How Does Digital Transformation Increase Corporate Sustainability? The Moderating Role of Top Management Teams

Abstract

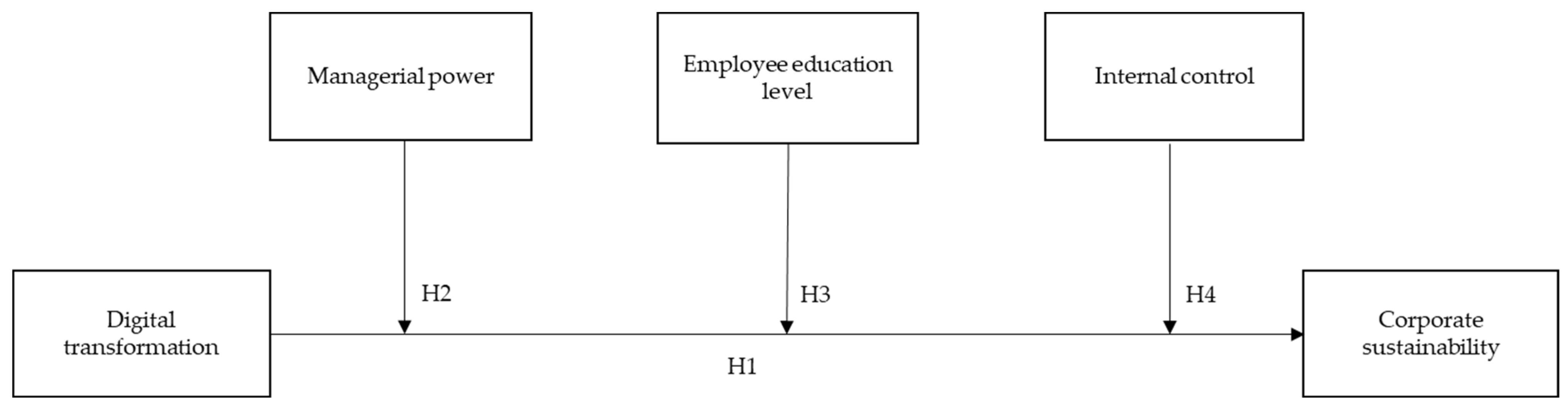

:1. Introduction

2. Theoretical Background and Hypothesis Development

2.1. Digital Transformation and Corporate Sustainability

2.2. The Moderating Effect of Managerial Power

2.3. The Moderating Effect of Employee Education Level

2.4. The Moderating Effect of Internal Control

3. Research Methodology and Design

3.1. Sample and Data Collection

3.2. Definition and Measurement of Variables

3.2.1. Dependent Variables

3.2.2. Independent Variables

3.2.3. Moderating Variables

3.2.4. Control Variables

3.3. Model Design

4. Results of the Empirical Analysis

4.1. Descriptive Statistics and Correlations

4.2. Analysis of the Empirical Results

Digital Transformation and Corporate Sustainability

4.3. Robustness Tests

4.3.1. Tests Based on Alternative Measurement of Dependent Variable

4.3.2. Tests Based on the Alternative Measurement of Independent Variable

4.3.3. Testing Based on Two-Stage Least Squares

5. Discussion and Conclusions

5.1. Discussion

5.2. Conclusions

5.3. Implications of the Study

- (1)

- The government perspective. There is a need to enhance financial and technical support for digital transformation initiatives within enterprises. Governments should acknowledge the significance of digital transformation as a crucial means to enhance the sustainability of businesses. Policymakers ought to implement effective measures that promote technology investments and offer targeted incentives, such as national Industry 4.0 programs. These actions not only foster the sustainability and resilience of business development in the face of challenges, such as the COVID-19 pandemic and global uncertainties, but also ensure the long-term success and adaptability of enterprises.

- (2)

- The corporate perspective. Firstly, companies should develop a digital transformation strategy that integrates sustainability goals, aligns digital initiatives with overall business strategies, and recognizes the potential of digital technologies for driving sustainability [15]. By actively transforming their business models, companies can enhance their competitive advantage through the effective use of digital technologies, thereby contributing to sustainable development objectives. Secondly, companies should prioritize genuine digitalization rather than mere informatization or networking. By leveraging digital technology, companies can establish seamless connectivity across various functions, such as procurement, production, marketing, finance, and human resources, thereby improving planning, coordination, monitoring, and control processes and eliminating “information silos”. Thirdly, digital transformation is a high-technology value-added transformation that often requires more qualified personnel. Companies can retain more high-quality “brains” by signing long-term contracts. Fourthly, it is essential to prioritize employee education, professional growth, and training to enhance their career development within the organization. This includes guiding employees with lower educational levels towards acquiring new skills and redirecting their career paths towards more specialized roles. Simultaneously, companies should actively encourage employees to pursue further education to expand their knowledge and qualifications, aligning with the evolving demands of the digital era. The organization can play an active role by sponsoring individuals to pursue higher education, facilitating their personal career development while also meeting the company’s specific needs in the digital landscape. Furthermore, organizations should implement training programs aimed at enhancing employees’ understanding of the principles and requirements of corporate sustainability. Such initiatives will help employees to comprehend their roles and responsibilities in driving sustainable development goals within the company [98].

