1. Introduction

Corporate social responsibility (CSR) has entered the political agenda of European governments. For this purpose, a series of principles and practices have been designed for its promotion and development, although the definition of CSR itself is somewhat vague and lacks consensus [

1].

According to Cuesta [

2], corporate social responsibility is a moral argument that does not have to be at odds with institutional benefits [

1]. Therefore, in our opinion, all agents have a certain responsibility, and thus it is necessary that they play their corresponding role and use their ability to affect change [

3]. Vogel [

4] argues that those companies that implement CSR actions will obtain positive outcomes for their business [

5], they will distinguish themselves from their competitors, projecting a better image and reputation [

6], and that they will also create goodwill in consumers and positive attitudes in employees [

7,

8,

9,

10]. In short, we could say that these companies will have a greater “competitive advantage” by integrating non-economic factors [

11]. CSR is an intangible resource of great international relevance, the application of which is beneficial for companies.

As indicated by Fuentes et al. [

12] it is necessary that the application instruments are disseminated and that participation is promoted. For this purpose, it is essential for companies to self-regulate whilst at the same time implement efficient and effective CSR-oriented strategies in the management of human and environmental resources. Also, the definition of CSR is complex and complicated [

13]. It is complex due to nature and context of the problems. The ecological, societal and economic systems are complex, dynamic systems which have an intimate relationship with CSR. However, it is necessary to clarify what CSR is and to clearly define the term [

14]. CSR is multifaceted in nature and involves different actors, locations and institutions. Each company and its business groups develop a CSR policy in response to social or environmental issues according to its own development process and even its own idiosyncrasies, depending on the framework of the relationship between the company and civil society. It is necessary to know the CSR agenda implemented in an organization, or if the actions of organizations are truly socially responsible [

13]. This is so others can accept the same processes and take a collaborative approach to resolving specific issues. The effort and research about CSR is perhaps relevant, however, the term is poorly understood. Now, it is fundamental to “understand and identify the specific differentia” [

13] (p. 638) in each institution in the case of Andalusia.

Andalusia (Spain), the most populated region of the country, contains 15.3% of the total companies nationwide, after Catalonia and Madrid [

15]. However, the productive fabric of Andalusia has its origins in a socio-historical situation characterized by the late onset of business development in comparison with the rest of the country, and a conservative class of landowning origin that emerged in the absence of a modern bourgeoisie [

16]. Capital investments from external sources [

17], along with a high dependency on aid and subsidies, may have favored the creation of a corporate image (and the image of the Andalusian population) that is passive and not particularly entrepreneurial. Therefore, these multiple realities have resulted in the development of a business with its own social and cultural features, an idiosyncrasy that can also be reflected in the way of understanding and assessing the components of social responsibility both globally and also within the productive sector. Sheehy (2015) mentioned the relevance of CSR idiosyncratic organizational innovation [

13].

Within this framework, the focus of our work is to address the current status of corporate social responsibility practices in terms of both human resources policy and environmental aspects. We focus our study on two basic ideas of Sheehy (2015). First, this study has determined whether or not the Andalusian organizations have characteristics and behaviors of CSR. Second, to understand the internal complexity, that is, to know better ways in which organizations can contribute to society and reduce social costs [

13]. In this regard, the general objective of this work is to determine if there is social responsibility in human and environmental resources management in certain Andalusian companies. For this, we will use the following specific objectives as references:

Objective 1. To examine if Andalusian entrepreneurs show social awareness in relation to corporate social responsibility in human and environmental resources management.

Objective 2. To explore whether there are statistically significant differences in the perception of social responsibility in the management of human and environmental resources across the different productive sectors of the community in Andalusian companies.

Objective 3. To identify the corporate social responsibility actions that are able to promote employee satisfaction.

2. Definition and Dimensions of CSR

Within this section we will firstly explain the concept of corporate social responsibility (CSR), after which we will describe the various dimensions that make up the construct.

