From Constant to Rough: A Survey of Continuous Volatility Modeling

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

- First of all, apart from more straightforward applications in, e.g., mean-variance portfolio theory originating from [7] by H. Markowitz, the concept of volatility has a crucial role in another significant area within finance, i.e., non-arbitrage pricing theory, conceptualized by F. Black, M. Scholes, and R. Merton in [8,9]. This theory has a unique and intricate perspective on volatility and has been the major driving force in volatility modeling for the past four decades. Therefore, in this survey, we consider the volatility predominantly from the option pricing viewpoint.

- Our focus primarily centers on continuous stochastic volatility models in continuous time. This means that we will not discuss various discrete-time models such as ARCH, GARCH, or EARCH of Engle [10], Bollerslev [11], and Nelson [12], or multiple jump-diffusion models including the approaches of Duffie et al. [13] or Barndorff-Nielsen and Shephard [14]. The omission of jumps seems to be the most notable gap in light of the realism this approach provides. However, given our desire to highlight fractional and rough volatility in more detail, the inclusion of discrete-time and jump-diffusion models with the level of detail they deserve would substantially inflate the size of this survey and result in a notable change in emphasis. Therefore, we leave these two topics for a separate work. Readers with a specific interest in discrete-time models are referred to [15,16]; for jump models, see the specialized books by Barndorff-Nielsen and Shepard [17], Gatheral [18], Rachev et al. [19], or Tankov and Cont [20]. For other modeling viewpoints that are different from stochastic volatility, see the overviews given by Shiryaev [21] and Mariani and Florescu [22].

2. Market Volatility: Empirical Challenges and Stylized Facts

2.1. From Random Walk to Geometric Brownian Motion

“…Discovery or rediscovery of Louis Bachelier’s 1900 Sorbonne thesis […] initially involved a dozen or so postcards sent out from Yale by the late Jimmie Savage, a pioneer in bringing back into fashion statistical use of Bayesian probabilities. In paraphrase, the postcard’s message said, approximately, ‘Do any of you economist guys know about a 1914 French book on the theory of speculation by some French professor named Bachelier?’

Apparently I was the only fish to respond to Savage’s cast. The good MIT mathematical library did not possess Savage’s 1914 reference. But it did have something better, namely Bachelier’s original thesis itself.

I rapidly spread the news of the Bachelier gem among early finance theorists. And when our MIT PhD Paul Cootner edited his collection of worthy finance papers, on my suggestion he included an English version of Bachelier’s 1900 French text…”

“Because options are specialized and relatively unimportant financial securities, the amount of time and space devoted to the development of a pricing theory might be questioned…”

“When judged by its ability to explain the empirical data, option pricing theory is the most successful theory not only in finance, but in all of economics.”

2.2. Implied Volatility and the Smile Phenomenon

“Yet that weakness is also its greatest strength. People like the model because they can easily understand its assumptions. The model is often good as a first approximation, and if you can see the holes in the assumptions you can use the model in more sophisticated ways.”

“Following the standard paradigm, assume that stock market returns are lognormally distributed with an annualized volatility of 20% (near their historical realization). On 19 October 1987, the two month S&P 500 futures price fell 29%. Under the lognormal hypothesis, this is a −27 standard deviation event with probability . Even if one were to have lived through the entire 20 billion year life of the universe and experienced this 20 billion times (20 billion big bangs), that such a decline could have happened even once in this period is a virtual impossibility.”

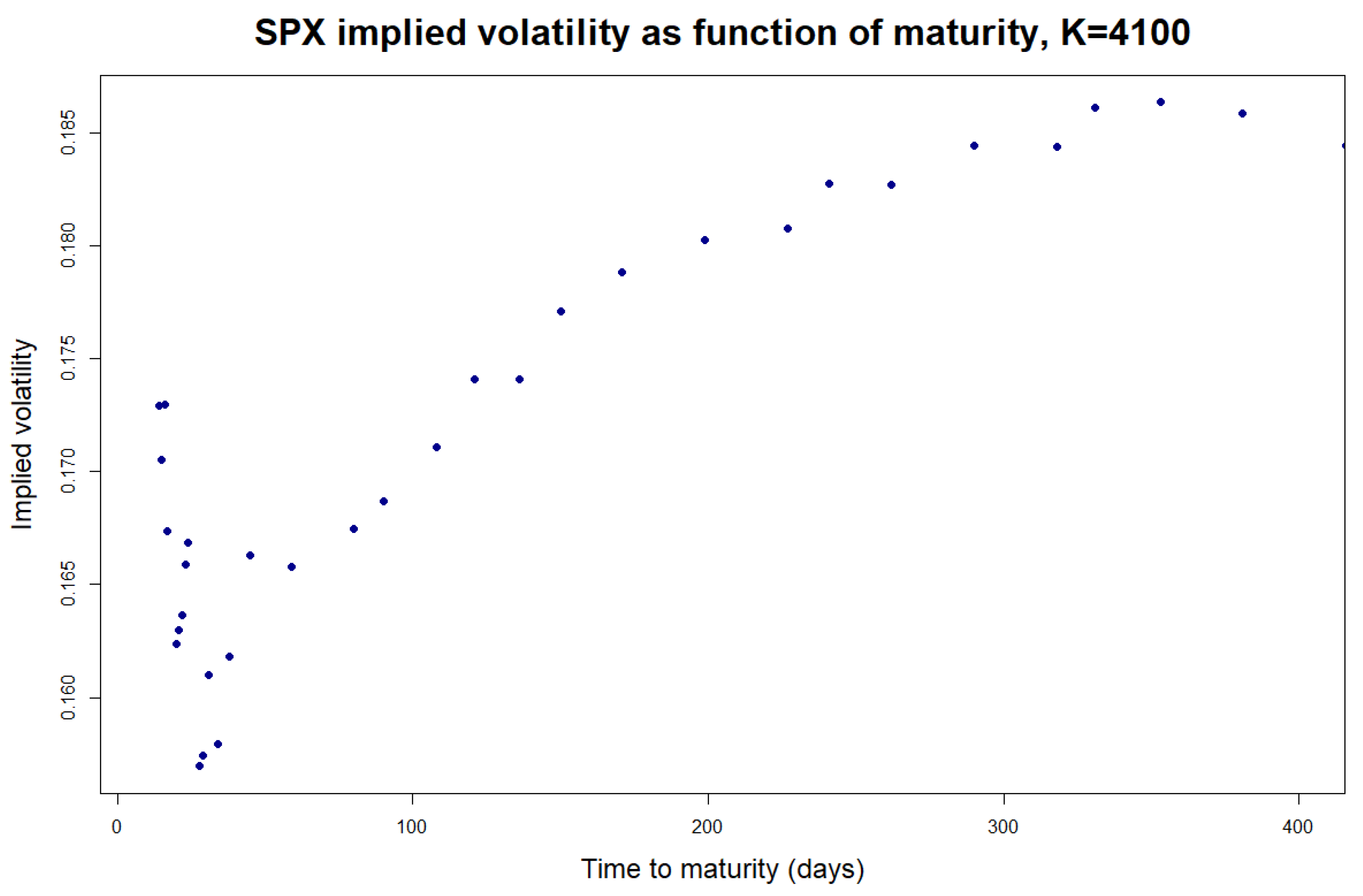

- First of all, note that the smile gradually flattens out as the time to maturity T increases. However, this decrease is fairly slow: for example, in Figure 2, the curvature is noticeable 262 days (Figure 2g) and even 962 days (Figure 2h) before maturity. The latter effect turns out to require special treatment; in this regard, see Section 3.3 below, as well as [46,47,48].

