Public Administration and Landowners Facing Real Estate Cadastre Modernization: A Win-Lose or Win-Win Situation?

Abstract

:1. Introduction

2. Background

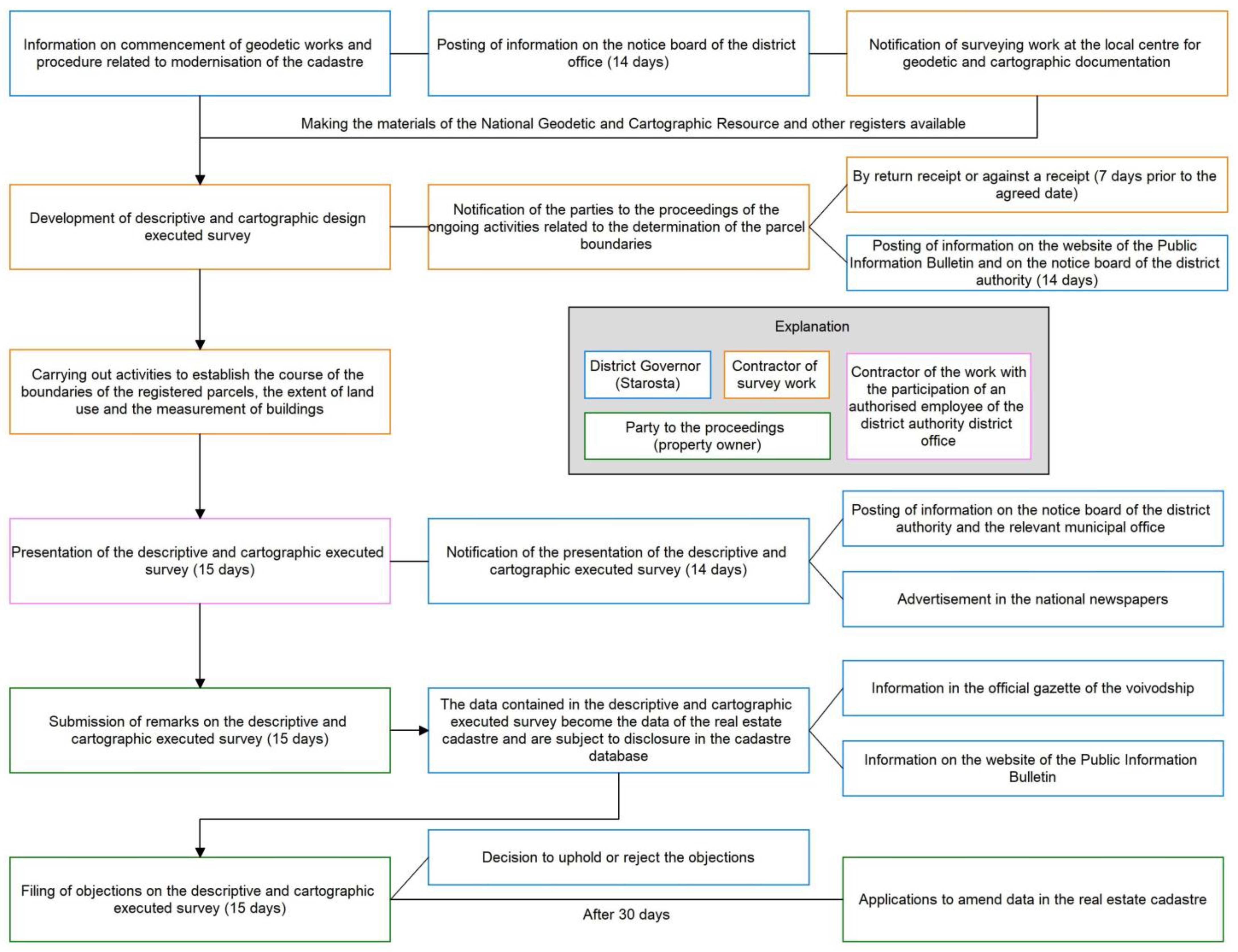

2.1. Cadastre Modernization Procedure

2.2. Cadastre System in Poland

3. Study Area, Data and Methods

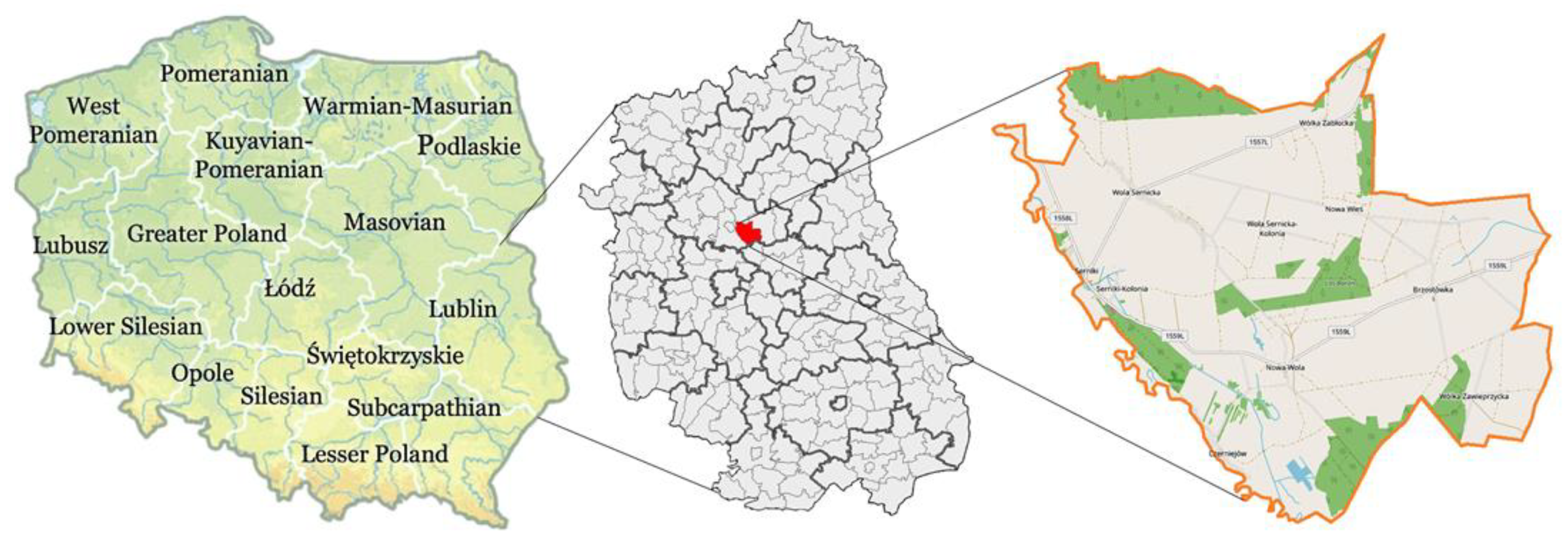

3.1. Study Area

3.2. Data: Modernization of the Cadastre in Poland—Case Study of Serniki Commune

3.3. Methods

- ▪

- Critical analysis (analysis of the literature on cadastre modernization in the world and Poland, taking into account the chronology of changes), particularly evident in the Introduction and Background sections.

- ▪

- Quantitative analysis of the geometric cadastral database. Modernization was carried out with the use of a digital orthophoto map (GSD = 0.07 m), which significantly influenced the character of changes introduced to the resource. The changes that took place during the modernization procedure of the Serniki cadastral unit are presented by comparing numerical data and their graphical presentations.

- ▪

- Analysis of changes in land use cadastral data. This is an inseparable and very important part of modernization works aimed at the creation and modification of digital data sets concerning land use and classification contours and thus revealing and modifying land use surface fields.

- ▪

- Analysis of changes in the building registration data. One of the purposes of the land and building registration modernization procedure is to acquire and complete digital spatial data sets concerning buildings and objects permanently associated with the buildings. Such activities were carried out in the course of the modernization of the Serniki cadastral unit.

- ▪

- Economic (financial) analysis of the modernization process. The procedure of modernization of the land and building registration carried out in the evidential unit of Serniki has a direct impact and introduces significant changes for the municipality. Calculations were made based on respective tax amounts, before and after modernization. The land and building registration provide the data which are the basis for the tax and benefit assessment. This undoubtedly generates significant changes regarding the calculation of agricultural, forestry, and real estate taxes, which is presented in the Results section.

- ▪

- A comparative analysis before and after modernization, especially visible in the Results and Discussion section.