2.1. The Concept of CSR

Corporate social responsibility is a relatively new concept, which is rapidly being implemented across all sectors [

18] due to the fact that it is extremely important for society. It has also been shown to produce considerable economic benefits, as a consequence of the greater perception of trustworthiness that is held by the public with regard to socially responsible companies [

19]. This is therefore a concept that is necessary for minimizing the negative impacts of companies on society, making it essential for employers to show a commitment towards complying with CSR measures. However, not all companies show such a social commitment [

20].

In l960, Keith Davis [

21] suggested that social responsibility is a term that, when referring to companies, is related to the decisions and measures adopted by these companies, that is, the decisions that are made by business people that go beyond economic interests or the technical workings of the company, and which instead take into account social interests.

Bowen [

22] established the first definition of social responsibility in business, with this term being understood as the “obligations of employers to follow those policies, to make those decisions, or to follow the lines of action that are desirable in terms of the objectives and values of our society” (p. 6). This led the author to identify social responsibility as a type of social awareness of business leaders who are responsible for the consequences of their actions, in a sphere that is somewhat more extensive than one that would be expected on the basis of profits and losses (p. 44).

Therefore, social responsibility could be defined as the responsibility, commitment, or obligation that members of a company have, both to themselves, and to society as a whole. It could be said that social responsibility is the commitment or obligation of the members of a society to the society as a whole. When CSR is studied in the European Union, the Green Paper [

23] is often used as a reference, and refers to a concept where the social and environmental dimensions are voluntarily integrated into both business and community development. Thus, it appears that Europe aspires to be a competitive economy with sustainable economic growth and greater social cohesion.

However, CSR should not be framed exclusively within issues of economic profitability, but should instead take into account the stability of the business itself, the organization of work, job security, or the preservation of the environment. It is therefore a question of regarding CSR as a field of study, management practices, and a practical approach towards improving the contribution of companies to society [

13].

In short, in order to ensure that a company is socially responsible, it is essential to identify relevant measurement variables and indicators in each social context [

3]. In spite of the clear importance of CSR and the proliferation of its norms and standards, the way in which it is developing is often unclear [

14]. The phenomenon of CSR began with a lack of any clear definition, and thus research on this concept is based on the description and classification of behavior, instead of focusing on the phenomenon itself, which is often fostered by the communities’ own policies.

2.2. Modalities and Dimensions of CSR

As Smith [

24] points out, a set of external forces, along with the social changes that have taken place, have contributed to the recent increase in the importance of corporate social responsibility (CSR). In particular, the author argues that the relevant social aspects include the following: (a) The increase in social expectations of companies expressed, in part, by powerful non-governmental organizations; (b) a decrease in the power and scope of the government; (c) globalization; (d) the way in which the media shapes the attainment of higher goals, driven particularly by advances in information technology; and, finally, (e) the greater diffusion of democracy.

In this regard, Carroll [

25] considers that CSR should include the following dimensions:

Economic responsibility. This refers to the notion that business organizations have been created as economic entities to provide goods and services to members of society.

Legal responsibility. The company sanctions business practices that are not only aimed at operating in accordance with the motive of gaining profit. Similarly, companies are expected to comply with laws and regulations declared by governments. In a sense, legal responsibilities reflect a vision of “codified ethics”, including the basic notions of fair operations.

Ethical responsibility. Ethical responsibility embodies norms or expectations that reflect the concerns of consumers, employees, and shareholders, as well as the view of what is considered fair within the community, or in accordance with the respect and protection of the moral rights of the various interested parties.

Philanthropic responsibility. This modality covers those corporate actions that constitute a response to the expectations of society, reflecting the fact that companies can also become good corporate citizens. In this sense, the strategies worth noting are those that include active participation in acts or programs for promoting human wellbeing or goodwill.

