Did Financial Consumers Benefit from the Digital Transformation? An Empirical Investigation

Abstract

:1. Introduction

2. Financial Sector Development and Digitalization

3. Valuing the Financial Services Sector in Korea

3.1. Cost of Financial Intermediation

3.2. Intermediated Asset and Unit Cost of Intermediation

3.3. Digital Transformation in Finance Sector

3.4. Digital Transformation and Unit Cost of Intermediation

4. Empirical Test and Result

4.1. Testing Methodology

4.2. Data and Statistics

4.3. Test Result

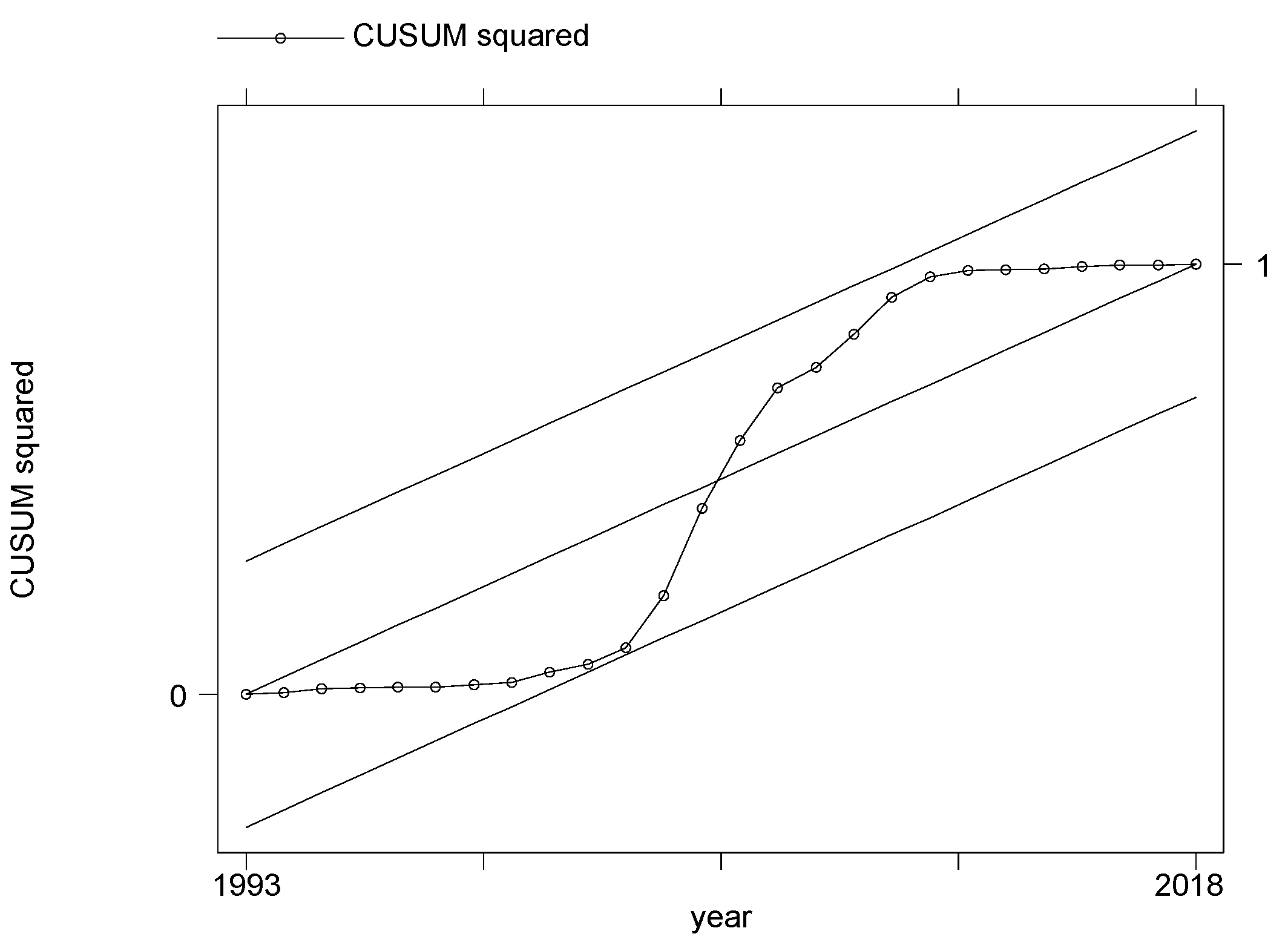

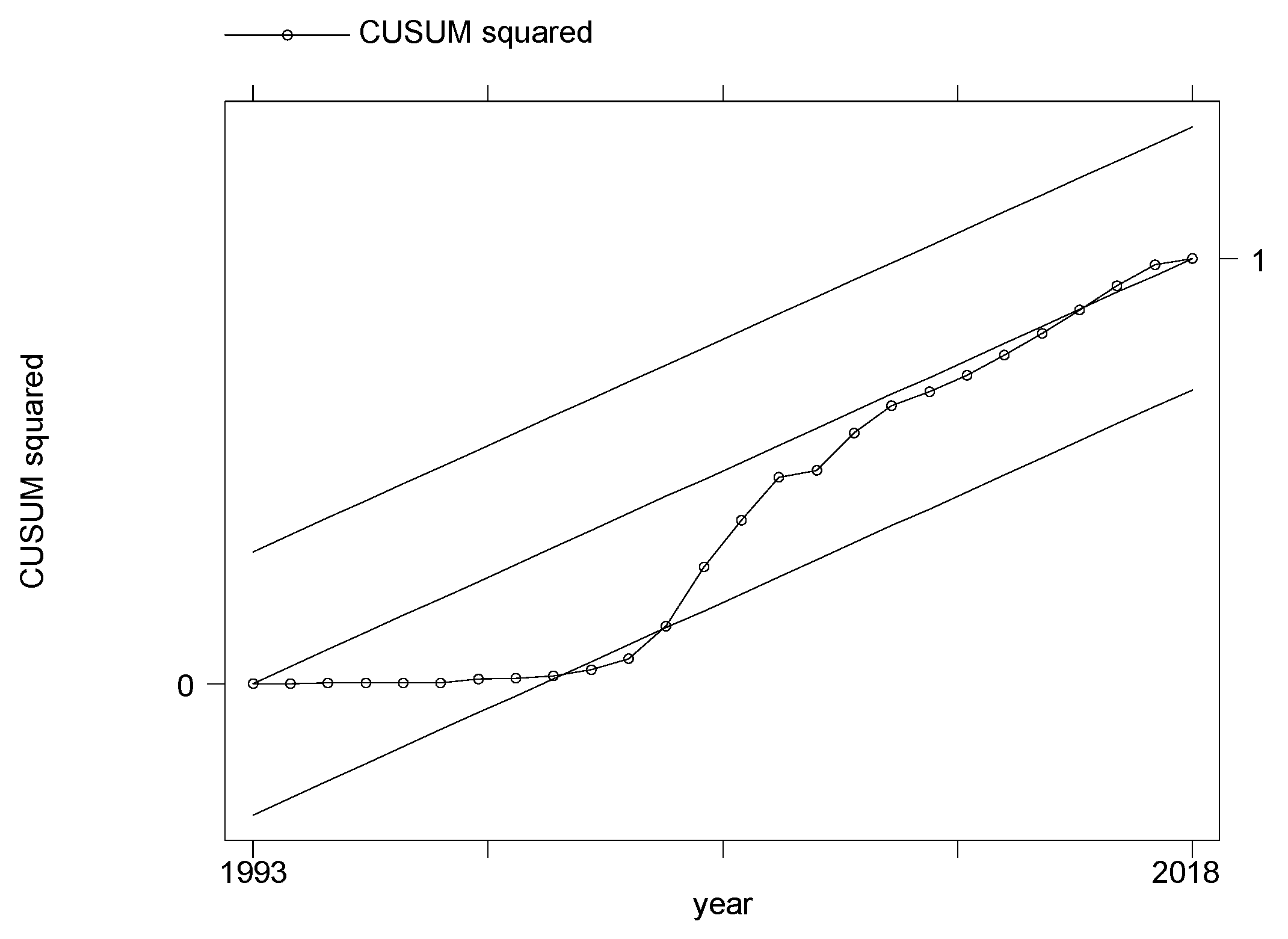

4.4. Robustness Check

4.5. Discussion and Policy Implication

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

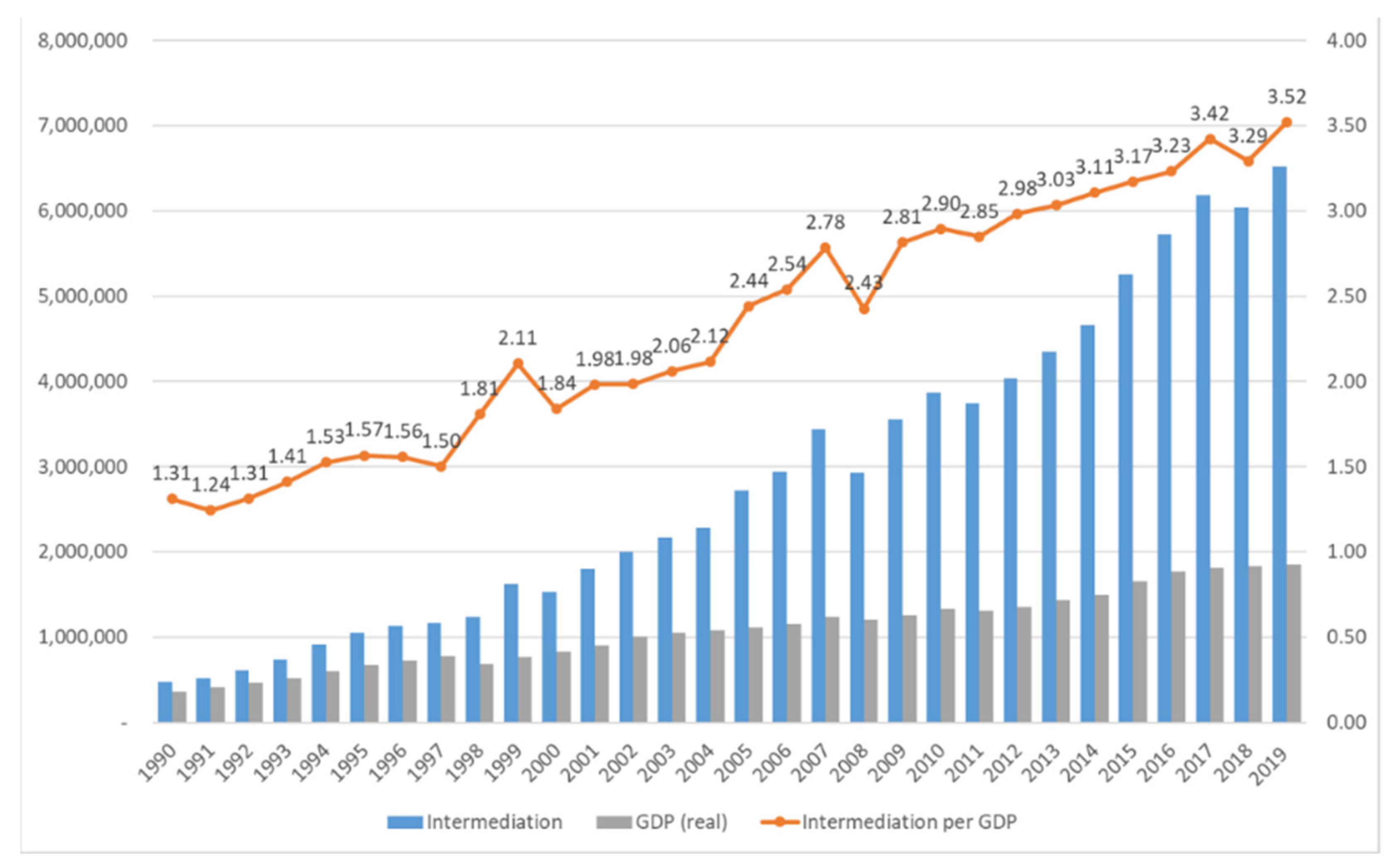

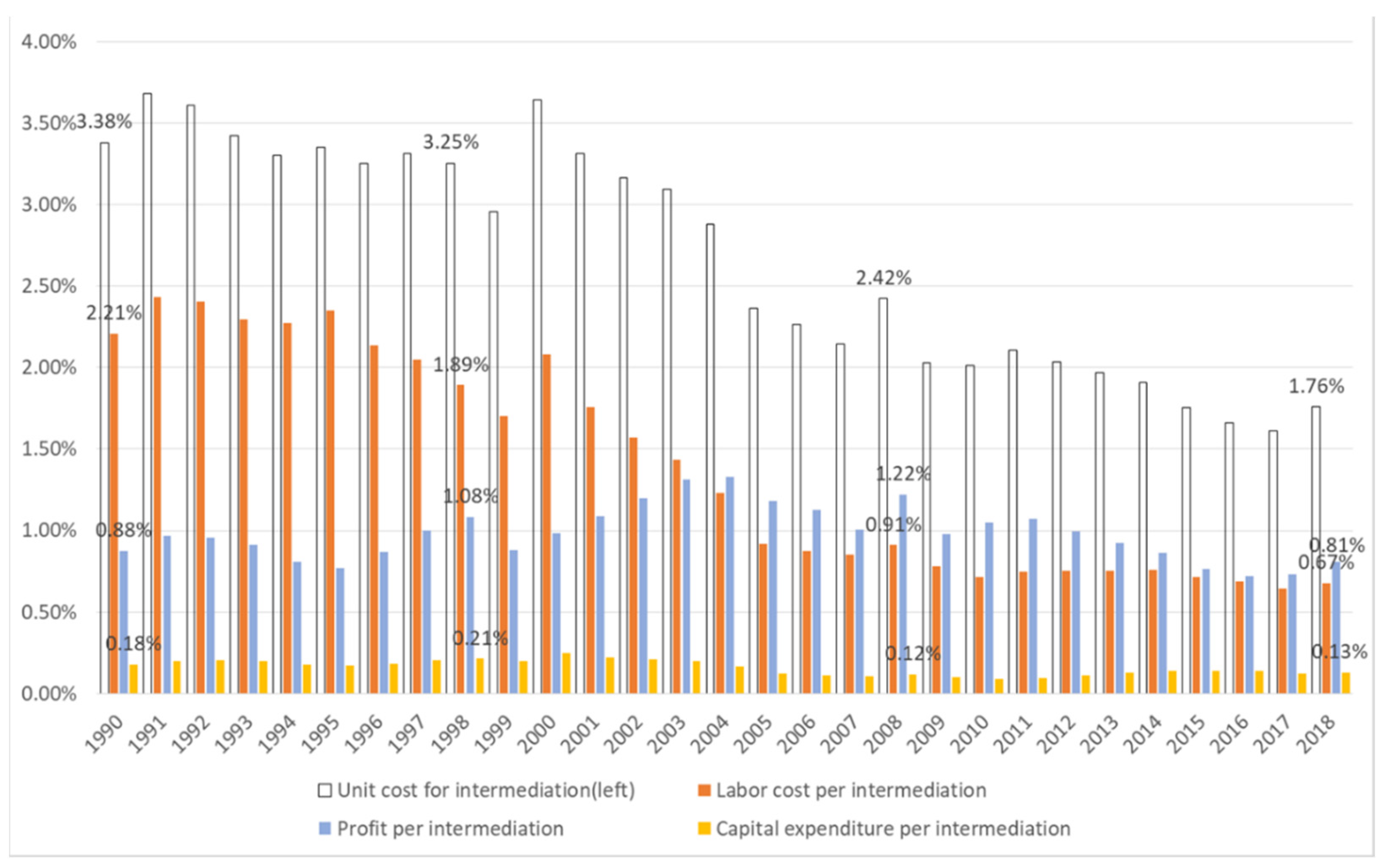

