5.1. Model Description

In this paper, the multivariate DCC-GARCH models proposed by [

61] Engle and Kevin Sheppard (2002) were used to estimate the dynamic conditional correlations between the stock returns of four emerging CEEC countries and the ones from the US and Germany.

The DCC-GARCH model has many advantages, such as estimating the standardized residuals’ correlation coefficients, and this directly accounts for heteroskedasticity. Additional explanatory variables can be added to the mean equation of the model to measure a common factor. Moreover, this model estimated parameters that increased linearly with the number of stock returns, so the model is relatively parsimonious.

The DCC-GARCH model requires a two-step estimation, thus, the number of simultaneously estimated parameters is small. In the first step, univariate GARCH models are fitted to each stock return, while in the second step, the residuals of the returns are trans- formed by their estimated standard deviations (obtained in the first step). These standardized residuals are further used to estimate the correlation coefficients. The time-varying correlation coefficients estimates provide dynamic trajectories of correlation behavior for the stock indices’ return rates, both in times of normal economic evolution and in times of financial crisis.

The stock market returns are assumed to follow this process:

where

,

and

.

is a (

n × 1) vector of stock market returns and

εt is a (

n × 1) vector of conditional residuals. In this study, the vector

rt consists of the returns on the four CEEC stock indices (BET, PX, BUX, WIG), as well as the rates of return on stock indices from the two developed countries considered (S&P500 and DAX). We initially considered both developed markets (US and German markets) with one day delay.

Potential motivation for the inclusion of the developed stock markets in the mean equation is that they serve as global (US) and regional (Germany) factors, playing a crucial role in determining the rates of return on stock indices from Central and Eastern Europe, [

6] (Chiang et al., 2007).

Within the analysis, we have also incorporated the different time zones (Drożdż et al., 2001 [

60]) in which the European and the US stock markets are traded, additionally estimating a new DCC-GARCH model for DAX index without delay.

The conditional variance–covariance matrix is further specified as follows:

where

is a diagonal matrix of size (

n ×

n), which contains time-varying standard deviations that are obtained from univariate GARCH models.

presents the terms

on the ith diagonal,

i = 1, 2, …,

n (The univariate GARCH(1,1) model is specified as:

, for

i = 1, 2, …,

n), and

is the time-varying correlation matrix of size (

n ×

n).

The DCC-GARCH model proposed by [

61] Engle and Sheppard (2002) involve two stages of estimation of the conditional variance–covariance matrix

:

- -

in the first stage, univariate volatility models are fitted for each rate of return and estimates for are obtained.

- -

in the second stage, stock return residuals are transformed by their estimated standard deviations, (obtained in the first stage), as follows: , then is used to estimate the parameters of the conditional correlation.

The expression gives the evolution of the correlation in the DCC-GARCH model:

where

is the (

n ×

n) time-varying variance–covariance matrix of

,

is the (

n ×

n) unconditional variance–covariance matrix of

, while

are non-negative scalar parameters that satisfy the expression

. (A typical element of

is:

, where

represents the unconditional correlations of

).

Because the matrix

is a variance–covariance matrix, it generally does not have the value 1 on the diagonal; therefore, it is adjusted to obtain an appropriate correlation matrix

. Thus:

where

is a diagonal matrix containing the elements

…

. Matrix

resizes the items in the

matrix, so that

1.

Now

from Equation (4) is a correlation matrix with the value 1 on the diagonal and off-diagonal elements smaller than 1 in absolute value, if

is positively definite.

5.2. Empirical Results and Discussions

In the first stage of the model, the volatilities of the returns on the four CEEC stock market indices were analyzed through univariate GARCH models, which highlighted, for all series, a first-order autoregressive structure, AR (1). This shows that the stock returns from the previous day significantly influence the returns of the current day. The empirical results unanimously reveal that the GARCH (1,1) model is optimal for all stock indices.

In the second phase of the analysis, the dynamic structure of the four emerging stock markets and the potential contagion effect from the two developed markets were explored. This was achieved by estimating two DCC-GARCH models in which S&P500 and DAX function as exogenous variables.

The results of the multivariate DCC-GARCH models are presented in

Table 1 and

Table 2. The models were run, one at a time, for each stock return on the four CEEC indices, first with the returns on the S&P500 index (as a global exogenous factor), and subsequently with the returns on the DAX index (as a regional exogenous factor).

Each table contains three sections, presenting the estimates of the coefficients from the following equations:

Panel B: Variance equation:

Panel A, from both tables, indicates that the intercept in the mean equation (Equation (1)) is statistically significant for all stock markets, while the term AR (1), , is statistically significant and negative for the Czech Republic and Poland and statistically significant and positive for Romania.

In

Table 1, the influence of the US stock market over the markets from the CEEC is highlighted by the term

, which is statistically significant for all Central and Eastern European stock markets at the 1% level. In

Table 2, the same coefficient is also significant at the 5% level, suggesting that the DAX index also influences the stock markets in Romania, the Czech Republic, Hungary, and Poland. These results are consistent with those in the literature [

6] (Chiang et al., 2007), which argue that the US and Germany play an important role in the evolution of emerging markets at both the global and regional level; in this case, the influence is observed on the stock markets in Central and Eastern Europe. Similar results have been obtained by [

11] Grabowski (2019), highlighting the significant impact of the US stock market on the euro area and transition countries.

Panel B contains the estimators in the variance equation. The coefficients (of the ARCH term—) and (of the GARCH term—) are statistically significant, justifying the use of the GARCH (1,1) model to capture the contagion effect in the analyzed markets. Furthermore, the persistence of volatility, measured by the sum of the coefficients and , is very close to 1 for all the stock markets examined. This indicates that volatility in the GARCH models is highly persistent.

The two rows in panel C represent the estimators of the DCC (1,1) parameters, a and b. Both parameters are statistically significant in correlation with the S&P500 and the DAX indices, revealing a substantial co-movement that varies over time between these stock returns. Furthermore, the conditional correlation coefficients also show high persistence, with the sum of the two coefficients (a + b) being more than 0.90 during the period considered.

We also tested the implications of different time zones in which the European and the US stock markets are traded, building a new DCCC-GARCH model that considers the German market as a benchmark and where the returns on the DAX index are considered as a regional exogenous factor (

Table 3.).

In each table, Panel A indicates that the intercept in the mean equation (Equation (1)) is statistically significant for all stock markets, while the term AR (1),

γ1, is statistically significant and negative for the Czech Republic and Poland and statistically significant and positive for Romania. In

Table 3, the influence of the German stock market over the markets from the CEEC is highlighted by the term

γ2, which is statistically significant for all Central and Eastern European stock markets at the 5% level, suggesting that the DAX index influences, as well, the stock markets in Romania, the Czech Republic, Hungary and Poland. These results are consistent with those in the literature [

8] (Chiang et al., 2007), which argue that the US and Germany play an important role at the global and regional levels.

In Panel B, which contains the estimators in the variance equation, the coefficients αi are statistically significant, justifying the use of the GARCH (1,1) model to capture the contagion effect in the analyzed markets. Furthermore, the persistence of volatility, measured by the sum of the coefficients αi and βi, is very close to 1 for all the stock markets examined. This indicates that volatility in the GARCH models is highly persistent. The two rows in panel C represent the estimators of the DCC (1,1) parameters, a and b. Furthermore, the conditional correlation coefficients also show high persistence, with the sum of the two coefficients (a + b) being more than 0.90 during the period considered.

