1. Introduction

The tremendous uncertainty and challenges of recent years, which have included the economic shocks generated by the COVID-19 pandemic and the Russia–Ukraine War, as well as the unstable international political situation, have significantly changed, and continue to change, the conditions for economic activity in multiple sectors. Further, they have had an impact on economic processes worldwide. Such circumstances make it increasingly challenging for governments and businesses to make predictions and plan for the future, which then impacts their ability to influence individuals’ outlook on the future and perception of the current situation.

While researchers have made efforts to examine the effect of a range of recent economic crises, the range of research remains limited due to the lack of comprehensive and up-to-date data, resulting in a concentration on the COVID-19 economic crisis. The health crisis became a global economic crisis as a result of globalization and internationalization. These had a profound effect on the world and created new relationships and possibilities for interaction and the development of innovative business ideas and products, traveling, and creating opportunities to share achievements and coincidences, either positive or negative. The COVID-19 pandemic is a good illustration of the interfaces of the world. It impacted multiple sectors and a range of countries, most of which are still dealing with the consequences, and businesses had to find a way to survive under the strict requirements of quarantine and new conditions. The crisis impacted the economy of every country and changed the typical routine of every person and company, no matter their size, type of activity, or other parameters (

Subačienė et al. 2022).

From the beginning of the COVID-19 crisis, professional bodies started to publish recommendations and insights on performance, reporting, auditing, and other issues related to the crisis. These included assessments of going concern, adjustments of post-balance sheet events and review periods, disclosures in management reports, effects on auditing financial statements, and other issues (

Coronavirus Crisis: Implications on Reporting and Auditing 2020). In addition, scholars have investigated the impact and consequences of the crisis in different spheres.

Rinaldi (

2022) conducted a systematic literature analysis of 135 articles from journals listed in the Academic Journal Guide, classified as “2”, “3”, or “4”. The analysis summarized the concentration of research results on budgetary and fiscal measures, broader accountability trends, disruptions in higher education, the transition and change of teaching and assessment methods, changes in accounting education, various approaches governments and public services took to understand and respond to emergencies related to the pandemic, the pandemic’s impact on financial markets, and the need for high-quality information for stakeholders.

Rybnikova et al. (

2022) investigated digitalization and e-leadership in local government before COVID-19 and concluded that even in the pre-pandemic period, an overall positive attitude toward digitalization and e-leadership had already been established. However, the authors revealed challenges associated with the need for suitable training, difficulties in establishing an appropriate work–life balance, and disparities between traditional organizational culture and digitalization.

Lăzăroiu et al. (

2023) investigated the recent boost of artificial intelligence and cloud computing technologies. The authors provided their opinion that by integrating blockchain and cloud computing technologies, AI algorithms, and big data analytics, fintech development enables organizational innovation by mitigating information asymmetry and financing limitations. They also noted that fintech optimizes financial organizations and services, economic structures and growth, data analysis, and digital banking performance through effective decision-making, coherent interconnectivity, and operational efficiency across entrepreneurial ecosystems. This results in increased financial accessibility and inclusion, and in risk mitigation in relation to bitcoin and automated trading. They concluded that the fintech-based banking sector integrates blockchain technology across digital finance, cryptocurrencies, transaction services, and loan risk management, leading to innovative economic growth.

Andronie et al. (

2023) analyzed Big Data management algorithms in artificial Internet of Things-based fintech and, under systematic review, stated that fintech-based banking management optimizes operational decision-making, risk assessment, efficiency, performance, forecasting, and regulation by using machine learning algorithms in financial and lending services. The authors concluded that fintech can articulate an extensive data system concerning companies’ financial and non-financial input to assist lenders in advancing heterogeneous customized financial products, decreasing the financial service threshold as enterprises can acquire inexpensive and accessible financial services effortlessly. Analysis and boosting of such possibilities may significantly increase the development of business and financial health in different economic cycles.

The purpose of this study is to evaluate accounting specialists’ perceptions of the changes in the efficiency of employees and companies and changes in several main performance indicators during economic crises, such as COVID-19. The study has the following objectives: (1) analyzing the changes in work conditions under quarantine and non-quarantine regimes; (2) evaluating the changes in employee work efficiency, and (3) assessing the changes in the performance efficiency of companies according to the perception of accounting specialists and actual statistical data.

The results of the study contribute to ongoing research examining the consequences of economic crises such as COVID-19. The findings show evidence of a broader transformation in the format of work (from office-based work to online work arrangements) even prior to this crisis, and this trend has since accelerated as a result. In addition, the study reveals changes in work efficiency in the changed work format as well as the comparison of perceptions of companies’ efficiency in the early phases of the economic crisis with actual data of financial ratios.

Kliestik et al. (

2020) indicate that financial ratios play an important role in revealing corporate financial soundness, a role which helps to maintain the competitive position of an enterprise, with the achievement of stable development contributing to the elimination of potential financial risks. The authors state that the enterprises with a financial health-oriented strategy can enjoy a competitive advantage. Financial ratios have traditionally been indicators of overall corporate performance and may help quantify the potential impact of internal ratings on financial performance; measuring and assessing the financial ratios help to create a competitive advantage for an enterprise.

2. Analysis of Literature

Scholars started to investigate economic shocks when the COVID-19 pandemic was first declared, as it prompted a previously unknown social and economic phenomenon with a significant global impact. Following the COVID-19 crisis, the world was rocked by the Russia–Ukraine war, which again changed economic relationships between countries and companies and caused serious problems, such as hikes in energy prices, broken supply chains, and others. The impact of recent economic shocks is still under evaluation, but various aspects of the COVID-19 crisis have been analyzed and evaluated.

An analysis of the literature was carried out using the bibliometric analysis method. It took several stages, presented in

Figure 1. The scientific literature was examined and analyzed manually (

Rinaldi 2022) by employing the Web of Science (Clarivate Analytics) database using the initial search criteria ‘economic shocks.’ The search was continued by adding keywords (‘COVID-19’ AND ‘war’) in several Web of Science categories (‘Economics’ or ‘Business Finance’ or ‘Management’) and searching within all fields related to ‘Business Efficiency’; this generated 383 papers for the last five years (2019–2023). Bibliometric visualization was carried out by VOSviewer. However, the search did not reveal any literature on the perception of changes in efficiency. Consequently, the carried-out research fills the gap in understanding the perception of accounting specialists regarding changes in efficiency during the COVID-19 economic crisis. The study contributes valuable insights into the multifaceted impact of the crisis on the efficiency dynamics and expands the current knowledge base on unprecedented economic challenges.

The first step of the literature review consists of an analysis of the 10 most highly cited publications in the field. Although the search included a wide range of economic crises involving the COVID-19 global pandemic and the Russia–Ukraine war, the studies analyzed were nonetheless concentrated on the topic of the COVID-19 economic crisis. This may be because the initiation of the Russia–Ukraine war was so recent (24 February 2022), and it takes time to move through the research, writing, and publication process.

The analysis of the top 10 most highly cited articles reveals several trends. First, there is a tendency to focus on issues related to financial markets and financial institutions.

Yarovaya et al. (

2021) investigated the impact of human capital efficiency on the performance of equity funds during three stages of the COVID-19 pandemic. The authors analyzed data for 799 open-ended equity funds across five EU countries, comparing their performance in terms of human capital efficiency and ranking them in five categories from high to low. The results suggest that during the COVID-19 outbreak, the equity funds that were ranked higher in human capital efficiency outperformed their counterparts.

Naeem et al. (

2021) investigated the comparative efficiency of green and conventional bond markets before and during the COVID-19 pandemic by applying asymmetric multifractal analysis. These scholars show that the degree of efficiency in green and conventional bond markets changes considerably over time, and the inefficiency of both increased substantially following the COVID-19 outbreak. However, the market for green bonds exhibited a higher level of efficiency during the COVID-19 crisis, showing the potential of these bonds to become effective diversifiers in times of extreme market turmoil for investors in traditional assets.

