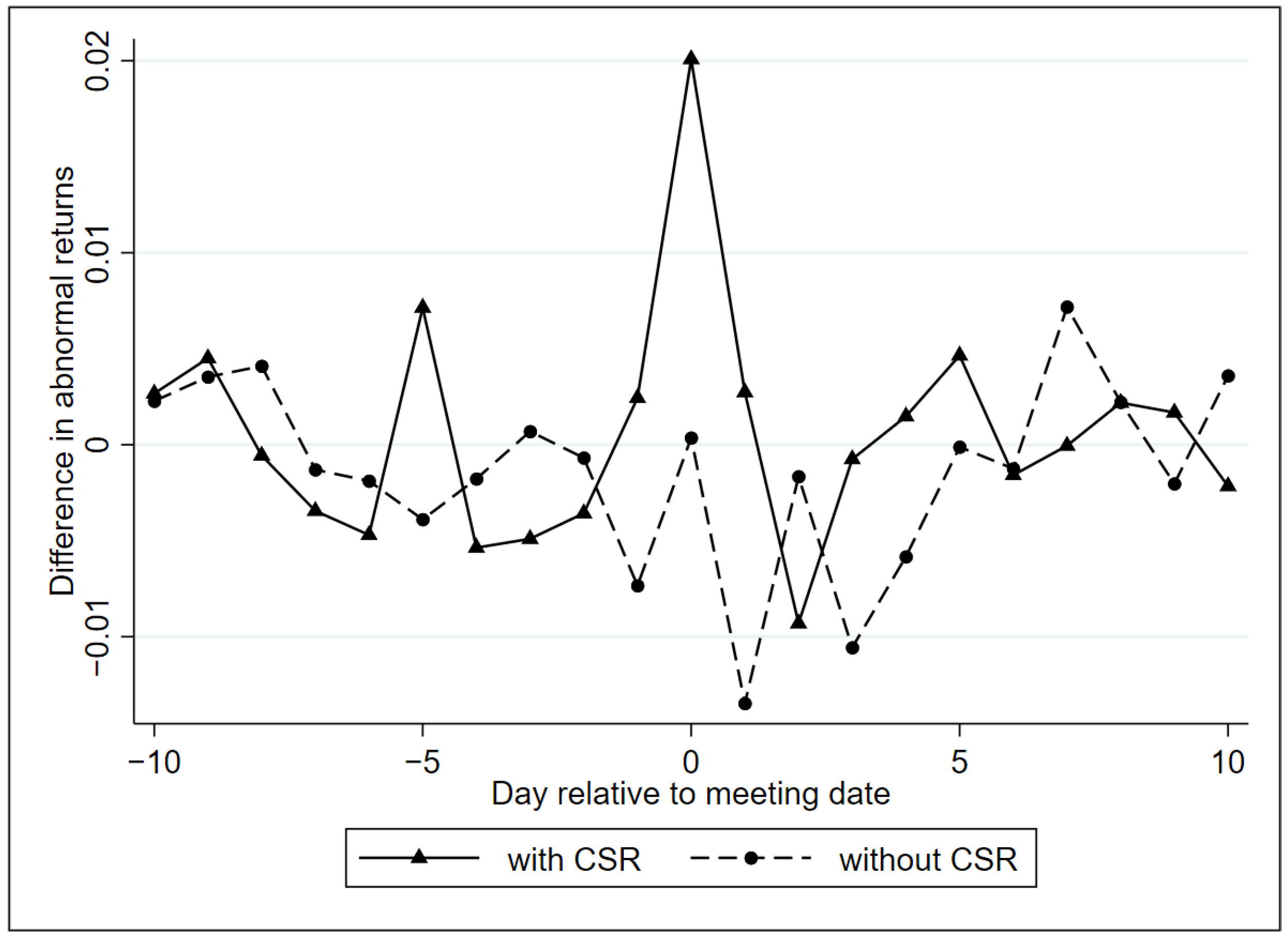

Figure 1.

