Fintech Credit and Bank Efficiency: International Evidence

Abstract

:1. Introduction

2. A Brief Literature Review

3. Data and Research Methodology

3.1. Data

3.2. First Stage: Estimating the Efficiency of Banking Systems

3.3. Second Stage: The Interrelationship between Banking Efficiency and Fintech Credit

4. Results

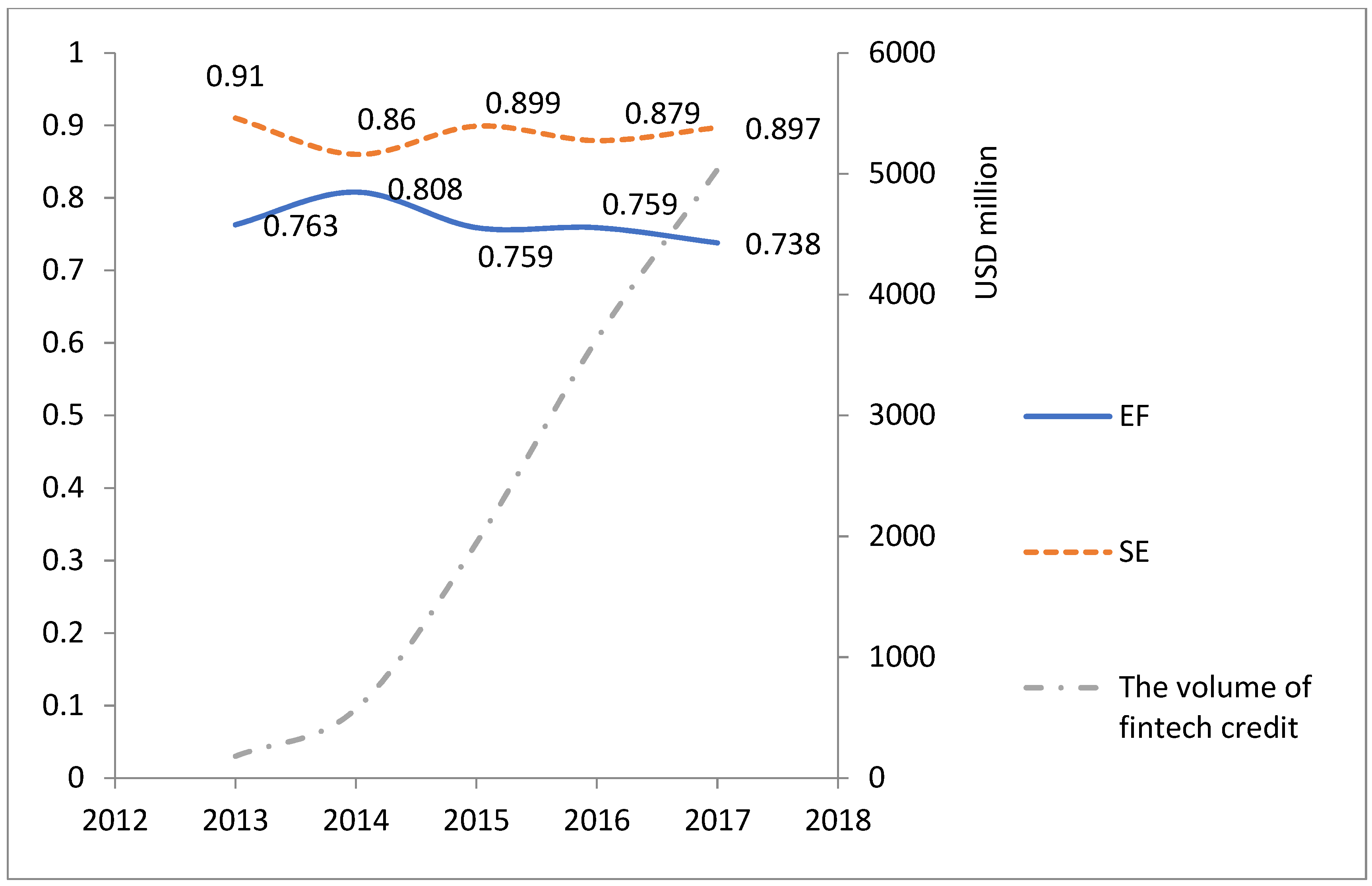

4.1. The Analysis of the Efficiency of Banking Systems around the World

4.2. The Interrelationships between Fintech Credit and Banking Efficiency

4.3. Robustness Checks

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| United Arab Emirates | France | Malaysia | Senegal |