Elnahass et al. (

2021) analyzed quarterly data for 1090 banks from 116 countries from 2019–2020. Their results show that, in the global banking sector, the COVID-19 outbreak has had detrimental impacts on financial performance in terms of various indicators of financial performance (i.e., accounting-based and market-based performance measures) and financial stability (i.e., high-risk indicators including default risk, liquidity risk, and asset risk). The authors considered various regions and countries (the US, China, and others) and different banks, considering the differential effects of the pandemic on alternative banking systems (i.e., conventional and Islamic); they identified a signal of the recovery for bank stability during the second quarter of 2020.

Li et al. (

2022) analyzed the link between COVID-19 fear and stock market volatility by using global daily volatility index statistics related to the COVID-19 pandemic. They found that with a 1% increase in COVID-19 cases, the stock return and GDP decreased by 0.8% and 0.56%, respectively. Public attention to the attitude of buying or selling was highly dependent on the reported cases, deaths, and global fear indexes. The authors recommended investment in gold rather than the stock market.

Another trend evident in the analysis of COVID-19’s impact is the inclusion of renewables, green energy and green technologies, different sectors, and recommendations for policy makers to gain public support tools to mitigate the consequences.

Zhao et al. (

2021) investigated firm-level pure innovation efficiency, green productivity, technical efficiency, scale efficiency, and total investment efficiency in the context of renewable energy. They explored the effectiveness of government subsidies and tax rebate policies on the investment efficiency of renewable energy firms using firm-level panel data for China’s renewable energy sector. The authors indicated that between 2001 and 2018, the aggregate degree of total investment performance from renewable energy firms rose steadily before declining. Current government subsidies and taxation rebates were found to have significant and positive effects on pure technological efficiency and total investment efficiency; additionally, government subsidies had a stronger positive impact on total investment efficiency and pure technical efficiency than taxation rebates.

Iqbal and Bilal (

2022) estimated the role of public support in energy-efficiency financing and presented a way to mitigate the energy-financing barriers raised during the COVID-19 crisis using data for G7 countries. The authors reported a consistent role for public support in indicators related to energy-efficiency financing during the COVID-19 crisis period. The authors concluded that during COVID-19, the G7 countries raised around 17% of funding through public support for energy efficiency financing, and raised 4% per unit energy usage to GDP, accelerated 16% energy efficiency and 24% output of renewable energy sources. The authors offered multiple policy recommendations to enhance energy efficiency through alternative sources, such as on-bill financing, direct energy-efficiency grants, guaranteed financial contracts for energy efficiency, and energy-efficiency credit lines, to mitigate the impact of the COVID-19 crisis and increase the financing of energy efficiency during structural crises.

Cui et al. (

2021) examined the impacts of the COVID-19 pandemic on China’s transport sectors and specified that the COVID-19 pandemic resulted in multiple shocks to transport sectors. These included supply-side shocks that raised the protective cost and reduced the sectors’ production efficiency, and demand-side shocks that reduced the demand of households and the productive sectors. The outputs of all transport sectors in China have been severely affected by the COVID-19 pandemic, with larger decreases in output in passenger transport than in the freight sector. The supply-side shocks of the pandemic drove output decline in the railway, waterway, and aviation transport sectors. The demand-side shocks impacted the road, pipeline, and other transport sectors.

Cui et al. (

2021) concluded that the COVID-19 pandemic had negative impacts on the output of most non-transport sectors and the macro-economy in China, and made policy recommendations to mitigate the damage caused to the transport sectors. These recommendations included more generous supporting policies for the passenger transport sector, as they showed much larger negative impacts than any other sector. The supporting policies for freight transport should focus on alleviating production costs and easing their shortage of funds, encouraging them to resume and maintain production. Furthermore, the government should stimulate the demand for transportation by accelerating the resumption of industrial production and encouraging investment and consumption through fiscal and monetary policy interventions.

Zhao et al. (

2022) tested the role of renewable energy financing in addressing climate change, and presented the implications for the key stakeholders in pursuing a post-pandemic recovery in Asian and, specifically, ASEAN economies. The authors found that higher energy consumption and an increase in environmental pollution have resulted in substantial changes in the economic climate in these economies, and modern and renewable energy sources are recommended for climate change mitigation. The authors suggested pooling the funds of different financial institutions, banks, and ministries in the renewable energy sectors to enhance energy efficiency, control climate change in the long run, and thereby obtain the desired outcomes.

Although some scholars have investigated other aspects of the impact of COVID-19,

Sharma et al. (

2021) explored the priorities for retail supply chains (RSCs) to align their business operations and strategies for the post-pandemic world. The authors found that the pandemic disruptions have placed intense pressure on retailers to deliver products to meet consumers’ changing behaviors in the purchase of essentials and other products. The authors identified ‘collaboration efficiency’ as the main criterion for accelerating the performance of RSCs in a dynamic social environment, concluding that ‘order fulfilment’ and ‘digital RSCs’ are the most appropriate and resilient business strategies to mitigate the long-term effects of the pandemic and ensure sustainability in the post-pandemic business world.

Parker (

2020) assessed how office and cost-control agendas intersect with corporate social accountability, and analyzed two sets of publicly available documents: published research in the scope of the investigation’s purpose, and web-based reports and articles regarding the observed and anticipated impacts of COVID-19 on office design and operation. The results revealed that office location, working processes, and controls were self-regulated and enacted by organizations and individual staff members as a socially disciplined response to government policies. In addition, management strategies reflect priorities and the choice between occupational health and safety or financial returns.

The second stage of the literature analysis focused on the identification of keywords for the 383-article list from the search phase. The VOSviewer tool was used to search for the keywords on the list of selected articles (limiting the minimum number of occurrences of the keywords to 10); see

Figure 2.

A further search was conducted using the keywords with the strongest links: COVID-19 (total link strength, 269; occurrences, 157; links, 31), efficiency (total link strength, 225; occurrences 102; links 30), performance (total link strength, 158; occurrences, 63; links, 27), and impact (total link strength, 162; occurrences, 60; 29 links). The process yielded 74 articles. A preliminary review of selected papers showed a concentration on macroeconomics and financial institutions. The search was focused on the Web of Science category ‘Business Finance’.

The results of the literature search were systemized by research object, topic, main research results, data employed, and research methods (see

Supplementary Table S1).

Figure 3 shows the main topics in the articles analyzed, with an emphasis on the investigation of efficiency or performance or the value of financial and non-financial institutions. The studies used various research methods, including descriptive statistical, regression, and ratio analysis, modeling, and survey questionnaires, and employed different sets of data from listed companies across industries and in different categories, banks, and stock exchanges.

The process of literature analysis shows that scholars have not investigated the perceptions of changes in the efficiency of employees and companies during the COVID-19 pandemic, and have not compared these perceptions with factual (actual) results. This emphasizes the novelty of the research topic. The literature analysis results show a variety of research methods and data sets, giving insights for conducting the survey questionnaire, and descriptive statistical and ratio analysis in the best way to reach the purpose of the study for the evaluation of accounting specialists’ perceptions of the changes in the efficiency of employees and companies and changes in the main performance indicators during economic crises, such as COVID-19.

4. Results

The analysis results regarding the possibility of working online in the ordinary and quarantine regimes show that 86% of respondents were able to work online under ordinary, non-crisis conditions; 49.1% could do so for more than 75% of their working time, and only 9.6% for up to a quarter of their working time. The possibility of remote working for accountants for more than 75% of their working time increased during the quarantine period by almost 7%. There were 2.1-percentage-point fewer respondents who reported that they were unable to work remotely even during the quarantine period, but the overall proportion of online work increased during the quarantine period, with 55.8% of respondents able to do so for more than 75% of their work time, and only 6.5% for up to a quarter of their time (see

Table S2). The Wilcoxon signed-rank test showed statistically significant differences (Z = −2.74,

p = 0.006) between the proportion of online work under normal and quarantine conditions; that is, there was an increase in the proportion of online work in the quarantine period compared to normal conditions.