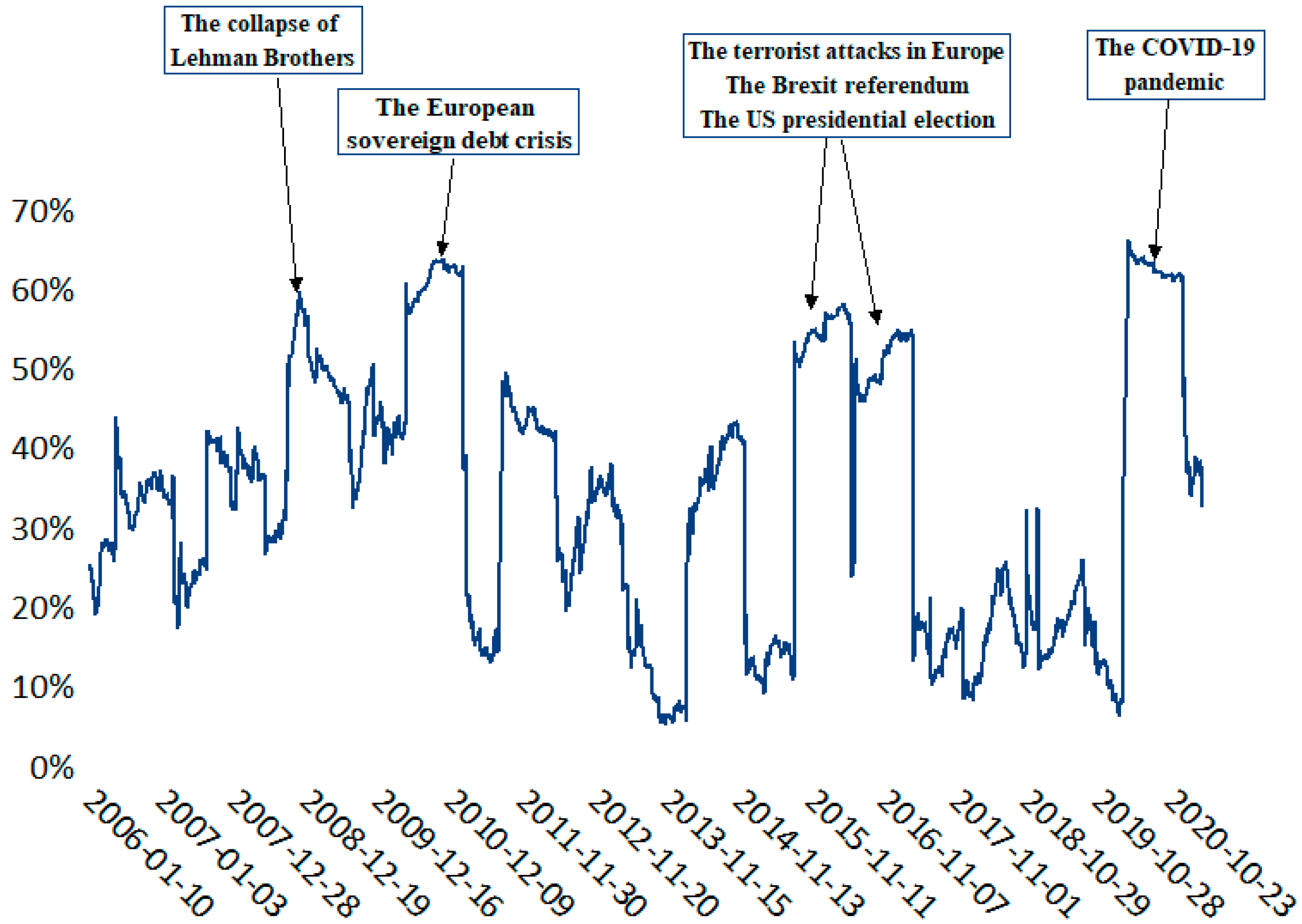

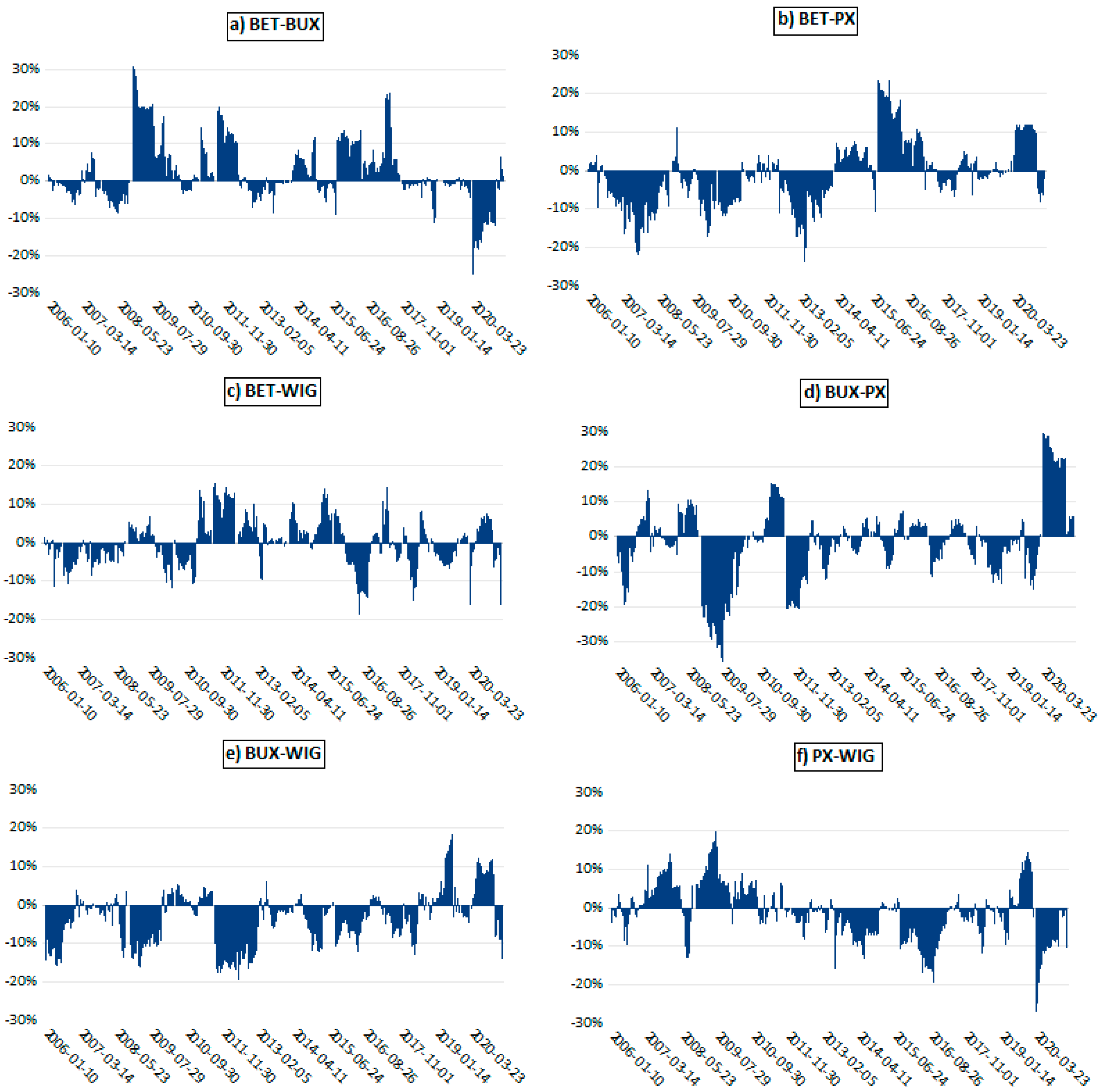

One of the most essential advantages of the DCC-GARCH model is obtaining all the possible correlations between the examined variables, allowing for study of coefficient behavior during periods of particular interest, such as economic crises.

