3.1. Free-Float Car-Sharing Business Models in Hungary and Germany

Specific free-float service providers are defined as companies offering the service of car-sharing, i.e., the use of vehicles that can be rented and parked freely throughout the entire business area without having to determine the start and the end of the rental period in advance. The beginning and end of the rent are established for all vehicles through a specific smartphone application. Payment is based on usage and according to a fixed minute rate.

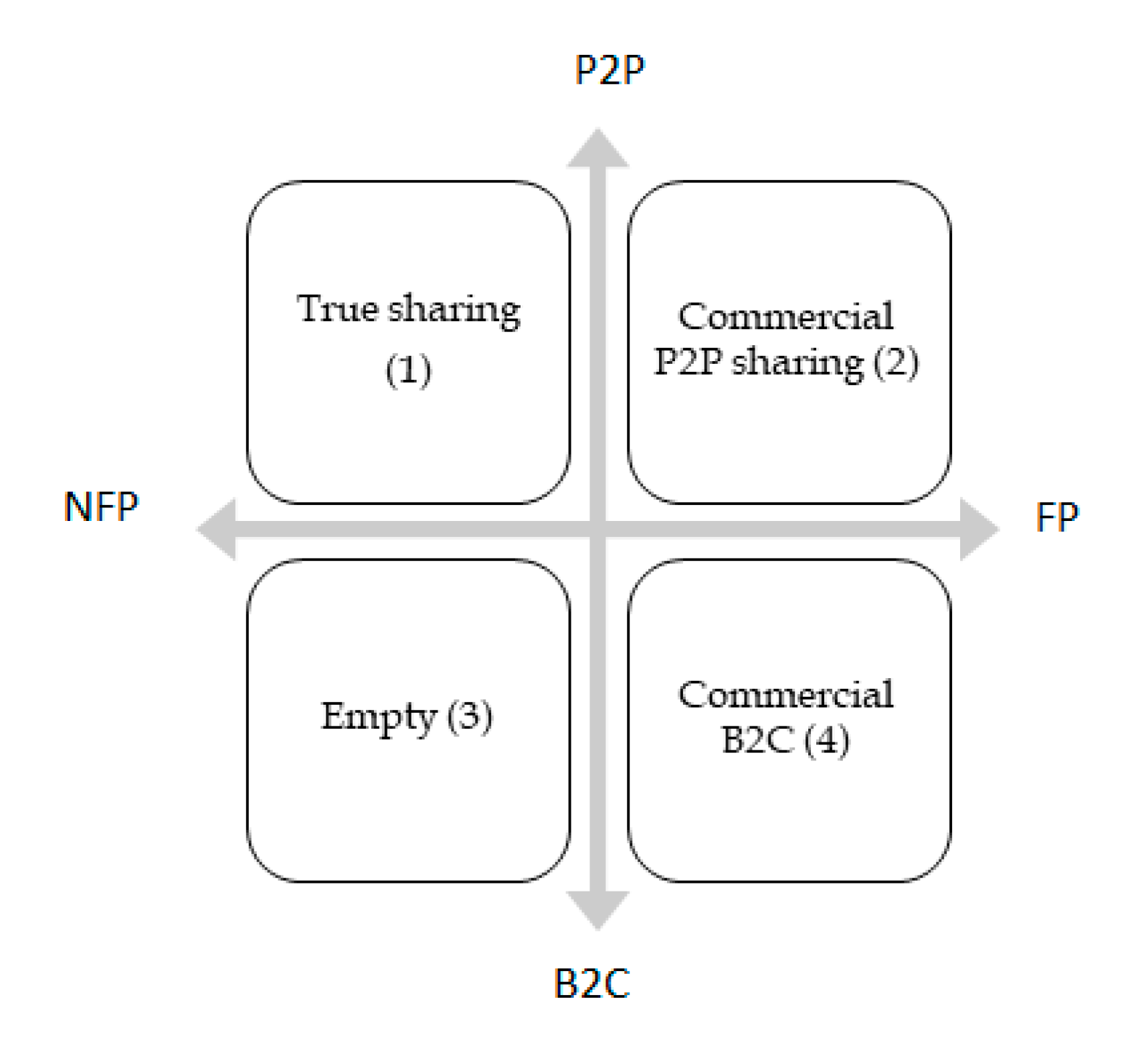

Comparing this market to the sharing economy review models, according to Codagnone and Martens [

30] (

Figure 1), free-float car-sharing entities are B2C entities focused on profitable operation, and this requires strict regulation (

Table 1). This business model represents a different resource utilization with respect to P2P-based common sharing, which motivated us to perform a parallel profitability and sustainability review.

