As is apparent from the previous section, system dynamics does not represent a mainstream approach to modelling environment–economy systems. However, the ideas published in Limits to Growth and later confirmed prove that the application of the system dynamics approach can be very fruitful. From a methodological point of view, it can provide an alternative perspective on modelled systems to investigators. Therefore, a brief introduction to system dynamics and its application in a neoclassical Solow–Swan growth model is presented in the next two subsections.

3.1. System Dynamics

The rationale for the application of system dynamics is that a non-systemic approach to economic modelling is in stark contrast to this modelling paradigm, which carefully considers various interactions between the economy and the environment, its inputs in the form of stocks of non-renewable and renewable resources, and outputs and sinks (e.g., greenhouse gases dumped into the atmosphere) during model development. According to Radzicki [

46], system dynamics is a computer simulation modelling methodology that is used to analyse complex nonlinear dynamic feedback systems to generate insight and design policies that will improve system performance. It was originally created in 1957 by Jay W. Forrester of the Massachusetts Institute of Technology as a methodology for building computer simulation models of problematic behaviour within corporations. The models were used to design and test policies aimed at altering a corporation’s structure so that its behaviour would improve and become more robust. Radzicki further states that there are three principal ways that system dynamics is used for economic modelling. The first involves translating an existing economic model into a system dynamics format, while the second involves creating an economic model from scratch by following the rules and guidelines of the system dynamics paradigm. The former approach is valuable because it enables well-known economic models to be represented in a standard format, which makes comparing and contrasting their assumptions, concepts, and behaviour easy. The latter approach is valuable because it usually yields models that are more realistic and that produce results that are counterintuitive.

From a system dynamics perspective, a system’s structure consists of stocks, flows and feedback loops. Stocks can be thought of as bathtubs that accumulate/decumulate a system’s flows over time. Flows can be thought of as pipe and faucet assemblies that fill or drain the stocks. Mathematically, the process of flows accumulating/decumulating in stocks is called integration. The integration process creates all dynamic behaviour in the world, be it in a physical system, a biological system, or a socioeconomic system. An example of stock and flow in the economic system can be the total capital present in the economy, its inflow of investment spending and its outflow of depreciation [

46].

Based on Radzicki’s classification, this study is based on the third way that system dynamics can be used for economic modelling. This is represented by a “hybrid” approach in which a well-known economic model is translated into a system dynamics format, critiqued, and then improved by modifying it so that it more closely adheres to the principles of system dynamics modelling. This approach attempts to blend the advantages of the first two approaches, although it is more closely related to the former. Existing economic models that have been created in an ordinary differential equation format can be translated into system dynamics, and in Figure 3 in his article Radzicki presents the Robert Solow’s ordinary differential equation growth model in a system dynamics format [

46].

We have selected this model for the extension by the energy sector despite the fact that it was published in 1956. Daron Acemoglu describes it as the ‘workhorse model’, still essential for macroeconomics, and praises it for its simplicity [

47]. This makes it ideal for the purposes of this article, as the extended model used in this study should be as simple as possible, to be relatively easily interpretable and understandable, in compliance with the term coined by Professor Bardi, the model should be ‘mind sized’ [

48]. Most of the models of economic growth introduced later on are variations of the basic Solow–Swan model, where the model is varied by the inclusion of human capital into the model (Uzawa–Lucas model) or endogenization of technical progress by explicit modelling of the R&D process (Romer model).

