Portuguese Agrifood Sector Resilience: An Analysis Using Structural Breaks Applied to International Trade

Abstract

:1. Introduction

2. Materials and Methods

2.1. Methods Issues

2.2. Structural Methods

2.3. Applied Data

3. Results

3.1. Stationarity Analysis of Trade Time Series

3.2. Analysis of Structural Breaks

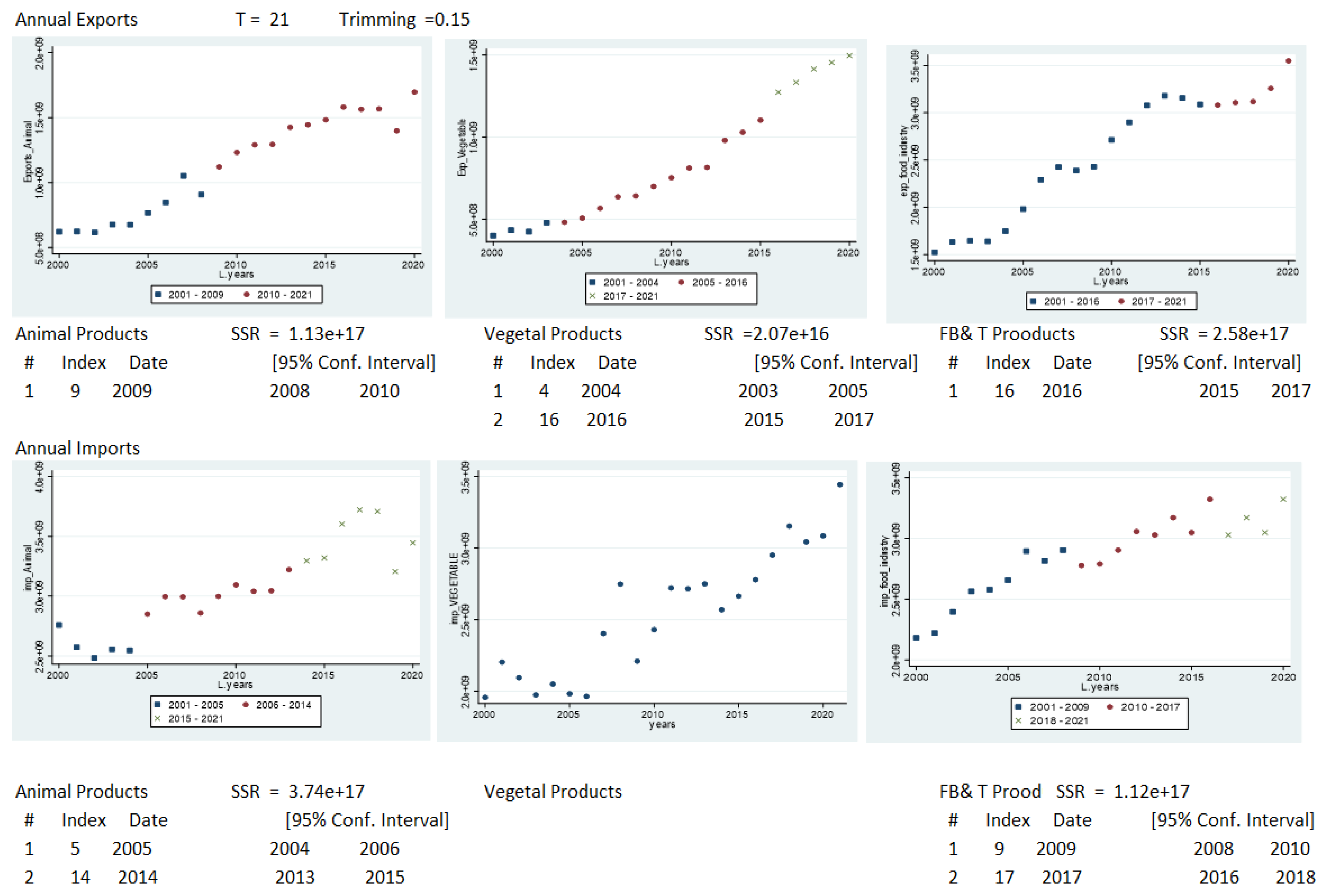

3.2.1. Results for Annual Time-Series Trade

3.2.2. Results for Monthly Time-Series Trade

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Annual Exports | Tests | Variable | Statistics | p-Value | Estimation of Breakpoints | Bai and Perron Critical Values | (95% Conf. Interval) | |||

|---|---|---|---|---|---|---|---|---|---|---|

| xtbreak | Animal | Sequential test for multiple breaks at unknown breakpoints | 1 break | 2 breaks | 1% | 5% | 10% | |||

| hypotheses A | Detected number of breaks and dates: | - | 1 | 1 | ||||||

| supW(tau) | H0: no break(s) vs. H1: 1 break(s) | 10.04 | 2009 | 12.29 | 8.58 | 7.04 | 2008–2010 | |||

| W(tau) | 1 break (2009) | 10.04 | 42.89 | |||||||

| 1 break (2012) | 0.28 | 0.60 | ||||||||

| estat sbsingle | swald | Animal (lag. 2) | 91.62 | 0.00 | 2012 | |||||

| estat sbknown | Wald test chi2(2) | 1 break (2009) | 42.89 | 0.00 | ||||||

| xtbreak | Vegetable | Sequential test for multiple breaks at unknown breakpoints | 1 break | 2 breaks | 1% | 5% | 10% | |||

| hypotheses A | Detected number of breaks and dates: | 1 | 2 | 2 | ||||||

| supW(tau) | H0: no break(s) vs. H1: 1 break(s) | 42.69 | 2016 | 12.29 | 8.58 | 7.04 | 2003–2005 | |||

| supW(tau) | H0: no break(s) vs. H1: 2 break(s) | 46.61 | 2004; 2016 | 9.36 | 7.22 | 6.28 | 2015–2017 | |||