To accurately identify all key free-float companies, the complete database of the firm registry was reviewed, considering the defined principal operational activity of each company. This classification (TEÁOR’08) is “identical and fully harmonized with the European one, NACE Rev.2. Statistical Classification of Economic Activities in the European Community, 2008 (Nomenclature des activités économiques dans les Communautés européennes) [

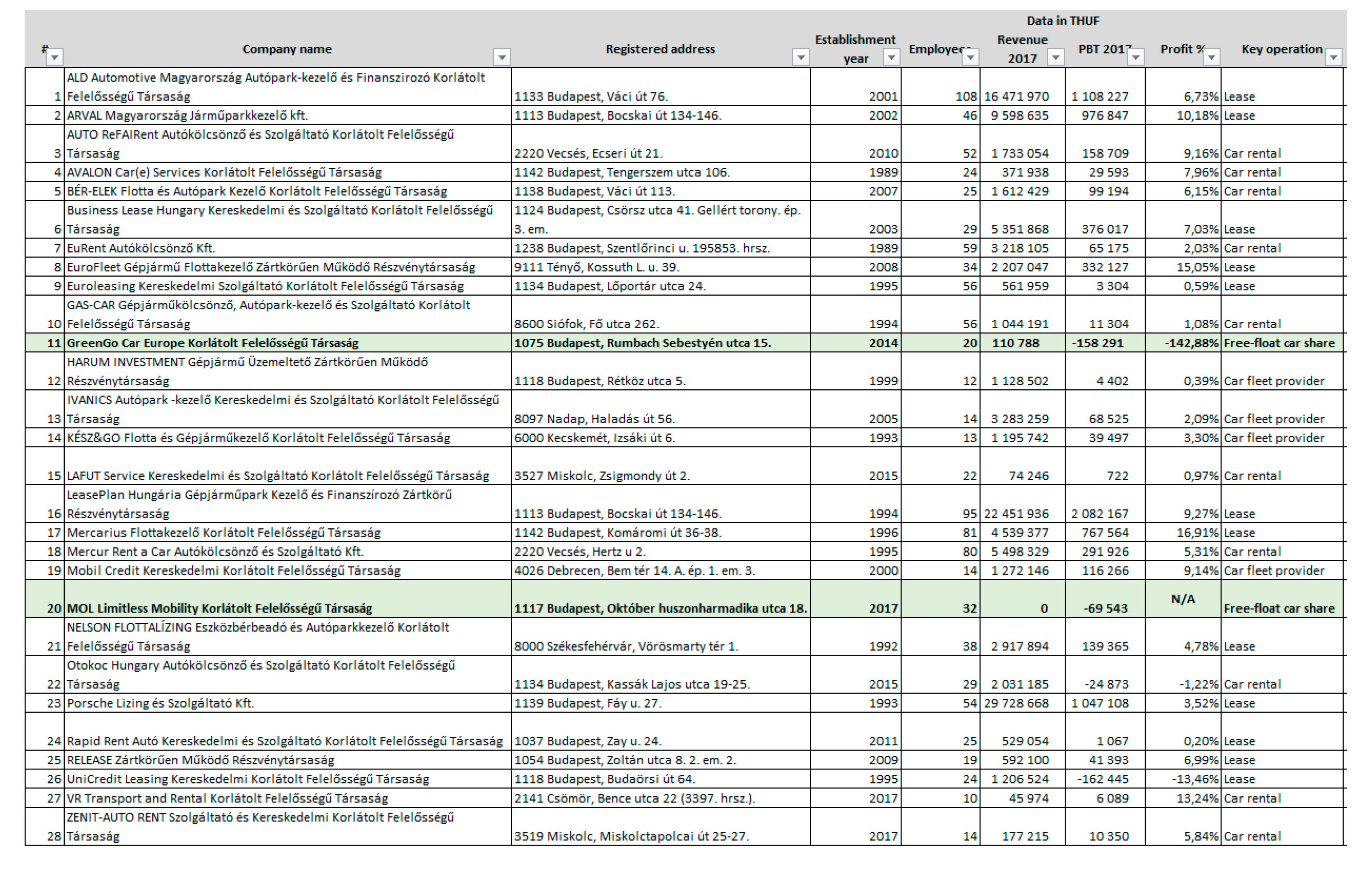

37]. Based on Regulation 1893/2006/EC, with effect from 1 January 2008, TEÁOR’08 is used to determine the principal activities of enterprises, in the calculation of economic and social indicators as well as for the publication of statistical data.” The car-sharing activities are classified under Section “N” as administrative and support service activities, in division 77, group 77.1, and class 77.11 “renting and leasing of cars and light motor vehicles”. From the registered Hungarian companies’ database, 362 companies were identified. This analysis covers all Hungarian operational entities. In order to include recently established objects, all companies above 10 staff headcounts were investigated, according to the EU commission-defined categories. On the basis of a detailed review, 28 companies were identified, as presented in

Appendix A (

Figure A1).