- (3)

- The management perspective. To promote digital transformation and sustainable development, it is crucial to foster digital awareness and cultivate a digital mindset within the organization. When managers recognize the positive impact of digital transformation on business growth, they actively prioritize enhancing the digital capabilities of the company. They utilize their authority to drive the digitalization process, thereby providing strong support for open innovation and sustainable practices. Firstly, managers should possess a vision of digitizing their organizations and acknowledge the significance of digital capabilities for long-term competitiveness. They must leverage their influence to guide companies in embracing the opportunities presented by the digital era. Secondly, managers need to acquire a solid understanding of digitalization fundamentals and enhance their digital awareness. This entails gaining comprehensive knowledge of digital technologies and their operational management. By doing so, managers can effectively lead their companies in developing a corporate culture, organizational structure, and management team that align with the demands of the digital age [96].

5.4. Limitations and Future Directions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Detailed Keywords

| Artificial intelligence | Artificial intelligence, business intelligence, image interpretation, investment decision support system, intelligent data analysis, intelligent robot, machine learning, deep learning, semantic search, biometric technology, face recognition, speech recognition, authentication, automatic driving, natural language processing. |

| Big data technology | Big data, data mining, text mining, data visualization, heterogeneous data, credit investigation, augmented reality, mixed reality, virtual reality. |

| Cloud computing technology | Cloud computing, stream computing, graph computing, memory computing, multi-party security computing, brain like computing, green computing, cognitive computing, fusion architecture, hundred million concurrence, EB level storage, the Internet of things, information physics system. |

| Blockchain technology | Blockchain, digital currency, distributed computing, differential privacy technology, smart financial contract. |

| Digital technology application | Mobile Internet, industrial Internet, internet medical, e-commerce, mobile payment, third-party payment, NFC payment, smart energy, B2B, B2C, C2B, C2C, O2O, Internet connection, smart wear, smart agriculture, smart transportation, smart medical, smart customer service, smart home, smart investment consultant, smart culture and tourism, smart environmental protection, smart grid, smart marketing, Digital marketing, unmanned retail, Internet finance, digital finance, Fintech, financial technology, quantitative finance, open banking. |

References

- Vial, G. Understanding Digital Transformation: A Review and a Research Agenda. J. Strateg. Inf. Syst. 2019, 28, 118–144. [Google Scholar] [CrossRef]

- Verhoef, P.C.; Broekhuizen, T.; Bart, Y.; Bhattacharya, A.; Qi Dong, J.; Fabian, N.; Haenlein, M. Digital Transformation: A Multidisciplinary Reflection and Research Agenda. J. Bus. Res. 2021, 122, 889–901. [Google Scholar] [CrossRef]

- Hanelt, A.; Bohnsack, R.; Marz, D.; Antunes, C. A Systematic Review of the Literature on Digital Transformation: Insights and Implications for Strategy and Organizational Change. J. Manag. Stud. 2020, 58, 1159–1197. [Google Scholar] [CrossRef]

- Lyu, W.; Liu, J. Artificial Intelligence and Emerging Digital Technologies in the Energy Sector. Appl. Energy 2021, 303, 117615. [Google Scholar] [CrossRef]

- Li, L. Digital Transformation and Sustainable Performance: The Moderating Role of Market Turbulence. Ind. Mark. Manag. 2022, 104, 28–37. [Google Scholar] [CrossRef]

- United Nations. The Sustainable Development Goals Report 2022; United Nations: New York, NY, USA, 2022; Available online: https://unstats.un.org/sdgs/report/2022/ (accessed on 12 May 2023).

- European Commission. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions 2030 Digital Compass: The European Way for the Digital Decade COM/2021/118 Final; European Commission: Brussels, Belgium, 2021; Available online: https://eur-lex.europa.eu/legal-content/en/TXT/?uri=CELEX%3A52021DC0118 (accessed on 12 May 2023).

- Deloitte China. Interpretation of the 2023 Government Work Report & Industry Outlook; Deloitte: London, UK, 2013; Available online: https://www2.deloitte.com/cn/en/pages/public-sector/articles/interpretation-outlook-government-work-report-2023.html (accessed on 25 April 2023).

- Fernandez-Vidal, J.; Antonio Perotti, F.; Gonzalez, R.; Gasco, J. Managing Digital Transformation: The View from the Top. J. Bus. Res. 2022, 152, 29–41. [Google Scholar] [CrossRef]

- Ferreira, J.J.M.; Fernandes, C.I.; Ferreira, F.A.F. To Be or Not to Be Digital, That Is the Question: Firm Innovation and Performance. J. Bus. Res. 2019, 101, 583–590. [Google Scholar] [CrossRef]

- Reuschl, A.J.; Deist, M.K.; Maalaoui, A. Digital Transformation during a Pandemic: Stretching the Organizational Elasticity. J. Bus. Res. 2022, 144, 1320–1332. [Google Scholar] [CrossRef]

- Jia, J.; Li, Z. Does External Uncertainty Matter in Corporate Sustainability Performance? J. Corp. Financ. 2020, 65, 101743. [Google Scholar] [CrossRef]

- Baumgartner, R.J.; Rauter, R. Strategic Perspectives of Corporate Sustainability Management to Develop a Sustainable Organization. J. Clean. Prod. 2017, 140, 81–92. [Google Scholar] [CrossRef]

- Ghobakhloo, M. Industry 4.0, Digitization, and Opportunities for Sustainability. J. Clean. Prod. 2020, 252, 119869. [Google Scholar] [CrossRef]

- Guandalini, I. Sustainability through Digital Transformation: A Systematic Literature Review for Research Guidance. J. Bus. Res. 2022, 148, 456–471. [Google Scholar] [CrossRef]

- United Nations. Transforming Our World: The 2030 Agenda for Sustainable Development|Department of Economic and Social Affairs; Sdgs; United Nations: New York, NY, USA, 2023; Available online: https://sdgs.un.org/2030agenda (accessed on 12 May 2023).