| Argentina | Ghana | Mozambique | El Salvador |

| Austria | Guatemala | Nigeria | Togo |

| Australia | Hong Kong | Netherlands | Thailand |

| Belgium | Indonesia | Norway | Turkey |

| Burkina Faso | Ireland | New Zealand | United Republic of Tanzania |

| Bulgaria | Israel | Panama | Uganda |

| Burundi | India | Peru | United States of America |

| Brazil | Italy | Philippines | Uruguay |

| Côte d’Ivoire | Jordan | Pakistan | Viet Nam |

| Chile | Japan | Poland | South Africa |

| China | Kenya | Portugal | Zambia |

| Colombia | Cambodia | Paraguay | Bolivia |

| Czech Republic | Korea | Russian Federation | Cameroon |

| Germany | Lebanon | Rwanda | Costa Rica |

| Denmark | Lithuani | Saudi Arabia | Georgia |

| Ecuador | Latvia | Sweden | Zimbabwe |

| Estonia | Madagascar | Singapore | |

| Egypt | Mali | Slovenia | |

| Spain | Myanmar | Slovakia | |

| Finland | Mexico | Sierra Leone |

| Variables | Definitions | Expected Signs | Sources | |

|---|---|---|---|---|

| LNFINCAP | The development of fintech credit | The natural logarithm of the volume of fintech credit per capita | ± | Cornelli et al. (2020) and CCAF |

| EF | Bank efficiency | Efficiency score of the individual banking system as derived from Data Envelopment Analysis under variable returns to scale assumption | ± | The Financial Development and Structural Dataset |

| GDPCAP | a country’s level of economic and financial development | The gross domestic product per capita | + | World Bank |

| REGFIN | Fintech regulation | A dummy variable that takes a value of 1 for a country where an explicit fintech credit regulation is in place, and 0 otherwise | + | Rau (2020) |

| MOBILE | Mobile phone subscriptions | Mobile phone subscriptions per 100 persons | + | World Bank |

| BRANCH | The density of bank branch network | The number of bank branches per 100,000 adult population | ± | World Bank |

| LERNER | Banking competition | The Lerner index of the banking sector mark-ups | ± | World Bank and Igan et al. (forthcoming) |

| CONCEN | Market concentration | The ratio of three largest banks’ assets to all commercial banks’ assets | ± | The Financial Development and Structural Dataset |

| RS | Banking regulation | A regulatory stringency index for the banking sector | ± | World Bank |

| GDPGR | Economic growth | The GDP growth rate | ± | World Bank |

| INF | Inflation | The inflation rate | ± | World Bank |

| 2013 | 2014 | 2015 | 2016 | 2017 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Mean | STD | Mean | STD | Mean | STD | Mean | STD | Mean | STD | |