| W(tau) | 1 break (2016) | 42.69 | 0.00 | |||||||

| W(tau) | 1 break (2004) | 20.16 | 0.00 | |||||||

| W(tau) | 1 break (2016; 2004) | 46.61 | 0.00 | |||||||

| W(tau) | 1 break (2015) | 29.09 | 0.00 | |||||||

| estat sbsingle | swald | Vegetable (1) | 71.40 | 0.00 | 2015 | |||||

| estat sbknown | Wald test chi2(2) | 1 break (2016) | 58.93 | 0.00 | ||||||

| 1 break (2004) | 5.28 | 0.02 | ||||||||

| 2 break(s) (2004 2016) | 81.40 | 0.00 | ||||||||

| xtbreak | FB&T | Sequential test for multiple breaks at unknown breakpoints | 1 break | 2 breaks | 1% | 5% | 10% | |||

| hypotheses A | Detected number of breaks and dates: | 1 | 1 | 1 | ||||||

| supW(tau) | H0: no break(s) vs. H1: 1 break(s) | 24.58 | 2016 | 12.29 | 8.58 | 7.04 | 2015–2017 | |||

| W(tau) | 1 break (2016) | 24.58 | 0.00 | |||||||

| W(tau) | 1 break (2010) | 4.53 | 0.05 | |||||||

| estat sbsingle | swald | FB&T (lag 3) | 67.53 | 0.00 | 2010 | |||||

| estat sbknown | Wald test chi2(2) | Break date (2016) | 27.64 | 0.00 | ||||||

| Annual Imports | Tests | Variable | Statistics | p-value | Estimation of breakpoints | Bai and Perron Critical Values | (95% Conf. Interval) | |||

| xtbreak | Animal | Sequential test for multiple breaks at unknown breakpoints | 1 break | 2 breaks | 1% | 5% | 10% | |||

| hypotheses A | Detected number of breaks and dates: | - | 2 | 2 | ||||||

| supW(tau) | H0: no break(s) vs. H1: 2 break(s) | 1.24 | 2013 | 12.29 | 8.58 | 7.04 | 2004–2006 | |||

| H0: no break(s) vs. H1: 2 break(s) | 3.14 | 2005–2014 | 9.36 | 7.22 | 6.28 | 2013–2015 | ||||

| W(tau) | 1 break (2005) | 1.22 | 0.280 | |||||||

| W(tau) | 1 break (2014) | 1.18 | 0.290 | |||||||

| W(tau) | 2 break(s) (2005 2014) | 3.14 | 0.060 | |||||||

| W(tau) | 1 break (2015) | 0.93 | 0.350 | |||||||

| estat sbsingle | swald | Animal (lag. 1) | 36.06 | 0.000 | 2015 | |||||

| estat sbknown | Wald test chi2(2 | 1 break (2005) | 8.81 | 0.003 | ||||||

| 1 break (2014) | 31.96 | 0.000 | ||||||||

| 2 break(s) (2005–2014) | 43.45 | 0.000 | ||||||||

| xtbreak | Vegetable | Sequential test for multiple breaks at unknown breakpoints | 1 break | 2 breaks | 1% | 5% | 10% | |||

| hypotheses A | Detected number of breaks and dates: | - | - | - | ||||||

| W(tau) | 1 break (2010) | 0.21 | 0.650 | |||||||

| swald | Vegetable (lag 3) | 41.86 | 0.000 | 2010 | ||||||

| FB&T | Sequential test for multiple breaks at unknown breakpoints | 1 break | 2 breaks | 1% | 5% | 10% | ||||

| hypotheses A | Detected number of breaks and dates: | - | 2 | 2 | ||||||

| supW(tau) | H0: no break(s) vs. H1: 2 break(s) | 16.36 | 0 | 2009–2017 | 9.36 | 7.22 | 6.28 | 2008–2010 | ||

| W(tau) | 1 break (2009) | 0.80 | 0.38 | 2016–2018 | ||||||

| W(tau) | 1 break (2017) | 11.02 | 0.00 | |||||||

| W(tau) | 2 break(s) (2009 2017) | 16.36 | 0.00 | |||||||

| estat sbsingle | swald | FB&T (lag 2) | 50.95 | 0.00 | 2009 | |||||

| estat sbknown | Wald test chi2(2) | Break date (2017) | 12.80 | 0.00 | ||||||

Appendix B

| Annual Exports | Hypotheses | Test | Statitic | 1% | 5% | 10% | Analysis | ||

|---|---|---|---|---|---|---|---|---|---|

| Animal | B | H0: no break(s) vs. H1: 1 ≤ s ≤ 1 break(s) | max = 1 | UDmax(tau) | 10.04 | 12.37 | 8.88 | 7.46 | Null hypotheses of no breaks against the alternative of up to 1 break. The null hypothesis is rejected at the 5% level. |

| C | H0: 0 vs. H1: 1 break(s) | s = 0 | F(s+1|s) | 10.04 | 12.29 | 8.58 | 7.04 | Null hypotheses of no breaks against 1 break. We can reject the null hypothesis at the 5% level and accept one break at the 5% level. | |

| C | H0: 1 vs. H1: 2 break(s) | s = 1 | F(s+1|s) | 6.16 | 13.89 | 10.13 | 8.51 | Null hypotheses of 1 break against 2 breaks. We cannot reject the null hypothesis. | |

| Vegetable | B | H0: no break(s) vs. H1: 1 ≤ s ≤ 2 break(s) | s max = 2 | UDmax(tau) | 46.61 | 12.37 | 8.88 | 7.46 | Null hypotheses of no breaks against the alternative of up to 2 breaks. The null hypothesis is rejected at the 1% level. |

| C | H0: 0 vs. H1: 1 break(s) | s = 0 | F(s+1|s) | 42.69 | 12.29 | 8.58 | 7.04 | Null hypotheses of 0 breaks against 1 break. We can reject the null hypothesis at the 1% level and accept one break at the 1% level. | |

| C | H0: 1 vs. H1: 2 break(s) | s = 1 | F(s+1|s) | 11.54 | 13.89 | 10.13 | 8.51 | Null hypotheses of 0 breaks against 2 breaks. We can reject the null hypothesis at the 5% level and accept two breaks at the 5% level. | |