Difference in Average Abnormal Returns for Vote Shares with Less Than 2% Margin around the Threshold. The vertical axis refers the difference in daily average abnormal returns between proposals approved with less than 2 percentage points margin and those rejected with less than 2 percentage points margin, where abnormal returns are calculated using the Fama-French 5-factor model. The horizontal axis corresponds to the day relative to the meeting date, where day 0 is the meeting date. The solid line is for corporate governance (CG) proposals voted with corporate social responsibility (CSR) proposals, and the dash line is for CG proposals voted without CSR proposals.

Figure 1.

Difference in Average Abnormal Returns for Vote Shares with Less Than 2% Margin around the Threshold. The vertical axis refers the difference in daily average abnormal returns between proposals approved with less than 2 percentage points margin and those rejected with less than 2 percentage points margin, where abnormal returns are calculated using the Fama-French 5-factor model. The horizontal axis corresponds to the day relative to the meeting date, where day 0 is the meeting date. The solid line is for corporate governance (CG) proposals voted with corporate social responsibility (CSR) proposals, and the dash line is for CG proposals voted without CSR proposals.

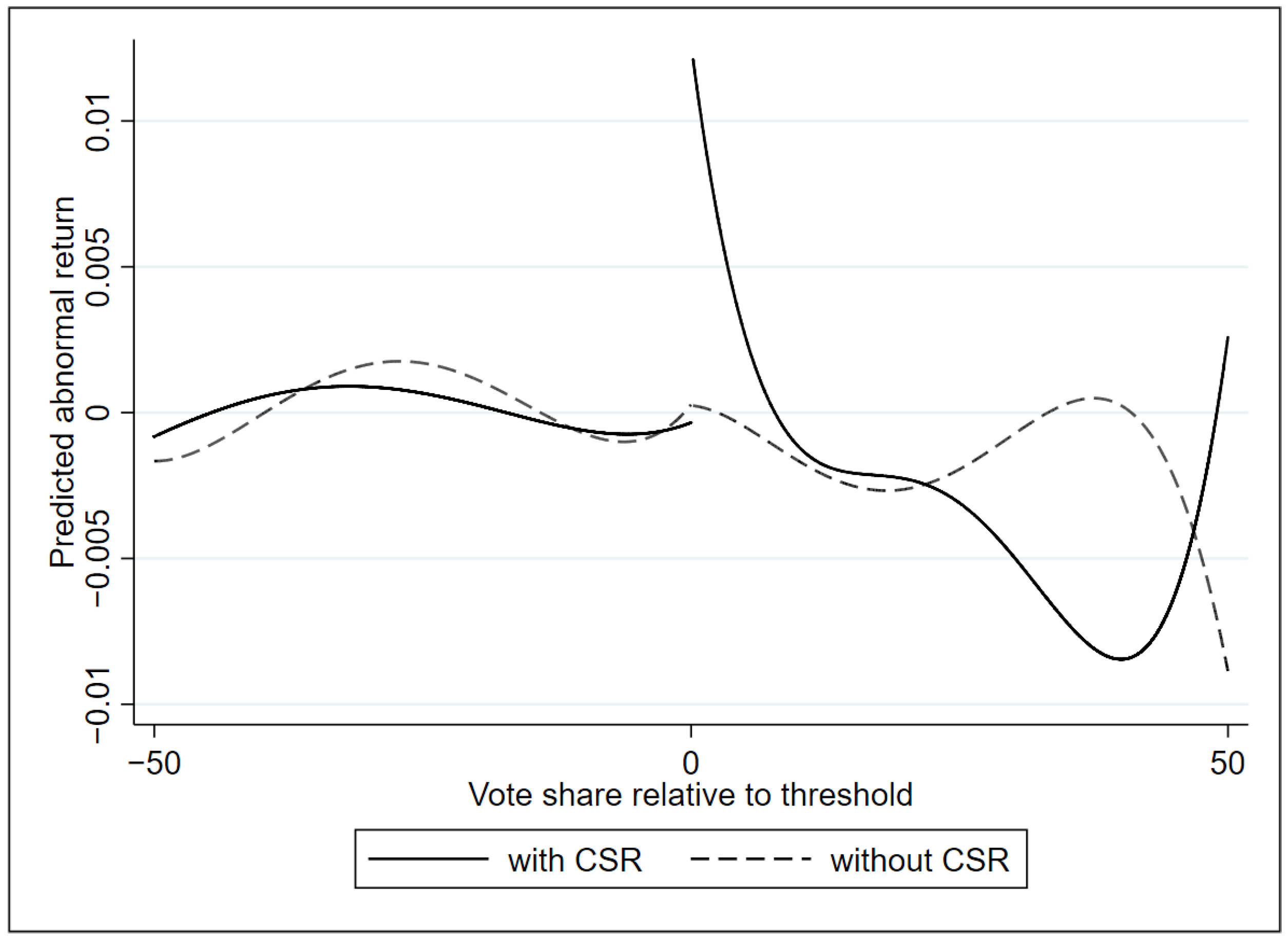

Figure 2.

Predicted Abnormal Returns for the Meeting Date. The vertical axis refers to the predicted abnormal return for the meeting date, where abnormal returns are calculated using the Fama-French 5-factor model. The predicted abnormal returns are from the regression of the abnormal returns for the day of the meeting on whether the proposal is approved, which includes fourth-order polynomials in the excess vote share for each side of the threshold. The horizontal axis corresponds to the vote share relative to the majority threshold. The solid line is for CG proposals voted with CSR proposals, and the dash line is for CG proposals voted without CSR proposals.

Figure 2.