According to the Hungarian Accounting Regulation Act C of 2000, in Hungary [

38], companies need to file a financial statement by the end of the fifth month after the fiscal year. Consequently, the latest reports available were for 2017.

From

Appendix A, on the basis of their financial statements, as of April 2019, only 2 companies out of the total 28 entities, i.e., #11 GreenGo Car Europe Korlátolt Felelősségű Társaság (hereinafter: GreenGo) and #20 MOL Limitless Mobility Korlátolt Felelősségű Társaság (hereinafter: MOL LIMO), were real flee-float car-sharing companies, and both operate in Budapest. This list contained all free-float service providers but did not represent the total lease market, because financial lease activities are classified in a different statistical segment, in section K Financial and insurance activities, divisions 64–66. It did, however, represent all non-micro-level free-float car-sharing companies. This is the consequence of the unclear current statistical data, which do not identify specific lease, rental, or free-float services. In the case of a larger population, it would be challenging to sort out such companies manually; sub-sections could be created to evaluate lease and rental services accurately in the statistical classification. In 2017 for Hungary, free-float car-sharing represented a 110.7 million Hungarian forint (HUF) (€358,300) market.

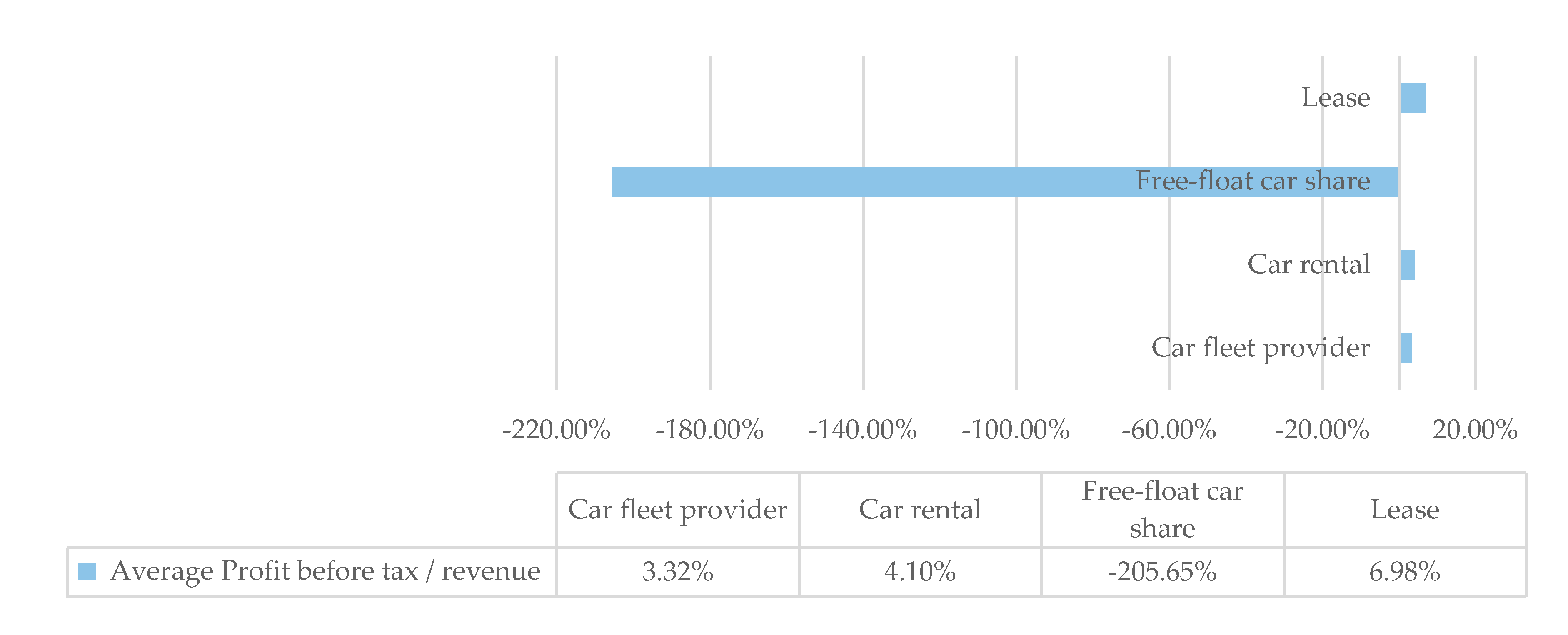

In the analyzed group from the profitability perspective, it was visible that the free-float car-sharing service providers delivered significantly worse results in Hungary compared to lease and rental service companies in 2017, as shown in

Figure 2.