- Wang, D.; Chen, S. Digital Transformation and Enterprise Resilience: Evidence from China. Sustainability 2022, 14, 14218. [Google Scholar] [CrossRef]

- Li, N.; Wang, X.; Wang, Z.; Luan, X. The Impact of Digital Transformation on Corporate Total Factor Productivity. Front. Psychol. 2022, 13, 1071986. [Google Scholar] [CrossRef] [PubMed]

- Kretschmer, T.; Khashabi, P. Digital Transformation and Organization Design: An Integrated Approach. Calif. Manag. Rev. 2020, 62, 86–104. [Google Scholar] [CrossRef]

- Zhai, H.; Yang, M.; Chan, K.C. Does Digital Transformation Enhance a Firm’s Performance? Evidence from China. Technol. Soc. 2022, 68, 101841. [Google Scholar] [CrossRef]

- Feng, H.; Wang, F.; Song, G.; Liu, L. Digital Transformation on Enterprise Green Innovation: Effect and Transmission Mechanism. Int. J. Environ. Res. Public Health 2022, 19, 10614. [Google Scholar] [CrossRef]

- Appio, F.P.; Frattini, F.; Petruzzelli, A.M.; Neirotti, P. Digital Transformation and Innovation Management: A Synthesis of Existing Research and an Agenda for Future Studies. J. Prod. Innov. Manag. 2021, 38, 4–20. [Google Scholar] [CrossRef]

- Su, J.; Su, K.; Wang, S. Does the Digital Economy Promote Industrial Structural Upgrading? A Test of Mediating Effects Based on Heterogeneous Technological Innovation. Sustainability 2021, 13, 10105. [Google Scholar] [CrossRef]

- Wu, L.; Sun, L.; Chang, Q.; Zhang, D.; Qi, P. How Do Digitalization Capabilities Enable Open Innovation in Manufacturing Enterprises? A Multiple Case Study Based on Resource Integration Perspective. Technol. Forecast. Soc. Change 2022, 184, 122019. [Google Scholar] [CrossRef]

- Zhang, T.; Shi, Z.Z.; Shi, Y.R.; Chen, N.J. Enterprise Digital Transformation and Production Efficiency: Mechanism Analysis and Empirical Research. Econ. Res.-Ekon. Istraživanja 2021, 35, 2781–2792. [Google Scholar] [CrossRef]

- Zeng, H.; Ran, H.; Zhou, Q.; Jin, Y.; Cheng, X. The Financial Effect of Firm Digitalization: Evidence from China. Technol. Forecast. Soc. Change 2022, 183, 121951. [Google Scholar] [CrossRef]

- Xu, Q.; Li, X.; Guo, F. Digital Transformation and Environmental Performance: Evidence from Chinese Resource-Based Enterprises. Corp. Soc. Responsib. Environ. Manag. 2023, 30, 1816–1840. [Google Scholar] [CrossRef]

- Del Río Castro, G.; González Fernández, M.C.; Uruburu Colsa, Á. Unleashing the Convergence amid Digitalization and Sustainability towards Pursuing the Sustainable Development Goals (SDGs): A Holistic Review. J. Clean. Prod. 2021, 280, 122204. [Google Scholar] [CrossRef]

- Bekaroo, G.; Bokhoree, C.; Pattinson, C. Impacts of ICT on the Natural Ecosystem: A Grassroot Analysis for Promoting Socio-Environmental Sustainability. Renew. Sustain. Energy Rev. 2016, 57, 1580–1595. [Google Scholar] [CrossRef]

- Solow, R. We’d Better Watch Out; New York Times Book Review: New York, NY, USA, 1987. [Google Scholar]

- Smith, A.; Voß, J.P.; Grin, J. Innovation Studies and Sustainability Transitions: The Allure of the Multi-Level Perspective and Its Challenges. Res. Policy 2010, 39, 435–448. [Google Scholar] [CrossRef]

- Beier, G.; Niehoff, S.; Ziems, T.; Xue, B. Sustainability Aspects of a Digitalized Industry: A Comparative Study from China and Germany. Int. J. Precis. Eng. Manuf.-Green Technol. 2017, 4, 227–234. [Google Scholar] [CrossRef]

- Flyverbom, M.; Deibert, R.; Matten, D. The Governance of Digital Technology, Big Data, and the Internet: New Roles and Responsibilities for Business. Bus. Soc. 2017, 58, 3–19. [Google Scholar] [CrossRef]

- Carnerud, D.; Mårtensson, A.; Ahlin, K.; Slumpi, T.P. On the Inclusion of Sustainability and Digitalisation in Quality Management: An Overview from Past to Present. Total Qual. Manag. Bus. Excell. 2020, 31, 1–23. [Google Scholar] [CrossRef]

- Oreg, S.; Bartunek, J.M.; Lee, G.; Do, B. An Affect-Based Model of Recipients’ Responses to Organizational Change Events. Acad. Manag. Rev. 2018, 43, 65–86. [Google Scholar] [CrossRef]