- Second, observe the behavior of the smile at-the-money, i.e., when (or, in terms of log-moneyness, when ): as T becomes smaller, the smile at-the-money tends to become steeper. Figure 3 characterizes this phenomenon in more detail: for each T, we took implied volatilities of seven options with strikes closest to , performed a least squares linear fit on them, and depicted the absolute values of the resulting slopes in Figure 3a. It turns out that the variation in absolute slopes with T for shorter maturities seems to be well described by the power law with , at least as a first approximation (see the discussion at the end of Section 3.3 below, as well as [49,50]). As an illustration, the red lines in Figure 3a,b depict power-law fits for the SPX implied volatility slopes corresponding to 3 May 2023; for our dataset, . A similar type of behavior is reported by, e.g., Fouque, Papanicolaou, Sircar, and Sølna (2004) [51], Gatheral, Jaisson, and Rosenbaum (2018) [52] and, more recently, by Delemotte, De Marco, and Segonne (2023) [50].

- (1)

- the parameters of the model are calibrated with respect to the market data;

- (2)

- the calibrated parameters are plugged into the model and the respective model no-arbitrage European option prices are computed;

- (3)

- these “synthetic” prices are then used to construct the implied volatility surface by the procedure described here in Section 2.2;

- (4)

- finally, the obtained model-generated surface is compared to the implied volatility surface extracted from real-world option prices.

2.3. Fat Tails, Leverage, Clustering, and Long Memory

2.3.1. Fat Tails and Non-Gaussian Distribution of log-Returns

2.3.2. Leverage and Zumbach Effect

2.3.3. Volatility Clustering

2.3.4. Long Range Dependence

3. Continuous Models of Volatility

3.1. Local Volatility

3.1.1. CEV Model

3.1.2. Local Volatility and Dupire Formula

3.1.3. Shortcomings of Local Volatility

“While absence of arbitrage is both a reasonable property to assume in a real market and a generic property of many stochastic models, market completeness is neither a financially realistic nor a theoretically robust property. From a financial point of view, market completeness implies that options are redundant assets and the very existence of the options market becomes a mystery, if not a paradox in such models.”

3.2. Stochastic Volatility Models

- To begin with, given the nature of volatility, it seems reasonable to model it with a non-negative process. In practice, this can be achieved by modeling log volatility and then taking an exponential. Alternatively, one may utilize non-negative diffusions such as Bessel-type processes (see, e.g., [30] chapter XI).

- Selecting an appropriate dependence structure between B and W from Equation (11) provides all the necessary tools to account for the leverage effect: a typical assumption is with .

- Another property shared by multiple stochastic volatility models is mean-reversion. As mentioned above in Section 2.3, this behavior seems to be a common trait for real-life volatility. Moreover, a thoroughly chosen mean-reverting process can, to some extent, mimic the clustering effect (see, e.g., [73], Chapter 3). A common approach to introduce mean reversion to the dynamics is to take a drift term of the formin the SDE for volatility. This drift “pulls σ back” to the level whenever deviates from it. The parameter calibrates the speed of mean-reversion.

- Hull and White [106] assumed that the squared volatility is itself a geometric Brownian motion, i.e., price and volatility satisfy stochastic differential equations of the formrespectively, where B and W are two Brownian motions that are allowed to be correlated to account for the leverage effect. Note that the volatility process is positive but not mean-reverting.

- Wiggins [39] suggested a slightly more general dynamics of the form

- Scott [107] and Stein and Stein [108] considered the volatility to be an Ornstein–Uhlenbeck process, i.e.,Note that is not positive: the Ornstein–Uhlenbeck process is Gaussian and, hence, can take negative values with positive probability. In practice, this issue is treated by either taking the absolute value of or introducing a reflecting barrier to the volatility dynamics [109].

- Heston [110] introduced the SDE of the formIn this model, now commonly referred to as the Heston model, the volatility follows the so-called Cox–Ingersoll–Ross or square root process (see also [111]), which enjoys strict positivity provided that . Benhamou et al. [112] considered a modification of Equation (17) of the formwith time-dependent , , and correlation to account for structural changes on the market. Another modification of Equation (17) was considered in [113]: there, the discounted price dynamics was assumed to followwhere Z is a homogeneous continuous-time Markov chain that represents market switching between different regimes.

- Lewis [117] and, later, Carr and Sun [118] (see also Baldeaux and Badran [119] section 2) considered the so-called 3/2 modelThe motivation behind the model partially comes from the statistical analysis of volatility models performed by Jawaheri [120] and Bakshi et al. [121], as well as from its ability to replicate the VIX skew (see Section 4 for further details). For more details on the existence and properties of the solution to Equation (20), we refer the reader to [98].

- Gatheral [122] presented the double CEV dynamics of the formwhere .

- Fouque et al. [123] propose a multiscale stochastic volatility. Their approach lies in modeling volatility with two diffusions, one fluctuating on a fast “time scale”, and the other fluctuating on a “slow” time scale. Namely, their model takes the formwhere f is a bounded positive function, are assumed to be small, Y is the fast scale volatility factor, i.e., a fast mean-reverting process, and Z is the slow scale volatility factor. Later, in [124], Fouque and Saporito employed the same multiscale paradigm to model the Heston-type stochastic volatility-of-volatility parameter:

3.3. Fractional and Rough Models

- is Gaussian;

- has stationary increments;

- is self-similar, i.e.,

3.3.1. Fractional Models with Long Memory:

- Ref. [130], which considers the model of the formwhere F, a, and f are nuisance parameters and is a random initial condition;

3.3.2. Rough Revolution:

3.3.3. Puzzles of Fractionality and Roughness

- econometric studies like [52], which involve regularity estimations of volatility from historical high-frequency samples of an asset (e.g., S&P500 index);

“…power law fits the term-structure of ATM skew of equity indexes quite well over a large range of maturities, from 1 month to a few years. But this should not lead one to conclude that the ATM skew blows up like this power law at zero maturity. Zooming in on the short maturities shows that the power-law extrapolation fits the data poorly.”

“As a result, both models could very reasonably be used to extrapolate the ATM skew for very short maturities, and in any case below the first maturity quoted on the market, while leading to different skew asymptotics: finite limiting skew in the 2-factors Bergomi model, and exploding skew in the 2PL model—indicating that the question of the explosive or non-explosive nature of the short-end of the skew curve might be (at least in the case of the SP500 index) hard to disambiguate.”