| C | H0: 2 vs. H1: 3 break(s) | s = 2 | F(s+1|s) | 2.75 | 14.8 | 11.14 | 9.41 | Null hypotheses of 2 breaks against 3 breaks. We cannot reject the null hypothesis. | |

| FB&T | B | H0: no break(s) vs. H1: 1 ≤ s ≤ 2 break(s) | s max = 2 | UDmax(tau) | 24.58 | 12.37 | 8.88 | 7.46 | Null hypotheses of no breaks against the alternative of up to 2 breaks. The null hypothesis at the 1% level is rejected. |

| C | H0: 0 vs. H1: 1 break(s) | s = 0 | F(s+1|s) | 24.58 | 12.2 | 8.58 | 7.04 | Null hypotheses of 0 breaks against 1 break. We can reject the null hypothesis at the 1% level and accept one break at the 1% level. | |

| C | H0: 1 vs. H1: 2 break(s) | s = 1 | F(s+1|s) | 5.28 | 13.89 | 10.13 | 8.51 | Null hypotheses of 1 break against 2 breaks. We cannot reject the null hypothesis. | |

| Annual Imports | |||||||||

| Animal | B | H0: no break(s) vs. H1: 1 ≤ s ≤ 2 break(s) | s max = 2 | UDmax(tau) | 3.14 | 12.37 | 8.88 | 7.46 | Null hypothesis of no breaks against the alternative of up to 1 break. We cannot reject the null hypothesis. |

| C | H0: 0 vs. H1: 1 break(s) | s = 0 | F(s+1|s) | 1.24 | 12.29 | 8.58 | 7.04 | Null hypothesis of 0 breaks against 1 break. We cannot reject the null hypothesis. | |

| Vegetable | B | H0: no break(s) vs. H1: 1 ≤ s ≤ 1 break(s) | s max = 1 | UDmax(tau) | 3.18 | 12.37 | 8.88 | 7.46 | Null hypotheses of no breaks against the alternative of up to 1 break. We cannot reject the null hypothesis. |

| C | H0: 0 vs. H1: 1 break(s) | s = 0 | F(s+1|s) | 1.27 | 12.29 | 8.58 | 7.04 | Null hypotheses of 0 breaks against 1 break. We cannot reject the null hypothesis. | |

| FB&T | B | H0: no break(s) vs. H1: 1 ≤ s ≤ 2 break(s) | s max = 2 | UDmax(tau) | 16.36 | 12.37 | 8.88 | 7.46 | Null hypothesis of no breaks against the alternative of up to 2 breaks. The null hypothesis at the 1% level is rejected. |

| C | H0: 0 vs. H1: 1 break(s) | s = 0 | F(s+1|s) | 11.02 | 12.29 | 8.58 | 7.04 | Null hypotheses of 0 breaks against 1 break. We can reject the null hypothesis at the 5% level and accept one break at the 5% level. | |

| C | H0: 1 vs. H1: 2 break(s) | s = 1 | F(s+1|s) | 13.84 | 13.89 | 10.13 | 8.51 | Null hypothesis of 1 break against 2 breaks. We can reject the null hypothesis at the 5% level and accept 2 breaks at the 5% level. | |

| C | H0: 2 vs. H1: 3 break(s) | s = 2 | F(s+1|s) | 4.39 | 14.80 | 11.14 | 9.41 | Null hypothesis of 2 breaks against 3 breaks. We cannot reject the null hypothesis. | |

Appendix C

| Monthly Exports | Tests | Variable | Statistics | p-Value | Estimation of Breakpoints | Bai and Perron Critical Values | (95% Conf. Interval) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| xtbreak | Animal | Sequential test for multiple breaks at unknown breakpoints | 1 break | 2 breaks | 1% | 5% | 10% | ||||||

| Hypothesis A | Detected number of breaks and dates: | 1 | 1 | ||||||||||

| supW(tau) | H0: no break(s) vs. H1: 1 break(s) | 10.87 | 2010m2 | 12.29 | 8.58 | 7.04 | 2010m1 2010m3 | ||||||

| W(tau) | 1 break (2010m2) | 10.87 | 0.00 | ||||||||||

| 1 break (2011m1) | 4.68 | 0.03 | |||||||||||

| estat sbsingle | Swald | Animal (lag. 4) | 633.94 | 0.00 | 2011m1 | ||||||||

| estat sbknown | Wald test chi2 | 1break (2010m2) | 586.19 | 0.00 | |||||||||

| xtbreak | Vegetable | Sequential test for multiple breaks at unknown breakpoints | 1 break | 2 breaks | 1% | 5% | 10% | ||||||

| Hypothesis A | Detected number of breaks and dates: | 2 | 2 | 2 | |||||||||

| supW(tau) | H0: no break(s) vs. H1: 1 break(s) | 77.63 | 2004m6 | 12.29 | 8.58 | 7.04 | 2005m2 2005m4 | ||||||

| supW(tau) | H0: no break(s) vs. H1: 2 break(s) | 89.29 | 2005m3; 2016m8 | 9.36 | 7.22 | 6.28 | 2016m7 2016m9 | ||||||

| W(tau) | 1 break (2004m6) | 77.63 | 0.00 | ||||||||||

| W(tau) | 1 break (2005m3) | 83.35 | 0.00 | ||||||||||

| W(tau) | 1 break (2016m8) | 149.93 | 0.00 | ||||||||||

| W(tau) | 2 break(s) (2005m3; 2016m8) | 89.29 | 0.00 | ||||||||||

| W(tau) | 1 break (2015m1) | 76.68 | 0.00 | ||||||||||

| estat sbsingle | Swald | Vegetable (4) | 777.04 | 0.00 | 2015m1 | ||||||||

| estat sbknown | Wald test chi2 | 1 break (2004m6) | 89.90 | 0.00 | |||||||||

| 1 break (2005m3) | 113.96 | 0.00 | |||||||||||

| 1 break (2016m8) | 677.68 | 0.00 | |||||||||||

| 2 break(s) (2005m3; 2016m8) | 1061.75 | 0.00 | |||||||||||

| xtbreak | FB&T | Sequential test for multiple breaks at unknown breakpoints | 1 break | 2 breaks | 1% | 5% | 10% | ||||||