4. Results

4.1. Geodetic Results as an Effect of the Real Estate Cadastre Modernization

4.2. Financial Results as an Effect of the Real Estate Cadastre Modernization

- ▪

- Agricultural tax is applied to land classified in the cadastre as agricultural land, except land used for business activity other than agricultural activity [69]. It should be emphasized here that developed agricultural land (Br) belongs to the agricultural land group, which is important in terms of the tax rate.

- ▪

- Forest tax is levied on forests classified in the register of land and buildings as forest land. The basis for taxing forest land is the area of forest, expressed in hectares, indicated by the real estate cadastre [70].

- ▪

- Real estate tax applies to ‘others’, to which ‘built-up and urbanized land’ belong. The tax base is the area indicated by the real estate cadastre [71].

4.3. Distinction of Land Use and the Tax Consequences of It for the Property Owner

- ▪

- Buildings intended for agricultural production, including barns, livestock buildings, warehouses, tanks, or yards, e.g., for agricultural machinery.

- ▪

- Buildings intended for agri-food processing, except industrial buildings for agricultural processing plants in which products are manufactured based on raw materials from outside the farm. Only when the farm carries out the full production process (raw material to produce), are there reasons to introduce Br use.

- ▪

- Residential buildings and other buildings and structures, such as garages, sheds, and yards, but only if they form an organized economic unit with the buildings described in the previous two items.

5. Discussion

- ▪

- Ongoing updates measure changes brought about by human activity, for example, the construction of new buildings. Updates of this type can be carried out as soon as the surveyor responsible has been made aware of the change. For this purpose, a reporting mechanism has been established by means of which building projects are reported to cadastral surveying before construction work commences. The costs associated with ongoing updates are covered on a user-pays basis.

- ▪

- Periodic updates measure changes that take place without human intervention, for example, a change in a forest perimeter. This type of update is required from time to time, and the associated costs are borne by the municipality.