- it is Gaussian, enabling the utilization of numerous methods from Gaussian process theory including efficient numerical methods, Malliavin calculus, etc. (see, e.g., [138] chapter 5);

- it has stationary increments and is ergodic, which facilitates various statistical estimation techniques (see, e.g., [162]);

- despite being non-semimartingale, fractional Brownian motion has a developed stochastic integration theory [129].

3.4. Usability Challenges of Stochastic Volatility Models

3.4.1. Positivity of Volatility

3.4.2. Possibility of Moment Explosions

3.4.3. Importance of Numerical Methods

4. VIX and the Joint Calibration Puzzle

4.1. Intermezzo: VIX and Its Interpretation

4.2. VIX Smile and the Joint Calibration Puzzle

- The SABR model, Equation (19), gives a flat skew, but its modification, called the mixed SABR modelwhere , , , , generates the required positive slope provided that and ;

- The quadratic rough Heston model, Equation (37).

- Cont and Kokholm [193] use jump diffusions to directly model forward variances and SPX; jumps indeed allow the ATM S&P500 skew and the ATM VIX implied volatility to be de-coupled, giving a good joint fit;

- Guyon and Mustapha [196] achieve an impressive calibration with the modelwhere the drift, volatility, and correlation functions , , , and are modeled with neural networks.

4.3. VIX and Continuous Models: Interpretation Issues

5. Concluding Remarks

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Cont, R. Long range dependence in financial markets. In Fractals in Engineering; Springer: London, UK, 2005; pp. 159–179. [Google Scholar]

- Cutler, D.; Poterba, J.; Summers, L. What moves stock prices? J. Portf. Manag. 1989, 15, 4–12. [Google Scholar] [CrossRef]

- Clark, P.K. A subordinated stochastic process model with finite variance for speculative prices. Econom. J. Econom. Soc. 1973, 41, 135. [Google Scholar] [CrossRef]

- Skiadopoulos, G. Volatility smile consistent option models: A survey. Int. J. Theor. Appl. Financ. 2001, 04, 403–437. [Google Scholar] [CrossRef]

- Shephard, N.; Andersen, T.G. Stochastic volatility: Origins and overview. In Handbook of Financial Time Series; Springer: Berlin/Heidelberg, Germany, 2009; pp. 233–254. [Google Scholar]

- Duong, D.; Swanson, N.R. Volatility in discrete and continuous-time models: A survey with new evidence on large and small jumps. In Missing Data Methods: Time-Series Methods and Applications; Emerald Group Publishing Limited: Bingley, UK, 2011; pp. 179–233. [Google Scholar]

- Markowitz, H. Portfolio Selection. J. Financ. 1952, 7, 77. [Google Scholar] [CrossRef]

- Black, F.; Scholes, M. The Pricing of Options and Corporate Liabilities. J. Political Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Merton, R.C. Theory of rational option pricing. Bell J. Econ. Manag. Sci. 1973, 4, 141. [Google Scholar] [CrossRef]

- Engle, R.F. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econom. J. Econom. Soc. 1982, 50, 987. [Google Scholar] [CrossRef]

- Bollerslev, T. Generalized autoregressive conditional heteroskedasticity. J. Econom. 1986, 31, 307–327. [Google Scholar] [CrossRef]

- Nelson, D.B. Conditional heteroskedasticity in asset returns: A new approach. Econom. J. Econom. Soc. 1991, 59, 347–370. [Google Scholar] [CrossRef]

- Duffie, D.; Pan, J.; Singleton, K. Transform analysis and asset pricing for affine jump-diffusions. Econom. J. Econom. Soc. 2000, 68, 1343–1376. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, O.E.; Shephard, N. Non-Gaussian Ornstein-Uhlenbeck-based models and some of their uses in financial economics. J. R. Stat. Soc. Ser. B Stat. Methodol. 2001, 63, 167–241. [Google Scholar] [CrossRef]

- Bollerslev, T.; Chou, R.Y.; Kroner, K.F. ARCH modeling in finance. J. Econom. 1992, 52, 5–59. [Google Scholar] [CrossRef]

- Francq, C. GARCH Models: Structure, Statistical Inference and Financial Applications, 2nd ed.; Wiley-Blackwell: Hoboken, NJ, USA, 2019. [Google Scholar]

- Barndorff-Nielsen, O.E.; Shephard, N. Lévy Driven Volatility Models. 2011. Available online: https://pure.au.dk/ws/files/193874249/levybook.pdf (accessed on 30 August 2023).

- Gatheral, J. The Volatility Surface: A Practitioner’s Guide; John Wiley & Sons: Nashville, TN, USA, 2006. [Google Scholar]

- Rachev, S.T.; Kim, Y.S.; Bianchi, M.L.; Fabozzi, F.J. Financial Models with Lévy Processes and Volatility Clustering; John Wiley & Sons: Chichester, UK, 2011. [Google Scholar]

- Cont, R.; Tankov, P. Financial Modelling with Jump Processes; Chapman & Hall/CRC: Philadelphia, PA, USA, 2003. [Google Scholar]

- Shiryaev, A.N. Essentials of Stochastic Finance: Facts, Models, Theory; World Scientific Publishing: Singapore, 1999. [Google Scholar]

- Mariani, M.C.; Florescu, I. Quantitative Finance; John Wiley & Sons: Nashville, TN, USA, 2020. [Google Scholar]

- Jovanovic, F.; Le Gall, P. Does God practice a random walk? The “financial physics” of a nineteenth-century forerunner, Jules Regnault. Eur. J. Hist. Econ. Thought 2001, 8, 332–362. [Google Scholar] [CrossRef]

- Regnault, J. Calcul des Chances et Philosophie de la Bourse; Mallet Bachelier and Castel: Paris, France, 1863. [Google Scholar]

- Bachelier, L. Théorie de la spéculation. Ann. Sci. l’Ecole Norm. Super. Quatr. Ser. 1900, 17, 21–86. [Google Scholar] [CrossRef]

- Bachelier, L.; Davis, M.; Etheridge, A. Louis Bachelier’s Theory of Speculation: The Origins of Modern Finance; Translated and with Commentary by Mark Davis and Alison Etheridge; Princeton University Press: Princeton, NJ, USA, 2006. [Google Scholar]

- Einstein, A. Über die von der molekularkinetischen Theorie der Wärme geforderte Bewegung von in ruhenden Flüssigkeiten suspendierten Teilchen. Ann. Phys. 1905, 322, 549–560. [Google Scholar] [CrossRef]

- Osborne, M.F.M. Brownian Motion in the Stock Market. Oper. Res. 1959, 7, 145–173. [Google Scholar] [CrossRef]

- Samuelson, P.A. Mathematics of speculative price. SIAM Rev. 1973, 15, 1–42. [Google Scholar] [CrossRef]

- Revuz, D.; Yor, M. Continuous Martingales and Brownian Motion, 3rd ed.; Springer: Berlin/Heidelberg, Germany, 1999. [Google Scholar]