3.2. Model Description

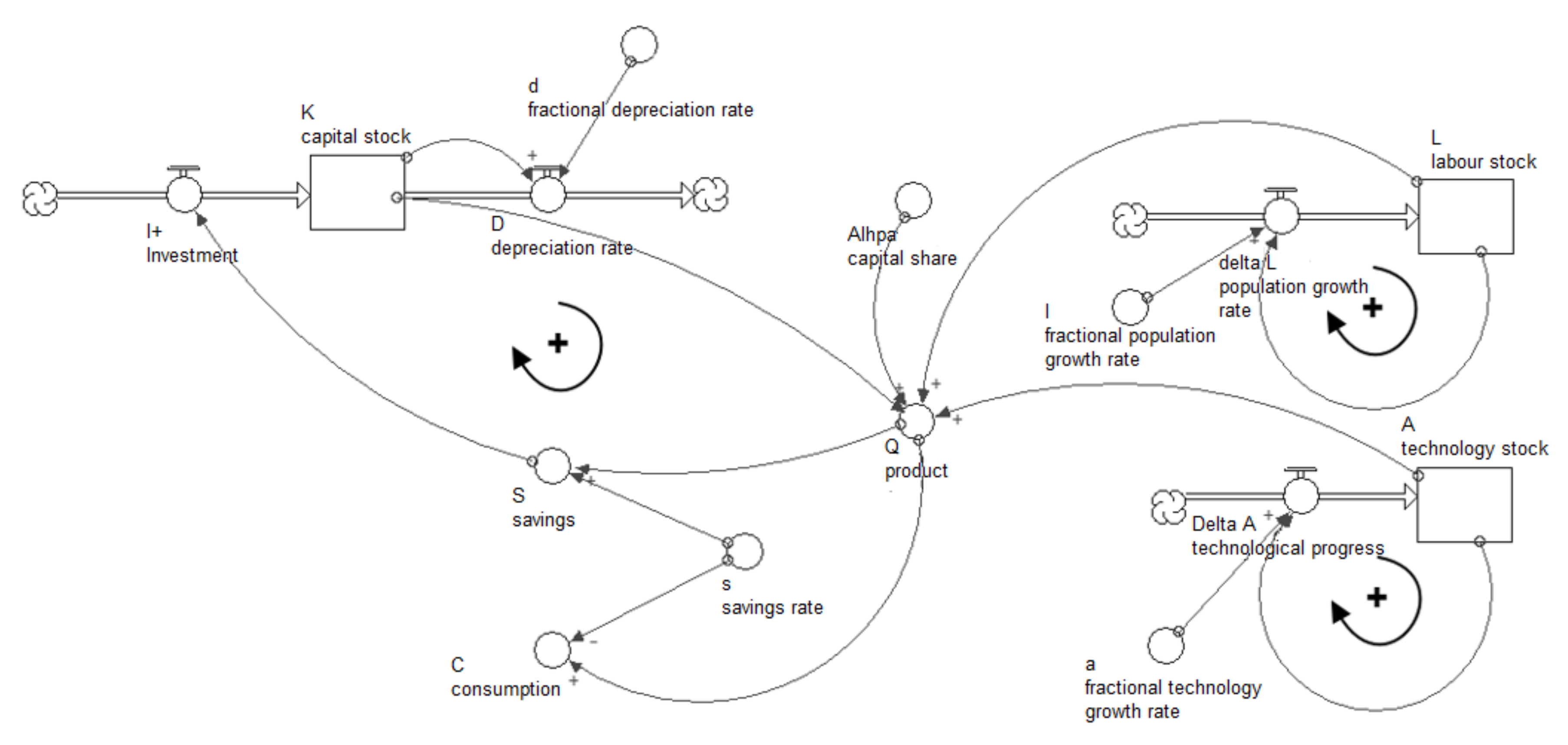

The Solow–Swan growth model consists of three stocks—the capital stock Kt, the population stock Lt (model assumes that all people work, therefore, it also represents total labour supply) and the third stock, At, which represents the state of technology.