| LNFINCAP | −2.31 | 2.14 | −2.26 | 2.6 | −1.36 | 2.56 | −0.5 | 2.39 | −0.18 | 2.55 |

| LNALTERCAP | 1.19 | 3.03 | 1.77 | 3.28 | 2.49 | 3.64 | 3.31 | 3.37 | 4.31 | 3.02 |

| GDPCAP | 19.17 | 16.68 | 23.15 | 19.91 | 23.71 | 19.78 | 22.31 | 18.79 | 22.5 | 19.06 |

| GDPCAP2 | 639.16 | 775.57 | 925.07 | 1270.4 | 946.89 | 1283.16 | 845.54 | 1229.45 | 864.56 | 1274.52 |

| REGFIN 1 | 0.14 | 0.35 | 0.17 | 0.38 | 0.19 | 0.4 | 0.24 | 0.43 | 0.29 | 0.45 |

| MOBILE | 99.22 | 34.36 | 108.97 | 37.33 | 112.7 | 35.6 | 112.8 | 31.13 | 116.07 | 34.13 |

| BRANCH | 16.47 | 15.99 | 17.57 | 15.5 | 17.49 | 14.97 | 17.97 | 14.59 | 15.94 | 12.44 |

| LERNER 2 | 0.28 | 0.09 | 0.3 | 0.14 | 0.29 | 0.13 | 0.31 | 0.15 | 0.31 | 0.15 |

| CONCEN | 63.14 | 18.32 | 63.28 | 18.93 | 62.48 | 17.22 | 60.5 | 15.55 | 60.21 | 17.26 |

| RS 3 | 0.72 | 0.08 | 0.73 | 0.09 | 0.73 | 0.08 | 0.73 | 0.09 | 0.64 | 0.09 |

| GDPGR | 4.12 | 3.67 | 3.75 | 2.42 | 3.12 | 4.65 | 3.05 | 2.18 | 3.84 | 1.94 |

| INF | 4.19 | 4.69 | 3.46 | 4.35 | 2.94 | 4.6 | 3.43 | 5.05 | 3.92 | 4.84 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. LNFINCAP | 1 | ||||||||||

| 2. LNALTERCAP | 0.8 *** | 1 | |||||||||

| (22.08) | |||||||||||

| 3. EF | −0.03 | 0.04 | 1 | ||||||||

| (−0.48) | (0.64) | ||||||||||

| 4. GDPCAP | 0.52 *** | 0.48 *** | −0.07 | 1 | |||||||

| (10.34) | (9.21) | (−1.25) | |||||||||

| 5. GDPCAP2 | 0.43 *** | 0.39 *** | −0.02 | 0.93 *** | 1 | ||||||

| (8.09) | (7.12) | (−0.37) | (43.74) | ||||||||

| 6. BRANCH | 0.26 *** | 0.22 *** | −0.18 *** | 0.49 *** | 0.29 *** | 1 | |||||

| (4.6) | (3.87) | (−3.06) | (9.37) | (5.12) | |||||||

| 7. MOBILE | 0.29 *** | 0.25 *** | −0.07 | 0.59 *** | 0.48 *** | 0.32 *** | 1 | ||||

| (5.04) | (4.43) | (−1.25) | (12.17) | (9.09) | (5.65) | ||||||

| 8. LERNER | 0.08 | 0.07 | 0.22 *** | 0.13 ** | 0.27 *** | −0.05 | 0.14 ** | 1 | |||

| (1.3) | (1.26) | (3.81) | (2.14) | (4.68) | (−0.91) | (2.4) | |||||

| 9. CONCEN | 0.19 *** | 0.06 | −0.04 | 0.28 *** | 0.28 *** | −0.01 | 0.12 ** | −0.01 | 1 | ||

| (3.24) | (1.08) | (−0.66) | (4.89) | (4.98) | (−0.19) | (2.03) | (−0.12) | ||||

| 10. GDP | −0.12 ** | −0.1 * | 0.04 | −0.22 *** | −0.11 * | −0.28 *** | −0.24 *** | 0.08 | −0.2 *** | 1 | |

| (−2.05) | (−1.72) | (0.63) | (−3.78) | (−1.89) | (−4.99) | (−4.16) | (1.38) | (−3.49) | |||

| 11. INF | −0.43 *** | −0.32 *** | 0.36 *** | −0.45 *** | −0.35 *** | −0.38 *** | −0.35 *** | 0.02 | −0.12 ** | 0.04 | 1 |

| (−8.07) | (−5.64) | (6.55) | (−8.38) | (−6.34) | (−6.86) | (−6.32) | (0.34) | (−1.99) | (0.67) |

| 1 | It is important to note that the data on fintech credit provided by Cornelli et al. (2020) and CCAF were available from 2013 to 2018, while the data used to estimate efficiency scores of banking systems were available until 2017. Therefore, our sample period of 2013–2017 was selected to maintain our observations as many as possible. |

| 2 | DEA techniques have been extensively used in finance studies. For more details, please see Boubaker et al. (2015) and Kaffash and Marra (2017). |

| 3 | Since the number of countries is relatively high, compared to the number of observations, we did not use the country fixed-effect dummy variables in our models. In addition, the inclusion of several country-specific regressors prevents us from using a set of country dummies. To be specific, we controlled for differences in the examined countries in terms of their banking competition (LERNER), market concentration (CONCEN), banking regulation (RS), fintech regulation (REGFIN) as well as other institutional characteristics (for robustness checks). We believe that any country-level differences should be accounted for in the robustness testing. |

References

- Aliber, Robert Z., and Charles P. Kindleberger. 2015. Manias Panics and Crashes: A History of Financial Crises. Hampshire: Palgrave Macmillan. [Google Scholar]