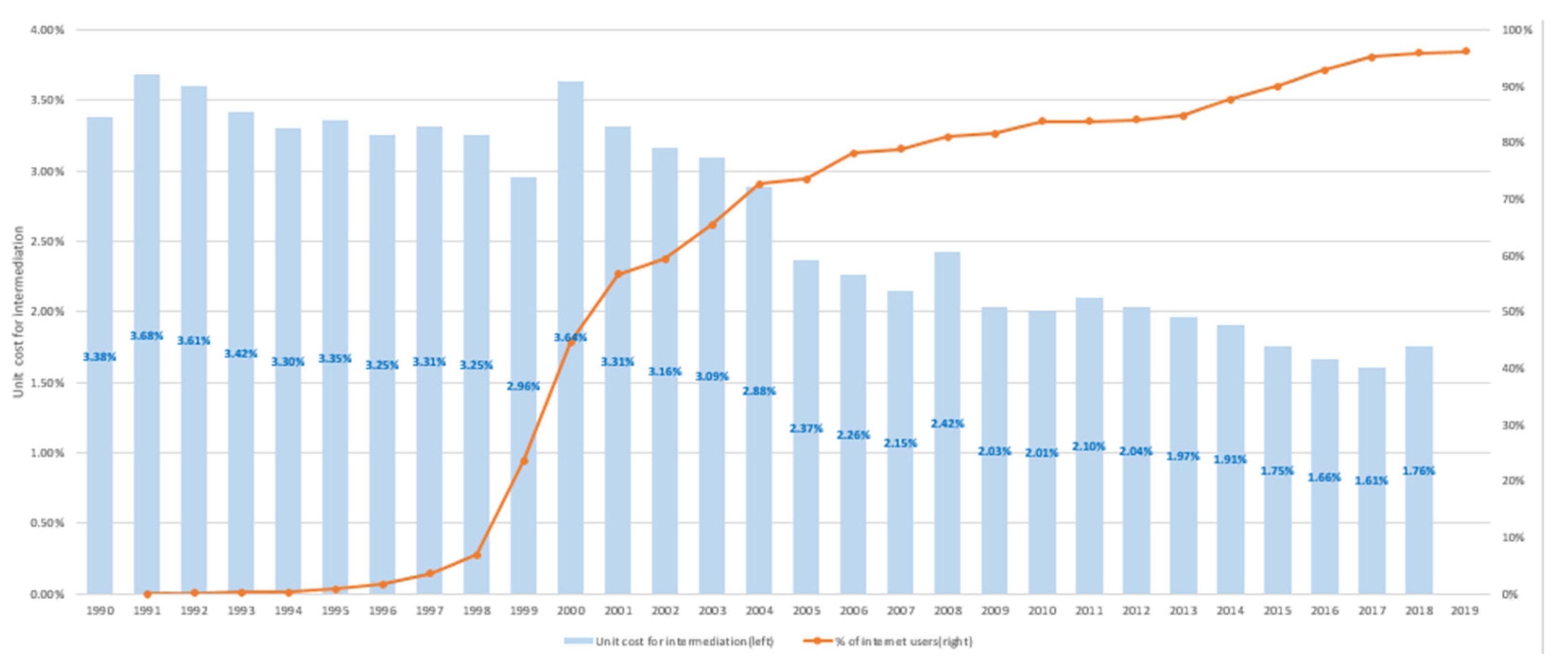

| 1 | |

| 2 | The size of household lending as a % of GDP has grown from 3.6% in 1975 to 99.1% in 2018; the size of insurance and pensions together has increased from 1.3% to 78.2% during the same period; and the total capitalization in the stock market has risen from 100% in 1997 to 1400% in 2018. |

| 3 | We selected the percentage of internet users as a proxy measure for the number of internet banking users and the number of mobile phone banking users as the latter two variables provide too short a period for analysis. The correlation measured between the percentage of internet users and the number of internet banking users is 0.883, and that between the percentage of internet users and the number of phone banking users is 0.891. |