Predicted Abnormal Returns for the Meeting Date. The vertical axis refers to the predicted abnormal return for the meeting date, where abnormal returns are calculated using the Fama-French 5-factor model. The predicted abnormal returns are from the regression of the abnormal returns for the day of the meeting on whether the proposal is approved, which includes fourth-order polynomials in the excess vote share for each side of the threshold. The horizontal axis corresponds to the vote share relative to the majority threshold. The solid line is for CG proposals voted with CSR proposals, and the dash line is for CG proposals voted without CSR proposals.

Table 1.

Corporate Governance (CG) Proposals. This table reports the frequency, approval rate, and average vote share of CG proposals. Data are collected from the Proxy Monitor database on all CG shareholder proposals of the 250 largest US publicly traded companies for annual shareholder meetings between 2006 and 2019.

Table 1.

Corporate Governance (CG) Proposals. This table reports the frequency, approval rate, and average vote share of CG proposals. Data are collected from the Proxy Monitor database on all CG shareholder proposals of the 250 largest US publicly traded companies for annual shareholder meetings between 2006 and 2019.

| Year | Total Proposals | Approved Proposals | Approval Rate | Average Vote Share |

|---|

| 2006 | 177 | 56 | 31.64% | 40.82% |

| 2007 | 138 | 35 | 25.36% | 35.95% |

| 2008 | 113 | 28 | 24.78% | 36.66% |

| 2009 | 161 | 45 | 27.95% | 39.91% |

| 2010 | 149 | 39 | 26.17% | 38.50% |

| 2011 | 123 | 24 | 19.51% | 38.82% |

| 2012 | 140 | 32 | 22.86% | 37.67% |

| 2013 | 121 | 21 | 17.36% | 33.64% |

| 2014 | 110 | 8 | 7.27% | 30.01% |

| 2015 | 142 | 32 | 22.54% | 37.38% |

| 2016 | 129 | 21 | 16.28% | 32.56% |

| 2017 | 109 | 12 | 11.01% | 32.78% |

| 2018 | 140 | 10 | 7.14% | 32.67% |

| 2019 | 127 | 13 | 10.24% | 31.16% |

| Total | 1879 | 376 | 20.01% | 35.94% |

Table 2.

Summary Statistics. This table reports summary statistics of the main variables at meeting dates for the sample. v refers to the excess vote share over the majority threshold, D the indicator variable for whether v is greater than 0, the abnormal return based on the Fama-French 5-factor model. , , , , and correspond to the market excess return over the risk-free rate, the size factor return, the book-to-market factor return, the profitability factor return, and the investment factor return of the Fama-French 5-factor model, respectively. Std. Dev., P25, P50, and P75 represent the standard deviation, 25th percentile, 50th percentile, and 75th percentile, respectively.