Economic product

Q is represented by the Cobb–Douglas production function:

where

is the capital elasticity in production. The model employs the pattern of exponential growth in two components—the labour force and technology:

where

and

are the stocks initial levels and

l and

a are their respective growth rates, and

t represents the time step in the model. Capital stock is influenced by the savings,

S, and depreciation rate,

D. Constant share of product is saved

and the model assumes a closed economy, therefore

Depreciation rate

D is defined as a constant rate of capital degradation:

The last equation describes capital dynamics:

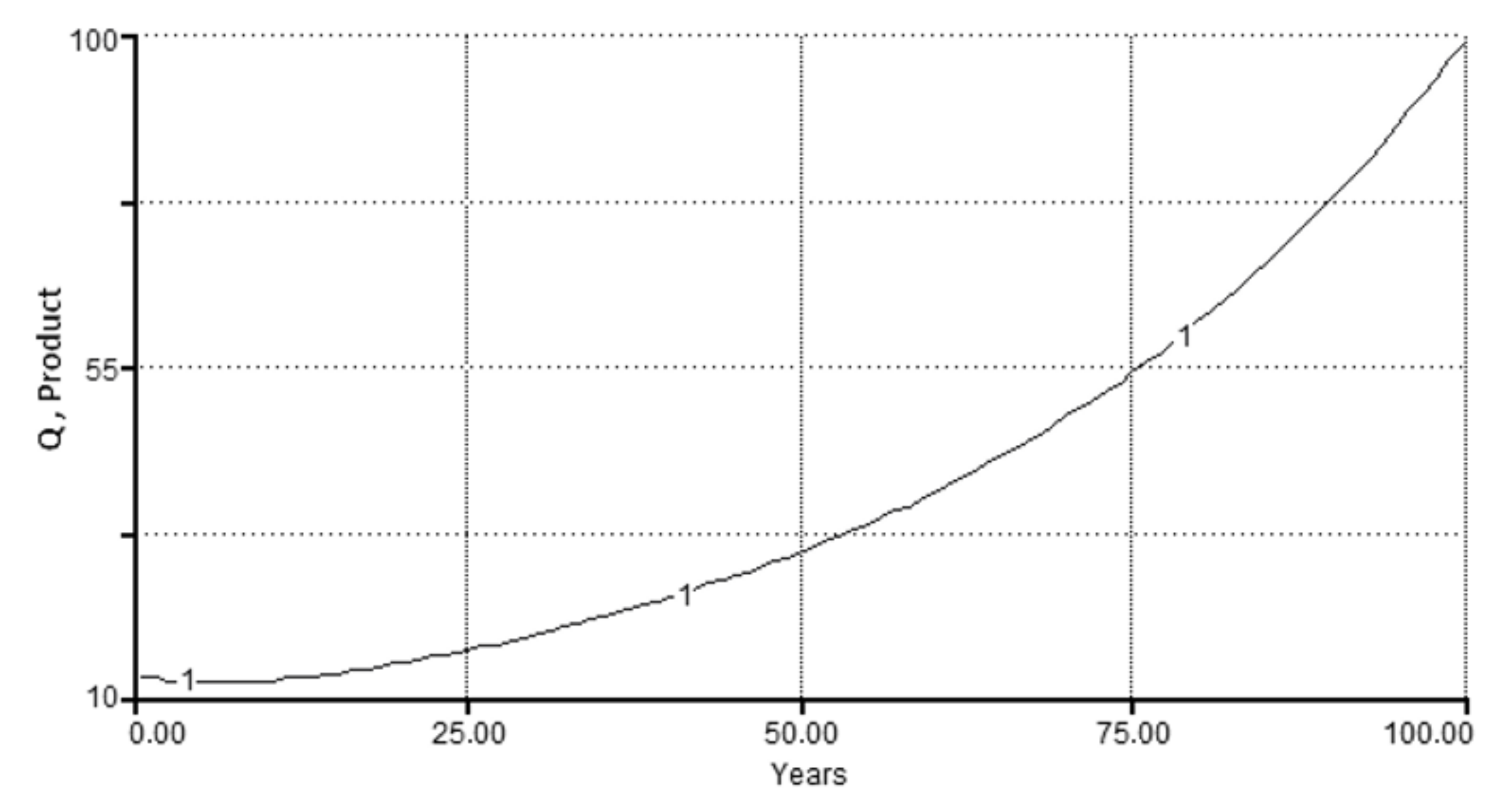

The model scheme in system dynamics notation is presented in

Figure 1 alongside the representative model output in

Figure 2.