Melé [

26], on the other hand, points out that the evolution of the term itself makes reference to three different scenarios. The first—strictly focused on the social responsibility of the company—is linked to the economic function and social values surrounding the performance of the activity of the company. Within this section, social responsibility is considered as voluntary or almost “philanthropic” and can “contribute to the sustainability of society” (p. 82) [

11]. However, as pointed out by Porter and Kramer [

11], philanthropic social responsibility is, in most cases, analyzed in terms of economic benefits rather than those of social impact. To achieve a balance between the interests of companies and society, there is a need to be aware of how things should be carried out.

The second scenario is linked to the social sensitivity of the company, that is, there is a need for the company to respond to social demands. This approach distinguishes between several types of social demands, including social obligations (market strength), social responsibility (norms, values, and expectations) and sensitivity (anticipating the facts). The third focuses on the social performance of the company, that is, the set of principles oriented towards permanent and proactive action that aligns the interests of companies with the demands of society.

In summary, it appears that CSR has aroused great interest in companies [

27,

28]. However, there is still a considerable amount of work to be done, particularly with regard to identifying the main strategies adopted within the different sectors. In addition, as pointed out by Fuentes, Núñez, and Veroz [

12], companies should include environmental and social actions that go beyond economic interests. In this regard, CSR is based on a shift in values, with concerns about environmental deterioration, discriminatory labor practices, and human rights, among others.

3. Materials and Methods

3.1. Instrument

In this case the instrument has been designed “ad hoc”. For this, the procedure followed several steps:

Step 1. A group of researchers was commissioned to collect and analyze the existing literature on the subject. Specifically, as a preliminary step to designing the questionnaire, a bibliographic search was conducted on various secondary sources, with particular reference to the United Nations Global Pact [

29] and the Green Paper on Innovation [

30]. In addition, other sources were used, such as the Journal of Employment [

31], the conclusions of the Forum of Experts on Social Responsibility of companies of the Ministry of Labor and Social Affairs [

32], the Annual Reports of the IBEX 35 companies [

33], the International Conference of Employment [

34] and Corporate Social Responsibility: Trends in Spain [

35], all of which form part of the fundamental references in CSR research.

Step 2. A preliminary version of the questionnaire was prepared and submitted for evaluation in relation to its wording and object of study. This was carried out by means of a pre-test conducted by the research team.

Step 3. Initial assessment of the questionnaire was carried out according to the perception of the business profile (employment position of the respondent, number of workers, subsector to which National Classification of Economic Activities belongs, and legal form).

Step 4. The questionnaire was evaluated by a panel of experts, who met across several sessions to refine the content of the instrument.

Step 5. Design of the final structure of the questionnaire

Step 6. The questionnaire was then validated by a researcher responsible for conducting a series of statistical analyses to establish the internal and external validity of this tool.

As a conclusion to this process, the final instrument included a total of 64 questions, with a Likert-type response format, with values ranging from 1 “strongly agree” to 5 “strongly disagree”.

The items in this questionnaire were organized into the following dimensions: The position of the sector in reference to the economic elements (including a total of 4 questions), socio-labor (including a total of 11 questions), environmental aspects (consisting of 5 questions), psychosocial and cultural aspects (covering 30 issues), and finally, social causes and behaviors (composed of 14 questions). The results of an internal consistency analysis using Cronbach’s alpha test revealed a value of 0.532, which indicates an acceptable level of reliability [

36,

37], although its alpha value may be low due to the large number of questions, low interrelation between elements, or heterogeneous constructions [

38], which should be taken into account in similar investigations in the future.

3.2. Participants

For this work 365 managers were recruited from a range of different positions including entrepreneur (60%), specialist in economic management (22%), human resources (6%), quality management (2%) and production (8%). These positions are distributed across the following different sectors: Industrial (31%), services (25%), tourism (20%), trade (13%) and agro-livestock (10%). Regarding the number of workers per company, it is important to highlight that the majority of companies have between 10 and 50 workers (49%), followed by companies that have less than 10 workers (35%), companies that have between 50 and 250 workers (12%), whilst only 3% of the companies have more than 250 workers. With regard to gender, we found that 75% are men and the remaining 25% are women. The majority of companies (48%) show a balanced economic situation.