Table 2.

Summary Statistics. This table reports summary statistics of the main variables at meeting dates for the sample. v refers to the excess vote share over the majority threshold, D the indicator variable for whether v is greater than 0, the abnormal return based on the Fama-French 5-factor model. , , , , and correspond to the market excess return over the risk-free rate, the size factor return, the book-to-market factor return, the profitability factor return, and the investment factor return of the Fama-French 5-factor model, respectively. Std. Dev., P25, P50, and P75 represent the standard deviation, 25th percentile, 50th percentile, and 75th percentile, respectively.

| Variable | Obs | Mean | Std. Dev. | P25 | P50 | P75 |

|---|

| v | 1683 | −14.25 | 20.43 | −27.68 | −14.14 | −3.58 |

| D | 1683 | 0.19 | 0.39 | 0 | 0 | 0 |

| 1683 | −0.0001 | 0.0164 | −0.0067 | −0.0004 | 0.0061 |

| 1683 | −0.0001 | 0.0100 | −0.0043 | 0.0005 | 0.0051 |

| 1683 | −0.0002 | 0.0054 | −0.0036 | −0.0002 | 0.0034 |

| 1683 | −0.0001 | 0.0065 | −0.003 | −0.0002 | 0.0026 |

| 1683 | 0.0003 | 0.0035 | −0.0019 | 0.0002 | 0.0023 |

| 1683 | −0.0001 | 0.0029 | −0.0021 | −0.0003 | 0.0016 |

Table 3.

Abnormal Returns around the Majority Voting Threshold. This table presents regression results of the abnormal returns for the day of the meeting on whether the proposal is approved. Panel A is for all CG proposals, Panel B for CG proposals voted with corporate social responsibility (CSR) proposals, and Panel C for CG proposals voted without CSR proposals. Abnormal returns are calculated using the Fama-French 5-factor model. The estimates based on all votes in the sample are reported in column (1). Column (2) is based on non-close vote shares, which refer to vote shares more than 10 percentage points away from the threshold. Columns (3)–(6) are based on vote shares less than 10, 5, 2, and 1 percentage points away from the threshold, respectively. Column (7) reports the estimation results, based on the full sample, after including fourth-order polynomials in the excess vote share for each side of the threshold. Standard errors are clustered by firm. t-statistics are reported in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Table 3.

Abnormal Returns around the Majority Voting Threshold. This table presents regression results of the abnormal returns for the day of the meeting on whether the proposal is approved. Panel A is for all CG proposals, Panel B for CG proposals voted with corporate social responsibility (CSR) proposals, and Panel C for CG proposals voted without CSR proposals. Abnormal returns are calculated using the Fama-French 5-factor model. The estimates based on all votes in the sample are reported in column (1). Column (2) is based on non-close vote shares, which refer to vote shares more than 10 percentage points away from the threshold. Columns (3)–(6) are based on vote shares less than 10, 5, 2, and 1 percentage points away from the threshold, respectively. Column (7) reports the estimation results, based on the full sample, after including fourth-order polynomials in the excess vote share for each side of the threshold. Standard errors are clustered by firm. t-statistics are reported in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