Apparently, there are only local feedbacks in the model, i.e., feedbacks that do not cause a change in more than one stock, which cannot support the non-linear behaviour of the system. That alongside the presence of only positive feedback in the model, is why the final product grows without limits in

Figure 2. On a similar note, another flaw is the representation of the population as a simple accumulation process, leaving out the possibility of its decline or collapse. The model thus absolutely misses the systemic perspective and the feedback structure that would capture the reality in a more realistic way.

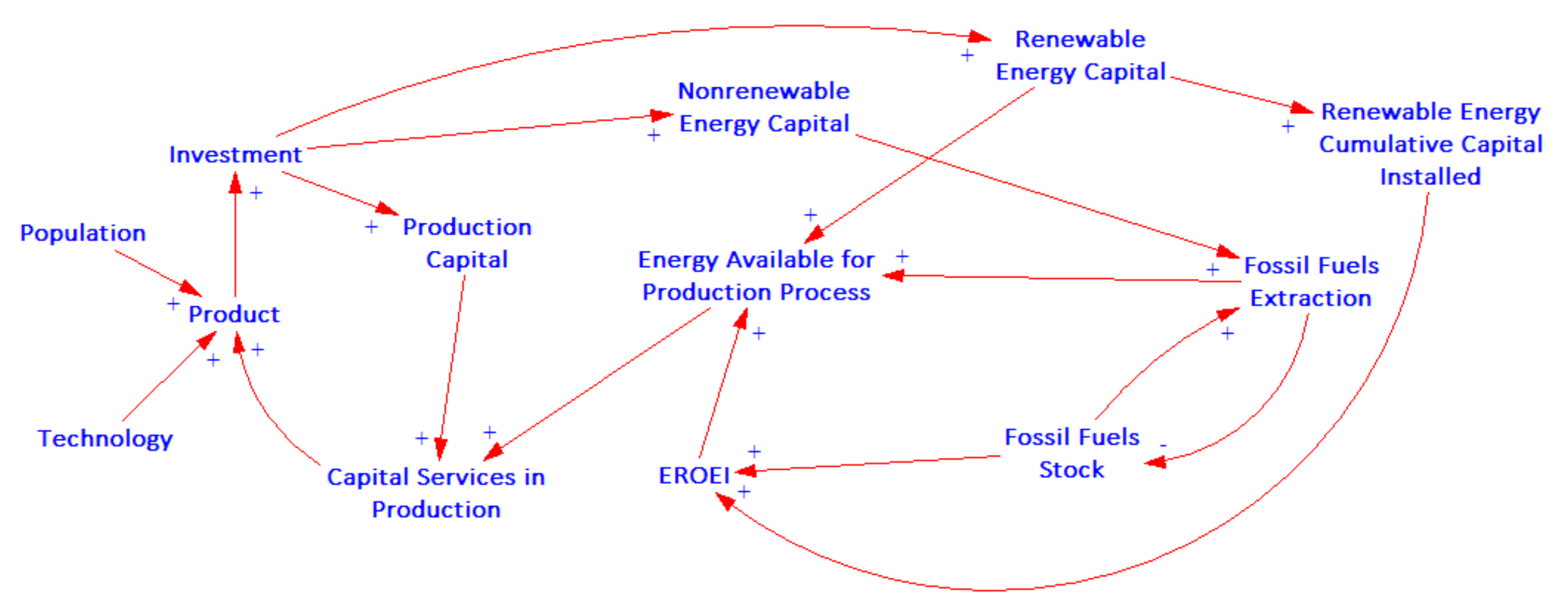

Below (

Figure 3) is a causal diagram representing the extension of the model by the energy sector.