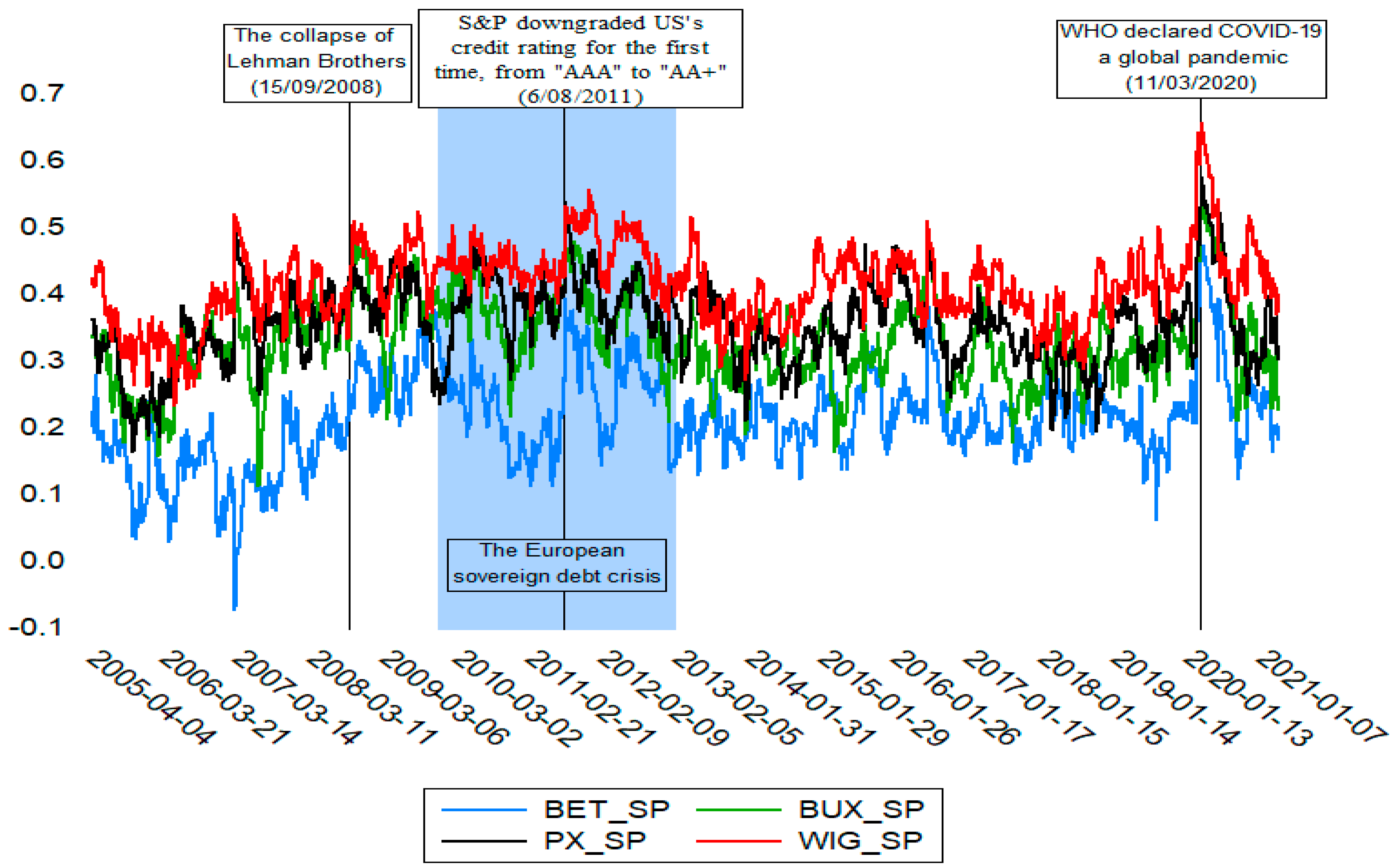

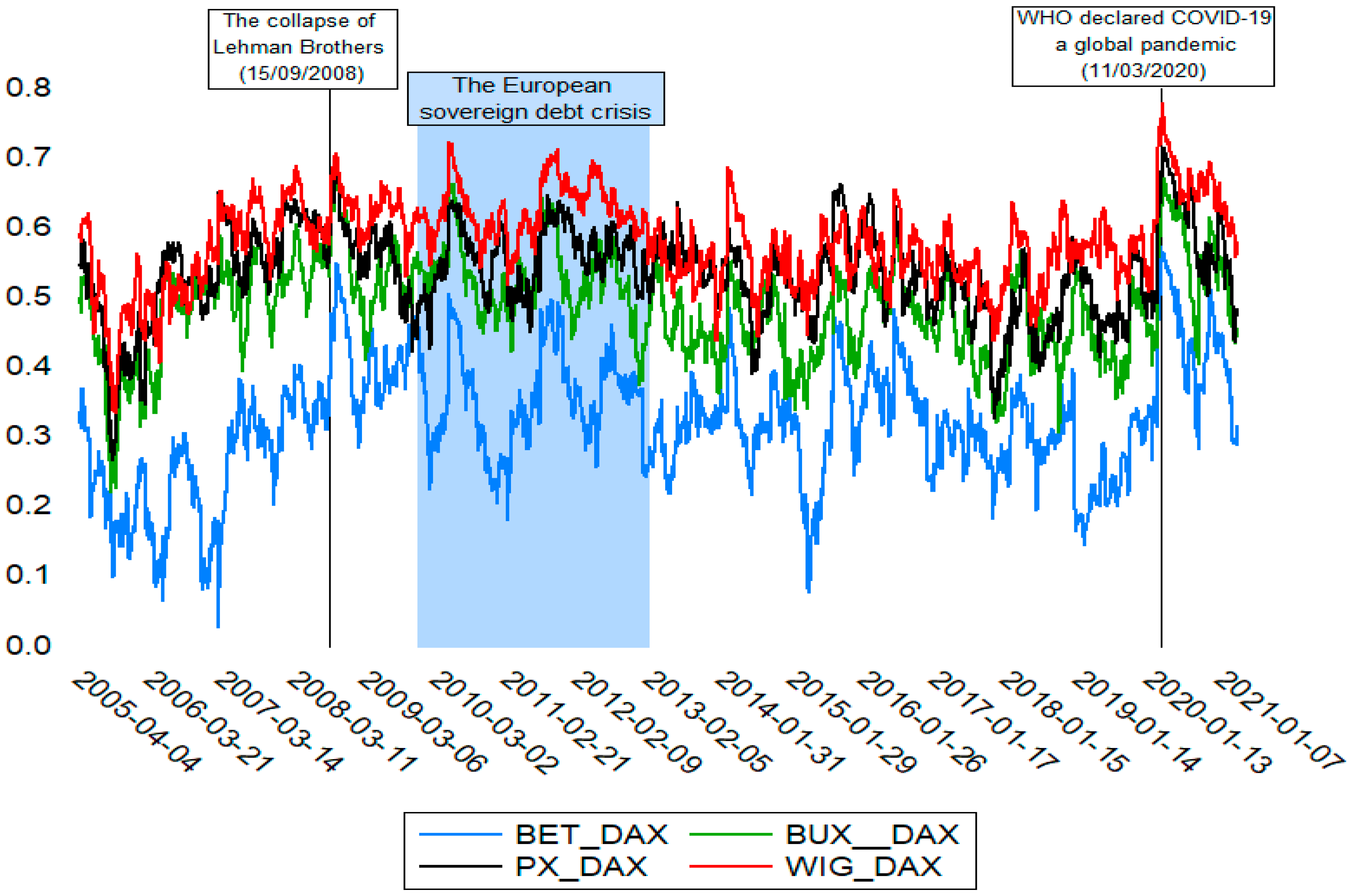

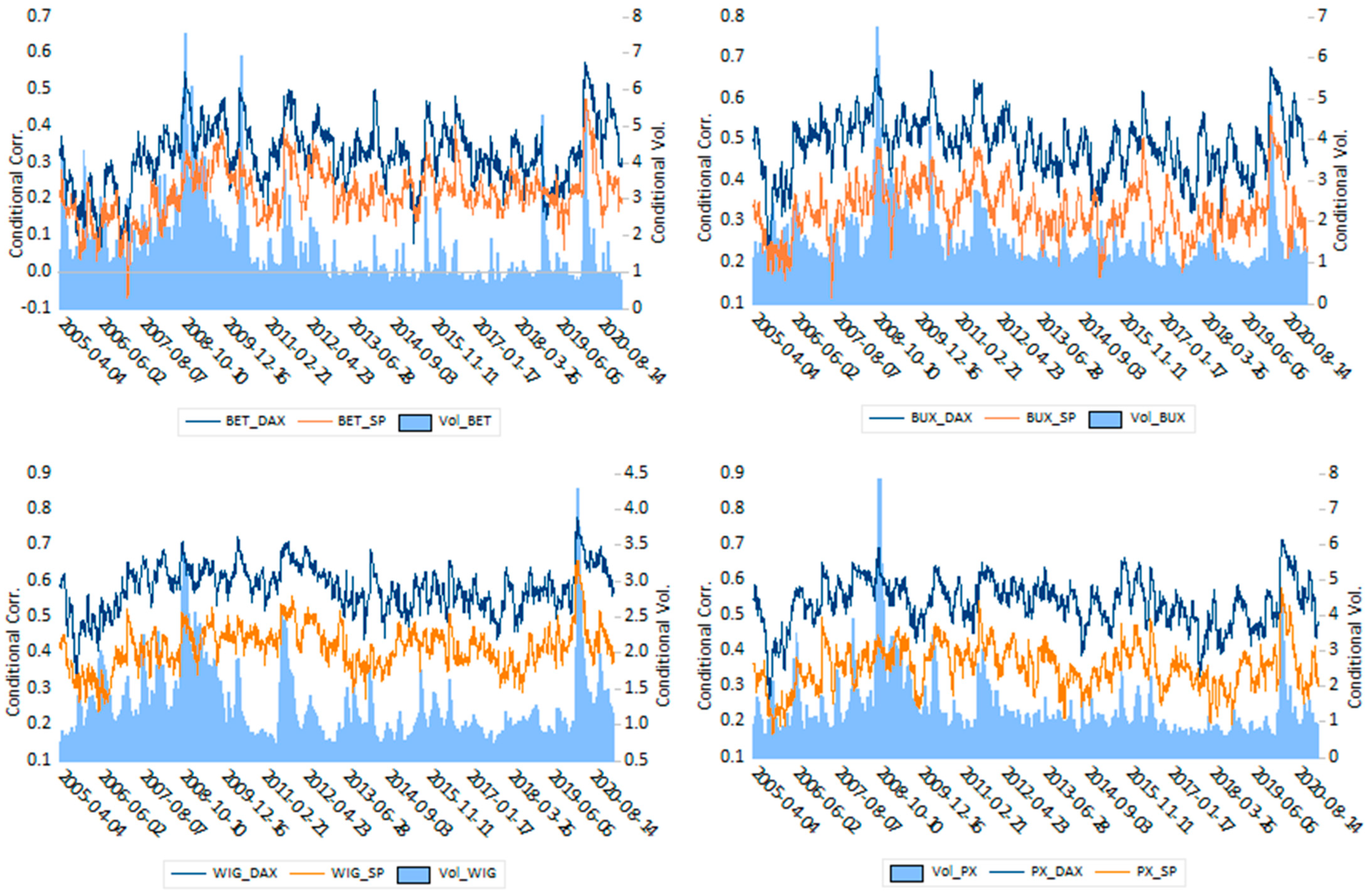

Therefore, the conditional correlation coefficients between the four CEEC stock indices and the S&P500 index, followed by the DAX index, were estimated, their graphic representations are shown in

Figure 2 and

Figure 3. In both models, we have considered one day delay for both markets (US and German). In

Appendix G, for each CEEC index, conditional correlations are presented along with the conditional volatilities, which were calculated in the first stage of the DCC-GARCH model.

Figure 2 and

Figure 3 show that the stock markets in Central and Eastern Europe generally have a higher conditional correlation with the DAX index than with the S&P500 index.

Poland and the Czech Republic, as counties that neighbor Germany, register the most significant correlations with it. Therefore, these markets are very sensitive to fluctuations in stock market returns in Germany. Grabowski (2019) [

11] and Bein and Tuna (2015) [

52] also acknowledged the higher conditional correlation of the Polish and Czech stock markets with Germany and the US compared to Hungary.

Compared to the CEE-4 nations, conditional correlations for developed markets are greater and follow different patterns. Poland, the Czech Republic, Romania, and Hungary’s stock markets had a weak integration with those of developed countries during 2005 and 2006. The more rapid response of the Prague stock market to shocks coming from developed countries soon after the EU’s admission is consistent with the findings of the paper by [

62] Savva and Aslanidis (2010). Following EU accession, there is an increase in the correlations between CEE countries and developed stock markets, confirmed by [

63] Deltuvaite (2016). During the euro area sovereign debt crisis, the stock markets in the CEE-4 nations showed themselves to be very susceptible to foreign shocks ([

11] Grabowski, 2019).

The above aspect is captured both in

Figure 3 and in

Table 4, where the average correlation coefficient (Avg. Rho) is presented.

