Agricultural Land Price Convergence: Evidence from Polish Provinces

Abstract

:1. Introduction

2. Methodology and Data

2.1. Methodology of Testing Agricultural Land Price Convergence

- Construct the cross-sectional variance ratio using the formula:where denotes the transition path of province in comparison to the panel average at time . In other words, a given transition path of a province represents price behaviour over time in relation to the average land price calculated based on data from all provinces. It should be noted that when for all , as , or alternatively when , as , there is land price convergence across provinces, i.e., the price differential between the provinces is reduced in time.

- Run the log t regression:where , for . For a small sample , however, it is suggested to set equal to 0.3.

- Assess the convergence of the entire sample using the t-statistic If , the null hypothesis is rejected, which indicates that land prices across all provinces tend to diverge. There is still the possibility, however, that convergence clubs occur in the data, i.e., the group of provinces where prices share a common trend in the long run.

- Extract the trend component from analysed time series (it is also required at previous stages).

- Order the provinces in the panel in decreasing order according to prices in the last period.

- Form a core group of provinces () in the panel based on the log t regression maximising with .

- Add to the core group one province and run the log t regression and check if or , respectively for large and small . If true, add the new province to the core group.

- For the rest of provinces that do not meet the condition outlined in previous step run the log t regression and check if . If true, the second convergence clubs is established. If not, repeat the previous steps to verify if the remaining provinces can be further subdivided.

- Try to merge initial convergence clubs. For example if club 1 and club 2 meet the convergence hypothesis merge the clubs into new club. Next, try to merge the new club with initial club 3. Continue this procedure until no clubs can be merged.