In order to be useful in the economic production, the

Production Capital has to be supplied with

Energy available for the production process yielding capital usable in the production process or

Capital services in production. From this viewpoint, it is possible to have huge capital stock in the model, which can be increasingly useless in production in a situation of increasing energy scarcity. The equation below represents a modified Cobb–Douglas production function used by the extended version of the model, where

is the energy extracted and

is the energy required to operate the whole available capital stock:

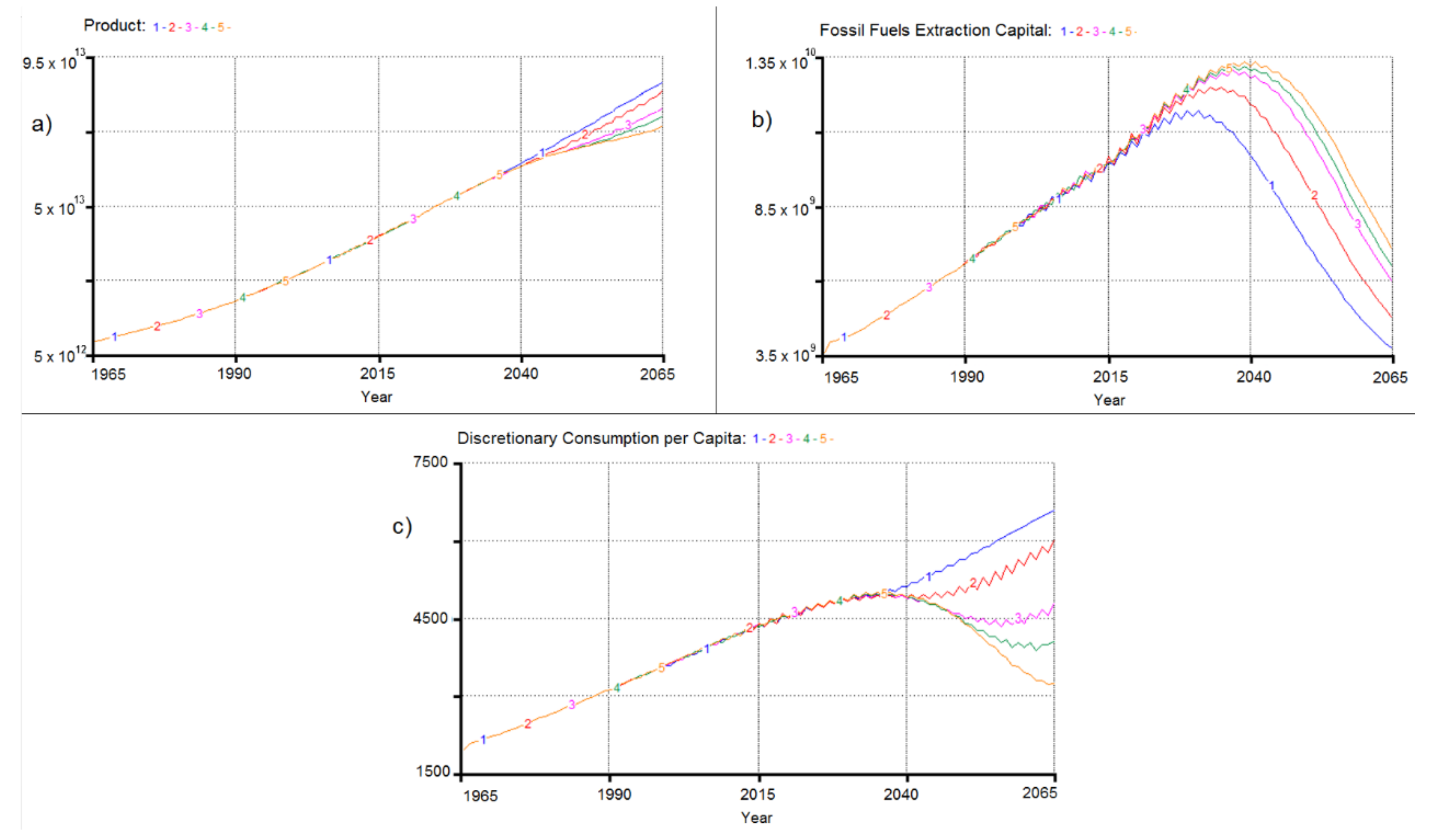

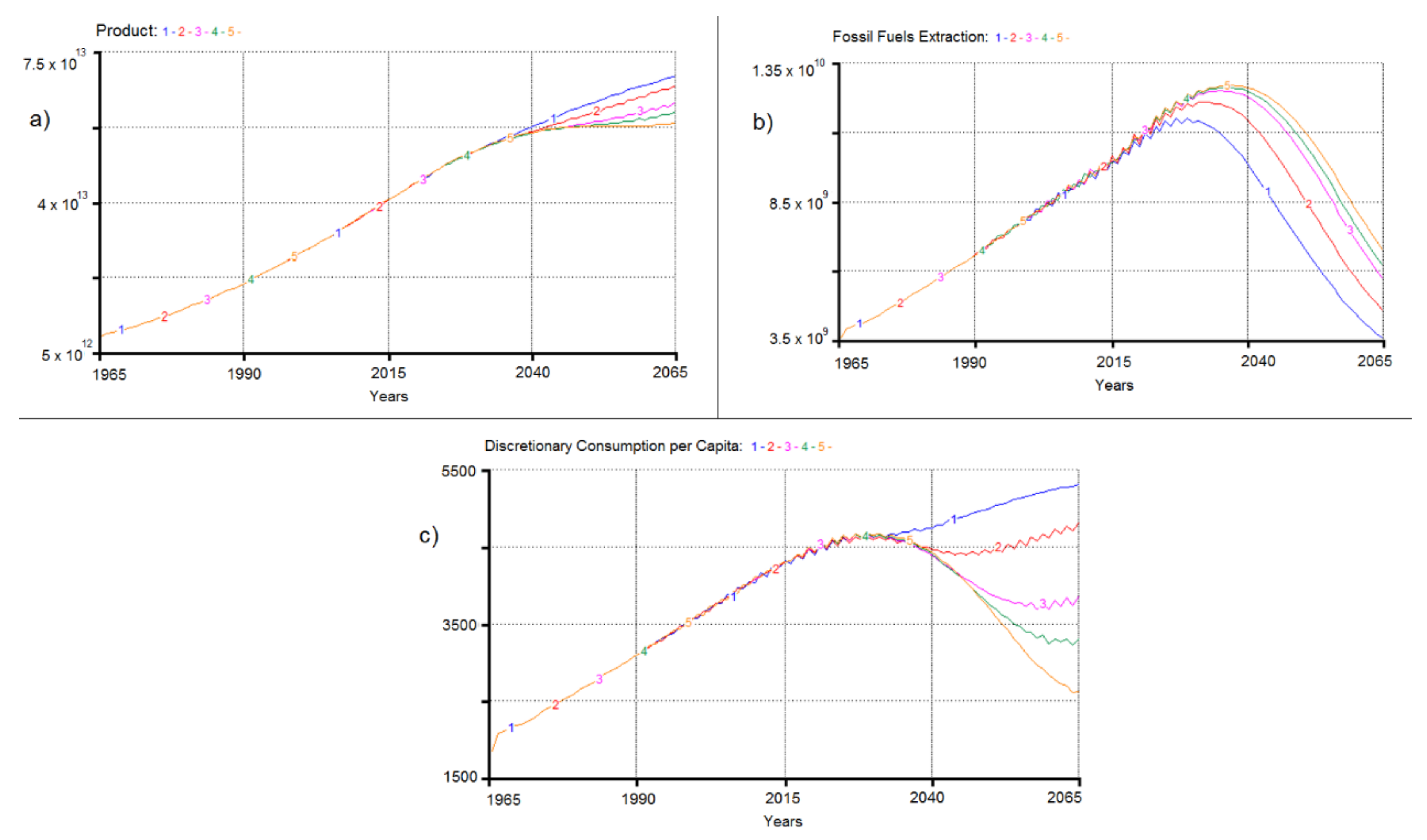

There are two other types of capital present in the model, Non-renewable energy Capital and Renewable Energy Capital. Non-renewable energy capital dominates in the model initial configuration (start year is 1950) and its increasing amount leads to a higher Fossil Fuels Extraction, which in turn supplies more Energy available for the production process. Unfortunately, Fossil Fuels Extraction leads to a reduced Fossil Fuels Stock, which in turn creates downward pressure on the Fossil Fuels Extraction and EROEI, and also imposes the total limit of energy that can be ultimately extracted. This effect introduces a negative feedback loop that can have a decisive impact on the model behaviour and output (Product). The resulting behaviour of the model can be seen as a fight for dominance between the aforementioned negative feedback loop and renewable energy loop, which in general has a reinforcing character, but Renewable Energy Capital (representing the ‘new’ renewables, Solar PV, Wind power) starts with very low EROEI values, which increase with its installed cumulative capacity. In this way, renewable resources quality determines the system performance in later periods when non-renewable energy sources are scarce.