References

- Arcand, Jean Louis, Enrico Berkes, and Ugo Panizza. 2012. Too Much Finance? IMF Working Paper 12/161. Washington, DC: IMF. [Google Scholar]

- Bank of Korea. 2020. National Account. Available online: https://kosis.kr/statHtml/statHtml.do?orgId=301&tblId=DT_111Y003&conn_path=I3 (accessed on 27 December 2020).

- Bank of Korea. 2021. Economic Statistics System. Available online: https://ecos.bok.or.kr/flex/EasySearch.jsp (accessed on 1 February 2021).

- Berg, Tobias, Valentin Burg, Ana Gombović, and Manju Puri. 2018. On the Rise of FinTechs—Credit Scoring using Digital Footprints. The Review of Financial Studies 33: 2845–97. [Google Scholar] [CrossRef]

- Brown, Robert L., James Durbin, and James M. Evans. 1975. Techniques for testing the constancy of regression relationships over time (with discussion). Journal of the Royal Statistical Society. Series B 37: 149–92. [Google Scholar]

- Buchak, Greg, Gregor Matvos, Tomasz Piskorski, and Amit Seru. 2017. Fintech, Regulatory Arbitrage, and the Rise of Shadow Banks (NBER Working Paper 23288). Journal of Financial Economics 130: 453–83. [Google Scholar] [CrossRef]

- Cecchetti, Stephen, and Enisse Kharroubi. 2012. Reassessing the Impact of Finance on Growth. BIS WP 381. Basel: Bank for International Settlements. [Google Scholar]

- Chamley, Christophe, Laurence J. Kotlikoff, and Herakles Polemarchakis. 2012. Limited-purpose banking–moving from “trust me” to “show me” banking. American Economic Review 102: 113–19. [Google Scholar] [CrossRef] [Green Version]

- Chava, Sudheer, and Nikhil Paradkar. 2018. Winners and Losers of Marketplace Lending: Evidence from Borrower Credit Dynamics. Georgia Tech Working Paper 18-16. Atlanta: Georgia Institute of Technology. [Google Scholar]

- Cho, Man. 2021. FinTech Megatrends: An Assessment of Their Industrial and Welfare Implications. International Review of Financial Consumers 6: 1. [Google Scholar]

- Cho, Man, and Soojin Park. 2021. Financial Consumer Protection in the Era of Digital Transformation: A Critical Survey of Literature and Policy Practices. KDI School of Pub Policy & Management Paper No. DP21-04. March 20. Available online: https://ssrn.com/abstract=3914573 (accessed on 5 January 2021).

- Cho, Man, Seung Dong You, and Young Man Lee. 2017. Financial Consumer Protection in the Household Lending Sector: An Assessment of the Korean Experience. The International Review of Financial Consumers 2: 15–23. [Google Scholar] [CrossRef]

- Citi Global Perspectives and Solutions. 2018. BANK OF THE FUTURE: The ABCs of Digital Disruption in Finance. March. Available online: http://www.smallake.kr/wp-content/uploads/2018/05/AHDX6.pdf (accessed on 5 January 2021).

- Cochrane, John H. 2014. Toward a run-free financial system. In Across the Great Divide: New Perspectives on the Financial Crisis. Edited by Martin Neil Baily and John B. Taylor. Stanford: Hoover Press. [Google Scholar]

- Cournède, Boris, and Oliver Denk. 2015. Finance and Economic Growth in OECD and G20 Countries. OECD Economics Department Working Papers No. 1223. ECO/WKP(2015)41. Paris: OECD. [Google Scholar]

- De Roure, Calebe, Loriana Pelizzon, and Anjan V. Thakor. 2021. P2P Lenders versus Banks: Cream Skimming or Bottom Fishing? SAFE Working Paper No. 206, Michael J. Brennan Irish Finance Working Paper Series. Research Paper No. 18-13. Available online: https://ssrn.com/abstract=3174632 (accessed on 5 January 2021).

- DiMaggio, Marco, and Vincent Yao. 2018. Fintech Borrowers: Lax-Screening or Cream Skimming? Available online: https://ssrn.com/abstract=3224957 (accessed on 5 January 2021).