2.2. Methodology of Studying the Driving Forces of Convergence

2.3. Study Area

2.4. Data—Studying the Convergence

2.5. Data—Studying the Driving Forces of the Convergence

3. Results and Discussion

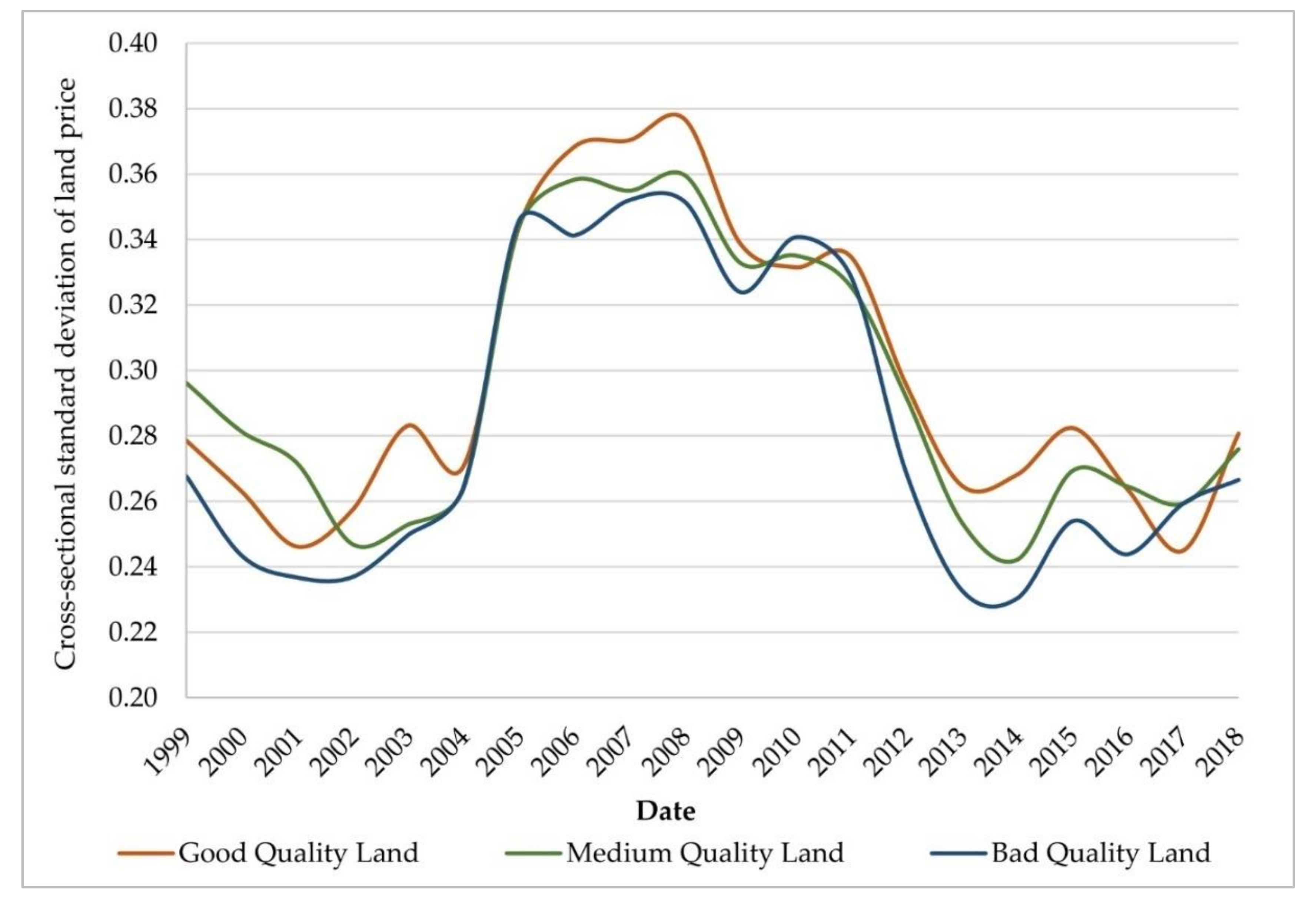

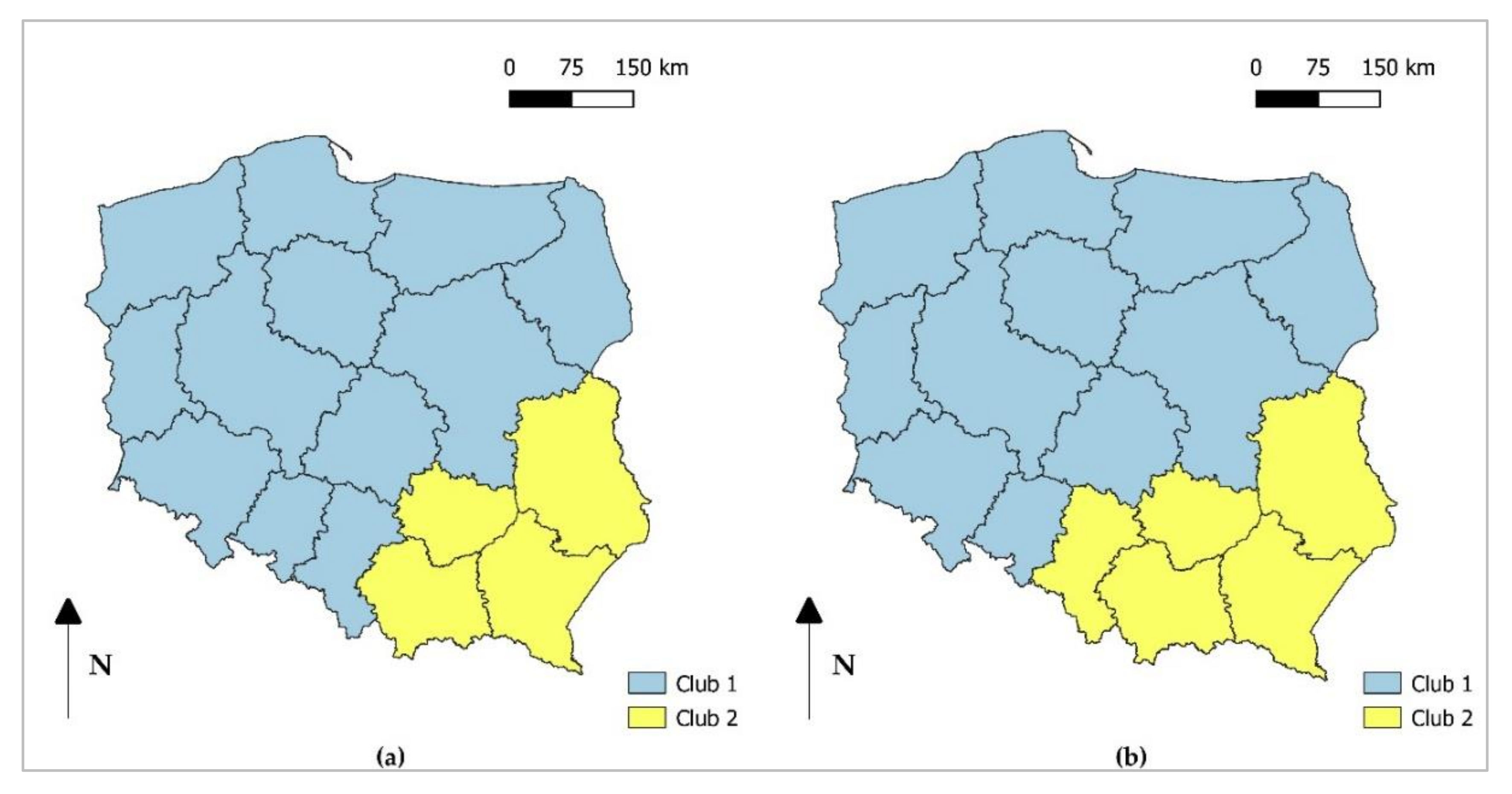

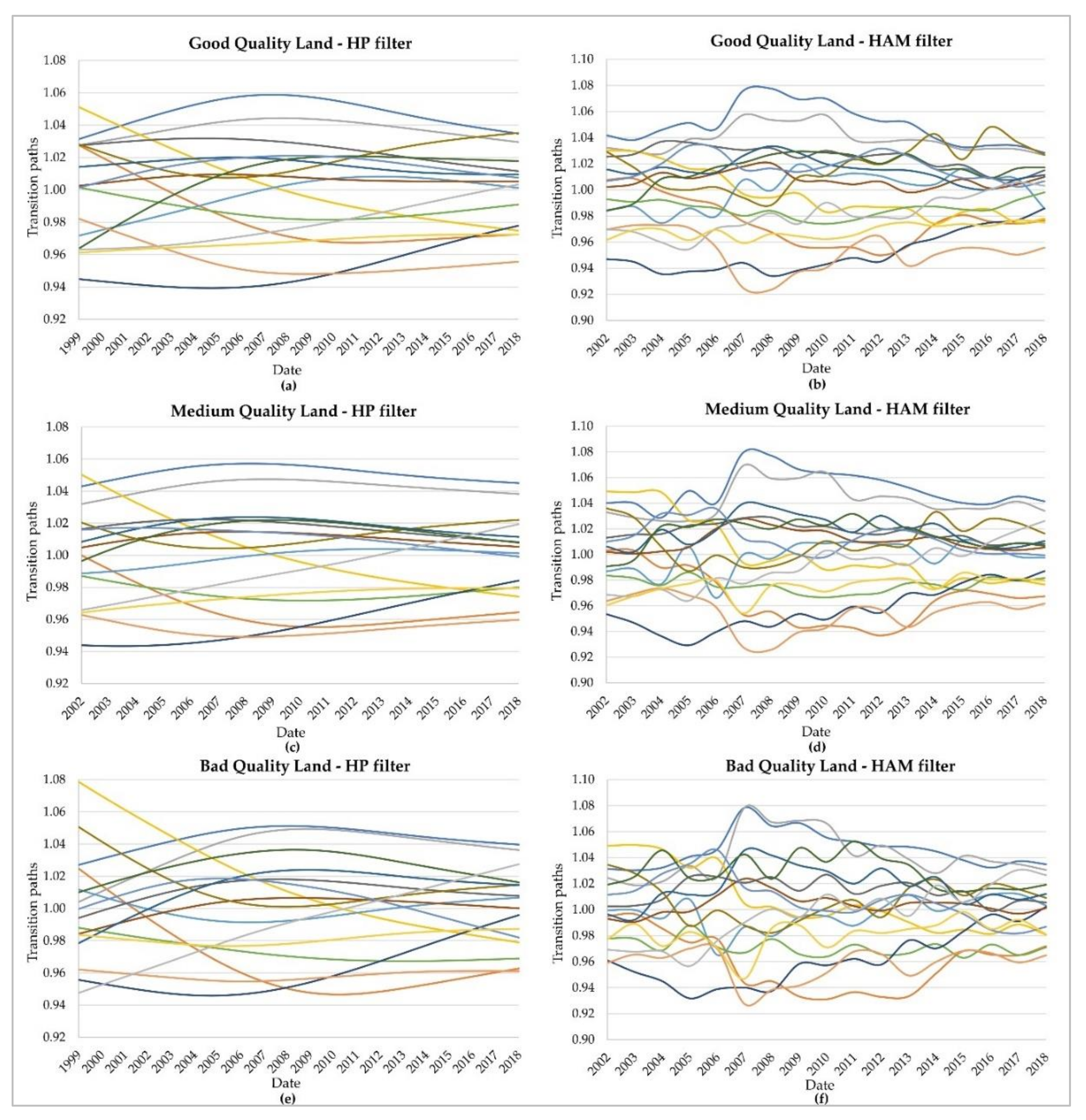

3.1. Studying Land Price Convergence

3.2. Studying the Driving Forces of Convergence

4. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Hubacek, K.; Fischer, G. The Role of Land in Economic Theory; International Institute for Applied Systems Analysis (IIASA): Laxenburg, Austria, 2002; pp. 1–48. [Google Scholar]