One of the simplifying assumptions of the Solow–Swan model is that the savings rate is constant. The Ramsey–Cass–Koopmans model allows households to make optimal consumption/saving decisions as a reaction to their environment. The capital stock then reflects interactions between households supplying savings to the firms, which demands it—the savings rate is no longer constant. Households face the problem of maximizing utility subject to specific budget constraints. For this problem, economics employs the method of dynamic optimization. For simplicity, we adopt a heuristic approach instead, in which the savings rate is adjusted according to the return rate on capital, dependent on the marginal productivity of capital in production. This approach was first used by Fiddaman [

41]. The model can also be simulated with a constant savings rate.

The study rationale is based on the answer to the following question: Why should such a model not be developed and tested using standard economic tools, namely various general or partial equilibrium models? Professor Keen puts it succinctly [

49]:“…

from neither general equilibrium nor microfoundations, but from the very sound rejection of both these concepts decades ago, by almost all the intellectual disciplines that build mathematical models apart from economics. In the mid-20th century, other modelling disciplines developed the concept of “complex systems”, along with the mathematical and computing techniques needed to handle them. These developments led them to the realisation that these systems were normally never in equilibrium—but they were nonetheless general models of their relevant fields. …Economics needs to embrace the reality that, even more so than the weather, the economy is a complex system, and it is never in equilibrium”.