To gain a better understanding of the situation, each Hungarian free-float service was separately examined and later compared to German service providers.

3.1.1. Financial Statement Analysis and Review of the Financing Model

GreenGo was established in 2014 as the first free-float car-sharing service in the Hungarian market, where it was the only market participant until 2017. The first day of real operation, when the company started to provide services, was in November 2016, with 45 electric cars.

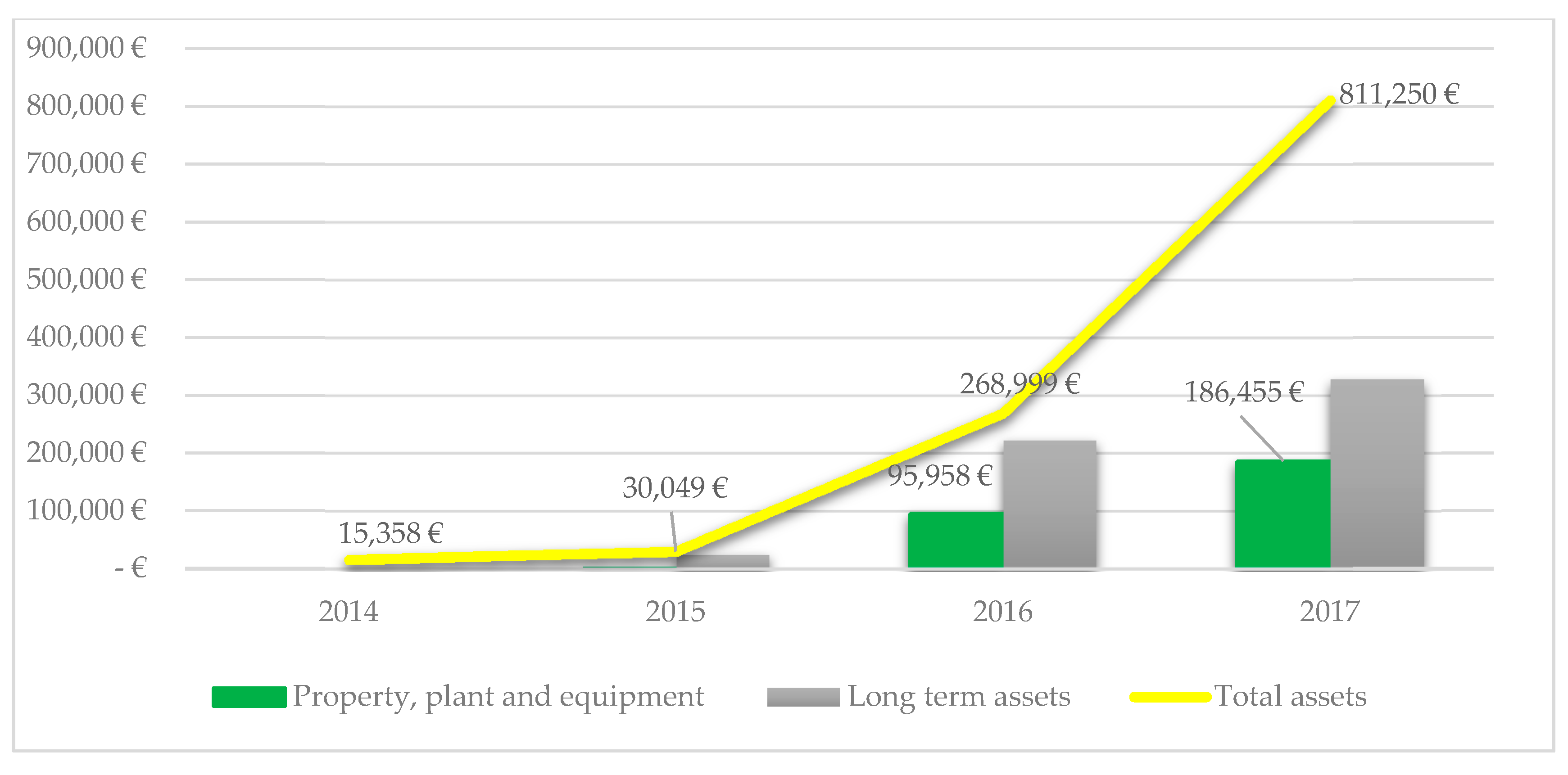

From the financial perspective, the assets and liabilities of the company looked as follows. Assets: The long-term assets value continuously increased from HUF 69 M in 2019 to HUF 102 M on 2017, which consists of intangible assets of HUF 43 M, tangible assets of HUF 58 M, and other investments of HUF 1 M. This breakdown would give the reader important information if we included the published data from January 2018 when GreenGo reported 168 vehicles, which in case of purchase, should be recorded as property, plant, and equipment (PPE). It appears that HUF 58 M/168 vehicles = HUF 0.34 M (approx. €1060) per car is a very unreasonable figure. The only reasonable explanation is if the company applied operational leases, and these assets are off-balance-sheet financed items. Later in this review, this business model will be compared to that of the other Hungarian competitor. Below in