There were statistically significant (χ

2 = 13.21,

p = 0.01) differences in these options between countries. In Lithuania, only 10.4% of accountants were unable to work online under normal conditions and in Latvia, this number was 17.1%. Around half of the accounting specialists in both countries could perform more than 75% of their work remotely. There were also statistically significant differences in the distribution of the share of online work during the quarantine between the countries (χ

2 = 14.42,

p = 0.006): in Lithuania, 65.4% of respondents were able to work online for more than 75% of their working time, compared to only 47.3% in Latvia. In Latvia, the number decreased by 2.4 percentage points compared to the business-as-usual options. The number of people unable to work online in the quarantine regime in Latvia and Lithuania decreased by 2.5 and 1.6 percentage points, respectively (see

Figure 4).

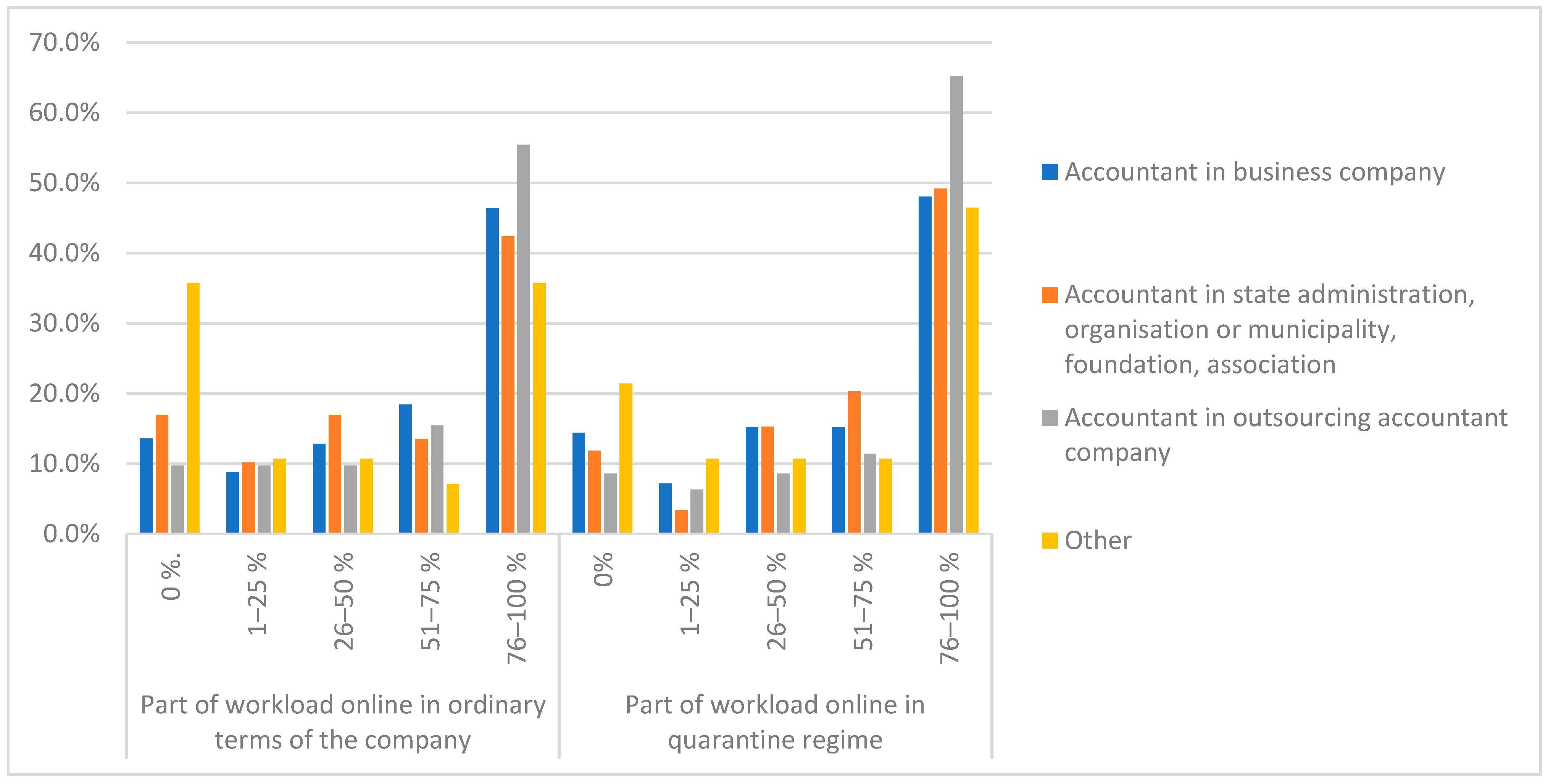

The possibility of working online under normal conditions also varied depending on the respondent’s current work position: 86.4% of businesses and 83.1% of accountants in the public sector indicated that they had this option, although the highest proportion (90.3%) of employees in accounting services companies had access to this option. During the quarantine period, these opportunities increased mostly for public sector accountants (5.1% points) and others (14.3% points). While the share of accounting staff able to work online for more than 75% of their time during the quarantine period and under normal conditions increased by only 1.6 percentage points in business enterprises, the share of accounting staff in accounting service providers increased by 6.8 percentage points, whereas the share of public sector employees increased by as much as 9.7 percentage points (see

Figure 5).