6. Conclusions

Limitations and Future Research

Author Contributions

Funding

Conflicts of Interest

References

- Williamson, I.; Enemark, S.; Wallace, J.; Rajabifard, A. Land Administration for Sustainable Development; ESRI Press Academic: Redlands, CA, USA, 2010; ISBN 9781589480414. [Google Scholar]

- Navratil, G.; Feucht, R. An Example for a Comprehensive Quality Description The Area in the Austrian Cadastre. In Spatial Data Quality; CRC Press: Boca Raton, FL, USA, 2009; pp. 197–209. [Google Scholar]

- Maciuk, K.; Peska-Siwik, A.; El-Mowafy, A.; Borowski, L.; Apollo, M. Crustal Deformation across and beyond Central Europe and Its Impact on Land Boundaries. Resources 2021, 10, 15. [Google Scholar] [CrossRef]

- Hanus, P.; Benduch, P.; Pęska-Siwik, A.; Szewczyk, R. Three-Stage Assessment of Parcel Area Quality. Area 2020, 53, 161–174. [Google Scholar] [CrossRef]

- Enemark, S.; Bell, K.C.; Lemmen, C.; McLaren, R. Fit-for-Purpose Land Administration; International Federation of Surveyors: Frederiksberg, Denmark, 2014. [Google Scholar]

- Polat, Z.A. Evolution and Future Trends in Global Research on Cadastre: A Bibliometric Analysis. GeoJournal 2019, 84, 1121–1134. [Google Scholar] [CrossRef]

- Habib, M. Developing a Sustainability Strategy for Multipurpose Cadastre in Post-Conflict Syria. Land Use Policy 2020, 97, 104782. [Google Scholar] [CrossRef]

- Lisec, A.; Navratil, G. The Austrian Land Cadastre: From the Earliest Beginnings to the Modern Land Information System. Geod. Vestn. 2014, 58, 482–516. [Google Scholar] [CrossRef]

- Alemie, B.K.; Bennett, R.M.; Zevenbergen, J. Evolving Urban Cadastres in Ethiopia: The Impacts on Urban Land Governance. Land Use Policy 2015, 42, 695–705. [Google Scholar] [CrossRef]

- dos Santos, J.C.; de Farias, E.S.; Carneiro, A.F.T. Analysis of the Parcel as a Land Unity of the Brazilian Urban Cadastre. Bol. Ciências Geodésicas 2013, 19, 574–587. [Google Scholar] [CrossRef] [Green Version]

- Akińcza, M.; Bieda, A.; Buśko, M.; Hannibal, H.; Hanus, P.; Hycner, R.; Krzyżek, R.; Kwartnik-Pruc, A.; Łuczyński, R.; Przewięźlikowska, A. Aktualne Problemy Katastru w Polsce; Oficyna Wydawnicza Politechniki Warszawskiej: Warszawa, Poland, 2015. [Google Scholar]

- Wójcik-Leń, J.; Maciąg, K.; Maciąg, M.; Moskal, A.; Moskal, K.; Leń, P. Analysis of the Implementation of Land Consolidation and Exchange in the Villages of the Leżajsk District. Geomat. Landmanagement Landsc. 2022, 1, 7–24. [Google Scholar] [CrossRef]

- Cashin, S.M.; McGrath, G. Establishing a Modern Cadastral System within a Transition Country: Consequences for the Republic of Moldova. Land Use Policy 2006, 23, 629–642. [Google Scholar] [CrossRef]

- Taratula, R. Land Cadastral Systems Application during the Agricultural Land Use. Motrol. Comm. Mot. Energ. Agric. 2017, 1, 71–77. [Google Scholar]

- Gürsoy Sürmeneli, H.; Alkan, M. Towards Standardisation of Turkish Cadastral System Using LADM with 3D Cadastre. Surv. Rev. 2021, 53, 543–558. [Google Scholar] [CrossRef]

- Apollo, M.; Jakubiak, M.; Nistor, S.; Lewinska, P.; Krawczyk, A.; Borowski, L.; Specht, M.; Krzykowska-Piotrowska, K.; Marchel, Ł.; Pęska-Siwik, A.; et al. Geodata in Science—A Review of Selected Scientific Fields. Acta Sci. Pol. Form. Circumiectus 2023, 22, 1–30. [Google Scholar]

- Ercan, O. Evolution of the Cadastre Renewal Understanding in Türkiye: A Fit-for-Purpose Renewal Model Proposal. Land Use Policy 2023, 131, 106755. [Google Scholar] [CrossRef]

- Aien, A.; Rajabifard, A.; Kalantari, M.; Shojaei, D. Integrating Legal and Physical Dimensions of Urban Environments. ISPRS Int. J. Geo-Inf. 2015, 4, 1442–1479. [Google Scholar] [CrossRef] [Green Version]

- Buśko, M.; Meusz, A. Current Status of Real Estate Cadastre in Poland with Reference to Historical Conditions of Different Regions of the Country. In Proceedings of the 9th International Conference on Environmental Engineering, ICEE 2014, Vilnius, Lithuania, 2–23 May 2014. [Google Scholar]

- Demir, O.; Uzun, B.; Çoruhlu, Y.E. Progress of Cost Recovery on Cadastre Based on Land Management Implementation in Turkey. Surv. Rev. 2015, 47, 36–48. [Google Scholar] [CrossRef]

- Mourafetis, G.; Apostolopoulos, K.; Potsiou, C.; Ioannidis, C. Enhancing Cadastral Surveys by Facilitating the Participation of Owners. Surv. Rev. 2015, 47, 316–324. [Google Scholar] [CrossRef]