- Gołębiewska, B.; Stefańczyk, J. Zmiany cen gruntów rolnych w Polsce po wejściu w życie nowej ustawy o kształtowaniu ustroju rolnego. Rocz. Nauk. Stowarzyszenia Ekon. Rol. Agrobiz. 2016, 18, 29–34. [Google Scholar]

- Qiang, W.; Niu, S.; Liu, A.; Kastner, T.; Bie, Q.; Wang, X.; Cheng, S. Trends in global virtual land trade in relation to agricultural products. Land Use Policy 2020, 92, 104439. [Google Scholar] [CrossRef]

- Firlej, K. Rozwój Przemysłu Rolno-Spożywczego w Sektorze Agrobiznesu i Jego Determinanty; Wydawnictwo Uniwersytetu Ekonomicznego w Krakowie: Krakow, Poland, 2008. [Google Scholar]

- Yang, X.; Odening, M.; Ritter, M. The Spatial and Temporal Diffusion of Agricultural Land Prices. Land Econ. 2019, 95, 108–123. [Google Scholar] [CrossRef] [Green Version]

- Grau, A.; Odening, M.; Ritter, M. Land price diffusion across borders—The case of Germany. Appl. Econ. 2019, 1–18. [Google Scholar] [CrossRef]

- Yang, X.; Ritter, M.; Odening, M. Testing for regional convergence of agricultural land prices. Land Use Policy 2017, 64, 64–75. [Google Scholar] [CrossRef]

- Carmona, J.; Roses, J.R. Land markets and agrarian backwardness (Spain, 1904–1934). Eur. Rev. Econ. Hist. 2012, 16, 74–96. [Google Scholar] [CrossRef] [Green Version]

- Thomson, D.N.; Lyne, M.C. A land rental market in Kwazulu: Implications for farming efficiency. Agrekon 1991, 30, 287–290. [Google Scholar] [CrossRef] [Green Version]

- Engsted, T. Do farmland prices reflect rationally expected future rents? Appl. Econ. Lett. 1998, 5, 75–79. [Google Scholar] [CrossRef]

- Czyżewski, B.; Kułyk, P.; Kryszak, Ł. Drivers for farmland value revisited: Adapting the returns discount model (RDM) to the sustainable paradigm. Econ. Res. Ekon. Istraživanja 2019, 32, 2080–2098. [Google Scholar] [CrossRef] [Green Version]

- Tegene, A.; Kuchler, F.R. Evidence on the existence of speculative bubbles in farmland prices. J. Real Estate Finan. Econ. 1993, 6, 223–236. [Google Scholar] [CrossRef]

- Cirera, X.; Arndt, C. Measuring the impact of road rehabilitation on spatial market efficiency in maize markets in Mozambique. Agric. Econ. 2008, 39, 17–28. [Google Scholar] [CrossRef] [Green Version]

- Cherevyk, D.; Hamulczuk, M. Ukraiński rynek kukurydzy na tle zmian światowych. Zesz. Nauk. SGGW Warszawie Probl. Rol. Światowego 2018, 18, 33–43. [Google Scholar] [CrossRef] [Green Version]

- Goldberg, P.K.; Verboven, F. Market integration and convergence to the Law of One Price: Evidence from the European car market. J. Int. Econ. 2005, 65, 49–73. [Google Scholar] [CrossRef] [Green Version]

- Goodwin, B.K.; Piggott, N.E. Spatial Market Integration in the Presence of Threshold Effects. Am. J. Agric. Econ. 2001, 83, 302–317. [Google Scholar] [CrossRef] [Green Version]

- Hamulczuk, M.; Makarchuk, O.; Sica, E. Price Behaviour and Market Integration: Preliminary Evidencefrom the Ukrainian and European Union Rapeseed Markets. Zesz. Nauk. SGGW Warszawie Probl. Rol. Światowego 2019, 19, 47–58. [Google Scholar] [CrossRef]

- Waights, S. Does the law of one price hold for hedonic prices? Urban Stud. 2018, 55, 3299–3317. [Google Scholar] [CrossRef]

- Twardowska, A. Konwergencja typu sigma cen gruntów rolnych w państwach Unii Europejskiej. Zesz. Nauk. SGGW Warszawie Probl. Rol. Światowego 2019, 19, 133–143. [Google Scholar] [CrossRef] [Green Version]

- Wyrzykowski, P. Konwergencja cen żywności w Unii Europejskiej. Rocz. Nauk. Stowarzyszenia Ekon. Rol. Agrobiz. 2015, 17, 356–361. [Google Scholar]