Figure 3 is a summary table related to the asset items for the period 2014–2017:

Liabilities, equity: The equity value remained relatively the same over 2016–2017, i.e., HUF 43 M; however, the generated loss increased significantly from HUF 18 M (€59,000) to HUF 158 M (€512,600), which was compensated by the equity contribution from owners. The debt/equity ratio also significantly increased in relation to the liabilities increase by HUF 129.3 M, mainly as a result of the short-term shareholders’ loans of HUF 115 M and the long-term related parties’ credit of HUF 16 M. Profit and loss statement: The realized revenue increased from the 2016 value of HUF 8 M (€26,000) to the 2017 value of HUF 111 M (€358,000), while the expenses increased from HUF 27 M to HUF 275 M. This was the principal reason for the generated loss as the company did not realize enough revenue to compensate for the increased material expenditures. Below in

Figure 4 is a summary of the statement of profit and loss of GreenGo for the period of 2014–2017.

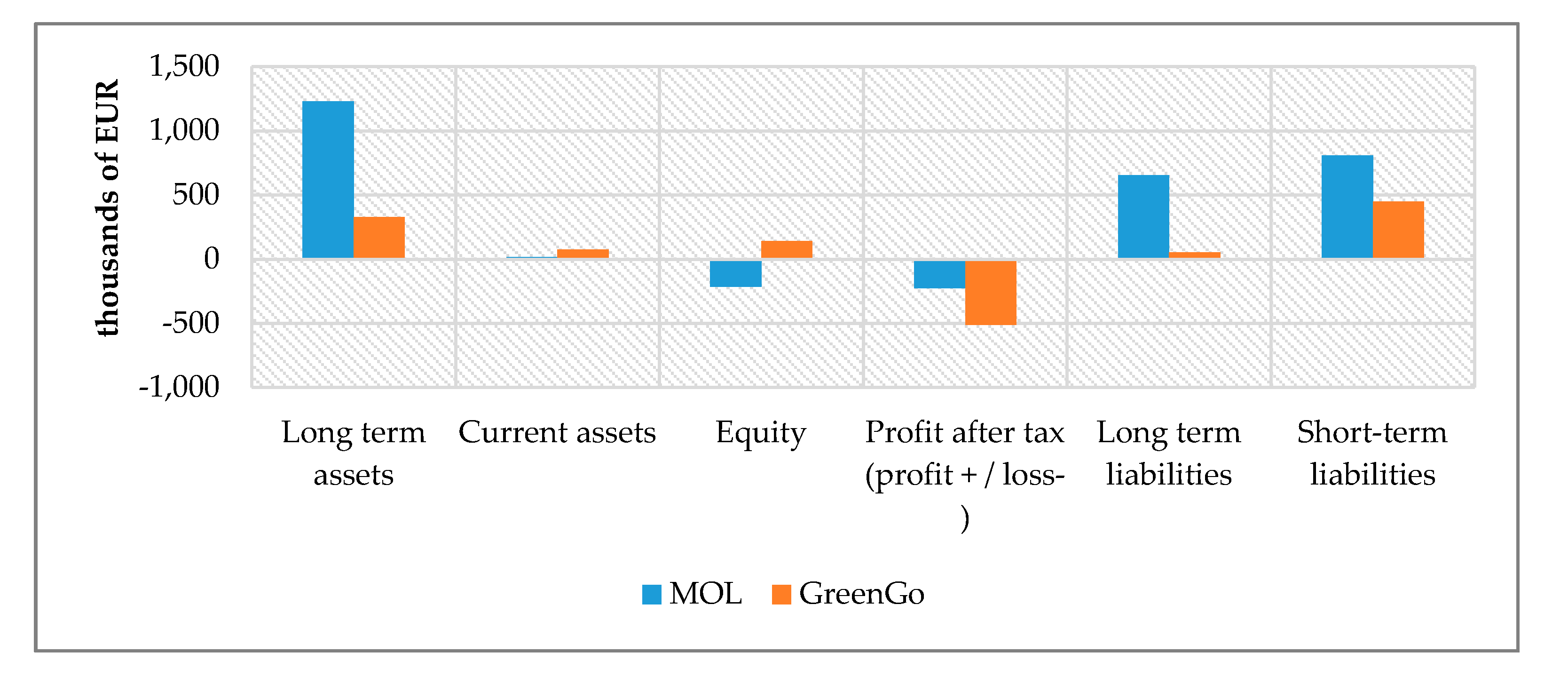

In 2017, MOL Limo entered the market with secured funding from the listed Hungarian Oil-and-Gas Company (whereas GreenGo owners are private investors). MOL Limo market presence did not cause the reported increasing loss of GreenGo, because, in 2017, it did not realize any revenue. In

Table 3, a comparison between the profit and loss statements of these two entities is presented.