- SkaloŠ, J.; Molnárová, K.; Kottová, P. Land Reforms Reflected in the Farming Landscape in East Bohemia and in Southern Sweden-Two Faces of Modernisation. Appl. Geogr. 2012, 35, 114–123. [Google Scholar] [CrossRef]

- Dawidowicz, A.; Źróbek, R. A Methodological Evaluation of the Polish Cadastral System Based on the Global Cadastral Model. Land Use Policy 2018, 73, 59–72. [Google Scholar] [CrossRef]

- Ali, A.; Imran, M. National Spatial Data Infrastructure vs. Cadastre System for Economic Development: Evidence from Pakistan. Land 2021, 10, 188. [Google Scholar] [CrossRef]

- Fuchs, R.; Verburg, P.H.; Clevers, J.G.P.W.; Herold, M. The Potential of Old Maps and Encyclopaedias for Reconstructing Historic European Land Cover/Use Change. Appl. Geogr. 2015, 59, 43–55. [Google Scholar] [CrossRef] [Green Version]

- Gopikrishnan, T.; Ramakrishnan, S. Projection Analysis for Cadastral Mapping. Bol. Ciências Geodésicas 2013, 19, 729–745. [Google Scholar] [CrossRef] [Green Version]

- Harvey, F. The Power of Mapping: Considering Discrepancies of Polish Cadastral Mapping. Ann. Assoc. Am. Geogr. 2013, 103, 824–843. [Google Scholar] [CrossRef]

- Hendrych, J.; Storm, V.; Pacini, N. The Value of an 1827 Cadastre Map in the Rehabilitation of Ecosystem Services in the Křemže Basin, Czech Republic. Landsc. Res. 2013, 38, 750–767. [Google Scholar] [CrossRef]

- Banasik, P.; Borowski, Ł. Georeferencing the Cadastral Map of the Krakow Region. Cartogr. J. 2022, 58, 329–340. [Google Scholar] [CrossRef]

- Bacior, S. Austrian Cadastre Still in Use—Example Proceedings to Determine the Legal Status of Land Property in Southern Poland. Land Use Policy 2023, 131, 106740. [Google Scholar] [CrossRef]

- Döner, F. Evaluation of Cadastre Renovation Studies in Turkey. Surv. Rev. 2015, 47, 141–152. [Google Scholar] [CrossRef]

- Lin, Q.; Kalantari, M.; Rajabifard, A.; Li, J. A Path Dependence Perspective on the Chinese Cadastral System. Land Use Policy 2015, 45, 8–17. [Google Scholar] [CrossRef]

- Bennett, R.M.; Alemie, B.K. Fit-for-Purpose Land Administration: Lessons from Urban and Rural Ethiopia. Surv. Rev. 2016, 48, 11–20. [Google Scholar] [CrossRef] [Green Version]

- Hanus, P.; Pęska-Siwik, A.; Szewczyk, R. Spatial Analysis of the Accuracy of the Cadastral Parcel Boundaries. Comput. Electron. Agric. 2018, 144, 9–15. [Google Scholar] [CrossRef]

- Dawidowicz, A.; Źróbek, R. Analysis of Concepts of Cadastral System Technological Development. In Proceedings of the 9th International Conference on Environmental Engineering, ICEE 2014, Vilnius, Lithuania, 2–23 May 2014. [Google Scholar]

- Ho, S.; Rajabifard, A.; Stoter, J.; Kalantari, M. Legal Barriers to 3D Cadastre Implementation: What Is the Issue? Land Use Policy 2013, 35, 379–387. [Google Scholar] [CrossRef] [Green Version]

- Ho, S.; Rajabifard, A.; Kalantari, M. “Invisible” Constraints on 3D Innovation in Land Administration: A Case Study on the City of Melbourne. Land Use Policy 2015, 42, 412–425. [Google Scholar] [CrossRef]

- Hajji, R.; Yaagoubi, R.; Meliana, I.; Laafou, I.; Gholabzouri, A. El Development of an Integrated BIM-3D GIS Approach for 3D Cadastre in Morocco. ISPRS Int. J. Geo-Inf. 2021, 10, 351. [Google Scholar] [CrossRef]

- Roić, M.; Križanović, J.; Pivac, D. An Approach to Resolve Inconsistencies of Data in the Cadastre. Land 2021, 10, 70. [Google Scholar] [CrossRef]

- Stoter, J.; Ploeger, H.; Roes, R.; Van Der Riet, E.; Biljecki, F.; Ledoux, H.; Kok, D.; Kim, S. Registration of Multi-Level Property Rights in 3d in the Netherlands: Two Cases and next Steps in Further Implementation. ISPRS Int. J. Geo-Inf. 2017, 6, 158. [Google Scholar] [CrossRef] [Green Version]

- Bird, R.M.; Slack, E. Land and Property Taxation in 25 Countries: A Comparative Review. In International Handbook of Land and Property Taxation; Edward Elgar Publishing: Cheltenham, UK, 2004; pp. 19–56. ISBN 1843766477. [Google Scholar]

- Pavlii, A.S. Analysis of the System of Land Taxation in Ukraine. Scientific Messenger of International Humanities University: Collection of Scientific Projects. Econ. Manag. 2015, 14, 262–267. [Google Scholar]

- Nizalov, D.; Ivinska, K.; Kubakh, S. Monitoring of Land Relations in Ukraine in 2014–2015; Yearbook 2014–2015; LandLinks: Kyiv, Ukraine, 2015. [Google Scholar]

- Act of May 17, 1989 Geodetic and Cartographic Law (Dz. U. z 2020 r. Poz. 276 z Późn. Zm.); Ministry of National Defence: Warsaw, Poland, 1989.