- Zawojska, A. Zróżnicowanie i konwergencja cen dóbr konsumpcyjnych w integrującej się Europie. Rocz. Ekon. Rol. Rozw. Obsz. Wiej. 2012, 99, 16–32. [Google Scholar]

- Roman, M. Spatial Integration of the Milk Market in Poland. Sustainability 2020, 12, 1471. [Google Scholar] [CrossRef] [Green Version]

- Nalepka, A.; Tomal, M. Identyfikacja czynników kształtujących ceny ofertowe deweloperskich lokali mieszkalnych na obszarze jednostki ewidencyjnej Nowa Huta. Świat Nieruchom. 2016, 11–18. [Google Scholar] [CrossRef]

- Małkowska, A.; Uhruska, M.; Tomal, M. Age and Experience versus Susceptibility to Client Pressure among Property Valuation Professionals—Implications for Rethinking Institutional Framework. Sustainability 2019, 11, 6759. [Google Scholar] [CrossRef] [Green Version]

- Głuszak, M.; Marona, B. Heterogeneity and clustering of housing demand: Case study. J. Int. Stud. 2011, 4, 89–97. [Google Scholar] [CrossRef] [PubMed]

- Phillips, P.C.B.; Sul, D. Transition Modeling and Econometric Convergence Tests. Econometrica 2007, 75, 1771–1855. [Google Scholar] [CrossRef] [Green Version]

- Phillips, P.C.B.; Sul, D. Economic transition and growth. J. Appl. Econ. 2009, 24, 1153–1185. [Google Scholar] [CrossRef] [Green Version]

- Tomal, M. House Price Convergence on the Primary and Secondary Markets: Evidence from Polish Provincial Capitals. Real Estate Manag. Valuat. 2019, 27, 62–73. [Google Scholar] [CrossRef] [Green Version]

- Young, A.T.; Higgins, M.J.; Levy, D. Sigma Convergence versus Beta Convergence: Evidence from U.S. County-Level Data. J. Money Credit Bank. 2008, 40, 1083–1093. [Google Scholar] [CrossRef]

- Bai, C.; Mao, Y.; Gong, Y.; Feng, C. Club Convergence and Factors of Per Capita Transportation Carbon Emissions in China. Sustainability 2019, 11, 539. [Google Scholar] [CrossRef] [Green Version]

- Matysiak, G.; Olszewski, K. A panel analysis of Polish regional cities: Residential price convergence in the primary market. NBP Work. Pap. 2019, 316, 1–39. [Google Scholar] [CrossRef] [Green Version]

- Du, K. Econometric convergence test and club clustering using Stata. Stata J. 2017, 882–900. [Google Scholar] [CrossRef]

- Kim, Y.S.; Rous, J.J. House price convergence: Evidence from US state and metropolitan area panels. J. Hous. Econ. 2012, 21, 169–186. [Google Scholar] [CrossRef]

- Schnurbus, J.; Haupt, H.; Meier, V. Economic Transition and Growth: A Replication. J. Appl. Econom. 2017, 32, 1039–1042. [Google Scholar] [CrossRef]

- Choi, C.-Y.; Wang, X. Discontinuity of output convergence within the united states: Why has the course changed? Econ. Inq. 2015, 53, 49–71. [Google Scholar] [CrossRef]

- Borsi, M.T.; Metiu, N. The evolution of economic convergence in the European Union. Empir. Econ. 2015, 48, 657–681. [Google Scholar] [CrossRef]

- Blanco, F.; Delgado, F.; Presno, M. R&D expenditure in the EU: Convergence or divergence? Econ. Res. 2020, 33, 1685–1710. [Google Scholar] [CrossRef]

- Wang, S.; Yang, Z.; Liu, H. Impact of urban economic openness on real estate prices: Evidence from thirty-five cities in China. China Econ. Rev. 2011, 22, 42–54. [Google Scholar] [CrossRef]

- Li, Q.; Chand, S. House prices and market fundamentals in urban China. Habitat Int. 2013, 40, 148–153. [Google Scholar] [CrossRef]

- Greene, W.H. Econometric Analysis, 8th ed.; Pearson: New York, NY, USA, 2018. [Google Scholar]

- Galvao, A.F. Quantile regression for dynamic panel data with fixed effects. J. Econom. 2011, 164, 142–157. [Google Scholar] [CrossRef]

- Zhu, H.; Li, Z.; Guo, P. The impact of income, economic openness and interest rates on housing prices in China: Evidence from dynamic panel quantile regression. Appl. Econ. 2018, 50, 4086–4098. [Google Scholar] [CrossRef]

- Hausman, J.A. Specification Tests in Econometrics. Econometrica 1978, 46, 1251. [Google Scholar] [CrossRef] [Green Version]