The influence of the German stock market on the analyzed CEEC stock markets is also because Germany is the leading trading partner of these countries, given the volume of imports and exports shown in

Table 3.

Table 4 suggests that the benefits of diversification for investors who own shares in mature markets such as Germany and those in CEEC markets may be limited, with PX, BUX, and WIG recording average correlations between 0.49 and 0.59 with DAX. In the case of the BET index, the average correlation coefficient with the German stock index is lower, 0.33. As shown in

Table 3, Romania has the lowest volume of exports/imports with Germany, approximately 1.3% of Germany’s total trade.

When there is correlation with both the DAX index and the S&P500 index, the coefficients increased significantly during turbulent periods, such as those identified in

Figure 2 and

Figure 3 above. For all CEEC countries, the maximum correlation coefficient was reached in March 2020, when COVID-19 was officially declared a global pandemic by the World Health Organization (WHO). This major event, which had affected the year even prior to the pandemic declaration, has had devastating effects on all sectors of activity because governments decided to restrict movement and limit economic activities to protect the population and slow down the spread of the virus. Under these strict mobility measures, exports and imports between trading partners have decreased significantly. Empirical evidence supporting these results has also been shown by [

64] Papathanasiou et al. (2022), highlighting that during 2020–2021, the level of volatility spillovers has been moderate, while [

42] Samitas et al. (2022) demonstrated the volatility spillovers between natural alternative instruments and a set of traditional high-demand instruments, revealing the integration of markets and total connectedness during stress periods. During this period, the highest coefficients of conditional correlation were recorded in the case of Poland, reaching values of around 0.8 with Germany and 0.7 with the US.