MOL Limo generated a significantly higher loss compared to GreenGo, but 2017 was the year of its establishment, with a large scale of operation and considerable fleet investment, as presented in

Table 3. The difference in asset value is related to a specific accounting regulation difference in lease accounting. MOL Limo prepared an IFRS-based financial statement, and GreenGo prepared a simplified national accounting-based financial report.

From the operation perspective, it is essential to mention that GreenGo only uses electric vehicles differently from MOL Limo. The total number of 400 electric vehicles operated by these two companies represents approx. 10% of the registered fully electric (excluding hybrids) cars in Hungary, as presented in

Table 4. It should also be highlighted that hybrid vehicles increased more significantly in Hungary compared to fully electric ones from 2017 to 2018. This trend seems to continue and could be a subject of future investigation.

3.1.2. Lease Accounting Differences

Lease accounting is significantly different in the C Act of 2000 compared to IFRS. According to Hungarian Accounting Law (HAL) and IFRS, the definition of lease is different, and other fundamental accounting difference regard, for example, operating leases, which are not required by HAL to be recorded in the balance sheet, as shown in

Table 5. Also, in the disclosure requirements, as in the HAL-based financial statements, operational leases only appear in the profit and loss statement.

IFRS 16 key objective was to record the operational lease committed rights (rights of use, ROU) as assets and committed liabilities to reduce the off-balance sheet items. For the entities reporting under HAL regulation, this is not a requirement, and in case of an independent financial analysis or a credit strength testing, they can be invisible. The recorded off-balance sheet value can be significant from a creditor’s or financial analysis’ point of view. GreenGo reported under HAL regulation, where the operational leases as off-balance sheet items might create a business advantage from the presentation perspective because the leverage ratio does not show the total minimum of liabilities from the lease obligations.

3.1.3. Comparison to German Entities

Germany has the most significant car-sharing market in Europe, with several service providers and over 30,000 registered users, as summarized below in

Table 6 in comparison to Hungary.

From this table, it can be concluded that German free-float car-sharing companies operate significantly larger fleets and have a substantially larger number of registered users in absolute terms. Hungarian companies operate only in one city, namely, Budapest, with a total of 750 vehicles for a 525 km2 city area, where the population is approx. 1.75 M. In contrast, only one company, ShareNow, operates approx. 4000 cars in Berlin for an 891 km2 city area with a 3.6 M population. For additional comparison, in the capital city in the region with the most similar population, Vienna, only ShareNow operates, with 2000+ vehicles for a 1.8 M population and a 415 km2 city area.

The service fees can also be compared, because in April 2019, ShareNow announced to extend the operation in Budapest as well, with approx. 240 vehicles (of which, 40 electric BMW i3).

Table 7 shows the fee and car type comparison.