- Pesaran, M.H. General Diagnostic Tests for Cross Section Dependence in Panels; Faculty of Economics, University of Cambridge: Cambridge, UK, 2004; CWPE0435. [Google Scholar] [CrossRef]

- Breusch, T.S.; Pagan, A.R. The Lagrange Multiplier Test and its Applications to Model Specification in Econometrics. Rev. Econ. Stud. 1980, 47, 239. [Google Scholar] [CrossRef]

- Driscoll, J.C.; Kraay, A.C. Consistent Covariance Matrix Estimation with Spatially Dependent Panel Data. Rev. Econ. Stat. 1998, 80, 549–560. [Google Scholar] [CrossRef]

- Hodrick, R.J.; Prescott, E.C. Postwar U.S. Business Cycles: An Empirical Investigation. J. Money Credit Bank. 1997, 29, 1. [Google Scholar] [CrossRef]

- Hamilton, J.D. Why You Should Never Use the Hodrick-Prescott Filter. Rev. Econ. Stat. 2018, 100, 831–843. [Google Scholar] [CrossRef]

- Firlej, K.; Kubala, S. Ceny ziemi rolnej w Polsce na tle Unii Europejskiej. Zesz. Nauk. UEK 2018, 159–171. [Google Scholar] [CrossRef]

- Kuźmiński, W. Ekonometryczny model cen gruntów rolnych. Studia Pr. WNEiZ 2015, 42, 227–240. [Google Scholar] [CrossRef] [Green Version]

- Lovrinčević, Ž.; Vizek, M. Agricultural land in the new EU member states and Croatia: Prices, affordabilities and convergence potential. Ekon. Pregl. 2009, 60, 28–49. [Google Scholar]

- Kulikowski, R. Produktywność i towarowość rolnictwa w Polsce. Rozw. Reg. Polityka Reg. 2014, 95. [Google Scholar] [CrossRef] [Green Version]

- Kocur-Bera, K. Determinants of agricultural land price in Poland—A case study covering a part of the Euroregion Baltic. Cah. Agric. 2016, 25, 25004. [Google Scholar] [CrossRef] [Green Version]

- Livanis, G.; Moss, C.B.; Breneman, V.E.; Nehring, R.F. Urban Sprawl and Farmland Prices. Am. J. Agric. Econ. 2006, 88, 915–929. [Google Scholar] [CrossRef]

- Tomal, M. The Impact of Macro Factors on Apartment Prices in Polish Counties: A Two-Stage Quantile Spatial Regression Approach. Real Estate Manag. Valuat. 2019, 27, 1–14. [Google Scholar] [CrossRef] [Green Version]

- Tomal, M. Moving towards a Smarter Housing Market: The Example of Poland. Sustainability 2020, 12, 683. [Google Scholar] [CrossRef] [Green Version]

- Nowak, K. Ceny mieszkań a wynagrodzenie i bezrobocie—Analiza z wykorzystaniem modeli wektorowo--autoregresyjnych na przykładzie Krakowa. Probl. Rozw. Miast 2014, 4, 20–33. [Google Scholar]

- Drescher, K.; McNamara, K.T. Determinants of German farmland prices. In ERSA Conference Papers, Proceedings of the 39th Congress of the European Regional Science Association, Dublin, Ireland, 23–27 August, 1999; European Regional Science Association (ERSA): Dublin, Ireland, 1999. [Google Scholar]

- Breustedt, G.; Habermann, H. The Incidence of EU Per-Hectare Payments on Farmland Rental Rates: A Spatial Econometric Analysis of German Farm-Level Data: Incidence of EU Per-Hectare Payments on Farmland Rental Rates. J. Agric. Econ. 2011, 62, 225–243. [Google Scholar] [CrossRef] [Green Version]

- Gloy, B.A.; Boehlje, M.; Dobbins, C.L.; Hurt, C.; Baker, T.G. Are economic fundamentals driving farmland values? Choices 2011, 26, 1–6. [Google Scholar] [CrossRef]

- Sherrick, B.J. Understanding Farmland Values in a Changing Interest Rate Environment. Choices 2018, 33, 1–8. [Google Scholar] [CrossRef]

- Gluszak, M. Expectations and House Prices: An Exploratory Analysis. World Real Estate J. 2019, 4, 15–28. [Google Scholar] [CrossRef]

- Czyżewski, B.; Trojanek, R. Czynniki wartości ziemi rolnej w kontekście zróżnicowanych funkcji obszarów wiejskich w Polsce. Zagadnienia Ekon. Rolnej 2016, 347, 3–25. [Google Scholar] [CrossRef] [Green Version]