The applied model is implemented in the software Stella, version 9.1.3 (ISEE Systems Inc., Lebanon, NH, USA). The representation of the model regarding system dynamics is associated with a few basic components, or sectors, as presented in

Figure 4. Population sector, general purpose capital goods sector and the technology sector are typical and not very different from mainstream economic models. The production process sector is highly modified and includes effects of energy availability on capital usability in production and endogenous savings rate, which reflects the total capital amount employed in production and the availability of energy resources for its operation. The energy sector is composed of a renewable energy source and a non-renewable energy source. At the start of the simulation, the non-renewable energy source is cheap and plentiful; however, with the decline of its limited reserves, its price grows. The renewable energy source starts with a high price, which declines with its cumulative installed capacity. The energy capital investment redistribution mechanism (which divides investment between the two aforementioned energy sources) is also part of the energy sector.

The model consists of standard components (Population, Capital, Capital Energy Consumption, Technology, Output, and Investment) and additional components (Fossil Fuels sector, Renewable energies sector, Renewable energy sources learning curve, EROEI, and Energy Demand and Supply).

Below is a simplified stock-flow diagram of the model extension (see

Figure 5), with pricing mechanism and EROEI computation parts excluded for clarity.

Table 1 sums up the primary variables of the model. Apparently, the model is in concordance with one of the most significant principles of systems thinking, i.e., it is as endogenous as possible. Moreover, selected essential but omitted variables are introduced. It is important to understand the limitations of the model that result from these omissions.

