- Kesner, Idalene F. 1988. Directors’ Characteristics and Committee Membership: An Investigation of Type, Occupation, Tenure, and Gender. Academy of Management Journal 31: 66–84. [Google Scholar]

- Konrad, Alison M., J. Edgar Ritchie Jr., Pamela Lieb, and Elizabeth Corrigall. 2000. Sex Differences and Similarities in Job Attribute Preferences: A Meta-Analysis. Psychological Bulletin 126: 593–641. [Google Scholar] [CrossRef] [PubMed]

- Konrad, Alison M., Vicki Kramer, and Sumru Erkut. 2008. The impact of three or more women on corporate boards. Organizational Dynamics 37: 145–64. [Google Scholar] [CrossRef]

- Lins, Karl V. 2003. Equity ownership and firm value in emerging markets. Journal of Financial and Quantitative Analysis 38: 159–84. [Google Scholar] [CrossRef] [Green Version]

- Marinova, Joana, Janneke Plantenga, and Chantal Remery. 2016. Gender diversity and firm performance: Evidence from Dutch and Danish boardrooms. The International Journal of Human Resource Management 27: 1777–90. [Google Scholar] [CrossRef]

- Oakley, Judith G. 2000. Gender-based Barriers to Senior Management Positions: Understanding the Scarcity of Female CEOs. Journal of Business Ethics 27: 321–34. [Google Scholar] [CrossRef]

- Peni, Emilia. 2014. CEO and Chairperson characteristics and firm performance. Journal of Management & Governance 18: 185–205. [Google Scholar]

- Reguera-Alvarado, Nuria, Pilar de Fuentes, and Joaquina Laffarga. 2017. Does board gender diversity influence financial performance? Evidence from Spain. Journal of Business Ethics 141: 337–50. [Google Scholar] [CrossRef]

- Ryan, Michelle K., and S. Alexander Haslam. 2007. The glass cliff: Exploring the dynamics surrounding the appointment of women to precarious leadership positions. Academy of Management Review 32: 549–72. [Google Scholar] [CrossRef]

- Seierstad, Cathrine, Gillian Warner-Søderholm, Mariateresa Torchia, and Morten Huse. 2017. Increasing the Number of Women on Boards: The Role of Actors and Processes. Journal of Business Ethics 141: 289–315. [Google Scholar] [CrossRef]

- Shehata, Nermeen, Ahmed Salhin, and Moataz El-Helaly. 2017. Board diversity and firm performance: Evidence from the U.K. SMEs. Applied Economics 49: 4817–32. [Google Scholar] [CrossRef]

- Shleifer, Andrei, and Robert W. Vishny. 1997. A Survey of Corporate Governance. The Journal of Finance 52: 737–83. [Google Scholar] [CrossRef]

- Singh, Val, Siri Terjesen, and Susan Vinnicombe. 2008. Newly appointed directors in the boardroom: How do women and men differ? European Management Journal 26: 48–58. [Google Scholar] [CrossRef] [Green Version]

- Singh, Amit Kumar, Shubham Singhania, and Varda Sardana. 2019. Do Women on Boards affect Firm’s Financial Performance? Evidence from Indian IPO Firms. Australasian Accounting, Business and Finance Journal 13: 53–68. [Google Scholar] [CrossRef]

- Smith, Wanda J., Richard E. Wokutch, K. Vernard Harrington, and Bryan S. Dennis. 2001. An examination of the influence of diversity and stakeholder role on corporate social orientation. Business and Society 40: 266–94. [Google Scholar] [CrossRef]

- Terjesen, Siri, Ruth Sealy, and Val Singh. 2009. Women directors on corporate boards: A review and research agenda. Corporate Governance: An International Review 17: 320–37. [Google Scholar] [CrossRef] [Green Version]

- Tharenou, Phyllis, Shane Latimer, and Denise Conroy. 1994. How do you Make it to the Top? An Examination of Influences on Women’s and Men’s Managerial Advancement. Academy of Management Journal 37: 899–931. [Google Scholar]