- Bellemare, M.F. Rising Food Prices, Food Price Volatility, and Social Unrest. Am. J. Agric. Econ. 2015, 97, 1–21. [Google Scholar] [CrossRef] [Green Version]

- Fousekis, P. Convergence of Relative State-level Per Capita Incomes in the United States Revisited. J. Reg. Anal. Policy 2007, 37, 80–89. [Google Scholar]

- Chrzanowska, M. Spatial analysis of agricultural land prices by regions in Poland. Econ. Sci. Rural Dev. 2016, 42, 30–37. [Google Scholar]

- Batóg, B.; Foryś, I. Structural Changes on Polish Housing Market: Has the Market Returned to the Level Before the Crisis? In Eurasian Economic Perspectives, Proceedings of the 25th Eurasia Business and Economics Society Conference, Berlin, Germany, 23–25 May 2018; Bilgin, M.H., Danis, H., Karabulut, G., Gözgor, G., Eds.; Springer International Publishing: Cham, Switzerland, 2020; pp. 55–69. [Google Scholar]

- Brzezicka, J.; Laszek, J.; Olszewski, K. An Analysis of the Relationships Between Domestic Real Estate Markets–A Systemic Approach. Real Estate Manag. Valuat. 2019, 27, 79–91. [Google Scholar] [CrossRef] [Green Version]

- Czyzewski, B.; Trojanek, R.; Matuszczak, A. The effects of use values, amenities and payments for public goods on farmland prices: Evidence from Poland. Acta Oeconomica 2018, 68, 135–158. [Google Scholar] [CrossRef]

- Delbecq, B.A.; Kuethe, T.H.; Borchers, A.M. Identifying the Extent of the Urban Fringe and Its Impact on Agricultural Land Values. Land Econ. 2014, 90, 587–600. [Google Scholar] [CrossRef]

- Schmutzler, A. The New Economic Geography. J. Econ. Surv. 1999, 13, 355–379. [Google Scholar] [CrossRef] [Green Version]

- Liu, L.; Ruiz, I. Convergence Hypothesis: Evidence from Panel Unit Root Test with Spatial Dependence. Ecos Econ. Lat. Am. J. Appl. Econ. 2006, 10, 37–56. [Google Scholar]

- Salim, R.; Hassan, K.; Rahman, S. Impact of R&D expenditures, rainfall and temperature variations in agricultural productivity: Empirical evidence from Bangladesh. Appl. Econ. 2019, 1–14. [Google Scholar] [CrossRef]

- Oladosu, G. Economic Impacts of Potential Foot and Mouth Disease Agroterrorism in the USA: A General Equilibrium Analysis. J. Bioterror. Biodef. 2012, s12. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | Urbanisation (%) | Salary (PLN) | GDP (PLN) | Agricultural Production (PLN) | Pigs (Units) | Agricultural Commodity Price (PLN) | Interest Rate (%) |