- Allen, Franklin, and Douglas Gale. 1999. Diversity of opinion and financing of new technologies. Journal of Financial Intermediation 8: 68–89. [Google Scholar] [CrossRef] [Green Version]

- Baltagi, Badi H. 2008. Econometric Analysis of Panel Data. New York: John Wiley. [Google Scholar]

- Banker, Rajiv D., Abraham Charnes, and William Wager Cooper. 1984. Some models for estimating technical and scale inefficiencies in data envelopment analysis. Management Science 30: 1078–92. [Google Scholar] [CrossRef] [Green Version]

- Beck, Thorsten, Asli Demirgüç-Kunt, and Ross Levine. 2000. A new database on financial development and structure. [Updated September 2019]. World Bank Economic Review 14: 597–605. [Google Scholar] [CrossRef]

- Berger, Allen N., and Timothy H. Hannan. 1998. The efficiency cost of market power in the banking industry: A test of the ‘quiet life’ and related hypotheses. Review of Economics and Statistics 80: 454–65. Available online: https://www.jstor.org/stable/2646754 (accessed on 30 April 2021). [CrossRef]

- Berger, Allen N., and David B. Humphrey. 1997. Efficiency of financial institutions: International survey and directions for future research. European Journal of Operational Research 98: 175–212. [Google Scholar] [CrossRef] [Green Version]

- Bömer, Max, and Hannes Maxin. 2018. Why fintechs cooperate with banks—Evidence from germany. Zeitschrift für die Gesamte Versicherungswissenschaft 107: 359–86. [Google Scholar] [CrossRef] [Green Version]

- Boubaker, Sabri, Amal Hamrouni, and Qi-Bin Liang. 2015. Corporate governance, voluntary disclosure, and firm information environment. Journal of Applied Business Research (JABR) 31: 89–102. [Google Scholar] [CrossRef] [Green Version]

- Boubaker, Sabri, Asma Houcine, Zied Ftiti, and Hatem Masri. 2018. Does audit quality affect firms’ investment efficiency? Journal of the Operational Research Society 69: 1688–99. [Google Scholar] [CrossRef]

- Boubaker, Sabri, Duc Trung Do, Helmi Hammami, and Kim Cuong Ly. 2020. The role of bank affiliation in bank efficiency: A fuzzy multi-objective data envelopment analysis approach. Annals of Operations Research S.I (MOPGP19). [Google Scholar] [CrossRef]

- Boubaker, Sabri, Riadh Manita, and Wael Rouatbi. 2021. Large shareholders, control contestability and firm productive efficiency. Annals of Operations Research 296: 591–614. [Google Scholar] [CrossRef]

- Buchak, Greg, Gregor Matvos, Tomasz Piskorski, and Amit Seru. 2018. Fintech, regulatory arbitrage, and the rise of shadow banks. Journal of Financial Economics 130: 453–83. [Google Scholar] [CrossRef]

- Charnes, Abraham, William W. Cooper, and Edwardo Rhodes. 1978. Measuring the efficiency of decision making units. European Journal of Operational Research 2: 429–44. [Google Scholar] [CrossRef]

- Cheng, Maoyong, and Yang Qu. 2020. Does bank FinTech reduce credit risk? Evidence from China. Pacific-Basin Finance Journal 63: 101398. [Google Scholar] [CrossRef]

- Claessens, Stijn, Jon Frost, Grant Turner, and Feng Zhu. 2018. Fintech Credit Markets around the World: Size, Drivers and Policy Issues. BIS Quarterly Review. Available online: https://www.bis.org/publ/qtrpdf/r_qt1809e.htm (accessed on 14 August 2021).

- Coelli, Timothy J., Dodla Sai Prasada Rao, Christopher J. O’Donnell, and George Edward Battese. 2005. An Introduction to Efficiency and Productivity Analysis. New York: Springer. [Google Scholar]

- Cornelli, Giulio, Jon Frost, Leonardo Gambacorta, P. Raghavendra Rau, Robert Wardrop, and Tania Ziegler. 2020. Fintech and Big Tech Credit: A New Database. BIS Working Papers No. 887. Basel: Bank for International Settlements. [Google Scholar]

- De Roure, Calebe, Loriana Pelizzon, and Paolo Tasca. 2016. How Does P2P Lending Fit into the Consumer Credit Market? Discussion Paper No 30/2016. Frankfurt: Deutsche Bundesbank. [Google Scholar]