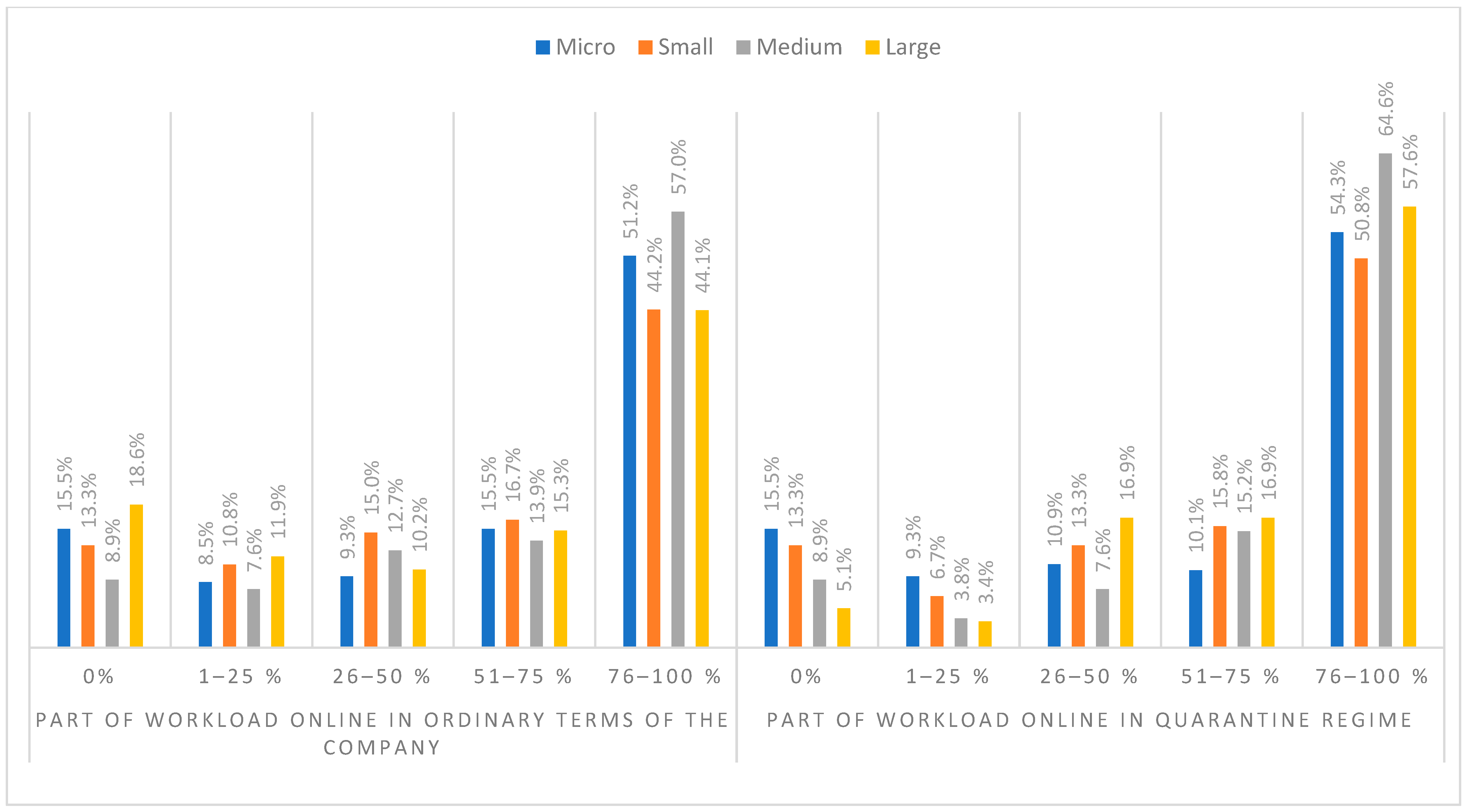

Accounting specialists in medium-sized companies had the highest chance of working online under normal conditions (91.1%), and employees in large companies had the lowest (81.4%). During the quarantine period and under ordinary conditions, the proportion of accounting specialists able to work online for more than 75% of their working time increased in companies of different sizes. This increase was more rapid in larger enterprises: while the share of such employees increased by 3.1% percentage points in micro-enterprises, it increased by 13.6% percentage points in large enterprises, with a corresponding decrease in the number of employees who could not work online in these enterprises before the quarantine. In other enterprises, the proportion of employees unable to work online remained the same (see

Figure 6).

However, there was no statistically significant relationship between an employee’s current work position and the distribution of the online share of work under normal conditions (χ2 = 23.91, p = 0.092) and during quarantine (χ2 = 20.89, p = 0.183) and between the distribution of the online share of work in enterprises of different sizes and the distribution of the online share of work under normal conditions (χ2 = 7.78, p = 0.802) and during quarantine (χ2 = 14.57, p = 0.266). We concluded that the country environment had an impact on the online work opportunities for accounting specialists both in ordinary and quarantine conditions, whereas enterprise size and current work position did not.

In terms of changes in the perceived efficiency of accounting specialists when working online under ordinary conditions, 32.6% of respondents indicated that their efficiency had increased compared to working in the office, 22.5% said it had decreased, and 26.1% said it had remained the same. Meanwhile, the efficiency of working online under quarantine conditions compared to working in an office was more evenly distributed: 28.5% of respondents reported an increase in efficiency, the same proportion reported a decrease, and a similar proportion (27.9%) reported no change (see

Table S3). The impact of quarantine conditions on the perceived online work efficiency was analyzed by the McNemar test, and binomial distribution was used. The impact of working online on the efficiency of work was compared when working online under ordinary and quarantine conditions. The McNemar test showed a statistically significant impact of quarantine conditions on the perceived online work efficiency of accounting specialists (

p = 0.02). A total of 165 respondents identified changes in perceived online efficiency under both normal and quarantine conditions. An increase in perceived online efficiency under normal conditions was reported by 103 respondents, while under quarantine, it was reported by only 85 respondents; a decrease in perceived online efficiency under normal conditions was reported by 62 respondents, while a decrease in perceived online efficiency under quarantine conditions was reported by 80 respondents (see

Table S4). According to the accounting specialists, quarantine conditions resulted in less of an increase in online working efficiency than under normal conditions.

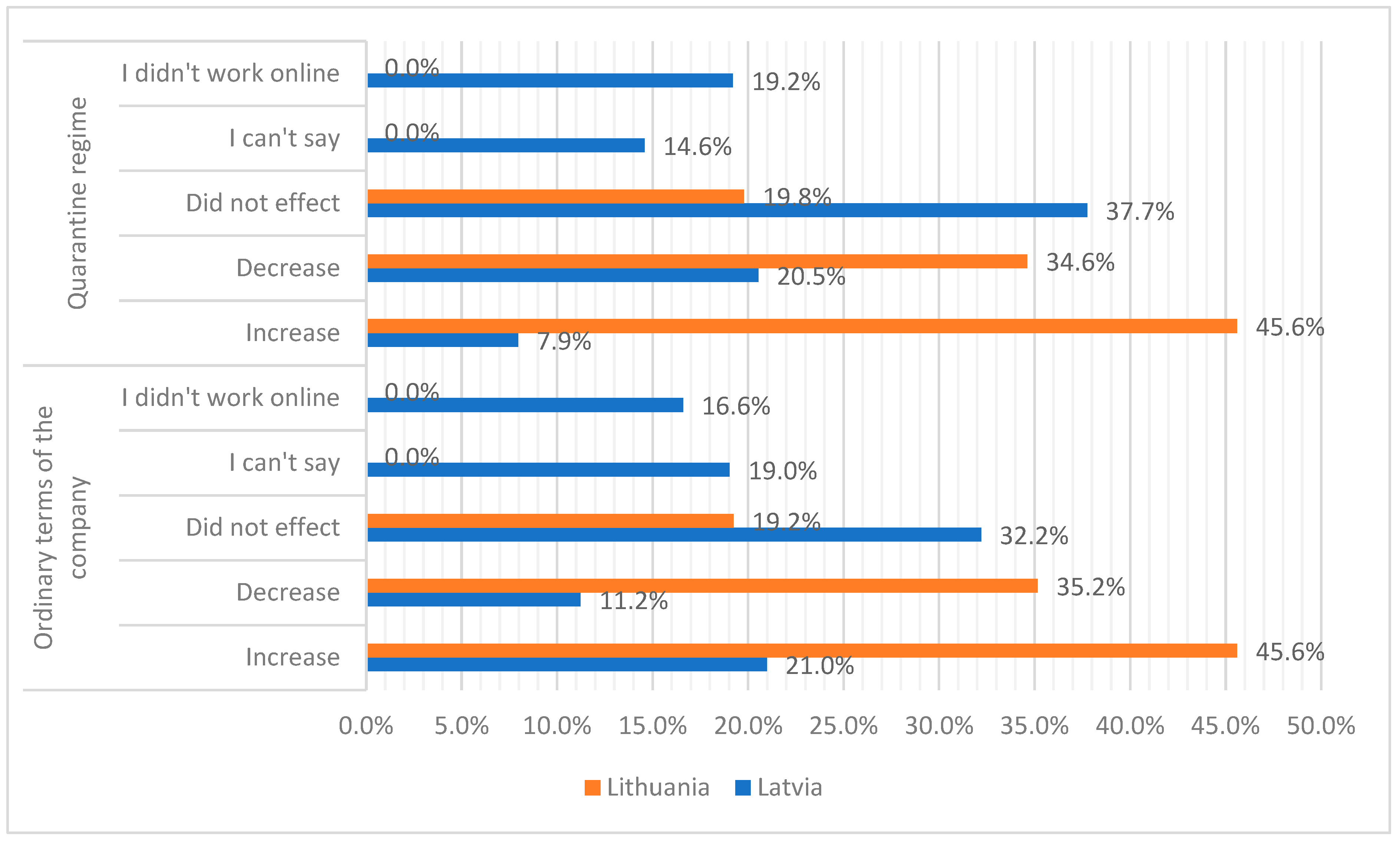

Statistically significant (χ

2 = 113.57,

p = 0.000) differences in attitudes towards changes in office and online efficiency were found for the countries surveyed: 45.6% of Lithuanian and 21% of Latvian respondents indicated an increase in efficiency, while 35.2% of Lithuanian and 11.2% of Latvian respondents indicated a decrease in efficiency under normal working conditions. Under quarantine conditions, the attitudes of the countries’ accounting specialists towards changes in efficiency also differed significantly (χ

2 = 117.83,

p = 0.000): 45.6% of Lithuanian and only 7.9% of Latvian respondents identified an increase in efficiency, while 34.6% of Lithuanian respondents and 20.5% of Latvian respondents identified a decrease in efficiency (see

Figure 7). A significantly higher proportion of Latvian respondents believed that working online had not affected their perceived effectiveness. Lithuanian accounting specialists did not perceive quarantine to have had any impact on their online performance, while Latvian respondents indicated a clear decrease in online performance under quarantine conditions compared to the company’s normal working conditions.

