Some Results on Measures of Interaction among Risks

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Preliminaries

2.1. Stochastic Orders

- (i)

- in the usual stochastic order (denoted by ) if (or ) for all ;

- (ii)

- in the increasing convex order (denoted by ) if , for all ;

- (iii)

- in the dispersive order (denoted by ) if for all ;

- (iv)

- in the excess wealth order (denoted by ) if , for all .

- (i)

- , for all

- (ii)

- , for all

2.2. Copula and Dependence

- (i)

- is said to be stochastically increasing (SI) in if the conditional distribution is stochastically increasing as increases;

- (ii)

- is said to be positive dependent through the stochastic order (PDS) if for ;

- (iii)

- is said to be weakly stochastically increasing (WSI) in Y (denoted ) if ) is increasing in y for all ;

- (iv)

- is said to be positively dependent through the upper orthant (PDUO) if for all .

2.3. Co-Risk Measures

- (i)

- the of at stress level given that is under stress at level for is

- (ii)

- the of at stress level given that is under stress at level for is

2.4. Risk Contribution Measures

- (i)

- of at stress level given that is under stress at level for is

- (ii)

- of at stress level given that is under stress at level for is

2.5. Arrangement Monotonicity

3. Co-Risk Measures

4. Risk Contribution Measures

5. Simulations

- For each stress level a sample of observations of and a sample of observations of , are generated.

- For , based on and calculate the adjusted empirical distribution functions, respectively,

- Denote at each stress level , for each stress level utilize the sample th quantilesandto estimate the risk measures and , respectively. Further, calculate the sample versionfor and , respectively.

- The following empirical estimators are used for and , respectively.

- 1.