- De Roure, Calebe, Loriana Pelizzon, and Anjan V. Thakor. 2018. P2P Lenders versus Banks: Cream Skimming or Bottom Fishing? SAFE Working Paper No. 206. Frankfurt: Sustainable Architecture for Finance in Europe. [Google Scholar]

- Deloitte. 2015. Millennials and wealth management: Trends and challenges of the new clientele. In Inside: Quaterly Insights, CFO Edition. Luxembourg: Deloitte. [Google Scholar]

- Demirgüç-Kunt, Ash, and Harry Huizinga. 1999. Determinants of commercial bank interest margins and profitability: Some international evidence. The World Bank Economic Review 13: 379–408. Available online: https://www.jstor.org/stable/3990103 (accessed on 30 April 2021).

- Drake, Leigh, J. B. Maximillan Hall, and Richard Simper. 2006. The impact of macroeconomic and regulatory factors on bank efficiency: A non-parametric analysis of Hong Kong’s banking system. Journal of Banking & Finance 30: 1443–66. [Google Scholar] [CrossRef] [Green Version]

- Gefen, David, Detmar Straub, and Marie-Claude Boudreau. 2000. Structural equation modeling and regression: Guidelines for research practice. Communications of the Association for Information Systems 4: 1–78. [Google Scholar] [CrossRef] [Green Version]

- Ho, Tin H., Dat T. Nguyen, Thanh Ngo, and Tu D. Q. Le. 2021. Efficiency in Vietnamese banking: A meta-regression analysis approach. International Journal of Financial Studies 9: 41. [Google Scholar] [CrossRef]

- Igan, Deniz, Maria Soledad Martinez Peria, Nicola Pierri, and Andrea F. Presbitero. forthcoming. When They Go Low, We Go High? Bank Market Power and Interest Rates. Washington: IMF Working Papers.

- Jagtiani, Julapa, and Catharine Lemieux. 2019. The roles of alternative data and machine learning in fintech lending: Evidence from the LendingClub consumer platform. Financial Management 48: 1009–29. [Google Scholar] [CrossRef]

- Kaffash, Sepideh, and Marianna Marra. 2017. Data envelopment analysis in financial services: A citations network analysis of banks, insurance companies and money market funds. Annals of Operations Research 253: 307–44. [Google Scholar] [CrossRef] [Green Version]

- Le, Tu D. Q. 2018. Bank risk, capitalisation and technical efficiency in the Vietnamese banking system. Australasian Accounting Business & Finance Journal 12: 42–61. [Google Scholar] [CrossRef]

- Le, Tu D. Q. 2020. The interrelationship among bank profitability, bank stability, and loan growth: Evidence from Vietnam. Cogent Business & Management 7: 1–18. [Google Scholar] [CrossRef]

- Le, Tu D. Q. 2021. The Roles of Financial Inclusion and Financial Markets Development in Fintech Credit: Evidence from Developing Countries. Ho Chi Minh City: Institute for Development & Research in Banking Technology, University of Economics and Law. [Google Scholar]

- Le, Tu D. Q., and Thanh Ngo. 2020. The determinants of bank profitability: A cross-country analysis. Central Bank Review 20: 65–73. [Google Scholar] [CrossRef]

- Le, Tu D. Q., and Xuan T. T. Pham. 2021. The inter-relationships among liquidity creation, bank capital and credit risk: Evidence from emerging Asia–Pacific economies. Managerial Finance 47: 1149–67. [Google Scholar] [CrossRef]

- Liu, John S., Louis Y. Y. Lu, Wen-Min Lu, and Bruce J. Y. Lin. 2013. A survey of DEA applications. Omega 41: 893–902. [Google Scholar] [CrossRef]

- Manlagnit, Maria Chelo V. 2015. Basel regulations and banks’ efficiency: The case of the Philippines. Journal of Asian Economics 39: 72–85. [Google Scholar] [CrossRef]

- Marquez, Robert. 2002. Competition, adverse selection, and information dispersion in the banking industry. The Review of Financial Studies 15: 901–26. [Google Scholar] [CrossRef]

- Navaretti, Giorgio Barba, Giacomo Calzolari, José Manuel Mansilla-Fernandez, and Alberto F. Pozzolo. 2017. Fintech and Banking. Friends or Foes. In Fintech and Banking. Edited by Giorgio Barba Navaretti, Giacomo Calzolari and Alberto Franco Pozzolo. Rome: Europeye srl. [Google Scholar]