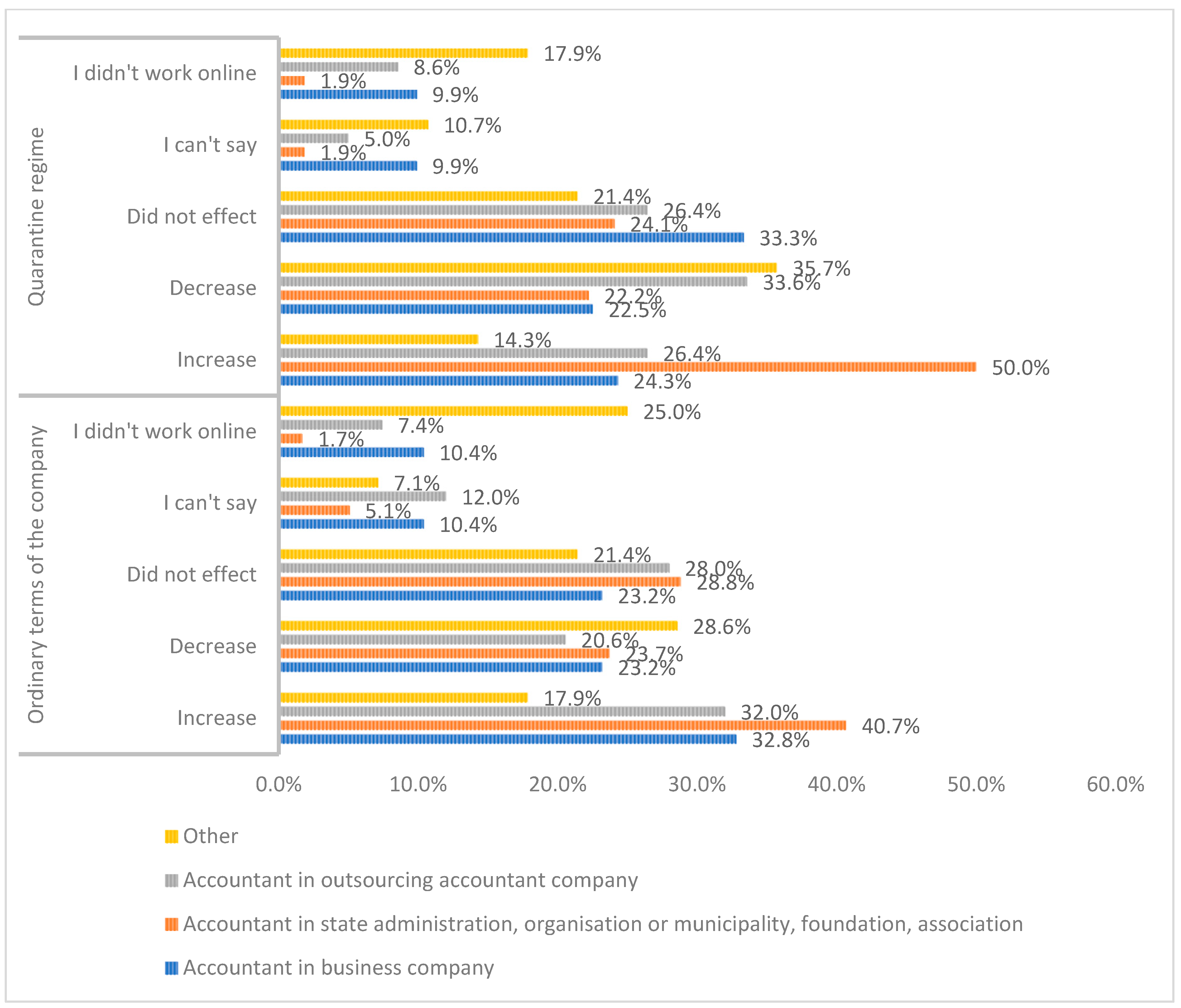

When analyzing changes in perceived work efficiency by current work position groups under normal working conditions, the highest proportion of employees indicating an increase in work efficiency when working online was found in public sector enterprises (40.7%), compared to 32% in private corporations and the accounting outsourcing enterprises. However, no statistically significant differences in attitudes towards online working efficiency were found on the basis of current job positions (χ

2 = 23.34,

p = 0.105). Meanwhile, changes in perceived work efficiency by current job position attribute during the quarantine period were statistically significantly different ((χ

2 = 31.47,

p = 0.012): only 24.3% of accounting specialists in business enterprises and 26.4% of employees in accountancy service providers, and even 50% of accounting employees in the public sector, reported an increase in efficiency, while only about 22% of accounting specialists in business enterprises and the public sector, and even 33.6% of employees in accounting service providers, observed a decrease in efficiency (see

Figure 8).