- Wrede, M.; Velamuri, V.K.; Dauth, T. Top Managers in the Digital Age: Exploring the Role and Practices of Top Managers in Firms’ Digital Transformation. Manag. Decis. Econ. 2020, 41, 1549–1567. [Google Scholar] [CrossRef]

- Bertrand, M.; Schoar, A. Managing with Style: The Effect of Managers on Firm Policies. Q. J. Econ. 2003, 118, 1169–1208. [Google Scholar] [CrossRef] [Green Version]

- Certo, S.T.; Lester, R.H.; Dalton, C.M.; Dalton, D.R. Top Management Teams, Strategy and Financial Performance: A Meta-Analytic Examination. J. Manag. Stud. 2006, 43, 813–839. [Google Scholar] [CrossRef]

- Finkelstein, S.; Hambrick, D.C.; Cannella, A.A. Strategic Leadership: Theory and Research on Executives, Top Management Teams, and Boards; Oxford University Press: New York, NY, USA, 2009. [Google Scholar]

- Firk, S.; Gehrke, Y.; Hanelt, A.; Wolff, M. Top Management Team Characteristics and Digital Innovation: Exploring Digital Knowledge and TMT Interfaces. Long Range Plan. 2021, 55, 102166. [Google Scholar] [CrossRef]

- Sun, S.; Li, T.; Ma, H.; Li, R.Y.M.; Gouliamos, K.; Zheng, J.; Han, Y.; Manta, O.; Comite, U.; Barros, T.; et al. Does Employee Quality Affect Corporate Social Responsibility? Evidence from China. Sustainability 2020, 12, 2692. [Google Scholar] [CrossRef] [Green Version]

- Ruiz-Pérez, F.; Lleó, Á.; Ormazábal, M. Employee Sustainable Behaviors and Their Relationship with Corporate Sustainability: A Delphi Study. J. Clean. Prod. 2021, 329, 129742. [Google Scholar] [CrossRef]

- Liu, Y.; Bian, Y.; Zhang, W. How Does Enterprises’ Digital Transformation Impact the Educational Structure of Employees? Evidence from China. Sustainability 2022, 14, 9432. [Google Scholar] [CrossRef]

- Call, A.C.; Kedia, S.; Rajgopal, S. Rank and File Employees and the Discovery of Misreporting: The Role of Stock Options. J. Account. Econ. 2016, 62, 277–300. [Google Scholar] [CrossRef]

- Call, A.C.; Campbell, J.L.; Dhaliwal, D.S.; Moon, J.R. Employee Quality and Financial Reporting Outcomes. J. Account. Econ. 2017, 64, 123–149. [Google Scholar] [CrossRef]

- Kong, D.; Zhang, B.; Zhang, J. Higher Education and Corporate Innovation. J. Corp. Financ. 2022, 72, 102165. [Google Scholar] [CrossRef]

- Păunescu, M. COSO Model for Internal Control (II). CECCAR Bus. Rev. 2020, 1, 40–46. [Google Scholar] [CrossRef] [Green Version]

- Liu, J.; Wu, Y.; Xu, H. The Relationship between Internal Control and Sustainable Development of Enterprises by Mediating Roles of Exploratory Innovation and Exploitative Innovation. Oper. Manag. Res. 2022, 15, 913–924. [Google Scholar] [CrossRef]

- Boulhaga, M.; Bouri, A.; Elamer, A.A.; Ibrahim, B.A. Environmental, Social and Governance Ratings and Firm Performance: The Moderating Role of Internal Control Quality. Corp. Soc. Responsib. Environ. Manag. 2022, 30, 134–145. [Google Scholar] [CrossRef]

- Akisik, O.; Gal, G. The Impact of Corporate Social Responsibility and Internal Controls on Stakeholders’ View of the Firm and Financial Performance. Sustain. Account. Manag. Policy J. 2017, 8, 246–280. [Google Scholar] [CrossRef]

- BUSINESS WIRE. Digital China Development Report (2022) Released, China’s Digital Economy Ranks Second in the World. San Francisco, United States. Available online: https://www.businesswire.com/news/home/20230429005017/en/Digital-China-Development-Report-2022-Released-Chinas-Digital-Economy-Ranks-Second-in-the-World (accessed on 15 May 2023).

- Reis, J.; Melão, N. Digital Transformation: A Meta-Review and Guidelines for Future Research. Heliyon 2023, 9, e12834. [Google Scholar] [CrossRef]

- Bieser, J.C.T.; Hilty, L.M. Indirect Effects of the Digital Transformation on Environmental Sustainability: Methodological Challenges in Assessing the Greenhouse Gas Abatement Potential of ICT. EPiC Ser. Comput. 2018, 52, 68–81. [Google Scholar] [CrossRef] [Green Version]

- Hrustek, L. Sustainability Driven by Agriculture through Digital Transformation. Sustainability 2020, 12, 8596. [Google Scholar] [CrossRef]

- Wernerfelt, B. A Resource-Based View of the Firm. Strateg. Manag. J. 1984, 5, 171–180. [Google Scholar] [CrossRef]

- Barney, J. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Amit, R.; Han, X. Value Creation through Novel Resource Configurations in a Digitally Enabled World. Strateg. Entrep. J. 2017, 11, 228–242. [Google Scholar] [CrossRef]

- Teece, D.J.; Pisano, G.; Shuen, A. Dynamic Capabilities and Strategic Management. Strateg. Manag. J. 1997, 18, 509–533. [Google Scholar] [CrossRef]