- Newey, Whitney K., and Kenneth D. West. 1987. A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica 55: 703–8. [Google Scholar] [CrossRef]

- Ngo, Thanh, and Tu Le. 2019. Capital market development and bank efficiency: A cross-country analysis. International Journal of Managerial Finance 15: 478–91. [Google Scholar] [CrossRef]

- Nguyen, James. 2012. The relationship between net interest margin and noninterest income using a system estimation approach. Journal of Banking & Finance 36: 2429–37. [Google Scholar] [CrossRef]

- Oh, Eun Young, and Peter Rosenkranz. 2020. Determinants of Peer-to-Peer Lending Expansion: The Roles of Financial Development and Financial Literacy. Working Paper Series 613. Philippines: Asian Development Bank. [Google Scholar]

- Paradi, Joseph C., H. David Sherman, and Fai Keung Tam. 2017. Data Envelopment Analysis in the Financial Services Industry: A Guide for Practitioners and Analysts Working in Operations Research Using DEA. Cham: Springer, vol. 266. [Google Scholar]

- Phan, Hanh Thi My, Kevin Daly, and Selim Akhter. 2016. Bank efficiency in emerging Asian countries. Research in International Business and Finance 38: 517–30. [Google Scholar] [CrossRef]

- Rau, P. Raghavendra. 2020. Law, Trust, and the Development of Crowdfunding. Cambridge: Cambridge Centre for Alternative Finance Working Paper. [Google Scholar]

- Reinhard, Stijn, C. A. Knox Lovell, and Geert J. Thijssen. 2000. Environmental efficiency with multiple environmentally detrimental variables; estimated with SFA and DEA. European Journal of Operational Research 121: 287–303. [Google Scholar] [CrossRef]

- Sheng, Tianxiang. 2021. The effect of fintech on banks’ credit provision to SMEs: Evidence from China. Finance Research Letters 39: 101558. [Google Scholar] [CrossRef]

- Siek, Michael, and Andrew Sutanto. 2019. Impact analysis of fintech on banking industry. Paper presented at the 2019 International Conference on Information Management and Technology (ICIMTech), Jakarta, Indonesia, August 19–20; pp. 356–61. [Google Scholar] [CrossRef]

- Song, Fengshua, and Anjan Thakor. 2010. Banks and capital markets as a coevolving financial system. VoxEU.org, December 1. [Google Scholar]

- Tang, Huan. 2019. Peer-to-peer lenders versus banks: Substitutes or complements? The Review of Financial Studies 32: 1900–38. [Google Scholar] [CrossRef]

- Vidal-García, Javier, Marta Vidal, Sabri Boubaker, and Majdi Hassan. 2018. The efficiency of mutual funds. Annals of Operations Research 267: 555–84. [Google Scholar] [CrossRef]

- Vives, Xavier. 2017. The impact of Fintech on banking. In Fintech and Banking. Friends or Foes? Edited by Giorgio Barba Navaretti, Giacomo Calzolari and Alberto Franco Pozzolo. Roma: Europeye srl. [Google Scholar]

- Wooldridge, Jeffrey M. 2001. Econometric Analysis of Cross Section and Panel Data. Cambridge: The MIT Press. [Google Scholar]

- World Bank. 2017. World Development Indicators (WDI). Washington: The World Bank. [Google Scholar]

- Yeo, Eunjung, and Jooyong Jun. 2020. Peer-to-Peer Lending and Bank Risks: A Closer Look. Sustainability 12: 6107. [Google Scholar] [CrossRef]