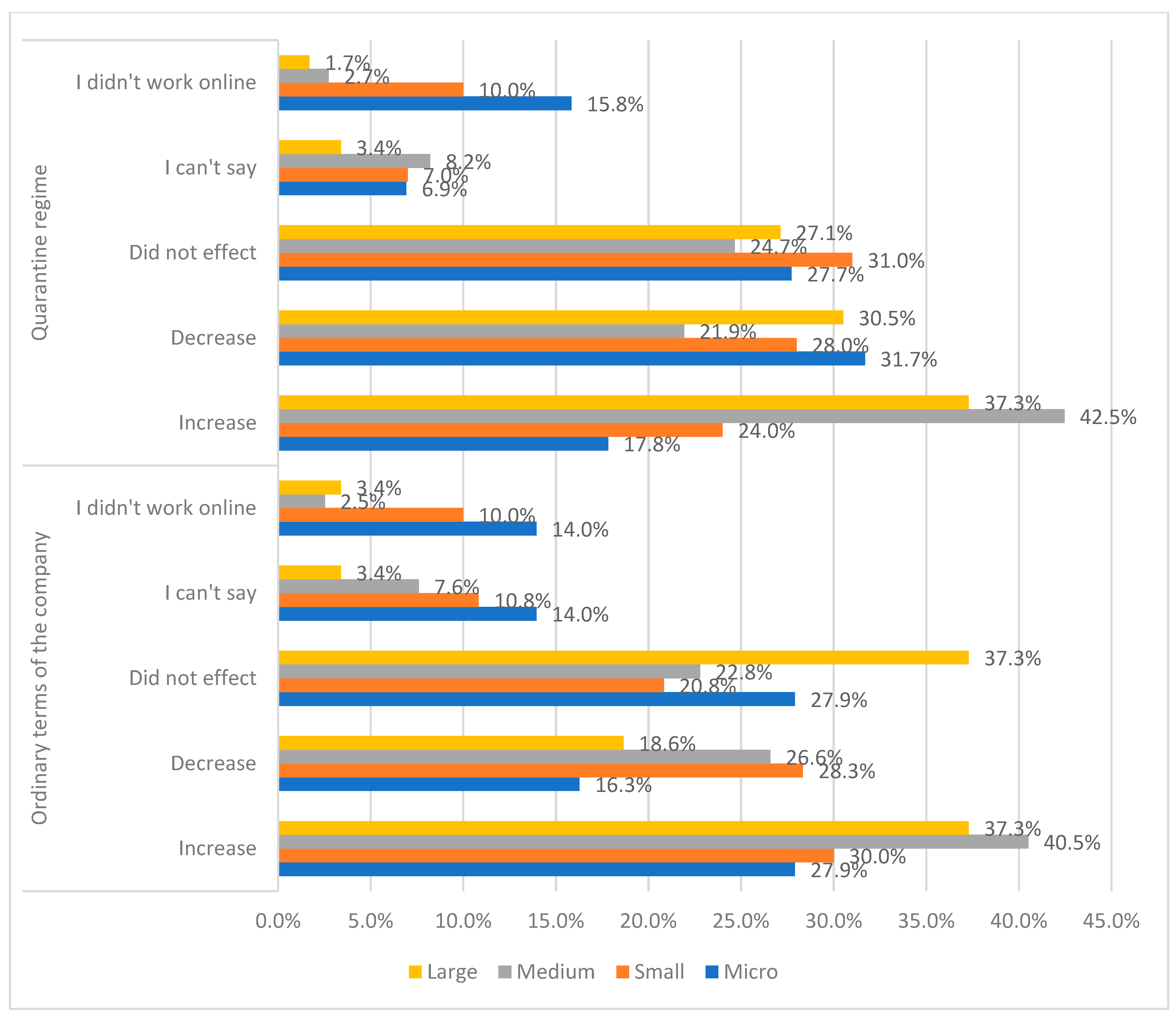

There was a statistically significant difference across enterprise categories in attitudes towards changes in efficiency observed under normal and quarantine conditions (Chi square test results respectively: χ

2 = 27.34,

p = 0.007 and χ

2 = 27.20,

p = 0.007). Under normal working conditions, a relatively higher proportion of employees in large and medium-sized enterprises indicated that efficiency had increased when working online, while the proportion of respondents in small and micro-enterprises who felt this way was significantly lower, at 27.9% and 30%, respectively. In large-sized enterprises, the highest proportion of accounting specialists reported that working online had no impact on their efficiency. While attitudes towards changes in efficiency as a result of online working remained similar under quarantine, there was a decrease in the proportion of respondents in micro-enterprises who thought that online working had a positive impact on their performance (see

Figure 9).

We concluded that country environment and enterprise size had an effect on the differences in perceived job performance of accounting specialists under normal and quarantine conditions, whereas the differences in perceived online work efficiency in various work position groups were significant under quarantine conditions.

Online work has, to a large extent, changed the level of functions, responsibilities, and additional projects of respondents: 40% of the respondents indicated an increase in the level of their functions and responsibilities, while 10% identified a decrease. In contrast, 38% of respondents stated that the scope of their responsibilities remained unchanged (see

Table S5).

The study sought to identify not only the impact of quarantine on changes in the working patterns and efficiency of accounting specialists but also on the business indicators commonly monitored by accountants. A total of 58.7% of respondents indicated that the quarantine regime had an impact on the efficiency of the company’s operations, and 35.4% said it did not. There were statistically significant differences observed in the distribution of this attribute (χ

2 = 39.58,

p = 0.00) when analyzing the distribution between countries: as many as 73.1% of Lithuanian respondents and only 45.9% of Latvian respondents indicated that the quarantine regime made an impact on company efficiency (see

Table S6). However, no statistically significant differences of quarantine regime impact on the efficiency of the company’s activities were identified in various groups of company size and sector. (Chi-square test results, respectively: χ

2 = 7.46,

p = 0.281, χ

2 = 9.96,

p = 0.126). (see

Tables S7 and S8).

A total of 43.7% of the respondents indicated a decrease in the revenue of their companies, but much less—only 26.4%—a decrease in the cost of sales. This disproportionate variation can be explained by the relatively high share of service companies. A total of 13.7% of the respondents indicated that their company’s revenue level increased during the quarantine period, but 25.3% of the companies indicated an increase in the cost of sales. However, for a relatively large proportion of respondents (over 40%) revenue, cost of sales, and profit all remained stable (see

Figure 10).

Statistically significant differences were found in the changes in the sales revenue level across countries (χ

2 = 55.66,

p = 0.000), company sizes (χ

2 = 18.76,

p = 0.027), and sectors (χ

2 = 24.54,

p = 0.004). Quarantine led to significant fluctuations in the revenue level of Lithuanian companies, with as many as 72% of Lithuanian respondents reporting a change in their revenue level, with the majority reporting a decrease (46.7%). Meanwhile, the income level of Latvian enterprises was much more stable, with as many as 50.7% of Latvian respondents indicating that their income remained at the same level (see

Table S9). When analyzing the relationship between changes in income levels and the size of enterprises, the share of enterprises with a stable income level was similar in all enterprise categories—around 40%. However, the change in income due to the quarantine affected the different sizes of enterprises differently: the most negatively affected were micro-enterprises, with 48.8% showing a fall in income levels and only 7% showing an increase. Medium-sized enterprises were the least negatively affected, with only 31.6% indicating a decrease in their level of income and 25.3% an increase (see

Table S10). When looking at the relationship between the sector of activity and the level of income, the most stable situation was observed in the mixed sector, with more than half of the enterprises surveyed maintaining their income at the same level. The largest fluctuations were observed in the trade sector: here, the highest proportion of respondents reported an increase in income levels (18.5%), but a decrease (59.3%) was also the most frequent (see

Table S11).

Statistically significant differences in the cost of sales level changes were found across countries (χ

2 = 60.98,

p = 0.000), company sizes (χ

2 = 19.36,

p = 0.022), and sectors (χ

2 = 22.76,

p = 0.007). As in the case of revenue, the majority (71.4%) of respondents from Lithuanian companies reported variations in the cost of sales level due to quarantine, with the majority reporting an increase (37.9%). Meanwhile, the cost of sales level was more stable in Latvian companies, with 58.5% of Latvian respondents indicating the same situation (see

Table S12). The most stable indicator was in micro-enterprises (55% of respondents indicated “unchanged”), with the largest increase in large enterprises and a decrease in medium-sized enterprises (see

Table S13). The most stable cost of sales level remained in the mixed sector (59.5%), while the greatest fluctuation was observed in the service sector (see

Table S14).

Statistically significant (χ

2 = 54.16,

p = 0.000) and very similar to the distribution of the other indicators were the changes in the level of profit (loss) found in the different countries: in Latvia, relatively more stability (47.8%) was observed; in Lithuania, variability of the indicator, including 43.4% of profit decreases and 24.2% of profit increases (see

Table S15). There were statistically significant differences among companies of different sizes (χ

2 = 20.39,

p = 0.016) in profit changes. Micro-enterprises were the most negatively affected by the quarantine: although respondents from this group of enterprises were more likely than the other groups to report an unchanged level of profit (43.4%), this group had the relatively lowest incidence of increase in profit (7.8%) and the highest incidence of decrease.

Meanwhile, medium-sized enterprises showed the highest number of increases in the level of profits and, correspondingly, fewer instances of decreases in the level of profits than other groups (see

Table S16). A statistically significant difference in the distribution of the level of profit was also found in the different sectors (χ

2 = 19.50,

p = 0.021): the most stable profit levels were found in the mixed sector (50.8%), while the highest variation was observed in the trading sector, ranging from 18.5% increases to 51.9% decreases (see

Table S17).