3.3. Procedure and Analysis

The sample consisted of a total of 365 organizations belonging to productive sectors, distributed in accordance with the proportionality indicated by the data provided by the Andalusian Council of Chambers of Commerce, Industry and Navigation. With this, a margin of error of 5% was established. The geographical scope of application was the entire region, although the presence of these sectors in some provinces or others determined the territorial application within Andalusia. The majority of productive sectors analyzed have the following proportionality: Agro-livestock (10%), industrial (31%), services (25%), commerce (14%) and tourism (20%). In detail, the surveys were conducted by productive sectors of the CNAE: CNAE Agriculture 01, 23 surveys; livestock CNAE 01, 14 surveys; wholesale trade CNAE 51, 24 surveys; CNAE retail trade 52, 26 surveys; CNAE transport 60 to 63, 26 surveys; restoration, hospitality and leisure CNAE 55, 73 surveys; community services CNAE 80 to 95, 20 surveys; services to CNAE companies 72 to 75, 30 surveys; other services CNAE 65 to 71, 15 surveys; agro-livestock industry CNAE 15, 21 surveys; metal industry CNAE 27, 17 surveys; natural stone industry CNAE 14, 13 surveys; chemical industry CNAE 24, 13 surveys; wood industry, cork, CNAE papers 20, 21 and 36, 17 surveys; auxiliary construction industry CNAE 40 to 45, 17 surveys; textile industry, 16 surveys.

The administration of the questionnaires was carried out during working hours, with participation being completely voluntary. The activity was implemented under the supervision of a researcher, who presented the objective of the work and ensured the absolute confidentiality of the results. After collecting the data, a matrix was created that was purified, after which the data were subjected to statistical analysis.

Once the data were obtained, they were purified and processed using the statistical package SPSS (version 18). Subsequently, various analyses were carried out to test the established objectives, specifically, an ANOVA followed by Tukey’s post-hoc test and linear regression analysis.

4. Results

This section is organized into two parts. The first includes the statistical analyses carried out to determine if the managerial employees belonging to the different sectors (agro-livestock, industry, services, trade, and tourism) value CSR, and if there are differences according to each sector. The second section includes the information related to CSR actions, and specifically which of these, according to the managers belonging to the different sectors, are determining factors in employee satisfaction.

4.1. Appraisal of CSR by Managers Belonging to Different Sectors

As a preliminary step, before comparing the means, we verified the assumptions of normality and homogeneity of the variance of all the items that make up the CSR questionnaire, which were then used as factors in the ANOVA. These data are listed in

Table 1, where we present only the scores of the items that yielded statistically significant differences, ordered by dimensions (see

Table 1).