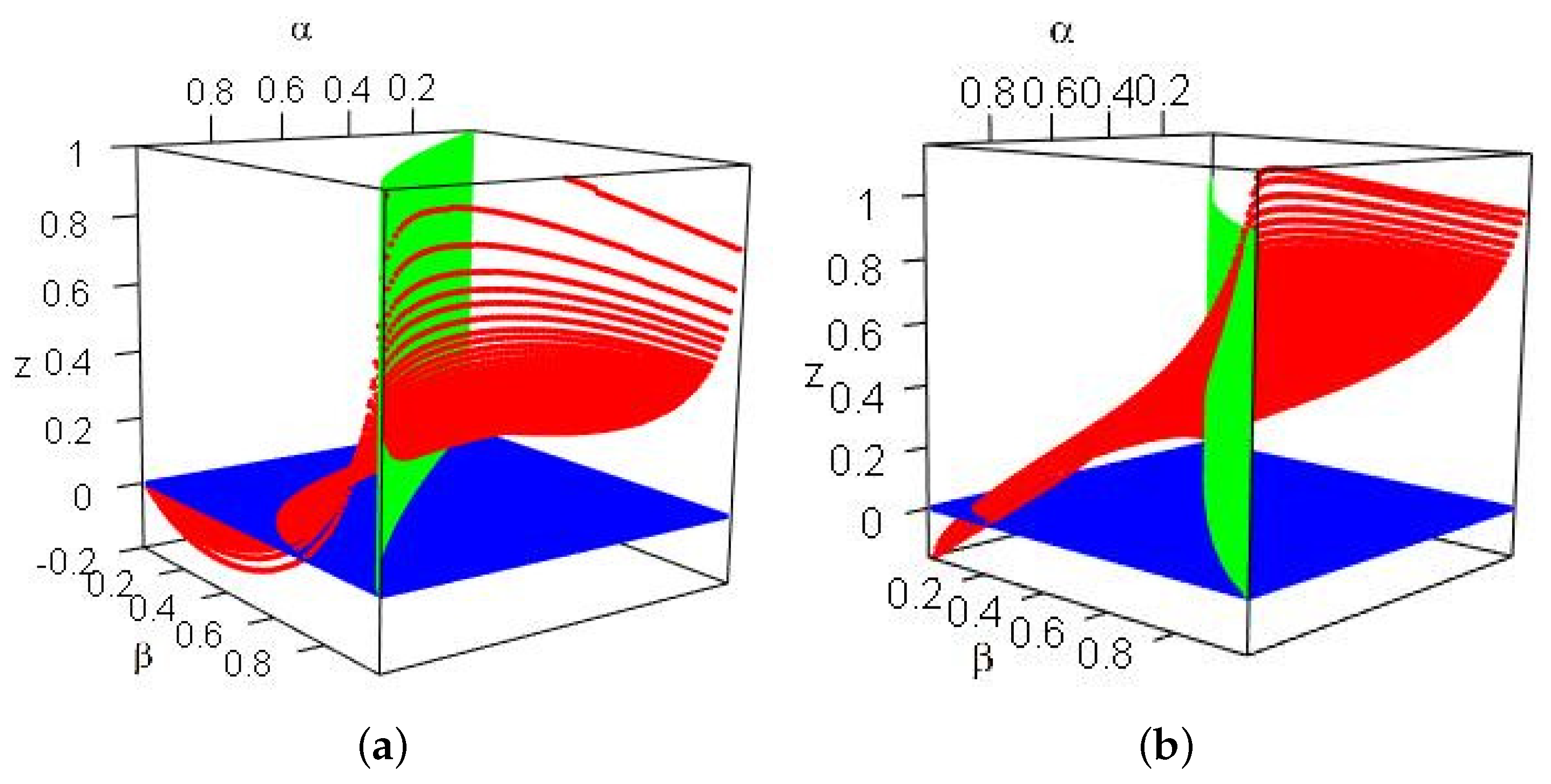

- For , , , three exponentially distributed random risks, by the definition of the usual stochastic order, it is plain that when we havefor all . Figure 1a plots the differenceAs can be seen, the difference is positive for all , confirming the theoretical finding. Moreover, for some , the difference may still be positive.

- 2.

- For , , , there are three normal distributed random risks, according to Table 1.1 of [38], one has . By the second assertion of Theorem 3, for ,Figure 1b shows the difference , which is positive for and for some .

- 3.

- 4.

6. Concluding Remarks

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Ghosh, B.; Papathanasiou, S.; Ramchandani, N.; Kenourgios, D. Diagnosis and prediction of IIGPS’ countries bubble crashes during BREXIT. Mathematics 2021, 9, 1003. [Google Scholar] [CrossRef]

- Yang, K.; Wei, Y.; He, J.; Li, S. Dependence and risk spillovers between mainland China and London stock markets before and after the Stock Connect programs. Phys. A Stat. Mech. Its Appl. 2019, 526, 120883. [Google Scholar] [CrossRef]

- Zhu, B.; Zhou, X.; Liu, X.; Wang, H.; He, K.; Wang, P. Exploring the risk spillover effects among China’s pilot carbon markets: A regular vine copula-CoES approach. J. Clean. Prod. 2020, 242, 118455. [Google Scholar] [CrossRef]

- Acerbi, C.; Nordio, C.; Sirtori, C. Expected shortfall as a tool for financial risk management. arXiv 2001, arXiv:0102304. [Google Scholar]

- Acerbi, C.; Tasche, D. On the coherence of expected shortfall. J. Bank. Financ. 2002, 26, 1487–1503. [Google Scholar] [CrossRef] [Green Version]

- Artzner, P.; Delbaen, F.; Eber, J.M.; Heath, D. Coherent measures of risk. Math. Financ. 1999, 9, 203–228. [Google Scholar] [CrossRef]

- Yamai, Y.; Yoshiba, T. Value-at-risk versus expected shortfall: A practical perspective. J. Bank. Financ. 2005, 29, 997–1015. [Google Scholar] [CrossRef]

- Chen, S.X. Nonparametric estimation of expected shortfall. J. Financ. Econom. 2008, 6, 87–107. [Google Scholar] [CrossRef] [Green Version]

- Righi, M.B.; Ceretta, P.S. A comparison of Expected Shortfall estimation models. J. Econ. Bus. 2015, 78, 14–47. [Google Scholar] [CrossRef]

- Denuit, M.; Dhaene, J.; Goovaerts, M.; Kaas, R. Actuarial Theory for Dependent Risks: Measures, Orders and Models; John Wiley & Sons: Hoboken, NJ, USA, 2006. [Google Scholar]

- Jorion, P. Value at Risk: The New Benchmark for Managing Financial Risk; McGraw-Hill: New York, NY, USA, 2000. [Google Scholar]

- Embrechts, P.; Höing, A.; Puccetti, G. Worst var scenarios. Insur. Math. Econ. 2005, 37, 115–134. [Google Scholar] [CrossRef]

- Kaas, R.; Laeven, R.J.; Nelsen, R.B. Worst VaR scenarios with given marginals and measures of association. Insur. Math. Econ. 2009, 44, 146–158. [Google Scholar] [CrossRef]

- Laeven, R.J. Worst VaR scenarios: A remark. Insur. Math. Econ. 2009, 44, 159–163. [Google Scholar] [CrossRef] [Green Version]

- Girardi, G.; Ergün, A.T. Systemic risk measurement: Multivariate GARCH estimation of CoVaR. J. Bank. Financ. 2013, 37, 3169–3180. [Google Scholar] [CrossRef]

- Adrian, T.; Brunnermeier, M.K. CoVaR. Am. Econ. Rev. 2016, 106, 1705–1741. [Google Scholar] [CrossRef]

- Mainik, G.; Schaanning, E. On dependence consistency of CoVaRand some other systemic risk measures. Stat. Risk Model. 2014, 31, 49–77. [Google Scholar] [CrossRef] [Green Version]

- Caporin, M.; Costola, M.; Garibal, J.C.; Maillet, B. Systemic risk and severe economic downturns: A targeted and sparse analysis. J. Bank. Financ. 2022, 134, 106339. [Google Scholar] [CrossRef]

- Jiang, Y.; Mu, J.; Nie, H.; Wu, L. Time-frequency analysis of risk spillovers from oil to BRICS stock markets: A long-memory Copula-CoVaR-MODWT method. Int. J. Financ. Econ. 2022, 27, 3386–3404. [Google Scholar] [CrossRef]