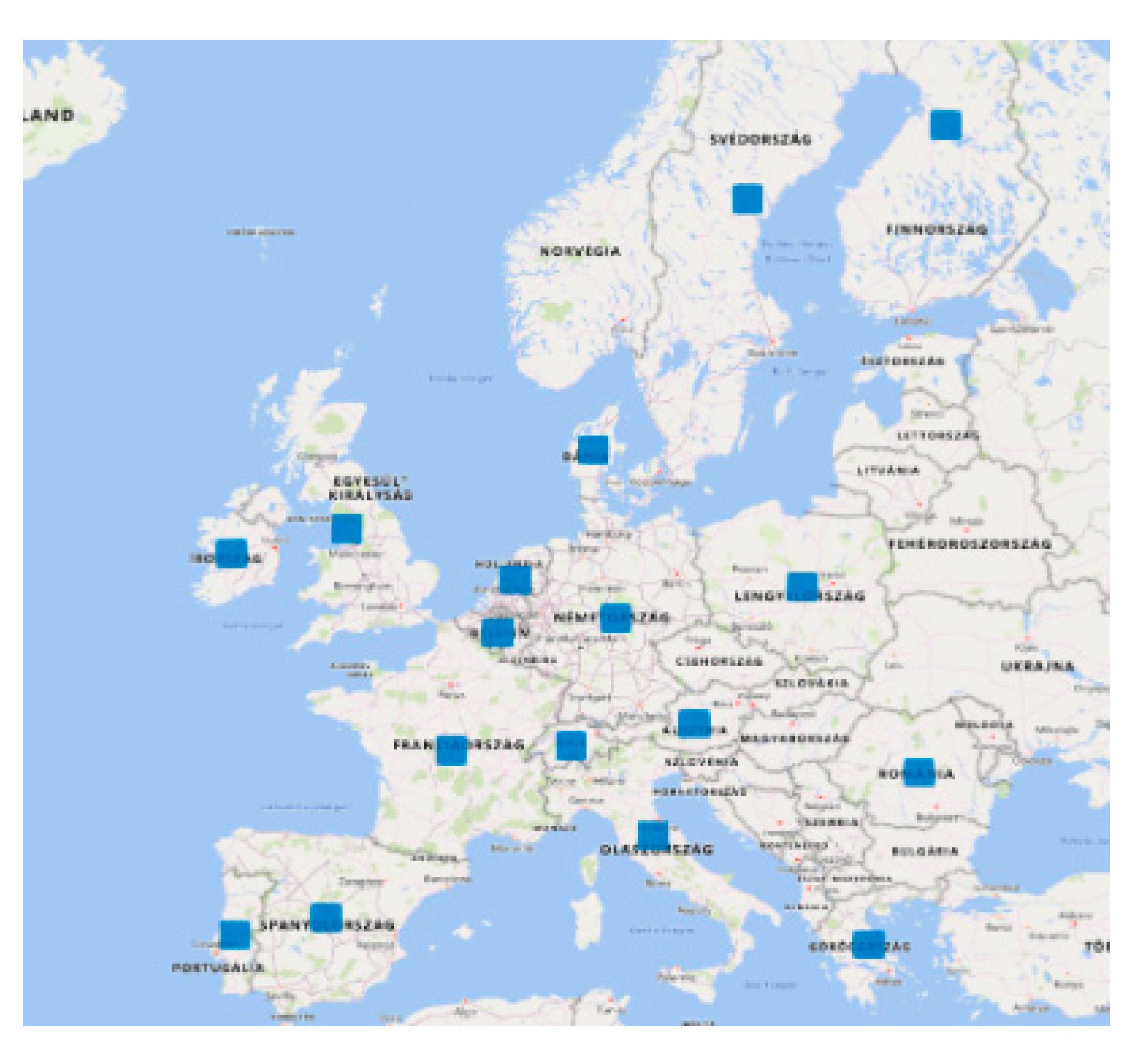

ShareNow provides services across the EU and, in 2019, established the most significant European fleet; additionally, it published a plan to invest further €1 billion. With 20,000+ vehicles, joint companies operate in 24 countries globally. It is only a matter of time to utilize the economies-of-scale advantage and provide service in all European countries. A coverage map for Car2Go and DriveNow is shown in

Figure 5.

From the operation and financial analysis perspectives, an apparent market concentration is happening now in Europe, which is a successful business model. Without doubts, it supports sustainability; however, there is no core sustainability element in this business model. The more effective utilization of the resources has an impact on sustainability, but it is based on a usual corporate profit model.

3.3. Analytic Hierarchy Process

To resolve the lack of reconciliation between financial and sustainability reporting, potential decision-support models, such as the analytic hierarchy process model, can be utilized to present the connection between the different reporting systems. It is crucial to determine the factors and to apply proper weights for the specific items. To measure impacts, the method of the analytic hierarchy process (AHP) was used, where the weights of the factors were identified in order from the most to the least significant from the investor decision’s perspective.

When constructing the decision-making environment, it is crucial to identify issues or attributes that may be helpful [

43,

44], which brings the disharmony of traditional financial performance measuring attributes and sustainability aspects into perspective. The AHP theory aims to find the preferable alternative by weighing the priorities of the involved factors on a 1–9 scale (1: equal importance, 9: higher importance with respect to another component) and carrying out pairwise comparisons and standardization of the results to validate the overall ranking of factors [

43,

44]. Considering the findings of the current study, six elements were selected and weighed (w), as shown in

Figure 6.