|---|---|---|---|---|---|---|---|

| 2001 | 4.63 | 1807.19 | 18,839.63 | 2684.21 | 52.48 | 58.35 | 14.5 |

| 2002 | 4.69 | 2081.07 | 19,594.13 | 3387.56 | 56.96 | 50.68 | 8.25 |

| 2003 | 4.83 | 2147.57 | 20,423.81 | 3255.69 | 55.44 | 52.39 | 5.88 |

| 2004 | 4.82 | 2238.16 | 22,518.13 | 3555.13 | 52.66 | 56.38 | 6.00 |

| 2005 | 4.90 | 2321.60 | 23,865.00 | 3930.75 | 55.98 | 45.00 | 5.00 |

| 2006 | 4.96 | 2439.83 | 25,755.63 | 3596.38 | 55.75 | 53.04 | 4.13 |

| 2007 | 4.96 | 2652.55 | 28,639.88 | 3988.50 | 52.13 | 78.47 | 4.63 |

| 2008 | 5.03 | 2919.96 | 31,039.63 | 4744.81 | 42.26 | 74.38 | 5.88 |

| 2009 | 5.09 | 3054.96 | 32,584.88 | 4798.94 | 42.63 | 57.56 | 3.88 |

| 2010 | 5.15 | 3181.44 | 34,160.06 | 4604.75 | 44.33 | 68.71 | 3.50 |

| 2011 | 5.23 | 3350.54 | 36,940.19 | 5238.25 | 38.83 | 92.48 | 4.13 |

| 2012 | 5.30 | 3471.52 | 38,343.88 | 6051.13 | 32.98 | 101.60 | 4.50 |

| 2013 | 5.38 | 3596.69 | 39,003.44 | 6774.31 | 31.98 | 92.67 | 3.13 |

| 2014 | 5.44 | 3719.73 | 40,510.19 | 7363.69 | 32.94 | 79.92 | 2.00 |

| 2015 | 5.51 | 3857.65 | 42,353.94 | 6656.50 | 30.63 | 77.46 | 1.50 |

| 2016 | 5.59 | 3993.79 | 43,766.81 | 6868.13 | 32.36 | 73.12 | 1.50 |

| 2017 | 5.66 | 4217.73 | 46,682.06 | 6741.13 | 34.45 | 78.69 | 1.50 |

| 2018 | 5.71 | 4497.43 | 49,567.56 | 7221.50 | 31.55 | 84.57 | 1.50 |

| Type of Land | (HP Filter) | t-Statistic (HP Filter) | (HAM Filter) | t-Statistic (HAM Filter) |

|---|---|---|---|---|

| Good-quality Land | −0.1847 | −1.5752 | 0.4224 | 2.5215 |

| Medium-quality Land | −0.2829 ** | −2.5140 | 0.4640 | 3.0044 |

| Bad-quality Land | −0.2543 ** | −2.0606 | 0.6404 | 4.3025 |

| Type of Land | Club 1 Provinces | (t-Statistic) | Club 2 Provinces | (t-Statistic) | ||

|---|---|---|---|---|---|---|

| Good-quality Land | 16 | −0.1847 | −1.5752 | 0 | NA | NA |

| Medium-quality Land | 12 | 0.2259 | 1.7515 | 4 | 1.5659 | 8.7746 |

| Bad-quality Land | 11 | 0.5579 | 2.8522 | 5 | 1.3886 | 5.1730 |

| Variable | Club 1 | Club 2 |

|---|---|---|

| Average farm size (ha) | 15.0 | 5.7 |

| Labour productivity (PLN) | 70,519.1 | 24,412.9 |

| Degree of commodity (%) | 95.6 | 88.8 |

| Land productivity per hectare of farmland (PLN) | 7081.4 | 7529.8 |

| Type of Land | Hausman | Pesaran | Breusch-Pagan |

|---|---|---|---|

| Good-quality Land | 75.13 *** | 14.78 *** | 325.02 *** |

| Medium-quality Land | 63.66 *** | 13.14 *** | 332.78 *** |

| Bad-quality Land | 58.00 *** | 10.96 *** | 282.02 *** |

| Variable | Good-Quality Land | Medium-Quality Land | Bad-Quality Land |

|---|---|---|---|

| 0.8374 *** | 0.9559 *** | 0.9875 *** | |

| −0.1436 | −0.2501 *** | −0.2756 *** | |

| Urbanisation | −0.3832 *** (−1.25) | −0.4259 *** (−1.45) | −0.5382 *** (−1.87) |

| Salary | −0.2194 (−0.72) | −0.0654 (−0.22) | 0.0835 (0.29) |

| Agricultural Production | 0.1482 (0.48) | 0.1237 (0.42) | 0.1152 (0.40) |

| GDP | 0.3883 ** (1.27) | 0.3544 * (1.20) | 0.4138 ** (1.44) |

| Pigs | −0.0132 (−0.04) | 0.0437 (0.15) | 0.0886 ** (0.31) |

| Agricultural Commodity Price | 0.2594 *** (0.85) | 0.2525 ** (0.86) | 0.2065 * (0.72) |

| Interest Rate | −0.1417 ** (−0.46) | −0.1139 ** (−0.39) | −0.0820 * (−0.28) |

| 0.9850 | 0.9860 | 0.9844 |

| Type of Land | Elasticity in the Long-Run |

|---|---|

| Good-quality Land | 1.24 *** |

| Medium-quality Land | 0.75 *** |

| Bad-quality Land | 0.70 *** |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tomal, M.; Gumieniak, A. Agricultural Land Price Convergence: Evidence from Polish Provinces. Agriculture 2020, 10, 183. https://doi.org/10.3390/agriculture10050183

Tomal M, Gumieniak A. Agricultural Land Price Convergence: Evidence from Polish Provinces. Agriculture. 2020; 10(5):183. https://doi.org/10.3390/agriculture10050183

Chicago/Turabian StyleTomal, Mateusz, and Agata Gumieniak. 2020. "Agricultural Land Price Convergence: Evidence from Polish Provinces" Agriculture 10, no. 5: 183. https://doi.org/10.3390/agriculture10050183

APA StyleTomal, M., & Gumieniak, A. (2020). Agricultural Land Price Convergence: Evidence from Polish Provinces. Agriculture, 10(5), 183. https://doi.org/10.3390/agriculture10050183