- Boness, A.J. Elements of a Theory of Stock-Option Value. J. Political Econ. 1964, 72, 163–175. [Google Scholar] [CrossRef]

- Sprenkle, C.M. Warrant prices as indicators of expectations and preferences. Yale Econ. Essays 1959, 1, 179–231. [Google Scholar]

- Thorp, E.O.; Kassouf, S.T. Beat the Market: A Scientific Stock Market System; Random House: New York, NY, USA, 1967. [Google Scholar]

- Samuelson, P.A. Rational theory of warrant pricing. Ind. Manag. Rev. 1959, 6, 13–39. [Google Scholar]

- Samuelson, P.A.; Merton, R.C. A Complete Model of Warrant Pricing that Maximizes Utility. Ind. Manag. Rev. 1972, 10, 17–46. [Google Scholar]

- Black, F. Citation Classic—The Pricing of Options and Corporate Liabilities. Curr. Contents Soc. Behav. Sci. 1987, 33, 16. [Google Scholar]

- Ross, S.A. Finance. In The New Palgrave Dictionary of Economics; Eatwell, J., Milgate, M., Newman, P., Eds.; Springer: London, UK, 1987; Volume 2, pp. 322–336. [Google Scholar]

- Fengler, M. Semiparametric Modeling of Implied Volatility, 2005th ed.; Springer: Berlin/Heidelberg, Germany, 2005. [Google Scholar]

- Wiggins, J.B. Option values under stochastic volatility: Theory and empirical estimates. J. Financ. Econ. 1987, 19, 351–372. [Google Scholar] [CrossRef]

- Jackwerth, J.C.; Rubinstein, M. Recovering probability distributions from option prices. J. Financ. 1996, 51, 1611. [Google Scholar] [CrossRef]

- Latané, H.A.; Rendleman, R.J. Standard deviations of stock price ratios implied in option prices. J. Financ. 1976, 31, 369–381. [Google Scholar] [CrossRef]

- Lee, R.W. Implied volatility: Statics, dynamics, and probabilistic interpretation. In Recent Advances in Applied Probability; Springer: Boston, MA, USA, 2006; pp. 241–268. [Google Scholar]

- S&P 500 Index. Available online: https://finance.yahoo.com/quote/%5ESPX?p=%5ESPX (accessed on 3 May 2023).

- Derman, E.; Miller, M.B.; Park, D. The Volatility Smile; John Wiley & Sons: Nashville, TN, USA, 2016. [Google Scholar]

- Das, S.R.; Sundaram, R.K. Of smiles and smirks: A term structure perspective. J. Financ. Quant. Anal. 1999, 34, 211. [Google Scholar] [CrossRef]

- Carr, P.; Wu, L. The finite moment log stable process and option pricing. J. Financ. 2003, 58, 753–777. [Google Scholar] [CrossRef]

- Comte, F.; Renault, E. Long memory in continuous-time stochastic volatility models. Math. Financ. 1998, 8, 291–323. [Google Scholar] [CrossRef]

- Funahashi, H.; Kijima, M. Does the Hurst index matter for option prices under fractional volatility? Ann. Financ. 2017, 13, 55–74. [Google Scholar] [CrossRef]

- Guyon, J.; El Amrani, M. Does the term-structure of equity at-the-money skew really follow a power law? SSRN Electron. J. 2022. [Google Scholar] [CrossRef]

- Delemotte, J.; De Marco, S.; Segonne, F. Yet another analysis of the SP500 at-the-money skew: Crossover of different power-law behaviours. SSRN Electron. J. 2023. [Google Scholar] [CrossRef]

- Fouque, J.P.; Papanicolaou, G.; Sircar, R.; Sølna, K. Maturity cycles in implied volatility. Financ. Stochastics 2004, 8. [Google Scholar] [CrossRef]

- Gatheral, J.; Jaisson, T.; Rosenbaum, M. Volatility is rough. Quant. Financ. 2018, 18, 933–949. [Google Scholar] [CrossRef]

- Ghysels, E.; Harvey, A.C.; Renault, E. Stochastic volatility. In Handbook of Statistics; Elsevier: Amsterdam, The Netherlands, 1996; pp. 119–191. [Google Scholar]

- Frey, R. Derivative Asset Analysis in Models with Level-Dependent and Stochastic Volatility. CWI Q. 1997, 10, 1–34. [Google Scholar]

- Cont, R. Empirical properties of asset returns: Stylized facts and statistical issues. Quant. Financ. 2001, 1, 223–236. [Google Scholar] [CrossRef]

- Zumbach, G. Discrete Time Series, Processes, and Applications in Finance, 2013rd ed.; Springer: Berlin/Heidelberg, Germany, 2012. [Google Scholar]

- Mandelbrot, B. The Variation of Certain Speculative Prices. J. Bus. 1963, 36, 394–419. [Google Scholar] [CrossRef]

- Fama, E.F. The Behavior of Stock-Market Prices. J. Bus. 1965, 38, 34–105. [Google Scholar] [CrossRef]

- Cootner, P. Random Character of Stock Market Prices; MIT Press: London, UK, 1967. [Google Scholar]

- Barndorff-Nielsen, O.E. Normal inverse Gaussian distributions and stochastic volatility modelling. Scand. J. Stat. Theory Appl. 1997, 24, 1–13. [Google Scholar] [CrossRef]

- Prause, K. The Generalized Hyperbolic Model: Estimation, Financial Derivatives, and Risk Measures. Ph.D. Thesis, Albert-Ludwigs-Universit, Freiburg, Germany, 1999. [Google Scholar]

- Bouchaud, J.P.; Potters, M. Theory of Financial Risks: From Statistical Physics to Risk Management; Cambridge University Press: Cambridge, UK, 2000. [Google Scholar]

- Cont, R.; Potters, M.; Bouchaud, J.P. Scaling in stock market data: Stable laws and beyond. SSRN Electron. J. 1997. [Google Scholar] [CrossRef]

- Eom, C.; Kaizoji, T.; Scalas, E. Fat tails in financial return distributions revisited: Evidence from the Korean stock market. Phys. A 2019, 526, 121055. [Google Scholar] [CrossRef]

- Black, F. Studies of Stock Price Volatility Changes; Business and Economics Section of the American Statistical Association: Washington, DC, USA, 1976; pp. 177–181. [Google Scholar]

- Christie, A. The stochastic behavior of common stock variances: Value, leverage and interest rate effects. J. Financ. Econ. 1982, 10, 407–432. [Google Scholar] [CrossRef]

- Cheung, Y.W.; Ng, L.K. Stock price dynamics and firm size: An empirical investigation. J. Financ. 1992, 47, 1985–1997. [Google Scholar] [CrossRef]

- Duffee, G. Stock returns and volatility a firm-level analysis. J. Financ. Econ. 1995, 37, 399–420. [Google Scholar] [CrossRef]

- Aït-Sahalia, Y.; Fan, J.; Li, Y. The leverage effect puzzle: Disentangling sources of bias at high frequency. J. Financ. Econ. 2013, 109, 224–249. [Google Scholar] [CrossRef]