The data shown in

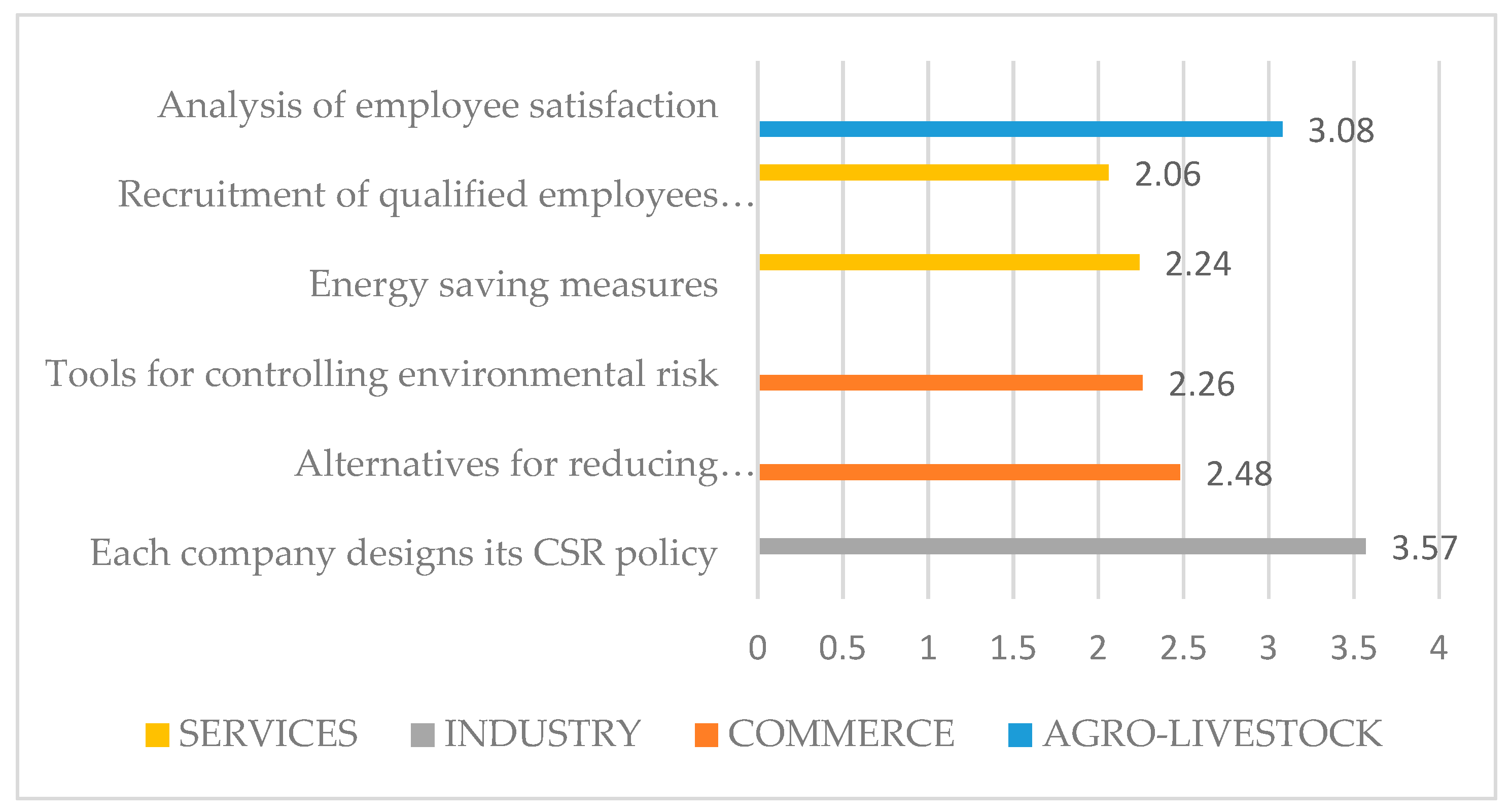

Table 1 indicate that entrepreneurs from different sectors of the Andalusian community show statistically significant differences in their understanding of the various components of CSR. To be more precise, it appears that these differences occur in the following items: Analysis of employee satisfaction (SC inter = 39.09, MC inter = 9.77, F = 7.269, significance = 000), followed by measures for saving energy consumption (SC inter = 10.131; MC inter = 2.53; F = 4.639; Sig = 0.001), environmental risk control tools (SC inter = 12.957; MC inter = 3.23; F = 3.83; significance = 0.005), alternatives for reducing environmental impact (SC inter = 6.51, MC inter = 1.62, F = 3.20, significance = 0.013), recruitment of employees trained for the position (SC inter = 8.02; MC inter = 2.00; F = 2.61; significance = 0.035), each company that designs its CSR policy (SC inter = 18.67; MC inter = 4.66; F = 2.39; significance = 0.500). In summary, on the basis of the ANOVA table, it can be concluded that in terms of the perception of employers, there are statistically significant differences in the aforementioned items.

Next, we present the average scores of each of the items for which statistically significant differences are found, distinguished by sector (see

Table 2).

