The Hidden Side of Electro-Mobility: Modelling Agents’ Financial Statements and Their Interactions with a European Focus

Abstract

:1. Introduction

1.1. Background

1.2. Current State of the Research Field

1.3. Objective, Focus and Structure

2. Materials and Methods

2.1. Methodology

- The financial statements of OEMs (i.e., vehicle manufacturers) were collected from their annual reports and data from the U.S. Securities and Exchange Commission filings. As for any other firm, the three main financial statements of OEMs are: a balance sheet, an income statement and a cash flow statement. Each of them facilitates the analysis of, respectively, solvency, profitability and liquidity. There are two broad economic and financial decisions firms need to make: investment (maximise profitability) and financing (minimise capital costs). Whereas the former is visible in the assets side of a balance sheet, the latter can be reflected in the equity and liabilities section [20]. Instead of profit maximising, “some companies may respond to daunting balance-sheet damage by minimizing debt” [21] (p. xii). This is a sufficient reason for us to model debt explicitly.

- Two balance sheet items (PPE and inventories) require an explanation, as their values can be affected by alternative assumptions. For each of them, we first read what the accounting rules are; we then check what has been assumed in previous SD work and identify what most OEMs adopt in practice.

- The information collected from the previous steps was implemented in the simulation software environment ‘Vensim’. A reference that was used for the preliminary version is [25].

- The variables for the initialisation of the model were created and initial values (see Table 2; money values are expressed in nominal terms) were assigned to those, so that the behaviour resulting from the structure represented in the model (step 4) could be simulated for the period 2005–2030. This was based on numerical integration using Euler, with a time step of 0.25 year (see, e.g., [26]).

- The structure was refined until there were, a priori, no financial leakages in the modelled system.

- The monetary structure was linked with the physical structure (e.g., revenues from selling vehicles) from which a series of key performance indicators (KPIs) could be computed.