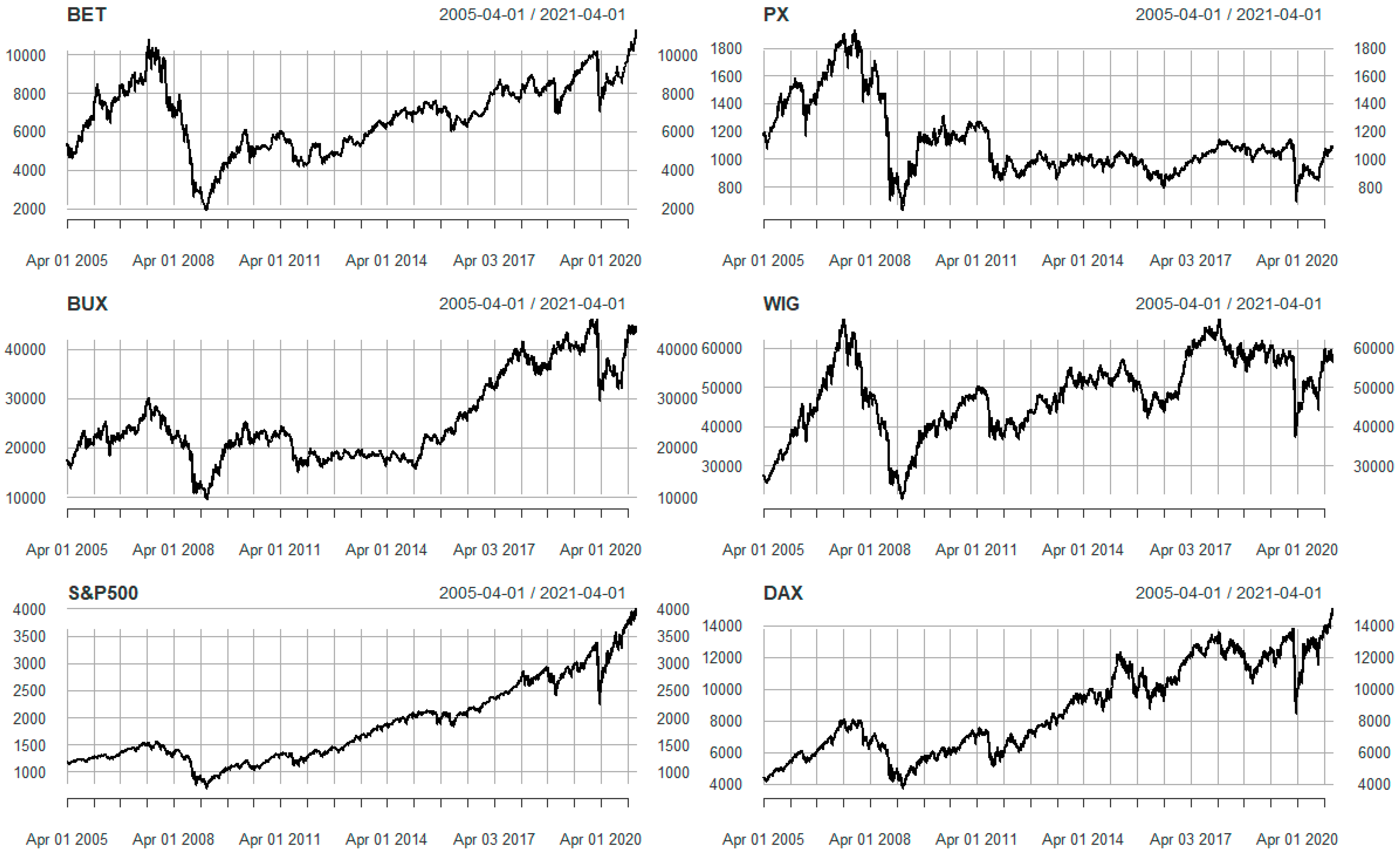

Over the entire period examined, the Polish index, WIG, was the most correlated with DAX and S&P500 indices compared to the other stock indices analyzed in Central and Eastern Europe. The BET index, meanwhile, is the least correlated with these two benchmark stock indices.

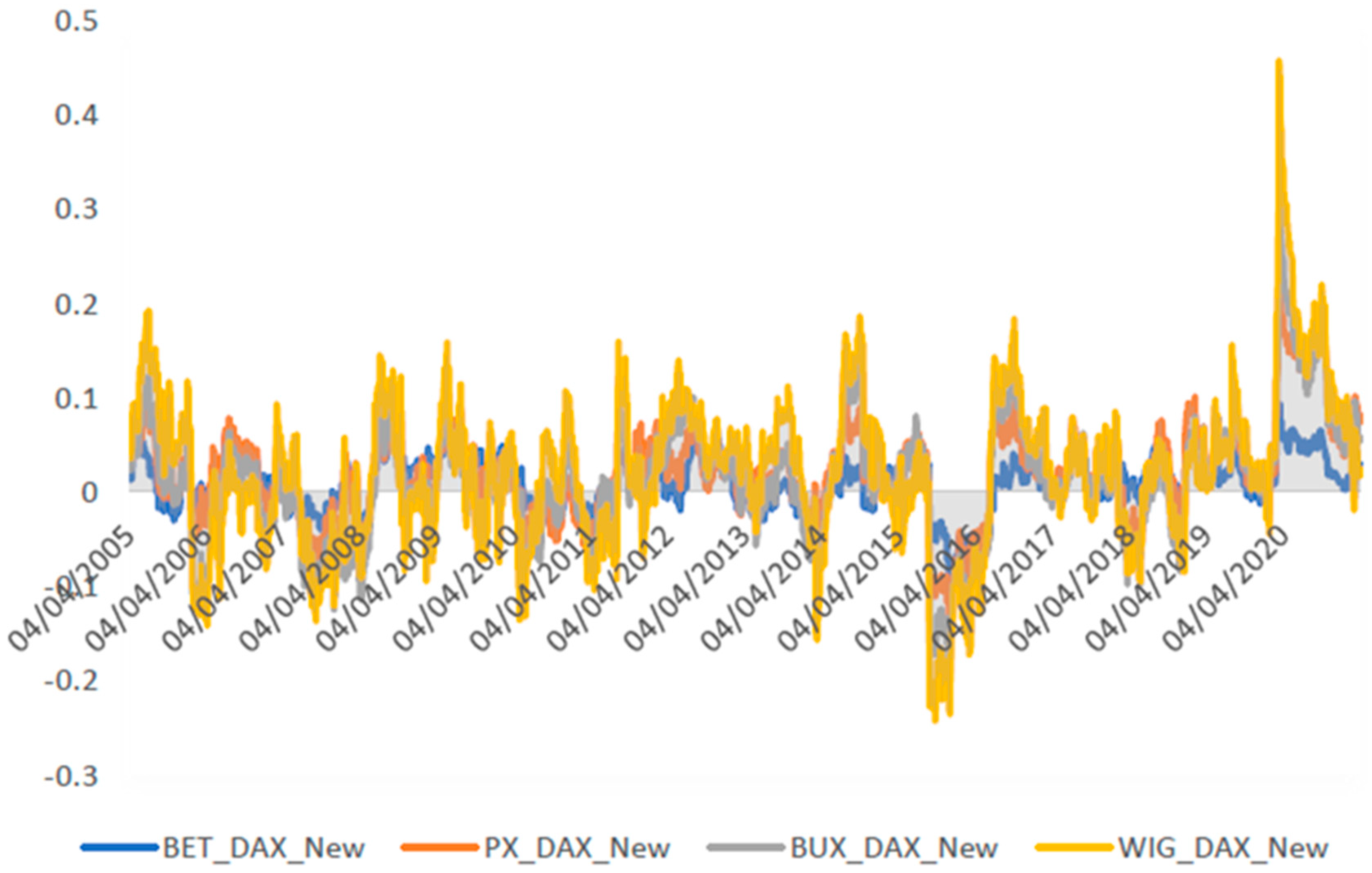

However, the results seem to be quite different when the European and the US stock markets are traded in different time zones, considering first the European and then American one day later. Analyzing now, the conditional correlation coefficients between the four CEEC stock indices and the DAX index in both cases (with and without delay) presented in

Figure 3 and

Figure 4 revealed a visible drop in the correlations when the German market was considered without delay.

Comparing these new conditional correlations of four European markets in relation to DAX with those concerning the US market but with one day delay (

Figure 2 and

Figure 4), it is worth mentioning that the stock markets in Central and Eastern Europe tend to have a higher conditional correlation with the S&P 500 index than with the DAX index.

Therefore, the different time zones in which the European and US stock markets trade are incorporated within the research; the main conclusion leads to the general idea, as in the case of [

60] Drożdż et al., that the US market dictates the trend.

The results are also in line with the study of [

10] Horváth et al.(2017), demonstrating that financial contagion occurred between 1998 and 2014. Kang and Lee (2019) [

65] showed that the UK and US futures index markets are the most important contributors of the volatility spillover shock of the global futures markets.