| Hypothesis A | Detected number of breaks and dates | 1 | 1 | 1 | |||||||||

| supW(tau) | H0: no break(s) vs. H1: 1 break(s) | 25.58 | 2015m11 | 12.29 | 8.58 | 7.04 | 2015m10; 2015m12 | ||||||

| W(tau) | 1 break (2015m11) | 25.58 | 0.00 | ||||||||||

| W(tau) | 1 break (2011m9) | 0.07 | 0.79 | ||||||||||

| estat sbsingle | Swald | FB&T (4) | 504.11 | 0.00 | 2011m9 | ||||||||

| estat sbknown | Wald test chi2 | Break date (2015m11) | 215.21 | 0.00 | |||||||||

| Monthly Imports | Tests | Variable | Statistics | p-value | Estimation of breakpoints | Bai and Perron Critical Values | (95% Conf. Interval) | ||||||

| xtbreak | Animal | Sequential test for multiple breaks at unknown breakpoints | 1 break | 2 breaks | 3 breaks | 4 breaks | 1% | 5% | 10% | ||||

| Hypothesis A | Detected number of breaks and dates: | 4 | 1 | 1 | |||||||||

| supW(tau) | H0: no break(s) vs. H1: 1 break(s) | 12.09 | 2008m10 | 12.29 | 8.58 | 7.04 | 2008m9 2008m11 | ||||||

| H0: no break(s) vs. H1: 2 break(s) | 12.88 | 2003m5; 2011m8 | 9.36 | 7.22 | 6.28 | ||||||||

| H0: no break(s) vs. H1: 3 break(s) | 11.85 | 2003m5; 2008m5; 2011m9 | 7.6 | 5.96 | 5.21 | ||||||||

| H0: no break(s) vs. H1: 4 break(s) | 10.06 | 2003m5; 2006m1; 2011m8; 2017m2 | 6.19 | 4.99 | 4.41 | ||||||||

| W(tau) | 1 break (2008m10) | 12.09 | 0.00 | ||||||||||

| 1 break (2003m5) | 7.73 | 0.01 | |||||||||||

| 1 break (2011m8) | 7.21 | 0.01 | |||||||||||

| 1 break (2008m5) | 9.73 | 0.00 | |||||||||||

| 1 break (2006m1) | 0.02 | 0.88 | |||||||||||

| 1 break (2017m2) | 27.57 | 0.00 | |||||||||||

| 2 break(s) (2003m5; 2011m8) | 12.88 | 0.00 | |||||||||||

| 3 break(s) (2003m5; 2008m5; 2011m9) | 11.85 | 0.00 | |||||||||||

| 4 break(s) (2003m5; 2006m1; 2011m8; 2017m2) | 11.73 | 0.00 | |||||||||||

| 1 break (2015m6) | 13.66 | 0.00 | |||||||||||

| estat sbsingle | swald | Animal (lag. 3) | 293.88 | 0.00 | 2015m6 | ||||||||

| estat sbknown | Wald test chi2 | 1 break (2008m10) | 148.78 | ||||||||||

| 2 break(s) (2003m5; 2011m8) | 184.14 | 0.00 | |||||||||||

| 3 break(s) (2003m5; 2008m5; 2011m9) | 206.40 | 0.00 | |||||||||||

| 4 break(s) (2003m5; 2006m1; 2011m8; 2017m2) | 462.27 | 0.00 | |||||||||||

| Vegetable | Sequential test for multiple breaks at unknown breakpoints | 1 break | 2 breaks | 1% | 5% | 10% | |||||||

| Hypothesis A | Detected number of breaks and dates | 1 | 1 | 1 | |||||||||

| supW(tau) | H0: no break(s) vs. H1: 1 break(s) | 17.47 | 2008m12 | 12.29 | 8.58 | 7.04 | 2008m11 | ||||||

| 2009m1 | |||||||||||||

| W(tau) | 1 break (2008m12) | 17.47 | 0 | ||||||||||

| W(tau) | 1 break (2017m3) | 26.63 | 0 | ||||||||||

| estat sbsingle | swald | Vegetable (3) | 271.70 | 0.00 | 2017m3 | ||||||||

| estat sbknown | Wald test chi2 | 1 break (2008m12) | 155.52 | 0.00 | |||||||||

| FB&T | Sequential test for multiple breaks at unknown breakpoints | 1 break | 2 breaks | 3 breaks | 4 breaks | 5 breaks | 1% | 5% | 10% | ||||

| Hypothesis A | Detected number of breaks and dates: | 5 | 5 | 5 | |||||||||

| supW(tau) | H0: no break(s) vs. H1: 1 break(s) | 18.69 | 2004m12 | 12.29 | 8.58 | 7.04 | 2003m10 2003m12 | ||||||

| H0: no break(s) vs. H1: 2 break(s) | 22.71 | 2003m11; 2011m11 | 9.36 | 7.22 | 6.28 | 2007m10 2007m12 | |||||||

| H0: no break(s) vs. H1: 3 break(s) | 15.15 | 2003m11; 2009m11; 2013m10 | 7.6 | 5.96 | 5.21 | 2011m10 2011m12 | |||||||

| H0: no break(s) vs. H1: 4 break(s) | 13.48 | 2003m11; 2009m11; 2013m10; 2019m6 | 6.19 | 4.99 | 4.41 | 2015m9 2015m11 | |||||||

| H0: no break(s) vs. H1: 5 break(s) | 11.09 | 2003m11; 2007m11; 2011m11; 2015m10; 2019m6 | 4.91 | 3.91 | 3.47 | 2019m5 2019m7 | |||||||