2.2. Model

2.2.1. Overview

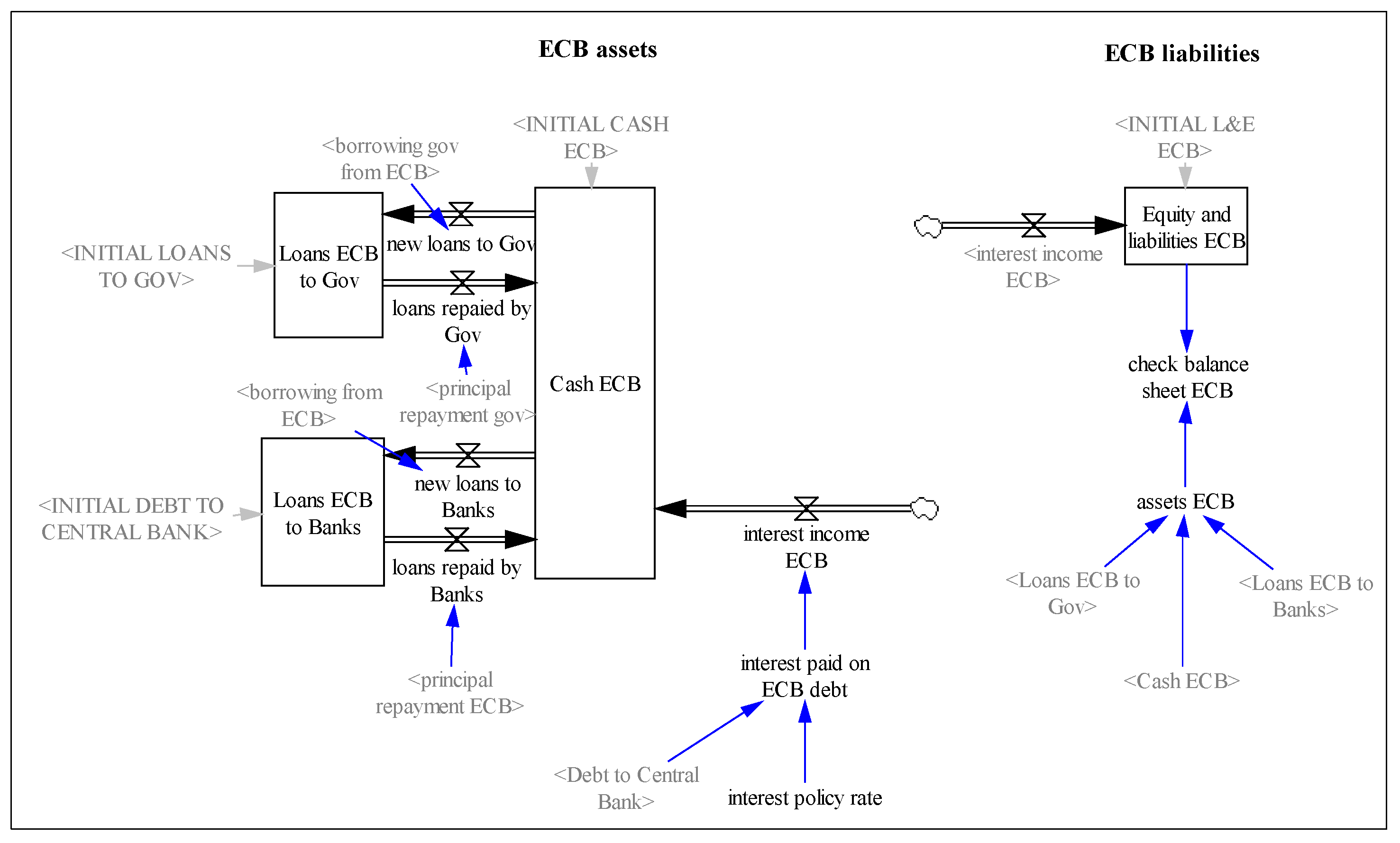

2.2.2. Authorities

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Sub-Agent | Assets | Liabilities & Equity |

|---|---|---|

| ECB | 6 × 1012 | 6 × 1012 |

| EIB | 2.8 × 1011 | 2.8 × 1011 |

| Government | 1011 | 1011 |

- Public infrastructure expenditures, calculated as follows: the historical and projected electric vehicle supply equipment (EVSE) values for the world, disaggregated into slow- and fast-charging points, provided by [31], are incorporated into the model. The project values reflect the STEPS scenario and are interpolated linearly as needed. The resulting estimates are used to compute annual deployment under the assumption that EVSE is long-lived. Next, the cost of the EVSE is as follows: EUR 9000/point for slow and EUR 100,000/point for fast. We work under the premise that the government provides the required funding for the deployment of such publicly accessible infrastructure.

- Public R&D expenditures: this variable is included and linked to OEMs to facilitate the analysis of government grants to the automotive industry. However, in the current version of the model, it takes a value of zero.

- Public transport procurement: all buses are purchased by this agent.

- Purchase subsidies: estimates of government purchase subsidies for the period 2016–2021 were collected from [32], with a linear decline to zero in 2025 assumed.