- Engle, Robert F., and Clive W. J. Granger. 1987. Co-integration and error correction: Representation, estimation, and testing. Econometrica 55: 251–76. [Google Scholar] [CrossRef]

- Freedman, Seth, and Ginger Zhe Jin. 2017. The Information Value of Online Social Networks: Lessons from Peer-to-Peer Lending. International Journal of Industrial Organization 51: 185–222. [Google Scholar] [CrossRef]

- Frost, Jon, Leonardo Gambacorta, Yi Huang, Hyun Song Shin, and Pablo Zbindenn. 2019. BigTech and the Changing Structure of Financial Intermediation. BIS Working Papers No 779. Available online: https://www.bis.org/publ/work779.htm (accessed on 5 January 2021).

- Fuster, Andreas, Matthew Plosser, Philipp Schnabl, and James Vickery. 2018. The Role of Technology in Mortgage Lending. NBER Working Paper 24500. Cambridge: NBER. [Google Scholar]

- G20/OECD/INFE. 2017. G20/OECD INFE Report on Adult Financial Literacy in G20 Countries. Paris: OECD. [Google Scholar]

- Graessley, Scott, Jakub Horak, Maria Kovacova, Katarina Valaskova, and Milos Poliak. 2019. Consumer Attitudes and Behaviors in the Technology-Driven Sharing Economy: Motivations for Participating in Collaborative Consumption. Journal of Self-Governance and Management Economics 7: 25–30. [Google Scholar] [CrossRef] [Green Version]

- Hassler, Uwe, and Jürgen Wolters. 2006. Autoregressive distributed lag models and cointegration. Allgemeines Statistisches Archiv 90: 59–74. [Google Scholar] [CrossRef] [Green Version]

- Hildebrand, Thomas, Manju Puri, and Jörg Rocholl. 2017. Adverse Incentives in Crowdfunding. Management Science 63: 587–608. [Google Scholar] [CrossRef] [Green Version]

- International Monetary Fund (IMF). 2017. Fintech and Financial Services: Initial Considerations. Staff Discussion Notes No. SDNEA2017005. Washington, DC: IMF. [Google Scholar]

- Ionescu, Luminiţa. 2020a. Digital Data Aggregation, Analysis, and Infrastructures in FinTech Operations. Review of Contemporary Philosophy 19: 92–98. [Google Scholar] [CrossRef]

- Ionescu, Luminiţa. 2020b. The Economics of the Carbon Tax: Environmental Performance, Sustainable Energy, and Green Financial Behavior. Geopolitics, History, and International Relations 12: 101–7. [Google Scholar] [CrossRef]

- Ionescu, Luminiţa. 2021a. Transitioning to a Low-Carbon Economy: Green Financial Behavior, Climate Change Mitigation, and Environmental Energy Sustainability. Geopolitics, History, and International Relations 13: 86–96. [Google Scholar] [CrossRef]

- Ionescu, Luminiţa. 2021b. Leveraging Green Finance for Low-Carbon Energy, Sustainable Economic Development, and Climate Change Mitigation during the COVID-19 Pandemic. Review of Contemporary Philosophy 20: 175–86. [Google Scholar] [CrossRef]

- Iyer, Rajkamal, Asim Ijaz Khwaja, Erzo F. P. Luttmer, and Kelly Shue. 2016. Screening Peers Softly: Inferring the Quality of Small Borrowers. Management Science 62: 1554–77. [Google Scholar] [CrossRef] [Green Version]

- Jagtiani, Julapa, and Catharine Lemieux. 2019. The Roles of Alternative Data and Machine Learning in Fintech Lending: Evidence from the LendingClub Consumer Platform (Philadelphia Fed Working Paper). Financial Management 48: 1009–29. [Google Scholar] [CrossRef]

- King, Robert G., and Ross Levine. 1993. Finance and Qrowth: Schumpeter Might be Right. Quarterly Journal of Economics 108: 713–37. [Google Scholar] [CrossRef]

- Korea Statistics Information System (KSIS). 2021. Available online: https://kosis.kr/statHtml/statHtml.do?orgId=101&tblId=DT_2KAAA13&conn_path=I3 (accessed on 20 January 2021).

- Le, Tu D. Q., Tin H. Ho, Dat T. Nguyen, and Thanh Ngo. 2021. Fintech Credit and Bank Efficiency: International Evidence. International Journal of Financial Studies 9: 44. [Google Scholar] [CrossRef]

- Lin, Mingfeng, Nagpurnanand R. Prabhala, and Siva Viswanathan. 2013. Judging Borrowers by the Company They Keep: Friendship Networks and Information Asymmetry in Online Peer-to-Peer Lending. Management Science 59: 17–35. [Google Scholar] [CrossRef]

- Manning, Mark J. 2003. Finance Causes Growth: Can We Be So Sure? The B.E. Journal of Macroeconomics 3: 1–24. [Google Scholar] [CrossRef]

- Narayan, Paresh Kumar. 2005. The saving and investment nexus for China: Evidence from cointegration tests. Applied Economics 37: 1979–90. [Google Scholar] [CrossRef]

- Odedokun, Matthew O. 1996. Alternative econometric approaches for analysing the role of the financial sector in economic growth: Time-series evidence from LDCs. Journal of Development Economics 50: 119–46. [Google Scholar] [CrossRef]

- Organization of Economic Cooperation and Development (OECD). 2019. The Digital Innovation Policy Landscape in 2019. OECD Science, Technology and Innovation Policy Papers, May 2019 No. 71. Available online: https://www.oecd-ilibrary.org/science-and-technology/the-digital-innovation-policy-landscape-in-2019_6171f649-en (accessed on 5 January 2021).