| W(tau) | 1 break (2004m12) | 18.69 | 0.00 | ||||||||||

| 1 break (2003m11) | 19.26 | 30.43 | |||||||||||

| 1 break (2009m11) | 1.84 | 0.18 | |||||||||||

| 1 break (2013m10) | 1.10 | 0.29 | |||||||||||

| 1 break (2019m6) | 30.43 | 30.43 | |||||||||||

| 1 break (2015m10) | 5.41 | 0.02 | |||||||||||

| 1 break (2007m11) | 51.91 | 0.00 | |||||||||||

| 2 break(s) (2003m11; 2011m11) | 22.71 | 0.00 | |||||||||||

| 3 break(s) (2003m11; 2009m11; 2013m10) | 15.15 | 0.00 | |||||||||||

| 4 break(s) (2003m11; 2009m11; 2013m10; 2019m6) | 13.48 | 0.00 | |||||||||||

| 5 break(s) (2003m11; 2007m11; 2011m11; 2015m10; 2019m6) | 11.09 | 0.00 | |||||||||||

| 1 break (2016m8) | 12.37 | 0.00 | |||||||||||

| estat sbsingle | Swald | FB&T (3) | 250.00 | 0.00 | 2016m8 | ||||||||

| estat sbknown | Wald test chi2 | 1 break (2004m12) | 76.35 | 0.00 | |||||||||

| 2 break(s) (2003m11; 2011m11) | 227.89 | 0.00 | |||||||||||

| 3 break(s) (2003m11; 2009m11; 2013m10) | 314.82 | 0.00 | |||||||||||

| 4 break(s) (2003m11; 2009m11; 2013m10; 2019m6) | 479.89 | 0.00 | |||||||||||

| 5 break(s) (2003m11; 2007m11; 2011m11; 2015m10; 2019m6) | 556.79 | 0.00 | |||||||||||

Appendix D

| Monthly Exports | Hypotheses | Test Statistics | 1% | 5% | 10% | Analysis | |||

|---|---|---|---|---|---|---|---|---|---|

| Animal | B | H0: no break(s) vs. H1: 1 ≤ s ≤ 1 break(s) | s max = 1 | UDmax(tau) | 10.87 | 12.37 | 8.88 | 7.46 | Null hypothesis of no breaks against the alternative of up to 1 break. The null hypothesis is rejected at the 5% level. |

| C | H0: 0 vs. H1: 1 break(s) | s = 0 | F(s+1|s) | 10.87 | 12.29 | 8.58 | 7.04 | Null hypothesis of no breaks against 1 break. We can reject the null hypothesis at the 5% level and accept one break at the 5% level. | |

| C | H0: 1 vs. H1: 2 break(s) | s = 1 | F(s+1|s) | 6.19 | 13.89 | 10.13 | 8.51 | Null hypothesis of 1 break against 2 breaks. We cannot reject the null hypothesis. | |

| Vegetable | B | H0: no break(s) vs. H1: 1 ≤ s ≤ 2 break(s) | s max = 2 | UDmax(tau) | 89.29 | 12.37 | 8.88 | 7.46 | Null hypotheses of no breaks against the alternative of up to 2 breaks. The null hypothesis is rejected at the 1% level. |

| C | H0: 0 vs. H1: 1 break(s) | s = 0 | F(s+1|s) | 77.63 | 12.29 | 8.58 | 7.04 | Null hypotheses of 0 breaks against 1 break. We can reject the null hypothesis at the 1% level and accept one break at the 1% level. | |

| C | H0: 1 vs. H1: 2 break(s) | s = 1 | F(s+1|s) | 57.65 | 13.89 | 10.13 | 8.51 | Null hypothesis of 0 breaks against 2 breaks. We can reject the null hypothesis at the 5% level and accept two breaks at the 1% level. | |

| C | H0: 2 vs. H1: 3 break(s) | s = 2 | F(s+1|s) | 7.14 | 14.8 | 11.14 | 9.41 | Null hypothesis of 2 breaks against 3 breaks. We cannot reject the null hypothesis. | |

| FB&T | B | H0: no break(s) vs. H1: 1 ≤ s ≤ 2 break(s) | s max = 2 | UDmax(tau) | 25.58 | 12.37 | 8.88 | 7.46 | Null hypothesis of no breaks against the alternative of up to 2 breaks. The null hypothesis at the 1% level is rejected. |

| C | H0: 0 vs. H1: 1 break(s) | s = 0 | F(s+1|s) | 25.58 | 12.29 | 8.58 | 7.04 | Null hypothesis of 0 breaks against 1 break. We can reject the null hypothesis at the 1% level and accept one break at the 1% level. | |

| C | H0: 1 vs. H1: 2 break(s) | s = 1 | F(s+1|s) | 6.58 | 13.89 | 10.13 | 8.51 | Null hypothesis of 1 break against 2 breaks. We cannot reject the null hypothesis. | |

| Monthly Imports | |||||||||

| Animal | B | H0: no break(s) vs. H1: 1 ≤ s ≤ 4 break(s) | s max =4 | UDmax(tau) | 12.88 | 12.37 | 8.88 | 7.46 | Null hypothesis of no breaks against the alternative of up to 4 breaks. The null hypothesis at the 1% level is rejected. |

| C | H0: 0 vs. H1: 1 break(s) | s = 0 | F(s+1|s) | 12.09 | 12.29 | 8.58 | 7.04 | Null hypotheses of 0 breaks against 1 break. We can reject the null hypothesis at the 5% level and accept one break at the 5% level. | |

| C | H0: 1 vs. H1: 2 break(s) | s = 1 | F(s+1|s) | 2.19 | 13.89 | 10.13 | 8.51 | Null hypothesis of 1 break against 2 breaks. We cannot reject the null hypothesis. | |

| Vegetable | B | H0: no break(s) vs. H1: 1 ≤ s ≤ 2 break(s) | s max = 2 | UDmax(tau) | 23.63 | 12.37 | 8.88 | 7.46 | Null hypothesis of no breaks against the alternative of up to 2 breaks. The null hypothesis at the 1% level is rejected. |