2.2.3. Banks and Insurance Firms

2.2.4. Households

2.2.5. Suppliers

2.2.6. Vehicle Manufacturers

3. Results

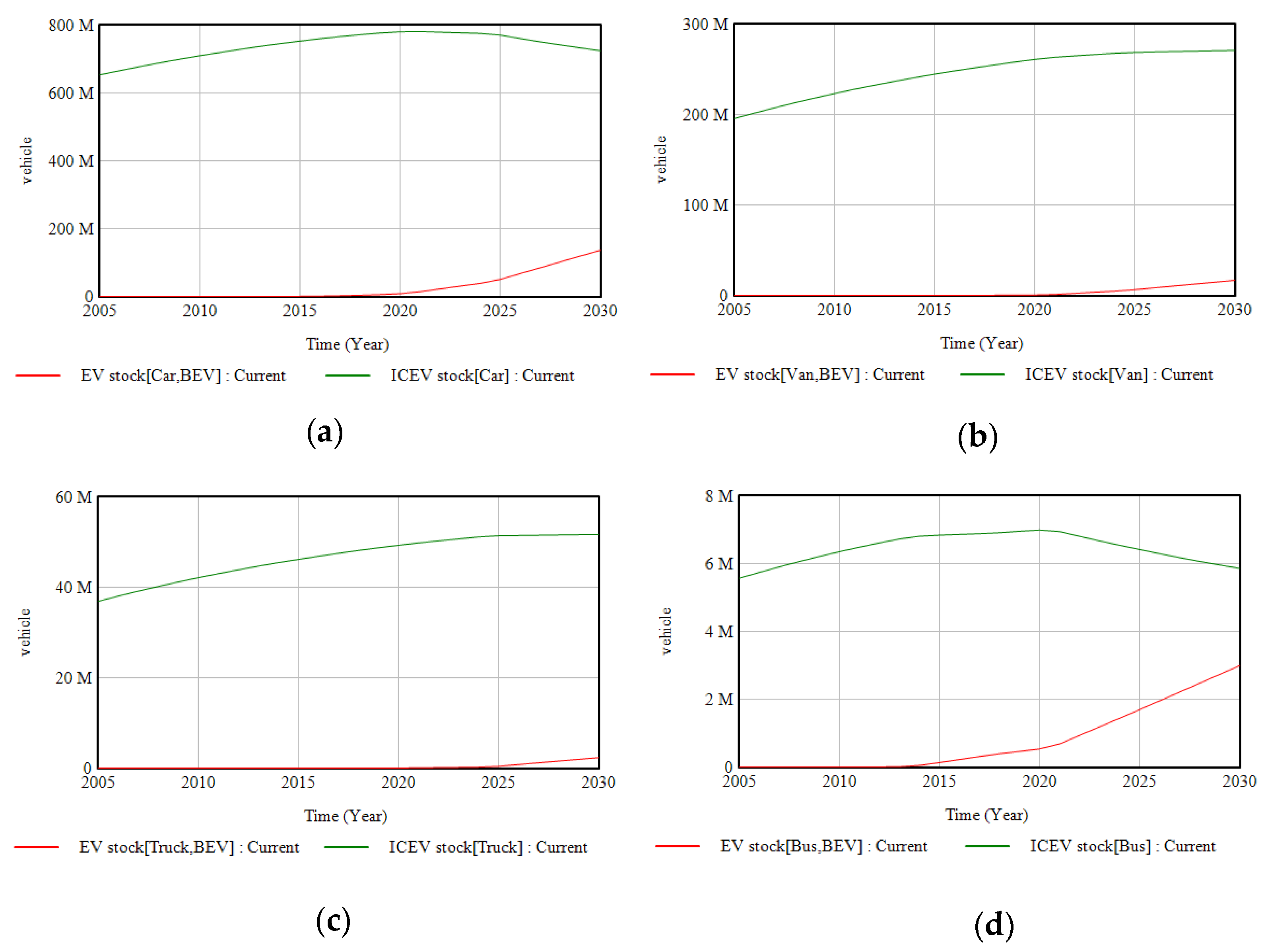

3.1. Evolution of the Vehicle Fleet

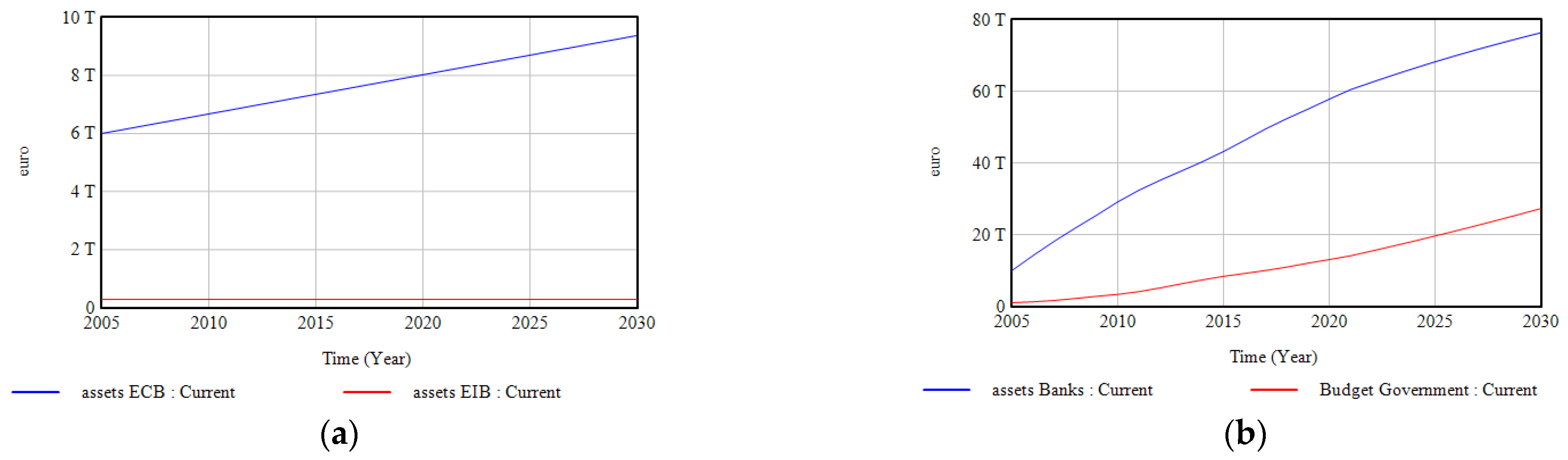

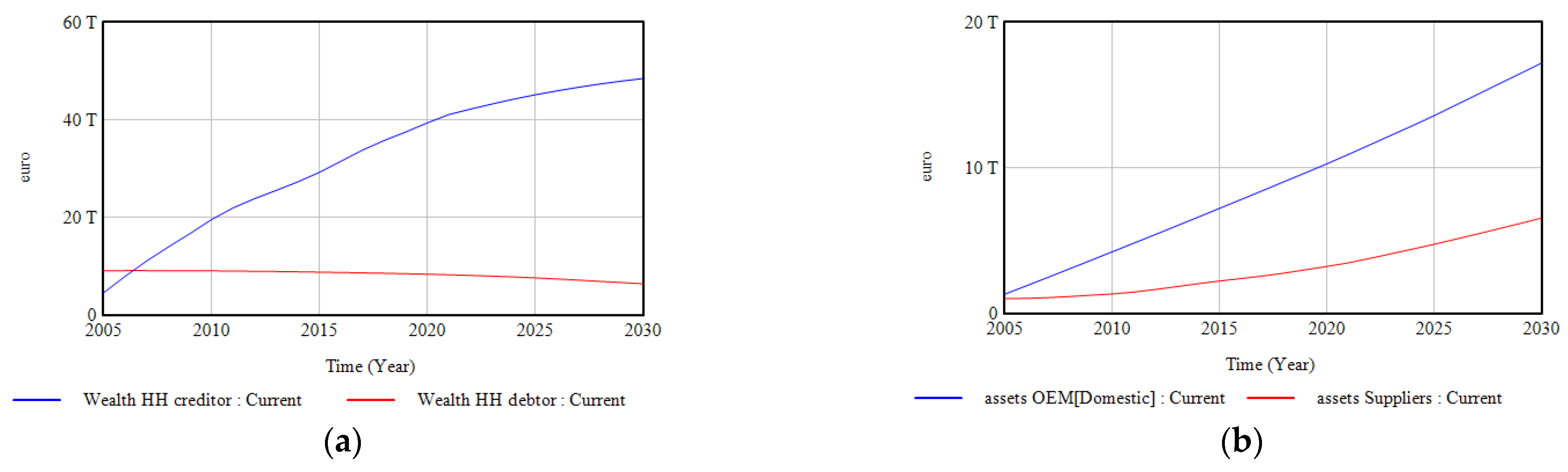

3.2. Balance Sheets

3.3. Key Performance Indicators

4. Discussion

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

References

- Harrison, G.; Thiel, C.; Jones, L. Powertrain Technology Transition Market Agent Model (PTTMAM): An Introduction; Publications Office of the European Union: Luxembourg, 2016. [Google Scholar]

- European Union. Regulation (EU) 2019/631 of the European Parliament and of the Council of 17 April 2019 Setting CO2 Emission Performance Standards for New Passenger Cars and for New Light Commercial Vehicles. 2019. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32019R0631 (accessed on 1 December 2022).