| Year | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|

| No. Obs | 50 | 59 | 66 | 75 | 80 |

| DEPOSIT | |||||

| Mean | 52.96 | 63.61 | 63.23 | 60.35 | 62.24 |

| STD | 44.02 | 57.41 | 54.95 | 42.27 | 51.05 |

| LABOR | |||||

| Mean | 3.75 | 3.18 | 3.56 | 3.4 | 3.56 |

| STD | 2.69 | 2.24 | 4.13 | 3.53 | 2.7 |

| CREDIT | |||||

| Mean | 67.47 | 60.12 | 61.25 | 59.58 | 61.34 |

| STD | 113.68 | 47.09 | 46.83 | 40.88 | 42.001 |

| NIM | |||||

| Mean | 4.86 | 4.12 | 3.86 | 4.09 | 4.92 |

| STD | 3.27 | 2.88 | 2.83 | 2.99 | 3.91 |

| Part 1. Equation (2) of SEM | |||

| Dependent Variable: LNFINCAP | |||

| Independent Variables | Coefficient | Standard Error | t-Statistic |

| Constant | −0.553 | 1.095 | −0.505 |

| EF | −2.944 ** | 1.285 | −2.291 |

| GDPCAP | 0.152 *** | 0.027 | 5.702 |

| GDPCAP2 | −0.001 *** | 0.0003 | −3.509 |

| REGFIN | 0.791 ** | 0.378 | 2.093 |

| MOBILE | −0.005 | 0.005 | −1.089 |

| BRANCH | −0.021 * | 0.012 | −1.815 |

| GDPGR | −0.01 | 0.046 | −0.212 |

| No. Obs | 330 | ||

| J-Statistics (p-value) | 0.158 | ||

| Part 2. Equation (3) of SEM | |||

| Dependent Variable: EF | |||

| Independent Variables | Coefficient | Standard Error | t-Statistic |

| Constant | 0.585 *** | 0.115 | 5.101 |

| LNFINCAP | 0.022 ** | 0.01 | 2.222 |

| LERNER | 0.295 *** | 0.071 | 4.168 |

| CONCEN | −0.0002 | 0.001 | −0.335 |

| RS | 0.05 | 0.149 | 0.332 |

| GDPGR | −0.001 | 0.004 | −0.177 |

| INF | 0.021 *** | 0.003 | 7.932 |

| No. Obs | 330 | ||

| J-Statistics (p-value) | 0.158 | ||

| Part 1. Equation (2) of SEM | |||

| Dependent Variable: LNALTERCAP | |||

| Independent Variables | Coefficient | Standard Error | t-Statistic |

| Constant | −0.149 | 0.662 | −0.225 |

| EF | 0.368 | 0.818 | 0.45 |

| GDPCAP | 0.082 *** | 0.013 | 6.178 |

| GDPCAP2 | −0.001 *** | 0.0002 | −3.840 |

| REGFIN | 0.352 * | 0.209 | 1.687 |

| MOBILE | −0.003 | 0.002 | −1.955 |

| BRANCH | −0.019 *** | 0.006 | −3.387 |

| GDPGR | 0.009 | 0.023 | 0.377 |

| No. Obs | 330 | ||

| J-Statistics (p-value) | 0.135 | ||

| Part 2. Equation (3) of SEM | |||

| Dependent Variable: EF | |||

| Independent Variables | Coefficient | Standard Error | t-Statistic |

| Constant | 0.551 *** | 0.131 | 4.197 |

| LNALTERCAP | 0.04 ** | 0.017 | 2.356 |

| LERNER | 0.280 *** | 0.067 | 4.166 |

| CONCEN | 0.0001 | 0.001 | 0.246 |

| RS | −0.002 | 0.142 | −0.017 |

| GDPGR | 0.001 | 0.004 | 0.288 |

| INF | 0.018 *** | 0.002 | 8.351 |

| No. Obs | 330 | ||

| J-Statistics (p-value) | 0.135 | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Le, T.D.Q.; Ho, T.H.; Nguyen, D.T.; Ngo, T. Fintech Credit and Bank Efficiency: International Evidence. Int. J. Financial Stud. 2021, 9, 44. https://doi.org/10.3390/ijfs9030044

Le TDQ, Ho TH, Nguyen DT, Ngo T. Fintech Credit and Bank Efficiency: International Evidence. International Journal of Financial Studies. 2021; 9(3):44. https://doi.org/10.3390/ijfs9030044

Chicago/Turabian StyleLe, Tu D. Q., Tin H. Ho, Dat T. Nguyen, and Thanh Ngo. 2021. "Fintech Credit and Bank Efficiency: International Evidence" International Journal of Financial Studies 9, no. 3: 44. https://doi.org/10.3390/ijfs9030044

APA StyleLe, T. D. Q., Ho, T. H., Nguyen, D. T., & Ngo, T. (2021). Fintech Credit and Bank Efficiency: International Evidence. International Journal of Financial Studies, 9(3), 44. https://doi.org/10.3390/ijfs9030044