| C | H0: 0 vs. H1: 1 break(s) | s = 0 | F(s+1|s) | 17.47 | 12.29 | 8.58 | 7.04 | Null hypothesis of 0 breaks against 1 break. We can reject the null hypothesis at the 1% level and accept one break at the 1% level. | |

| C | H0: 1 vs. H1: 2 break(s) | s = 1 | F(s+1|s) | 4.88 | 13.89 | 10.13 | 8.51 | Null hypothesis of 1 break against 2 breaks. We cannot reject the null hypothesis. | |

| FB&T | B | H0: no break(s) vs. H1: 1 ≤ s ≤ 5 break(s) | s max =5 | UDmax(tau) | 22.71 | 12.29 | 8.58 | 7.04 | Null hypotheses of no breaks against the alternative of up to 5 breaks. The null hypothesis at the 1% level is rejected. |

| C | H0: 0 vs. H1: 1 break(s) | s = 0 | F(s+1|s) | 18.69 | 12.29 | 8.58 | 7.04 | Null hypothesis of 0 breaks against breaks. We can reject the null hypothesis at the 1% level and accept one break at the 1% level. | |

| C | H0: 1 vs. H1: 2 break(s) | s = 1 | F(s+1|s) | 22.9 | 13.89 | 10.13 | 8.51 | Null hypothesis of 1 break against 2 breaks. We can reject the null hypothesis at the 1% level and accept 2 breaks at the 1% level. | |

| C | H0: 2 vs. H1: 3 break(s) | s = 2 | F(s+1|s) | 16.27 | 14.80 | 11.14 | 9.41 | Null hypothesis of 2 breaks against 3 breaks. We can reject the null hypothesis at the 1% level and accept 3 breaks at the 1% level. | |

| C | H0: 3 vs. H1: 4 break(s) | s = 3 | F(s+1|s) | 20.13 | 15.28 | 11.83 | 10.04 | Null hypothesis of 3 breaks against 4 breaks. We can reject the null hypothesis at the 1% level and accept 4 breaks at the 1% level. | |

| C | H0: 4 vs. H1: 5 break(s) | s = 4 | F(s+1|s) | 35.78 | 15.76 | 12.25 | 10.58 | Null hypothesis of 4 breaks against 5 breaks. We can reject the null hypothesis at the 1% level and accept 5 breaks at the 1% level. | |

| C | H0: 5 vs. H1: 6 break(s) | s = 5 | F(s+1|s) | 38.18 | 16.27 | 12.66 | 11.03 | Null hypothesis of 5 breaks against 6 breaks. We can reject the null hypothesis at the 1% level and accept 6 breaks at the 1% level. | |

References

- Christopher, M. Logistics and Supply Chain Management. Strategies for Reduction Costs and Improving Services, 1st ed.; Financial Times; Pitman Publishing: London, UK, 1992. [Google Scholar]

- Bowersow, J.; Closs, J.; Stank, P. How to master cross-enterprise collaboration. Supply Chain. Manag. Rev. 2003, 7, 18–26. [Google Scholar]

- Holmberg, S. A system perspective in supply chain measurement. Int. J. Phys. Distrib. Mater. Manag. 2000, 30, 847–866. [Google Scholar] [CrossRef]

- Houlihan, J.B. International supply chain management. Int. J. Phys. Distrib. Mater. Manag. 1987, 19, 51–66. [Google Scholar]

- Hassini, E.; Surti, C.; Searcy, C. A literature review and a case study of sustainable supply chains with a focus on metrics. Int. J. Prod. Econ. 2012, 140, 69–82. [Google Scholar] [CrossRef]

- OECD. International Trade during the COVID-10 Pandemic: Big Shifts and Uncertainty; OECD: Paris, France, 2022. [Google Scholar]

- Oliveira, F. Análise de Quebra Estrutural no Número de Casos de COVID-19 no Rio Grande do Norte. Bachelor’s Thesis, Universidade Federal do Rio Grande do Norte, Natal, Brazil, 2022. Available online: https://repositorio.ufrn.br/bitstream/123456789/45889/1/An%C3%A1lise%20De%20Quebra%20Estrutural%20COVID19%20no%20RN%20_%20Canind%C3%A9%20Oliveira%20_%202022.pdf (accessed on 20 November 2022).

- Ditzen, J.; Karavias, Y.; Westerlund, J. Xtbreak: Testing for Structural Breaks in Stata. 2020. Available online: https://www.stata.com/meeting/switzerland20/slides/Switzerland20_Ditzen.pdf (accessed on 1 December 2020).

- Ditzen, J.; Karavias, Y.; Westerlund, J. Testing and Estimating Structural Breaks in Time Series and Panel Data in Stata. arXiv 2021, arXiv:2110.14550. [Google Scholar]

- FAO. Agricultural Trade & Policy Responses during the First Wave of the COVID-19 Pandemic in 2020; Finance Research Letters; FAO: Rome, Italy, 2021; Volume 36, ISSN 1544-6123. [Google Scholar] [CrossRef]

- Erol, E.; Saghaian, S.H. The COVID-19 Pandemic and Dynamics of Price Adjustment in the U.S. Beef Sector. Sustainability 2022, 14, 4391. [Google Scholar] [CrossRef]

- Bergamelli, M.; Urga, G. Detecting Multiple Structural Breaks: Dummy Saturation vs. Sequential Bootstrapping. With an Application to the Fisher E’. In Proceedings of the 12th OxMetrics User Conference, Aarhus, Denmark, 5–6 September 2013; pp. 1–43. [Google Scholar]

- Allaro, H.B. A Time Series Analysis of Structural Break Time in Ethiopian GDP, Export and Import. J. Glob. Econ. 2018, 6, 3. [Google Scholar] [CrossRef]

- Kalsie, A.; Arora, A. Structural break, US financial crisis and macroeconomic time series: Evidence from BRICS economies. Transnatl. Corp. Rev. 2019, 11, 250–264. [Google Scholar] [CrossRef]

- GPP. Complexo Agroflorestal (CAF) e Principais Setores. Séries Longas 2000–2020. 2022. Available online: https://agricultura.gov.pt/estatisticas-cominter-balanca-comercial (accessed on 23 June 2023).