- Joint Research Centre. Powertrain Technology Transition Market Agent Model (PTTMAM). 2022. Available online: https://joint-research-centre.ec.europa.eu/scientific-tools-and-databases/powertrain-technology-transition-market-agent-model-pttmam/powertrain-technology-transition-market-agent-model-pttmam_en (accessed on 1 December 2022).

- Daimler. Annual Report 2020; Daimler AG: Stuttgart, Germany, 2021. [Google Scholar]

- Volkswagen. Annual Report 2020; Volkswagen (VW) AG: Wolfsburg, Germany, 2021. [Google Scholar]

- European Investment Bank. European Investment Bank (EIB). 2021. Available online: www.eib.org (accessed on 1 December 2022).

- Lam, A.; Mercure, J.-F. Which policy mixes are best for decarbonising passenger cars? Simulating interactions among taxes, subsidies and regulations for the United Kingdom, the United States, Japan, China, and India. Energy Res. Soc. Sci. 2021, 75, 101951. [Google Scholar] [CrossRef]

- Mercure, J.-F.; Salas, P.; Vercoulen, P.; Semieniuk, G.; Lam, A.; Pollitt, H.; Holden, P.B.; Vakilifard, N.; Chewpreecha, U.; Edwards, N.R.; et al. Reframing incentives for climate policy action. Nat. Energy 2021, 6, 1133–1143. [Google Scholar] [CrossRef]

- Jochem, P.; Gómez Vilchez, J.J.; Ensslen, A.; Schäuble, J.; Fichtner, W. Methods for forecasting the market penetration of electric drivetrains in the passenger car market. Transp. Rev. 2018, 38, 322–348. [Google Scholar] [CrossRef] [Green Version]

- Gómez Vilchez, J.J.; Jochem, P. Simulating vehicle fleet composition: A review of system dynamics models. Renew. Sustain. Energy Rev. 2019, 115, 109367. [Google Scholar] [CrossRef]

- Gómez Vilchez, J.J.; Jochem, P.; Fichtner, W. Interlinking major markets to explore electric car uptake. Energy Policy 2020, 144, 111588. [Google Scholar] [CrossRef]

- Gómez Vilchez, J.J.; Thiel, C. Simulating the battery price and the car-mix in key electro-mobility markets via model coupling. J. Simul. 2020, 14, 242–259. [Google Scholar] [CrossRef]

- Cavana, R.Y.; Dangerfield, B.C.; Pavlov, O.V.; Radzicki, M.J.; Wheat, I.D. Feedback Economics: Economic Modeling with System Dynamics; Springer International Publishing: Berlin/Heidelberg, Germany, 2021. [Google Scholar]

- Godley, W.; Lavoie, M. Monetary Economics: An Integrated Approach to Credit, Money, Income, Production and Wealth; Palgrave Macmillan: London, UK, 2007. [Google Scholar]

- Pasqualino, R.; Jones, A.W. Resources, Financial Risk and the Dynamics of Growth: Systems and Global Society; Taylor & Francis: Abingdon, UK, 2020. [Google Scholar]

- Battiston, S.; Monasterolo, I.; Riahi, K.; van Ruijven, B.J. Accounting for finance is key for climate mitigation pathways. Science 2021, 372, 918–920. [Google Scholar] [CrossRef] [PubMed]

- Dunz, N.; Naqvi, A.; Monasterolo, I. Climate sentiments, transition risk, and financial stability in a stock-flow consistent model. J. Financ. Stab. 2021, 54, 100872. [Google Scholar] [CrossRef]

- Xing, X.; Pan, H.; Deng, J. Carbon tax in a stock-flow consistent model: The role of commercial banks in financing low-carbon transition. Financ. Res. Lett. 2022, 50, 103186. [Google Scholar] [CrossRef]