- Teece, D.J. Explicating Dynamic Capabilities: The Nature and Microfoundations of (Sustainable) Enterprise Performance. Strateg. Manag. J. 2007, 28, 1319–1350. [Google Scholar] [CrossRef] [Green Version]

- Dwivedi, Y.K.; Ismagilova, E.; Rana, N.P.; Raman, R. Social Media Adoption, Usage and Impact in Business-To-Business (B2B) Context: A State-Of-The-Art Literature Review. Inf. Syst. Front. 2021, 25, 971–993. [Google Scholar] [CrossRef]

- Kusiak, A. Smart Manufacturing Must Embrace Big Data. Nature 2017, 544, 23–25. [Google Scholar] [CrossRef] [PubMed]

- Teece, D.; Peteraf, M.; Leih, S. Dynamic Capabilities and Organizational Agility: Risk, Uncertainty, and Strategy in the Innovation Economy. Calif. Manag. Rev. 2016, 58, 13–35. [Google Scholar] [CrossRef] [Green Version]

- Helfat, C.E.; Winter, S.G. Untangling Dynamic and Operational Capabilities: Strategy for the (N)Ever-Changing World. Strateg. Manag. J. 2011, 32, 1243–1250. [Google Scholar] [CrossRef]

- Vaska, S.; Massaro, M.; Bagarotto, E.M.; Dal Mas, F. The Digital Transformation of Business Model Innovation: A Structured Literature Review. Front. Psychol. 2021, 11, 539363. [Google Scholar] [CrossRef]

- Kohtamäki, M.; Parida, V.; Patel, P.C.; Gebauer, H. The Relationship between Digitalization and Servitization: The Role of Servitization in Capturing the Financial Potential of Digitalization. Technol. Forecast. Soc. Change 2020, 151, 119804. [Google Scholar] [CrossRef]

- Colombi, C.; D’Itria, E. Fashion Digital Transformation: Innovating Business Models toward Circular Economy and Sustainability. Sustainability 2023, 15, 4942. [Google Scholar] [CrossRef]

- Zhang, Y.; Ma, X.; Pang, J.; Xing, H.; Wang, J. The Impact of Digital Transformation of Manufacturing on Corporate Performance—The Mediating Effect of Business Model Innovation and the Moderating Effect of Innovation Capability. Res. Int. Bus. Financ. 2023, 64, 101890. [Google Scholar] [CrossRef]

- Demartini, M.; Evans, S.; Tonelli, F. Digitalization Technologies for Industrial Sustainability. Procedia Manuf. 2019, 33, 264–271. [Google Scholar] [CrossRef]

- Shang, Y.; Raza, S.A.; Huo, Z.; Shahzad, U.; Zhao, X. Does Enterprise Digital Transformation Contribute to the Carbon Emission Reduction? Micro-Level Evidence from China. Int. Rev. Econ. Financ. 2023, 86, 1–13. [Google Scholar] [CrossRef]

- Zhang, Y.; Ren, S.; Liu, Y.; Si, S. A Big Data Analytics Architecture for Cleaner Manufacturing and Maintenance Processes of Complex Products. J. Clean. Prod. 2017, 142, 626–641. [Google Scholar] [CrossRef] [Green Version]

- Hambrick, D.C.; Mason, P.A. Upper Echelons: The Organization as a Reflection of Its Top Managers. Acad. Manag. Rev. 1984, 9, 193–206. [Google Scholar] [CrossRef]

- Finkelstein, S. Power in Top Management Teams: Dimensions, Measurement, and Validation. Acad. Manag. J. 1992, 35, 505–538. [Google Scholar] [CrossRef]

- Demerjian, P.; Lev, B.; McVay, S. Quantifying Managerial Ability: A New Measure and Validity Tests. Manag. Sci. 2012, 58, 1229–1248. [Google Scholar] [CrossRef] [Green Version]

- Milgrom, P.; Roberts, J. Predation, Reputation, and Entry Deterrence. J. Econ. Theory 1982, 27, 280–312. [Google Scholar] [CrossRef] [Green Version]

- Bebchuk, L.A.; Fried, J.M. Executive Compensation as an Agency Problem. J. Econ. Perspect. 2003, 17, 71–92. [Google Scholar] [CrossRef] [Green Version]

- Jiang, B.; Murphy, P.J. Do Business School Professors Make Good Executive Managers? Acad. Manag. Perspect. 2007, 21, 29–50. [Google Scholar] [CrossRef] [Green Version]

- Coff, R. Human Capital, Shared Expertise, and the Likelihood of Impasse in Corporate Acquisitions. J. Manag. 2002, 28, 107–128. [Google Scholar] [CrossRef]

- Wang, M.; Yan, W. Brain Gain: The Effect of Employee Quality on Corporate Social Responsibility. Abacus 2022, 58, 679–713. [Google Scholar] [CrossRef]

- Li, L.; Ye, F.; Zhan, Y.; Kumar, A.; Schiavone, F.; Li, Y. Unraveling the Performance Puzzle of Digitalization: Evidence from Manufacturing Firms. J. Bus. Res. 2022, 149, 54–64. [Google Scholar] [CrossRef]

- Committee of Sponsoring Organisations of the Treadway Commission (COSO). Internal Control: Integrated Framework; Academia: San Francisco, CA, USA, 1992; Available online: https://www.academia.edu/12912529/INTERNAL_CONTROL_INTEGRATED_FRAMEWORK_Committee_of_Sponsoring_Organizations_of_the_Treadway_Commission (accessed on 15 May 2023).