- Pinto, M.A. Crise de Dívida Soberana na Área do Euro. Master Thesis, Faculdade de Economia e Gestão, Universidade do Porto, Porto, Portugal, 2014. Available online: https://sigarra.up.pt/fep/pt/pub_geral.show_file?pi_doc_id=26887 (accessed on 6 January 2023).

- Teles, P. Crises de Dívida Soberana. Banco de Portugal. 2014. Available online: https://www.bportugal.pt/sites/default/files/anexos/papers/ab201414_p.pdfm (accessed on 6 January 2023).

- Coelho, L. Efeitos da Crise da Dívida Soberana Sobre o Emprego de Diferentes Grupos da População. Master’s Thesis, Universidade de Coimbra, Coimbra, Portugal, 2014. [Google Scholar]

- Manteu, C.; Monteiro, N.; Sequeira, A. The Short-Term Impact of the COVID-19 Pandemic on Portuguese Companies. Occasional Papers, Lisboa, Banco de Portugal. 2020. Available online: https://www.bportugal.pt/en/paper/short-term-impact-covid-19-pandemic-portuguese-companies (accessed on 1 January 2022).

- Fadiga, P. Impactos da COVID-19 nas Cadeias Agrícolas. Master’s Thesis, ESAC, Instituto Politécnico de Coimbra, Coimbra, Portugal, 2022. [Google Scholar]

- OECD. OECD Economic Outlook; Volume 2023 Issue 1: Preliminary Version; OECD: Paris, France, 2023. [Google Scholar]

- Karavias, Y.; Narayan, P.K.; Westerlund, J. Structural Breaks in Interactive Effects Panels and the Stock Market Reaction to COVID-19. J. Bus. Econ. Stat. 2022, 41, 653–666. [Google Scholar] [CrossRef]

- Zhang, D.; Hu, M.; Ji, Q. Financial markets under the global pandemic of COVID-19. Financ. Res. Lett. 2020, 36, 101528. [Google Scholar] [CrossRef]

- Barbero, J.; de Lucio, J.J.; Rodríguez-Crespo, E. Effects of COVID-19 on trade flows: Measuring their impact through government policy responses. PLoS ONE 2021, 16, e0258356. [Google Scholar] [CrossRef] [PubMed]

- Syed, S.A.S.; Zwick, H.S. Oil Price Shocks and the US Stock Market: Slope Heterogeneity Analysis. Theor. Econ. Lett. 2016, 6, 480–487. [Google Scholar] [CrossRef]

- Glynn, J.; Perera, N.; Verma, R. Unit Root Tests and Structural Breaks: A Survey with Applications. Rev. Métodos Cuantitativos Para Econ. Empresa 2007, 3, 63–79. [Google Scholar]

- Baldwin, J. Price Volatility and Structural Breaks in U.S. Dairy Markets. All Graduate Plan B and Other Reports. 2016. 819. Available online: https://digitalcommons.usu.edu/gradreports/819 (accessed on 20 March 2021).

- Enders, W. Applied Econometric Time Series; John Wiley & Son, Inc.: Hoboken, NJ, USA, 1995. [Google Scholar]

- Gujarati, D. Basic Econometrics, 4th ed.; McGraw-Hill/lrwin: New York, NY, USA, 2003; ISBN 978-0-07-233542-2. Available online: https://www.uop.edu.pk/ocontents/gujarati_book.pdf (accessed on 12 March 2021).

- Lütkepohl, H. New Introduction to Multiple Time Series Analysis; Springer: Berlin/Heidelberg, Germany, 2005. [Google Scholar] [CrossRef]

- Angulo, A.; Gil, J. Integration Vertical y Transmission de Precio em el Sector Avicola Espagnol. Investig. Agrárias Econ. 1995, 10, 355–381. [Google Scholar]

- Yi, R. Chow Test Analysis on Structural Change in New Zealand Housing Price During Global Subprime Financial Crisis. In Proceedings of the 18th Annual Pacific-Rim Real Estate Society Conference, Adelaide, Australia, 15–18 January 2012. [Google Scholar]

- Nelson, C.R.; Plosser, C.I. Trends and random walks In Macroeconomic Time Series. J. Monterey Econ. 1982, 10, 139–162. [Google Scholar] [CrossRef]

- Perron, P. The Great Crash, the Oil Price Shock, and the Unit Root Hypothesis. Econometrica 1989, 57, 1361. [Google Scholar] [CrossRef]

- Hansen, B. The New Econometrics of Structural Change: Dating Breaks in U.S. Labour Productivity. J. Econ. Perspect. 2001, 15, 117–128. [Google Scholar] [CrossRef]

- Lumsdaine, L.; Papell, H. Multiple Trend Breaks and the Unit-Root Hypothesis. Rev. Econ. Stat. 1997, 79, 212–218. [Google Scholar] [CrossRef]

- Valadkhani, A.; Pahlavani, M. Structural Changes in Australia’s Monetary Aggregates and Interest Rates. 2005. Available online: https://ro.uow.edu.au/commpapers/2251 (accessed on 20 June 2022).

- Doan, T. LPUNIT: RATS Procedure to Implement Lumsdaine-Papell Unit Root Test with Structural Breaks. Statistical Software Components, n.d. Available online: https://ideas.repec.org/c/boc/bocode/rts00110.html (accessed on 10 December 2021).

- Shikida, C.; Paiva, L.; Junior, A. Análise de quebras estruturais na série do preço do boi gordo no Estado de São Paulo. Econ. Apl. 2016, 20, 265–286. [Google Scholar] [CrossRef]

- Stata. Stata.Comestat ic—Display Information Criteria. 2022. Available online: https://www.stata.com/manuals/restatic.pdf (accessed on 20 January 2022).