If we order the average scores, we observe that in the item analysis of employee satisfaction, the highest score is obtained in the agro-livestock sector (M = 3.39, SD = 0.988). On the other hand, in the item that refers to recruiting employees trained for the position, we discovered that the highest average score emerges in the industrial sector (M = 2.14, SD = 0.949). When we refer to energy saving measures, we found that the highest score is obtained in the industrial sector (M = 2.50, SD = 0.650). In the case of environmental risk control tools, we found the highest value in the commerce sector (M = 2.42, SD = 0.857). In alternatives for reducing environmental impact, we found that the highest score is obtained in the trade sector (M = 2.54, SD = 0.647). Finally, with regard to each company designing its CSR policy, it appears that the highest score is evident in the commerce sector (M = 3.38, SD = 1.79).

Next, we were interested in determining where the differences lie for the CSR questions that show statistically significant differences (see

Figure 1).

Broadly speaking, the data indicate statistically significant differences according to sector. In particular, for the item that refers to the analysis of employee satisfaction, we found differences between the agro-livestock sector and the services sector (mean difference = 1.013, significance = 0.000), between the agro-livestock sector and trade sector (mean difference = 0.919; significance = 0.002) and, finally, between the agro-livestock sector and the tourism sector (mean difference = 0.750, significance = 0.012). We also found that the industrial sector differed significantly from the services sector (mean difference = 0.607; significance = 0.002). On the other hand, when we analyzed the item referring to the recruitment of employees qualified for the position, we found differences between the services sector and the trade sector (mean difference = −445, significance = 0.034). With regard to energy saving measures, there were statistically significant differences between the industrial and tourism sectors (mean difference = 3.53, significance = 0.014) and the services and tourism sectors (mean difference = 4.48; significance = 0.000). With regard to environmental risk control tools, sectoral differences emerged between agriculture and trade (mean difference = 0.576, significance = 0.031) and the industrial and trade sectors (mean difference = −0.534; significance = 0.006). Regarding the alternatives for reducing environmental impact, we found differences between the services and trade sectors (mean difference = −358, significance = 038). Finally, in the question related to whether each company designs its own CSR policy, we found differences between the industrial and agro-livestock sectors (mean difference = −777, significance = 0.026).

In summary, throughout this study we have revealed the interest shown by the various Andalusian sectors in terms of corporate social responsibility from the perspective of managerial employees. In addition, the data generally indicate differences between the various sectors involved (agro-livestock, tourism, trade, services, and industry). In general, it appears that the agro-livestock sector is more interested in the analysis of employee satisfaction, whilst the trade sector focuses more on attracting employees qualified for the position, and having tools for controlling environmental risks along with alternatives for reducing environmental impact. Further, the services sector is primarily concerned with energy saving measures whilst the industrial sector appears to be associated with each company designing its own CSR policy.

4.2. CSR Actions that Determine the Satisfaction of Employees According to the Perception of Managers

Within this section we will analyze, by sector, what managers perceive to be the CSR actions that determine employee satisfaction. To do this, we conducted a linear regression analysis in successive steps (see

Table 3). The dependent variable is employee satisfaction and the independent variables are other terms about CSR (recruitment, tools for controlling, corruption practices, talent for corporate social innovation and no options to go beyond management). The general statistical results are quadratic mean = 2.43, df = 41, F = 1.76, corrected square R = 0.081; significance = 0.004. Thus, the data show that the managers of the different Andalusian sectors understand that their employees will be satisfied with the measures of corporate social responsibility when companies recruit employees trained for their job (beta = 0.178; significance = 023); use tools for controlling environmental risk (beta = 0.194; significance = 010); apply corruption practices to obtain greater benefits (beta = 0.118; significance = 008); and there are no options to go beyond management (beta = 0.119; significance = 022). With statistically significant scores (but with negative values) we find that companies have talent for corporate social innovation (beta = −0.134; significance = 048) (see

Table 3).