Analyzing the spillover effects between US stock, crude oil, and gold markets from 2006 through 2019, [

66] Bouri et al. (2021) proved that the stock index is the main net transmitter, oil is the main net transmitter, and gold is a net receiver.

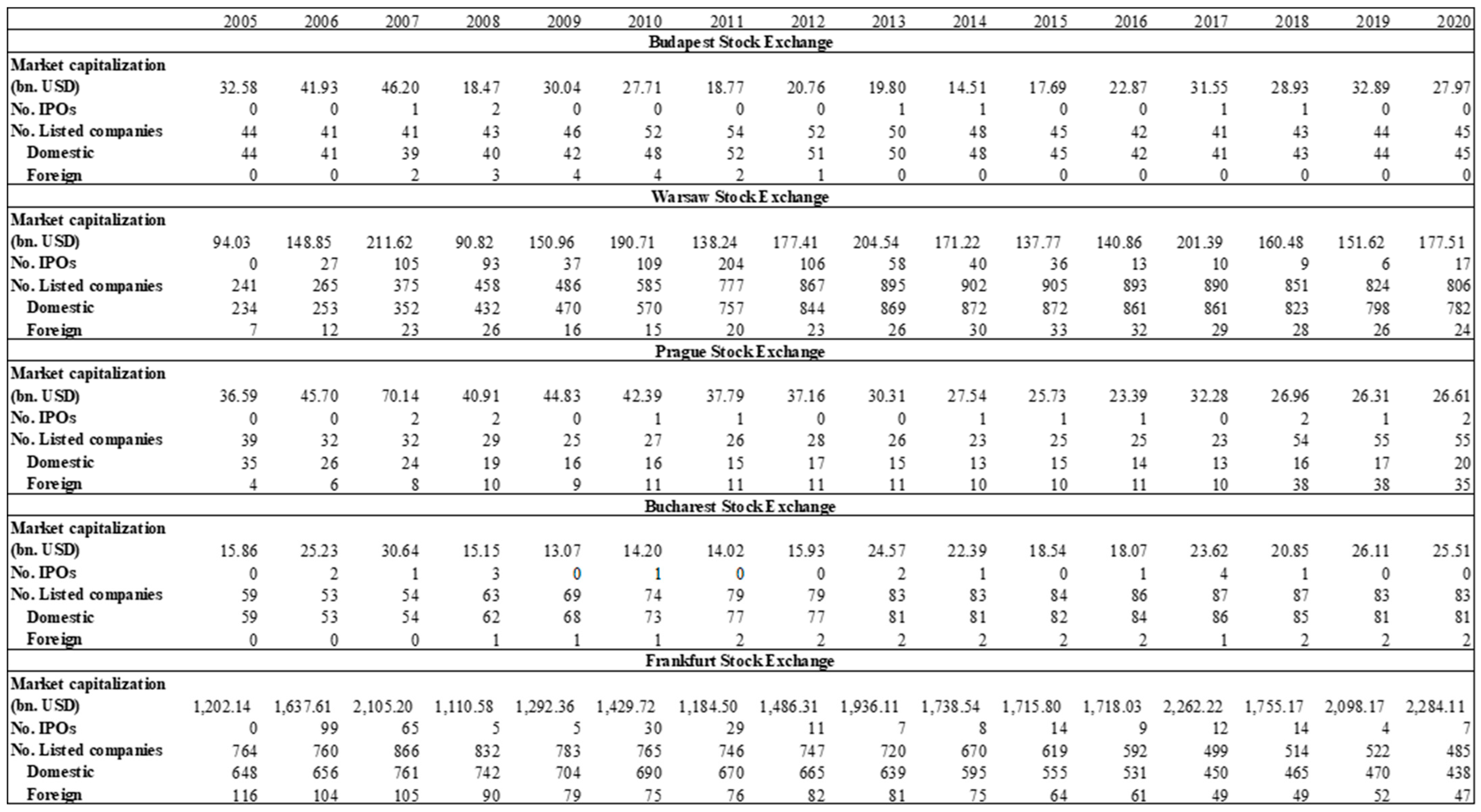

The Warsaw Stock Exchange is the largest in the CEEC area. At the end of 2020, the WSE had 806 listed companies and a market capitalization of approximately 178 billion USD, while the remaining CEEC stock markets registered below 100 listed companies and a market capitalization between 25–28 billion USD. Furthermore, Poland is the only country in this group that was promoted from emerging to developed market status by Financial Times Stock Exchange Russell (FTSE Russell), a global index and financial rating provider.

According to the FTSE Russell classification, global capital markets fall into three broad categories: developed, emerging, and frontier markets. These are determined according to several essential criteria: economic development, size, liquidity, and accessibility.

The Prague Stock Exchange and the Budapest Stock Exchange were classified as emerging markets before 2008. In September 2020, the Bucharest Stock Exchange was moved from frontier market to emerging market status in the FTSE Russell indices. The promotion of the Bucharest Stock Exchange will attract substantial funds to listed companies (which was not previously possible because of restrictions generated by the Frontier market status), and implicitly, to the development of the Romanian economy.

The existing literature argues that the contagion phenomenon in the financial markets can be induced in two ways: interdependencies between markets or investor behavior. The concept of interdependence was discussed by [

4] Forbes and Rigobon (2002); it represented the spread of shocks from one financial market to another, leading to a significant increase in the correlation in these markets. According to the article written by [

3] Dornbusch, Park, and Claessens (2000), however, the increase in correlation between financial markets during periods of crisis could also be attributed to contagion caused by the herding behavior of investors. Investors follow the behavior of other market participants, thus trading in the same direction over a certain period. Several studies in the literature (including [

6] Chiang, Jeon, and Li (2007); [

8] Syllignakis and Kouretas (2011)) use models such as the DCC-GARCH model to investigate possible herding behavior in emerging financial markets during turbulent periods.

5.3. Quantification of the Contagion Effect in Times of Crisis—Analysis Based on DUMMY Variables

The behavior of the conditional correlation coefficients over time has been further studied, providing insight into the impact that periods of crisis have on the evolution of these correlations. Specifically, 3 DUMMY variables were used to capture the dynamics of the conditional correlation coefficients for different periods of crisis.

Therefore, the regression model used is given by the following expression:

where

is the dynamic correlation coefficient between the US and Germany and the four CEEC countries analyzed (

= US, Germany;

= Romania, Czech Republic, Poland, and Hungary). The DUMMY variable

was selected to represent the period of the SARS-CoV-2 pandemic, and two different time frames were chosen for the correlation with the S&P500 index and the DAX index, as the pandemic affected the economies differently depending on the degree of spread of the virus.

The lag order in Equation (6) was selected through the analysis of the correlograms and the Akaike information criterion (AIC), with lag 1 being selected for all equations.

Table 5 presents the estimates of the regression model described above. Economic events with a major impact on stock markets were used to establish the crisis periods, as well as the VIX index (also used by [

13] Beirne John et al. (2013)) and the Composite Indicator of Systemic Stress (CISS) calculated by the ECB for the eurozone. The VIX Index is calculated by the Chicago Board Options Exchange (CBOE), based on the prices of options on the S&P500 index, thus measuring the stock market’s volatility over the following 30 days.

Appendix H presents the evolution of the VIX and the CISS indices, respectively, with turbulent periods captured by the threshold defined at a standard deviation above the average.