- Ashbaugh-Skaife, H.; Collins, D.W.; Kinney, W.R. The Discovery and Reporting of Internal Control Deficiencies prior to SOX-Mandated Audits. J. Account. Econ. 2007, 44, 166–192. [Google Scholar] [CrossRef]

- Sun, Y.; He, M. Does Digital Transformation Promote Green Innovation? A Micro-Level Perspective on the Solow Paradox. Front. Environ. Sci. 2023, 11, 1134447. [Google Scholar] [CrossRef]

- Feng, M.; Li, C.; McVay, S. Internal Control and Management Guidance. J. Account. Econ. 2009, 48, 190–209. [Google Scholar] [CrossRef]

- Zhang, C.; Chen, P.; Hao, Y. The Impact of Digital Transformation on Corporate Sustainability: New Evidence from Chinese Listed Companies. Front. Environ. Sci. 2022, 10, 1047418. [Google Scholar] [CrossRef]

- Liao, Y.; Qiu, X.; Wu, A.; Sun, Q.; Shen, H.; Li, P. Assessing the Impact of Green Innovation on Corporate Sustainable Development. Front. Energy Res. 2022, 9, 800848. [Google Scholar] [CrossRef]

- Wu, K.; Fu, Y.; Kong, D. Does the Digital Transformation of Enterprises Affect Stock Price Crash Risk? Financ. Res. Lett. 2022, 48, 102888. [Google Scholar] [CrossRef]

- Guo, X.; Song, X.; Dou, B.; Wang, A.; Hu, H. Can Digital Transformation of the Enterprise Break the Monopoly? Pers. Ubiquitous Comput. 2022, 26, 1–14. [Google Scholar] [CrossRef]

- Cao, Q.; Yang, F.; Liu, M. Impact of Managerial Power on Regulatory Inquiries from Stock Exchanges: Evidence from the Text Tone of Chinese Listed Companies’ Annual Reports. Pac.-Basin Financ. J. 2022, 71, 101646. [Google Scholar] [CrossRef]

- Ji, Z.; Zhou, T.; Zhang, Q. The Impact of Digital Transformation on Corporate Sustainability: Evidence from Listed Companies in China. Sustainability 2023, 15, 2117. [Google Scholar] [CrossRef]

- Zheng, S.; Jin, S. Can Companies Reduce Carbon Emission Intensity to Enhance Sustainability? Systems 2023, 11, 249. [Google Scholar] [CrossRef]

- Pappas, I.O.; Mikalef, P.; Dwivedi, Y.K.; Jaccheri, L.; Krogstie, J. Responsible Digital Transformation for a Sustainable Society. Inf. Syst. Front. 2023, 25, 945–953. [Google Scholar] [CrossRef]

- Tian, G.; Li, B.; Cheng, Y. Does Digital Transformation Matter for Corporate Risk-Taking? Financ. Res. Lett. 2022, 49, 103107. [Google Scholar] [CrossRef]

- Wang, A.; Han, R. Can Digital Transformation Prohibit Corporate Fraud? Empir. Evid. China 2023, 30, 1–8. [Google Scholar] [CrossRef]

- Lin, B.; Zhang, Q. Corporate Environmental Responsibility in Polluting Firms: Does Digital Transformation Matter? Corp. Soc. Responsib. Environ. Manag. 2023, 30, 2. [Google Scholar] [CrossRef]

- Feroz, A.K.; Zo, H.; Eom, J.; Chiravuri, A. Identifying Organizations’ Dynamic Capabilities for Sustainable Digital Transformation: A Mixed Methods Study. Technol. Soc. 2023, 73, 102257. [Google Scholar] [CrossRef]

- Shin, J.; Mollah, M.A.; Choi, J. Sustainability and Organizational Performance in South Korea: The Effect of Digital Leadership on Digital Culture and Employees’ Digital Capabilities. Sustainability 2023, 15, 2027. [Google Scholar] [CrossRef]

- Brenner, B.; Hartl, B. The Perceived Relationship between Digitalization and Ecological, Economic, and Social Sustainability. J. Clean. Prod. 2021, 315, 128128. [Google Scholar] [CrossRef]

- Pellegrini, C.; Rizzi, F.; Frey, M. The Role of Sustainable Human Resource Practices in Influencing Employee Behavior for Corporate Sustainability. Bus. Strategy Environ. 2018, 27, 1221–1232. [Google Scholar] [CrossRef]

{kind=link}

| Types | Variables | Definition | Measurement |

|---|---|---|---|

| Dependent Variable | SGR | Sustainable development | Net sales interest rate × total asset turnover × income retention rate × equity multiplier/(1 − net sales interest rate × total asset turnover × income retention rate × equity multiplier) |

| Independent variable | DT | Digital transformation | Natural logarithm of the frequency of occurrence of the corresponding digital keywords in the annual reports plus 1 |

| Moderating variables | MP | Managerial power | Tenure, Dual, Insider, and Mgshder, which were synthesized into a composite index using principal component analysis |

| EDU | Employee education level | Employees with bachelor’s degree or higher/total employees | |

| IC | Internal control | DIB internal control index | |

| Control variables | Size | Firm size | Natural logarithm of total assets for the year |

| Age | Listing age | Natural logarithm of the difference between the current year and the listing year plus 1 | |