| Panel A: All CG Proposals |

| | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

| | All Votes | Non-close | ±10% | ±5% | ±2% | ±1% | Full Model |

| D | −0.0006 | −0.0026 | 0.0024 * | 0.0034 * | 0.0074 ** | 0.0090 ** | 0.0048 * |

| | (−0.67) | (−1.61) | (1.77) | (1.68) | (2.42) | (2.37) | (1.73) |

| Observations | 1683 | 1205 | 478 | 221 | 79 | 48 | 1683 |

| 0.0002 | 0.0033 | 0.0046 | 0.0101 | 0.0511 | 0.0683 | 0.006 |

| Panel B: CG Proposals Voted with CSR Proposals |

| | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

| | All Votes | Non-close | ±10% | ±5% | ±2% | ±1% | Full Model |

| D | 0.0006 | −0.0039 ** | 0.0046 *** | 0.0065 *** | 0.0201 *** | 0.0210 *** | 0.0129 *** |

| | (0.47) | (−2.24) | (2.83) | (2.72) | (3.70) | (4.22) | (2.83) |

| Observations | 869 | 638 | 231 | 104 | 33 | 23 | 869 |

| 0.0003 | 0.0066 | 0.0268 | 0.0519 | 0.2757 | 0.2857 | 0.0179 |

| Panel C: CG Proposals Voted without CSR Proposals |

| | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

| | All Votes | Non-close | ±10% | ±5% | ±2% | ±1% | Full Model |

| D | −0.0015 | −0.0021 | 0.00003 | 0.0007 | 0.0004 | 0.0005 | −0.00003 |

| | (−0.94) | (−0.97) | (0.02) | (0.24) | (0.10) | (0.11) | (−0.01) |

| Observations | 814 | 567 | 247 | 117 | 46 | 25 | 814 |

| 0.0011 | 0.0023 | 0.0000 | 0.0003 | 0.0001 | 0.0002 | 0.0051 |

Table 4.

Abnormal Returns around the Majority Voting Threshold: Aggregation of Multiple Votes and Consideration of Dynamic Effects. This table presents the effect of approving a CG proposal on abnormal returns on the meeting date (t) and on the day after (t + 1), and the sum of the effects on t + 2 to t + 7. Panel A is for all CG proposals, Panel B for CG proposals voted with CSR proposals, and Panel C for CG proposals voted without CSR proposals. Abnormal returns in columns (1)–(3) are calculated using the Fama–French 5-factor model (FF5F), the Fama–French 3-factor model (FF3F), and the Capital Asset Pricing Model (CAPM), respectively. The regression specification accounts for the dynamic effects and multiple votes. Standard errors are clustered by firm. t-statistics are reported in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Table 4.

Abnormal Returns around the Majority Voting Threshold: Aggregation of Multiple Votes and Consideration of Dynamic Effects. This table presents the effect of approving a CG proposal on abnormal returns on the meeting date (t) and on the day after (t + 1), and the sum of the effects on t + 2 to t + 7. Panel A is for all CG proposals, Panel B for CG proposals voted with CSR proposals, and Panel C for CG proposals voted without CSR proposals. Abnormal returns in columns (1)–(3) are calculated using the Fama–French 5-factor model (FF5F), the Fama–French 3-factor model (FF3F), and the Capital Asset Pricing Model (CAPM), respectively. The regression specification accounts for the dynamic effects and multiple votes. Standard errors are clustered by firm. t-statistics are reported in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