- Enders, W. Applied Econometric Times Series, 3rd ed.; Willey: Hoboken, NJ, USA, 2010; p. 517. [Google Scholar]

- Chow, G.C. Tests of Equality Between Sets of Coefficients in Two Linear Regressions. Econometrica 1960, 28, 591–605. [Google Scholar] [CrossRef]

- de Oliveira, A.M.B.; Mandal, A.; Power, G.J. Impact of COVID-19 on Stock Indices Volatility: Long-Memory Persistence, Structural Breaks, or Both? Ann. Data Sci. 2022. [Google Scholar] [CrossRef]

- Brown, R.L.; Durbin, J.; Evans, J.M. Techniques for Testing the Constancy of Regression Relationships Over Time. J. R. Stat. Soc. Ser. B 1975, 37, 149–192. [Google Scholar] [CrossRef]

- Ploberger, W.; Kramer, W. The Cusum Test with Ols Residuals. Econometrica 1992, 60, 271–285. [Google Scholar] [CrossRef]

- Turner, P. Power properties of the CUSUM and CUSUMSQ tests for parameter instability. Appl. Econ. Lett. 2010, 17, 1049–1053. [Google Scholar] [CrossRef]

- Krämer, W.; Ploberger, W.; Schlüter, I. Recursive vs. OLS Residuals in the CUSUM Test. In Economic Structural Change; Hackl, P., Westlund, A.H., Eds.; Springer: Berlin/Heidelberg, Germany, 1991. [Google Scholar] [CrossRef]

- Zeileis, A. Alternative boundaries for CUSUM tests. Stat. Pap. 2004, 45, 123–131. [Google Scholar] [CrossRef]

- Das, P. Econometrics in Theory and Practice: Analysis of Cross Section, Time Series and Panel Data with Stata 15; Springer Nature: Berlin/Heidelberg, Germany, 2019. [Google Scholar]

- Vasco, G. Testes de Alteração de Estrutura em Modelos Multivariados: Uma Visita Guiada pela Literatura. Notas Económicas nº 16, Faculdade de Economia da Universidade de Coimbra. 2002. Available online: http://hdl.handle.net/10316.2/24973 (accessed on 26 May 2022).

- Johnston, J.; DiNardo, J. Econometric Methods, 4th ed.; The McGraw-Hill Companies, Inc.: New York, NY, USA, 1997. [Google Scholar]

- Andrews, D.W.K. Tests for Parameter Instability and Structural Change with Unknown Change Point. Econometrica 1993, 61, 821–856. [Google Scholar] [CrossRef]

- Zivot, E.; Andrews, D.W.K. Further Evidence on the Great Crash, the Oil-Price Shock, and the Unit-Root Hypothesis. J. Bus. Econ. Stat. 1992, 10, 251–270. [Google Scholar] [CrossRef]

- Banerjee, A.; Lumsdaine, R.L.; Stock, J.H. Recursive and Sequential Tests of the Unit-Root and Trend-Break Hypotheses: Theory and International Evidence. J. Bus. Econ. Stat. 1992, 10, 271–287. [Google Scholar] [CrossRef]

- Bai, J.; Perron, P. Estimating and Testing Linear Models with Multiple Structural Changes. Econometrica 1998, 66, 47–78. [Google Scholar] [CrossRef]

- Urban, K.; Jensen, H.G.; Brockmeier, M. How decoupled is the Single Farm Payment and does it matter for international trade? Food Policy 2016, 59, 126–138. [Google Scholar] [CrossRef]

- Martinho, V.J.P.D. Testing for Structural Changes in the European Union’s Agricultural Sector. Agriculture 2019, 9, 92. [Google Scholar] [CrossRef]

| Tests | AIC | HQIC | SBIC | AIC | HQIC | SBIC | |

|---|---|---|---|---|---|---|---|

| Type of series | Annual | Monthly | |||||

| Animal | 2 | 2 | 2 | 4 | 4 | 4 | |

| Exports | Vegetables | 1 | 1 | 1 | 4 | 4 | 4 |

| Food, Beverage, and Tobacco (FB&T) | 3 | 3 | 3 | 4 | 4 | 4 | |

| Animal | 1 | 1 | 1 | 3 | 3 | 2 | |

| Imports | Vegetables | 3 | 3 | 3 | 3 | 3 | 3 |

| Food, Beverage, and Tobacco (FB&T) | 2 | 2 | 2 | 3 | 3 | 2 | |

| Tests | Recursive CUSUM | OlS CUSUM | Recursive CUSUM | OlS CUSUM | |

|---|---|---|---|---|---|

| Type of series | Annual | Monthly | |||

| Animal | 1.9782 | 1.9925 | 6.5568 | 6.8659 | |

| Exports | Vegetables | 1.8382 | 1.9031 | 5.9350 | 6.8224 |

| FB&T | 2.2393 | 1.8667 | 7.2923 | 6.6261 | |

| Animal | 1.6640 | 1.7734 | 4.5841 | 5.6884 | |

| Imports | Vegetables | 1.4983 | 1.7465 | 4.3526 | 5.3816 |

| FB&T | 2.5150 | 1.7872 | 4.3855 | 5.6469 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Oliveira, M.d.F.; Reis, P. Portuguese Agrifood Sector Resilience: An Analysis Using Structural Breaks Applied to International Trade. Agriculture 2023, 13, 1699. https://doi.org/10.3390/agriculture13091699

Oliveira MdF, Reis P. Portuguese Agrifood Sector Resilience: An Analysis Using Structural Breaks Applied to International Trade. Agriculture. 2023; 13(9):1699. https://doi.org/10.3390/agriculture13091699

Chicago/Turabian StyleOliveira, Maria de Fátima, and Pedro Reis. 2023. "Portuguese Agrifood Sector Resilience: An Analysis Using Structural Breaks Applied to International Trade" Agriculture 13, no. 9: 1699. https://doi.org/10.3390/agriculture13091699

APA StyleOliveira, M. d. F., & Reis, P. (2023). Portuguese Agrifood Sector Resilience: An Analysis Using Structural Breaks Applied to International Trade. Agriculture, 13(9), 1699. https://doi.org/10.3390/agriculture13091699