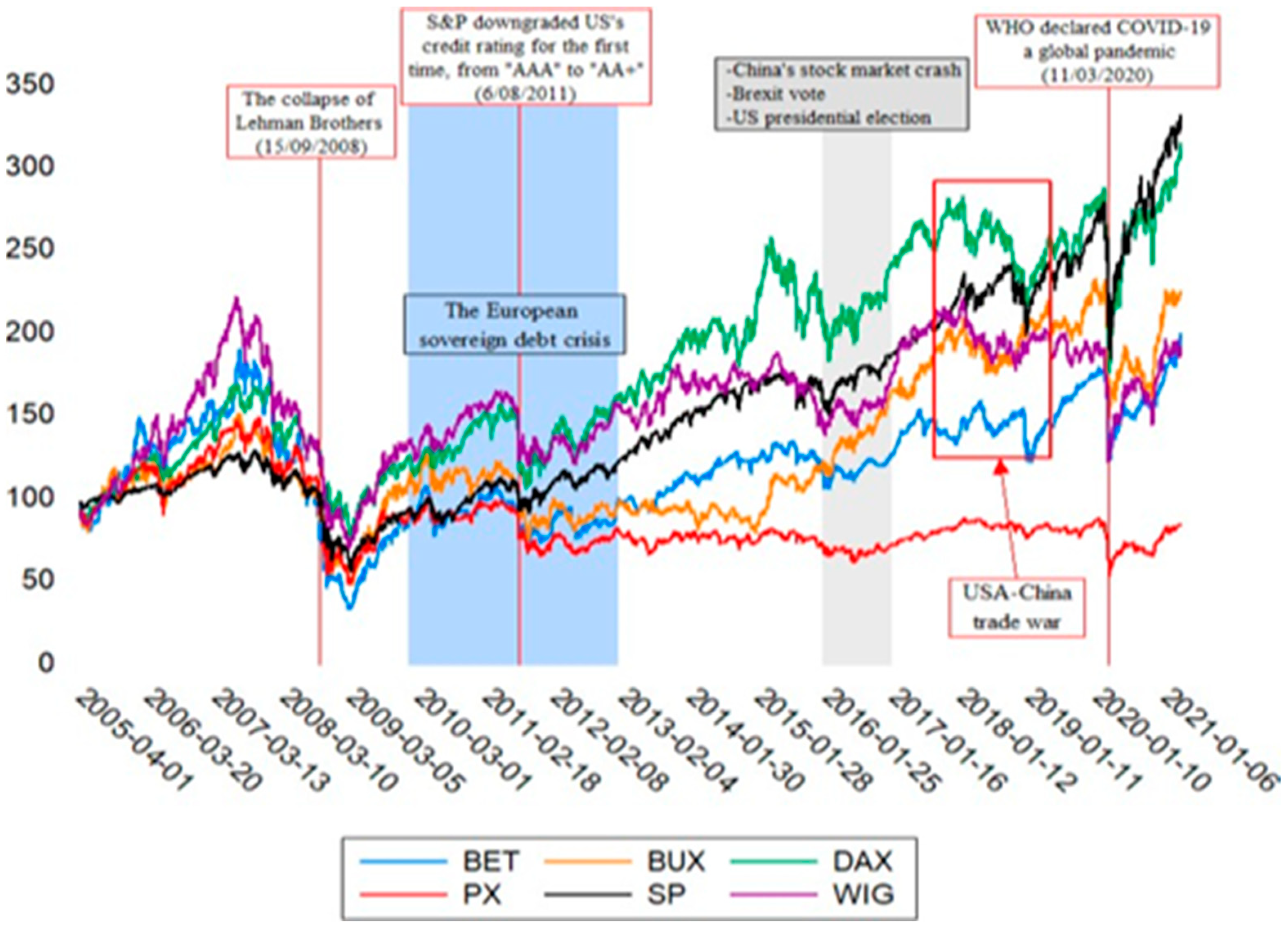

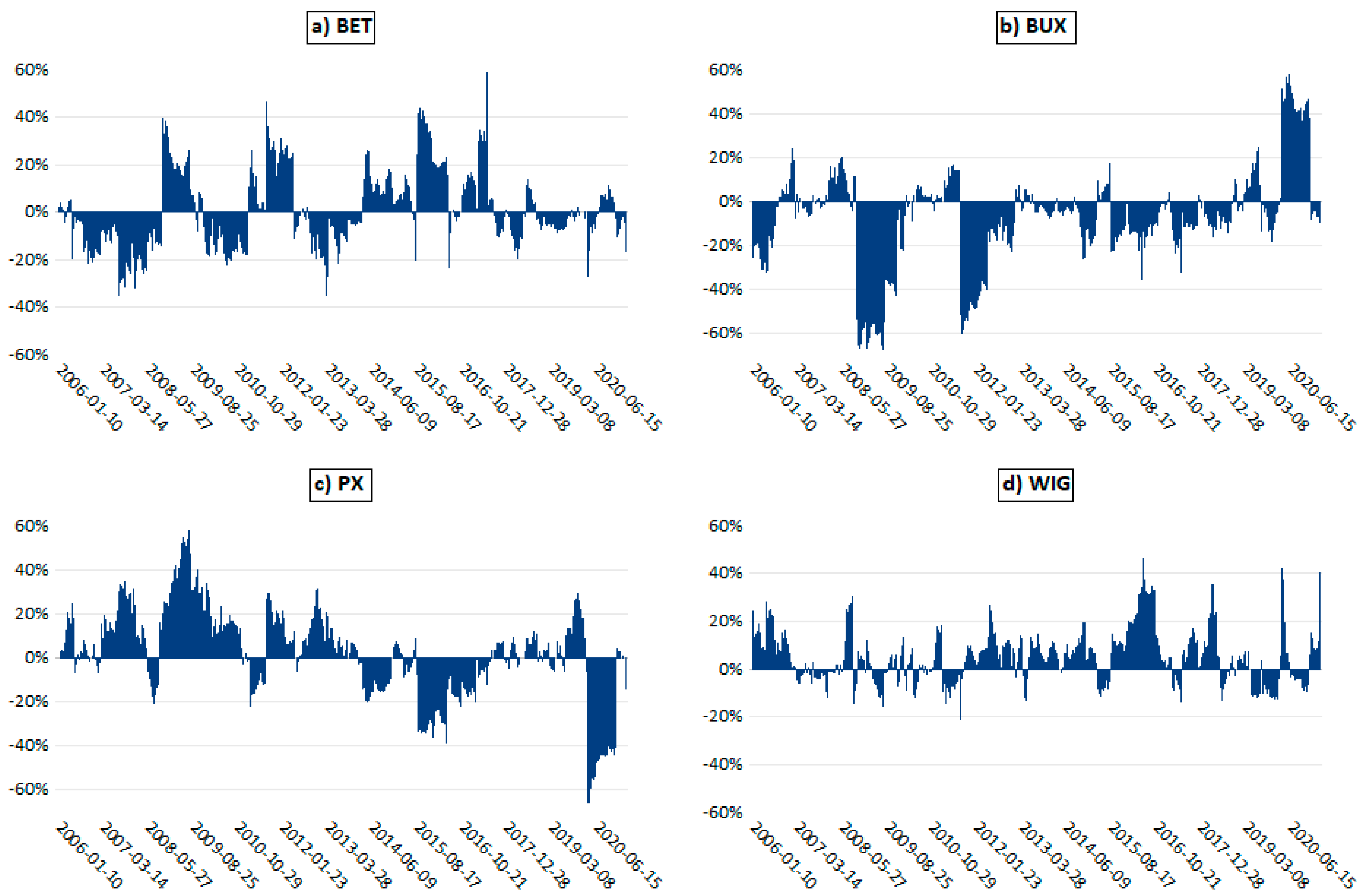

The first analysis of the dynamics of correlation coefficients refers to the period of the Great Recession, with the first DUMMY variable taking the value 1 between 15 September 2008–31 July 2009 and 0 otherwise. This turbulent period began with the bankruptcy of Lehman Brothers, the selection of the interval being also based on the analysis of the volatility of the VIX index and that of the CISS index.