- Regulation of the Minister of Regional Development and Construction of March 29, 2001 on Land and Building Records (Dz. U. z 2019 r. Poz. 393 z Poźn. Zm.); Ministry of Development, Labor and Technology: Warsaw, Poland, 2021.

- Sansoni, M.; Bonazzi, E.; Goralczyk, M.; Stauvermann, P.J.R. How to Support Regional Policies towards Sustainable Development. Sustain. Dev. 2010, 18, 202–210. [Google Scholar] [CrossRef]

- Williamson, I.P. Land Administration “Best Practice” Providing the Infrastructure for Land Policy Implementation. Land Use Policy. 2001, 18, 297–307. [Google Scholar] [CrossRef] [Green Version]

- Mika, M. Modernisation of the Cadastre in Poland as a Tool to Improve the Land Management and Administration Process. Surv. Rev. 2020, 52, 224–234. [Google Scholar] [CrossRef]

- Mika, M. An Analysis of Possibilities for the Establishment of a Multipurpose and Multidimensional Cadastre in Poland. Land Use Policy 2018, 77, 446–453. [Google Scholar] [CrossRef]

- Mjøs, L.B. Cadastral Development in Norway: The Need for Improvement. Surv. Rev. 2020, 52, 473–484. [Google Scholar] [CrossRef]

- Brown, G.; Raymond, C.M. Methods for Identifying Land Use Conflict Potential Using Participatory Mapping. Landsc. Urban Plan. 2014, 122, 196–208. [Google Scholar] [CrossRef]

- Kanianska, R.; Kizeková, M.; Nováček, J.; Zeman, M. Land-Use and Land-Cover Changes in Rural Areas during Different Political Systems: A Case Study of Slovakia from 1782 to 2006. Land Use Policy 2014, 36, 554–566. [Google Scholar] [CrossRef]

- Dizdaroglu, D. The Role of Indicator-Based Sustainability Assessment in Policy and the Decision-Making Process: A Review and Outlook. Sustainability 2017, 9, 1018. [Google Scholar] [CrossRef] [Green Version]

- Ceccarelli, T.; Bajocco, S.; Perini, L.L.; Salvati, L. Urbanisation and Land Take of High Quality Agricultural Soils-Exploring Long-Term Land Use Changes and Land Capability in Northern Italy. Int. J. Environ. Res. 2014, 8, 181–192. [Google Scholar] [CrossRef]

- Noszczyk, T.; Hernik, J. Modernization of the Land and Property Register. Acta Sci. Pol. Form. Circumiectus 2016, 15, 3–17. [Google Scholar] [CrossRef]

- Kovalyshyn, O.; Buśko, M. Land-Use Structure–Analysis on Example of Rural and Urban Communes in Poland and Ukraine. Geomat. Environ. Eng. 2018, 12, 59. [Google Scholar] [CrossRef]

- Taratula, R.; Stupen, N. Land resources management in ukraine under the conditions of the local government reforming. Sci. Pap. Manag. Econ. Eng. Agric. Rural Dev. 2018, 18, 375–381. [Google Scholar]

- NIK. Cyfryzacja Ewidencji Gruntów i Budynków Na Szczeblu Powiatowym. 2022. Available online: https://www.nik.gov.pl/kontrole/P/21/032 (accessed on 1 April 2023).

- Mika, M.; Kotlarz, P.; Jurkiewicz, M. Strategy for Cadastre Development in Poland in 1989–2019. Surv. Rev. 2020, 52, 555–563. [Google Scholar] [CrossRef]

- Buśko, M. Updated Land Use in the Modernization of the Cadastre-Analysis of the Surveying and Legal Procedures and the Financial Consequences. In Proceedings of the 10th International Conference on Environmental Engineering, ICEE 2017, Kos Island, Greece, 5–7 September 2007. [Google Scholar]

- Zyga, J. Evaluation of usefulness of real estate data contained in the register of prices and values of real estates. Infrastrukt. I Ekol. Teren. Wiej. Infrastruct. Ecol. Rural Areas 2017, III, 1017–1030. [Google Scholar]

- Busko, M.; Wysocki, P. Evaluation of the Effectiveness of Methods for Delimitation of the Boundaries of Registered Parcels in the Process of Modernization of Land and Building Registration. In Proceedings of the Proceedings-2018 Baltic Geodetic Congress, BGC-Geomatics, Olsztyn, Poland, 21–23 June 2018; pp. 186–190. [Google Scholar]

- Klimach, A.; Dawidowicz, A.; Dudzińska, M.; Źróbek, R. An Evaluation of the Informative Usefulness of the Land Administration System for the Agricultural Land Sales Control System in Poland. J. Spat. Sci. 2020, 65, 419–443. [Google Scholar] [CrossRef]

- DIRECTIVE. Infrastructure for Spatial Information in the European Community (INSPIRE); The European Parliament and of the Council: Strasbourg, France, 2007. [Google Scholar]

- Gus Local Data BANK. Available online: https://bdl.stat.gov.pl/BDL/start (accessed on 1 April 2023).