- Figlewski, S.; Wang, X. Is the “leverage effect” a leverage effect? SSRN Electron. J. 2001. [Google Scholar] [CrossRef]

- Hasanhodzic, J.; Lo, A.W. On Black’s leverage effect in firms with no leverage. J. Portf. Manag. 2019, 46, 106–122. [Google Scholar] [CrossRef]

- Zumbach, G. Volatility conditional on price trends. Quant. Financ. 2010, 10, 431–442. [Google Scholar] [CrossRef]

- Fouque, J.P.; Papanicolaou, G.; Sircar, K.R. Derivatives in Financial Markets with Stochastic Volatility; Cambridge University Press: Cambridge, UK, 2000. [Google Scholar]

- Cont, R. Volatility clustering in financial markets: Empirical facts and agent-based models. In Long Memory in Economics; Springer: Berlin/Heidelberg, Germany, 2006; pp. 289–309. [Google Scholar]

- Bollerslev, T.; Ole Mikkelsen, H. Modeling and pricing long memory in stock market volatility. J. Econom. 1996, 73, 151–184. [Google Scholar] [CrossRef]

- Breidt, F.J.; Crato, N.; de Lima, P. The detection and estimation of long memory in stochastic volatility. J. Econom. 1998, 83, 325–348. [Google Scholar] [CrossRef]

- Ding, Z.; Granger, C.W.J. Modeling volatility persistence of speculative returns: A new approach. J. Econom. 1996, 73, 185–215. [Google Scholar] [CrossRef]

- Ding, Z.; Granger, C.W.J.; Engle, R.F. A long memory property of stock market returns and a new model. J. Empir. Financ. 1993, 1, 83–106. [Google Scholar] [CrossRef]

- Guillaume, D.M.; Dacorogna, M.M.; Davé, R.R.; Müller, U.A.; Olsen, R.B.; Pictet, O.V. From the bird’s eye to the microscope: A survey of new stylized facts of the intra-daily foreign exchange markets. Financ. Stochastics 1997, 1, 95–129. [Google Scholar] [CrossRef]

- Beran, J. Statistics for Long-Memory Processes; Chapman and Hall/CRC: Boca Raton, FL, USA, 1994. [Google Scholar]

- Samorodnitsky, G. Stochastic Processes and Long Range Dependence; Springer International Publishing: Cham, Switzerland, 2016. [Google Scholar]

- Mikosch, T.; Starica, C. Is it really long memory we see in financial returns? Extrem. Integr. Risk Manag. 2000, 12, 149–168. [Google Scholar]

- Willinger, W.; Taqqu, M.S.; Teverovsky, V. Stock market prices and long-range dependence. Financ. Stochastics 1999, 3, 1–13. [Google Scholar] [CrossRef]

- Lobato, I.N.; Velasco, C. Long memory in stock-market trading volume. J. Bus. Econ. Stat. 2000, 18, 410–427. [Google Scholar] [CrossRef]

- Ross, S.A. A Simple Approach to the Valuation of Risky Streams. J. Bus. 1978, 51, 453–475. [Google Scholar] [CrossRef]

- Harrison, J.M.; Kreps, D.M. Martingales and arbitrage in multiperiod securities markets. J. Econ. Theory 1979, 20, 381–408. [Google Scholar] [CrossRef]

- Harrison, J.M.; Pliska, S.R. Martingales and stochastic integrals in the theory of continuous trading. Stoch. Process. Their Appl. 1981, 11, 215–260. [Google Scholar] [CrossRef]

- Kreps, D.M. Arbitrage and equilibrium in economies with infinitely many commodities. J. Math. Econ. 1981, 8, 15–35. [Google Scholar] [CrossRef]

- Delbaen, F.; Schachermayer, W. A general version of the fundamental theorem of asset pricing. Math. Ann. 1994, 300, 463–520. [Google Scholar] [CrossRef]

- Delbaen, F.; Schachermayer, W. The fundamental theorem of asset pricing for unbounded stochastic processes. Math. Ann. 1998, 312, 215–250. [Google Scholar] [CrossRef]

- Delbaen, F.; Schachermayer, W. Mathematics of Arbitrage; Springer: New York, NY, USA, 2006. [Google Scholar]

- Schachermayer, W. The fundamental theorem of asset pricing. In Handbook of the Fundamentals of Financial Decision Making; World Scientific: Singapore, 2013; pp. 31–48. [Google Scholar]

- Cox, J.C. Notes on Option pricing I: The constant elasticity of variance option pricing model. J. Portf. Manag. 1997, 23, 15–17. [Google Scholar] [CrossRef]

- Cox, J.C.; Ross, S.A. The valuation of options for alternative stochastic processes. J. Financ. Econ. 1976, 3, 145–166. [Google Scholar] [CrossRef]

- Emanuel, D.C.; MacBeth, J.D. Further results on the constant elasticity of variance call option pricing model. J. Financ. Quant. Anal. 1982, 17, 533. [Google Scholar] [CrossRef]

- Linetsky, V.; Mendoza, R. Constant elasticity of variance (CEV) diffusion model. Encycl. Quant. Financ. 2010. [Google Scholar] [CrossRef]

- Yamada, T.; Watanabe, S. On the uniqueness of solutions of stochastic differential equations. Kyoto J. Math. 1971, 11, 155–167. [Google Scholar] [CrossRef]

- Cherny, A.S.; Engelbert, H.J. Singular Stochastic Differential Equations; Springer: Berlin/Heidelberg, Germany, 2005. [Google Scholar]

- Andersen, L.B.G.; Piterbarg, V.V. Moment explosions in stochastic volatility models. Financ. Stochastics 2006, 11, 29–50. [Google Scholar] [CrossRef]

- Derman, E.; Kani, I. Riding on the Smile. Risk 1994, 7, 32–39. [Google Scholar]

- Dupire, B. Pricing with a smile. Risk 1994, 7, 18–20. [Google Scholar]

- Bergomi, L. Stochastic Volatility Modeling; Chapman & Hall/CRC: Oakville, MO, USA, 2016. [Google Scholar]

- Buraschi, A.; Jackwerth, J. The price of a smile: Hedging and spanning in option markets. Rev. Financ. Stud. 2001, 14, 495–527. [Google Scholar] [CrossRef]

- Dumas, B.; Fleming, J.; Whaley, R.E. Implied volatility functions: Empirical tests. J. Financ. 1998, 53, 2059–2106. [Google Scholar] [CrossRef]

- Aït-Sahalia, Y.; Jacod, J. Testing Whether Volatility Can Be Written As a Function of the Asset Price. In Workshop on Asset Pricing and Risk Management; Duke University: Durham, NC, USA, 2019. [Google Scholar]

- Hull, J.; White, A. The pricing of options on assets with stochastic volatilities. J. Financ. 1987, 42, 281–300. [Google Scholar] [CrossRef]

- Scott, L.O. Option pricing when the variance changes randomly: Theory, estimation, and an application. J. Financ. Quant. Anal. 1987, 22, 419. [Google Scholar] [CrossRef]