| Cashflow | Cash flow ratio | Net cash flow from operating activities/total assets | |

| Lev | Debt to assets ratio | Total liabilities/total assets | |

| Top1 | Largest ownership | Shareholding ratio of the largest shareholder |

| Variables | N | Mean | SD | Min | Median | Max |

|---|---|---|---|---|---|---|

| SGR | 12,544 | 0.055 | 0.043 | −0.021 | 0.049 | 0.332 |

| DT | 12,544 | 1.122 | 1.266 | 0 | 0.693 | 5.088 |

| MP | 12,544 | 0.342 | 1.231 | −2.226 | 0.222 | 3.191 |

| EDU | 12,544 | 0.237 | 0.203 | 0 | 0.181 | 0.874 |

| IC | 12,544 | 5.958 | 1.985 | 0 | 6.615 | 7.5 |

| Size | 12,544 | 21.631 | 1.149 | 19.349 | 21.512 | 25.274 |

| Lev | 12,544 | 0.365 | 0.194 | 0.044 | 0.347 | 0.833 |

| Age | 12,544 | 1.868 | 0.906 | 0 | 1.946 | 3.258 |

| Cashflow | 12,544 | 0.045 | 0.063 | −0.15 | 0.045 | 0.233 |

| Top1 | 12,544 | 0.34 | 0.139 | 0.09 | 0.321 | 0.724 |

| Variables | SGR | DT | MP | EDU | IC | Size | Lev | Age | Cashflow | Top1 |

|---|---|---|---|---|---|---|---|---|---|---|

| SGR | 1 | |||||||||

| DT | 0.121 *** | 1 | ||||||||

| MP | 0.052 *** | 0.154 *** | 1 | |||||||

| EDU | 0.078 *** | 0.424 *** | 0.082 *** | 1 | ||||||

| IC | 0.034 *** | 0.089 *** | −0.097 *** | 0.070 *** | 1 | |||||

| Size | 0.052 *** | 0.045 *** | −0.364 *** | 0.044 *** | 0.314 *** | 1 | ||||

| Lev | 0.040 *** | −0.061 *** | −0.269 *** | −0.051 *** | 0.175 *** | 0.566 *** | 1 | |||

| Age | −0.076 *** | 0.017 * | −0.385 *** | 0.002 | 0.506 *** | 0.625 *** | 0.412 *** | 1 | ||

| Cashflow | 0.283 *** | −0.014 | −0.038 *** | −0.054 *** | 0.069 *** | 0.070 *** | −0.127 *** | 0.072 *** | 1 | |

| Top1 | 0.069 *** | −0.129 *** | −0.055 *** | −0.089 *** | −0.024 *** | 0.098 *** | 0.058 *** | −0.042 *** | 0.050 *** | 1 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| SGR | SGR | SGR | SGR | |

| DT | 0.0034 *** | 0.0032 *** | 0.0031 *** | 0.0031 *** |

| (6.4577) | (6.0684) | (5.8652) | (5.8929) | |

| MP | 0.0003 | |||

| (0.5276) | ||||

| DT × MP | 0.0014 *** | |||

| (4.5091) | ||||

| EDU | 0.0018 | |||

| (0.3961) | ||||

| DT × EDU | 0.0120 *** | |||

| (6.2648) | ||||

| IC | 0.0025 *** | |||

| (9.5455) | ||||

| DT*IC | 0.0010 *** | |||

| (5.3181) | ||||

| Size | 0.0002 | 0.0003 | −0.0001 | −0.0008 |

| (0.1619) | (0.2944) | (−0.0940) | (−0.7584) | |

| Lev | 0.0326 *** | 0.0315 *** | 0.0316 *** | 0.0370 *** |

| (8.2550) | (7.9625) | (7.9922) | (9.3319) | |

| Age | −0.0053 *** | −0.0062 *** | −0.0058 *** | −0.0133 *** |

| (−4.0997) | (−4.7357) | (−4.4910) | (−8.0028) | |

| Cashflow | 0.1557 *** | 0.1552 *** | 0.1558 *** | 0.1564 *** |

| (23.7017) | (23.6521) | (23.7601) | (23.9173) | |

| Top1 | 0.0129 * | 0.0129 * | 0.0132 ** | 0.0057 |

| (1.9411) | (1.9397) | (1.9953) | (0.8614) | |

| _cons | 0.0312 | 0.0312 | 0.0369 | 0.0663 *** |

| (1.2300) | (1.2286) | (1.4431) | (2.5846) | |

| Industry | Yes | Yes | Yes | Yes |

| Firm | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes |

| N | 12,544 | 12,544 | 12,544 | 12,544 |

| R2 | 0.0728 | 0.0746 | 0.0764 | 0.0815 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| SGR | SGR | SGR | SGR | |