- Pagano, Marco, and Giovanni Pica. 2012. Finance and Employment. Economic Policy 27: 5–55. [Google Scholar] [CrossRef]

- Pennachi, George. 2012. Narrow banking. Annual Review of Financial Economics 4: 141–159. [Google Scholar] [CrossRef]

- Pesaran, M. Hashem, and Yongcheol Shin. 1999. An Autoregressive Distributed Lag Modelling Approach to Cointegration Analysis. In Econometrics and Economic Theory in the 20th Century: The Ragnar Frisch Centennial Symposium. Edited by Steinar Strøm. Cambridge: Cambridge University Press. [Google Scholar]

- Pesaran, M. Hashem, Yongcheol Shin, and Richard J. Smith. 2001. Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics 16: 289–326. [Google Scholar] [CrossRef]

- Philippon, Thomas. 2015. Has the us finance industry become less efficient? on the theory and measurement of financial intermediation. The American Economic Review 105: 1408–38. [Google Scholar] [CrossRef] [Green Version]

- Philippon, Thomas. 2016. The Fintech Opportunity. NBER Working Paper No. w22476. Available online: https://ssrn.com/abstract=2819862 (accessed on 5 January 2021).

- Priem, Randy. 2021. An Exploratory Study on the Impact of the COVID-19 Confinement on the Financial Behavior of Individual Investors. Economics, Management, and Financial Markets 16: 9–40. [Google Scholar] [CrossRef]

- Puri, Manju, Jörg Rocholl, and Sascha Steffen. 2017. What do a million observations have to say about loan defaults? Opening the black box of relationships. Journal of Financial Intermediation 31: 1–15. [Google Scholar] [CrossRef]

- Rajan, Raghuram, and Luigi Zingales. 1998. Financial Dependence and Growth. American Economic Review 88: 559–86. [Google Scholar]

- Stamatiou, Pavlos P., and Nikolaos Dritsakis. 2014. The impact of Foreign Direct Investment on the Unemployment Rate and Economic Growth in Greece: A Time Series Analysis. Paper presented at International Work-Conference on Time Series Analysis (ITISE), Granada, Spain, 25–27 September; vol. 1, pp. 97–108. [Google Scholar]

- The World Bank. 2012. Good Practices for Financial Consumer Protection. Washington, DC: The World Bank. [Google Scholar]

- The World Bank. 2019. Last updated in 27 February 2019. The G20 Basic Set of Financial Inclusion Data Repository. Available online: https://databank.worldbank.org/reports.aspx?source=g20-basic-set-of-financial-inclusion-indicators (accessed on 1 March 2021).

- The World Bank. 2021. Global Partnership for Financial Inclusion. G20 Financial Inclusion Indicators|Home|The World Bank. Available online: https://datatopics.worldbank.org/g20fidata/ (accessed on 21 January 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Name of Variables | Mean | Description | Unit |

|---|---|---|---|

| VAF | Value add in finance industry | Value add of financial industry * selected from national accounts of Korea | billion Korea Won |

| Labor | Labor cost | Labor cost among VAF, selected from national accounts of Korea | billion Korea Won |

| Profit | Profit | Profit among VAF, selected from national accounts of Korea | billion Korea Won |

| Capex | Capital expenditure | Capital expenditure among VAF, selected from national accounts of Korea | billion Korea Won |

| Tax | Tax | Tax among VAF, selected from national accounts of Korea | billion Korea Won |

| GDP_growth | GDP growth rate | GDP growth rate in Korea (year to year) | percent |

| Empl | Number of employees | Thousand number of employees in financial industry of Korea | thousand people |

| Wage | Total wage of financial industry | Total sum of wages in financial industry of Korea | billion Korea Won |

| Intermedi | Intermediated asset of financial industry | Scale of financial services, measured by the liquidity aggregate (L) minus monetary base (M0) plus market cap of stock in Korea | billion Korea Won |

| Internet | Number of internet banking users | Thousand people of internet banking users in Korea | thousand people |

| Mobile | Number of mobile banking users | Thousand people of mobile phone banking users in Korea | thousand people |

| user_internet | Percentage of internet users | Percentage of internet users in Korea | percent |

| Variable | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| cost_intermedi | 29 | 2.6810 | 0.7122 | 1.61 | 3.64 |