- Stein, E.M.; Stein, J.C. Stock Price Distributions with Stochastic Volatility: An Analytic Approach. Rev. Financ. Stud. 1991, 4, 727–752. [Google Scholar] [CrossRef]

- Schöbel, R.; Zhu, J. Stochastic volatility with an Ornstein–Uhlenbeck process: An extension. Rev. Financ. 1999, 3, 23–46. [Google Scholar] [CrossRef]

- Heston, S.L. A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options. Rev. Financ. Stud. 1993, 6, 327–343. [Google Scholar] [CrossRef]

- Cox, J.C.; Ingersoll, J.E.; Ross, S.A. A theory of the term structure of interest rates. Econom. J. Econom. Soc. 1985, 53, 385–407. [Google Scholar] [CrossRef]

- Benhamou, E.; Gobet, E.; Miri, M. Time dependent Heston model. SIAM J. Financ. Math. 2010, 1, 289–325. [Google Scholar] [CrossRef]

- Goutte, S.; Ismail, A.; Pham, H. Regime-switching stochastic volatility model: Estimation and calibration to VIX options. Appl. Math. Financ. 2017, 24, 38–75. [Google Scholar] [CrossRef]

- Melino, A.; Turnbull, S.M. Pricing foreign currency options with stochastic volatility. J. Econom. 1990, 45, 239–265. [Google Scholar] [CrossRef]

- Melino, A.; Turnbull, S.M. Misspecification and the pricing and hedging of long-term foreign currency options. J. Int. Money Financ. 1995, 14, 373–393. [Google Scholar] [CrossRef]

- Hagan, P.; Kumar, D.; Lesniewski, A.; Woodward, D. Managing Smile Risk. Wilmott Mag. 2002, 1, 84–108. [Google Scholar]

- Lewis, A.L. Option Valuation under Stochastic Volatility; Finance Press: Vancouver, BC, Canada, 2000. [Google Scholar]

- Carr, P.; Sun, J. A new approach for option pricing under stochastic volatility. Rev. Deriv. Res. 2007, 10, 87–150. [Google Scholar] [CrossRef]

- Baldeaux, J.; Badran, A. Consistent Modelling of VIX and Equity Derivatives Using a 3/2 plus Jumps Model. Appl. Math. Financ. 2014, 21, 299–312. [Google Scholar] [CrossRef]

- Javaheri, A. The volatility process: A study of stock market dynamics via para- metric stochastic volatility models and a comparison to the information embedded in option prices. Ph.D. Thesis, Ecole de Mines de Paris, Paris, France, 2004. [Google Scholar]

- Bakshi, G.; Ju, N.; Ou-Yang, H. Estimation of continuous-time models with an application to equity volatility dynamics. J. Financ. Econ. 2006, 82, 227–249. [Google Scholar] [CrossRef]

- Gatheral, J. Consistent Modeling of SPX and VIX options. In Proceedings of the 5th World Congress of the Bachelier Finance Society, London, UK, 15–19 July 2008. [Google Scholar]

- Fouque, J.P.; Papanicolaou, G.; Sircar, R.; Sølna, K. Multiscale stochastic volatility asymptotics. Multiscale Model. Simul. 2003, 2, 22–42. [Google Scholar] [CrossRef]

- Fouque, J.P.; Saporito, Y.F. Heston stochastic vol-of-vol model for joint calibration of VIX and S&P 500 options. Quant. Financ. 2018, 18, 1003–1016. [Google Scholar] [CrossRef]

- Renault, E.; Touzi, N. Option hedging and implied volatilities in a stochastic volatility model. Math. Financ. 1996, 6, 279–302. [Google Scholar] [CrossRef]

- Alòs, E.; León, J.A.; Vives, J. On the short-time behavior of the implied volatility for jump-diffusion models with stochastic volatility. Financ. Stochastics 2007, 11, 571–589. [Google Scholar] [CrossRef]

- Kolmogorov, A. Wiener Spirals and some other interesting curves in Hilbert space. Dokl Akad. Nauk SSSR 1940, 26, 115–118. [Google Scholar]

- Mandelbrot, B.B.; Van Ness, J.W. Fractional Brownian motions, fractional noises and applications. SIAM Rev. 1968, 10, 422–437. [Google Scholar] [CrossRef]

- Mishura, Y. Stochastic Calculus for Fractional Brownian Motion and Related Processes, 2008th ed.; Springer: Berlin/Heidelberg, Germany, 2007. [Google Scholar]

- Rosenbaum, M. Estimation of the volatility persistence in a discretely observed diffusion model. Stoch. Process. Their Appl. 2008, 118, 1434–1462. [Google Scholar] [CrossRef]

- Chronopoulou, A.; Viens, F.G. Estimation and pricing under long-memory stochastic volatility. Ann. Financ. 2012, 8, 379–403. [Google Scholar] [CrossRef]

- Bezborodov, V.; Persio, L.D.; Mishura, Y. Option Pricing with Fractional Stochastic Volatility and Discontinuous Payoff Function of Polynomial Growth. Methodol. Comput. Appl. Probab. 2018, 21, 331–366. [Google Scholar] [CrossRef]

- Mishura, Y.; Yurchenko-Tytarenko, A. Fractional Cox–Ingersoll–Ross process with non-zero “mean”. Mod. Stochastics Theory Appl. 2018, 5, 99–111. [Google Scholar] [CrossRef]

- Mishura, Y.; Yurchenko-Tytarenko, A. Fractional Cox–Ingersoll–Ross process with small Hurst indices. Mod. Stochastics Theory Appl. 2018, 6, 13–39. [Google Scholar] [CrossRef]

- Mishura, Y.; Yurchenko-Tytarenko, A. Approximating expected value of an option with non-Lipschitz payoff in fractional Heston-type model. Int. J. Theor. Appl. Financ. 2020, 23, 2050031. [Google Scholar] [CrossRef]

- Bäuerle, N.; Desmettre, S. Portfolio optimization in fractional and rough Heston models. SIAM J. Financ. Math. 2020, 11, 240–273. [Google Scholar] [CrossRef]

- Alòs, E.; Garcia Lorite, D. Malliavin Calculus in Finance: Theory and Practice; CRC Press: London, UK, 2021. [Google Scholar]

- Nualart, D. The Malliavin Calculus and Related Topics; Springer: Berlin/Heidelberg, Germany, 2006. [Google Scholar]

- Gihman, I.; Skorokhod, A. The Theory of Stochastic Processes I; Springer: Berlin/Heidelberg, Germany, 2004. [Google Scholar]

- Fukasawa, M. Volatility has to be rough. Quant. Financ. 2021, 21, 1–8. [Google Scholar] [CrossRef]

- Rough Volatility Literature. Available online: https://sites.google.com/site/roughvol/home/rough-volatility-literature?authuser=0 (accessed on 30 August 2023).