- Mao, T.; Zhao, Q.; Wu, Q. Worst-case conditional value-at-risk and conditional expected shortfall based on covariance information. JUSTC 2022, 52, 4. [Google Scholar] [CrossRef]

- Sordo, M.A.; Bello, A.J.; Suárez-Llorens, A. Stochastic orders and co-risk measures under positive dependence. Insur. Math. Econ. 2018, 78, 105–113. [Google Scholar] [CrossRef]

- Fang, R.; Li, X. Some results on measures of interaction between paired risks. Risks 2018, 6, 88. [Google Scholar] [CrossRef] [Green Version]

- Shaked, M.; Shanthikumar, J.G. Stochastic Orders; Springer: Berlin/Heidelberg, Germany, 2007. [Google Scholar]

- Belzunce, F.; Riquelme, C.M.; Mulero, J. An Introduction to Stochastic Orders; Academic Press: New York, NY, USA, 2015. [Google Scholar]

- Li, H.; Li, X. Stochastic orders in reliability and risk. In Honor of Professor Moshe Shaked; Springer: New York, NY, USA, 2013. [Google Scholar]

- Shaked, M.; Shanthikumar, J.G. (Eds.) Univariate Stochastic Orders. In Stochastic Orders; Springer New York: New York, NY, USA, 2007; pp. 3–79. [Google Scholar] [CrossRef]

- Sordo, M.A.; Ramos, H.M. Characterization of stochastic orders by L-functionals. Stat. Pap. 2007, 48, 249–263. [Google Scholar] [CrossRef] [Green Version]

- Balbás, A.; Garrido, J.; Mayoral, S. Properties of distortion risk measures. Methodol. Comput. Appl. Probab. 2009, 11, 385–399. [Google Scholar] [CrossRef] [Green Version]

- Glynn, P.W.; Peng, Y.; Fu, M.C.; Hu, J.Q. Computing sensitivities for distortion risk measures. INFORMS J. Comput. 2021, 33, 1520–1532. [Google Scholar] [CrossRef]

- Nelsen, R.B. An Introduction to Copulas; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2007. [Google Scholar]

- Cai, J.; Wei, W. On the invariant properties of notions of positive dependence and copulas under increasing transformations. Insur. Math. Econ. 2012, 50, 43–49. [Google Scholar] [CrossRef]

- Karimalis, E.N.; Nomikos, N.K. Measuring systemic risk in the European banking sector: A copula CoVaR approach. Eur. J. Financ. 2018, 24, 944–975. [Google Scholar] [CrossRef] [Green Version]

- Kim, J.S.; Proschan, F. A review: The arrangement increasing partial ordering. Comput. Oper. Res. 1995, 22, 357–371. [Google Scholar] [CrossRef]

- Barlow, R.E.; Proschan, F. Statistical Theory of Reliability and Life Testing: Probability Models; Holt, Rinehart & Winston: New York, NY, USA, 1975. [Google Scholar]

- Metropolis, N.; Ulam, S. The monte carlo method. J. Am. Stat. Assoc. 1949, 44, 335–341. [Google Scholar] [CrossRef]

- Rubinstein, R.Y.; Kroese, D.P. Simulation and the Monte Carlo Method; John Wiley & Sons: Hoboken, NJ, USA, 2016. [Google Scholar]

- McNeil, A.J.; Frey, R.; Embrechts, P. Quantitative Risk Management: Concepts, Techniques and Tools-Revised Edition; Princeton University Press: Princeton, NJ, USA, 2015. [Google Scholar]

- Mccomb, M.A. Comparison Methods for Stochastic Models and Risks. Techometrics 2003, 45, 370–371. [Google Scholar] [CrossRef]

- Ortega-Jiménez, P.; Sordo, M.; Suárez-Llorens, A. Stochastic orders and multivariate measures of risk contagion. Insur. Math. Econ. 2021, 96, 199–207. [Google Scholar] [CrossRef]

- Zhou, C. Are Banks Too Big to Fail? Measuring Systemic Importance of Financial Institutions. Int. J. Cent. Bank. 2010, 6, 46. [Google Scholar] [CrossRef]

- Raineri, L.; Shanske, D. Municipal Finance and Asymmetric Risk. Belmont Law Rev. 2017, 4, 65. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fan, Y.; Fang, R. Some Results on Measures of Interaction among Risks. Mathematics 2022, 10, 3611. https://doi.org/10.3390/math10193611

Fan Y, Fang R. Some Results on Measures of Interaction among Risks. Mathematics. 2022; 10(19):3611. https://doi.org/10.3390/math10193611

Chicago/Turabian StyleFan, Yiting, and Rui Fang. 2022. "Some Results on Measures of Interaction among Risks" Mathematics 10, no. 19: 3611. https://doi.org/10.3390/math10193611

APA StyleFan, Y., & Fang, R. (2022). Some Results on Measures of Interaction among Risks. Mathematics, 10(19), 3611. https://doi.org/10.3390/math10193611