| Panel A: All CG Proposals |

| | (1) | (2) | (3) |

| | FF5F | FF3F | CAPM |

| t | 0.0066 * | 0.0055 * | 0.0088 ** |

| | (1.94) | (1.68) | (2.39) |

| t + 1 | 0.0008 | 0.0004 | −0.0008 |

| | (0.18) | (0.08) | (−0.18) |

| t + 2 to t + 7 | 0.0133 | 0.0155 | 0.0298 |

| | (0.89) | (0.96) | (1.15) |

| Observations | 11,868 | 11,868 | 11,868 |

| 0.1074 | 0.1078 | 0.1116 |

| Panel B: CG Proposals Voted with CSR Proposals |

| | (1) | (2) | (3) |

| | FF5F | FF3F | CAPM |

| t | 0.0175 *** | 0.0155 *** | 0.0200 *** |

| | (3.05) | (2.65) | (3.20) |

| t + 1 | 0.0086 | 0.0073 | 0.0036 |

| | (1.20) | (1.00) | (0.43) |

| t + 2 to t + 7 | 0.0291 | 0.0299 | 0.0587 |

| | (1.14) | (1.07) | (1.01) |

| Observations | 5460 | 5460 | 5460 |

| 0.1112 | 0.1133 | 0.1241 |

| Panel C: CG Proposals Voted without CSR Proposals |

| | (1) | (2) | (3) |

| | FF5F | FF3F | CAPM |

| t | 0.0001 | −0.0002 | 0.0019 |

| | (0.03) | (−0.05) | (0.43) |

| t + 1 | −0.0048 | −0.0042 | −0.0041 |

| | (−0.97) | (−0.84) | (−0.79) |

| t + 2 to t + 7 | 0.0031 | 0.0059 | 0.0094 |

| | (0.17) | (0.31) | (0.50) |

| Observations | 6408 | 6408 | 6408 |

| 0.1164 | 0.1156 | 0.1166 |

Table 5.

Abnormal Returns around a Hypothetical Majority Voting Threshold. This table presents regression results of the abnormal returns for the day of the meeting on whether the proposal is approved with a hypothetical majority threshold set as 25%. Panel A is for all CG proposals, Panel B for CG proposals voted with CSR proposals, and Panel C for CG proposals voted without CSR proposals. Abnormal returns are calculated using the Fama-French 5-factor model. The estimates based on all votes in the sample are reported in column (1). Column (2) is based on non-close vote shares, which refer to vote shares more than 10 percentage points away from the threshold. Columns (3)–(6) are based on vote shares less than 10, 5, 2, and 1 percentage points away from the threshold, respectively. Column (7) reports the estimation results, based on the full sample, after including fourth-order polynomials in the excess vote share for each side of the threshold. Standard errors are clustered by firm. t-statistics are reported in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Table 5.

Abnormal Returns around a Hypothetical Majority Voting Threshold. This table presents regression results of the abnormal returns for the day of the meeting on whether the proposal is approved with a hypothetical majority threshold set as 25%. Panel A is for all CG proposals, Panel B for CG proposals voted with CSR proposals, and Panel C for CG proposals voted without CSR proposals. Abnormal returns are calculated using the Fama-French 5-factor model. The estimates based on all votes in the sample are reported in column (1). Column (2) is based on non-close vote shares, which refer to vote shares more than 10 percentage points away from the threshold. Columns (3)–(6) are based on vote shares less than 10, 5, 2, and 1 percentage points away from the threshold, respectively. Column (7) reports the estimation results, based on the full sample, after including fourth-order polynomials in the excess vote share for each side of the threshold. Standard errors are clustered by firm. t-statistics are reported in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

| Panel A: All CG Proposals |

| | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

| | All Votes | Non-close | ±10% | ±5% | ±2% | ±1% | Full Model |

| D | −0.0008 | 0.0001 | −0.0017 | −0.0009 | −0.0021 | −0.0021 | 0.0008 |

| | (−0.73) | (0.08) | (−1.22) | (−0.49) | (−0.92) | (−0.62) | (0.27) |

| Observations | 1683 | 1147 | 536 | 258 | 106 | 49 | 1683 |

| 0.0005 | 0.0000 | 0.0034 | 0.0009 | 0.0083 | 0.0106 | 0.004 |

| Panel B: CG Proposals Voted with CSR Proposals |

| | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

| | All Votes | Non-close | ±10% | ±5% | ±2% | ±1% | Full Model |

| D | −0.0008 | 0.0008 | −0.0032 | −0.0013 | 0.0005 | −0.0031 | 0.0035 |

| | (−0.53) | (0.56) | (−1.37) | (−0.57) | (0.25) | (−0.71) | (1.38) |

| Observations | 869 | 572 | 297 | 142 | 65 | 31 | 869 |

| 0.0007 | 0.0007 | 0.0105 | 0.0021 | 0.0007 | 0.0219 | 0.0132 |

| Panel C: CG Proposals Voted without CSR Proposals |

| | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

| | All Votes | Non-close | ±10% | ±5% | ±2% | ±1% | Full Model |

| D | −0.0008 | −0.0005 | 0.0001 | −0.0002 | −0.0066 | −0.0012 | −0.0031 |

| | (−0.48) | (−0.17) | (0.08) | (−0.06) | (−1.43) | (−0.23) | (−0.48) |

| Observations | 814 | 575 | 239 | 116 | 41 | 18 | 814 |

| 0.0004 | 0.0001 | 0.0000 | 0.0000 | 0.0591 | 0.0032 | 0.0042 |

Table 6.