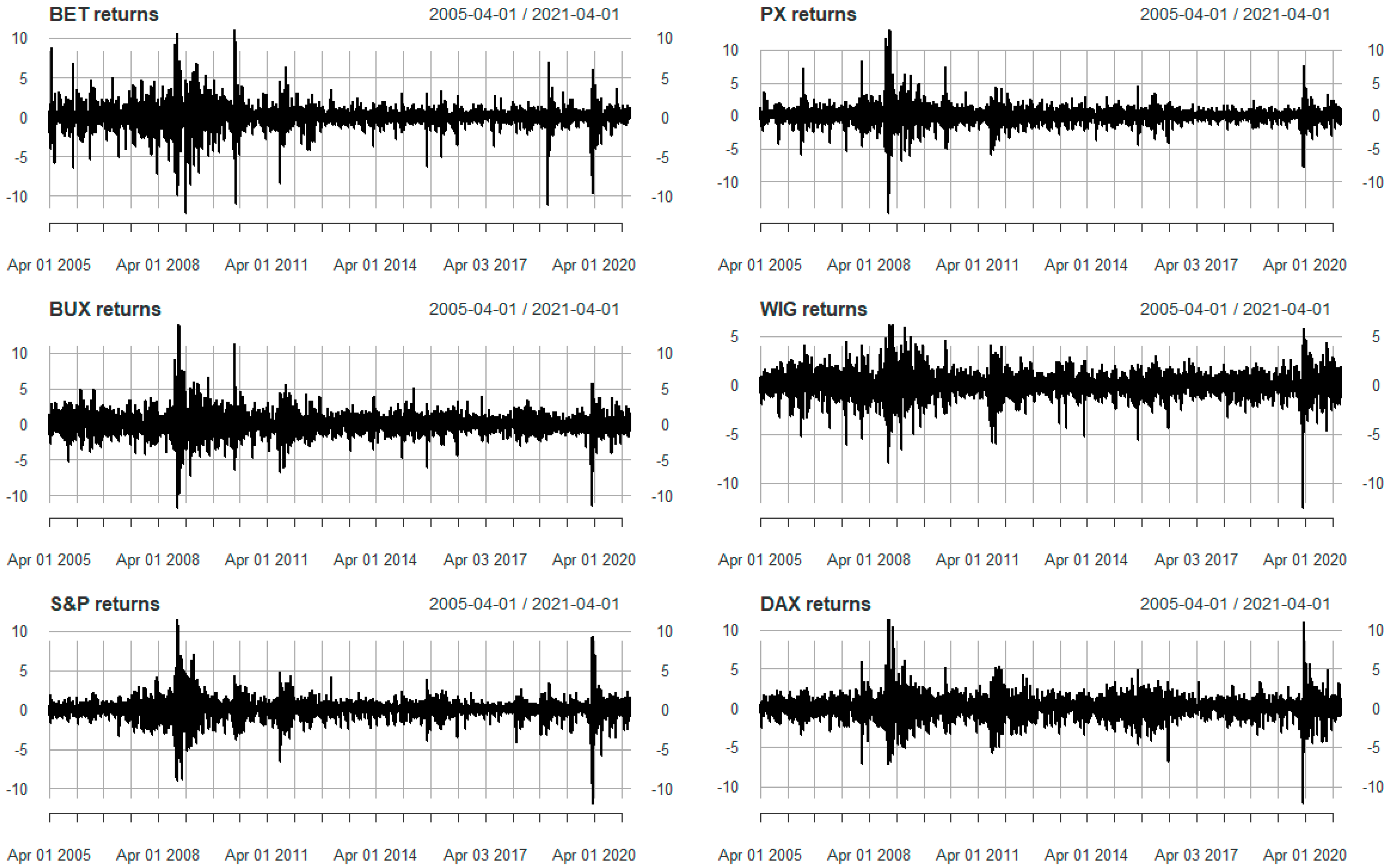

Although the premises of this crisis have been the same since the end of 2007, the Great Recession was triggered by the bankruptcy of the largest American investment bank, Lehman Brothers, on 15 September 2008; the crisis then spread globally. Worldwide stock markets collapsed, the Dow Jones and the S&P500 indices recording major “intraday” declines of 6.98% and 8.8%, respectively, on 29 September 2008 (after the US Congress rejected the $700 billion financial aid plan).

The effects of this economic crisis have also been felt strongly in the European financial markets. In Europe, the evolution of stock market indices at the end of 2008, compared to 2007, showed major decreases, with the German stock market index DAX falling by 40.4%. At the level of the four CEEC stock markets analyzed, the WIG index decreased by 48.2%, PX by 52.7%, and BUX by 53.3%. The BET index recorded the largest decrease, falling to 70% below the value at the end of 2007. It should also be noted that on 8 October 2008, because the volatility on the stock market was very high, it was necessary to suspend the Bucharest Stock Exchange’s trading activity for the day; this was the first time this had occurred in the exchange’s history.

By the end of 2009, large sovereign debts and significant budget deficits combined with high borrowing costs and the financial crisis, led to the collapse of the European Union’s financial system, also known as the European sovereign debt crisis. This began when Greece’s public debt reached 113% of its GDP in 2009, which was almost twice the 60% limit set in the euro area. Other countries, such as Ireland, Italy, Portugal, Cyprus, and Spain have followed in the footsteps of Greece, forming the GIIPS group. Each country requested financial assistance from the International Monetary Fund (IMF) and the EU to be able to emerge from the crisis.

The second DUMMY variable takes the value 1 in the period 04 August 2011—28 November 2011 and 0 otherwise. The VIX index and the CISS index were used to choose this range, showing high volatility during this period. This interval is representative of the European sovereign debt crisis; at that time, there were concerns about the spread of the crisis to countries such as Spain and Italy. Stock market indices continued to experience severe volatility until the end of 2011. Moreover, stock indices in the United States, Europe, and Asia suffered significant declines in August 2011. This was because Standard & Poor’s downgraded the US credit rating for the first time in the agency’s history; it had been at AAA since 1941, but was reduced to AA+ on 6 August 2011.

To capture the recent crisis caused by the SARS-CoV-2 virus, two different DUMMY variables were used: and . DUMMY variable , related to the correlation with the DAX index and takes the value 1 between 14 February 2020 (when the first death outside Asia was recorded, in France) and 27 December 2020 (when vaccination began in the European Union) and 0 otherwise. Variable , related to the correlation with the S&P500 index, takes the value 1 between 30 January 2020 and 27 July 2020 and 0 otherwise. This period was chosen given the remarkable volatility of the VIX index; on 30 January 2020, the COVID-19 outbreak was declared a Public Health Emergency of International Concern by the WHO.

The SARS-CoV-2 pandemic has affected the activity of international capital markets. This negative shock was triggered by the prospect of a new global crisis, by the fact that most economic activities have been frozen, and by the uncertainties about the evolution of the pandemic. In the first quarter of 2020, all stock market indices in the developed and the analyzed CEEC countries showed a negative trend (S&P500 −24.2%; DAX −28.7%; BET −25.7%; PX −31.4%; BUX −30%; WIG −30.5%). The BET index’s biggest decrease (−28.6% compared to the beginning of 2020) was recorded on 16 March 2020.

In March 2020, the Federation of European Securities Exchanges (FESE) recommended that the European stock markets continue to operate smoothly and respect regular operating hours despite the extreme market conditions caused by the COVID-19 pandemic. Stock exchanges were recommended to implement business continuity plans, thus remaining open for all investors to manage their portfolios in a transparent framework.

The estimation results of Equation (6) are given in

Table 5. In the case of the correlation between the S&P500 index and the indices in the CEEC countries, all the coefficients of the DUMMY variables are positive and statistically significant (at the 5% level), for all of the three crises analyzed.

In the case of the correlation with the German stock market, the coefficients of the DUMMY variables , are also positive and statistically significant (at the 5% level), except for the indices PX and BUX, for which and (only for BUX) are statistically insignificant. This analysis indicates a remarkable increase in the correlation between the stock indices analyzed during the previously identified crises, thus demonstrating the contagion phenomenon transmitted from the stock markets in Germany and the US to those in Central and Eastern Europe.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}