- Sanders, M.; Serebriakova, A.; Fragkos, P.; Polzin, F.; Egli, F.; Steffen, B. Representation of financial markets in macro-economic transition models—A review and suggestions for extensions. Environ. Res. Lett. 2022, 17, 083001. [Google Scholar] [CrossRef]

- Sanz, R.A.; Arias, J.G.; Fidalgo, J.M.G.; García, R.M. Finanzas Empresariales; Centro de Estudios Ramón Areces: Madrid, Spain, 2016. [Google Scholar]

- Koo, R.C. The Holy Grail of Macroeconomics: Lessons from Japan’s Great Recession; Wiley: Hoboken, NJ, USA, 2011. [Google Scholar]

- KPMG. IFRS® Compared to US GAAP; KPMG International Limited: Amstelveen, The Netherlands, 2020. [Google Scholar]

- Ittelson, T. Financial Statements: A Step-by-Step Guide to Understanding and Creating Financial Reports; CAREER Press: Wayne, NJ, USA, 2020. [Google Scholar]

- Berk, J.; DeMarzo, P. Corporate Finance; Pearson: London, UK, 2019. [Google Scholar]

- Yamaguchi, K. Money and Macroeconomic Dynamics—Accounting System Dynamics Approach; Japan Futures Research Center: Awaji Island, Japan, 2020; Available online: http://www.muratopia.org/Yamaguchi/MacroBook.html (accessed on 10 February 2023).

- Bossel, H. Systems and Models: Complexity, Dynamics, Evolution, Sustainability; BoD—Books on Demand: Norderstedt, Germany, 2007. [Google Scholar]

- Sterman, J.D. Business Dynamics: Systems Thinking and Modeling for a Complex World; McGraw-Hill/Irwin: Boston, MA, USA, 2000. [Google Scholar]

- López, B.B.; Julve, V.M. Fundamentos de Contabilidad Financiera; Ediciones Pirámide: Madrid, Spain, 2021. [Google Scholar]

- Requeijo, J.; González, J.R. Técnicas Básicas de Estructura Económica; Delta Publicaciones: Kiel, WI, USA, 2007. [Google Scholar]

- Wheat, I.D. The feedback method of teaching macroeconomics: Is it effective? Syst. Dyn. Rev. 2007, 23, 391–413. [Google Scholar] [CrossRef]

- International Energy Agency. Global EV Data Explorer; International Energy Agency (IEA): Paris, France, 2021; Available online: https://www.iea.org/articles/global-ev-data-explorer (accessed on 1 December 2022).

- International Energy Agency. Global EV Outlook 2022; International Energy Agency (IEA): Paris, France, 2022. [Google Scholar]

- Blatcher, R. Distributor Markup and Profit Margins in the Supply Chain. PROS. 2018. Available online: https://pros.com/learn/blog/distributor-pricing-profit-margins-pricing-markups (accessed on 1 December 2022).

- Organización de Consumidores y Usuarios. Los coches más fiables; Organización de Consumidores y Usuarios (OCU), 2022. Available online: https://www.ocu.org/coches/coches/noticias/coches-mas-fiables (accessed on 1 December 2022).

- Eurofinas. Annual Survey 2021; Eurofinas: Brussels, Belgium, 2022. [Google Scholar]

- Pierson, K. Operationalizing Accounting Reporting in System Dynamics Models. Systems 2020, 8, 9. [Google Scholar] [CrossRef] [Green Version]

- Wells, P.E. The Automotive Industry in an Era of Eco-Austerity: Creating an Industry as If the Planet Mattered; Edward Elgar: Cheltenham, UK, 2010. [Google Scholar]

- Graham, B.; Dodd, D.L.F. Security Analysis: The Classic 1951 Edition; McGraw-Hill Education: New York, NY, USA, 2005. [Google Scholar]

- de Haan, J.; Oosterloo, S.; Schoenmaker, D. Financial Markets and Institutions; Cambridge University Press: Cambridge, UK, 2015. [Google Scholar]

- European Investment Bank. Energy Crisis Makes Public Banks Even More Important; European Investment Bank (EIB), 2022. Available online: https://www.eib.org/en/stories/energy-crisis-net-zero-transition?utm_source=mailjet&utm_medium=Email&utm_campaign=november&utm_content=na (accessed on 1 December 2022).