In summary, the data seem to indicate that Andalusian managers consider that there are certain basic corporate social responsibility actions to achieve employee satisfaction, with particular importance being given to the use of tools that allow for controlling environmental risks.

5. Discussion

Throughout this work we aimed to identify the predisposition of managers to take actions related to CSR in Andalusian companies belonging to different sectors. As pointed out by Aguilera and Puerto [

39] (p. 3), “Corporate social responsibility offers a new alternative to “compete”, which is conceived as the transfer of added value to society”. It seems, then, that socially responsible companies show business growth.

Broadly speaking, the data indicate the importance that is assigned to CSR throughout the business community. One practical consequence of this work is that it provides helpful knowledge regarding the perception of corporate social responsibility in the different sectors of the autonomous community of Andalusia. Therefore, we understand that this study contributes to society by offering intervention guidelines on CSR. Likewise, this research sets a precedent in our community, which is evidenced by the lack of previous existing studies on this subject.

Regarding our first specific objective related to social conscience, we particularly sought to examine whether there is social awareness of Andalusian entrepreneurs in relation to corporate social responsibility in human and environmental resources management, and the data collected here seem to indicate the existence of such an awareness. These results are supported by the report issued by the AECA [

40], according to which companies have voluntary commitments to society. In particular, and as indicated by the data, we observed that the psychosocial and cultural dimensions were those most valued.

With regard to the second objective, where we were interested in exploring whether there are statistically significant sectoral differences in the perception of social responsibility in Andalusian business workers in human resources and environmental management, the data indicate clear differences according to sector. More precisely, it should be pointed out that the agro-livestock sector is more interested in the analysis of employee satisfaction, whilst the trade sector focuses more on attracting employees trained for the position, tools for controlling environmental risks, and alternatives for reducing environmental impact. Moreover, the services sector is mainly concerned with energy saving measures and the industrial sector seems to be more interested in the idea of each company designing its own CSR policy.

These data are consistent with the suggestions of Munuera and Rodríguez [

41], who argue that the success of a business is associated with the institution adopting a multiple perspective that allows for reconciling the divergences and conflicts of interests between the different objectives of the participants of a group. Likewise, we understand that our work represents a great step forward in relation to the study described by Castellanos, Martín and Caro [

27], since we have identified the factors that motivate Andalusian business workers to take CSR actions. In a certain sense, this study offers the key to identifying the future approaches that organizations must adopt in order to show socially responsible behavior.

Finally, in terms of the third objective, which was concerned with establishing the perception held by managers in relation to the corporate social responsibility actions that generate employee satisfaction, we discovered that there are specific actions that are highly valued by employers as determinants of employee satisfaction. Of particular importance is the use of tools that allow for the control of environmental risks. This idea is reinforced by the approaches of Porter and Kramer [

11], who point out that measures (internal and external) are necessary to achieve a balance between the interests of companies and environmental interests.

This work presents relevant contributions related to CSR in Andalusia. However, this study has some limitations that we would like to mention. In this research the first limitation is methodological, as we used a quantitative methodology, and it is also necessary to perform qualitative research [

13]. This work is a cross-sectional study, we consider that to know more about CSR in the Andalusia organizations in detail, it would be advisable to carry out longitudinal studies.

The main practical implication that we would like to highlight lies in demonstrating that the general dimensions used as indicators of CSR in the European community (see United Nations Global Pact [

29], and the European Commission Green Paper [

30], from which the questionnaire used in this study was constructed), are not of a universal nature, that is, it seems that they are generally not valid for all sectors, particularly in Andalusia. This argument is reinforced by the existence of statistically significant differences in the item related to each company designing its CSR policy. With this diagnosis, we could argue that if the objective is to promote CSR in companies, it is necessary to apply an idiosyncratic plan, that is, a plan adapted to each sector. Therefore, this work offers valid guidelines that indicate how action plans could be followed in the Andalusian community. In our opinion, this is essential to ensure the success of the company. Further, following the suggestions offered by Donaldson and Preston [

42], it is essential to achieve the balance between the different agents that contribute to the wellbeing of the company. In short, we can highlight the importance of taking into account the idiosyncrasy of the productive sector when promoting action plans to ensure the application of CSR. This idea finds its theoretical sustenance in the postulates offered by Wang et al. [

43], who, on the basis of their findings, emphasize that a CSR education program should be designed accordingly and, in addition, be adapted to different personal characteristics. This implies the need to design CSR programs “in company”.