| DIG | 0.0048 *** | 0.0044 *** | 0.0034 *** | 0.0047 *** |

| (5.3360) | (4.7513) | (3.5504) | (5.1427) | |

| MP | 0.0001 | |||

| (0.1951) | ||||

| DT × MP | 0.0015 *** | |||

| (2.7427) | ||||

| EDU | 0.0042 | |||

| (0.9543) | ||||

| DT × EDU | 0.0139 *** | |||

| (4.5196) | ||||

| IC | 0.0022 *** | |||

| (8.6271) | ||||

| DT × IC | 0.0007 *** | |||

| (2.5900) | ||||

| Size | 0.0007 | 0.0007 | 0.0005 | −0.0003 |

| (0.6932) | (0.7093) | (0.4863) | (−0.3416) | |

| Lev | 0.0325 *** | 0.0320 *** | 0.0320 *** | 0.0369 *** |

| (8.2158) | (8.0858) | (8.0857) | (9.2804) | |

| Age | −0.0052 *** | −0.0056 *** | −0.0055 *** | −0.0138 *** |

| (−4.0310) | (−4.2701) | (−4.2147) | (−8.2733) | |

| Cashflow | 0.1549 *** | 0.1545 *** | 0.1548 *** | 0.1556 *** |

| (23.5734) | (23.5090) | (23.5783) | (23.7677) | |

| Top1 | 0.0112 * | 0.0114 * | 0.0113 * | 0.0041 |

| (1.6888) | (1.7240) | (1.7100) | (0.6215) | |

| _cons | 0.0190 | 0.0220 | 0.0256 | 0.0571 ** |

| (0.7522) | (0.8710) | (1.0050) | (2.2327) | |

| Industry | Yes | Yes | Yes | Yes |

| Firm | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes |

| N | 12,544 | 12,544 | 12,544 | 12,544 |

| R2 | 0.0716 | 0.0723 | 0.0736 | 0.0784 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| SGRA | SGRA | SGRA | SGRA | |

| DT | 0.0043 *** | 0.0041 *** | 0.0040 *** | 0.0037 *** |

| (7.1366) | (6.7883) | (6.6217) | (6.2172) | |

| MP | 0.0001 | |||

| (0.1230) | ||||

| DT × MP | 0.0018 *** | |||

| (4.9662) | ||||

| EDU | −0.0013 | |||

| (−0.2610) | ||||

| DT × EDU | 0.0157 *** | |||

| (6.7325) | ||||

| IC | 0.0009 *** | |||

| (3.1126) | ||||

| DT*IC | 0.0016 *** | |||

| (7.6197) | ||||

| Size | −0.0046 *** | −0.0045 *** | −0.0049 *** | −0.0045 *** |

| (−4.0460) | (−3.9195) | (−4.2534) | (−3.9295) | |

| Lev | 0.0388 *** | 0.0373 *** | 0.0374 *** | 0.0396 *** |

| (8.5448) | (8.2106) | (8.2381) | (8.6836) | |

| Age | −0.0176 *** | −0.0188 *** | −0.0184 *** | −0.0176 *** |

| (−11.8530) | (−12.4922) | (−12.3300) | (−9.1885) | |

| Cashflow | 0.1693 *** | 0.1688 *** | 0.1694 *** | 0.1695 *** |

| (22.4520) | (22.4010) | (22.5043) | (22.5379) | |

| Top1 | −0.0021 | −0.0019 | −0.0017 | −0.0031 |

| (−0.2760) | (−0.2530) | (−0.2228) | (−0.4082) | |

| _cons | 0.1616 *** | 0.1620 *** | 0.1662 *** | 0.1639 *** |

| (5.5543) | (5.5571) | (5.6629) | (5.5552) | |

| Industry | Yes | Yes | Yes | Yes |

| Firm | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes |

| N | 12,544 | 12,544 | 12,544 | 12,544 |

| R2 | 0.0934 | 0.0957 | 0.0979 | 0.0986 |

| Stage 1 | Stage 2 | |

|---|---|---|

| DT | SGR | |

| DT | 0.0160 *** | |

| (3.5430) | ||

| DTmean | 0.5267 *** | |

| (12.9448) | ||

| Size | 0.2013 *** | −0.0024 |

| (10.8277) | (−1.5527) | |

| Lev | −0.0821 | 0.0335 *** |

| (−1.1065) | (7.3343) | |

| Age | 0.1327 *** | −0.0072 *** |

| (5.4553) | (−4.8397) | |

| Cashflow | −0.2200 * | 0.1582 *** |

| (−1.7849) | (19.8768) | |

| Top1 | −0.8440 *** | 0.0241 *** |

| (−6.7845) | (2.6635) | |

| Industry | Yes | Yes |

| Firm | Yes | Yes |

| Year | Yes | Yes |

| N | 12,538 | 12,328 |

| R2 | 0.3349 | 0.0196 |

| Number of ID | 2137 | 1927 |

| Kleibergen–Paap rk LM statistic | 103.62 (Chi-sq(1)p-val = 0.0000) | |

| Cragg–Donald Wald F statistic | 167.57 | |

| Kleibergen–Paap Wald rk F statistic | 118.77 | |

| 10% maximal IV size | 16.38 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, Y.; Jin, S. How Does Digital Transformation Increase Corporate Sustainability? The Moderating Role of Top Management Teams. Systems 2023, 11, 355. https://doi.org/10.3390/systems11070355

Zhang Y, Jin S. How Does Digital Transformation Increase Corporate Sustainability? The Moderating Role of Top Management Teams. Systems. 2023; 11(7):355. https://doi.org/10.3390/systems11070355

Chicago/Turabian StyleZhang, Yaxin, and Shanyue Jin. 2023. "How Does Digital Transformation Increase Corporate Sustainability? The Moderating Role of Top Management Teams" Systems 11, no. 7: 355. https://doi.org/10.3390/systems11070355

APA StyleZhang, Y., & Jin, S. (2023). How Does Digital Transformation Increase Corporate Sustainability? The Moderating Role of Top Management Teams. Systems, 11(7), 355. https://doi.org/10.3390/systems11070355