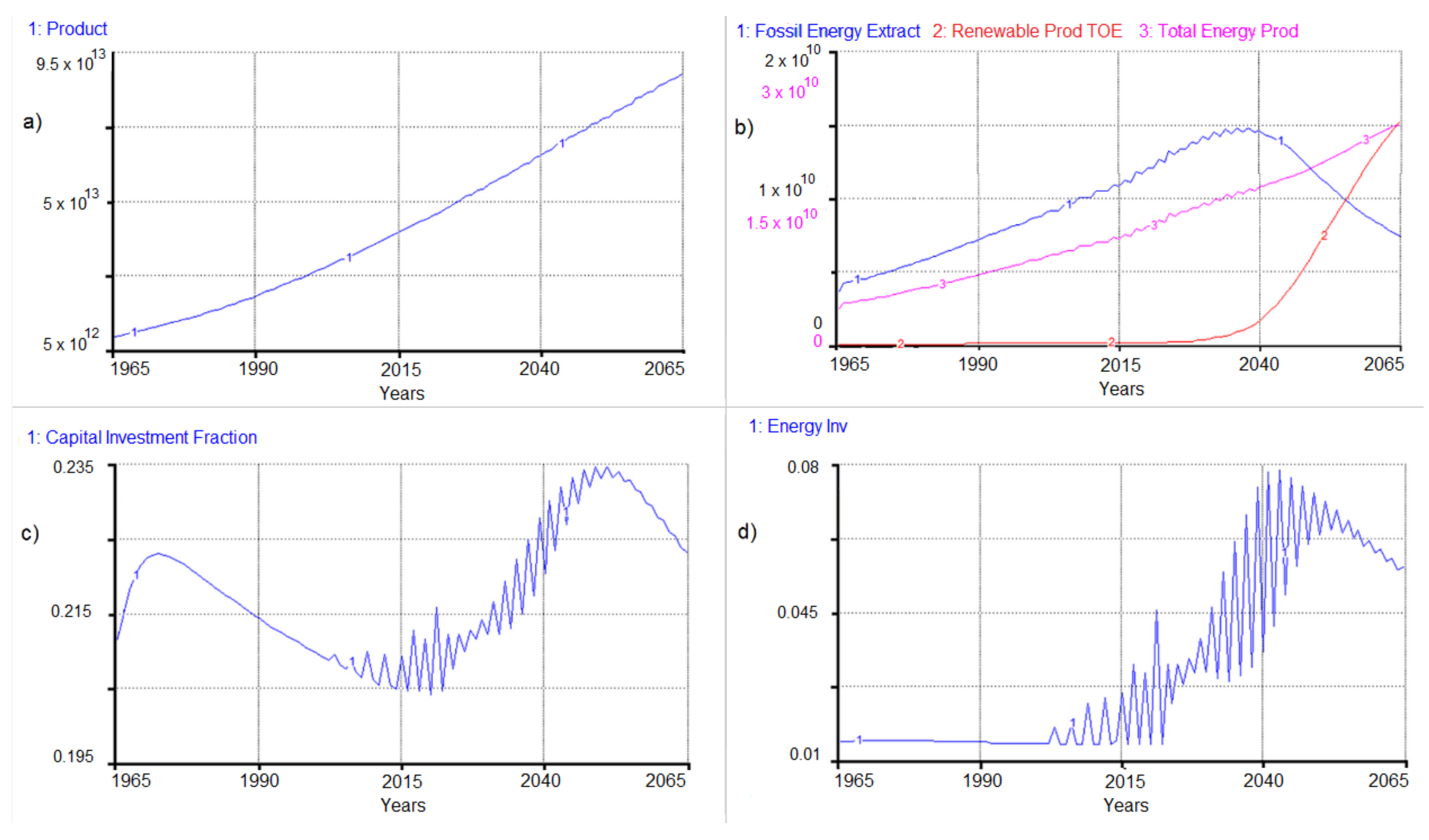

The simulation period for the model is 1965–2065. The model recreates historical behaviour over the last 50 years and then forecasts the next 50.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}