Despite the relevance that this work seems to have for the scientific community, it presents further limitations. First, it is appropriate to point out the small number of existing studies, which made the design and development of our study difficult. In addition, we must add that recent studies were based on the education sector [

43,

44]. Second, it is important to note the unique time of application of the data, which could affect the results. Third, the geographical area used, could, in our opinion, be an important determinant of the findings obtained in the different sectors. We therefore believe that more studies are needed to address the aforementioned limitations. In this sense, we consider that more work is necessary to determine if these findings are affected by the territory or, if conversely, the results are directly linked to the profile or sector of the companies. Similarly, we believe that it would be advisable to extend the temporal and spatial scope of this research, including different times of application of the instruments whilst also covering different geographical areas or other productive sectors.

In the same vein, as a future perspective

, it would be of interest to analyze social intelligence to develop competencies associated with corporate social responsibility [

45]. This issue is, therefore, concerned with the development of institutional competencies, adapted to the specific context, to ensure the maximum effectiveness of corporate social responsibility actions. By acting in this way, that is, by designing an adapted CSR plan, we offer certain guarantees that the company would retain both its external and internal clients [

44].

Further, from a future perspective we highlight the postulates established by Post et al. [

46], who emphasize the need to build long-term relationships with the different actors involved in the companies. In this sense, the greatest challenge seems to lie in the development, maintenance, and integration of favorable relationships with the different actors with whom the companies interact, with the role played by employees being of particular relevance. Therefore, we encourage members of the scientific community to study the CSR factors that determine employee satisfaction, taking into account the diversity of the sector.

6. Conclusions

CSR is responsive to particular social circumstances [

47], so if we want to clearly define the term, it is necessary to describe and to understand the differentiae. So, in this research we identify the characteristic elements of CSR in Andalusia.

On the basis of the results presented here, several conclusions can be drawn. First, when defining the core components of CSR, employers highlight job satisfaction of employees, energy saving measures, and control of environmental risks. Second, there are differences in the scores of the components depending on the economic sector. The job satisfaction of employees is predominant in the agro-livestock sector, whilst in the commerce sector, environmental issues obtain the highest scores. And, finally, according to Andalusian business managers, the use of tools that allow for controlling environmental risks is essential in ensuring employee satisfaction. So, “the recognition of variety allows new claims to be recognized and new power and obligations to arise” [

47] (p. 33).

In summary, the data offer clues as to how and what aspects companies in various sectors should develop or improve to achieve more optimal and beneficial CSR practices for the general society. Whilst the guidelines for achieving good practices in CSR are of a general or universal nature, the reality is that the contexts and their idiosyncrasies play a role in determining whether the emphasis is placed on one component or another. Currently, CSR is based on private self-regulation, although there are calls and efforts to switch to other types of regulation, established in the public agenda, where implementation in practice is developed in line with scientific progress.

According to Kuhn (1970) knowledge of CSR is necessary to focus on the knowledge of science. This knowledge is created to improve, so a “paradigms shift” is necessary, based on different actors and different methods. The main arguments will be to know the differences [

13] which explain types of CSR in different cities and to know different configurations of CSR in various national and regional contexts [

48]. This information could help to identify the particular role national governments may have in developing appropriate and effective CSR strategies [

13]. Finally, we think that to understand, critique and evaluate transnational CSR has significant effects for socially committed institutions [

49].

{kind=link}