| labor_intermedi | 29 | 1.4041 | 0.6773 | 0.64 | 2.34 |

| capex_intermedi | 29 | 0.1596 | 0.0470 | 0.08 | 0.24 |

| user_internet | 30 | 54.0933 | 38.1594 | 0.00 | 96.20 |

| gdp_grow | 30 | 5.1833 | 3.4747 | −5.10 | 11.50 |

| internetb | 15 | 52,792.93 | 31,511.59 | 10,918 | 109,760 |

| wage_empl | 29 | 42.3806 | 10.6291 | 23.53 | 59.53 |

| Model # | Dependent Variable | Independent Variable | Selected Lag Orders (p, q) | Bounds Test | |

|---|---|---|---|---|---|

| F-Test Result | t-Test Result | ||||

| 1 | labor_intermedi | user_internet | (2, 3) | 6.507 ** | −3.314 ** |

| 2 | capex_intermedi | user_internet | (2, 3) | 6.233 ** | −3.522 ** |

| 3 | cost_intermedi | user_internet | (1, 3) | 10.050 *** | −4.444 *** |

| D.labor_Intermedi | Adjustment | Long Run | Short Run |

|---|---|---|---|

| VARIABLES | |||

| LD.labor_intermedi | 0.614 *** | ||

| (0.141) | |||

| D.user_internet | 0.0153 *** | ||

| (0.00354) | |||

| LD.user_internet | −0.00787 | ||

| (0.00551) | |||

| L2D.user_internet | 0.0102 * | ||

| (0.00507) | |||

| L.labor_intermedi | −0.433 *** | ||

| (0.131) | |||

| user_internet | −0.0168 *** | ||

| (0.000920) | |||

| Constant | 0.933 *** | ||

| (0.296) | |||

| Observations | 26 | 26 | 26 |

| R-squared | 0.747 | 0.747 | 0.747 |

| D.capex_Intermedi | Adjustment | Long Run | Short Run |

|---|---|---|---|

| VARIABLES | |||

| LD.capex_intermedi | 0.538 *** | ||

| (0.159) | |||

| D.user_internet | 0.00203 *** | ||

| (0.000702) | |||

| LD.user_internet | −0.000755 | ||

| (0.000826) | |||

| L2D.user_internet | 0.00163 * | ||

| (0.000805) | |||

| L.capex_intermedi | −0.450 *** | ||

| (0.128) | |||

| user_internet | −0.000955 *** | ||

| (0.000152) | |||

| Constant | 0.0852 *** | ||

| (0.0242) | |||

| Observations | 26 | 26 | 26 |

| R-squared | 0.634 | 0.634 | 0.634 |

| D.cost_Intermedi | Adjustment | Long Run | Short Run |

|---|---|---|---|

| VARIABLES | |||

| D.user_internet | 0.0246 *** | ||

| (0.00616) | |||

| LD.user_internet | −0.00157 | ||

| (0.00797) | |||

| L2D.user_internet | 0.0168 ** | ||

| (0.00744) | |||

| L.cost_intermedi | −0.498 *** | ||

| (0.112) | |||

| user_internet | −0.0180 *** | ||

| (0.00131) | |||

| Constant | 1.643 *** | ||

| (0.383) | |||

| Observations | 26 | 26 | 26 |

| R-squared | 0.624 | 0.624 | 0.624 |

| Tests | Model 1 | Model 2 | Model 3 | |||

|---|---|---|---|---|---|---|

| Test Value | Decision | Test Value | Decision | Test Value | Decision | |

| Durbin–Watson (d-statistic) | 1.9073 | No autocorrelation | 1.997 | No autocorrelation | 1.8520 | No autocorrelation |

| Breusch–Godfrey LM test (Prob > chi2) | 0.9072 | No serial correlation | 0.7529 | No serial correlation | 0.3095 | No serial correlation |

| White test (Prob > chi2) | 0.4076 | No heteroskedasticity | 0.4070 | No heteroskedasticity | 0.6799 | No heteroskedasticity |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Park, S.; Kesuma, P.E.; Cho, M. Did Financial Consumers Benefit from the Digital Transformation? An Empirical Investigation. Int. J. Financial Stud. 2021, 9, 57. https://doi.org/10.3390/ijfs9040057

Park S, Kesuma PE, Cho M. Did Financial Consumers Benefit from the Digital Transformation? An Empirical Investigation. International Journal of Financial Studies. 2021; 9(4):57. https://doi.org/10.3390/ijfs9040057

Chicago/Turabian StylePark, Soojin, Prida Erni Kesuma, and Man Cho. 2021. "Did Financial Consumers Benefit from the Digital Transformation? An Empirical Investigation" International Journal of Financial Studies 9, no. 4: 57. https://doi.org/10.3390/ijfs9040057

APA StylePark, S., Kesuma, P. E., & Cho, M. (2021). Did Financial Consumers Benefit from the Digital Transformation? An Empirical Investigation. International Journal of Financial Studies, 9(4), 57. https://doi.org/10.3390/ijfs9040057