- Land and Buildings Modernization Survey. In Land and Buildings Modernization Survey of the Serniki Registration Unit-P.0608.2020.305; Available for Review on 16 June 2021; Starosta: Serniki, Poland, 2021.

- Mierzwa, W. Problemy Modernizacji Ewidencji Gruntów Na Terenach Byłego Katastru Austriackiego. Geodezja 2002, 8, 323–330. [Google Scholar]

- Buśko, M. Intended Use of a Building in Terms of Updating the Cadastral Database and Harmonizing the Data with Other Public Records. Rep. Geod. Geoinformatics 2017, 103, 78–93. [Google Scholar] [CrossRef] [Green Version]

- Act of November 15, 1984 on Agricultural Tax (Dz.U. z 2020 r. Poz. 333); Marshal of the Sejm of the Republic of Poland: Warsaw, Poland, 1984.

- Act of 30 October 2002 on Forest Tax (Dz. U. z 2019 r. Poz. 888); Marshal of the Sejm of the Republic of Poland: Warsaw, Poland, 2002.

- Act of January 12, 1991 on Local Taxes and Fees (Dz. U. z 2019r. Poz. 1170); Marshal of the Sejm of the Republic of Poland: Warsaw, Poland, 1991.

- Regulation of the Minister of Finance of December 10, 2001 on Including Communes and Cities in One of the Four Tax Districts (Dz.U. z 2001 r. Nr 143 Poz. 1614); Minister of Finance: Warsaw, Poland, 2001.

- Resolution No. XV/76/2015 of the Serniki Commune Council of November 26, 2015 on the Introduction of Real Estate Tax Exemptions in the Serniki Commune; Serniki Commune Council: Serniki, Poland, 2015.

- Resolution No. XXVI/168/2016 of the Serniki Commune Council of November 9, 2016 on the Determination of the Real Estate Tax Rates Applicable in the Serniki Commune; Serniki Commune Council: Serniki, Poland, 2016.

- Mivšek, E.; Ravnihar, F.; Žnidaršič, H. Land Cadastre Plan Making. Geod. Vestn. 2012, 56, 691–697. [Google Scholar] [CrossRef]

- Szafranska, B.; Busko, M.; Kovalyshyn, O.; Kolodiy, P. Building a Spatial Information System to Support the Development of Agriculture in Poland and Ukraine. Agronomy 2020, 10, 1884. [Google Scholar] [CrossRef]

- Sladić, D.; Radulović, A.; Govedarica, M. Development of Process Model for Serbian Cadastre. Land Use Policy 2020, 98, 104273. [Google Scholar] [CrossRef]

- Busko, M.; Szafranska, B. Analysis of Changes in Land Use Patterns Pursuant to the Conversion of Agricultural Land to Non-Agricultural Use in the Context of the Sustainable Development of the Malopolska Region. Sustainability 2018, 10, 136. [Google Scholar] [CrossRef] [Green Version]

- Lanau, M.; Liu, G. Developing an Urban Resource Cadaster for Circular Economy: A Case of Odense, Denmark. Environ. Sci. Technol. 2020, 54, 4675–4685. [Google Scholar] [CrossRef]

- Olfat, H.; Atazadeh, B.; Rajabifard, A.; Mesbah, A.; Badiee, F.; Chen, Y.; Shojaei, D.; Briffa, M. Moving towards a Single Smart Cadastral Platform in Victoria, Australia. ISPRS Int. J. Geo-Inf. 2020, 9, 303. [Google Scholar] [CrossRef]

- Bielska, A.; Wendland, A.; Delnicki, M. Possibilities for the Development of Building Plots with an Unfavorable Structure in the Context of Spatial Justice: A Case Study of Poland. Sustainability 2020, 12, 2472. [Google Scholar] [CrossRef] [Green Version]

- Bielska, A.; Stańczuk-Gałwiaczek, M.; Sobolewska-Mikulska, K.; Mroczkowski, R. Implementation of the Smart Village Concept Based on Selected Spatial Patterns—A Case Study of Mazowieckie Voivodeship in Poland. Land Use Policy 2021, 104, 105366. [Google Scholar] [CrossRef]

- Kaufmann, J.; Steudler, D. Cadastre 2014. A Vision for a Future Cadastral System. FIG Comm. 1998, 38, 173. [Google Scholar]

- Stubkjær, E. Cadastre. Encycl. GIS 2017, 137–144. [Google Scholar] [CrossRef]

- Buśko, M.; Zyga, J.; Hudecová, Ľ.; Kyseľ, P.; Balawejder, M.; Apollo, M. Active Collection of Data in the Real Estate Cadastre in Systems with a Different Pedigree and a Different Way of Building Development: Learning from Poland and Slovakia. Sustainability 2022, 14, 5046. [Google Scholar] [CrossRef]

- Jurkiewicz, M.; Hudecová, Ľ.; Kyseľ, P.; Klapa, P.; Mika, M.; Ślusarski, M. A Comparison of Cadastre in Slovakia and Poland. Slovak J. Civ. Eng. 2023, 31, 1–9. [Google Scholar] [CrossRef]