- Van der Walt, Nicholas, and Coral Ingley. 2003. Board Dynamics and the Influence of Professional Background, Gender and Ethnic Diversity of Directors. Corporate Governance 11: 218–34. [Google Scholar] [CrossRef]

| Country | Observations | % |

|---|---|---|

| Austria | 310 | 2.2 |

| Belgium | 554 | 4.0 |

| Denmark | 606 | 4.3 |

| Finland | 721 | 5.2 |

| France | 3.069 | 22.0 |

| Germany | 2.530 | 18.1 |

| Greece | 937 | 6.7 |

| Ireland | 262 | 1.9 |

| Italy | 1.183 | 8.5 |

| Luxembourg | 215 | 1.5 |

| Netherlands | 567 | 4.1 |

| Portugal | 265 | 1.9 |

| Spain | 695 | 5.0 |

| Sweden | 2.066 | 14.8 |

| Total | 13.980 | 100 |

| Sector of Activity | Observations | % |

|---|---|---|

| Agriculture, forestry and fishing | 168 | 1.2 |

| Mining and quarrying | 270 | 1.9 |

| Manufacturing | 6.933 | 49.6 |

| Electricity, gas, steam, and air conditioning supply | 399 | 2.9 |

| Water supply; sewerage, waste management, and remediation activities | 103 | 0.7 |

| Construction | 446 | 3.2 |

| Wholesale and retail trade; repair of motor vehicles and motorcycles | 1.181 | 8.4 |

| Transportation and storage | 464 | 3.3 |

| Accommodation and food service activities | 202 | 1.4 |

| Information and Communication | 2.169 | 15.5 |

| Professional, scientific, and technical activities | 638 | 4.6 |

| Administrative and support service activities | 356 | 2.5 |

| Human health and social work activities | 207 | 1.5 |

| Arts, entertainment and recreation | 273 | 2.0 |

| Other service activities | 171 | 1.2 |

| Total | 13.980 | 100 |

| Mean | Standard Deviation | Median | Minimum | Maximum | |

|---|---|---|---|---|---|

| Tobin’s Q | 1.068 | 1.978 | 0.643 | 0.002 | 145.923 |

| ROA | 0.021 | 0.112 | 0.031 | −1.045 | 2.501 |

| Operating Margin | 0.064 | 1.05 | 0.060 | −37.380 | 101.388 |

| Chair_W | 0.033 | 0.178 | 0 | 0 | 1 |

| CEO_W | 0.042 | 0.200 | 0 | 0 | 1 |

| CFO_W | 0.056 | 0.230 | 0 | 0 | 1 |

| Gov_W | 0.223 | 0.416 | 0 | 0 | 1 |

| Size | 19.437 | 2.391 | 19.247 | 11.928 | 26.850 |

| Lev | 0.551 | 0.191 | 0.563 | 0.003 | 0.999 |

| Growth | 0.250 | 9.668 | 0.041 | −92.943 | 986.455 |

| Age | 3.510 | 0.924 | 3.401 | 0 | 6.482 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) Tobin’s Q | 1.000 | ||||||||||

| (2) ROA | 0.137 *** | 1.000 | |||||||||

| (3) Operating Margin | 0.010 | 0.126 *** | 1.000 | ||||||||

| (4) Char_W | 0.035 *** | −0.013 | −0.008 | 1.000 | |||||||

| (5) CEO_W | 0.030 *** | −0.016 * | −0.005 | 0.226 *** | 1.000 | ||||||

| (6) CFO_W | 0.047 *** | 0.017 ** | −0.023 *** | 0.060 *** | 0.104 *** | 1.000 | |||||

| (7) GOV_W | 0.040 *** | 0.046 *** | 0.018 ** | -0.068 *** | −0.050 *** | −0.070 *** | 1.000 | ||||

| (8) Size | −0.145 *** | 0.220 *** | 0.049 *** | 0.007 | −0.019 ** | 0.010 | 0.006 | 1.000 | |||

| (9) Lev | −0.241 *** | −0.192 *** | 0.000 | 0.006 | −0.033 *** | −0.017 ** | −0.052 *** | 0.260 *** | 1.000 | ||

| (10) Growth | 0.013 | 0.004 | 0.006 | −0.003 | −0.002 | −0.005 | −0.008 | −0.014 * | −0.028 ** | 1.000 | |

| (11) Age | −0.110 *** | 0.126 *** | 0.017 ** | 0.017 * | −0.021 ** | −0.016 * | 0.110 ** | 0.280 *** | 0.072 *** | −0.014 * | 1.000 |

| Tobin’s Q (1) | Tobin’s Q (2) | Tobin’s Q (3) | Tobin’s Q (4) | |

|---|---|---|---|---|

| ROA | 2.405 *** | - | 2.386 *** | |

| (0.290) | (0.289) | |||

| Operating margin | - | 0.030 *** | 0.028 *** | |

| (0.008) | (0.008) | |||

| Chair_W | 0.397 | 0.380 | 0.424 | 0.409 |

| (0.347) | (0.346) | (0.346) | (0.346) | |

| CEO_W | 0.106 | 0.082 | 0.118 | 0.095 |

| (0.107) | (0.108) | (0.107) | (0.108) | |

| CFO_W | 0.328 *** | 0.347 *** | 0.351 *** | 0.371 *** |

| (0.062) | (0.063) | (0.062) | (0.063) | |

| Gov_W | - | - | 0.198 *** | 0.212 *** |

| (0.032) | (0.033) | |||

| Size | −0.087 *** | −0.056 *** | −0.086 *** | −0.056 *** |

| (0.009) | (0.009) | (0.009) | (0.009) | |

| Lev | −1.864 *** | −2.240 *** | −1.841 *** | −2.213 *** |

| (0.111) | (0.109) | (0.112) | (0.110) | |

| Growth | 0.001 | 0.001 | 0.001 | 0.001 |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Age | −0.182 *** | −0.162 *** | −0.192 *** | −0.173 *** |