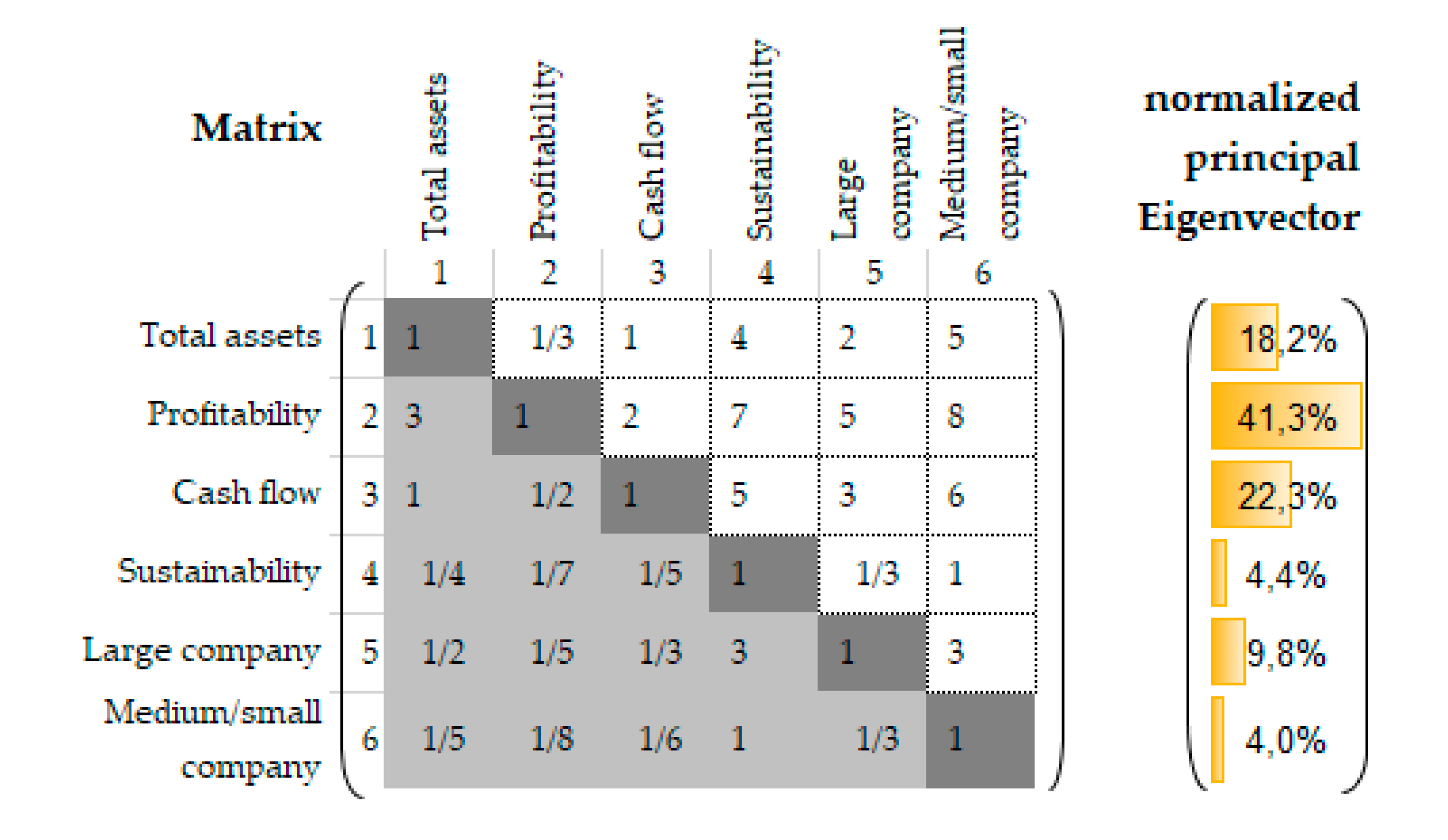

In the analysis process, pairwise comparisons were developed for each criterion using linear integer scaling, summarized in a 6 × 6 matrix, which was then normalized using natural logarithms (

)) [

45]. Using the AHP template and methodology of Goepel [

46], the results were then averaged by rows, and the impacts were measured by the Eigenvector method (EVM). The summary matrix is presented in

Figure 7.

Additionally, the Eigenvalue (or

, consistency measure), the consistency index (CI), the mean relative error (MRE) of the weights, and the consistency ratio (CR) were calculated [

47]. If the Eigenvalue (the matrix product of normalized principal Eigenvectors) equals the sample size (6), perfect consistency can be identified (

), which in our case corresponds to the value of 6.091.

The priorities pi in the input matrix were transformed into a near-consistent model using the EVM. In the pairwise

n ×

n comparison matrix

, where

are comparable elements with a positive numerical value, the transformation procedure is as follows:

with the use of EVM, the measuring procedure can be adapted to pairwise comparisons:

, where

are the principal Eigenvectors [

48].

The normalization process is as follows:

The CI was calculated by:

Error calculation of the priority vector

with the used EVM followed:

In the CR, the Alonson/Lamata linear fit was used:

[

47].

From the hierarchical structure and from the potential AHP model presented in

Figure 7, profitability remains the most significant factor in an investor company valuation with a normalized principal Eigenvector of 41.3%, followed by the cash flows (22.3%) and total assets (18.2%). From the investor decision’s perspective, as long as sustainability reporting does not harmonize with financial reporting, the sustainability aspects tend to have a low impact factor (4.4%). In conclusion, the AHP statistical method is usable for the prioritization of factors, but it should be emphasized that the applied weights of the factors can be depend on subjective evaluations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}