- Václavík, T.; Rogan, J. Identifying Trends in Land Use/Land Cover Changes in the Context of Post-Socialist Transformation in Central Europe: A Case Study of the Greater Olomouc Region, Czech Republic. GIScience Remote Sens. 2009, 46, 54–76. [Google Scholar] [CrossRef] [Green Version]

- Diogo, V.; Koomen, E.; Kuhlman, T. An Economic Theory-Based Explanatory Model of Agricultural Land-Use Patterns: The Netherlands as a Case Study. Agric. Syst. 2015, 139, 1–16. [Google Scholar] [CrossRef]

- SCS. The Swiss Cadastral System: A Basis for Security and Prosperity; Swiss Cadastral System: Bern, Switzerland, 2017. [Google Scholar]

- Jiang, G.; Ma, W.; Qu, Y.; Zhang, R.; Zhou, D. How Does Sprawl Differ across Urban Built-up Land Types in China? A Spatial-Temporal Analysis of the Beijing Metropolitan Area Using Granted Land Parcel Data. Cities 2016, 58, 1–9. [Google Scholar] [CrossRef]

- Jiang, G.; He, X.; Qu, Y.; Zhang, R.; Meng, Y. Functional Evolution of Rural Housing Land: A Comparative Analysis across Four Typical Areas Representing Different Stages of Industrialization in China. Land Use Policy 2016, 57, 645–654. [Google Scholar] [CrossRef]

- Guanghui, J.; Wenqiu, M.; Deqi, W.; Dingyang, Z.; Ruijuan, Z.; Tao, Z. Identifying the Internal Structure Evolution of Urban Built-up Land Sprawl (UBLS) from a Composite Structure Perspective: A Case Study of the Beijing Metropolitan Area, China. Land Use Policy 2017, 62, 258–267. [Google Scholar] [CrossRef]

- Erba, D.A. Latin American Cadastres: Successes and Remaining Problems; Lincoln Institute of Land Policy: Cambridge, MA, USA, 2004; pp. 2–3. [Google Scholar]

- Erba, D.A.; Piumetto, M.A. Making Land Legible: Cadastres for Urban Planning and Development in Latin America; Lincoln Institute of Land Policy: Cambridge, MA, USA, 2016. [Google Scholar]

- Wójcik-Leń, J.; Leń, P.; Mika, M.; Kryszk, H.; Kotlarz, P. Studies Regarding Correct Selection of Statistical Methods for the Needs of Increasing the Efficiency of Identification of Land for Consolidation—A Case Study in Poland. Land Use Policy 2019, 87, 104064. [Google Scholar] [CrossRef]

- Kurowska, K.; Kryszk, H.; Marks-Bielska, R.; Mika, M.; Leń, P. Conversion of Agricultural and Forest Land to Other Purposes in the Context of Land Protection: Evidence from Polish Experience. Land Use Policy 2020, 95, 104614. [Google Scholar] [CrossRef]

- Mika, M.; Leń, P.; Oleniacz, G.; Kurowska, K. Study of the Effects of Applying a New Algorithm for the Comprehensive Programming of the Hierarchization of Land Consolidation and Exchange Works in Poland. Land Use Policy 2019, 88, 104182. [Google Scholar] [CrossRef]

- Vitikainen, A. An Overview of Land Consolidation in Europe. Nord. J. Surv. Real Estate Res. 2004, 1, 25–44. [Google Scholar]

- Pašakarnis, G.; Maliene, V. Towards Sustainable Rural Development in Central and Eastern Europe: Applying Land Consolidation. Land Use Policy 2010, 27, 545–549. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| 2019 | Administrative units | 10 |

| Area [km2] | 76 | |

| Population | 4934 |

| Cadastral Unit 060812_2 Serniki | |||||

|---|---|---|---|---|---|

| No. | Bounds | Information about the Bounds | |||

| Id | Name | Area [ha] | Number of Plots | Number of Registration Units | |

| 1 | 060812_2.0001 | Brzostówka | 1067 | 1593 | 602 |

| 2 | 060812_2.0002 | Czerniejów | 361 | 1055 | 235 |

| 3 | 060812_2.0003 | Nowa Wola | 1601 | 4072 | 1009 |

| 4 | 060812_2.0004 | Nowa Wieś | 332 | 719 | 296 |

| 5 | 060812_2.0005 | Wola Sernicka | 1533 | 3853 | 935 |

| 6 | 060812_2.0006 | Wola Sernicka Kolonia | 864 | 874 | 428 |

| 7 | 060812_2.0007 | Serniki Wieś | 319 | 1564 | 351 |

| 8 | 060812_2.0008 | Serniki Kolonia | 477 | 688 | 320 |

| 9 | 060812_2.0009 | Wólka Zabłocka | 465 | 685 | 264 |

| 10 | 060812_2.0010 | Wólka Zawieprzycka | 540 | 1909 | 389 |

| Total | 7559 | 17,012 | 4829 | ||

| The Area of Land Use in the Serniki Cadastral Unit (ha) | ||

|---|---|---|

| Area Group: Agricultural Land | ||

| Type of Agricultural Land (Polish Abbreviations) | Before Modernization | After Modernization |