- Bayer, C.; Friz, P.; Gatheral, J. Pricing under rough volatility. Quant. Financ. 2016, 16, 887–904. [Google Scholar] [CrossRef]

- Jacquier, A.; Martini, C.; Muguruza, A. On VIX futures in the rough Bergomi model. Quant. Financ. 2018, 18, 45–61. [Google Scholar] [CrossRef]

- Guyon, J. On the Joint Calibration of SPX and VIX Options: A Dispersion-Constrained Martingale Transport Approach. In Proceedings of the Research in Options 2019, IMPA, Rio de Janeiro, Brazil, 15–19 July 2019. [Google Scholar]

- Lacombe, C.; Muguruza, A.; Stone, H. Asymptotics for volatility derivatives in multi-factor rough volatility models. Math. Financ. Econ. 2021, 15, 545–577. [Google Scholar] [CrossRef]

- Fukasawa, M.; Gatheral, J. A rough SABR formula. Front. Math. Financ. 2022, 1, 81. [Google Scholar] [CrossRef]

- Harms, P.; Stefanovits, D. Affine representations of fractional processes with applications in mathematical finance. Stoch. Process. Their Appl. 2019, 129, 1185–1228. [Google Scholar] [CrossRef]

- Garnier, J.; Sølna, K. Optimal hedging under fast-varying stochastic volatility. Siam J. Financ. Math. 2020, 11, 274–325. [Google Scholar] [CrossRef]

- El Euch, O.; Rosenbaum, M. The characteristic function of rough Heston models. Math. Financ. 2019, 29, 3–38. [Google Scholar] [CrossRef]

- Gatheral, J.; Jusselin, P.; Rosenbaum, M. The quadratic rough Heston model and the joint S&P 500/VIX smile calibration problem. SSRN Electron. J. 2020. [Google Scholar] [CrossRef]

- Rosenbaum, M.; Zhang, J. Deep calibration of the quadratic rough Heston model. arXiv 2021, arXiv:2107.01611. [Google Scholar]

- Dandapani, A.; Jusselin, P.; Rosenbaum, M. From quadratic Hawkes processes to super-Heston rough volatility models with Zumbach effect. Quant. Financ. 2021, 21, 1235–1247. [Google Scholar] [CrossRef]

- El Euch, O.; Gatheral, J.; Radoičić, R.; Rosenbaum, M. The Zumbach effect under rough Heston. Quant. Financ. 2020, 20, 235–241. [Google Scholar] [CrossRef]

- El Euch, O.; Fukasawa, M.; Rosenbaum, M. The microstructural foundations of leverage effect and rough volatility. Financ. Stochastics 2018, 22, 241–280. [Google Scholar] [CrossRef]

- Rogers, L.C.G. Things We Think We Know (Working Paper). 2019. Available online: https://www.skokholm.co.uk/wp-content/uploads/2019/11/TWTWKpaper.pdf (accessed on 23 August 2023).

- Cont, R.; Das, P. Rough volatility: Fact or artefact? arXiv 2022, arXiv:2203.13820. [Google Scholar] [CrossRef]

- Fukasawa, M.; Takabatake, T.; Westphal, R. Is volatility rough? arXiv 2019, arXiv:1905.04852. [Google Scholar]

- Fukasawa, M.; Takabatake, T.; Westphal, R. Consistent estimation for fractional stochastic volatility model under high-frequency asymptotics. Math. Financ. Int. J. Math. Stat. Financ. Econ. 2022, 32, 1086–1132. [Google Scholar] [CrossRef]

- Bolko, A.E.; Christensen, K.; Pakkanen, M.S.; Veliyev, B. A GMM approach to estimate the roughness of stochastic volatility. J. Econom. 2023, 235, 745–778. [Google Scholar] [CrossRef]

- Funahashi, H.; Kijima, M. A solution to the time-scale fractional puzzle in the implied volatility. Fractal Fract. 2017, 1, 14. [Google Scholar] [CrossRef]

- Bennedsen, M.; Lunde, A.; Pakkanen, M.S. Decoupling the short- and long-term behavior of stochastic volatility. J. Financ. Econom. 2022, 20, 961–1006. [Google Scholar] [CrossRef]

- Kubilius, K.; Mishura, Y.; Ralchenko, K. Parameter Estimation in Fractional Diffusion Models; Springer International Publishing: Cham, Switzerland, 2017. [Google Scholar]

- Corlay, S.; Lebovits, J.; Lévy Véhel, J. Multifractional stochastic volatility models. Math. Financ. 2014, 24, 364–402. [Google Scholar] [CrossRef]

- Ayache, A.; Peng, Q. Stochastic volatility and multifractional Brownian motion. In Stochastic Differential Equations and Processes; Springer: Berlin/Heidelberg, Germany, 2012; pp. 211–237. [Google Scholar]

- Catalini, G.; Pacchiarotti, B. Asymptotics for multifactor Volterra type stochastic volatility models. Stoch. Anal. Appl. 2022, 1–31. [Google Scholar] [CrossRef]

- Merino, R.; Pospíšil, J.; Sobotka, T.; Sottinen, T.; Vives, J. Decomposition formula for rough Volterra stochastic volatility models. Int. J. Theor. Appl. Financ. 2021, 24, 2150008. [Google Scholar] [CrossRef]

- Di Nunno, G.; Mishura, Y.; Yurchenko-Tytarenko, A. Option pricing in Volterra sandwiched volatility model. arXiv 2022, arXiv:2209.10688. [Google Scholar] [CrossRef]

- Di Nunno, G.; Yurchenko-Tytarenko, A. Sandwiched Volterra Volatility model: Markovian approximations and hedging. arXiv 2022, arXiv:2209.13054. [Google Scholar] [CrossRef]

- Biagini, F.; Guasoni, P.; Pratelli, M. Mean-Variance Hedging for Stochastic Volatility Models. Math. Financ. 2000, 10, 109–123. [Google Scholar] [CrossRef]

- Alòs, E.; Rolloos, F.; Shiraya, K. Forward start volatility swaps in rough volatility models. arXiv 2022, arXiv:2207.10370. [Google Scholar] [CrossRef]

- Ocone, D.L.; Karatzas, I. A generalized Clark representation formula, with application to optimal portfolios. Stochastics Stochastics Rep. 1991, 34, 187–220. [Google Scholar] [CrossRef]

- Edwards, T.; Lazzara, C. Realized Volatility Indices: Measuring Market Risk; Research for S&P Dow Jones Indices; McGraww Hill Financial: New York, NY, USA, 2016. [Google Scholar]

- Abi Jaber, E.; El Euch, O. Multifactor approximation of rough volatility models. SIAM J. Financ. Math. 2019, 10, 309–349. [Google Scholar] [CrossRef]

- Abi Jaber, E.; Illand, C.; Li, S. Joint SPX-VIX calibration with Gaussian polynomial volatility models: Deep pricing with quantization hints. arXiv 2022, arXiv:2212.08297. [Google Scholar] [CrossRef]

- Di Nunno, G.; Mishura, Y.; Yurchenko-Tytarenko, A. Drift-implicit Euler scheme for sandwiched processes driven by Hölder noises. Numer. Algorithms 2023, 93, 459–491. [Google Scholar] [CrossRef]