- Bayerische Motoren Werke. Annual Report 2019; Bayerische Motoren Werke (BMW) AG: Munich, Germany, 2020. [Google Scholar]

- Stigum, M.; Crescenzi, A. Stigum’s Money Market, 4E; McGraw Hill LLC: New York, NY, USA, 2007. [Google Scholar]

- McKinsey. In The Rise and Rise of the Global Balance Sheet—How Productively Are We Using Our Wealth? McKinsey Global Institute: Washington, DC, USA, 2021.

- European Central Bank. Annual Consolidated Balance Sheet of the Eurosystem; European Central Bank (ECB), 2022. Available online: https://www.ecb.europa.eu/pub/annual/balance/html/index.en.html (accessed on 1 December 2022).

- European Investment Bank. Shareholders. Shareholders; European Investment Bank (EIB), 2022. Available online: https://www.eib.org/en/about/governance-and-structure/shareholders/index.htm (accessed on 1 December 2022).

- International Monetary Fund. Public Sector Balance Sheet (PSBS) Database; International Monetary Fund (IMF), 2022. Available online: https://data.imf.org/?sk=82A91796-0326-4629-9E1D-C7F8422B8BE6 (accessed on 1 December 2022).

- Martinez-Moyano, I.J. Documentation for model transparency. Syst. Dyn. Rev. 2012, 28, 199–208. [Google Scholar] [CrossRef]