Abnormal Returns around the Majority Voting Threshold with a Hypothetical Meeting Date. This table presents regression results of the abnormal returns for a hypothetical meeting date, which is set as 7 days earlier than the actual meeting date, on whether the proposal is approved. Panel A is for all CG proposals, Panel B for CG proposals voted with CSR proposals, and Panel C for CG proposals voted without CSR proposals. Abnormal returns are calculated using the Fama-French 5-factor model. The estimates based on all votes in the sample are reported in column (1). Column (2) is based on non-close vote shares, which refer to vote shares more than 10 percentage points away from the threshold. Columns (3)–(6) are based on vote shares less than 10, 5, 2, and 1 percentage points away from the threshold, respectively. Column (7) reports the estimation results, based on the full sample, after including fourth-order polynomials in the excess vote share for each side of the threshold. Standard errors are clustered by firm. t-statistics are reported in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Table 6.

Abnormal Returns around the Majority Voting Threshold with a Hypothetical Meeting Date. This table presents regression results of the abnormal returns for a hypothetical meeting date, which is set as 7 days earlier than the actual meeting date, on whether the proposal is approved. Panel A is for all CG proposals, Panel B for CG proposals voted with CSR proposals, and Panel C for CG proposals voted without CSR proposals. Abnormal returns are calculated using the Fama-French 5-factor model. The estimates based on all votes in the sample are reported in column (1). Column (2) is based on non-close vote shares, which refer to vote shares more than 10 percentage points away from the threshold. Columns (3)–(6) are based on vote shares less than 10, 5, 2, and 1 percentage points away from the threshold, respectively. Column (7) reports the estimation results, based on the full sample, after including fourth-order polynomials in the excess vote share for each side of the threshold. Standard errors are clustered by firm. t-statistics are reported in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

| Panel A: All CG Proposals |

| | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

| | All Votes | Non-close | ±10% | ±5% | ±2% | ±1% | Full Model |

| D | −0.0003 | 0.0002 | −0.0011 | −0.0022 | −0.0015 | 0.0005 | −0.0039 |

| | (−0.28) | (0.21) | (−0.82) | (−1.14) | (−0.53) | (0.15) | (−1.39) |

| Observations | 1683 | 1205 | 478 | 221 | 79 | 48 | 1683 |

| 0.0001 | 0.0000 | 0.0010 | 0.0044 | 0.0028 | 0.0003 | 0.0069 |

| Panel B: CG Proposals Voted with CSR Proposals |

| | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

| | All Votes | Non-close | ±10% | ±5% | ±2% | ±1% | Full Model |

| D | −0.0018 | −0.0006 | −0.0023 | −0.0032 | −0.0034 | −0.0031 | −0.0055 |

| | (−1.37) | (−0.31) | (−0.99) | (−0.94) | (−0.67) | (−0.61) | (−1.06) |

| Observations | 869 | 638 | 231 | 104 | 33 | 23 | 869 |

| 0.0021 | 0.0002 | 0.0036 | 0.0078 | 0.0125 | 0.0087 | 0.0094 |

| Panel C: CG Proposals Voted without CSR Proposals |

| | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

| | All Votes | Non-close | ±10% | ±5% | ±2% | ±1% | Full Model |

| D | 0.0003 | 0.0002 | 0.0005 | −0.0013 | −0.0013 | 0.0019 | −0.0033 |

| | (0.26) | (0.16) | (0.24) | (−0.56) | (−0.36) | (0.39) | (−0.94) |

| Observations | 814 | 567 | 247 | 117 | 46 | 25 | 814 |

| 0.0001 | 0.0000 | 0.0002 | 0.0020 | 0.0025 | 0.0054 | 0.0114 |

{kind=link}

{kind=link}