| (0.025) | (0.024) | (0.024) | (0.024) | |

| Constant | 4.327 *** | 3.929 *** | 4.292 *** | 3.894 *** |

| (0.295) | (0.291) | (0.296) | (0.291) | |

| Observations | 13.980 | 13.980 | 13.980 | 13.980 |

| Adjusted R2 | 0.090 | 0.074 | 0.092 | 0.076 |

| F-statistic | 104.882 | 98.899 | 100.519 | 95.954 |

| P-value | 0.000 | 0.000 | 0.000 | 0.000 |

| Tobin’s Q (1) | Tobin’s Q (2) | Tobin’s Q (3) | Tobin’s Q (4) | |

|---|---|---|---|---|

| ROA | 2.399 *** | - | 2.420 *** | - |

| (0.290) | (0.289) | |||

| Operating Margin | - | 0.029 *** | - | 0.030 *** |

| (0.008) | (0.009) | |||

| Chair_W | 0.576 | 0.565 | 0.207 | 0.198 |

| (0.429) | (0.429) | (0.266) | (0.265) | |

| CEO_W | 0.154 | 0.132 | 0.129 | 0.103 |

| (0.123) | (0.124) | (0.096) | (0.099) | |

| CFO_W | 0.307 *** | 0.324 *** | 0.495 *** | 0.502 *** |

| (0.063) | (0.065) | (0.096) | (0.096) | |

| Shareholder_Chair_W | −0.881 ** | −0.907 ** | - | - |

| (0.426) | (0.425) | |||

| Shareholder_CEO_W | −0.338 ** | −0.346 ** | - | - |

| (0.153) | (0.157) | |||

| Shareholder_CFO_W | 0.343 | 0.363 | - | - |

| (0.335) | (0.374) | |||

| Change_Chair_W | - | - | 0.635 * | 0.603 |

| (0.381) | (0.381) | |||

| Change_CEO_W | - | - | −0.062 | −0.055 |

| (0.104) | (0.107) | |||

| Change_CFO_W | - | - | −0.217 | −0.201 |

| (0.206) | (0.205) | |||

| Size | −0.088 *** | −0.058 *** | −0.086 *** | −0.056 *** |

| (0.010) | (0.009) | (0.009) | (0.009) | |

| Lev | −1.858 *** | −2.233 *** | −1.857 *** | −2.236 *** |

| (0.110) | (0.108) | (0.108) | (0.107) | |

| Growth | 0.001 | 0.001 | 0.001 | 0.001 |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Age | −0.179 *** | −0.159 *** | −0.180 *** | −0.160 *** |

| (0.024) | (0.024) | (0.023) | (0.023) | |

| Constant | 4.352 *** | 3.955 *** | 4.311 *** | 3.911 *** |

| (0.299) | (0.294) | (0.285) | (0.279) | |

| Observations | 13.980 | 13.980 | 13.980 | 13.980 |

| Adjusted R2 | 0.092 | 0.075 | 0.092 | 0.076 |

| F-statistic | 77.114 | 72.930 | 77.683 | 73.237 |

| P-value | 0.000 | 0.000 | 0.000 | 0.000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gonçalves, T.C.; Gaio, C.; Rodrigues, M. The Impact of Women Power on Firm Value. Adm. Sci. 2022, 12, 93. https://doi.org/10.3390/admsci12030093

Gonçalves TC, Gaio C, Rodrigues M. The Impact of Women Power on Firm Value. Administrative Sciences. 2022; 12(3):93. https://doi.org/10.3390/admsci12030093

Chicago/Turabian StyleGonçalves, Tiago Cruz, Cristina Gaio, and Micaela Rodrigues. 2022. "The Impact of Women Power on Firm Value" Administrative Sciences 12, no. 3: 93. https://doi.org/10.3390/admsci12030093

APA StyleGonçalves, T. C., Gaio, C., & Rodrigues, M. (2022). The Impact of Women Power on Firm Value. Administrative Sciences, 12(3), 93. https://doi.org/10.3390/admsci12030093