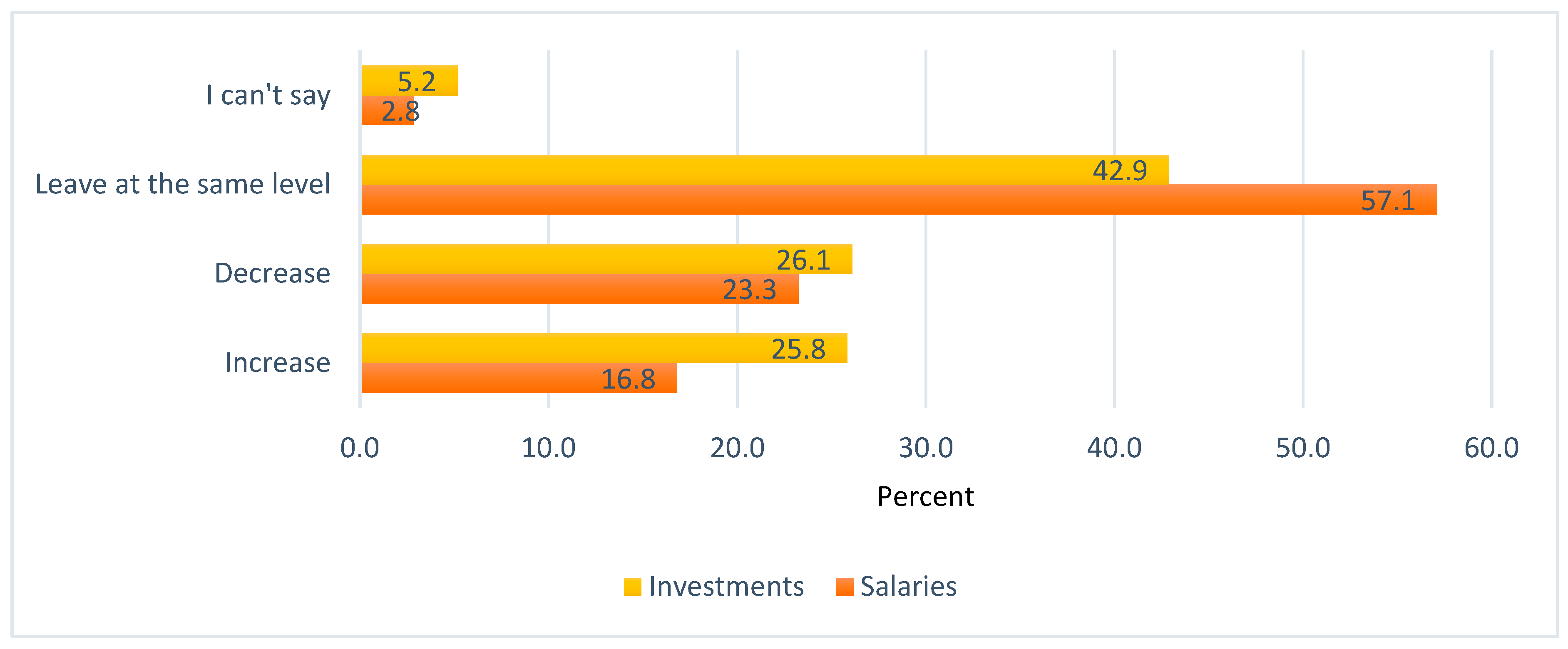

As

Figure 11 shows, in most cases, the level of salaries remained unchanged, while almost a quarter of respondents reported a decrease. In turn, changes in investments were quite different. While around 40% of enterprises reported no change in the level of investments, a quarter reported a decrease. However, almost the same number reported investments in computers, communication facilities, furniture, and other long-term assets that were higher than previous levels.

Statistically significant differences in the extent of salary changes were identified across countries as well as across companies of different sizes (chi-square test results, respectively: χ

2 = 76.75,

p = 0.000, and χ

2 = 41.74,

p = 0.000). In Latvia, the level of salaries remained largely stable (68.3%), while in Lithuania, significant changes were observed, with as many as 33.5% of respondents reporting a decrease in salaries (see

Table S18). Our analysis of the changes in the level of salaries in the categories of enterprises revealed that in medium-sized enterprises, almost equal shares (one third) of respondents indicated an increase, a decrease, and stability of the indicator.

A very different pattern was seen in micro-enterprises, where two thirds of cases showed stability in salaries, but only 7.8% indicated an increase (see

Table S19). In the context of the level of salaries, agricultural enterprises were the least affected, with two-thirds of the cases showing no change in the level of salaries in this sector, while the most negatively affected by the quarantine regime were trade enterprises, which had the highest number of decreases in the level of salaries and the lowest number of increases (see

Table S20).

The level of investments differed significantly (χ

2 = 74.27,

p = 0.000) by country: in Latvia, the level of investments was again stable (54.1%), with an indication of respondents of a small increase (9.8%), while in Lithuania, there were significant changes, including an increase in the level of investments in 44% of cases (see

Table S21). A statistically significant (χ

2 = 25.85,

p = 0.002) distribution of the level of investments was also found in the different sectors: companies in the trade sector show the highest proportion of decreases in the level of investments and the lowest proportion of increases, while the services sector shows the highest increase (36.6%) and the lowest proportion of decreases (see

Table S22). No statistically significant differences in the change of the level of investment were found in various enterprise-size groups (χ

2 = 11.50,

p = 0.243).

We conclude a company’s size, sector, and country environment have an impact on the change in the company’s financial performance (revenue, cost of sales, profit) during quarantine. The level of salaries was influenced by the country’s environment and the size of the company, while the level of investments was influenced by the company’s national environment and sector.