| Arable land (R) | 266 | 4276 |

| Orchards (S) | 5 | 44 |

| Permanent meadows (Ł) | 15 | 1135 |

| Permanent pastures (Ps) | 7 | 124 |

| Built-up agricultural land (Br) | 36 | 241 |

| Land under water (Wsr) | 0 | 2 |

| Land under ditches (W) | 1 | 39 |

| Wooded and bushy land (on agricultural land) (Lzr) | 2 | 338 |

| Total | 332 | 6159 |

| The Area of Land Use in the Serniki Cadastral Unit [ha] | ||

|---|---|---|

| Area Group: Forest Land | ||

| Type of Forest Land (Polish Abbreviation) | Before Modernization | After Modernization |

| Forests (Ls) | 290 | 1072 |

| Wooded and bushy lands (Lz) | 0 | 7 |

| Total | 290 | 1079 |

| The Area of Land Use in the Serniki Cadastral Unit (ha) | |||

|---|---|---|---|

| Area Land: Built-Up and Urban Areas | |||

| Type of the Built-Up and Urban Areas (Polish Abbreviation) | Before Modernization | After Modernization | |

| Residential areas (B) | 6 | 15 | |

| Industrial areas (Ba) | 7 | 7 | |

| Other built-up areas (Bi) | 3 | 16 | |

| Undeveloped or under construction urbanized areas (Bp) | 1 | 1 | |

| Recreational and leisure areas (Bz) | 0 | 3 | |

| Mining grounds (K) | 3 | 6 | |

| Communication areas | Roads (dr) | 34 | 175 |

| Railway areas (Tk) | not present | not present | |

| Other communication areas (Ti) | not present | not present | |

| Land intended for the construction of public roads or railroads (Tp) | 0 | 0 | |

| Total | 54 | 223 | |

| Serniki Commune (Values in PLN—Polish Zloty) | |

|---|---|

| Tax district | II |

| Average rye purchase price (GUS) | 58.46 |

| Average rye purchase price (reduced due to a resolution made by the Serniki Commune Council) | 37.50 |

| Rate per 1 physical ha (agricultural tax) | 187.50 |

| Rate per 1 comparative fiscal ha * (agricultural tax) | 93.75 |

| The rate from 1 ha of forest tax | 42.7328 |

| The rate per 1 m2 of remaining land (real estate tax) | 0.47 |

| Type of Use (Polish Abbreviation) | The Area before Modernization (ha) | Amount of Tax (PLN) | Area after Modernization (ha) | Amount of Tax (PLN) |

|---|---|---|---|---|

| Built-up agricultural land (Br) 1 | 36 | 3375.00 | 241 | 22,593.75 |

| Residential areas (B) 2 | 6 | 28,200.00 | 15 | 70,500.00 |

| Forest (Ls) 3 | 290 | 12,392.51 | 1072 | 45,809.56 |

| Agricultural Tax before the Modernization Procedure (Tax Amount 93.75 PLN per Comparative Fiscal Hectare) | ||||

|---|---|---|---|---|

| Plot Number | Type of Use (ALC) | Area Size (ha) | Area Size in Comparative Fiscal Hectare (ha) | Amount of Tax (PLN) |

| 369/18 | arable land (ALC V) | 0.0070 | 0.0021 | 0.20 |

| 369/20 | arable land (ALC IVb) | 0.0012 | 0.0009 | 0.08 |

| arable land (ALC V) | 0.1800 | 0.0540 | 5.06 | |

| 794 | arable land (ALC IIIa) | 0.4000 | 0.6000 | 56.25 |

| arable land (ALC IIIb) | 0.3600 | 0.4500 | 42.19 | |

| Total | 0.9482 | 1.1070 | 103.78 | |

| Agricultural Tax before the Modernization Procedure (Tax Amount 93.75 PLN per Comparative Fiscal Hectare) | ||||

|---|---|---|---|---|

| Plot Number | Type of Use (ALC) | Area Size (ha) | Area Size in Comparative Fiscal Hectare (ha) | Amount of Tax (PLN) |

| 369/20 | arable land (ALC V) | 0.0940 | 0.0282 | 2.64 |

| 794 | arable land (ALC IIIa) | 0.4000 | 0.6000 | 56.25 |

| arable land (ALC IIIb) | 0.3600 | 0.4500 | 42.19 | |

| Property tax (Tax amount 4.70000 per ha) | ||||

| 369/18 | residential areas—B | 0.0070 | Not applicable | 32.90 |

| 369/20 | residential areas—B | 0.0872 | Not applicable | 409.84 |

| Total | 0.9482 | Not applicable | 543.82 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Busko, M.; Apollo, M. Public Administration and Landowners Facing Real Estate Cadastre Modernization: A Win-Lose or Win-Win Situation? Resources 2023, 12, 73. https://doi.org/10.3390/resources12060073

Busko M, Apollo M. Public Administration and Landowners Facing Real Estate Cadastre Modernization: A Win-Lose or Win-Win Situation? Resources. 2023; 12(6):73. https://doi.org/10.3390/resources12060073

Chicago/Turabian StyleBusko, Malgorzata, and Michal Apollo. 2023. "Public Administration and Landowners Facing Real Estate Cadastre Modernization: A Win-Lose or Win-Win Situation?" Resources 12, no. 6: 73. https://doi.org/10.3390/resources12060073

APA StyleBusko, M., & Apollo, M. (2023). Public Administration and Landowners Facing Real Estate Cadastre Modernization: A Win-Lose or Win-Win Situation? Resources, 12(6), 73. https://doi.org/10.3390/resources12060073