| Year | Name/Area | Firm | Finance [EURmio] |

|---|---|---|---|

| 2010 | R&D trucks | Daimler | 400 |

| 2010 | Environmentally friendly vehicles | Ford | 450 * |

| 2010 | EV and battery production | Nissan | 220 |

| 2011 | Research to meet emission targets | Fiat | 250 |

| 2011 | Hybridisation | BMW | 325 |

| 2011 | R&D (electrification) | Renault | 180 |

| 2012 | R&D (emissions/safety) | Daimler | 300 |

| 2013 | Innovative technologies | BMW | 400 |

| 2013 | Research to meet emission targets | Renault | 400 |

| 2013 | FCEV | Daimler | 400 |

| 2014 | R&D trucks | Daimler | 500 |

| 2014 | Innovative powertrains | VW | 500 |

| 2015 | R&D (efficient engines) | FCA | 600 |

| 2016 | R&D (alternative fuel/hybrid engines) | FCA | 250 |

| 2017 | Innovative powertrains | PSA | 250 |

| 2017 | R&D (hybrid/electric) | Volvo Cars | 245 |

| 2018 | Hybrid and electric vehicles | FCA | 420 |

| 2019 | Electric motor development | PSA/NIDEC | 145 |

| 2020 | EV (BEV/PHEV) production | FCA (Stellantis) | 300 |

| 2020 | PHEV production/R&D (automation) | FCA (Stellantis) | 485 |

| Balance Sheet Item | From OEM (Automotive) | From OEM (Financial) |

|---|---|---|

| Cash and cash equivalents | 1011 | |

| Loans to consumers | 7.87 × 1012 | |

| OEM debt (short-term) | 1.25 × 1011 | 7.21 × 1011 |

| OEM debt (long-term) | 1.73 × 1011 | 1.02 × 1012 |

| Deposits | 4.5 × 1012 | |

| Debt to central bank Equity | 4.5 × 1012 1012 | |

| Assets | 1013 | |

| Liabilities and equity | 1013 | |

| Balance Sheet Item | Creditor | Debtor |

|---|---|---|

| Wealth (assets) | 4.5 × 1012 | 9.04 × 1012 |

| Bank loans | 0 | 7.87 × 1012 |

| Debt to OEM (short-term) | 0 | 5.19 × 1011 |

| Debt to OEM (long-term) | 0 | 6.51 × 1011 |

| Equity | 4.5 × 1012 | 0 |

| Assets | 1.35 × 1013 | |

| Liabilities and equity | 1.35 × 1013 | |

| Balance Sheet Item | Automotive Division | Financial Division |

|---|---|---|

| Cash and cash equivalents | 9.73 × 1010 | 1.10 × 1010 |

| Securities | 8.43 × 1010 | 5.52 × 109 |

| Trade receivables | 5.51 × 1010 | 0 |

| Financial services receivables | 0 | 2.60 × 1011 |

| Inventories | 8.75 × 1010 | 0 |

| Property, plant & equipment | 2.16 × 1011 | 0 |

| Intangibles | 2.40 × 1010 | 0 |

| Leases | 0 | 1.40 × 1011 |

| Financial services noncurrent | 0 | 3.26 × 1011 |

| Trade payables | 1.07 × 1011 | 0 |

| Debt (short-term) | 6.27 × 1010 | 3.60 × 1011 |

| Debt (long-term) | 8.96 × 1010 | 5.08 × 1011 |

| Retained earnings | 1.55 × 1011 | |

| Reserves | 2.31 × 1010 | |

| Assets | 1.31 × 1012 | |

| Liabilities and equity | 1.31 × 1012 | |

| Constant/Variable | Value | Justification |

|---|---|---|

| Administrative intensity | 4% | Own analysis 1 |

| Corporate tax rate | 30% | [5] (p. 128) |

| Dividend distribution ratio | 40% | [4] (p. 133) |

| Emission penalties | EUR 0 | Assuming targets are met |

| Lifetime plant | 50 yr | Values range up to 60 yr |

| Lifetime vehicle | 5 yr | Values range up to 10 yr |

| Marketing intensity | 10% | Own analysis 1 |

| R&D intensity | 6% | Own analysis 1 |

| Revenues from leasing | EUR 4900/car | Own assumption |

| Spread over APR | 1% | Own assumption |

| Constant/Variable | Unit | Car | Van | Truck | Bus |

|---|---|---|---|---|---|

| Battery capacity 1 | kWh | 24/30/50 | 24/30/50 | 300 | 250 |

| Labour cost | EUR/vehicle | 5000 | 3750 | 25,000 | 50,000 |

| Material cost [BEV] | EUR/vehicle | 7845 | 4095 | 32,069 | 114,224 |

| Material cost [ICEV] | EUR/vehicle | 5000 | 3750 | 25,000 | 50,000 |

| Annual mileage | km/vehicle | 12,000 | 24,000 | 80,000 | 110,000 |

| Fuel efficiency [BEV] | kWh/km | 0.2 | 0.2 | 1.3 | 1.3 |

| Fuel efficiency [ICEV] | litre/km | 0.08 | 0.08 | 0.36 | 0.36 |

| KPI | Simulated 1 | 25% | Median | 75% |

|---|---|---|---|---|

| Gross margin | 42/37% | 28% | 43% | 63% |

| Operating margin | 20/16% | 6% | 12% | 22% |

| EBIT margin | 20/16% | 5% | 11% | 18% |

| Net profit margin | 13/11% | 2% | 7% | 15% |

| ROE | 7/4% | 3% | 10% | 18% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gómez Vilchez, J.J.; Pasqualino, R. The Hidden Side of Electro-Mobility: Modelling Agents’ Financial Statements and Their Interactions with a European Focus. Systems 2023, 11, 132. https://doi.org/10.3390/systems11030132

Gómez Vilchez JJ, Pasqualino R. The Hidden Side of Electro-Mobility: Modelling Agents’ Financial Statements and Their Interactions with a European Focus. Systems. 2023; 11(3):132. https://doi.org/10.3390/systems11030132

Chicago/Turabian StyleGómez Vilchez, Jonatan J., and Roberto Pasqualino. 2023. "The Hidden Side of Electro-Mobility: Modelling Agents’ Financial Statements and Their Interactions with a European Focus" Systems 11, no. 3: 132. https://doi.org/10.3390/systems11030132

APA StyleGómez Vilchez, J. J., & Pasqualino, R. (2023). The Hidden Side of Electro-Mobility: Modelling Agents’ Financial Statements and Their Interactions with a European Focus. Systems, 11(3), 132. https://doi.org/10.3390/systems11030132