- CBOE. Cboe Global Markets Annual Report 2022; Cboe Global Markets, Inc.: Chicago, IL, USA, 2023. [Google Scholar]

- Carr, P.; Lee, R. Volatility derivatives. Annu. Rev. Financ. Econ. 2009, 1, 319–339. [Google Scholar] [CrossRef]

- Gastineau, G.L. An index of listed option premiums. Financ. Anal. J. 1977, 33, 70–75. [Google Scholar] [CrossRef]

- Cox, J.C.; Rubinstein, M. Options Markets; Pearson: Upper Saddle River, NJ, USA, 1985. [Google Scholar]

- Brenner, M.; Galai, D. New financial instruments for hedging changes in volatility. Financ. Anal. J. 1989, 45, 61–65. [Google Scholar] [CrossRef]

- Fleming, J.; Ostdiek, B.; Whaley, R.E. Predicting stock market volatility: A new measure. J. Futur. Mark. 1995, 15, 265–302. [Google Scholar] [CrossRef]

- Breeden, D.T.; Litzenberger, R.H. Prices of state-contingent claims implicit in option prices. J. Bus. 1978, 51, 621–651. [Google Scholar] [CrossRef]

- Dupire, B. Arbitrage Pricing with Stochastic Volatility. 1993. Available online: https://cims.nyu.edu/~essid/ctf/stochvol.pdf (accessed on 30 August 2023).

- Carr, P.; Madan, D. Towards a theory of volatility trading. In Volatility; Jarrow, R., Ed.; Risk Publications: London, UK, 1998; pp. 417–427. [Google Scholar]

- Guyon, J. Dispersion-constrained martingale Schrödinger problems and the exact joint S&P 500/VIX smile calibration puzzle. SSRN Electron. J. 2021. [Google Scholar] [CrossRef]

- VIX Index Historical Data. Available online: https://www.cboe.com/tradable_products/vix/vix_historical_data/ (accessed on 26 September 2023).

- CBOE. Volatility Index Methodology: Cboe Volatility Index. 2023. Available online: https://cdn.cboe.com/api/global/us_indices/governance/Volatility_Index_Methodology_Cboe_Volatility_Index.pdf (accessed on 30 August 2023).

- Kwok, Y.K.; Zheng, W. Pricing Models of Volatility Products and Exotic Variance Derivatives; Chapman & Hall/CRC: Philadelphia, PA, USA, 2022. [Google Scholar]

- Alòs, E.; García-Lorite, D.; Gonzalez, A.M. On smile properties of volatility derivatives: Understanding the VIX skew. SIAM J. Financ. Math. 2022, 13, 32–69. [Google Scholar] [CrossRef]

- Kokholm, T.; Stisen, M. Joint pricing of VIX and SPX options with stochastic volatility and jump models. J. Risk Financ. 2015, 16, 27–48. [Google Scholar] [CrossRef]

- Rømer, S.E. Empirical analysis of rough and classical stochastic volatility models to the SPX and VIX markets. Quant. Financ. 2022, 22, 1805–1838. [Google Scholar] [CrossRef]

- Abi Jaber, E.; Illand, C.; Li, S. The quintic Ornstein-Uhlenbeck volatility model that jointly calibrates SPX & VIX smiles. arXiv 2022, arXiv:2212.10917. [Google Scholar] [CrossRef]

- Cont, R.; Kokholm, T. A Consistent Pricing Model for Index Options and Volatility Derivatives. Math. Financ. 2013, 23, 248–274. [Google Scholar] [CrossRef]

- Guyon, J. The joint S&P 500/VIX smile calibration puzzle solved. SSRN Electron. J. 2019. [Google Scholar] [CrossRef]

- Guyon, J.; Bourgey, F. Fast exact joint S&P 500/VIX smile calibration in discrete and continuous time. SSRN Electron. J. 2022. [Google Scholar] [CrossRef]

- Guyon, J.; Mustapha, S. Neural joint S&P 500/VIX smile calibration. SSRN Electron. J. 2022. [Google Scholar] [CrossRef]

- Aït-Sahalia, Y.; Karaman, M.; Mancini, L. The term structure of equity and variance risk premia. J. Econom. 2020, 219, 204–230. [Google Scholar] [CrossRef]

- Andersen, T.G.; Bondarenko, O.; Gonzalez-Perez, M.T. Exploring return dynamics via corridor implied volatility. Rev. Financ. Stud. 2015, 28, 2902–2945. [Google Scholar] [CrossRef]

- Carr, P.; Lee, R.; Wu, L. Variance swaps on time-changed Lévy processes. Financ. Stochastics 2012, 16, 335–355. [Google Scholar] [CrossRef]

- Martin, I. Simple Variance Swaps; NBER Working Paper Series; National Bureau of Economic Research: Cambridge, MA, USA, 2011. [Google Scholar]

- Guyon, J.; Lekeufack, J. Volatility is (mostly) path-dependent. Quant. Financ. 2023, 23, 1221–1258. [Google Scholar] [CrossRef]

- Buehler, H.; Gonon, L.; Teichmann, J.; Wood, B. Deep hedging. Quant. Financ. 2019, 19, 1271–1291. [Google Scholar] [CrossRef]

- Bühler, H.; Horvath, B.; Lyons, T.; Arribas, I.P.; Wood, B. A data-driven market simulator for small data environments. arXiv 2020, arXiv:2006.14498. [Google Scholar] [CrossRef]

- Cuchiero, C.; Gazzani, G.; Möller, J.; Svaluto-Ferro, S. Joint calibration to SPX and VIX options with signature-based models. arXiv 2023, arXiv:2301.13235. [Google Scholar] [CrossRef]

- Cuchiero, C.; Gazzani, G.; Svaluto-Ferro, S. Signature-based models: Theory and calibration. SIAM J. Financ. Math. 2023, 14, 910–957. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Di Nunno, G.; Kubilius, K.; Mishura, Y.; Yurchenko-Tytarenko, A. From Constant to Rough: A Survey of Continuous Volatility Modeling. Mathematics 2023, 11, 4201. https://doi.org/10.3390/math11194201

Di Nunno G, Kubilius K, Mishura Y, Yurchenko-Tytarenko A. From Constant to Rough: A Survey of Continuous Volatility Modeling. Mathematics. 2023; 11(19):4201. https://doi.org/10.3390/math11194201

Chicago/Turabian StyleDi Nunno, Giulia, Kęstutis Kubilius, Yuliya Mishura, and Anton Yurchenko-Tytarenko. 2023. "From Constant to Rough: A Survey of Continuous Volatility Modeling" Mathematics 11, no. 19: 4201. https://doi.org/10.3390/math11194201

APA StyleDi Nunno, G., Kubilius, K., Mishura, Y., & Yurchenko-Tytarenko, A. (2023). From Constant to Rough: A Survey of Continuous Volatility Modeling. Mathematics, 11(19), 4201. https://doi.org/10.3390/math11194201