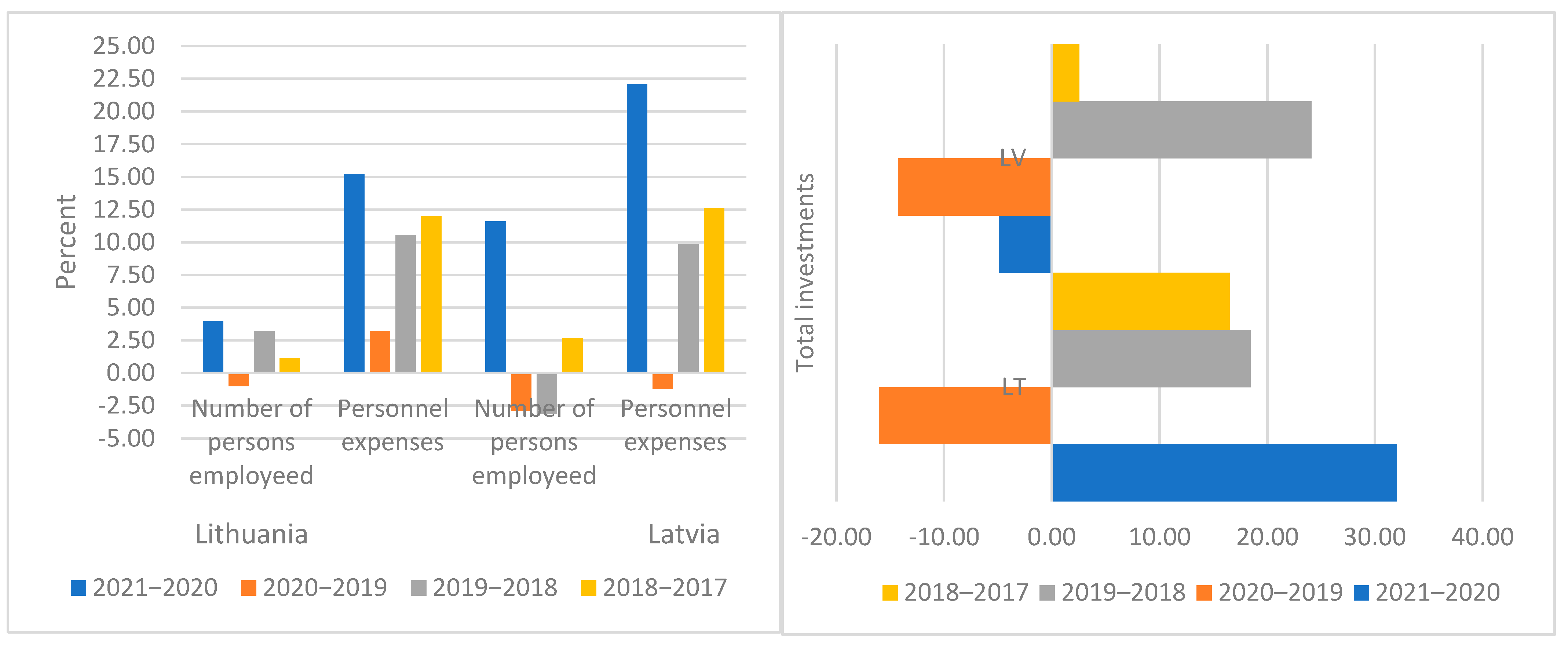

Figure 12 shows the changes in main performance indicators under statistical data of Lithuania and Latvia.

The analysis of the statistical data shows that, generally, all the main performance indicators analyzed dropped during the first phases of the crisis period (2020); however, clear differences between the countries were evident, even if net turnover and total purchases fluctuated from −1.24% to −6.4% and from −3.3% to −7%, respectively, in both countries. In Lithuania, profits after taxes increased by 21% compared with the previous year, and in Latvia, these decreased by almost 33%. However, overall, average fluctuations in the main performance indicators from 2017–2021 reached almost 13% in Lithuania and less than 14% in Latvia.

Figure 13 depicts the changes in investments, number of employees, and personnel expenses according to statistical data, and shows the same tendency for greater fluctuations in Latvia. However, compared with 2019, in 2020, the value of total investments decreased by 14% in Latvia and by 16% in Lithuania. However, the number of employees in Lithuania only decreased by slightly more than 1% and personnel expenses increased by 3%; in Latvia, these decreased by almost 5% and more than 1%, respectively.

During the period analyzed, the biggest noticeable difference was the change in total investments—in Lithuania these increased, on average, by almost 13% and in Latvia by almost 2%. However, in Lithuania, the number of employees increased, on average, by almost 2% and personnel expenses by 10%; in Latvia, the number of employees increased by 2% and personnel expenses by 11%. According to the statistical data, both countries showed signs of recovery and stability.

An analysis of the survey results and statistical data may lead to the conclusion that the perceptions of respondents were partly correct and, overall, saw the main financial indicators to be worse than the actual statistical data showed to be the case. It should be noted that the survey was carried out during the second wave of COVID-19 (autumn 2020—spring 2021), when people were tired of the long-term constraints, when some companies were again on hold, when uncertainty prevailed, and when the economic crisis was being depicted in the darkest colors. Pessimistic assessments by respondents could therefore be expected. The results of our survey can only be compared with the official statistics on changes in corporate performance in 2019–2020. The analysis shows that accountants were quite correct in their perception of changes in corporate performance. The statistics showed a drop in companies’ combined revenues and purchases of up to 3% in Lithuania and 7% in Latvia, and respondents’ opinions reflected this trend, although there was more pessimism, with 30% more respondents indicating that revenues had fallen rather than having stayed at the same level or increased. Meanwhile, the assessment of changes in investment was more optimistic: the statistics showed a 14% drop in investment in Latvia and 13% in Lithuania, but 26% of respondents reported an increase and the same number a decrease in investment. However, it should be noted that respondents did not assess the amount of change, whereas the statistics reflect this. What is more interesting in this case are the different statistical changes in the profits and employee expenses of the companies in the countries analyzed: while Latvia showed a 33% drop in profits in 2020 compared to 2019, Lithuania showed a 21% increase in profits; while employee expenses had decreased by 1.23% in Latvia, they had increased by 3.17% in Lithuania. This might be an indication of the faster adaptability of Lithuanian companies to economic shocks or the influence of the different economic structures of the countries (e.g., Lithuania has more developed transport and IT sectors, which were not adversely affected during the COVID-19 period, while Latvia has a more developed tourism sector, which was one of the most affected). This could be a direction for further research: why do similar neighboring countries with similar economies, cultures and historical backgrounds perform so differently in a crisis?

5. Conclusions

Our study shows that in non-crisis conditions, the vast majority (86%) of accounting specialists were able to work online with different workload possibilities, although almost half of employees were able to work online for more than 75% of their time. Under the quarantine regime, the number of remote-work possibilities for accounting specialists increased, as did the proportion of online work compared to the case under usual conditions. However, statistically significant differences were revealed between Lithuania and Latvia, where the number of cases in which individuals were unable to work online, even during quarantine, was significantly higher, and the proportion of the workload for which online work was possible was lower.

Respondents differed in their perceptions of the effectiveness of accounting specialists when working online under non-crisis conditions, with one third indicating an increase in online work efficiency. There was a statistically significant difference in the perceived online work efficiency of accounting specialists under quarantine conditions compared to their work efficiency in an office. Respondents were of the view that working online under quarantine conditions was slightly more efficient than working in non-crisis conditions. In Latvia, accountants indicated a clear decrease in efficiency when working online under quarantine conditions, whereas Lithuanian accountants did not identify any significant differences. There were statistically significant differences in the perceived change in work efficiency under these different conditions depending on the respondent’s current work position and the company category (size) attributes.

The majority of respondents indicated that the quarantine regime made an impact on company performance; this was stated by 73.1% of respondents in Lithuania and 45.9% in Latvia. However, slightly more than 40% of respondents indicated that the company’s main performance indicators (revenue, cost of sales, profit) remained stable under the quarantine regime. The variation in these indicators also differed by country, company category, and sector. In all cases, Latvian companies showed greater stability (no change), while Lithuanian companies showed greater fluctuations in both the upward and downward directions. The largest fluctuations in revenue and profit levels were observed in the trade sector, while the highest cost-of-sales fluctuations were observed in the service sector.

The level of salaries remained stable in most companies during the quarantine period, although salaries decreased in a quarter of the companies. There was also variation across countries: while in Latvia the level of salaries remained largely stable, in Lithuania significant changes were observed, both in the upward and downward direction. The quarantine regime had the most negative impact on the trade sector, with the greatest decreases in the level of salaries and the lowest number of increases. Changes in investment were quite different across enterprises: the trade sector showed the highest decrease in the level of investment and the lowest level of salary increases, while the services sector showed the highest increase and the lowest decrease.

The analysis of the statistical data showed that during the pandemic, Latvia experienced greater fluctuations in the main performance indicators, but overall, both countries maintained positive tendencies toward stability and recovery. However, the perceptions of respondents were more negative than the actual level of the main performance indicators that might be influenced by the big range of uncertainty, strict restrictions, huge change in lifestyle, and future insecurity.

The limitations of the study take several facets into account. Two countries were involved in the research, potentially yielding specific results for this study, and meaning that the findings may not be universally applicable. Future research directions might include an investigation of more countries to provide a broader understanding of changes in efficiency and the economic implications of the pandemic, analysis of their economic structure, and other factors. Addressing this limitation could enhance the generalizability of the study’s findings and contribute to a more comprehensive understanding of the global impact of the COVID-19 economic crisis. However, the study significantly contributes to the existing literature by presenting findings on the perception of efficiency among both employees and companies. The study goes beyond the immediate impact of the COVID-19 economic crisis by revealing a pre-existing landscape on the possibilities for accounting specialists to work online, providing valuable insights into the readiness and adaptability of the profession to remote work even before the unprecedented challenges posed by the pandemic. The research offers a comprehensive view, enriching the understanding of efficiency perceptions and work modalities.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}